Magic Quadrant for HCM Suites for 1,000+ Employee Enterprises

8 September 2025 - ID G00825432 - 48 min read

By Josie Xing, Ranadip Chandra, and 12 more

GenAI innovations and the rise of agentic AI are transforming how HCM suites address employee, manager and business requirements. HR technology leaders can use this Magic Quadrant to assess HCM solutions in the context of the rapidly evolving HR technology landscape and tightening budgets.

Strategic Planning Assumption

By 2028, 80% of global midsize and large enterprises will have invested in a cloud-deployed human capital management (HCM) suite for administrative HR and talent management, but will still need to use other solutions for 20% to 30% of their HR requirements.

Market Definition/Description

Gartner defines HCM suites for 1,000+ employee enterprises as cloud applications that deliver functionality for attracting, developing, engaging, administering and rewarding employees.

HCM suites for 1,000+ employee enterprises are designed to support transactions and/or analytical processing on a cloud architecture for more than one of the following use cases within a single integrated solution:

- Manage organization and employee data, life cycle processes and transactional employee/manager self-service.

- Manage organizational structure through creating, planning, monitoring and controlling job positions. Maintain a record of workforce data through assigned positions for effective workforce management and budget planning.

- Attract, select and onboard talent through recruiting, internal mobility and onboarding.

- Retain and develop the workforce through compensation, learning, performance and career pathing.

- Pay employees timely and accurately along with essential benefits to address employee requirements in health, retirement, wellness and/or well-being.

- Manage the operational deployment of salaried and hourly workers to capture time, attendance and absences.

- Deliver tools to assist employers in managing country-specific compliance with legislation and agreements pertaining to data residency and labor laws.

- Integrate with notable enterprise applications and provide robust reporting capabilities (e.g., finance, procurement).

Mandatory Features

Mandatory features of HCM suites for enterprises with more than 1,000 employees include:

- Administrative HR — Employee data, organization structure, employment life cycle transaction, role-based self-service, payroll and benefits administration. It may also include absence management, health and safety administration, and other value-added capabilities.

- Talent management — Recruiting, onboarding, performance management, compensation planning, career and succession planning, learning and skills development.

- Integrated HR service management (IHRSM) — Personalized direct access to policy, procedure and program guidance for employees and managers. It may also include integrated case management, knowledge bases, digital document management, virtual assistants and workflow management.

- Solution(s) deployed on a cloud architecture.

At a minimum, an HCM suite for enterprises with more than 1,000 employees must deliver:

- Core HR administrative transaction support, reporting and analytics capabilities, all hosted on a cloud-based platform.

- At least three of the following talent management functions including recruiting/onboarding, performance management, career/succession management, learning, compensation, workforce planning, or a combination of workforce management and one talent management function.

Common Features

Common features for this market include:

- Workforce management (WFM) — Time and attendance administration and workforce scheduling. It may also include task and activity tracking, budgeting and forecasting, fatigue management, and capabilities supporting the experience of frontline workers.

- Employee experience (EX) — Includes functions designed to support the experience of employees, including voice of the employee (VoE), employee well-being, coaching and mentoring, employee campaigns, and recognition and rewards.

- Cross-functional enabling capabilities — These capabilities (which are often emerging) use data from and interact with the above capabilities, and they are increasingly embedded in HCM suites. They include talent analytics, HR virtual assistants (HRVAs) and internal talent marketplace capabilities.

- Applied artificial intelligence (AI) — Includes generative AI, nongenerative machine learning (ML), natural language processing (NLP), graphs and other AI technologies to improve HR processes and employee experience.

