Magic Quadrant for Digital Employee Experience Management Tools

ARCHIVED

26 May 2025 - ID G00822534 - 55 min readBy Dan Wilson, Stuart Downes, and 1 more

The ability to measure and continually improve the digital employee experience using technology, employee sentiment and organizational data is critical for a thriving digital workplace. This research helps IT leaders responsible for DEX select the right tool vendor.

Strategic Planning Assumptions

Through 2027, 80% of digital employee experience management (DEX) tool deployments that account for only IT-focused use cases will fail to achieve a sustainable ROI.

Through 2027, 75% of organizations without a DEX strategy and tool will fail to successfully reduce digital friction.

Through 2028, IT executives will replace more than half of the end-user services leaders who fail to measurably improve the digital employee experience.

By 2028, digital workplace teams that have fully implemented a DEX tool will carry half the backlog of those that have not.

Market Definition/Description

Digital employee experience management tools measure and help IT continuously improve employee sentiment toward and the performance of company-provided technology. They continuously surface actionable insights, drive self-healing automations, and optimize support and employee engagement via the near-real-time processing of aggregated data from endpoints, applications, employee sentiment and organizational context. These insights enable self-healing and can enhance employee interactions with self-service portals and chatbots. They also help IT support, asset management, procurement and other teams whose work depends on reliable information.

DEX tools help IT improve the digital employee experience by quickly identifying and remediating technology issues. Benefits for IT teams include greater visibility of device and application performance, reliability and usage; reduced overhead through automation; and improved endpoint configuration and patch compliance. Benefits for the workforce include reduced digital friction that impedes productivity, the ability to offer feedback, faster issue resolution, and rightsized virtual and physical endpoints with optimized life spans.

Common use cases include:

- Discovering and remediating configuration drift from company, vertical industry or regulatory standards

- Measuring and improving application adoption and reliability

- Improving sustainability and reducing spend by transitioning from scheduled to performance-based refresh cycles

- Reducing security risk and improving patching compliance by identifying and remediating the cause of missing patches, which endpoint management or patching tools often cannot identify or self-heal

- Ensuring readiness for OS upgrades inclusive of reliability, capacity, performance, configuration and requirements checks

- Establishing digital personas based on technology usage data to create technology bundles, simplifying and accelerating employee onboarding

Mandatory Features

Tools in this market must offer:

- Native data collection through a Windows and macOS agent, and APIs to import data from other IT management tools and data sources.

- Imported organizational context data from IT directory services or HR systems.

- Turnkey integration with IT service management (ITSM) platforms for service desk and ITSM process enhancements.

- Bidirectional employee engagement, which includes the ability to collect employee sentiment and feedback, and the ability to communicate with employees through agent-based pop-up or toast notifications, email, mobile device apps, or integration with collaboration tools.

- Analysis to derive actionable insights, which includes device and application usage and performance, anomaly detection, root cause analysis, and a DEX or health score.

- Ability to act on insights by executing scripts or self-healing automations, or by communicating with employees. The vendor also must provide a library of predefined scripts or automations and a workflow orchestration engine to enable customers to build their own automations.

Optional Features

Tools in this market may include:

- Data collection for mobile, Linux or Google ChromeOS devices, and support for additional workloads, such as:

- Virtual experience management through turnkey integrations with virtual desktop infrastructure (VDI) and desktop as a service (DaaS) environments. This includes session details from the virtual desktop, endpoint device, remote connection protocol and connection path.

- Application experience management for locally installed applications via a software agent and web/SaaS applications through a browser extension, turnkey or API integration.

- Unified communications (UC) experience management via turnkey or API integration and includes ingest session, meeting, call and/or interaction metrics.

- Mobile experience management via native capabilities, as well as turnkey or API integration with endpoint management or mobile monitoring tools.

- Enhanced employee engagement with advanced surveys that can be triggered by the employee, events or time. This includes question branching; AI-based sentiment analysis of written text; and advanced outbound communications to mobile devices, with native digital adoption platforms (DAP) capabilities or turnkey integration with third-party DAP.

- Advanced analysis to derive actionable insights that may include persona-based DEX scores or the ability to calculate an employee’s DEX score across multiple devices, virtual desktops and applications. AI/ML-based correlation and causation analysis helps with issue prioritization. Endpoint device life cycles can be managed based on performance, usage and predictive failure analytics, instead of age and warranty status. Digital personas can be defined to help align technology needs to employee segments and can be monitored as needs change. Unused, obsolete or rogue software can be identified and removed. OS upgrade compatibility and readiness can be assessed and managed. Configuration drift can be identified and remediated. Organizational sustainability goals can be supported by monitoring power consumption, configuring power savings features and engaging employees to promote better habits.

- Advanced integrations with IT service portals and chatbots for improved self-service. Single sign-on (SSO) integration and role-based access control (RBAC) optimizes access for various groups that use DEX tools. Reporting data can be exported to business intelligence (BI) or other reporting and data analytics platforms. Unified observability can be achieved through integration with other monitoring and observability tools. Improvements to asset tracking and desired state can be accomplished through asset and configuration management tool integrations. DEX tools can support organizational environmental, social and governance (ESG) strategies by estimating power consumption and enabling device life span extension initiatives, and offer integration with ESG management and reporting software.

