Magic Quadrant for Strategic Portfolio Management

ARCHIVED

4 August 2025 - ID G00818813 - 37 min readBy John Spaeth, Shailesh Muvera, and 3 more

Strategic portfolio management technologies integrate various portfolio structures to model alternative paths to successful business outcomes. This research helps portfolio management leaders focused on digital investments identify vendors dedicated to increasing SPM effectiveness with technology.

Strategic Planning Assumptions

By 2028, 80% of portfolio management offices (PMOs) will principally provide outcome-driven portfolio management and will not be directly involved in delivery orchestration.

By 2027, 75% of organizations will enrich business architecture by connecting financial benefits to digital investment decisions.

By 2027, 80% of portfolio leaders will adopt collaborative capability-based methods for the planning and prioritization of all work needed to support the democratized delivery of digital outcomes.

Market Definition/Description

Gartner defines the strategic portfolio management (SPM) market as comprising both cloud-based and on-premises applications for enterprisewide strategic planning and execution, supporting advanced portfolio management. SPM offerings integrate multiple portfolios with interdependent structures, creating a dynamic model of the path to realize strategic outcomes. These products are ideally suited for organizations pursuing digital strategies, which demand extensive stakeholder collaboration to continually adapt to changing conditions.

Organizations use SPM to align portfolios with strategy and apply value-based decision making for ongoing flexibility in the midst of progress, disruptions and opportunities. Digital strategies combine portfolios representing different contexts, such as business capabilities, investments, applications, services, assets, programs, products and projects. Strategists, business leaders, IT leaders and PMOs cooperatively align the utilization of these diverse portfolios to progressively achieve strategic objectives. SPM technology is beneficial in the pursuit of digital business outcomes as it helps navigate complexity while balancing the following fundamental constraints:

- Limited funding to invest

- Expected value of opportunities

- Availability of people with necessary skills to perform work

- Enterprise IT needs for business capabilities

- Time required to accomplish strategic goals

SPM technology offerings enable organizations to effectively engage stakeholders to conduct strategic planning and execution. It supports the following key use cases:

- Strategy execution management: The projected value generated through planned execution is compared with defined measurable goals. This process allows for adaptation to enhance business outcomes. SPM enables ongoing assessment of progress, forecasts and dynamic conditions to evaluate alternative courses of action that improve goal realization.

- Enterprise program and portfolio management: SPM optimizes the utilization of funding, people and other resources managed in portfolios, empowering enterprisewide stakeholders to achieve goals. Portfolio governance is performed in alignment with strategy to distribute accountability for results. Continual monitoring and analysis support collaboration to adapt plans for better outcomes.

- Integrated IT portfolio analysis: The progressive transition of IT to support the future state of digital business is managed through distinct portfolios. The various IT elements that are modified and built to help achieve business outcomes are interdependent. SPM enhances the planning and execution of strategies by integrating enterprise IT and investment considerations.

Mandatory Features

The mandatory features for this market include:

- Strategy-based performance management: Strategy, defined as goals achieved over time, provides the primary representation of measurable success and is refined as needed. It ensures accountability, establishes a value basis for impact analysis and decision making, and supports outcome-oriented portfolio assessments.

- Outcome-driven planning: Helps develop plans that span near to long-range horizons for initiatives at different life cycle stages, and progressively elaborate plans as understanding improves. It reflects the utilization of portfolio capacity and achievement of goals using roadmaps, forecasts and analyses that compare expected goal realization to desired outcomes.

- Strategic portfolio optimization: Provides real-time dashboards and interactive navigation built upon interdependent portfolios, strategic goals, actual execution, available capacity, current plans and alternative scenarios. It also supports stakeholder collaboration and workflows to respond to changing conditions and evaluate opportunities that drive better outcomes.

- Technology strategy analysis: Applies common representations for IT strategy to support portfolio analysis in the context of the changing technology landscape. It integrates the unique life cycles of business capabilities and IT portfolio elements with investment and value forecasts to provide a comprehensive strategic planning and execution model.

- Configurable programs: Establishes distinct scopes across portfolios to focus on specific aspects of broader strategic objectives. It supports stakeholder concentration on specific programs, products, regions, domains, teams, etc. relevant to the organization while respecting constraints driven by external dependencies.

