Emerging Tech Impact Radar: Generative AI

14 February 2025 - ID G00809486 - 122 min read

By Annette Zimmermann, Danielle Casey, and 15 more

High-impact technologies such as AI agents and reasoning models will disrupt how the world interacts with technology. Use this Impact Radar to make critical decisions on investing in emerging Gen-AI technologies to enable customers to reach new heights of value in their business.

Overview

Key Findings

- The development of reasoning models will offer a significant advancement for businesses due to their ability to solve complex problems with high accuracy. Such models use a chain-of-thought approach that allows them to analyze and articulate the necessary steps to reach a solution.

- Agentic AI will create significant opportunities to improve productivity, customer experience and decision making, but it will require user trust to gain sustained adoption.

- Multimodal GenAI will transform enterprise applications by enabling the addition of new user interfaces, features and functionalities.

- Synthetic data will revolutionize multiple industries and use cases in the next three years as it removes reliance on real-world data and enables endless opportunities for simulations and data-generation techniques.

Recommendations

- Identify high-value applications for reasoning models, particularly agents requiring multistep actions, models serving as coordinators to orchestrate multiagent systems, and improving small-model reasoning performance through distillation and fine-tuning.

- Establish the basis for agentic AI adoption by starting with agents that carry out simple actions reliably and consistently, such as completing expense claim fills or parsing patient intake data in healthcare.

- Accelerate to high-quality multimodal experiences by first exploring acquiring curated text, image, video and audio datasets from AI marketplaces instead of developing in house.

- Create a strategic roadmap prioritizing short-term synthetic data use cases focused on augmenting model training, especially for domain-specific tasks where real data is hard to acquire and noisy, while using simulations to understand and improve business processes in the long term.

Strategic Planning Assumptions

By 2028, one-third of interactions with enterprise generative AI software will invoke autonomous agents to achieve tasks, up from less than 1% in 2023.

By 2028, 40% of AI asset purchases, including models and data by enterprises, will take place via AI marketplaces, up from less than 5% in 2024.

By 2030, 80% of enterprise software and applications will be multimodal, up from 1% in 2024.

By 2030, synthetic data will constitute more than 90% of the data to fill in edge scenarios for training AI models, up from 5% today.

Analysis

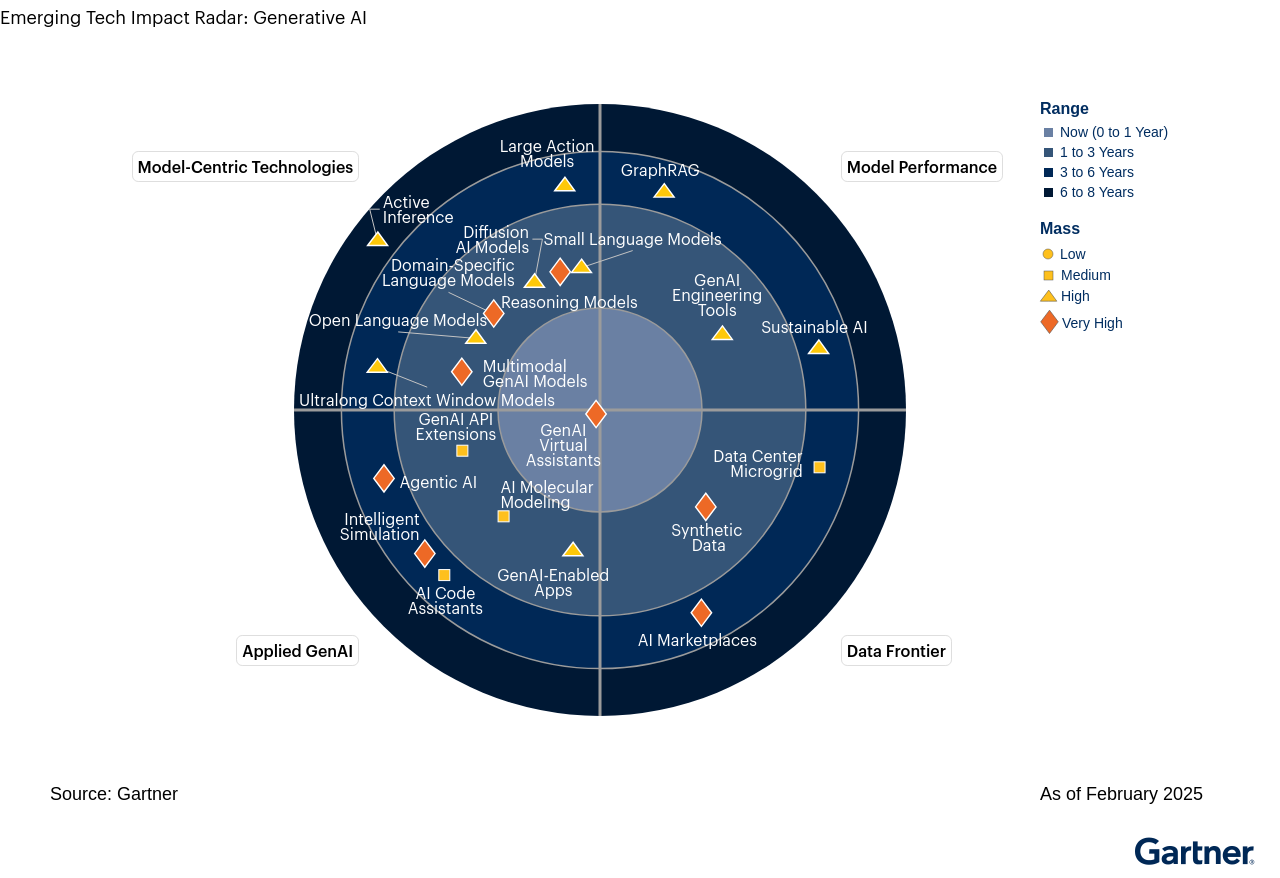

This Impact Radar discusses 22 of the most important GenAI technologies and trends along four main themes: model-centric technologies, model performance tools and techniques, the AI data frontier and AI-enabled applications (applied GenAI).

Model-Centric Technologies Are the Basis for Disruption

Model-centric technologies in this Emerging Tech Impact Radar fall under three sub-themes, which include:

- Enhanced reasoning and contextual understanding

- Reasoning Models

- Long-context window models

- Active inference

- Model efficiency and accessibility

- Domain-specific language models

- Small language Models

- Open language Models

- Other capabilities

- Multimodal GenAI

- Diffusion AI models

- Large action models

Enhanced reasoning and contextual awareness in AI focus on improving the ability to tackle complex tasks through better problem solving and text processing. A key development in this area is “inference time scaling.” Reasoning models like OpenAI o1 and DeepSeek-R1 use reinforcement learning to improve performance in logic, math and coding by generating “chains of thought.” Long-context window models, such as Qwen2.5-1M, excel in facilitating in-context learning, a vital aspect of generative AI. These models manage up to 1 million tokens using techniques like Dual Chunk Attention, allowing them to adapt to various tasks without explicit retraining. By leveraging context in prompts, they efficiently generate responses, enhancing performance in nuanced tasks and simplifying user interaction. Active inference, based on the free energy principle, further boosts AI adaptability by integrating perception, cognition and action, focusing on continual learning and real-time interaction.

Model efficiency and accessibility are key trends in AI, focusing on making technology more usable and affordable. Innovations such as outsize small language models (SLMs) and domain-specific models are at the forefront of this movement. The evolution of small model development, highlighted by DeepSeek, enables the creation of SLMs that can match or even surpass the performance of larger models while using two to three orders of magnitude fewer parameters. This advancement allows powerful AI to run on consumer-grade hardware, including laptops and edge devices, freeing generative AI from the data center for a wide range of use cases. Additionally, domain-specific models, tailored to particular industries or tasks, can now be developed on local hardware. This is made possible by the lower barriers to entry demonstrated by a mix of known and new innovations from DeepSeek’s efficient architectures, thereby making AI more accessible to a broader range of users.