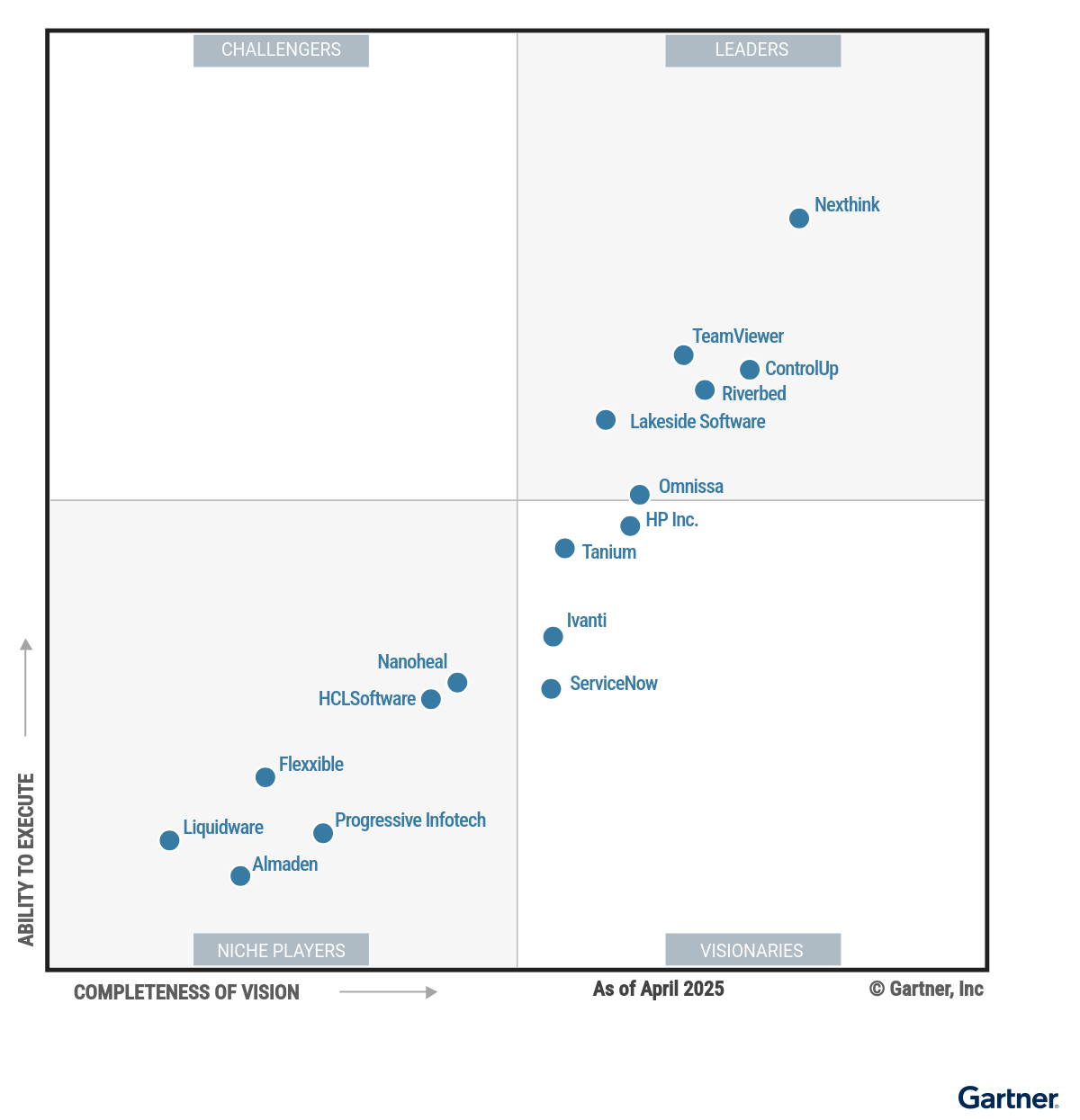

Magic Quadrant

Vendor Strengths and Cautions

Almaden

Almaden is a Niche Player in this Magic Quadrant. Its Collective IQ (CIQ) product is sold as a SaaS offering, hosted in Amazon Web Services. Almaden’s operations are based in the U.S., the U.K. and Brazil. It sells to enterprise customers, primarily in South America. Almaden is privately owned.

OS support includes Windows, macOS, Linux and thin clients. DEX for UC is available for Microsoft Teams. DEX for applications is limited to local PC apps. DEX for virtualization and web/SaaS apps, mobile devices, and turnkey ITSM integration is not available. Almaden does not provide a library of remediations, but customers can self-create with the virtual assistant and low-code workflow.

- Sales strategy: Almaden’s value proposition promotes rapid ROI for IT service desks by enabling and promoting employee self-service, automating repetitive IT work, and reducing tickets. CIQ has simple bundling, with Essentials and Business editions, and is less expensive than other products in this market. Almaden offers discounting that aligns with budgets of small to enterprise customers, resellers and managed service providers (MSPs).

- Overall viability: Almaden is privately owned and founder-led. It has demonstrated consistent double-digit revenue growth over the last two years. Company leadership is stable, with most leaders having been with the company since it was founded.

- Innovation: Almaden’s CIQ Business Edition is an AI-first product that leverages GenAI to identify predictors of experience, improve insights and enable IT administrators to interact with the product. AI is also leveraged for DEX scoring. The product leverages OpenAI’s ChatGPT using a point-and-click paradigm for ease of use. Customers that have a ChatGPT Business license can use that with the Almaden virtual assistant.

- Customer experience: Almaden’s customer success approach is nascent, compared to competitors that have more formal programs. Gartner was unable to find any customer case studies on its website or reference to Almaden CIQ in client interactions.

- Vertical industry strategy: Though Almaden has recently created a separate public-sector sales team, it does not differentiate its product or marketing strategy based on industry verticals. This may limit its ability to be successful within markets that have specialized regulatory or security requirements.

- Marketing execution: Almaden has little brand awareness in the DEX tools market. It was not mentioned by vendors in this report as a top competitor. Its limited marketing efforts are focused on its website, social media and participation in partner events.

ControlUp

ControlUp is a Leader in this Magic Quadrant. ControlUp ONE Platform is sold as a SaaS offering, hosted in Microsoft Azure and Amazon Web Services. Its operations are based in the U.S., Europe and Israel. The company sells to customers of all sizes. ControlUp is a venture-backed, privately held company.

OS support includes Windows, macOS, Linux, Google ChromeOS and most thin clients. ControlUp offers DEX for all major virtualization environments and applications, as well as Microsoft Teams and Zoom for UC. ControlUp also integrates with ServiceNow for ITSM and several endpoint management and security tools. ControlUp provides remediations, and customers can create their own using a recently enhanced low-code workflow orchestration.

- Product strategy: ControlUp continues to expand capabilities and consolidate its offerings into a platform that extends historically strong virtualization experience management to endpoints, applications, UC and security experience. It recently added support for Microsoft Windows 365 and ChromeOS. The company also launched Workflows, a low-code workflow orchestration solution from its acquisition of Takoto, and ControlUp for Apps, which now includes real-user monitoring (RUM) via its acquisition of Avanite.

- Sales strategy: The company recently simplified its packaging under the complete ControlUp ONE Platform and ControlUp for Desktops (Essential and Advanced), ControlUp for VDI (Essential and Advanced), ControlUp for Apps, and ControlUp for Compliance bundles. ControlUp aggressively prices its solution below market average, with higher discounts for larger bundles and multiyear commitments. Custom enterprise licensing agreements are available for large customers. Pricing is also available for MSPs.

- Innovation: ControlUp demonstrates innovation via partnerships, acquisitions and product development. In addition to the new and enhanced products cited above, the company has increased its use of AI and machine learning (ML). The vendor remains focused on simplifying IT work via tool consolidation and expanded offerings for application management, employee enablement, autonomous endpoint management (AEM), and mobile and Internet of Things (IoT) use cases.

- Vertical industry strategy: Although ControlUp has customers in all defined vertical industries, it has little product or sales strategy differentiation for industry verticals. This was not improved in 2024, which may limit growth in verticals with special regulatory or security requirements.

- Marketing execution: ControlUp focuses on strengths in virtualization and IT operations, such as faster troubleshooting, automation and optimization. This focus might limit its perceived broader platform scope, which could explain why Gartner clients are less aware of its nonvirtualization use cases.

- Geographic strategy: ControlUp is less focused on international growth than some competitors and has not developed a comprehensive, geographic go-to-market strategy. The company’s geographic efforts are limited to event-based engagement and marketing across North America, Europe, the Middle East and Asia/Pacific, and rely heavily on technology and channel partners.

Flexxible

Flexxible is a Niche Player in this Magic Quadrant. Its FlexxClient is available as a SaaS offering, hosted in Microsoft Azure. Flexxible’s operations span Europe, the U.S., Brazil and India. The company sells to midmarket and enterprise customers in the Americas and Europe. Flexxible is privately owned and led.

OS support includes Windows, macOS, Android, Linux and ChromeOS. DEX is offered for all major virtualization environments but not applications or UC. ITSM integration is available for ServiceNow, as are integrations with endpoint security tools. Flexxible provides remediations, and customers can create their own using low-code workflow orchestration.

- Sales strategy: Flexxible lowered prices to make FlexxClient more affordable than most competitors and repackaged the offering to enable customers to start small and expand. The FlexxClient Core package provides remote control, basic automation and monitoring. The FlexxClient Advanced package adds advanced autoremediation. The FlexxClient Transform package adds advanced customer success and DEX management.

- Geographic strategy: Flexxible has employees and support centers in all regions where it has customers. It demonstrates the awareness required to tailor its product, marketing, sales and customer engagement strategies by geography. Being hosted in Microsoft Azure offers broad geographic coverage as well.

- Product strategy: Flexxible provides automation and management of the workspace experience, where a workspace can be a physical device or a virtual desktop. Its product strategy focuses more holistically on improving software asset management (SAM), IT support, compliance, sustainable IT reporting, and alerting, in addition to DEX.