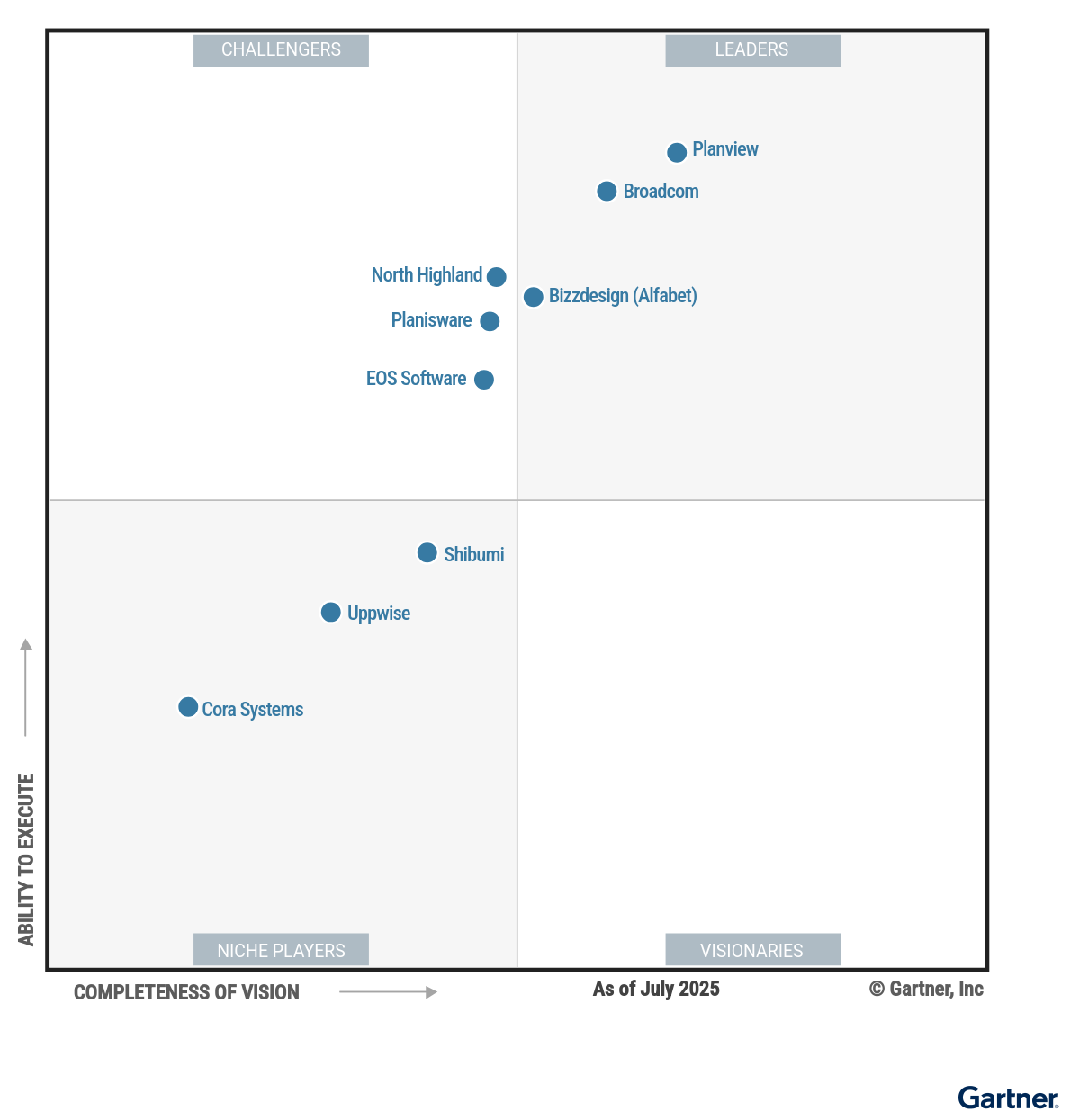

Magic Quadrant

Vendor Strengths and Cautions

Bizzdesign (Alfabet)

Bizzdesign is a Leader in this Magic Quadrant. Its Strategic Portfolio Management (SPM) solution, Alfabet — acquired from Software AG in January 2025 — emphasizes the integration of enterprise architecture (EA) and SPM for transformation. Bizzdesign maintains a strong global presence, serving a diverse range of industries. Most of Alfabet’s customers are in EMEA and North America. Alfabet’s roadmap highlights preconfigured accelerators for faster and more effective adoption.

- Bizzdesign and its Alfabet offering have a strong track record in supporting enterprise architecture and IT portfolio management with detailed information and analysis. Its strengths align well with prospective customers managing complex IT transformations with SPM.

- Bizzdesign’s horizontal practice framework approach within Alfabet is relevant across industry verticals. Alfabet’s flexible accelerators and workspaces enable organizations to tailor the product’s implementation with their SPM adoption objectives.

- Bizzdesign demonstrates a strong commitment to compliance, addressing international, regional and national regulatory requirements. This experience in compliance aligns well with organizations operating in highly regulated sectors.

- Bizzdesign’s EA-centric transformation approach hasn’t heavily influenced Alfabet at this stage. Currently, Alfabet aligns with IT-strategy-driven organizations and roles, which may reduce its appeal among non-IT leaders and broader business stakeholders.

- Alfabet’s capabilities in investment planning, value forecasting and performance monitoring lack the refinement of competing SPM solutions. Prospective customers should evaluate its fit for strategy execution management (SEM) and enterprise program and portfolio management (EPPM) use-case needs.

- Bizzdesign’s future investment in Alfabet will reflect an SPM product within the context of its software portfolio. Alfabet’s roadmap may be disrupted to align with broader product strategies. Prospective customers should closely monitor how Bizzdesign harmonizes Alfabet within its transformation suite.

Broadcom

Broadcom is a Leader in this Magic Quadrant. Its SPM product, Clarity, focuses on improving decision-making and digital transformation effectiveness across enterprises. With operations spanning North America, EMEA and Asia/Pacific, Broadcom supports a global customer base that spans a wide range of industries. The Clarity product roadmap emphasizes AI-driven productivity enhancements and improved analytical capabilities, with a strong focus on usability.

- Broadcom’s robust partner network effectively integrates third-party implementation and consulting partnerships with its own scalable customer success programs. This model enables a broader range of services than typically offered directly by providers in this market.

