Magic Quadrant for Distributed Hybrid Infrastructure

8 September 2025 - ID G00824109 - 36 min read

By Julia Palmer, Jeffrey Hewitt, and 3 more

Heads of I&O are seeking a unified experience across public and private cloud, as well as edge deployments. The DHI market aims to reduce operational complexity and prove a unified cloud-to-edge management and control plane to simplify workload management and ensure policy enforcement.

Strategic Planning Assumption

By 2028, 55% of enterprises will initiate proofs of concept for alternative distributed hybrid infrastructure (DHI) products to replace their VMware-based deployments and embrace hybrid cloud infrastructure delivery, up from 15% in 2025.

Market Definition/Description

Distributed hybrid infrastructure (DHI) are solutions incorporating cloud-native infrastructure principles (e.g., programmability, elasticity, modularity and resiliency). DHI can be deployed and managed, delivering cloud services wherever the customer chooses, including on-premises, at the colocation, at the edge or in the public cloud. This flexibility sets DHI apart from traditional public cloud infrastructure as a service (IaaS), which typically relies on a centralized approach. Vendors fall into three categories, with distinct strategies: cloud platform providers, full stack hyperconverged vendors and software infrastructure platform providers. Their offerings include software and/or integrated hardware with a unified management and control plane.

DHI serves as the foundation for deploying applications in a distributed manner, while maintaining a cloud-native or cloud-inspired approach. This approach enhances agility and flexibility for workloads that require deployment beyond the public cloud infrastructure and addresses potential limitations of traditional on-premises setups. DHI offers greater consistency, flexibility, mobility, isolation and availability across customer environments.

Enterprises can benefit from the principles of cloud computing, while retaining the ability to deploy resources whenever and wherever they are needed, and provide options to address workload specific characteristics, such as latency, performance and data sovereignty. Infrastructure and operations (I&O) leaders targeting this market typically have strong hybrid needs and do not necessarily adhere to a cloud-only or cloud-first strategy, often maintaining substantial on-premises deployments. This strategic approach enables enterprises to harness the advantages of both environments, offering the flexibility needed to standardize and optimize operations, uphold performance and availability service-level agreements (SLAs), and support a variety of workloads.

Mandatory Features

- Integrated platform services comprising hypervisor, storage and virtualized networking services.

- Vendor-engineered, hybrid cloud infrastructure, resource management control plane.

- Management of the distributed infrastructure that is supported by a set of APIs that encompasses all of the distributed infrastructure’s capabilities.

- Centralized management portal that provides a secure, automated, full-stack solution for operating and supporting the distributed infrastructure.

- Ability to deploy the infrastructure services in multiple locations that must include on-premises customer data centers or colocations sites, and at least one hyperscale public cloud platform.

- Support for virtual machines (VMs).

Common Features

- Ability to deliver the distributed hybrid infrastructure solution as a service.

- Ability to deploy their services across multiple public clouds.

- Vendor-supplied facilities or other deployment options, such as colocation, edge and remote locations.

- Integrated hardware — either supported by the same vendor that offers the software; or certified for the integrated software, but managed by the enterprise, the vendor that provides the software or a third-party partner.

- Additional platform services — e.g., as-a-service, add-on offerings, such as database as a service (DBaaS) and disaster recovery as a service (DRaaS).

- Product integration with traditional enterprise infrastructure systems — e.g., directory services, IT service management (ITSM).

- Metered consumption-based services — customers are charged only for what they consume.

- Scalable and elastic — the offering will provision and deprovision resources to fit the customer’s continuous requirements (e.g., bursting to the public cloud or dynamic preemptive ordering).

- Support for GPUs and AI infrastructure accelerators.

- Ability to provision and orchestrate bare-metal servers.

- Ability to provision, support and orchestrate containers, or integrate with third-party container orchestration platforms.

- Ability to provide sovereign cloud support with lightly tethered operations.