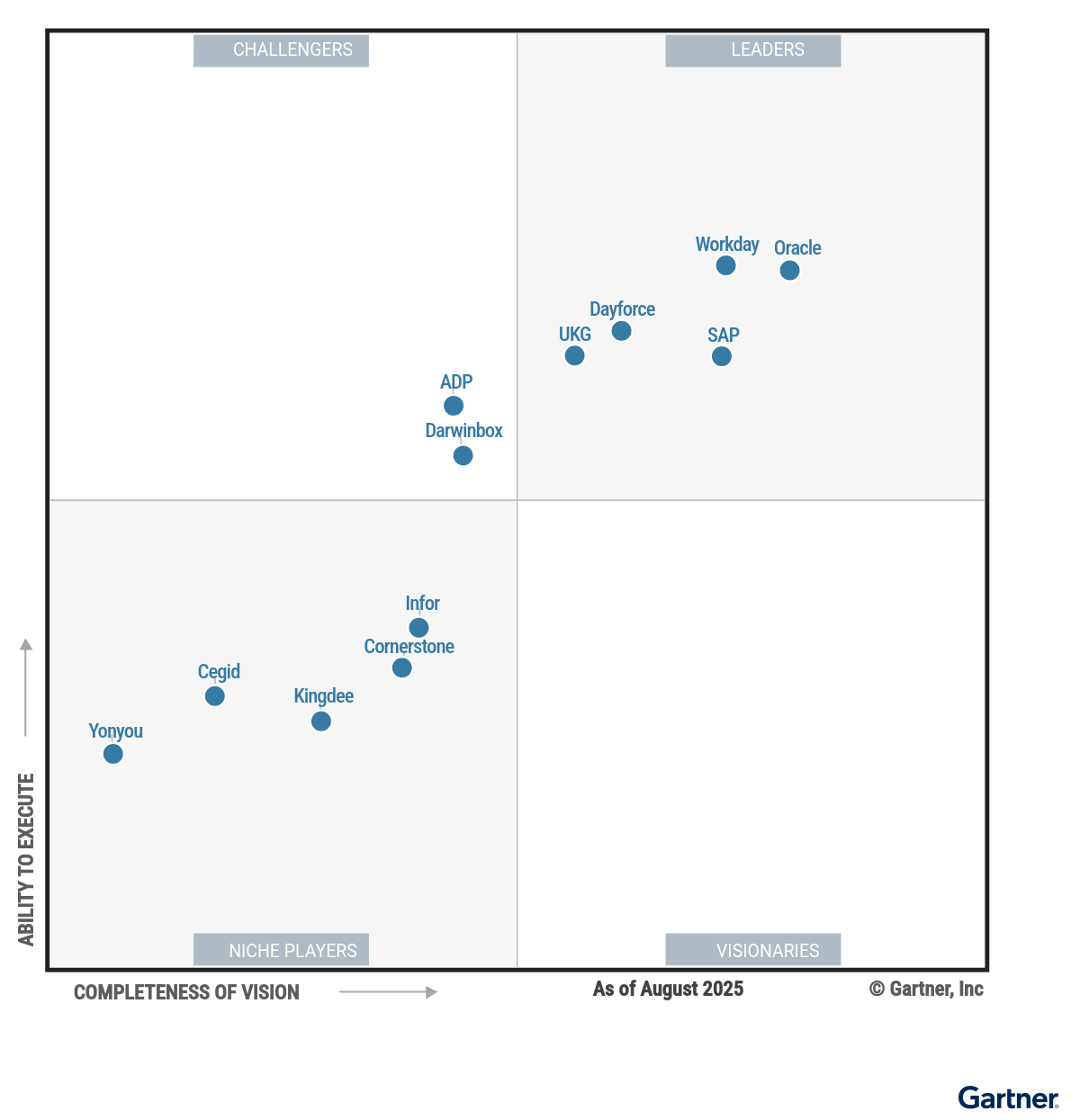

Magic Quadrant

Vendor Strengths and Cautions

ADP

ADP is a Challenger in this Magic Quadrant. ADP Workforce Now targets organizations with fewer than 5,000 employees seeking a configurable, comparatively lower total cost of ownership (TCO) solution with strong WFM and payroll compliance. ADP has over 90,000 clients on ADP Workforce Now, and approximately 2,300 of these have more than 1,000 employees. The product is sold only to U.S. and Canada-based organizations. Ninety-seven percent of ADP Workforce Now customers are deployed in the private cloud.

ADP is focused on enhancing its AI capabilities, particularly its virtual assistant, ADP Assist, which helps employees and HR experts resolve pay anomalies, provides analytics and insights, generates job descriptions and handles HR-related employee queries.

ADP’s skills graph supports talent management by improving profile relevancy for candidate matching. In October 2024, ADP announced the acquisition of WorkForce Software, a leading provider of workforce management solutions, to deliver advanced WFM capabilities to its largest clients.

- Payroll: ADP has a long track record in payroll services and a global payroll presence. It has combined the HCM solution’s payroll engines with its expertise in processing services across payroll, taxes and regulations. ADP has enhanced ADP Assist to support both payroll administrators and employees with guided experiences and chat-based interactions.

- WFM: ADP offers WFM capabilities, ranging from advanced scheduling to forecasting and optimization. These capabilities have expanded since ADP acquired WorkForce Software. Data integration and single sign-on are available today, while a fully integrated user experience is in progress.

- Reporting and analytics: ADP’s reporting and analytics capabilities have external benchmarking for median wage, attrition and cost of operations sourced from a wide range of industries, collected by ADP DataCloud. Analytics enhanced by ADP Assist can create a dashboard via Q&A prompts with access to underlying employee data.

- Geographic coverage: ADP’s core capabilities are designed for North American use, so companies must rely on ADP-owned or third-party add-ins to meet country-specific requirements, especially for functions like payroll and absence management outside the U.S. and Canada.

- Talent management: ADP’s talent management modules are more focused on smaller organizations with basic needs compared with other vendors in this Magic Quadrant. For example, performance management offers less flexibility in customizing review forms. Career planning remains a functionality gap.

- IHRSM: ADP Workforce Now offers basic integrated HR service management (IHRSM), but employee journey support is still on the future product roadmap. The Employee Assist module lacks advanced employee relations and disciplinary case support, and the personalized workflows don’t offer dynamic task assignment or contextual content delivery.

Cegid

Cegid is a Niche Player in this Magic Quadrant. Cegid HR targets organizations headquartered in Europe with 1,000 to 10,000 employees, although it does support larger clients, particularly in the French market. Cegid offers localized payroll support for Western European and Latin American markets. The vendor has around 1,500 live customers, including those in the French public sector/semigovernment, manufacturing, energy and retail segments.

Cegid HR is primarily sold in Western Europe as part of Cegid’s broader ERP suite. Ninety-five percent of Cegid HR customers are deployed in the public cloud — that is, using an infrastructure as a service (IaaS) model such as Amazon Web Services (AWS) or Microsoft Azure.

Cegid is focused on maintaining its European midmarket customer base and boosting its presence in the enterprise segment. The vendor acquired KMB Labs, a European conversational specialist technology, in June 2024 to enhance its AI assistant capabilities.

- Learning management: Cegid Learning — inherited from the Talentsoft acquisition — offers multiple learning content types, enables user-generated content publication and provides tools to create learning paths for different scenarios. Cegid’s AI-enabled skills library can detect new skills by analyzing its customers’ training catalog and job library.

- Geographic strategy: Cegid HR has a strong focus on European markets and compliance with local regulations, such as GDPR. Cegid offers native payroll capabilities in France, Portugal and Spain, making it suitable for global organizations with European operations.

- Alliances and sales strategy: Cegid has built a clear multisegment, three-year sales strategy that articulates its growth plan for its targeted markets, such as Europe, Latin America and account segments. Cegid also has a range of longstanding partners that advise and service customers and enhance the product’s overall value proposition. Newly added partners include Uptale for VR training for frontline workers.

- Applied AI roadmap: While Cegid introduced a virtual assistant this year, its AI roadmap lags those of both market Leaders and Challengers in this Magic Quadrant. The current offering lacks sufficient GenAI use cases in critical areas such as payroll, while the absence of advanced AI agent capabilities — for example, the ability to autonomously take actions — hinders end-user support in task execution and decision making.

- Product strategy: Some capabilities, such as talent acquisition, onboarding, analytics and employee experience (EX), are less mature compared with those of other vendors in this Magic Quadrant. Integration from past acquisitions, such as Talentsoft and Meta4, are still a work in progress, which may be noticeable for customers using multiple modules and products.

- Customer experience (CX): Gartner Peer Insights evaluations of Cegid HR continue to indicate below-average CX compared with other vendors in this research. Based on our customer inquiry volume data, Cegid has limited market momentum.

Cornerstone

Cornerstone is a Niche Player in this Magic Quadrant. It originated in learning and expanded into core HR, performance management and talent acquisition. Cornerstone has over 7,000 customers (including suite and stand-alone learning solution customers) globally, with 80% deployed in the public cloud (on an IaaS model such as AWS or Microsoft Azure). Approximately 60% of Cornerstone’s customers are in the U.S., with 30% in EMEA and 10% in Asia/Pacific and Japan.

In 2024, Cornerstone renamed its HCM product Cornerstone Galaxy. It is centered around a skills-based approach that uses a skills repository to recommend personalized development opportunities and learning content.

In 2025, Cornerstone has continued its focus on integrating its acquired technology solutions — specifically EdCast, Talespin and SkyHive — into a unified content ecosystem. Additionally, Cornerstone has launched Galaxy AI Assist, a conversational, role-specific assistant that provides contextual help, interactive chat and workflow guidance within its Learning Experience and Talent Marketplace platforms.

- Learning: Cornerstone retains a market-leading position in learning technology. Integrations with advanced AI, VR for immersive learning from Talespin (the learning experience platform it acquired), and expanded skills and marketplace intelligence powered by SkyHive have further amplified its learning capabilities.