Other capabilities focus on enhancing AI’s ability to seamlessly integrate into a wide range of use cases and workflows. Innovations such as multimodal generative AI, diffusion models and large action models are driving this trend. These technologies enable AI to process and synthesize diverse data types, including text, images and audio, enhancing its contextual understanding and applicability. Large action models, in particular, empower AI to execute complex task sequences and make informed decisions in dynamic environments, significantly expanding its utility. This equips AI systems with the capabilities needed to effectively integrate into fields like healthcare, entertainment and autonomous systems. By developing these capabilities, AI systems become more effective and valuable tools, ensuring high-quality outputs and adaptability in real-world scenarios, while complementing advancements in model efficiency, accessibility and reasoning.

Model Performance Tools and Techniques Will Drive Accuracy, Safety and Sustainability

The technologies included in this theme include:

- Sustainable AI

- GraphRAG

- GenAI engineering tools

The technologies included in this theme are enabling advancements in model accuracy and safety, as well as ethical considerations concerning the use of GenAI outputs. Sustainable AI incorporates environmental, social and governance aspects into decision making. The rapid development and adoption of small language models (see model-centric technology theme) present an opportunity for enterprises and product leaders to leverage GenAI models that are much more resource-efficient than generic LLMs. A critical driver is the alignment of cost and sustainability benefits, with resource-efficient models being, in general, considerably cheaper as well. We expect the breakthroughs demonstrated by DeepSeek to accelerate this trend. With the lower costs and compute requirements, the whole industry will move from large, generic LLMs to more industry- and domain-specific models.

GraphRAG alleviates some of the accuracy challenges with GenAI solutions, which result from generating responses based on patterns in data rather than verified facts, leading to hallucinations or misinformation.

The AI Data Frontier Is Expanding to Address Advanced Model Building

This theme includes the following technologies:

- Synthetic data

- AI marketplaces

- Data center microgrid

This theme discusses some of the critical steps that involve building a GenAI model and the decisions that have to be made with each of these steps and building blocks. Helping clients make their data AI-ready is one of the key building blocks in any AI journey and a common challenge that will need to be addressed by tech providers. Whether data is AI-ready is determined by different parameters, including the use case and the qualification of datasets. AI marketplaces help organizations to address some of these key issues by making high-quality data accessible. AI marketplaces accelerate collaboration, innovation, processes and know-how. These marketplaces will become indispensable and drive over 40% of transactions (data, apps, and model sharing and selling), exceeding direct transactions outside of AI marketplaces.

Emerging types of datasets, including synthetic data, can enhance real-world datasets. At the current rate of adoption, we expect synthetic data to play a critical role in the near term to the point where it will become indispensable, as real-world data will not keep up with the demand for training data. This represents a great opportunity for vendors to offer value, especially in situations where high-quality data is needed or real-world data cannot be used or sourced. Moreover, synthetic data can play an important role in enhanced reasoning. There is an opportunity to create a wide range of scenarios with synthetic data, including edge cases that are not available with real-world data. With these extended scenarios, the system can learn broader concepts and therefore exhibit strong reasoning capabilities by handling rare and extreme cases.

Applied GenAI Will Concurrently Enhance Existing Experiences While Enabling New Use-Cases

Applying GenAI in practice includes:

- GenAI virtual assistants

- Agentic AI

- GenAI API extensions

- AI molecular modeling

- GenAI-enabled apps

- Intelligent simulation

- AI code assistants

Higher performance, parameter efficient models will enable new use cases, particularly in resource-constrained environments. We expect a myriad of new applications to emerge over the next three years, some of which will enable new use cases, while others will enhance existing experiences. Prominent examples include agentic AI and polyfunctional robots. We expect new applications, such as workflow tools and agentic AI, to have a fundamental impact on how people work and complete tasks.

Advanced simulation techniques, such as simulation twins, will eventually enable test environments to operate at a fraction of the cost and time required for testing in the real world. An increasing number of organizations are focusing on augmenting existing software and solutions with GenAI.

Figure 1 depicts the 22 emerging generative AI technologies and trends across the 4 different themes in the respective quadrants.

The Impact Radar

Product leaders should use the Radar Profile range to plan investment timing in the related emerging technology or trend (ETT). “Range” represents Gartner’s estimate of time to reach early majority (more than 16% target market adoption), not when product leaders should act on investment. Considering time to plan, develop and launch, a starter guide to product leader investment timing, based on product strategy, is as follows:

- First movers should be acting now on items in the 6-to-8-years ring (or beyond).

- Fast followers should be acting now on ETTs in the 3-to-6-years ring.

- Majority followers should be acting on ETTs in the Now and 1-to-3-years rings.

- Laggard followers can wait until the ETT has passed through to early, or even late, majority.

Refer to the About the Impact Radar section for more information.

Emerging Technologies or Trend Profiles

Priority Matrix for Generative AI

| Mass | Range | |||

|---|---|---|---|---|

| Now (0 to 1 Year) | 1 to 3 Years | 3 to 6 Years | 6 to 8 Years | |

Very High | ||||

High | ||||

Medium | ||||

Low | ||||

Source: Gartner

Now

GenAI Virtual Assistants

Analysis By: Danielle Casey

Definition:

Generative AI (GenAI) virtual assistants (VAs) represent a new generation of VAs that leverage large language models (LLMs) to deliver functionality not obtained with traditional conversational AI technology. GenAI enables improved Q&A support, new features and modalities, extended task automation and improved value outcomes.

Sample Vendors

Aisera; Google; Haptik; IBM; Kore.ai; Leena AI; OneReach.ai; Openstream.ai; Ushur

Range: Now (0 to 1 Year)

The range for GenAI virtual assistants is “now” because they have emerged as one of the foremost applications of GenAI technology within the organization.

Large language models have materially augmented VAs to enable new capabilities and enhance the quality of outputs, with leading providers having already productized or at least piloted GenAI capabilities in their VAs. However, adoption of GenAI VAs varies by industry, use case and organizational risk tolerance.

Despite the growing popularity of GenAI VAs, 2024 adoption rates have not yet surpassed early majority customer adoption (16% of the target customer base). This is expected to change in 2025 as trust in GenAI VAs and their performance improve.

There are different approaches to incorporating an LLM into a VA. They include chaining multiple LLMs, embedding an out-of-box model into an offering, using an architecture based on retrieval-augmented generation (RAG), model fine-tuning, retraining or otherwise customizing an LLM for use. Each option must be evaluated against performance requirements, implementation time and costs.

Gartner predicts that by 2026, GenAI will be embedded in 90% of conversational AI offerings, up from 50% in 2024.

Both venture capital firms and established conversational AI tech providers are driving significant investments in GenAI VAs, leading to rapid market growth and a rapidly changing competitive landscape. There are several drivers and inhibitors impacting GenAI VA adoption.

GenAI VAs are being driven by:

- Customer demand for GenAI: GenAI hype has organizations wanting to pilot the technology. GenAI VAs are popular as the VA use cases and KPIs are well-defined and the need to improve customer or employee support may already be recognized.

- Vendors rapidly pivoting and repositioning offerings: Many VA providers have preexisting knowledge graphs, indexed vector databases and in-house technical expertise. Coupled with existing high-performing out-of-box models, repositioning VAs as “GenAI-enabled” is achievable for most vendors.

- LLM-enabled capabilities and value: Vendors are incorporating LLMs into their VA offerings to support more advanced Q&A, provide summarization and generation capabilities, and expand language and modality support. GenAI VAs promise improved value outcomes over their non-GenAI counterparts due to higher Q&A resolution rates.

Obstacles inhibiting adoption include:

- Accuracy: Low accuracy translates into poor VA performance and value outcomes, presenting a significant challenge in scaling adoption. Many vendors are actively investing in improving accuracy, hallucination detection and mitigation techniques.