- Market responsiveness: FlexxClient has limited tenure in the DEX market and is less mature in breadth and depth of features and integrations than most competitors. The company delivered some but not all 2024 roadmap items, and analysis showed misalignment between its top three roadmap items for 2025 and the top three things its customers are asking for. Limited use of and focus on AI/ML will limit the vendor’s ability to compete in a market being transformed by AI.

- Marketing execution: Flexxible has little brand awareness in the DEX tools market. It was not mentioned by vendors in this report as a top competitor.

- Vertical industry strategy: Flexxible does not differentiate go-to-market strategies for vertical markets, but is planning to test this later in 2025. Its current strategy is limited to use of industry-specific language in messaging.

HCLSoftware

HCLSoftware is a Niche Player in this Magic Quadrant. HCL BigFix Workspace includes on-premises or self-hosted offerings. HCLSoftware’s operations and enterprise customers are globally distributed. It is a division of publicly traded HCLTech.

The HCL BigFix client supports most OSs, but its DEX capabilities are limited to Windows and macOS in BigFix 11 or higher environments. ITSM integration with ServiceNow is available, as are endpoint management and security tool integrations. Turnkey DEX for virtualization, applications and UC is not available, but can be built using APIs. HCL BigFix provides an extensive library of Fixlet remediations and allows customers to build their own.

- Sales strategy: DEX capabilities are included at no cost for customers that have active maintenance or subscription licensing to HCL BigFix Workspace. Once upgraded to HCL BigFix 11, customers will see the new DEX features. Those looking for the AI-enhanced capabilities of HCL BigFix AEX will need to upgrade to the HCL BigFix Workspace+ license.

- Geographic strategy: HCLSoftware has staff in all geographic regions except China, and partners to fill gaps in supporting its globally distributed customer base. DEX capabilities can be added for global customers already using HCL BigFix, enabling them to manage endpoints, servers, applications and containers. HCLSoftware’s customer support services are globally distributed and centrally managed.

- Operations: HCLSoftware has a large network of technology integration, manufacturer, reseller and systems integrator partners to help scale. It leans on its large community of certified BigFix professionals for peer support, product awareness and execution.

- Customer experience: Analysis revealed little evidence of DEX-related customer case studies, few customer reviews on Gartner Peer Insights and similar sources, and low customer awareness of HCL BigFix as a DEX tool.

- Sales execution: HCLSoftware reported increased sales, but was unable to demonstrate growth in adoption of its DEX tool, due to limited telemetry from on-premises implementations. HCL BigFix was not cited as a top competitor by any other vendors in this research. Pricing for non-BigFix customers is higher than the market average.

- Product: HCLSoftware has improved its DEX tool in the last year; however, it is less mature in breadth and depth of features and integrations than most competitors and demonstrates little differentiation from competing offerings. Functionality is focused primarily on extending and automating endpoint management efforts, which aligns to lower-maturity IT organizations that have not yet fully embraced human-centric DEX strategies.

HP Inc.

HP Inc. is a Visionary in this Magic Quadrant. Its Workforce Experience Platform (WXP) is sold as SaaS, hosted in Amazon Web Services. The publicly traded company’s operations and enterprise customers are globally distributed.

OS support includes Windows, macOS and Android. WXP imports iOS, iPadOS, ChromeOS and printer data from turnkey integrations. WXP integrates with ServiceNow for ITSM, but not self-service portals or chatbots. DEX for virtualization is limited to HP Anyware and agents on persistent desktops. DEX for web/SaaS applications is available. UC is available via acquired Vyopta. WXP offers a library of remediations and enables customers to deploy their own scripts.

- Sales strategy: WXP’s packaging is simple, with one SKU. Pricing is more affordable than many competitors, with additional discounts available for larger and longer-term deals, and for MSPs and global systems integrators (GSIs). WXP is included at no additional cost within the company’s managed device life cycle services deals and for HP Proactive Insights customers.

- Geographic strategy: HP Inc. has staff in all geographic regions and partners that fill staff gaps to support a globally distributed customer base. The company has a proven track record of success in the global marketplace and demonstrates a deep awareness of geographic regional differences by tailoring its DEX tool’s product, sales, customer and marketing strategies accordingly.

- Overall viability: HP Inc. is profitable and has over a thousand resources developing WXP as a successor to Proactive Insights. Stable executive and product leadership have built a solid roadmap, established a steady cadence of updates, and assembled a broad network of partners that include technology integrations, hardware manufacturers, resellers, systems integrators and some DEX tool competition.

- Marketing execution: Despite increased event participation and a stand-alone website, HP’s WXP is still a lesser-known brand in the DEX market. The company was not mentioned by vendors in this report as a top competitor and ranked lower among competitor mentions within reviews on Gartner Peer Insights and similar sources.

- Market responsiveness: WXP has been generally available for less than a year and is less mature in breadth and depth of features and integrations than leading competition. WXP’s product roadmap addresses the top three things its customers are asking for, but HP Inc. needs to demonstrate a sustained, consistent ability to deliver over time.

- Sales execution: Due to WXP’s short tenure, there is insufficient evidence of HP Inc. demonstrating sustained growth. The company has not yet amassed an installed base comparable to leading competition. Gartner has yet to see clients migrating to WXP from another DEX tool.

Ivanti

Ivanti is a Visionary in this Magic Quadrant. Ivanti Neurons for Digital Experience is sold as a SaaS offering, hosted in Microsoft Azure. Its operations and customers are globally distributed. Ivanti is private-equity-owned.

OS support includes Windows, macOS and Linux. Mobile data is imported from turnkey integrations. ITSM integration is offered for Ivanti Neurons and ServiceNow ITSM. DEX for applications and UC for Microsoft Teams are also available. Virtualization is limited to agents installed on virtual desktops. Ivanti also provides remediation bots, and customers can create their own using low-code workflow orchestration.

- Geographic strategy: Ivanti has staff in all geographic regions, in addition to partners that support its globally distributed customers. The company tailors its DEX tool’s product, sales, customers and marketing strategies accordingly. The Neurons platform is hosted in Microsoft Azure, which also provides broad geographic coverage.

- Market understanding: Ivanti brings a unique perspective to the market by converging DEX with IT service management, as well as endpoint management, discovery and security. The vendor’s self-healing and automation bot framework is also unique. Ivanti has a solid understanding of DEX tools’ market positioning, opportunities and challenges for clients of all sizes.

- Innovation: The Ivanti Neurons platform uses AI/ML to drive intelligence and automation across DEX, endpoint discovery, management and security, and IT service and asset management use cases. The Neurons platform continues to evolve and expand to address buyer needs.

- Sales execution: Ivanti has fewer actively deployed DEX agents and lower annual growth of its installed base than the majority of the vendors in this market. Its licensing fees do not include additional items like training, implementation, customer success and premium support included by some competitors. Ivanti is rarely mentioned by vendors in this report as a top DEX competitor or by Gartner clients during inquiry.

- Customer experience: Analysis revealed little evidence of DEX-related customer case studies, limited customer reviews on Gartner Peer Insights and similar sources, and little awareness of Ivanti’s DEX tool offering beyond current Neurons customers. The company also charges extra for customer success services, instead of including that in base prices.

- Operations: Significant changes in company leadership, including appointment of a new chief executive officer and chief product officer, could cause DEX to be deprioritized in favor of products with higher returns or strategic value. Ivanti’s smaller installed base and market share contributes less to overall company revenue than leading competition.