- Skills management: Cornerstone’s skills management engine delivers AI-enabled skills recommendations, tags and maps skills to job profiles and career paths, and pinpoints skills gaps. The SkyHive acquisition has added to this strength by embedding advanced analytics and boosting labor-market benchmarking.

- Performance management: Cornerstone provides unified performance management capabilities, including goal management, real-time feedback, AI-enabled comment assistance and structured development planning. Cornerstone also allows individuals to link development goals to career planning, enabling them to receive recommendations for relevant skills and training.

- Product strategy: Cornerstone continues to focus its product strategy on learning and wider talent management functions, while placing less priority on foundational HR functionalities, such as core HR and payroll. This strategy inhibits traction in the HCM suite market, where end users increasingly seek a well-rounded HCM suite to address evolving needs across core HR, pay, benefits and talent.

- Payroll, benefits administration and WFM: Cornerstone’s HCM does not offer native payroll, benefits administration or WFM functionality. It relies on its partner network, which requires prospective customers to assess the partner’s ability to ensure alignment with customer needs.

- IHRSM: Cornerstone’s IHRSM is maturing, with enhanced capabilities of workflow creation and management. However, Cornerstone primarily relies on its partner ServiceNow to deliver full IHRSM functionality.

Darwinbox

Darwinbox is a Challenger in this Magic Quadrant. It primarily focuses on India and Southeast Asia, but has been scaling its presence in the U.S. and the Middle East and North Africa (MENA) in recent years. Darwinbox has over 1,000 customers, 70% of which have more than 1,000 employees. All Darwinbox customers are deployed in the public cloud (on an IaaS model such as AWS or Microsoft Azure).

Darwinbox has enhanced its AI capabilities and multicountry offerings, particularly through its integrated talent management and mobile-first experience for frontline workforces. Target customers include multivertical, multinational organizations expanding across Asia/Pacific, MENA, the Americas and Europe.

In response to the rise of agentic AI, Darwinbox was the first HCM platform to develop its own model context protocol (MCP) server to facilitate interaction between its platform and any MCP-compatible AI agent deployed by its customers. This initiative aims to improve Darwinbox agent interoperability with other enterprise agentic AI platforms.

- Product strategy vision: Darwinbox’s product development is well-rounded, with a focus that spans its HCM suite modules. Recent advances include analytics with contextual intelligence and visual insights, a native payroll offering for 11 countries and talent search that combines semantic similarity and text-based matching.

- Applied AI and innovation roadmap: Darwinbox continues to embed AI in use cases that yield high customer adoption. It has launched a dozen AI agents in talent, analytics and employee support, as well as an AI studio for customers to build custom tools and integrate their own agents or partner agents.

- Recruitment and onboarding: Darwinbox also supports stand-alone recruiting buyers. It facilitates complex hiring needs, along with included bonus capabilities, such as budget headcounts, interview feedback collection and comparison, and an opportunity marketplace for internal career, learning and project opportunities.

- Benefits administration: Darwinbox handles employee benefits communications natively but leverages partner benefits platforms to perform the bulk of benefits processing, such as enrollment and claims management.

- Global deployment strategy: Darwinbox is expanding its presence in North America, the U.K. and MENA, but it is still building its customer base in these regions. While the vendor delivers a number of international deployments directly, it still complements select areas, such as payroll and benefits, with partner support to ensure compliance.

- Learning: Despite some natively developed learning capabilities, such as learning experience platform (LXP), the vendor still primarily leverages its partner network for a learning management system. This limits the vendor’s ability to determine its learning product roadmap.

Dayforce

Dayforce is a Leader in this Magic Quadrant. The Dayforce Suite has over 6,800 customers, with 99% deployed in the public cloud managed by the vendor. The product has a strong presence in retail, manufacturing and the services sector, and is growing its presence in financial services, healthcare and the public sector. Dayforce’s global customer base continues to grow, with an developing presence in Germany, Asia/Pacific and Japan adding to established adoption in North America, the U.K., Ireland, Australia and New Zealand.

Dayforce is focused on delivering productivity gains through its full-suite HCM platform and complementary solutions, such as managed payroll and benefit services, clocks, and tax and payments services. Dayforce targets midsize to large enterprises that operate distributed and multijurisdictional workforces.

Dayforce continues to enhance its AI capabilities across various HCM use cases. This includes candidate grading and skills inference and management in offerings such as Dayforce Recruiting and Dayforce AI Assistant for answering employee queries. Dayforce is currently enabling agent-to-agent integration through model context protocol (MCP) and creating a new agent studio for customized solutions to address customer and partner needs.

- Payroll and benefits administration: Dayforce has further enhanced its strong payroll and benefits administration offerings. Its native payroll localizations span three regions, including India, and integrates with Dayforce Wallet for on-demand pay. Embedded benefits decision support helps employees make informed choices about their benefits during enrollment.

- WFM: Dayforce’s WFM has long been one of its key strengths. The vendor has added progressive enhancements, such as a centralized Experience Hub for frontline workers, a shift marketplace for internal staff, and Dayforce Flex Work, which enables alumni and contingent workers to pick up shifts. It also offers a smart clock with instant pay summaries. The mobile interface provides a cleaner and more intuitive user experience compared with its peer solutions.

- Compensation: Dayforce’s compensation module incorporates performance-based rewards, total rewards visibility, pay equity dashboards and peer comparison for comparative ratios. AI-driven predictive analytics further enhance decision making by surfacing insights across compensation, performance and retention risk.

- IHRSM and employee experience: Although Dayforce’s IHRSM solution is maturing, its case tracking and routing remain basic due to limited prebuilt workflows and knowledge base articles. A lack of external benchmarking for employee engagement within its voice of the employee (VoE) functionality places Dayforce behind the leaders in this category.

- Learning: Following the strategic acquisition of eloomi, Dayforce enhanced its learning capabilities with added skills-based learning functionality. However, Gartner client inquiry suggests Dayforce Learning has yet to receive substantial customer validation, and some users have expressed concerns over the high cost of learning modules.

- Succession planning: Dayforce’s succession planning features fall short of the advanced functionality that mature organizations need to scale. In particular, it does not support rules for defining dynamic talent pools.

Infor

Infor is a Niche Player in this Magic Quadrant. Infor is a large, global technology provider that offers Infor HCM, as well as other ERP products for finance, field service, sales, asset management and supply chain management.

Infor HCM targets midsize to large enterprises with predominantly hourly paid workers, such as healthcare, the public sector, manufacturing, distribution, retail and hospitality. Infor product capabilities are best-suited to organizations with frontline, shift-based and deskless workers. Infor HCM has over 1,600 customers, with an average customer size of 13,000 employees. All of Infor’s cloud-based customers are hosted on the public cloud, and its U.S. public-sector customers are offered AWS GovCloud.