- Broadcom has continually refined its understanding of strategy, business, IT and portfolio leaders’ needs, particularly in a digital business context. Its people- and value-centric product optimization aligns well with predominant customer challenges in this market.

- Clarity accommodates a wide range of portfolio management maturity levels, enabling organizations to meet immediate needs while evolving toward more advanced, value-driven decision-making and product-oriented practices.

- Broadcom’s strategic focus on value stream management (VSM), with Clarity positioned as part of its ValueOps suite, may not align with all organizations. When evaluating Clarity, prospective customers should distinguish its SPM use-case support from its extended VSM capabilities.

- Broadcom Clarity’s strong reputation as a program and portfolio management (PPM) product overshadows its reputation as an SPM offering. This perception could limit its appeal to organizations seeking a dedicated SPM product, potentially limiting the customer base driving SPM-focused roadmap developments.

- Broadcom’s Clarity strategy is not focused on SPM exclusively. Organizations with a technology strategy to build an SPM model by integrating across several detailed planning and execution tools may find limited value in Clarity’s full feature set.

Cora Systems

Cora Systems (Cora) is a Niche Player in this Magic Quadrant. Its SPM product, Cora SPM, emphasizes long-term strategic planning and optimization of project-driven portfolios. Cora’s operations and customers are concentrated in EMEA and North America. Its customers represent the manufacturing, aerospace and defense, life sciences, and government verticals. The Cora SPM roadmap includes AI integration, predictive analysis and customer-industry-oriented enhancements.

- Cora maintains a close partnership with its customers, resulting in vertical expertise. Its product roadmap aligns with the specialized needs of its customers’ industries. Cora’s market strategy continues to target growth in these verticals.

- Cora’s optimized project analysis and reporting for complex and regulated industries is a differentiator. Cora’s expertise in industrial manufacturing use cases and challenges facilitated expansion into adjacent sectors such as government contracting.

- Cora is a SAP as a PartnerEdge Build partner. Cora provides a two-way connector for time sheet data, project cost accounting and contract management. This integration enhances accuracy and streamlines critical reporting and regulatory compliance.

- Currently, Cora has limited focus on digital business, and very few of its existing customers require integrated IT portfolio analysis (IIPA) use-case support, thus resulting in a minimal voice of the customer informing its product roadmap. Cora SPM may not align with organizations with business-IT alignment objectives and dynamic technology landscapes.

- Cora’s strengths in highly regulated industries result in country-level expertise, including the U.S., the U.K. and Ireland. Prospective customers in other countries interested in Cora for its regulatory experience should assess Cora’s ability to incorporate relevant standards.

- Cora’s integration capabilities are used primarily for project-level source data in a project portfolio, which is optimized using SPM. Cora SPM is not yet commonly integrated with other portfolio data sources, such as applications, products, services and assets.

EOS Software

EOS Software (EOS) is a Challenger in this Magic Quadrant. Its SPM product, EOS ITPM, is designed to align IT and business strategies. EOS operates primarily in North America and Asia/Pacific, with a customer base concentrated in North America and a smaller customer presence in both EMEA and Asia/Pacific. Its clients span various private-sector industries. EOS ITPM’s roadmap focuses on AI enablement, including process automation, integrations and experience enhancements.

- EOS promotes a technology-centric SPM approach. EOS ITPM provides strong capabilities for optimizing technology portfolios through outcome-driven planning and execution. This focus aligns well with IT leaders and extended IT stakeholders.

- EOS provides implementation, configuration and ongoing consulting support, as well as industry and best-practice packages at no additional cost. This flexible approach enables its customers to progressively increase SPM maturity at a sustainable pace, based on their current state and objectives.

- EOS ITPM supports extensive customization of workflows and visualizations, delivering a personalized SPM experience that incorporates best practices. EOS ITPM’s low-code configuration also enables customers to refine their practices and technology use concurrently.

- EOS ITPM’s strong focus on technology may be more detailed than what strategy, business and portfolio leaders prefer. Prospective customers should assess whether platform tailoring can provide intuitive, decision-ready insights for all roles involved in SPM.

- EOS’s strategy of flexible configuration requires co-creation of effective practices to maximize effectiveness. Prospective customers should partner with EOS to pursue broad improvement objectives, rather than specific processes. In addition, wide stakeholder engagement is essential to tailor the user experience during implementation.

- EOS lacks a physical presence and strategic partnerships in EMEA and Latin America. Prospective customers in these regions should confirm the availability and adequacy of remote support, including service hours and response levels.

North Highland

North Highland is a Challenger in this Magic Quadrant. Its SPM product, NH360 Strategic Portfolio Manager (NH360 SPM), focuses on aligning strategy with evolving operating models. North Highland’s operations and customers are primarily in North America and EMEA, and it serves a wide range of industries, including utilities, manufacturing, healthcare and financial services. The NH360 SPM’s product roadmap includes enhancing portfolio insights and expanding architecture representations.

- North Highland supports digital transformation with business and EA integration, modeling the evolving landscape as investments drive change. NH360 SPM’s holistic top-down views support diverse leaders’ perspectives.

- North Highland leverages its deep transformation consulting expertise to inform NH360 SPM’s product roadmap. Its near-term strategy includes building vertical, industry-specific solutions and accelerating alignment with common business models and sector-specific needs.