- Customization requirements: To unlock value, GenAI VAs must be connected to customer data via RAG and prompt engineering, data vectorization, model fine-tuning, or other techniques, requiring customer education, budget, skills, custom integrations and data-readiness.

- ROI: Tokenization and generative inferences are changing VAs’ cost structure. Difficulty proving ROI may slow adoption of new offerings versus traditional VA offerings priced on a consumption basis.

- Privacy and security: Privacy and security concerns may necessitate stricter model hosting and data integration requirements.

- Responsible AI: GenAI explainability and model maintenance and monitoring tools will help address accuracy, reliability and compliance concerns and drive usage.

Mass: Very High

The mass for GenAI virtual assistants is very high because of their expected impact across all industries, multiple use cases and many different business functions.

GenAI virtual assistants are being adopted across all industries, though the pace of change and the nature of implementation vary by regulatory environment.

Typically, internal-facing GenAI VAs are the first to pilot, with use cases around employee self-service, information discovery and generation, and intelligent agent assist for call center operators.

External-facing GenAI VAs that support B2C engagements may be pursued after internal-facing GenAI VAs have gone into production and some of the aforementioned inhibitors have been addressed. Some industries (such as retail and media, communications and services) are more receptive to external-facing GenAI VAs than others (such as financial services and healthcare) due to perceived risk.

Generative AI will transform virtual assistant offerings by:

- Enabling complex conversational dialogue with greater contextuality. GenAI VAs capable of handling more complex user requests can improve user self-service and satisfaction rates, reducing call center volumes and associated costs.

- Extending automation beyond Q&A support to content discovery and creation, and analytics capabilities.

- Supporting multimodal interactions (beyond text and voice) to include image, video, code and unstructured data (such as emails, PDFs and websites).

VA providers that enhance their products with GenAI may also offer new services to support data readiness and solution development.

Recommended Actions

- Reduce adoption inhibitors by prioritizing technology investments that will improve model and application accuracy and, therefore, solution performance.

- Drive and scale GenAI VA adoption by developing offerings that solve use-case- or industry-specific business problems and deliver measurable value.

- Differentiate in a GenAI-washed market by investing in LLM accuracy and controls, responsible AI features, multimodal capabilities or advanced analytics tools.

Gartner Recommended Reading

1 to 3 Years

AI Molecular Modeling

Analysis By: Reuben Harwood

Definition:

AI molecular modeling is the application of artificial intelligence techniques to predict and analyze the 3D structures, interactions and properties of molecules. It significantly reduces the time and cost of drug discovery, while enabling the analysis of innovative compounds, which would otherwise have been overlooked or considered too risky to explore. In the life sciences industry, AI molecular modeling underpins a shift from trial-and-error to precision engineering of therapeutics.

Sample Vendors

Dassault Systèmes; DeepMind; Cadence; Chemical Computing Group; Fujitsu; Insilico Medicine; NVIDIA; Schrödinger

Range: 1 to 3 Years

The range for AI molecular modeling is one to three years because the value of AI molecular modeling output continues to be scrutinized, requiring more data and new operating models to fully implement these approaches.

Early adopters are already benefiting from the implementation of AI molecular modeling, with preliminary use cases in protein engineering, drug development and repurposing, biomarker discovery and personalized medicine. Leading pharmaceutical companies have established billion-dollar partnerships with AI-native drug discovery companies, and the software market in this space is also rapidly expanding.

Training AI for molecular modeling is still expensive, time-consuming and held back by the availability of high-quality biological data. Further work needs to be done to integrate these computational approaches with wet lab validation of AI-generated output. However, AI models greatly accelerate development timelines and reduce costs, raising high expectations in the R&D community. The requisite redesign of R&D workflows and implementation of new operating models is expected to take another 18 to 24 months.

Accumulating evidence that AI molecular modeling can help compress the time and reduce the cost of drug development is garnering interest and investment in this technology. Early analysis of AI-discovered drugs in clinical trials showed an 80% to 90% success rate in Phase I, when the drug is tested with a small group of people for the first time. (See How Successful Are AI-Discovered Drugs in Clinical Trials? A First Analysis and Emerging Lessons, Drug Discovery Today.) This is substantially higher than historic industry averages. AI molecular modeling is accelerating the rate of drug discovery to the point where it will rapidly become mandatory for companies wishing to remain competitive. This technology is growing fast, in part due to advances led by big tech companies, including Google DeepMind and NVIDIA.

Mass

The mass for AI molecular modeling is medium. While AI molecular modeling and computational drug discovery as a whole are likely to transform life sciences R&D, this technology has limited relevance outside of the life sciences, chemicals and materials engineering sectors.

While the applicability of AI molecular modeling is focused, the advancements within life sciences, chemicals and materials engineering underscore its critical role in these fields, making it indispensable for future innovations and breakthroughs. Notably, the Nobel Prize in Chemistry 2024 was awarded to David Baker (University of Washington, USA), Demis Hassabis and John Jumper (DeepMind) in part for developing the AI model, AlphaFold2, which predicts proteins’ complex structures. In materials engineering, AI molecular modeling can accelerate discovery and optimization of new materials with specific, tailored properties such as enhanced strength, durability, thermal resistance or electrical conductivity.

In an industry where 90% of trials fail, any technique that can reduce the cost of drug development and improve the success rate of clinical trials will have a significant impact. Existing projects have a strong emphasis on proving the viability of the technique, for example, by focusing on targets with validated biology. But momentum in this field will see a rapid uptick as the first wholly AI-designed-and-developed drugs proceed through clinical trials and gain regulatory approval, which we expect to happen within the next two to three years. Still, there are several hurdles to address:

- AI molecular modeling requires high-quality, extensive datasets to train sophisticated algorithms

- It is computationally intensive requiring cloud-based infrastructure and high-performance computing (HPC)

- It mandates expertise in both AI and specific scientific domains (for example, protein biology, materials science).

Recommended Actions

- Identify parts of the drug development process where the implementation of broader AI-enabled techniques will have the maximum business value by partnering with stakeholders to understand current inefficiencies and future opportunities.

- Help drug development companies differentiate by assisting in customizing their models and integrating proprietary data into the training process, via connections with common laboratory platforms (e.g., laboratory information management systems [LIMS], electronic lab notebook [ELN])

- Prioritize transparency in AI model performance and the explainability of AI output to guide scientist decision making.

Gartner Recommended Reading

Diffusion AI Models

Analysis By: Roberta Cozza, Radu Miclaus

Definition:

Diffusion models are generative models that use probabilistic variation to add noise to data (for example, blurring an image) and then reverse the process (clearing of the image) to generate new samples of data. Diffusion models have proven more effective than generative adversarial networks (GANs), especially in applications related to image/video processing, synthesis and summarization, and computer vision.

Sample Vendors

Adobe; Baidu; Google; Hugging Face; Midjourney; OpenAI; Shutterstock; Stability AI

Range: 1 to 3 Years

The range for diffusion models to reach early majority adoption is one to three years because applications targeted for creative content creation and synthetic media are already available and are adopted rapidly.

These models are evolving rapidly both in their capability to refine image and video generation, achieving higher resolutions and photorealism. Since the introduction of OpenAI DALL·E and earlier models, more diffusion models and applications for content generation have increasingly entered the market. These applications, which include multimodal type outputs (such as avatars, video and others), are penetrating both the consumer and enterprise sectors, thereby intensifying competition. Recently, there has been a surge in efforts to create diffusion models capable of running on-device in smartphones for tasks like text-to-image generation or enhancement of computational photography. Initiatives like Google’s MobileDiffusion and others, along with efforts in graphics processing unit (GPU) optimization to execute diffusion models locally, exemplify this trend.

The creative user community has seen rapid growth in the experimentation with diffusion model-based applications. Concurrently, there is increasing scrutiny and concern regarding intellectual property (IP) protection, particularly around generative outputs produced from models trained on protected content. This can expose companies to IP infringement litigation. Regulations around IP protection, along with self-regulation of vendors of models and applications, continue to evolve and adapt to the pace of change. In addition to this, ethical considerations are paramount in order to ensure diversity in the visual data used to train diffusion models to avoid perpetuation of social or cultural biases.