In 2025, Infor introduced the Infor Velocity Suite, which brings together GenAI, advanced analytics and automation. It also rolled out a GenAI-enabled virtual assistant to support frontline employees with real-time assistance on tasks like scheduling, time-off requests and accessing training content.

- Vertical strategy: Infor demonstrates strong performance in vertical strategy, with a particular focus on the healthcare sector. It also supports industry requirements for the retail, pharmaceutical, manufacturing and public sectors. Infor has further expanded its industry coverage by leveraging its alliance network of over 2,000 global partners, 1,200 resellers and 300 regional alliances.

- WFM: Infor offers advanced WFM capabilities required for frontline workers, particularly in the healthcare sector. Among vendors in this research, Infor is the closest to achieving skills-based scheduling, where the system identifies qualified, available employees based on labor rules, overtime limits, employee preferences, and qualifications and skills.

- IHRSM: Infor’s integrated HR service management capability extends to the level of granular support for employee grievance cases, providing legally defensible templates. Infor HCM also leverages AI to support the automatic segmentation and classification of service requests.

- Career planning: Infor HCM’s career planning capabilities are still maturing. While the product supports career development for its target industries, features such as dynamic career path modeling and AI-driven role recommendations remain limited.

- Employee experience: Compared with some vendors’ solutions in this Magic Quadrant, Infor HCM lacks sentiment analysis, external benchmarking for VoE findings and employee resource group curation.

- Product maturity: While Infor HCM emphasizes industry-specific HR administration and workforce management, other modules are at varying stages of maturity. This may limit Infor’s competitiveness in industries that require more advanced and integrated talent management capabilities.

Kingdee

Kingdee International Software Group is a Niche Player in this Magic Quadrant. Headquartered in Shenzhen, China, it is one of China’s largest enterprise application software vendors. Kingdee has offered its HCM suite since May 2001. Kingdee HCM Cloud targets global enterprises entering China’s market, as well as Chinese multinationals seeking global expansion with multilanguage, multicurrency and localized compliance capabilities.

Kingdee has around 5,800 HCM suite customers, 66% of which have more than 1,000 employees globally. Approximately 87% of Kingdee HCM Cloud customers are hosted in the cloud, including both private and public cloud deployments. Beyond its strong presence in Greater China (which includes the Chinese mainland, Hong Kong and Taiwan) and Southeast Asia, Kingdee has established subsidiaries and data centers in Singapore and Qatar to meet its customers’ globalization needs.

In 2025, Kingdee launched Intelligent Recruitment, its first AI agent purposely built for recruitment scenarios. Furthermore, Kingdee provides an employee self-service agent to address employee queries about HR policies through voice and text inputs.

- Payroll: Kingdee has payroll localized in Greater China and has a proven record of addressing complex and stringent local compliance requirements. It leverages GenAI capabilities to enhance payroll case management and service delivery.

- Scheduling: Kingdee delivers end-to-end scheduling powered by AI. Advancements include a scheduling engine that forecasts absenteeism risks based on historical attendance data and triggers targeted interventions for managers.

- Alliances: Kingdee HCM Ecosystem Alliance enhances the product’s extensibility and streamlines integration with third-party solutions. The vendor has broadened its industry- and region-focused partner network, including service providers like PwC and KPMG, to better support global, complex organizations, especially Chinese firms expanding overseas.

- Brand awareness: Kingdee has limited brand visibility outside of Greater China despite expanding its partner marketplace to improve global deployment capabilities. Evidence of successful deployments outside Greater China is limited, making it challenging for prospective clients to assess Kingdee’s track record in other regions.

- Reliance on partner ecosystem: Kingdee’s strategic focus on expanding its alliance and partner ecosystem to meet global customer requirements may constrain its investment in developing deep, native HCM capabilities, requiring customers to depend on external extensions to access full functionality.

- Posthire and employee experience capabilities: Kingdee’s posthire suite and IHRSM are primarily optimized for large, China-headquartered organizations and thus, may not fully address the needs of globally distributed enterprises. Gaps remain in career-path modeling, particularly in providing richer visual frameworks for lateral moves, promotions and specialist tracks. Additionally, limited flexibility in workflow configuration hinders the delivery of a truly intuitive self-service HR experience.

Oracle

Oracle is a Leader in this Magic Quadrant. Oracle launched its Fusion Cloud HCM in 2012 as a unified part of Oracle Fusion Cloud Applications. Oracle Fusion Cloud HCM is sold to midsize and large enterprises worldwide. Gartner estimates that Oracle Fusion Cloud HCM has over 4,600 customers — primarily organizations with up to 15,000 employees. All customers are deployed in the public cloud, managed by Oracle.

Oracle Fusion Cloud HCM spans core HR, talent, payroll and workforce management functions. Since its initial GenAI pilot in 2023, Oracle has delivered over 67 GenAI use cases. In 2025, the vendor launched 29 AI agents embedded across all areas of the HCM suite, leveraging AI MCP and agent-to-agent (A2A) models. Oracle also introduced its AI Agent Studio to allow customers to build, configure and manage agents.

Oracle’s new event management capability in Oracle Communicate enables HR and employees to create and manage internal events — such as onboarding sessions, learning workshops and community gatherings — directly within Oracle Fusion Cloud HCM.

- AI innovation: Oracle continues to embed AI across its suite, supporting HR and service delivery, talent management, recruiting, payroll, and workforce management and planning. AI Agent Studio, together with “Ask Oracle,” one of several methods for invoking AI agents, enhances AI accessibility and reduces reliance on traditional transactional pages.

- Prehire talent management: Oracle’s recruitment and onboarding capabilities demonstrate strong performance. Oracle Recruiting and Recruiting Booster provide embedded talent acquisition from sourcing, candidate relationship management, hiring events, messaging and high-volume interview automation. Its newest AI agent, Career Coach, guides preapplication prospects through profile creation, screening and job discovery.

- Product maturity and cohesion: Oracle demonstrates significant product maturity in analytics, skills management, EX and user interface. All product capabilities are natively developed with extensible capabilities, which help deliver a unified user experience.

- Implementation and maintenance effort: Oracle’s HCM customers often find implementing and maintaining Oracle Fusion Cloud HCM requires significant time and effort, especially given Oracle’s rapidly evolving product roadmap.

- Total cost of ownership: Oracle’s HCM Now program offers midmarket customers a lower-cost entry point. However, subscription fees, add-on modules and ongoing maintenance can still be high for midsize organizations with more constrained budgets seeking a full-fledged suite.