- North Highland offers a wide range of services — including support, consulting, education and training — tailored to various organizational roles. Its consulting coverage of practices includes capability roadmaps, gap analysis, process refinement and transformation delivery.

- The synergy between North Highland’s consulting services and its SaaS platform may not be as beneficial for smaller-scale transformations. Prospective customers should assess whether NH360 SPM’s accelerators and vertical solutions align with their SPM objectives.

- NH360 SPM offers limited out-of-the-box integrations, and NH360 Data Exchange supports primarily data import. While NH360 SPM’s Microsoft Power Platform integration allows process-driven real-time connections, customers should confirm that all their integration requirements can be met.

- NH360 SPM’s deep integration with Microsoft 365 can introduce complexity for release management. As both North Highland and Microsoft update their products, close coordination is essential to avoid disruptions in critical strategic workflows.

Planisware

Planisware is a Challenger in this Magic Quadrant. Its SPM product, Planisware Enterprise, focuses on strategy-driven portfolio optimization. The company operates primarily in EMEA and North America, with a strong customer base in manufacturing, natural resources, healthcare and insurance. The product roadmap for Planisware Enterprise includes expanding AI-driven analysis and automation, enhancing IT integration, and UI or user experience (UX) improvements.

- Planisware has responded to market needs for business-IT alignment as essential for SPM in digital business. Planisware Enterprise has steadily improved support for IIPA and digital transformation.

- Planisware’s vertical industry alignment approach includes segmented teams that specialize in specific use cases or business functions. Its industry-aligned best-practice packages are also included at no cost.

- Planisware maintains close relationships with its customers through dedicated customer success managers, regular health assessments, best-practice working groups and annual conferences. A customer advisory board also contributes to product roadmap prioritization, ensuring alignment with user needs.

- Planisware’s digital business and IIPA use-case improvements are more recent developments. As a result, Planisware Enterprise has not yet fully benefited from broad adoption and iterative customer feedback. Prospective customers should evaluate how current capabilities align with their IIPA goals and stakeholder expectations.

- The Planisware Enterprise product roadmap includes expanding SPM use-case coverage, extensive AI advancements and a major release. The combined scale of changes increases risks of disruption for user adoption and incremental fixes.

- Planisware Enterprise’s robust functionality can be challenging for some users, particularly for impact analysis and roadmaps. The upcoming version (8.x) is expected to address these gaps. Prospective customers should request a detailed demonstration of the new version to evaluate alignment with different user role expectations.

Planview

Planview is a Leader in this Magic Quadrant. Its SPM product, Planview Portfolios, is designed to accelerate value delivery through adaptive portfolio prioritization. With a broad global presence, Planview serves a wide range of industries. Its customer base is strongest in North America and EMEA and growing in Asia/Pacific. Planview Portfolios’ roadmap includes elevating generative AI (GenAI) insights and UX improvements, and enhancing planning capabilities.

- With Planview’s tenure in the SPM market, Planview Portfolios is a comprehensive and mature solution that continues to evolve rapidly. Planview’s proven track record supporting advanced practices and diverse delivery modes in many industries aligns well with complex organizations.

- Planview has expanded its partner network, contributing to geographic expansion and significant wins. This expanded network gives organizations greater flexibility to engage with partners that bring regional, business or domain-specific expertise critical to outcomes with SPM.

- Planview actively promotes the value of SPM as a thought leader in the market. It leverages customer insights and research to deliver knowledge via multiple channels, elevating understanding of SPM practices independent of technology.

- Planview Portfolios is a comprehensive enterprise solution that delivers the most value to organizations with mature practices or those undergoing long-term transformation. Prospective customers should consider the total investment — beyond software acquisition and implementation — required to realize full SPM benefits.

- Planview’s fast-paced innovation can be disruptive. Organizations must be prepared to adopt a continuous improvement mindset to keep pace with new features and enhancements that drive higher levels of SPM effectiveness.

- As Planview grows its partner network to supplement direct sales, some verticals and regions may have limited third-party options. Prospective customers seeking partner engagement should carefully evaluate partners’ domain expertise and product familiarity to ensure alignment with their needs.

Shibumi

Shibumi is a Niche Player in this Magic Quadrant. Its SPM product, also named Shibumi, focuses on enterprise-scale strategic transformation. Shibumi’s operations are headquartered in North America, with field presences in EMEA and Asia/Pacific. Its customer base spans diverse industries and regions. Shibumi’s roadmap includes reporting and visualization enhancements, AI-enabled predictions, and role-driven UX.

- Shibumi is highly focused on the needs of executives. Its SPM product is optimized for outcome-driven portfolio modeling that supports strategic decision making. A significant portion of its user base comprises non-IT leaders.

- Shibumi’s integration-centric product strategy allows its SPM solution to be layered above existing fit-for-purpose technologies. Real-time interfaces create a unified SPM model as a source of truth, while allowing teams to continue using their preferred tools.

- Shibumi has a robust partner network that includes major advisory firms, which often use Shibumi at the core of transformation programs. This network enables customers to build and sustain SPM practices without ongoing dependency on professional services or proprietary solutions.

- While Shibumi’s integration capabilities support IT and EA sources and some customers incorporate these portfolios, Shibumi is not widely used for the IIPA use case. As a result, its IIPA-related capabilities are foundational in comparison to its advanced SEM and EPPM use-case support.