Lakeside Software

Lakeside Software is a Leader in this Magic Quadrant. SysTrack is sold primarily as a SaaS offering, hosted in Microsoft Azure. Lakeside’s operations span the U.S., Europe and Asia/Pacific. The vendor sells to global enterprise customers. Lakeside is private-equity-owned.

OS support includes all major operating systems, devices and thin clients. SysTrack integrates with several chatbots, ServiceNow for ITSM, Qualtrics for experience management and Splunk for observability. Lakeside offers DEX for all major virtualization environments, applications and UC solutions. The vendor provides a library of remediations, and customers can create their own using low-code workflow orchestration.

- Customer experience: Lakeside customers speak positively about SysTrack’s existing Black Box data collection and retention capabilities, and how that contributes to root cause analysis. Customer success services are included in base license costs. The vendor hosts frequent office hour sessions and publishes success blueprints to improve awareness and use of SysTrack.

- Market responsiveness: Lakeside is one of the longest-tenured vendors assessed in this market. SysTrack’s value proposition is well-aligned to customers’ needs, and the volume and frequency of data collected enhance the vendor’s development, marketing and sales.

- Vertical industry strategy: Lakeside has customers in most industry verticals and targets other verticals through partners and by participating in special events and producing unique content. The vendor is working to obtain certifications to extend its SaaS offering to government and highly regulated verticals.

- Sales execution: Lakeside has a smaller installed base than some competitors in this Magic Quadrant. The company did not disclose growth metrics, but Gartner estimates that it underperformed, compared with average market growth. SysTrack has several packages and licensing options on a per-user and per-device basis. Clients should consider which best fits their needs to prevent compliance concerns.

- Product strategy: In 2024, Lakeside’s feature delivery did not always match the highest priorities of Gartner clients. For 2025, the company has revised its roadmap to include top customer requests, including additional AI capabilities and expanded proactive IT tools. With quarterly major releases, Lakeside also follows a slower cadence than most competitors.

- Geographic strategy: Lakeside is the smallest company in the Leaders quadrant, which raises concerns about its ability to scale globally as successfully as the competition. With most of its staff in North America and Europe, Lakeside has a greater dependency on partners to cover other regions.

Liquidware

Liquidware is a Niche Player in this Magic Quadrant. Its Stratusphere UX Plus bundle includes on-premises or cloud-hosted Stratusphere UX and SaaS-hosted CommandCTRL in Google Cloud. Liquidware’s operations and enterprise customers span the U.S., Europe and Asia/Pacific.

OS support includes Windows, macOS, Linux and thin clients. Turnkey ITSM integration is not offered, but ServiceNow for ITAM integration is. Stratusphere API Builder enables custom integrations. DEX for all virtualization environments is available, but application and UC experiences are limited to monitoring endpoint applications. Liquidware offers a library of remediations, but not low-code workflow orchestration.

- Vertical industry strategy: Liquidware’s vertical strategy is demonstrated by a distinct go-to-market and web presence for several verticals that are not addressed by competitors. The company emphasizes healthcare, pharmaceuticals, government, education and financial services in its marketing, and has customers in many of the major vertical industries.

- Marketing execution: Liquidware has established a strong brand and mind share within the end-user computing technology community and often participates in industry events and conferences. The company produces webinars, videos and podcasts that increase customer awareness of products and engage with industry experts and thought leaders.

- Customer experience: Liquidware has received positive customer reviews for its high-touch, highly technical support services. Customers also like that added capabilities extend beyond virtualization optimization and endpoint management into DEX. Customer awareness and utilization of the vendor’s products and customer relationships are also bolstered by its event participation and community involvement.

- Product strategy: Liquidware does not offer comprehensive DEX for UC and applications, low-code workflow orchestration, and/or turnkey ITSM integrations, but does provide an API Builder to address specific needs. Liquidware’s annual release cadence is slower than competitors; however, it does provide optional updates for specific customers or use cases as required, which may include new features. Clients should validate Liquidware’s roadmaps and monitor progress to address requirements.

- Product: During the analysis period (May 2024 to February 2025), Liquidware did not release updates for Stratusphere UX, which has feature gaps compared to competitors. Liquidware released a CommandCTRL update in June 2024, which included on-demand licensing, Windows logs exporting and customizable thresholds.

- Business model: Despite the significant contribution of Liquidware’s DEX tool to company revenue, it has the fewest allocated resources in this research. Without additional investment and accelerated product development, the company will likely struggle to close product gaps.

Nanoheal

Nanoheal is a Niche Player in this Magic Quadrant. Nanoheal is sold as an on-premises or SaaS offering hosted in Amazon Web Services, Microsoft Azure or Google Cloud. Its operations are U.S.- and India-based. The vendor sells to MSPs, GSIs and resellers. Nanoheal is founder-owned and led.

OS support includes Windows, macOS, Linux, iOS, iPadOS, Android and ChromeOS. Nanoheal offers ServiceNow ITSM integration. DEX for all major UC solutions, virtualization environments and application types is available. Nanoheal provides remediations and enables customers to create their own, using low-code workflow orchestration.

- Sales strategy: Nanoheal’s packaging for MSPs and IT organizations is simple to understand, with one SKU and a few add-ons. Its pricing is not publicly disclosed, but is among the lowest of vendors in this research.

- Innovation: Nanoheal made significant improvements in 2024 with the use of AI/ML within the platform for anomaly detection, behavioral analytics, sentiment analysis and scoring functionality. The Nanoheal AI engine is opt-in, with basic functionality offered at no additional cost. However, advanced AI analytics do require an add-on license. The company also demonstrated a beta of its GenAI assistant for DEX and other use cases that are planned for release in mid-2025.

- Market responsiveness: Nanoheal remains focused on improving DEX and optimizing endpoint operations through no-code automation. This aligns well with the needs of its target buyers (MSPs and GSIs) who want to improve the scale of their service offerings. The company’s roadmap addresses common customer requests to integrate GenAI and sustainability reporting tools, and to add support for nontraditional endpoint devices, such as workplace IoT.

- Marketing strategy: Nanoheal does not prioritize marketing to end-user customers. Its primary go-to-market routes are through MSPs, GSIs and other partners. The vendor’s marketing strategy is limited to attending other companies’ conferences, occasionally hosting webinars and user groups, and distributing newsletters to customers and partners.

- Marketing execution: Nanoheal has built little brand awareness in the DEX tools market. It is rarely mentioned by vendors in this report as a top competitor or by Gartner clients during inquiry, and was absent in customer reviews. It has little content on its website, and all video channels and social media accounts are inactive. Nanoheal did not execute any major marketing campaigns in the last year.

- Customer experience: Analysis revealed no evidence of DEX-related customer case studies, limited customer reviews on Gartner Peer Insights and similar sources, and little awareness of Nanoheal outside of its partners and current customers. Basic customer success is available at no additional cost, but the small size of the company limits the scale and effectiveness, unless delivered primarily by partners.

Nexthink

Nexthink is a Leader in this Magic Quadrant. Nexthink Infinity is sold as a SaaS offering, hosted in Amazon Web Services. Nexthink’s operations and enterprise customers are globally distributed. Nexthink is founder-led and privately owned.

OS support includes Windows, macOS, and thin clients from IGEL and Dell Technologies. Nexthink provides DEX for all major virtualization environments, applications, and Microsoft Teams and Zoom UC. Nexthink Amplify integrates with ITSM and ITAM tools. Nexthink also integrates with several chatbots, Qualtrics for experience management, and Splunk and other observability tools. The vendor provides remediations and enables self-created remediations using Nexthink Flow.