- Limited integrations: Although no single vendor can support all of clients’ broad HCM technology needs, Oracle has a highly selective and relatively limited third-party marketplace of predefined integrations, with specialized add-on capabilities. Clients should recognize this potential challenge to future-proofing their unique and flexing HCM needs.

SAP

SAP is a Leader in this Magic Quadrant. SAP offers SAP SuccessFactors HCM alongside other finance and ERP solutions, such as SAP Cloud ERP. The SAP SuccessFactors HCM suite is built on a multitenant, cloud-based architecture. SAP Business Technology Platform (SAP BTP) provides extensibility for AI, analytics and security, and is enhanced with built-in integration across SAP Business Suite solutions.

Gartner estimates that SAP SuccessFactors has over 11,000 customers, and that the SAP SuccessFactors Employee Central solution has more than 6,500 customers. The HCM suite targets midsize to large organizations. The solution has more than 150 large customers exceeding 100,000 employees. Ninety-seven percent of SAP SuccessFactors customers are deployed in the public cloud (managed by SAP or optionally hosted in IaaS).

SAP continues to enhance its cross-platform AI copilot, Joule, which has evolved into an AI orchestrator that manages a team of agents to support key HCM tasks and collaborate via A2A protocol. Joule is available in 11 languages and on mobile. SAP also introduced WalkMe (acquired in 2024) for SAP SuccessFactors HCM. WalkMe is a digital adoption platform providing contextual in-app guidance and automation for workflow improvement. In August 2025, SAP announced it had entered into an agreement to acquire talent acquisition software provider SmartRecruiters.

- Geographic coverage: SAP SuccessFactors is localized for core HR in 104 countries, with compliance tracked by HR and legal experts. Its SAP SuccessFactors Employee Central Payroll solution has 53 localizations, more than any other vendor featured in this research.

- Talent management: SAP SuccessFactors has strengthened its talent management suite with AI-driven enhancements. The career and talent development module now offers targeted learning journeys, smart skills recommendations and AI-assisted performance conversations.

- Alliances and sales strategy: The SAP SuccessFactors HCM suite benefits from a broad partner ecosystem, including over 350 independent software vendors that enhance the overall product proposition and develop custom applications via SAP BTP. SAP has over 1,200 partners that advise and service customers around the world.

- Customer transition guidance: Guidance for SAP on-premises HCM customers migrating to SuccessFactors remains unclear for organizations with special requirements, such as compliance, particularly in the Middle East and European public sector.

- WFM approach: The recent acquisition of WorkForce Software (one of SAP’s primary WFM partners) by ADP has raised customer questions about the future of the SAP and WorkForce Software alliance. This shift may encourage SAP to steer clients toward its own emerging WFM offerings despite SAP’s track record of successful collaboration with ADP.

- AI pricing model: SAP offers two pricing models for its premium AI capabilities: a per user per month (PUPM) model for specific AI units, and a transactional, usage-based model for services such as SAP Document AI. While these options provide flexibility, the variety of pricing packages can introduce complexity for end users, particularly when it comes to contracting.

UKG

UKG is a Leader in this Magic Quadrant. UKG Pro targets midsize to large global organizations headquartered in the U.S. or Canada and has over 6,800 HCM suite customers. Nearly 40% of UKG Pro customers have over 1,000 employees, and around 1,000 use UKG Pro as their HR system of record for employees outside North America. UKG Pro provides a full HCM suite, with a robust WFM solution, payroll compliance and integrated HR service management. UKG Pro supports all verticals but primarily focuses on retail, healthcare, manufacturing, and services and distribution verticals.

Using its Great Place to Work Hub, UKG offers insights on skills; diversity, equity and inclusion; and employee satisfaction to build an inclusive culture and enhance the employee experience for its customers. All UKG customers are deployed in the public cloud (managed by UKG).

Since the 2024 release of UKG Bryte, an AI-powered virtual assistant, UKG has expanded its AI capabilities with new HCM and WFM agents that automate tasks across HR, pay and time. In 2025, UKG announced its partnership with ServiceNow to integrate UKG’s AI-driven capabilities with ServiceNow’s AI Agent Fabric. This connection is designed to automate routine administrative tasks across payroll, workforce management and HR.

- WFM: UKG Pro demonstrates strong WFM functionality when compared with other HCM suites in this Magic Quadrant. Advancements include automatically generated schedules using historical data and employee preferences via UKG Bryte. UKG’s AI-enabled Shift Incentivization addresses labor shortages and supports worker needs by identifying hard-to-fill shifts and recommending appropriate incentives.

- Employee experience: EX is another area where UKG demonstrates strong capabilities in this research. UKG’s Great Place to Work Hub provides data insights into employee sentiment and culture, external benchmarks and best practices to drive employee engagement and retention. UKG Wallet, supported by Payactiv, gives employees instant access to earned wages.

- Vertical strategy: UKG supports a broad range of industries and organizations with a strategic focus on frontline or hourly paid workers. Alliance strategy and partner integrators further support this vertical expertise.

- Geographic coverage: UKG only actively sells UKG Pro to organizations headquartered in the U.S. and Canada, and does not offer a native core HR system of record outside North America. Customers headquartered outside these two countries hoping to leverage UKG Pro must rely on UKG partners in other regions or use UKG solutions like UKG One View for multicountry payroll and UKG Pro WFM for global workforce management.

- Customer experience and perception: Despite modest improvements reflected in recent Gartner inquiries, UKG’s customer satisfaction has not fully rebounded from organizational changes in the past year. Lingering concerns around service and support remain, though signs of improvement are emerging.

- Partner reliance for talent acquisition: Despite AI-enabled candidate matching, scoring, automated job description and interview question generation, UKG Pro still depends on partners — such as Eightfold for candidate relationship management — to round out its talent acquisition suite.

Workday

Workday is a Leader in this Magic Quadrant. Workday offers the Workday Human Capital Management (HCM) suite alongside other products for ERP functions. Workday targets its solution to midsize and large enterprises in key industries like healthcare, retail, hospitality, higher education, government and financial services.

Workday HCM has approximately 6,000 customers worldwide. Over 68% of Workday customers have over 1,000 employees, and 38% fall into the 1,000 to 5,000 employee segment. Overall, customer employee counts range from under 500 to over 100,000. Eighty percent are deployed in the private cloud.

In 2025, Workday launched Workday GO for small and midsize businesses, aiming to deliver fast deployment and achieve business outcomes in a shorter time frame. Since launching its AI brand, Workday Illuminate, Workday has introduced AI innovations in talent, wellness, analytics and role-based agents such as Recruiting Agent. Furthermore, Workday announced the Workday Agent System of Record to help organizations manage their AI agents — from Workday and third-parties alike — in one place.

- AI adoption: Workday’s AI brand — Illuminate — has driven broad adoption of AI features among its core HCM customers. Nearly 73% of entitled core HCM customers now use at least one AI feature, and almost 10% are leveraging agentic AI use cases.