- Shibumi doesn’t offer vertical-industry-specific implementation packages. Instead, it relies on combining templates and best practices as needed, along with partner-developed solutions. Prospective customers should assess whether they prefer organization-specific tailoring or a more comprehensive industry-aligned partner deployment.

- Shibumi’s integration-based model may not align with organizations seeking a single-vendor for SPM and detailed initiative management software to address all strategy planning and execution technology gaps. Prospective customers should evaluate whether a natively integrated platform better supports their strategy to build SPM effectiveness.

Uppwise

Uppwise is a Niche Player in this Magic Quadrant. Its SPM product, Uppwise SPM, is focused primarily on enterprise portfolio management, supporting strategic decision making to enhance business value realization. With operations in EMEA and Asia/Pacific, Uppwise serves a diverse range of industries, primarily within EMEA. Its product roadmap emphasizes AI-driven capabilities for prioritization and predictive analytics.

- Uppwise targets midsize organizations that are pursuing high-integrity strategic alignment to optimize investments and initiatives. Uppwise SPM provides outcome-oriented analysis with a portfolio model that balances robustness and simplicity, enhancing adaptability.

- Uppwise demonstrates commitment on customer success, starting with its WisePath delivery framework, which accelerates implementation and adoption. Uppwise supports ongoing effectiveness by supporting transition to adaptive practices and shaping its roadmap with customer feedback.

- Uppwise SPM’s modular architecture allows organizations to mature their practices and scale usage at their own pace. The platform is adaptable across industries and organizational structures through configuration rather than deep customization.

- Uppwise’s growth has been concentrated in EMEA, with recent expansion into northern areas of the region. Prospective customers outside EMEA should assess Uppwise’s support coverage and service levels based on the organization’s system criticality tier for SPM.

- Uppwise SPM offers limited support for the IIPA use case. Its customer base has not yet asked for deeper business-IT modeling. Organizations requiring comprehensive technology portfolio analysis may be constrained with Uppwise.

- Uppwise’s customer-centric strategy has driven SPM product capability advancements at a slower pace compared with other providers evaluated in this Magic Quadrant. Prospective customers seeking cutting-edge capabilities should assess whether Uppwise’s product roadmap aligns with their innovation needs.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

Bizzdesign (Alfabet) was added as a result of Bizzdesign’s acquisition of Alfabet from Software AG.

Dropped

Software AG was dropped as a result of Bizzdesign’s acquisition of Alfabet from Software AG.

Wellspring (Sopheon) was dropped from this Magic Quadrant. Wellspring’s Accolade is optimized for innovation portfolio orchestration with a concentration on industries that manufacture and deliver physical goods. Consequently, it did not satisfy the inclusion criteria for this Magic Quadrant.

Inclusion and Exclusion Criteria

To qualify for inclusion, providers must meet all of the following criteria:

- Demonstrate active participation in the SPM market as a pure-play primary technology provider of SPM software offering integrated strategy, goal, business capability, investment, portfolio, program, project, digital product and application management features.

- Deliver an SPM product with a clear software business model, not a consulting business model that includes software for customer use.

- Provide stand-alone SPM technology products or online application services that don’t require purchase of, or upgrades to, non-SPM or non-PPM technology platforms or external solutions to obtain full SPM functionality.

- Demonstrate a clear focus on digital business and the integration of SEM, EPPM and IIPA use cases catering to the needs of strategy, business, IT and portfolio leaders.

- Demonstrate an evolving market presence aligned with digital business use of SPM, including market penetration, sales and support for multiple regions of the world.

- Sustain a responsive SPM product development and innovation cadence with multiple product releases per year.

- Demonstrate stability and longevity as a provider and for its product(s) in the open SPM market. For at least the past 10 consecutive years, it must have provided generally available SPM product(s) and active marketing to strategy, business, IT and portfolio leaders for SEM, EPPM and IIPA use cases, and without any significant company, product or service disruptions.

- Have secured at least 10 new SPM customers (not renewals or additional seats) during the past 12 months, using its product(s) specifically for SEM, EPPM and/or IIPA use cases performed by strategy, business, IT and portfolio leaders.

- Have at least $5 million in annual SPM software revenue in the previous 12 months, derived from sales supporting SEM, EPPM and IIPA use cases, and/or reliable financial backing.

In conjunction with the inclusion criteria, the following exclusion criteria are the conditions/boundaries by which vendors are excluded from consideration in this research:

- This Magic Quadrant excludes providers participating primarily in markets adjacent to or outside of the SPM or PPM market. This is true even in cases where the vendors offer SPM “extensions” or “modules” as part of a “single source” value proposition. Therefore, ERP, IT service management (ITSM), sales force automation (SFA) and other similar platform providers offering such extensions or modules are excluded from this research.

- Providers with a primary focus on, and significant presence in, niche or specialized PPM or SPM markets are excluded (e.g., architecture, engineering, construction; and professional service automation).

- “Certified partners,” systems implementers or consulting firms using a third party’s technologies to deliver “products” or “solutions” for SPM are excluded from this Magic Quadrant.

- Providers of proprietary technology solutions delivered only in combination with ongoing professional services, advisory services, managed services or operational as-a-service offerings are excluded from this research.