Mass: High

The mass for this technology is high because it can be applied to multiple areas and industries.

These models can produce high-quality synthetic media, creating realistic and compelling content for applications ranging from entertainment and marketing, to education and training. They enhance the professional’s ability to generate and edit visual content, extending beyond creative sectors like marketing and media to unlock new opportunities in fields such as life sciences and intelligent simulation.

While application in the image generation and editing has been one of the front-running applications of diffusion models, the use cases for diffusion models include:

- Image processing — generation, resolution, restauration, editing, anomaly detection.

- Computer vision — synthetic image and video generation, semantic segmentation, resolution.

- Multimodal generation — text-to-image, text-to-3D, text-to-motion, text-to-video, text-to-audio/sound.

- Natural language processing — various use cases.

- Temporal data processing — time series data imputation, forecasting, anomaly and signal detection.

Beyond the rapid generation of images or videos from text prompts, which finds applications in media, gaming and marketing, diffusion models are increasingly contributing to other fields. Their growing impact is evident in applications based on sequences and connections like material design, medical image processing, biochemistry applications — encompassing industrial and life science applications. In particular, these models can be used for the generation and support of GenAI-driven simulation of molecule and protein structures, impacting fields like drug discovery, for example. Other opportunities are in the area of simulation and modeling of networks, environment and construction.

Diffusion models will enable transformational capabilities in the democratization of visual content-generation capabilities. These will enable critical optimization and time savings in creative tasks and workflows, both within enterprises and across a variety of creative industries. The evolution of future models will further enhance sophistication of content output. In addition, we see continuous investment aimed at enhancing the efficiency and maintenance of diffusion models, with a focus on optimizing them to limit their substantial computational requirements.

Recommended Actions

- Advance the content creation capability for enterprise software with human-augmentation capabilities by exploring both open-source and proprietary diffusion models to benefit from GenAI-enabled productivity experimentation.

- Build or integrate with models developed in an ethical manner, ensuring that they are free from exposure to IP-protected content. This approach will provide a competitive advantage in enterprise use cases that are focused on mitigating such risks.

- Invest in superior prompt engineering experience and a support community to share best practices for refining the completion from diffusion model-based applications.

Gartner Recommended Reading

Domain-Specific Language Models

Analysis By: Ray Valdes, Danielle Casey, Akhil Singh

Definition:

Domain-specific language models (DSLMs) are designed to address knowledge requests within a particular area, including functional domains (such as sales, HR, marketing or research), industry domains (such as finance or retail) and use cases (such as recruitment or lead generation). They are trained on focused datasets representative of the specific domain. Because of their focused nature, they can be valuable as constituent elements of agentic solutions (broad systems that combine and take action across multiple domains). Unlike general-purpose models such as GPT4 or Gemini, which have been exposed to a wide range of topics, these models focus on specific areas. Although an industry refers to a particular economic sector (such as manufacturing or healthcare), a domain is a more general field of study or activity — such as sales, HR, marketing or research — that can be found across various industries.

Sample Vendors

Jasper AI; Oracle; SAP; Salesforce; ServiceNow; Workday; Writer; Zendesk; Zest AI

Range: 1 to 3 years

The range for DSLMs is one to three years because of rapid model proliferation, including those incorporated into legacy applications as well as those from pure-play generative AI (GenAI) startup vendors.

Domain-specific models have proliferated over the past year, and this trend will continue: The entire tech sector is pivoting to incorporate generative AI into their products and services.

For example, the sales function is found in many industries, in roughly the same pattern, with some variations. Historically, the sales function in an enterprise has been supported by enterprise applications (such as Salesforce CRM) that target that domain. Legacy enterprise CRM applications have more recently been augmented by domain-oriented models. In addition, there are emerging GenAI-intensive solutions that use domain-oriented models. Established vendors of legacy applications (in categories such as CRM, ERP, IT service management [ITSM] and human capital management [HCM]) have added or are adding generative-AI-based capabilities. In addition, there are a host of new tech startups creating and launching solutions based on domain-oriented models for human resources, sales, research, marketing, accounting, legal and research.

The speed at which GenAI capabilities are being added to domain-oriented solutions is rapid because the technical effort is relatively low for the first wave of GenAI augmentation. In the simplest case, it is technically straightforward to embed a text window into an enterprise application that launches a conversation with a large language model (LLM) through an API. This approach provides only limited incremental value to the user. The next step is multipoint integration in various workflows, such as generating a draft email to a prospect, generating a summary of an interaction, or prioritizing a dataset based on conversational input. This kind of augmentation provides more value, but is still incremental in nature. Progressing further, deeper use of GenAI in a domain-oriented application can transform high-value, inefficient processes and make them faster and more effective. This could result in significant productivity benefits, cost reduction and, in some cases, increased revenue.

Mass: Very High

The mass for DSLMs is very high because of their ability to leverage vast amounts of data within a specific domain to generate results that are impactful, relevant and accurate. Though near-term value will be incremental, as the technology matures and industry specialization deepens, these systems will evolve to reinvent business processes.

Domain-specific models can be quite focused. For example, an LLM for the oil and gas (O&G) industry may have knowledge of O&G practices in sales, shipping, refinery operations, geologic sampling, environmental regulations and reports. This industry-specific LLM can support a range of functional areas or domains within that industry sector, possibly including sales, HR and accounting functions (hence the overlap). The overlap is why, in some cases, it may be hard to distinguish a functional-specific LLM versus an industry-specific LLM. Further examples of utility are:

- Medical image analysis: Analyze X-rays, EKGs or other lab results and correlate diverse datapoints

- Language translation for human languages that are not widely used, or for industry domains that have specialized vocabularies

- Drug discovery: Identify potential drug candidates and predict their properties

- Legal contract analysis and generation

- Financial analysis and forecasting: Analyze financial statements and reports, and generate a financial model that enables prediction of future results

- Fraud detection: Correlate diverse datasets to identify fraudulent transactions and bad actors

- Credit scoring and risk assessment: Evaluate the credit-worthiness of individuals or businesses

- Marketing campaign: Generate plans for online advertising that will produce optimal results

- Content creation: Write blog posts and social media posts for product vendors

- HR job applications: Evaluate resumes and generate draft response emails

Initial use of domain-specific models is incremental in nature: They are used to incrementally automate or improve certain workflows in established applications. This is because the domains in question (such as sales, HR, finance or marketing) are well-understood and have been well-served by legacy applications (such as CRM, HCM and ERP). Established vendors in those categories have added or are adding generative AI capability. The first wave of improvements will deliver incremental benefits, making some specific tasks (such as drafting a letter to a prospect) more efficient.

As the technology matures and understanding of the problem deepens, high-value business processes and workflows could be significantly transformed, and this could lead to more impactful benefits. Also, within a domain, there will regularly emerge new workflows and tasks that are not well-served by legacy applications and can be addressed by GenAI products that use domain-oriented models. Examples include managing online advertising campaigns or undertaking credit scoring for individuals who have limited credit histories. These emerging pockets of opportunity could grow to have a significant impact on the business.

Domain-specific models benefit from some overlapping trends in models: small models, open-source models and industry-specific models. These trends can make it easier and cheaper to build domain-specific models and get effective results. Domain-specific models can benefit from the recent trend of small models, which are often open-source and can run on-premises or in colocated hosting. Though linked, small models are not essential to meeting the requirement of domain specificity. Synthetic data generation can also accelerate time to market by reducing the need for large domain datasets.

Recommended Actions

- Within a domain, analyze business processes and workflows to identify high-value processes that can be made more efficient, or whose timelines can be accelerated, in order to deliver significant business value.