- Analytics: Workday provides comprehensive reporting and analytics capabilities through People Analytics (focused analytics and storytelling), Peakon Employee Voice (VoE), Discovery Boards (self-service analytics) and Prism Analytics (dashboard creation and external data integration). Its AI-driven analytics engine captures critical HR trends and presents them in tailored reports and interactive dashboards.

- Skills management and internal mobility: Workday demonstrates strong capabilities in skills management and internal mobility. Skills Cloud supports personalized, skills-based recommendations for roles, projects, learning and upskilling. Workday’s Talent Marketplace uses AI to match employees to internal opportunities based on current skills, identified gaps and development potential.

- Payroll localization development: Workday offers payroll localization in six countries (U.S., Canada, U.K., Ireland, France and Australia). However, due to a change in payroll strategy, new customers needing French payroll are encouraged to leverage Workday’s partners, such as Strada. Overall, Workday’s localization footprint remains limited compared with other vendors in this Magic Quadrant, and planned rollouts in Germany have been delayed.

- Total cost of ownership: When it comes to analyzing pricing for individual functionalities, customers find Workday’s practice of bundling multiple applications challenging. If customers wish to drop one or more SKUs from the bundle at renewal, it is nearly impossible to independently validate the correct cost of the remaining service lines.

- Global reach and industry adoption: Workday’s global presence and industry adoption still trail other leading HCM vendors, particularly for enterprises headquartered outside North America. Recent partner and vertical-focused initiatives signal a shift, but broader adoption in complex, product-based industries such as manufacturing is still developing.

Yonyou

Yonyou Network Technology is a Niche Player in this Magic Quadrant. Yonyou is one of the largest enterprise application software vendors in China, with a strong customer base among large local enterprises in the public sector and manufacturing. Yonyou’s Digital HR supports Chinese enterprises with a global expansion ambition and overseas enterprises entering China’s market.

Yonyou’s current HCM product, YonBIP, is part of a unified applications suite with nearly 8,900 HCM suite customers. While most customers are based in China, YonBIP is increasingly deployed in South Africa, Western Europe and Latin America. Forty-five percent of YonBIP customers are deployed in the private cloud and 46% in the public cloud, managed by Yonyou and optionally hosted in IaaS.

The vendor has launched various AI agents, including employee service, HR administration, compensation and time AI agents. Yonyou also introduced its first AI agent, YonMate, which integrates with Chinese AI models, including DeepSeek, providing autonomous decision making, rapid feedback and task execution for HR leaders.

- Compressed implementation timeline: Yonyou delivers the full HCM suite in a comparatively short timeline — six months on average. Recently, an organization with more than 150,000 employees deployed Yonyou in 162 days.

- Payroll localization: Yonyou has payroll localizations for regions known for difficult data residency statutes and unscheduled legislation changes — Singapore, Malaysia, Saudi Arabia and Greater China (which includes the Chinese mainland, Hong Kong and Taiwan). Support for optical character recognition to fluently convert documents for payroll considerations is a differentiator for Yonyou in Southeast Asia.

- Subscription tiers and pricing: Yonyou has a volume-based pricing model, and its unit subscription cost is below the global average. These are important considerations for Asia/Pacific organizations that often operate with more constrained resources.

- Sales strategy: Yonyou’s concentrated focus on midsize and large manufacturing and public-sector enterprises limits its reach in other industry segments. This narrow targeting may result in missed opportunities outside its core markets.

- Product strategy: As Yonyou primarily concentrates on serving organizations based in China, the product roadmap is driven by HR administration capabilities. As a result, customers seeking deeper talent management and employee experience functionalities will find it difficult to adopt YonBIP.

- Financial viability: Yonyou is the only vendor in this research whose revenue declined in 2024, raising concerns about the company’s financial stability and long-term viability.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

Kingdee International Software Group was added because it met the qualifications listed in the inclusion criteria section of this report.

Dropped

No vendors were dropped from this Magic Quadrant.

Inclusion Criteria

To be included in this Magic Quadrant, each vendor had to:

- Deliver core HR administrative transaction support and reporting/analytics capabilities, plus at least three of the following talent management functions — recruiting/onboarding, performance management, career/succession management, learning, compensation and workforce planning — or a combination of WFM and at least one TM function.

- Deploy its solution(s) on a cloud architecture.

- Have at least 150 customers, each with more than 1,000 employees, that use its core HR capabilities and at least two TM functions in a production environment in either a community cloud or a public cloud.

- Actively market, sell and implement an HCM suite on a stand-alone basis, regardless of any additional bundling with ERP suites or other applications.

- Provide evidence of market momentum by documenting at least 50 net-new deals during the previous four fiscal quarters (31 March 2024 through 31 March 2025) — each with more than 1,000 employees — for its core HR capabilities and either two or more TM functions or one TM function and WFM.

- Rank among the top 20 for the Customer Interest Indicator (CII) as defined by Gartner. CII was calculated using a weighted mix of internal and external inputs that reflect Gartner client interest, vendor customer engagement and vendor customer sentiment from 1 February 2024 through 28 February 2025.

Some vendors did not satisfy all of these criteria and were therefore excluded from this research. However, their offerings do meet many customer requirements and could also be included in an evaluation of HCM suites. See Market Guide for Cloud HCM Suites for Regional and/or Sub-1,000 Employee Enterprises for more information.

Evaluation Criteria

Ability to Execute

Product or Service: This includes the vendor’s capabilities in administative HR, TM, WFM and HR service delivery (refer to the Market Definition/Description section for a detailed list of functions). These areas are assessed for functional breadth and ease of use. How well the vendor integrates the components is also important. The architecture, delivery models, and use of mobile and social capabilities are also rated. The focus is on the vendor’s current functionality, although enhancements and/or new modules on the verge of general availability are also considered.

Overall Viability (Business Unit, Financial, Strategy, Organization): Key aspects of this criterion are the vendor’s ability to ensure the continued vitality of a product, including support for current and future releases, and a clear roadmap for the next three years. The vendor must have consistent revenue growth during the past four quarters to fund current and future employee burn rates and to generate profits. The vendor is also rated on its commitment to the specific product being evaluated, and the ability to leverage it to generate revenue and profits in the cloud HCM suite market.

Sales Execution/Pricing: The vendor must provide multicountry regional and/or global sales and distribution coverage that aligns with its marketing messages. It must have specific experience and success in selling cloud HCM suite solutions to HCM buying centers. This includes deal management, partnering, pricing and negotiations, presales support, and the overall effectiveness of the sales channels.

Market Responsiveness/Record: The provider’s ability to continually invest, innovate and take customer feedback into consideration as HR needs evolve and market dynamics change is crucial. This criterion also considers the provider’s history of responsiveness to changing market demands.