Evaluation Criteria

Ability to Execute

Product or Service: Evaluation of the application services of the providers in this defined market is conducted, including current product/service capabilities, quality, feature sets and skills, as defined in the Market Definition and detailed in the subcriteria. The ability to deploy and use the provider’s product specifically and only for SPM is verified. Product features and capabilities provided for key SPM end users, including business, IT and portfolio leaders, in conjunction with integrated SPM use cases, are evaluated. Ease of use, balanced with functional depth and cost-effective pricing, are examined, as well as how well and how complete the vendors and products support SPM depth and breadth. Advancements in applying emerging technologies for SPM are measured, as well as the availability and adoption by customers in the field. Use of the SPM product specifically for digital business scaling and harvesting, as well as the benefits tracking of the same, is also measured.

Capabilities specifically needed for strategy, business, IT and portfolio leaders are evaluated. Scalability of any applicable products and breadth of deployment options for SPM use cases, including SEM, IIPA and EPPM, are also assessed. Advancements in applying AI and robotic process automation (RPA) to SPM technology are measured, as well as the availability of AI and RPA capabilities in the product, and adoption by customers in the field. Use of the SPM product specifically for digital business scaling and harvesting, as well as the benefits tracking of the same, is also measured.

Overall Viability: Viability includes an assessment of the organization’s overall financial health, as well as the financial and practical success of the business unit. This criterion views the likelihood of the organization to continue to offer and invest in the SPM product, as well as the product position in the current portfolio. Also assessed is the probability that the provider will advance the state of the art within the product. Organic and other signs of growth are noted.

Sales Execution/Pricing: The organization’s capabilities in all presales activities and the structure that supports them are examined. These include deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel. Renewal rates, compared to reported losses due to nonrenewals, are evaluated. The ability of the provider to sell the product specifically to business, IT leaders and portfolio leaders for the purposes of SPM is also measured.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve, and market dynamics change are reviewed. This criterion also considers the provider’s history of responsiveness to changing market demands. The provider’s adaptation of its SPM product strategy to support an emergent SPM marketplace is measured. Track record in the field is also examined.

Marketing Execution: We analyze the clarity, quality, creativity and efficacy of programs designed to deliver the organization’s message in order to influence the market, promote the brand, increase awareness of products and establish a positive identification in the minds of customers. This “mind share” can be driven by a combination of publicity, promotional activity, thought leadership, social media, referrals and sales activities. Effectiveness in the context of digital business is also considered.

Customer Experience: Products and services and/or programs that enable customers to achieve anticipated results with the products evaluated are researched. Specifically, this includes quality supplier/buyer interactions, technical support or account support. This may also include ancillary tools, customer support programs, availability of user groups and service-level agreements. The effectiveness of customer engagement to influence product evolution is also evaluated.

Operations: The ability of the organization to meet goals and commitments is measured. Factors include quality of the organizational structure, skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently. The integration of operations following mergers, acquisitions or divestitures is also considered.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | High |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | High |

Marketing Execution | Medium |

Customer Experience | High |

Operations | Medium |

Source: Gartner (August 2025)

Completeness of Vision

Market Understanding: This criterion assesses the provider’s ability to understand SPM customer needs and translate them into products and services. Vendors that show a clear vision of their market listen, understand customer demands, and can shape or enhance market changes with their added vision. The provider’s approach to address the needs of an emerging SPM marketplace is evaluated in the context of the Market Definition. Exploratory product development and other activities (for example, M&As) to set market direction are also considered.

Marketing Strategy: Clear, differentiated SPM messaging consistently communicated internally, and externalized through social media, advertising, customer programs, and positioning statements, is evaluated. The provider’s expression of customer value propositions that align with the Market Definition are evaluated.

Sales Strategy: A sound strategy for selling that uses the appropriate networks, including direct and indirect sales, marketing, service, and communication, is assessed. The ability of partners to extend the scope and depth of market reach, expertise, technologies, services and their customer base, is also researched. The ability of the provider to engage with key SPM roles, including business, IT and portfolio leaders, is evaluated.

Offering (Product) Strategy: An approach to product development and delivery that emphasizes market differentiation, functionality, methodology, and features as they map to current and future requirements is evaluated. The product’s alignment with digital business and the needs of business, IT and portfolio leaders is considered. Product functionality supporting the depth, breadth and integration of SPM use cases are evaluated. Process consulting options that enhance customer success are considered. Integration with data sources essential for SPM modeling are examined. The ability to support a global installed base is evaluated. The transformation of past product acquisitions and emerging technologies into greater and lasting customer value are examined. Product roadmap alignment with the Market Definition is also considered.

Business Model: The design, logic and execution of the organization’s business proposition to achieve continued success is evaluated. How well the business model provides value to customers is also examined, as well as its alignment with the Market Definition and integrated SPM use cases.

Vertical/Industry Strategy: The strategy to direct resources (sales, product and development), skills and products to meet the specific needs of individual market segments, including verticals in the context of the Market Definition, is evaluated.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or preemptive purposes are evaluated. The level of innovation specifically in SPM is measured in the context of the Market Definition and integrated SPM use cases. Also evaluated is the vendor’s ability to offer regular product releases and exhibit rapid development and adaptive releases. Functionality demonstrating a strong SPM product vision that pushes the market — not just the provider — in new directions is recognized. This is a gauging of the ability to lead the “herd” of the market, rather than follow it. Acquisitions should relate to customer value and be followed by strong evidence of innovation in added product development, product integration, and customer care and support programs, rather than simple maintenance of a product line and installed base.