- Conduct a thorough inventory of all data within a domain — including traditional structured data controlled by legacy applications as well as unstructured data (such as documents, emails, meeting transcripts, voicemails and focus group raw data) that can be ingested into a domain-oriented model — so that it can produce relevant and effective output.

- Evaluate and deploy tools, techniques and technologies such as open models, small models, Low-Rank Adaptation (LoRA) and related fine-tuning advancements that can greatly facilitate the task of building and using domain-specific models.

Gartner Recommended Reading

GenAI API Extensions

Analysis By: John Santoro, Jim Hare

Definition:

Generative AI (GenAI) API extensions augment the capabilities of GenAI models by giving them the ability to retrieve real-time information, incorporate company and other business data, perform new types of computations and safely take action on a user’s behalf. GenAI extensions indicate, via their metadata, the types of prompts that they support. They map keywords in those prompts to API calls that can access information or take actions that otherwise could not be performed by the GenAI model.

Sample Vendors

Adobe; AppDirect; AWS; Google; Microsoft; Nuance; OpenAI; SAP; Zapier

Range 1 to 3 Years

The range for GenAI extensions is one to three years because the technology has become simpler to implement and technology providers need to invoke APIs to make large language models (LLMs) useful in the context of their product experiences.

Providers initially created extensions to connect their content to the user interface tool associated with the LLM. But, the majority use case quickly has become application providers embedding LLMs into their products via API. As a result, users will enter a prompt within a product’s user interface and not even be aware that the prompt is executed by an LLM (or which one is used) with GenAI extensions to give it product-specific capabilities.

GenAI models need to invoke APIs to take action or to access data that changes more frequently than the model can be updated. Therefore, the simplicity with which GenAI models support API extensions will affect the speed of adoption by product providers and independent software vendors. A lack of a standard extension architecture across AI models will inhibit adoption, as providers and developers will have to reproduce some portion of their effort developing, testing, supporting and maintaining API extensions for multiple GenAI models.

Mass: Medium

The mass for this technology is medium, because not all providers will need API access. They may not need to access real-time data or to take action via APIs, and some will use custom models or chatbots to achieve the same result without extensions.

GenAI plug-ins offer the potential to be used across industry verticals by automating tasks, enhancing creativity and delivering personalized experiences at scale. In healthcare, they can streamline medical reporting, diagnostics and drug discovery, while in finance, they can automate financial analysis and improve fraud detection. Retail and e-commerce can benefit from AI-driven product descriptions and inventory optimization, whereas manufacturing could see gains in product design, predictive maintenance, and supply chain management. Media, entertainment and education could leverage AI for content creation and adaptive learning, while legal, real estate and human resources sectors could use it for document generation, market insights and candidate screening. Across marketing and advertising, AI promises to boost campaign efficiency with personalized content and real-time performance analytics.

The impact of this technology also will depend on the simplicity of employing API extensions, including whether LLMs provide a marketplace for customers to discover extensions that they wish to buy.

Vendors are increasingly investing in GenAI plug-ins by developing flexible, modular tools that can be easily integrated into various platforms and applications. They are focusing on creating plug-ins that support a wide range of use cases, from content creation to personalized recommendations, to cater to diverse industry needs. Many vendors are also building extensive developer ecosystems, offering APIs and software development kits (SDKs) to enable customization and scalability. Also, they are enhancing plug-in capabilities by incorporating advanced AI models and ensuring compatibility with popular software environments aiming to provide seamless user experiences and accelerate adoption.

Recommended Actions

- Create a GenAI extension to enhance a product that uses an LLM but requires dynamic information or needs to take actions.

- Verify the accuracy of the information an extension provides before attempting to use it. AI accuracy and hallucinations remain common issues with GenAI models so consider supporting guardrails.

- Identify whether supporting multiple LLMs or BYO LLMs would be useful, weighing portability across models and licensing costs to determine potential feasibility and profitability.

Gartner Recommended Reading

GenAI Engineering Tools

Analysis By: Eric Goodness

Definition:

Generative AI (GenAI) engineering tools enable enterprises to operationalize development models faster, balancing both governance and time to market. AI engineering tools can be subdivided into model-centric and data-centric tools. There are numerous terms, such as DataOps, LLMOps, LangOps, FMOps and, more broadly, ModelOps and MLOps, that are used frequently to refer to AI engineering but are really subsets of AI engineering. Prominent tool categories specific to GenAI engineering include prompt engineering, vector and graph databases, model fine-tuning, model deployment, application frameworks, and AI trust, risk and security management (TRiSM) tools.

Sample Vendors

C3 AI; DataRobot; Fiddler AI; Holistic AI; Humanloop; IBM; OctoAI; Palantir; Snorkel AI; Weights & Biases

Range: 1 to 3 Years

The market for GenAI engineering tools will reach early majority adoption in one to three years. GenAI engineering tools make up a fast-emerging, critical set of middleware necessary for developing and managing GenAI technologies to achieve business goals. The emergence of purpose-built software to support the life cycle requirements of generative models is key to the technology’s adoption.

Despite the utility of these tools, the marketplace is highly fractured, with a set of existing data science and machine learning/MLOps software, and a large number of specialty tools brought to market by a growing collection of startup software companies. Very few providers offer end-to-end platforms to manage the life cycle of LLMs. Many enterprises lack experience in operationalizing GenAI, and this is magnified during the due diligence process of choosing the right tools for their GenAI projects and initiatives.

This presents users with the decision of whether to accept “good enough” solutions with legacy providers or to engage in extended due diligence with a marketscape of emerging and innovative providers where viability and a deep pool of references are concerns.

Despite the challenges of this emerging market, there is a stabilizing element where coalescing ecosystems of large and small providers of GenAI engineering tools are partnering with large independent software vendors (ISVs) and hyperscalers in their AI marketplaces and model hubs.

Mass: High

The impact of GenAI engineering tools is high as the software is the main catalyst for the development, monitoring and operationalization of generative models.

GenAI engineering tools are critical for developing and managing GenAI technologies to achieve business goals. In short, GenAI engineering tools are the picks and shovels to the GenAI gold rush. Some of the valuable capabilities offered by GenAI engineering tools include:

- Steering models without incurring significant retraining costs

- Enabling applications to respond with low latency to high concurrency requests (prompts)

- Fine-tuning base models for task specificity, higher model performance and fewer hallucinations

- Orchestrating workflows by chaining prompts or models together to achieve intended outcomes

- Protecting against loss of intellectual property, hallucinations, a lack of model explainability, bias and toxicity in model output, and misinformation

- Providing AI observability for GenAI-enabled systems and applications

- Optimizing models through techniques such as quantization and low-rank adaption (LoRA), among others

The tools will affect all sectors and businesses operationalizing GenAI directly or indirectly. GenAI engineering tools that embody end-to-end foundation model operations (FMOps) capabilities would help organizations pave a clear path from data preparation to experimentation, and then to model deployment and production monitoring.

Because of the proliferation and use of GenAI, it is expected that many different product types, which did not offer organic MLOps prior to the emergence (commercialization) of GenAI, may integrate one or many elements of the toolsets, such as data preparation, model development, prompting, model deployment, model monitoring and governance. Gartner believes that over the next 24 months, there will be a huge increase in the acquisition of these smaller, pure-play tool providers by hyperscale providers and larger ISVs and legacy data science and machine learning platform companies.

Recommended Actions

- Speed up bottom-up adoption to accelerate sales cycles and promote growth and advocacy by exploring product-led growth initiatives focused on developers and citizen data scientists.

- Engage in GenAI ecosystem partnerships to enhance your offerings by collaborating with providers that supplement and complement capabilities when offering single-purpose tools, such as model fine-tuning, model deployment or prompt engineering.

- Create demand for your GenAI engineering tools by demonstrating capabilities to add value with both closed- and open-source models and model hubs.