Marketing Execution: The clarity, creativity and efficacy of blog posts, marketing collateral and branding efforts are essential to delivering the vendor’s message, influencing the cloud HCM market and increasing awareness of capabilities. It is crucial to clearly understand the target personas and establish a positive identification in the minds of all stakeholders (e.g., CHRO, human resources IT [HRIT], head of people success).

Customer Experience: We consider feedback from active customers on generally available releases during the past 12 to 18 months. Primary data sources include Gartner inquiries and other customer-facing interactions taking place at Gartner and industry conferences. Sources of feedback also include analyst-validated customer reviews from Gartner Peer Insights relevant to the audience.

Operations: The vendor’s ability to manage work location strategies (including HR-related data), maintain a reputation in the industry as an employer, and create diverse and inclusive work environments is critical. We highly evaluate vendors that administer robust operating cycles, engage in CSR activities and launch new programs while maintaining growth.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Low |

Sales Execution/Pricing | High |

Market Responsiveness/Record | High |

Marketing Execution | Medium |

Customer Experience | High |

Operations | High |

Source: Gartner (September 2025)

Completeness of Vision

Market Understanding: This refers to the vendor’s ability to understand buyers’ needs and translate them into products and services. We specifically looked for how vendors described the integrated market and opportunity for their cloud HCM suites as a whole, not merely that of the component products.

Marketing Strategy: Clear, differentiated messaging centered around a tagline should be communicated through diverse channels. We highly evaluate vendors that aim to deliver buyer-centric messaging that addresses innovation, employee experience, culture and human-centric solution development.

Sales Strategy: Key elements of the strategy include a sales and distribution plan, internal investment prioritization and timing, and partner alliances.

Offering (Product) Strategy: The vendor should demonstrate a vision for application functionality across the breadth and depth of the cloud HCM suite. We place additional focus on the vendor’s vision for the use of emerging technologies; advanced analytics; relevant social, geographic or industry use cases; integration and ease of use; and support for process transformations enabling the digital workforce. The product strategy can be a combination of organic development, acquisition and/or ecosystems. For ecosystems, we focus on the quality and support of third-party partners. For those that acquire functionality, we pay close attention to integration strategy and roadmaps.

Business Model: The vendor needs to have a clear business plan for how it will be successful in the cloud HCM suite market. This plan should include appropriate levels of investment to achieve healthy growth during the next three to five years.

Vertical/Industry Strategy: The vendor’s strategy to deliver a tailored approach for industries involves directing resources (sales, product development), skills and products to meet the specific needs of individual market segments, including verticals. This may also include relevant compliance certification/authorization (such as FedRAMP).

Innovation: The vendor must show a marshaling of resources, expertise and/or capital for competitive advantage or investments in new areas. Potential areas include advanced analytics; machine learning (ML); diversity, equity and inclusion; service delivery; and engagement measurement. The vendor must also show UX improvements or new access methods, such as conversational UIs, chatbots and virtual assistants.

Geographic Strategy: Examples of criteria include core HR locations, payroll localizations, number of existing languages supported and local compliance (for example, with GDPR).

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Medium |

Sales Strategy | Medium |

Offering (Product) Strategy | High |

Business Model | Low |

Vertical/Industry Strategy | High |

Innovation | High |

Geographic Strategy | High |

Source: Gartner (September 2025)

Quadrant Descriptions

Leaders

Leaders demonstrate a market-defining vision for how HCM technology can help HR organizations achieve business objectives. Leaders have the ability to work toward that vision through products and services and have demonstrated solid business results in the form of revenue and earnings. They are well-aligned with industry trends for AI, deployment and/or experiences, and are ahead of their peers in integrating these AI capabilities. In the cloud HCM suite market, Leaders show a consistent ability to win deals. These include the foundational elements of administrative HR (with many country-specific HR localizations) and result in high attach rates for talent management, WFM and HR service delivery capabilities. Leaders have multiple proofs of successful global and/or regional implementations by organizations of different sizes (judged by number of employees) with workforces in multiple regions and across a wide variety of industries. Leaders are often the companies against which other providers in this market measure themselves.

Challengers

Challengers have developed a substantial presence in at least one market and have a growing presence in multiple submarkets. Although they have a broader addressable market than Niche Players, they are unable to execute consistently or equally well in all geographies. Challengers understand the evolving needs of HR organizations but may not lead customers into new functional areas with a strong functional vision. Challengers tend to have a good technology vision for architecture and other considerations of IT organizations but are not as operationally mature as Leaders. They have strong customer growth and momentum, financial health and sustained product investment. Challengers are further distinguished from Leaders primarily by their reduced ability to execute consistently throughout the full range of cloud HCM suite functionality for large and complex global enterprises.

Visionaries

Visionaries are ahead of most competitors in delivering innovative products and/or delivery models. They anticipate emerging and changing market needs and can lead the market into new areas. Although Visionaries have a strong potential to influence the direction of the cloud HCM suite market, they are limited in execution and/or lack a demonstrable track record.

There are no Visionaries in this edition of the Magic Quadrant, mainly due to the greater emphasis on the execution of administrative HR functions (including cost-effective and reliable delivery of standardized processes) that are less subject to innovation. Much of the innovation in the field of HCM, such as AI capabilities, has been embedded in niche talent management and analytics applications, which do not constitute an HCM suite.

Niche Players

Niche Players offer cloud HCM suite functionality, but they may lack some functional components, focus on a limited geographic or workforce scale, or lack strong business execution in their chosen niche. They may offer complete portfolios for a specific industry or workforce size, but they cannot fully support cross-industry requirements for several HCM functions, such as WFM, recruiting and learning. They may offer only limited localizations for administrative HR. From an execution standpoint, Niche Players may lack the ability to support large enterprise requirements or complex global deployments. Nevertheless, Niche Players can offer the best solutions for HR organizations whose requirements align with their market focus and capabilities. The price-to-value ratio for these vendors is often attractive. They may win consistently in a certain region or industry but do not consistently win in multiple regions. This may be due to limitations of execution or maturity, or it may simply reflect their market focus.

Context

The market for cloud HCM suites continues to mature and attract investment. Since the last iteration of this research, vendors have responded to customer demands by delivering improvements in the following areas:

- Digital adoption — Vendors are enhancing digital adoption by introducing guided journeys for new features, ensuring users can easily learn and use new capabilities. Some vendors have developed or acquired digital adoption platforms that provide contextual in-app guidance and workflow automation, accelerating feature uptake.

- User experience and AI — Vendors are enhancing user experience through role-specific, persona-based AI assistants/agents tailored to HR super users. Popular offerings include recruiter AI, analytics AI and scheduler AI that are designed to boost HR users’ productivity, support decision making and automate workflows.