Geographic Strategy: This criterion assesses the provider’s strategy to direct SPM resources, skills and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels and subsidiaries, as appropriate for that geography and market.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | High |

Sales Strategy | High |

Offering (Product) Strategy | High |

Business Model | Medium |

Vertical/Industry Strategy | Low |

Innovation | High |

Geographic Strategy | Low |

Source: Gartner (August 2025)

Quadrant Descriptions

Leaders

Leaders continually refine their market understanding to effectively adapt their offerings to customers’ current needs and anticipate future priorities. They build on existing strengths and regularly deliver enhancements to maximize business outcomes from digital investments through SPM’s integrated use cases (SEM, EPPM and IIPA). Leaders maintain a balanced SPM technology roadmap, incorporating bold innovations, continuous improvement and customer-driven needs. Failure to maintain a steady pace of advancement in line with maturing expectations can result in a Leader losing ground within the market.

Leaders also effectively support customers’ pursuit of greater strategic execution effectiveness in the climate of continuous disruption and uncertainty. In addition to their products, Leaders promote SPM practices, digital innovation, adaptability, and agility to educate and feed customer interests. They have robust marketing, sales and operations potency to customer acquisition, implementation and success across a broad geographies and industries, which drives SPM recognition and overall market growth.

Challengers

Challengers have an established foundation built on their success in one of the preceding portfolio-based market opportunities targeting SEM, EPPM or IIPA use cases. Challengers have supplemented their established core strengths to cover all three SPM use cases. More recent capabilities developed, or added through acquisition, are being refined and integrated in the product.

Challengers are gaining recognition as technology providers that can fully support SPM effectiveness. Challengers ensure their product roadmaps meet the demands of existing customers and position their offering to earn new SPM-driven customers. They actively promote their enhanced offerings and the SPM’s benefits to expand within existing customer relationships. New customer growth momentum also continues based on a firmly established reputation.

Visionaries

The SPM market does not yet have any identified Visionaries. SPM is gaining recognition as a modern portfolio management approach to increase digital business success in dynamic conditions. There is strong potential for Visionaries to emerge as the market matures. Future Visionaries may include new providers and existing vendors currently in other markets (e.g., CRM, CWM, enterprise agile planning [EAP], ITSM and adaptive project management and reporting [APMR]). Providers rebranding offerings established in other markets as “SPM” and reflecting an SPM value proposition isn’t sufficient to be considered a Visionary based on Gartner’s Market Definition.

Niche Players

Niche Players typically cover at least two, but not all three, SPM use cases (SEM, EPPM and IIPA) well. Each has a solid portfolio management base that is extended to address strategy-to-execution alignment. Niche Players’ product focus often discounts IIPA’s importance for digital business strategic objective achievement initially. This strategy builds SEM and EPPM use-case effectiveness for multidimensional, integrated program and portfolio management, bringing IIPA-driven innovation and growth within reach. Niche Players may also be regionally concentrated, impacting their global reach. Niche Players address the needs of a subsegment of the broader and still emerging SPM market. They can be an optimal fit for customers with SPM objectives that align with the vendor’s focus.

Context

This Magic Quadrant offers a comparative analysis of providers that are the main players in the emerging SPM market as defined by the inclusion criteria. Relative placement within the quadrants is based on a variety of criteria, and the strengths and cautions further characterize the included providers. The results were developed according to the Magic Quadrant process, which includes a combination of research and analysis. Evaluation of SPM providers also includes input from the Gartner SPM research community, ongoing provider briefings, interactions with Gartner clients, market developments and other sources.

Gartner’s SPM Magic Quadrant is a useful input for identifying and evaluating SPM software providers that align with common digital business enterprise needs. Gartner’s Critical Capabilities for Strategic Portfolio Management provides essential insight for SPM product selection, as it evaluates the SPM products against Gartner’s SPM use cases (SEM, EPPM and IIPA). Prospective customers must clarify their enterprise objectives for increasing strategic effectiveness and assess alignment with these specific use cases to best utilize this research.

SPM technologies combine interdependent and varied portfolios representing the transition toward future states of operation. Portfolios of business capabilities and technology landscape elements are highly relevant life cycle contexts that are integrated with investment and initiative-oriented portfolios. SPM technologies are stand-alone enterprise-level portfolio modeling solutions that don’t require specific portfolio structures, strategic approaches, architecture frameworks or delivery methodologies. Different practice domains often use technologies optimized for their purposes and roles. Integration with multiple tools is essential for SPM technologies to build and sustain a comprehensive portfolio model as a trusted source of insight. Furthermore, offerings in this research do not require acquisition of other solutions for project planning and execution, work management, agile development technologies (e.g., APMR, collaborative work management [CWM] and EAP) or enterprise platforms (e.g., ERP and ITSM).

SPM transforms how organizations collaborate using portfolio management in the pursuit of desired outcomes, which extends throughout an enterprise and requires unique technologies. Gartner’s SPM Magic Quadrant includes only providers that have demonstrated experience supporting strategic planning and execution through enterprisewide portfolio modeling and contextual use cases involving strategy, business, IT and portfolio leaders. SPM effectiveness involves progressive maturity growth, often over several years. Inclusion in this Magic Quadrant requires a proven track record of product evolution and customer success. Providers in this research are a distinct group with deep understanding of customer journeys to attain effective SPM, gained over 10 or more years.