- Market responsiveness: Nexthink was among the first to integrate with ServiceNow, Qualtrics, Moveworks and others to extend its offering. The company recently added VDI Experience to expand virtualization support, and Adopt, the new name for acquired and integrated AppLearn, which extends into the digital adoption platform (DAP) market. When generally available, Nexthink Autopilot will provide agentic AI analysis and automated remediation.

- Marketing: Nexthink attracts the most Gartner client and competitor mentions. Nexthink leverages many marketing channels to reach customers, prospects and partners. It demonstrates thought leadership with its DEX Show podcast, DEX Hub website, Experience conferences and survey-based reports.

- Product: The Infinity platform is highly extensible and scalable, supporting over 1 million endpoints per customer and data residency wherever Amazon has data centers. Nexthink continues to deliver two new modules and new partner integrations per year, in addition to new capabilities and items to the Nexthink Library, and additional connectors to Nexthink Flow each month.

- Sales strategy: Nexthink’s complete bundle costs more than most other DEX tools. Customers report having difficulty understanding the vendor’s complex a la carte options. Nexthink does not offer lower-cost entry point packages. It sells primarily to enterprise organizations, so customers with under 5,000 endpoints usually have to go through resellers or partners.

- Vertical industry strategy: Nexthink has limited differentiation of its product, marketing and sales strategy based on industry verticals. Organizations should align vertical requirements for configuration and accreditation during planning and deployment phases.

- Product strategy: Nexthink has less endpoint diversity than some competitors, focusing primarily on Windows and macOS. Mobile device support is limited to basic device inventory ingested from the Collaboration Experience product.

Omnissa

Omnissa is a Leader in this Magic Quadrant. Its Workspace ONE Experience Management is sold as a SaaS offering hosted in Amazon Web Services. Omnissa’s operations and customers are globally distributed. Omnissa is private-equity-owned.

Workspace ONE’s OS support includes all major operating systems, devices and thin clients. Omnissa offers DEX for all major virtualization environments, applications and UC solutions. ITSM integrations are available for ServiceNow, TOPdesk, BMC and Atlassian. Chatbot integrations are available for Moveworks and Slack. Omnissa provides remediations and enables customers to create their own using Freestyle Orchestrator.

- Innovation: Omnissa demonstrated effective use of its GenAI-enabled Omni AI Assistant and the ability to deliver an autonomous future for endpoint and experience management. New and expanded partner integrations include CrowdStrike, IGEL, Intel, Zebra, Microsoft and Apple.

- Product: The vendor’s DEX tool integrates seamlessly with Workspace ONE Unified Endpoint Management (UEM) and Assist, as well as Omnissa Access, Freestyle Orchestrator and Horizon. It is highly extensible, with integrations to third-party products such as ServiceNow, Moveworks, TOPdesk, CrowdStrike and more. The solution supports all primary enterprise workloads, endpoints and device types, and is highly scalable due to its microservices architecture that supports over 1 million devices within a customer environment.

- Geographic strategy: Omnissa has a globally distributed staff and partners in all regions where it has major customers. Its platform can scale globally, to wherever Amazon has data centers. This includes local data residency. The company tailors its go-to-market strategy by region for all of its products.

- Customer experience: Analysis revealed no evidence of DEX-related customer case studies, few mentions of DEX on the vendor’s new website, and below-average ratings on Gartner Peer Insights and similar sources. Customer success services are included at no additional cost, but are limited to key or focused accounts. Omnissa faces some lingering concerns related to its spin-off into a separate company. Some Gartner clients are still unaware of these transactions.

- Sales execution: Omnissa demonstrated positive DEX installed base growth in 2024, following a decline in 2023. Growth will need to continue through 2025 to be considered sustained. Gartner has not heard of clients leaving other DEX tools for Omnissa. Only one other vendor in this report mentioned Omnissa as a top DEX competitor.

- Marketing execution: Since becoming a stand-alone company, the company has yet to effectively address what Omnissa is and how it positions itself in the DEX tools market, resulting in little overall awareness. The company earned few mentions by vendors in this report as a top competitor and ranked in the bottom half of customer mentions in Gartner Peer Insights and similar sources.

Progressive Infotech

Progressive Infotech is a Niche Player in this Magic Quadrant. Its Workelevate platform is sold as a SaaS offering, hosted in Microsoft Azure, on-premises or cloud-hosted. Its operations are based in India. The company sells to midmarket to enterprise customers. Workelevate is a subsidiary of Progressive Infotech and is founder-owned and led.

OS support includes Windows, macOS and Linux. Workelevate can build DEX integrations per customer for on-premises Citrix and Microsoft virtual environments, but does not offer DEX for applications or UC. Workelevate integrates with many ITSM, UEM and observability tools. It provides remediations and enables customers to code their own.

- Innovation: Workelevate leverages AI/ML for predictive analytics, sentiment analysis, anomaly detection and automated remediation. The vendor uses GenAI for its custom-built chatbot that can also integrate other large language models. The vendor’s roadmap includes enhancements to its AI capabilities to increase employee engagement, well-being and retention, and address security use cases.

- Sales strategy: Workelevate’s packaging is simple, with one SKU that includes its AI Copilot and endpoint management capabilities. Base pricing is among the lowest in the market, and discounts are available for larger or longer-term deals. Add-ons are available for IT asset and OS patch management, as well as AI for IT service management capabilities. Administrator training is available at no additional cost.

- Vertical industry strategy: Workelevate’s product, marketing and customer strategies are tailored to many vertical industries. The product provides regulated industries with on-premises deployment to meet compliance and data security requirements. Customers with large frontline workforces can leverage SaaS offerings that integrate with workstream collaboration and communication tools, and help automate on/offboarding tasks.

- Marketing execution: Workelevate has built little brand awareness in the DEX tools market. It was not mentioned by vendors in this report as a top competitor, by Gartner clients during inquiry, or as an alternative solution considered by reviewers on Gartner Peer Insights. DEX-related content was found on its website and blog, but it is more educational than thought-leading.

- Operations: Workelevate has one of the smallest teams working on DEX among vendors in this market. It is now a separate business unit that is not profitable on its own. More than half of customers are operating on-premises-hosted solutions, which increases support and life cycle management efforts. All staff are based in India, which limits regional expansion.

- Sales execution: Despite reporting significant growth in 2024, Workelevate ranks near the bottom of vendors in this research in terms of market share and size of installed base. Sales are made primarily through resellers and partners. Direct sales are focused on midmarket to enterprise customers in India and surrounding regions.

Riverbed

Riverbed is a Leader in this Magic Quadrant. Riverbed Aternity is sold primarily as a SaaS offering, hosted in Amazon Web Services or Microsoft Azure. Its operations and customers are globally distributed. Riverbed is private-equity-owned.

OS support includes all major operating systems and devices. Riverbed offers DEX for all virtualization environments, applications and UC solutions. Aternity directly integrates with ServiceNow for ITSM, Intel for deeper visibility and Tableau for reporting, as well as endpoint management and observability tools. Riverbed provides a library of remediations, and customers can create no-code remediations and runbooks using Intelligent Service Desk.

- Market responsiveness: Riverbed has significant tenure in the DEX tools market and has improved Aternity’s maturity in 2024. It has a unified agent and data platform, which simplifies the addition of new capabilities. Aternity Mobile has attracted attention as the market’s only mobile DEX offering. In addition, deeper integration with Intel enables Thunderbolt and Wi-Fi connectivity analytics.

- Market understanding: Riverbed’s market value proposition is centered around a platform strategy that offers broader management of mobile, network, infrastructure, UC and application experience. For diverse environments, Riverbed’s use of OpenTelemetry (OTel) ensures extensibility for non-DEX buyers. The vendor’s roadmap addresses the top three things that its customers are asking for.