Gartner Recommended Reading

GenAI-Enabled Apps

Analysis By: Annette Zimmermann, Radu Miclaus

Definition:

Generative AI (GenAI)-enabled applications use generative AI for user experience (UX) and task augmentation to accelerate and assist the completion of a user’s desired outcomes. When embedded in the experience, generative AI offers richer contextualization for singular tasks like generating and editing text, code, images and other multimodal output. As an emerging capability, process-aware generative AI agents can be prompted by users to accelerate workflows that tie multiple tasks together.

Sample Vendors

Adobe; Amazon Web Services (AWS); Google; INFORM Software; Microsoft; OpenAI; Salesforce; ServiceNow; UiPath; Uniphore

Range: 1 to 3 Years

The range for generative AI-enabled apps is one to three years from early majority customer adoption, as the majority of B2B software vendors are either planning to, starting to or have already implemented, GenAI capabilities into their software experiences.

B2B GenAI-enabled applications are already in production and accessible in general availability, preview or beta stages. These applications span across multiple productivity domains, including text editing, creative design support, as well as software engineering tasks like coding and low-code/no-code applications. Independent software vendors (ISVs), encompassing both incumbent vendors in the hyperscalers, SaaS providers as well as specialized vendor startups and scale ups are actively announcing ongoing roadmaps. These plans focus on integrating new GenAI capabilities into their applications for the second half of the year.

The rapid adoption of GenAI-enabled apps by both end users and tech providers alike, coupled with the growing number of offerings from both major tech companies and startups suggests that early majority adoption may be imminent. We expect continuous investments in this area by both startups and large tech. This is both induced by vendors offering software such as virtual assistants that are migrating the underlying technology to large language models (LLMs) as well as the development of brand new software powered by GenAI.

Despite these fast developments, some challenges remain. The main challenge with GenAI-enabled applications lies in the nature of “upgrading” a legacy application with next-generation technology. The user organization is often not prepared in terms of cultural readiness as well as data readiness. The former relates to employees’ concerns regarding whether the new GenAI application could potentially replace them, which may lead to delays in adoption. The latter arises from the fact that many organizations do not possess AI-ready data because a common data structure simply does not exist. This and eliminating data silos are needed to drive adoption of the low-hanging fruit in GenAI, such as enterprise search, virtual assistants and the automation of manual tasks (like summaries and reports).

Mass: High

GenAI-enabled applications are projected to achieve a high mass due to their pervasive application throughout the entire technical stack, their applicability across horizontal and vertical use cases, and their broad adoption across industries.

GenAI-enabled application providers are designing experiences that focus on ease of adoption and scale onboarding for users, without forcing steep learning curves. These experiences are either augmented from current task workflows or completely redesigned for intuitive and easy-to-use interfaces, for example, conversational interfaces for users. The increased democratization afforded by GenAI-enabled applications will lower the technical barriers for operating applications, increasing the volume of users and interactions within applications.

Technology advancements are made continuously by augmenting existing applications with LLMs in combination with other capabilities and techniques, such as knowledge graphs, reasoning, plug-ins and retrieval-augmented generation (RAG). For example, for the development of an advanced semantic search solution leveraging GenAI for a large pharma company, the generative pretrained transformer-3 (GPT-3)-based model extracted information from medical research articles. The RAG architectural pattern was used on a library of 2,000 historical papers to ensure sources were delivered along with result output. The process of extracting the most relevant information from medical research articles was previously a manual process. With the enhancement of the LLM-powered search solution, process efficiency increased tenfold, reducing manual effort significantly. Accuracy and lack of short-term memory in extended chat conversations, as well as effective guardrails, remain challenges that could potentially lower the overall impact of embedded-GenAI applications. As demonstrated in the aforementioned example, there are tools and techniques available that contribute to organizations’ transparency and reliability efforts.

Recommended Actions

- Prepare your clients for GenAI by offering data advisory services, including data integration management and data governance, or by facilitating access to such services via a third party. A strong data strategy will prove critical to the success of any GenAI application project.

- Help your clients overcome cultural barriers to the adoption of embedded GenAI applications by actively getting involved and directly supporting change management within those organizations.

Gartner Recommended Reading

Multimodal GenAI Models

Analysis By: Roberta Cozza, Danielle Casey

Definition:

Multimodal GenAI provides the ability to use multiple types of data inputs and outputs — such as images, videos, audio (speech), text and numerical data — within a single generative model. Multimodality augments the usability of GenAI by allowing models to interact with and create outputs across data in various modalities. Today, many multimodal models offer processing across two or three modalities (e.g., text-to-video or speech-to-image). This will increase over the next few years to include more modalities.

Sample Vendors

Anthropic; Apple; DeepSeek; Google; Meta; Microsoft; Mistral; OpenAI

Range

The range for multimodal GenAI is one to three years from early majority adoption due to the accelerated availability of general-purpose multimodal large language models (LLMs) from hyperscalers mainly and some smaller players. In addition, we are seeing the increased availability of smaller multimodal GenAI models built around domain-specialized content.

Multimodality scales the benefits of GenAI across potentially all data types and applications. It removes traditional unimodal data barriers by allowing users to interact with, manipulate, and create outcomes from numerous data types typically used in different business environments.

Early models have mainly been about processing two or three well-understood modalities as inputs, and generating outputs that mainly include text, speech, images and video. Over the next few years GenAI models will include additional modalities, as well as more advanced techniques for training on video data and analytics generation.

During the past year we have seen more investment from all key players in extending the multimodal capabilities of their large language model (LLM) offerings, both for generic-knowledge LLMs and domain-specific models. Multimodal GenAI models bring key benefits:

- Increased accuracy: Since multimodal GenAI models do not depend on one modality, they can provide responses that are richer and have more context.

- New applications: The ability to process and ultimately analyze data from various modalities opens the door to new or more innovative applications (such as multimodal questioning/retrieval, or video generation from text input).

- Augmented capabilities: Cross-modal information and reasoning helps identify complex patterns (i.e., emotion, intent nuances) to increase the relevance of GenAI models’ responses.

- Rise of specialized multimodal models: Models trained on data about specific industries and business functions that are intrinsically multimodal (e.g., legal, finance, healthcare, marketing and multimedia) will be able to enhance productivity and add new value in these areas.

Multimodal GenAI models are not easy to build or integrate. They can be costly as they are computationally heavy and require disparate types of data. Faster adoption is currently inhibited by the following challenges:

- Training challenges: Multimodal GenAI models use deep learning, data alignment and fusion techniques to train on and integrate data sourced from the multiple modalities. Multimodal data can have varying degrees of quality and formats versus unimodal data; in addition, data may be limited in some modalities. For example, the availability of 3D images or large-scale audio datasets is more limited compared to other modalities like 2D images and text.

- Risk of privacy violations: Multimodal GenAI increases the exposure to a wider range of sensitive data, potentially increasing data privacy concerns. This is important as more government regulations will be increasingly in place and demand transparency in the use of sensitive data for model training.

- Data management: Keeping multimodal data with varying degrees of quality up to date, clean and accurate is a more complex task than for unimodal data.

- Bias and inaccurate or fabricated outputs: The risk of such outputs is potentially amplified by multimodal data sources.

Mass

The mass for multimodal GenAI is very high because it supports the creation and expedition of new tasks, workflows and applications, such as extracting multimodal data, converting one data type to another, and creating new data outcomes. Applications that support multimodality will have higher automation potential across industries.

Over the next one to three years, multimodal GenAI models will increasingly appear in more and more applications, as the future of GenAI is multimodal. Emerging use cases include the following:

- Data and analytics (D&A) by supporting the manipulation of text, numerical, voice and visual data to glean insights.

- Multimodal content and website creation, including website design, product descriptions and images, and content creation for the marketing function or e-commerce applications.

- Visualization of text, graphs and numerical information in data-heavy industries (such as financial services) for D&A support.

- AI avatars (which use multimodal UI layers) used for corporate training or as virtual assistants.

- Multimodal search, in which search engines are leveraging multimodal LMs and natural language processing (NLP) for conversational capability and to deliver more relevant answers or artifacts by handling multimodal data extraction. For example, domain-specific GenAI multimodal models are able to extract and process multimodal information (such as tables, images, graphs and slides) from enterprise knowledge documents.