Market Overview

Portfolio management leaders are increasingly realizing that disparate portfolio practices and analysis cannot support the pace of digital business. According to the Gartner Technology Adoption Roadmap for Large Enterprises for 2025 Survey, the number of SPM frameworks, processes and tools that are in deployment this year have almost doubled compared to last year (32% this year versus 17% last year).

SPM technologies maintain strategy-to-outcome alignment across diverse portfolios The heart of SPM is the portfolio model of integrated business, IT and investment structures with elements that have unique life cycles. SPM’s advanced analysis capabilities enable strategy, business, IT and portfolio leaders to chart the path to success and rapidly respond to dynamic conditions with a continuous focus on strategic goals.

The major trends that Gartner sees in analyzing this emerging market include:

- SPM practices are paramount for successful adoption. Organizational readiness remains the greatest roadblock to adopting SPM frameworks, processes and tools. An investment in SPM extends well beyond the technology. To succeed with SPM, organizations must commit to new practices, collaborate and expand trust, all while moving at an ever-increasing pace. Providers and their partners offer customer success services following initial implementation to support building best practices with SPM technology.

- AI enablement is steadily progressing. Providers are expanding their ability to integrate SPM technologies with an enterprise’s broader AI strategy and selected models. Most providers have introduced conversational capabilities, summarization and suggestions to support interpretation, reduce administration effort and facilitate learning. Scenario development and predictive analytics are also available from most providers. AI’s value for SPM is heavily dependent on organization-specific data to produce trusted and actionable results.

- More customers are recognizing the benefits of integrated IT portfolio analysis (IIPA). When an organization first adopts SPM, they typically focus on aligning investments with desired outcomes through the enterprise program and portfolio management (EPPM) and strategic execution management (SEM) and use cases. However, more organizations are now focusing on strengthening business-IT partnership and increasing adaptability. As a result, organizations are expanding their SPM objectives to include integration of IT portfolio structures to enhance insight and collaboration.

- Technology adaptation is getting simpler. Providers are offering no-code and low-code interfaces that make it easier for customers to configure portfolio structures, processes, dashboards and interfaces. This flexibility simplifies the process of aligning SPM technologies with the needs of different stakeholders and supports progressive refinement to increase maturity.

- Products marketed as SPM may not be complete SPM solutions. “SPM” has become a broadly and inconsistently applied marketing term, suggesting portfolio modeling and decision-making capabilities that products might not actually fulfill. Currently, the providers that can support enterprise-scale portfolio modeling for digital business also demonstrate effective capabilities in key SPM use cases as defined in the SPM market definition for this Magic Quadrant.

Acronym Key and Glossary Terms

| EA | enterprise architecture |

| EAP | enterprise agile planning |

| EMEA | Europe, the Middle East and Africa |

| EPMO | enterprise portfolio management office |

| EPPM | enterprise program and portfolio management |

| GenAI | generative artificial intelligence |

| IIPA | integrated IT portfolio analysis |

| ITSM | IT service management |

| M&A | mergers and acquisition |

| PPM | program and portfolio management |

| RPA | robotic process automation |

| SEM | strategy execution management |

| SLA | service-level agreement |

| SPM | strategic portfolio management |

| UI/UX | user interface/user experience |

Gartner Technology Adoption Roadmap for Large Enterprises for 2025 Survey. This survey harnesses the collective wisdom of IT leaders to understand deployment plans, adoption timelines, value and risks of more than 200 technologies across infrastructure and operations; data and analytics; software engineering; cybersecurity; and strategic portfolio management. The survey was conducted through an online panel from August through October 2024 among 569 respondents from North America, EMEA and Asia/Pacific across industries in enterprises with annual revenue of more than $1 billion. Qualified respondents were CxOs, senior IT leaders, their peers and their direct reports. This research summarizes findings from 120 respondents identified as SPM leaders. SPM leaders indicate their enterprise’s current adoption plan for each technology across the following stages: not monitoring, monitoring, planning, piloting, in deployment and already deployed. These results are aggregated to determine a final adoption stage for each technology. The results will allow leaders in SPM function to cut through vendor hype to determine which technologies to invest in and when, to remain competitive among peers.

Methodology Statement: C-24337 Gartner Technology Adoption Roadmap for Large Enterprises for 2025 Survey

Gartner Technology Adoption Roadmap for Large Enterprises for 2025 Survey. This survey harnesses the collective wisdom of IT leaders to understand deployment plans, adoption timelines, value and risks of more than 200 technologies across infrastructure and operations; data and analytics; software engineering; cybersecurity; and strategic portfolio management. The survey was conducted through an online panel from August through October 2024 among 569 respondents from North America, EMEA and Asia/Pacific across industries in enterprises with annual revenue of more than $1 billion. Qualified respondents were CxOs, senior IT leaders, their peers and their direct reports. This research summarizes findings from 125 respondents identified as I&O leaders. I&O leaders indicate their enterprise’s current adoption plan for each technology across the following stages: not monitoring, monitoring, planning, piloting, in deployment and already deployed. These results are aggregated to determine a final adoption stage for each technology. The results will allow leaders in infrastructure and operations to cut through vendor hype to determine which technologies to invest in and when, to remain competitive among peers.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.