- Business model: Riverbed is profitable and has demonstrated sustained growth in the last two years. In 2024, accelerated product feature expansion and platform integration drove above-market-average revenue growth. The vendor delivers capabilities to address the needs of multiple IT buyers from a single platform and agent.

- Marketing execution: Gartner clients seeking a DEX tool may overlook Riverbed. This is because the vendor’s platform-based messaging focuses on broader capabilities that span several adjacent markets, and targets existing customers and prospects at varying maturity levels. The company produced fewer DEX-related, thought-leading reports than in prior periods.

- Customer experience: Customer success services are available at no additional cost, but are limited to target accounts. Administrator training is available at no additional cost but is limited to the basic-level Aternity Core. Advanced training will not be available until later in 2025.

- Sales: Riverbed’s list pricing is higher than most other DEX tool vendors. The company’s installed base grew at a slower rate than leading competitors in 2024. Gartner has seen a slight, recent increase in clients renewing and extending use of Aternity, but not as a replacement for other DEX tools. Selling a broader platform vision is more difficult, given that multiple target roles often have competing priorities within enterprise IT organizations.

ServiceNow

ServiceNow is a Visionary in this Magic Quadrant. ServiceNow Digital End-User Experience (DEX) is sold as a SaaS offering, hosted on its own Now Platform. ServiceNow’s operations and enterprise customers are globally distributed. ServiceNow is a public company.

OS support includes Windows and macOS. ServiceNow DEX fully integrates with all of the company’s other offerings, which include ITSM and ITAM. DEX for UC solutions is not available. Virtualization support is limited to agents installed on persistent desktops. Application experience includes locally installed PC apps and web/SaaS via a browser extension. ServiceNow provides remediations and enables customers to create their own.

- Geographic strategy: ServiceNow tailors its go-to-market strategy to geographic regions. ServiceNow DEX allows customers to choose data residency locations. The company runs a global Knowledge conference and then hosts smaller regional World Forums.

- Vertical industry strategy: ServiceNow tailors product, marketing and customer strategies for most vertical industries. It also has vertical-specific products for healthcare, financial services, public sector, manufacturing, retail, technology and more. Some regulated industries may obtain special approval for private or sovereign cloud deployments to meet compliance and data security requirements.

- Innovation: ServiceNow’s vision of putting AI to work for people aligns with buyer needs in the DEX tools market. While the vendor’s DEX tool is new, its key differentiation is being built on a platform that already supports IT services and processes, and has demonstrated extensibility. Recently released AI agents are likely to extend to DEX and be a differentiator in the near future, due to having access to more data across the platform.

- Customer experience: Analysis revealed no evidence of DEX-related customer case studies or customer ratings on Gartner Peer Insights and similar sources. ServiceNow offers customer success services, but at an additional cost.

- Marketing execution: ServiceNow has made progress with product capabilities and sales in its short tenure, but buyers are less aware of ServiceNow DEX than other vendors’ DEX tools. The vendor was not mentioned by other vendors in this report as a top competitor. DEX-related marketing execution has been limited and focused on building awareness of the product and its features, with little thought leadership.

- Product: ServiceNow DEX has improved since becoming generally available in May 2024. The product is less mature than other DEX tools in this research. It is missing turnkey support for UC solutions and virtualization support is limited to agents installed on persistent desktops.

Tanium

Tanium is a Visionary in this Magic Quadrant. Tanium DEX is sold as an on-premises or SaaS offering, hosted in Amazon Web Services, Microsoft Azure or Oracle Cloud. Tanium’s operations and enterprise customers are globally distributed. Tanium is a private company.

OS support includes Windows and macOS. Turnkey integration is available for ServiceNow ITSM and ITAM. DEX for virtualization environments, UC solutions, web/SaaS applications and mobile devices is not available. Tanium provides remediations and enables customers to create their own using Tanium Automate, which is included at no additional cost.

- Market understanding: Tanium DEX is built directly into the company’s AEM platform, which aggregates and leverages technology configuration, performance, security risk, compliance, and experience data to autonomously execute core IT maintenance tasks, freeing up IT staff for more value-added work. Most items on the company’s roadmap are customer-requested, which demonstrates a pragmatic approach of not chasing the competition.

- Marketing strategy: Tanium broadly leverages all marketing channels, including an active blog, as well as social media, podcast and video channels. Tanium also hosts its own annual Converge conference and regional roadshows. These are backed by messaging that addresses what its primary buyers are seeking today and will need in the near future. The vendor’s DEX offering positioning is aligned with customers’ critical need of transparency into and management of DEX.

- Vertical industry strategy: Tanium has customers and go-to-market strategies in nearly all vertical industries. The company’s large partner network helps them address vertical-specific requirements and regulations. Tanium participates in vertical industry conferences and events, and collaborates with administrative bodies and government agencies.

- Sales execution: Tanium did not disclose the size of its active DEX installed base, but reported increased customer adoption compared to 2024. Tanium DEX was not cited as a top competitor by any other vendors in this research, and Gartner has not seen clients leaving another DEX tool for Tanium. Historically, non-Tanium customers needed to purchase licenses for Tanium’s Core and Performance modules, for which combined pricing was above market average. The announced Engage module’s consolidation into Core on 1 May 2025 removes that license requirement.

- Marketing execution: Buyers, even existing Tanium customers, are less aware of Tanium DEX than of other vendors’ DEX tools. The vendor has attracted few reviews in Gartner Peer Insights or similar sources. DEX-specific marketing execution is limited beyond product-specific videos and webinars.

- Product: Tanium DEX is less mature than other DEX tools in this research. It lacks turnkey support for virtualization environments, UC solutions and mobile devices. Current capabilities address the needs of IT operations and security buyers who are just starting their DEX journey.

TeamViewer

TeamViewer (which acquired 1E) is a Leader in this Magic Quadrant. TeamViewer DEX (formerly the 1E Platform) is sold primarily as a SaaS offering, hosted in Microsoft Azure. Its operations are segmented into European, North American and Asia/Pacific regions, supporting enterprise customers based primarily in North America and Europe. TeamViewer is a public company.

OS support includes Windows, macOS, IGEL OS and Linux. DEX for applications and virtualization environments is available natively. UC requires the Exoprise agent. TeamViewer offers ServiceNow and Atlassian Jira ITSM integration and a library of remediations, and customers can create their own using low-code workflow orchestration.

- Operations: TeamViewer adds to 1E’s partnerships and the combined company has significantly more staff to scale. Its elastic SaaS platform is highly extensible via DEX Packs, REST APIs and direct integrations with ServiceNow and others. It provides local data residency where Microsoft has Azure data centers.

- Sales strategy: Packaging includes three bundles of increasing capability and costs, several add-ons and solution packs, offering customers a lower-cost entry and the ability to expand features as they mature. The 1E acquisition creates opportunities to cross-sell DEX to TeamViewer’s existing customers. DEX annual revenue per opportunity is higher than existing revenue per customer, so go-to-market changes are required beyond TeamViewer’s recently announced DEX offering for smaller organizations.

- Market responsiveness: TeamViewer’s acquisition of 1E recognizes a shift to proactive operations enabled by analytics and automation. This complements the vendor’s previous endpoint management and remote support offerings. Prior to being acquired, 1E’s responsiveness was demonstrated by acquiring Exoprise to enhance its monitoring capability and establishing partnerships with B2M Solutions for frontline workers and Goliath Technologies for healthcare use cases.