- Multimodal domain-specific models used for specialized tasks, such as legal research and analysis, or in healthcare handling multimodal patient data to generate treatment plans, or to combining medical images, textual medical records and electronic health records (EHRs).

Multimodal GenAI will have a transformational impact on enterprise applications by enabling the addition of new features and functionality that are otherwise unachievable. These models will have a major impact on the development of industry-specialized applications and services, as they can better support domain-specific LMs and take advantage of multimodal data specific to vertical domains like healthcare, finance, insurance and manufacturing. Multimodality in GenAI models will also help achieve greater accuracy and better decision-making processes for future agentic AI types of applications. These will be highly impactful tools for automating and optimizing employees’ operations and driving more contextual decision intelligence, as agentic AI will be able to proactively take actions in a semi- to fully autonomous way.

Recommended Actions

- Start with your customer use case by assessing what modalities are best aligned to truly optimize workflows, tasks and user experiences via a multimodal model.

- Improve data quality and obtain curated multimodal datasets by assessing how AI marketplaces can be leveraged for quality text, image, video and audio datasets.

- Build or acquire expertise to cover the technical complexities of processing and integrating data inputs and outputs from diverse multimodal sources, and validate early how these can best be integrated with key legacy or more current data workflows.

Gartner Recommended Reading

Open Language Models

Analysis By: Annette Zimmermann, Ray Valdes

Definition:

Open-source language models (OLMs) — or more correctly, “open language models” — are foundation models distinguished by the terms of use and distribution granted to developers. Open language models are publicly available through various licenses that allow one to access, use, modify and distribute different parts of the system. Most open models are, strictly speaking, not “open source” per the definition from opensource.org (Open Source Initiative). Instead, there are degrees of openness depending on access to system components such as training data, training scripts, model architecture, model weights and inference code, and whether the system can be used for commercial purposes. In models that are fully open source, all these components are available for viewing, modification and deployment. This complete openness is found in open-source software packages (such as Linux or Python), but rare in the world of generative AI (GenAI) models. Most GenAI models are not fully open source and are termed “open weight.” These are models for which the pretrained weights are released but the training data, algorithms and architecture remains private.

Sample Vendors

Alibaba; BigCode; Cerebras; DeepSeek; EleutherAI; H2O.ai; IBM; Meta; Mistral; NVIDIA

Range

The range for OLMs is one to three years because open models are closing the gap with commercial proprietary LMs in terms of accuracy, completeness, quality and cost, thereby boosting the rate of adoption.

OLMs are halfway to early majority adoption. The key drivers behind them are increased flexibility, transparency and control, the ease of fine-tuning for small models and the perception that they cost less than proprietary LMs. The perceived cost advantage (“free and open source”) depends on many factors and is not always borne out in terms of total cost of ownership.

OLMs often provide access to developer communities in enterprises, academia and other research roles that are working toward a common goal of improving the models. Organizations can leverage new model architectures and training techniques from open LMs, using them to build additional innovation into their own technology. This collaboration and adaptation makes the models more valuable by improving the speed and quality of innovation, and the increased value drives greater adoption. OLMs often also provide greater transparency than proprietary LMs, which have become more opaque due to increased competitive pressure. OLMs’ greater transparency drives adoption among certain segments of the market that prioritize this aspect.

OLMs often provide access to developer communities in enterprises, academia and other research roles that are working toward a common goal of improving the models. Organizations can leverage new model architectures and training techniques from open LMs, using them to build additional innovation into their own technology. This collaboration and adaptation makes the models more valuable by improving the speed and quality of innovation, and the increased value drives greater adoption. OLMs often also provide greater transparency than proprietary LMs, which have become more opaque due to increased competitive pressure. OLMs’ greater transparency drives adoption among certain segments of the market that prioritize this aspect.

The emergence and growth of open-source communities is driving the adoption of OLMs. Their adoption is going hand-in-hand with the increased use of small language models, on-premises deployments and edge AI. The motivators include the need for cost reduction, increased data privacy, increased flexibility and customization for narrow-scope use cases, and vendor product portfolio augmentation. Vendors and enterprises that value one or more of these attributes are gravitating toward small models run on-premises, which are typically open models such as Llama 3.2 or Mistral. Closed commercial models running in hyperscale clouds remain by far the dominant segment of the market. Open models and small models are growing at a rate that outpaces the broad market, but are ascending from a tiny market share (single digits).

Recent revelations from the open-source community reflect the enormous investments in strategic AI initiatives by the Chinese government and Chinese enterprises. Globally, OLMs like Qwen, DeepSeek and Mistral will serve as the foundation for organizations to improve resource efficiency that will accelerate GenAI adoption.

Adoption challenges for open large language models (LLMs) include the following:

- Investments in data engineering, tooling integration and infrastructure to train and run OLMs can be high. These costs represent a significant fixed cost compared with proprietary alternatives.

- The variety of licensing agreements in open models impedes adoption. Open-source licenses (such as Apache, MIT or GPL) have been adopted by GenAI creators. Some organizations have defined their own variant licenses, with some unique restrictions.

- Model systems’ level of openness varies greatly, presenting trade-offs to anyone studying or adopting an open-source model.

- One specific area of weakness in several of the open-weight models is a lack of transparency in training datasets. While this problem is not unique to open-source LMs, it hinders adoption given enterprises’ increased attention to privacy and ethics.

As measured by various benchmarks, the accuracy gap between proprietary and open-source LLMs is still present, but has narrowed significantly. The remaining gap might not matter, depending on your product’s or service’s requirements.

Mass

The mass for open-source LMs is high because it will improve customization, align with specific enterprise requirements, enhance privacy and security controls, provide collaborative development and model transparency, and reduce vendor lock-in.

This will improve the utility of LMs across multiple industries. Ultimately, many OLMs will offer enterprises smaller models that are easier and less costly to train, and that enable business applications and core business processes.

Increased interest in customization is driving OLM adoption across use cases and industries. The recent industry trend toward growth in domain-specific and industry-specific models and solutions is having an impact, as these are easier to build with small models that can run on-premises, as opposed to large models deployed in the cloud. The small models tend to be open-source rather than closed-source. Financial services, healthcare, and telecom and media are among the leading industries to adopt open (and domain-specific) models.

Open LMs are more customizable than proprietary LMs because engineers can access their model parameters, source code and data. This access gives developers and product leaders more control over costs, output and alignment. By investing in OLMs, enterprises maintain ownership and control, and can continuously develop solutions. This ongoing investment can result in a short-term “moat” against early adopters.

Open LMs are more customizable than proprietary LMs because engineers can access their model parameters, source code and data. This access gives developers and product leaders more control over costs, output and alignment. By investing in OLMs, enterprises maintain ownership and control, and can continuously develop solutions. This ongoing investment can result in a short-term “moat” against early adopters.

Adoption of open LMs is following a trajectory similar to that of closed LMs, with a certain time lag that we expect to close in the next three years. OLMs are advancing GenAI initiatives for both vendors and end-user organizations, and are clearly growing at a robust rate based on recent Gartner interaction volumes and observations of online developer communities. The recent announcements by Chinese vendors offer a trajectory for researchers and enterprises to learn and benefit from. Specifically, organizations can build on the Chinese models’ advanced reasoning capabilities, allowing language models to solve more complex tasks.

There are many robust examples of open LM adoption, such as the following:

There are many robust examples of open LM adoption, such as the following:

- Uber has built a unified platform for all LM use cases within the company, which provides access to both open models (like Meta Llama) and closed models (such as OpenAI GPT4 variants). This platform (Uber GenAI Gateway) is itself open-sourced.

- NVIDIA’s ChipNeMo project is an LM solution built on an open LM (in this case, Llama’s series of small models from Meta) that performs better than the large GPT4 models on technical tasks such as electronic design automation (EDA) script generation. Over time, this system could potentially transform the way the next generation of semiconductor products is built.