Yet, some vendor roadmap commitments and desired outcomes are delivering more slowly than vendor and customer expectations:

- Data sharing for AI use-case creation — Vendors still struggle to convince customers to share their data for more tailored use cases despite implementing responsible AI practices and robust guardrails. This challenge is particularly pronounced for HCM vendors that rely on hybrid AI architectures to fine-tune their outputs with customer-specific data.

- Postacquisition integration — Vendors are struggling to assimilate acquisitions they make in ways that realize the expected synergy and business value. Even after closing an acquisition, the resulting unified product is often less than the sum of its premerger parts.

Market Overview

The market for cloud HCM suites continuously demonstrated strong growth in 2024, with a market growth close to 16.4%. Total revenue for cloud HCM suites reached $27.5 billion at the end of 2024. The HCM software market remained the top segment in the ERP market, at 55.3% revenue share. It is projected to display double-digit growth through 2029.1

The market is maturing, consolidating around a stable group of established megavendors with diversified portfolios. High barriers to entry and entrenched competitors mean few new entrants are expected in the near future. Ongoing market consolidation is driven by M&A activity, though integration challenges remain.

Many vendors continue to rapidly innovate. GenAI and AI agent pilots are evolving into high-impact HR use cases, and vendors are embedding AI across HR, ERP, CRM and other systems to orchestrate true end-to-end workflows. As AI advances and budgets tighten, product maturity and buyer expectations have risen. Many early adopters — especially those with 7- to 10-year-old deployments — are reimplementing HCM systems to integrate modern capabilities. Cloud migration continues, with on-premises customers shifting steadily to cloud platforms.

Despite continuous investment in HCM solutions, HR software buyers’ regret is widespread. Forty-three percent of CHROs report significant dissatisfaction — well above the 32% average across other functions.2 In response, vendors are enhancing implementation support, alliances, deployment speed, post-go-live services and user-adoption strategies. Quickly demonstrating a clear ROI is becoming a critical differentiator.

This year, Gartner added one new vendor to the Magic Quadrant to further reflect HCM coverage in East Asia. All vendors have shifted to the right, reflecting innovation traction since last year. However, no previously included vendor has changed quadrants. Below is a summary of three key trends in the HCM suites for 1,000+ employee enterprises market.

Strong emphasis on agentic AI/autonomous agents: Vendors across the market are prioritizing agentic AI — the autonomous or semiautonomous software entities that use AI techniques to perceive, make decisions, take actions and achieve goals in digital or physical environments. Today’s offerings largely function as AI assistants or assistive tools, but roadmaps uniformly target progressively greater autonomy and a shift to AI agents. This shift signals a move from supportive assistants toward independent agents capable of driving HR processes either fully or semiautonomously.

Evolving pricing models: Amid continuing uncertain economic conditions, organizations are growing more price-sensitive. Many cloud-to-cloud migrations now stem from customer budget constraints. With vendors racing to deliver enhanced AI capabilities, pricing structures play a decisive role in subscription and adoption decisions. Gartner is seeing a shift toward tiered, credit- or token-based, and value-based models for advanced or premium AI features, reflecting a more dynamic approach to commercialization.

Unified platform strategy: Vendors are embracing a unified platform strategy, embedding AI and other new capabilities not only in HR but also across ERP, CRM and collaboration tools like Microsoft Teams and Salesforce to enable seamless end-to-end workflows. To support this, they’ve expanded partner and alliance networks beyond their home regions and core industries. HCM vendors are fully leveraging their platform as a service (PaaS) capabilities to build, extend and integrate both proprietary and third-party applications. HCM vendors aim to leverage these extensible apps to bridge HCM systems with external solutions, helping meet customers’ last-mile needs.

Acronym Key and Glossary Terms

| AI | Artificial intelligence |

| EMEA | Europe, Middle East and Africa |

| ERP | Enterprise resource planning |

| GDPR | General Data Protection Regulation |

| GenAI | Generative AI |

| Greater China | Unless otherwise specified, “Greater China” in this research refers collectively to the markets of the Chinese mainland, Hong Kong and Taiwan. |

| HCM | Human capital management |

| LXP | Learning experience platform |

| UX | User experience |

| VoE | Voice of the employee |

| VR | Virtual Reality |

| WFM | Workforce management |

Gartner used the following sources to collect information about vendors and their cloud HCM offerings:

- Vendor presentations and demonstrations to the Gartner analyst team: Specifically, to support this research, each vendor presented information about its company, capabilities and functionality using a product demonstration script that Gartner provided to all participating vendors. Each vendor was allotted the same amount of time for this research. Gartner also conducts interactions with vendors throughout the year as part of normal and ongoing relationships with user and vendor clients.

- Research and data collection: Gartner also asked each vendor to respond to and fill out a survey that investigates, in more detail, factual information about its company and HCM offering. As part of this exercise, Gartner reviewed customer references on Gartner Peer Insights submitted in the past 12 months.

Endnotes

1 Market Share Analysis: Human Capital Management Software, Worldwide, 2024

2 2025 Gartner Business Buyer Survey. This survey sought to understand how functional business units (customer service, finance, human resources, marketing, sales and supply chain management) within organizations approach large-scale software purchases to support their business function. The survey was conducted online from October through December 2024 among 3,068 respondents from organizations with annual revenue of at least $50 million or equivalent from North America (36%), Western Europe (32%), Asia/Pacific (19%) and Southern Europe (13%). Industries surveyed include education providers, energy, financial services, government, healthcare, health payer, technology, telecom, insurance, manufacturing, natural resources, retail, transportation and utilities. Qualified respondents were at manager level or higher, and had been actively involved in the purchasing process for the most impactful software capabilities for their respective functional business units during 2023 or 2024. Software purchases were either new, replacement or expansion purchases. Disclaimer: The results of this survey do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.

Note 1: Mergers and Acquisitions

Recent M&A activity in this space includes:

- Dayforce completed the acquisition of eloomi, a learning management platform, in February 2024.

- Workday completed the acquisition of HiredScore, an AI-enabled talent orchestration solution, in February 2024.

- Cornerstone completed acquisitions of Talespin, a virtual reality (VR)-based training solution, in March 2024, and SkyHive, a skills management solution, in May 2024.

- ADP announced the acquisition of WorkForce Software, a leading provider of workforce management solutions, in October 2024.

- Cegid acquired KMB Labs, a European conversational technologies company specializing in designing, building and scaling chatbots, search engines and messaging solutions, in June 2024.

- SAP acquired WalkMe, a digital adoption platform providing contextual in-app guidance and automation for workflow improvement in September 2024. It also announced it had entered into an agreement to acquire SmartRecruiters, a leading talent acquisition software provider, on 1 August 2025.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.