- Vertical industry strategy: TeamViewer traditionally offered differentiated go-to-market for manufacturing, retail, healthcare, pharmaceutical and government verticals, while 1E did not differentiate by industry. A strategy transition is required for the company’s DEX offerings. More than half of the TeamViewer DEX installed base still operates within on-premises-hosted environments as the company obtains the necessary certifications for its SaaS platform to be used in highly regulated and federal government verticals.

- Product: TeamViewer is progressing through significant organizational and technology integration and migration efforts to bring together the employees, intellectual property, platforms and agents from Exoprise, 1E and TeamViewer. While this work is underway, the company could face unforeseen challenges when trying to combine three companies and technology platforms.

- Geographic strategy: Geographic expansion beyond North America and Europe was not a major focus for 1E preacquisition, but expansion is accelerating based on TeamViewer’s geographic footprint, which includes Asia/Pacific. Regional hosting for the platform is currently available only in North America and Europe at no additional cost.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

- ServiceNow

- TeamViewer (acquired 1E, which acquired Exoprise)

Dropped

- Access IT Automation, due to not offering a DEX agent for macOS.

Inclusion and Exclusion Criteria

The inclusion criteria represent the specific attributes that analysts believe are necessary for vendors to be in this Magic Quadrant. To qualify for inclusion, vendors must provide a solution that satisfies the following technical criteria:

1: A generally available, single-license SKU as of 12 August 2024 that includes all must-have functionality defined in the market definition and the following before the research cut-off date on 12 February 2025:

- A: Collection of data via an agent for Windows and macOS (browser extension or server-based agent does not meet the requirement).

- B. Collection of employee sentiment via surveys.

- C. Calculate, report and trend a DEX or health score on an endpoint or employee basis. At a minimum, the score must include endpoint, application and sentiment data.

- D. Analyze data and generate actionable insights on ways to improve DEX.

- E. Act on insights by executing vendor-provided or customer-developed scripts, self-healing automations, runbooks and workflows.

- F. Send outbound employee engagement messages, nudges or campaigns.

- G. Ingest organizational context data from directory services, SSO and/or an HR system.

- H. Integrate with or provide web-browser overlay for ITSM platforms to improve service desk support and self-service.

- I. Extensibility via webhooks and/or APIs to enable integrations with other services/tools.

2: The DEX tool must be purchasable as a stand-alone product and must not solely be sold or licensed as an add-on to another product.

3: Core DEX tool capabilities (see 1A through 1E above) must be the vendor’s own intellectual property and not dependent on third-party functionality, partnerships or a white-labeled product.

4: Rank in the top 15 vendors in Gartner’s Customer Interest Indicator (CII) compiled by Gartner Secondary Research Service for this market in January 2025.1

Honorable Mentions

Access IT Automation: Access IT Automation delivers tailored implementations of Access Symphony to meet each customer’s unique integration, reporting and workload requirements. This includes ITSM, HR and other integrations and workload support for physical and virtual endpoints, applications, and UC solutions. Access Symphony platform supports Windows and includes a library of self-healing remediations. Customers can also create their own using low-code workflow orchestration capabilities. The company operates the largest DEX tool implementations in the financial services vertical, supporting over 1 million endpoints. Access IT Automation did not meet the inclusion criteria for having a macOS agent. macOS support is in development.

eG Innovations: eG Innovations End-User Experience Monitoring (EUEM) supports Windows, macOS, ChromeOS, Linux and thin client endpoints. eG offers DEX for all virtualization environments, applications and popular UC solutions. Turnkey integrations are offered for more than 15 different ITSM platforms, and others can be set up using webhooks. Insights can be acted upon using scheduled and self-triggered automations and optimization scripts. Multitenancy is available for MSPs and GSIs. eG Innovations did not meet the inclusion criteria for collecting employee sentiment and sending outbound communications to employees.

Microsoft: Microsoft Intune Endpoint Analytics is included in all Intune licenses, and Advanced Analytics is available as an add-on or in the Intune Suite license. Both offer improved reporting, anomaly detection, insights and automation. DEX support for virtualization includes Windows 365 and Azure Virtual Desktop, and persistent virtual desktops enrolled into Intune. DEX support for applications and UC is not available. Turnkey ITSM integration with ServiceNow is offered. Microsoft did not meet the inclusion criteria for having a macOS agent, collecting employee sentiment and sending outbound communications to employees.

Zscaler: Zscaler Digital Experience (ZDX) is available as an add-on to the company’s zero-trust access solution in Standard, Advanced and Advanced Plus tiers. ZDX provides performance monitoring and usage metrics for endpoints, web/SaaS applications, network connectivity, and popular UC solutions. ZDX integrates with ServiceNow for ITSM, calculates and trends a ZDX score, and can be used to send outbound communications to employees. Zscaler did not meet the inclusion criteria for collecting employee sentiment or for acting on insights by executing vendor-provided or customer-developed scripts, self-healing automations and workflows. These are on the vendor’s near-term roadmap.

Evaluation Criteria

Gartner evaluates vendors on their Ability to Execute and their Completeness of Vision, as per the definitions below. When the two sets of criteria are evaluated together, the resulting analysis provides a view of how well a provider performs compared with its peers and how well it is positioned for the future.

For more information on Gartner’s Magic Quadrant research methodology, refer to our Research Methodologies on the Gartner website.

Ability to Execute

Gartner analysts evaluate vendors on the quality and efficacy of their DEX tool; their ability to be competitive, efficient and effective; and their ability to positively impact revenue, retention and reputation. Ultimately, vendors are judged on their ability to deliver on their vision.

General evaluation criteria are available at the bottom of this research. For this market, assessments were primarily based on:

- Product: Tool extensibility; support for standard, must-have and optional capabilities; and the vendor’s track record of delivering on its roadmap. The overall breadth of capabilities and the depth of product functionality are other important factors.

- Overall viability: Sustainability of investment/ownership structure, profitability, leadership stability, organizational and partner scalability, and year-over-year product revenue growth.

- Sales execution: Clarity and competitiveness of the vendor’s packaging and pricing model, sustainability of new business growth, and ability to replace competitors.

- Market responsiveness: Tenure in the market, product vision, value proposition and quality of the vendor’s roadmap.

- Marketing execution: Use of various channels and creation of thought-leading content, as well as overall market awareness of the vendor’s DEX tool.

- Customer experience: General customer feedback, availability of customer success services and related case studies.

- Operations: Size and scalability of the organization, partners and platform.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | High |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | Medium |

Marketing Execution | Medium |

Customer Experience | High |

Operations | Medium |

Source: Gartner (May 2025)

Completeness of Vision

Gartner analysts evaluate vendors on their ability to understand current market opportunities and create and articulate their vision for future market direction, innovation, customer requirements and competitive forces. Ultimately, vendors are rated on their vision for the future, and how well that maps to Gartner’s position.

General evaluation criteria are available at the bottom of this research. For this market, assessments were primarily based on:

- Market understanding: Unique value to the market, understanding of external market forces and alignment with customer objectives and use cases.

- Marketing strategy: Overall ability to communicate a unique value proposition, effectively use various marketing channels and address needs of target buyer personas.

- Sales strategy: Pricing and bundling, sales channels and sales partnership strategies.

- Product strategy: Vision to deliver expanded capabilities and a consistent product release cadence, as well as the ability to ensure that its roadmap addresses common customer needs and use cases.

- Business model: Business, value proposition and unique capabilities (for example, patents, people, technology and data).

- Vertical industry strategy: Most common industries among customers, specific target industries, and compliance with common industry regulations or certifications.

- Innovation: Level of investment in product development in new areas related or adjacent to DEX, third-party and partner relationships and integrations, and use of AI/ML, and other novel capabilities.