- Shopify has added an image generator using an open-source visual language model to assist their customers in creating product illustrations.

- Wells Fargo bank has deployed applications that use open-source LMs for internal uses. Their GenAI platform, called Tachyon, supports multiple models, both open and closed.

Recommended Actions

- Perform due diligence to understand the legal exposure related to training data and the potential biases in LMs. This applies to both open models and closed models.

- Proactively engage with open LM communities as part of the due-diligence process to discern the advantages and drawbacks associated with various models.

- Evaluate different open LMs based on factors such as performance, resource requirements, compatibility and documentation by testing the models on sample data, and compare their outputs against your defined objectives.

Gartner Recommended Reading

Reasoning Models

Analysis By: George Brocklehurst, Ray Valdes, Eric Goodness

Definition:

Reasoning models are an advanced evolution of AI models, capable of performing logical inference, complex problem solving and multistep reasoning. These models utilize chain-of-thought processes and self-reflection to mimic human-like thought patterns, moving beyond simple pattern recognition to understand the underlying structures and relationships within data. Enhanced reasoning capabilities emerge during reinforcement learning, where the model takes feedback on the accuracy and format of its outputs. During this phase, a reward system encourages the development of longer chain-of-thought outputs, which correlate with increased output accuracy. This chain-of-thought reasoning results in significantly more output tokens and, consequently, increased compute demand compared to traditional LLMs. Reasoning models are part of a broader trend toward inference time scaling, an approach intended to continue the improvement of LLM performance. They are designed to tackle intricate queries that require a deeper level of understanding and analytical capacity.

Sample Vendors

AI2; Alibaba; ByteDance; DeepSeek; Kimi; OpenAI

Range: 1 to 3 Years

The range for reasoning models is one to three years because high demand for their advanced capabilities, such as complex problem solving and logical reasoning, will accelerate the knowledge development needed to exploit their capabilities in the field.

The rate of adoption is driven by demand for enhanced capabilities that address the limitations of traditional language models. Reasoning models excel in multistep tasks requiring logical inference, complex problem solving and understanding of context, making them highly valuable in fields like coding, mathematics and scientific reasoning. These enhanced reasoning capabilities are crucial for increasing the autonomy of agentic and multiagent AI systems, allowing them to plan, execute and adapt more effectively. Adoption inhibitors include increased computational overhead due to inference and integration complexity, necessitating improvements in efficiency and user-friendly deployment tools to facilitate widespread use.

In 2024, significant advancements were made in reasoning models, marked by the introduction of new models in the latter part of the year and continuing into early 2025. These developments underscore rapid progress in the field, characterized by reduced training costs and enhanced inference efficiency.

A key trend is the increasing accessibility of these models through platforms that facilitate broader community engagement, thereby accelerating innovation and adoption. This progress has led to widespread excitement and quick integration into major cloud platforms, highlighting the growing demand for advanced reasoning capabilities and a shift toward more autonomous and intelligent AI systems.

Moreover, improvements in reasoning are not confined to large-scale models. A recent initiative by AI researchers demonstrated that core reasoning abilities can be replicated with minimal compute resources, showcasing emergent reasoning behavior in smaller models. Such advancements are expected to further accelerate the adoption of reasoning models across various applications.

Mass: Very High

The impact of reasoning models is very high because they will accelerate the deployment of agentic systems across virtually all industries and businesses.

Reasoning models offer a significant advancement for businesses by providing the unique ability to solve complex problems with high accuracy through a chain-of-thought approach, whereby they analyze and articulate the necessary steps to reach a solution. This capability impacts businesses in two major ways:

- Enhancing agentic systems: Reasoning models improve agentic systems by enabling them to solve complex problems with greater accuracy and autonomy. These models utilize chain-of-thought reasoning and self-verification, allowing agents to make more informed decisions and tackle sophisticated tasks.

- Augmenting human decision making: For humans, reasoning models provide logical, step-by-step analysis to support complex decision making. This allows individuals to concentrate on higher-ROI tasks while AI manages the logical analysis. The collaboration between human creativity and AI analytical skills ensures superior outcomes.

Reasoning models are poised to have a significant impact across all verticals and businesses due to their enhanced, domain-agnostic capabilities. While their core abilities are applicable across various fields, their performance can be further optimized through domain-specific fine-tuning or by providing context via retrieval-augmented generation. This adaptability ensures that reasoning models can effectively address the unique challenges and requirements of different industries, maximizing their utility and impact.

Examples include:

- Finance: While prior LLMs excelled in automating customer service and analyzing market sentiment, reasoning models can identify unusual patterns for real-time fraud detection and develop sophisticated investment strategies by analyzing market trends and historical data. As reasoning models improve, adoption will spread to broader agentic uses where current state-of-the-art LLMs are not trusted for automating customer-facing functions, such as loan origination, know your customer and compliance monitoring.

- Healthcare: Beyond automating patient communication and summarizing medical literature, reasoning models can analyze patient data to suggest diagnoses and personalized treatment plans, considering complex medical histories. They can also accelerate drug discovery by predicting molecular interactions and potential drug efficacy.

- Legal: In addition to summarizing legal documents and extracting contract terms, reasoning models can review legal documents, identify relevant case law and provide detailed legal reasoning for case preparation. They also enhance compliance monitoring by continuously analyzing regulatory adherence data.

- Disinformation security: In addition to detecting and verifying disinformation, reasoning models can be used to analyze context, generate counternarratives and educate users on recognizing false information. They can also automate content moderation and collaborate with experts to enhance strategies for responding to disinformation.

Recommended Actions

- Expand market reach by integrating or developing solutions with open-source models, which offer cost-effectiveness and accessibility, aligning with the growing interest in smaller, self-hosted models.

- Reduce development costs by adopting lean development practices, such as model distillation and mixture of experts (MoE) architecture, to create efficient AI models that operate on resource-constrained hardware.

- Boost the efficiency of generative AI investments by investing in robust software platforms for managing AI model life cycles, ensuring effective development, deployment and maintenance.

- Build user trust by incorporating transparency and explainability in AI models, similar to DeepSeek R1’s chain-of-thought reasoning, to improve user experience and facilitate error resolution.

Gartner Recommended Reading

Small Language Models

Analysis By: Annette Zimmermann, Ray Valdes

Definition:

Small language models (SLMs), also called “light language models” or “small models,” support use cases where traditional large language models (LLMs) are not feasible or ideal. SLMs represent a trade-off between the generalized power of LLMs and the narrower requirements of resource-constrained environments, such as on-premises deployments, smartphones or edge network nodes. SLMs are much smaller than their LLM counterparts. Examples include Meta’s Llama 3.2 1B, Mistral AI’s Mistral 7B, Aleph Alpha’s Pharia-1-LLM-7B-control and DeepSeek-VL2. The number of parameters that categorize a language model as small has changed over time in relation to mainstream LLMs. In addition, the dichotomy of small versus large has become more complex, with various sizes for different use cases. These include 3 billion parameters or fewer for edge devices, 7 billion parameters or fewer for smartphones, 70 billion parameters for laptops or equivalents, and 130 billion parameters or more for on-premises servers. This spectrum of sizes and use cases is evolving rapidly. Most of the SLMs mentioned are open source.

Sample Vendors

Apple; Databricks; DeepSeek; Google; IBM; Meta; Microsoft; Mistral AI; NVIDIA; OpenAI

Range: 1 to 3 Years

SLMs are one to three years from reaching early majority customer adoption due to rapid innovation and strong market demand.

Investment is growing from startups and hyperscalers in the development of SLMs. This vendor activity and the emergence of SLMs so soon after the popularization of LLMs signal strong market demand for language models that can:

- Run in an enterprise data center or in disconnected mode (i.e., without a cloud connection)

- Reduce infrastructure and operational costs

- Run on small devices like mobile phones or laptops