- Geographic strategy: The number of employees allocated to different regions, tailoring of go-to-market or product strategy to address regional differences, and the depth and scope of partners available in countries with existing and new customers.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Medium |

Sales Strategy | High |

Offering (Product) Strategy | High |

Business Model | High |

Vertical/Industry Strategy | Low |

Innovation | Medium |

Geographic Strategy | Low |

Source: Gartner (May 2025)

Quadrant Descriptions

Leaders

Leaders exhibit strong execution and vision scores and exemplify the functionality required for IT organizations to continuously evaluate and improve DEX. Leaders have the broadest set of capabilities, strongest roadmaps, a larger installed base, and cover the most geographic regions and industries.

Challengers

Challengers exhibit a strong set of technologies, marketing and sales execution, and intellectual property — as also exhibited by Leaders — but do not have the requisite strategic support, vision, innovation or roadmap to compete in the Leaders quadrant. Many Challengers tailor solutions to specific market segments or use cases.

Visionaries

Visionaries exhibit strong strategic support, vision, innovation and a robust roadmap, but have not yet amassed the requisite size, installed base, platform breadth or integration points to compete in the Leaders quadrant.

Niche Players

Niche Players exhibit consistent ability to address specific use cases, geographic regions, market segments or verticals. Their offerings, however, fail to provide a breadth of features and cannot scale to be relevant to all buyers.

Context

The goal of any Magic Quadrant is to provide a level view of comparable vendors (size, capability and corporate structure) and their products’ ability to address the demands of a wide variety of buyers. Not every company’s requirements are identical. We encourage clients to review the accompanying Critical Capabilities research to review use-case and functionality requirements, and this Magic Quadrant research to align industry expertise, vision, technology and cost requirements to the right vendor, regardless of the vendor’s quadrant.

Market Overview

Demand for objective DEX measurement and improvement continues to rise, as organizations recognize its impact on overall employee experience (EX). Gartner’s 2024 Digital Worker Survey found that digital workers who interact with IT for more than support have a Net Promoter Score that is almost three times higher than workers who see IT as a support provider.2 Contrary to some shift-left or zero ticket strategies, digital workers do not want to avoid engagement with IT. They want engagement to be less transactional and more meaningful to help solve business problems or to boost their productivity.

IT departments face a critical choice: stick to traditional operations and risk entering the commoditization zone, or pivot to enhancing technology value and experience and elevate beyond being a service provider. The pivot to business value and human centricity starts by ensuring IT management processes become consistent and reliable disciplines, so that significant oversight is not needed to maintain them. DEX is the key factor in making this decision and charting the future path. DEX tools immensely help to do just that and can free up more time for IT staff to focus on employee enablement, increasing digital dexterity.

Gartner estimates that the DEX tool market grew an additional 15% in 2024, eclipsing $700 million. Gartner forecasts that the market will grow at a compound annual rate of 23% through 2028 to exceed $1.7 billion, based on constant currency (see Forecast: IT Operations Management Software, Worldwide, 2022-2028, 2Q24 Update). Overall, most DEX tool vendors forecast at least 20% annual growth in annual recurring revenue (ARR).

To better understand DEX tool adoption rates, polling was conducted during the “Top 10 Ways to Improve the Digital Employee Experience in 2025” sessions at Gartner’s Infrastructure, Operations and Cloud Strategies (IOCS) conference in London and Las Vegas, as well as its Digital Workplace Summit Texas events.3,4,5 When asked “What is the current stage of your organization’s digital employee experience (DEX) management tool implementation?,” 402 attendees responded. Results were as follows:

- Fully implemented: 11%

- Partially implemented: 26%

- Piloting, procurement underway: 9%

- Planning to implement within the next 12 months: 18%

- Planning to implement beyond the next 12 months: 11%

- No plans to implement at all: 24%

Over the next year, Gartner predicts the DEX market will be shaped by:

- Enhanced AI and GenAI. DEX tools will continue to improve anomaly detection, correlation and causation analysis, identification of remediation actions, and automated problem resolution. GenAI will become common for recommending remediations, drafting employee-facing campaigns, and providing natural language interfaces to tool administrators and DEX leaders.

- Market expansion. 2024 was an active year for M&A, with three significant and several other acquisitions and partnerships. Gartner expects 2025 to be M&A-active. Several new market entrants are also expected within 2025.

- Use-case expansion. Requirements will expand to include non-IT-focused use cases, as well as those for mobile and frontline workers.

- Sustainability. Gartner expects expanded functionality for reporting and delivering sustainable IT contributions.

- More autonomous actions. Automation will gain traction for eliminating repetitive tasks, with IT departments maintaining control.

- Agentic AI. Gartner expects to see a few vendors introduce early-stage AI agents to perform tasks on behalf of administrators.

1 Customer Interest Indicator (CII): Gartner’s CII used for this Magic Quadrant calculates and ranks included vendors using a balanced set of measures that include, but are not limited to:

- Gartner client interaction and Gartner.com search volume and trend data.

- Frequency of mentions as a competitor to other DEX tool vendors within reviews on Gartner’s Peer Insights forum between May 2024 and January 2025.

- Customer interest and engagement as represented by various social media and other platform engagement measurements.

2 2024 Gartner Digital Worker Survey. This survey sought to understand workers’ technological and workplace experience and sentiments. The research was conducted online from April through July 2024 among 5,141 respondents, who were from the U.S. (n = 1,121), Australia (n = 1,086), India (n = 996), the U.K. (n = 973) and China (n = 965). Participants were screened for full-time employment in organizations with 100 or more employees and were required to use digital technology for work purposes. Ages ranged from 18 through 74 years old, with quotas and weighting applied for age, gender, region and income, so that results were representative of countries’ working populations. We defined “digital technology” as including any combination of technological devices (such as laptops, smartphones and tablets), applications, and web services that people use for communication, information or productivity. Disclaimer: The results of this survey do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.

3 2024 Gartner Top 10 Ways to Improve the Digital Employee Experience in 2025 Poll. The poll “What is the current stage of your organization’s digital employee experience (DEX) management tool implementation?” was conducted among attendees of the breakout session “Top 10 Ways to Improve the Digital Employee Experience in 2025” at the IT Infrastructure, Operations and Cloud Strategies Conference (EMEA) on 18-19 November 2024. In all, 117 participated in this poll. Disclaimer: Results of this survey do not represent global findings or the market as a whole but reflect the sentiment of the respondents surveyed.

4 2024 Gartner Top 10 Ways to Improve the Digital Employee Experience in 2025 Poll. The poll “What is the current stage of your organization’s digital employee experience (DEX) management tool implementation?” was conducted among attendees of the breakout session “Top 10 Ways to Improve the Digital Employee Experience in 2025” at the IT Infrastructure, Operations and Cloud Strategies Conference (NA) on 10-12 December 2024. In all, 145 participated in this poll. Disclaimer: Results of this survey do not represent global findings or the market as a whole but reflect the sentiment of the respondents surveyed.

5 2025 Gartner Top Ways to Improve the Digital Employee Experience in 2025 Poll. The poll “What is the current stage of your organization’s DEX management tool implementation?” was conducted among attendees of the breakout session “Top Ways to Improve the Digital Employee Experience in 2025” at the 2025 Gartner Digital Workplace Summit (NA) on 12-13 March 2025. In all, 140 participated in this poll. Disclaimer: Results of this survey do not represent global findings or the market as a whole but reflect the sentiment of the respondents surveyed.

Gartner Peer Insights: We considered reviews for Gartner Peer Insights posted from May 2025 through January 2025 for representative vendors in the DEX tools market.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.