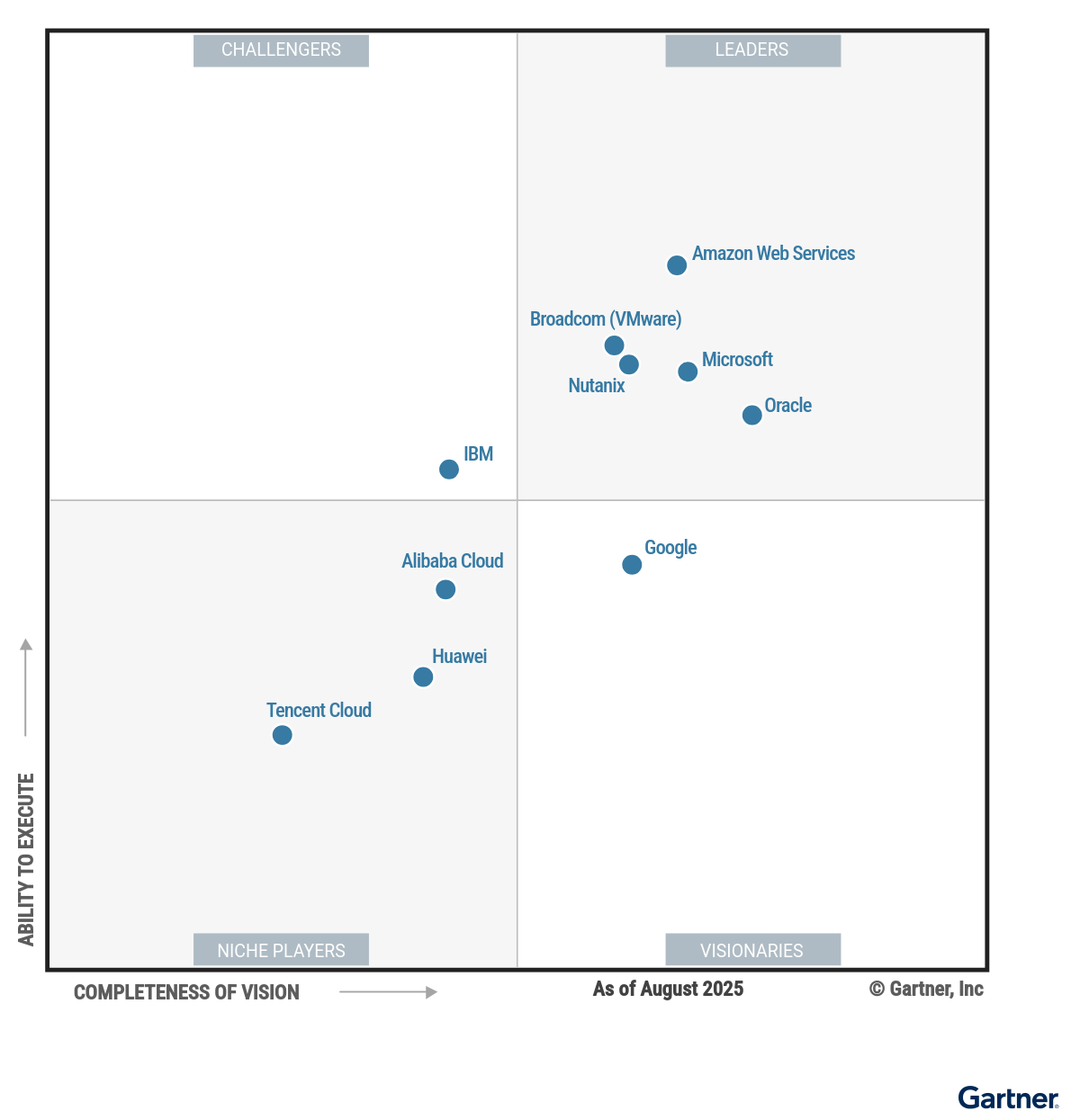

Magic Quadrant

Vendor Strengths and Cautions

Alibaba Cloud

Alibaba Cloud is a Niche Player in this Magic Quadrant. This evaluation focuses on Apsara Stack and Edge Node Service (ENS), available worldwide. Alibaba Cloud also offers CloudBox, a hardware-integrated solution for on-premises deployment, but global availability is limited. All of Alibaba’s DHI products are built on the Apsara architecture of the vendor’s public cloud, offering a unified management console and consistent APIs across cloud, edge and on-premises environments. The vendor serves customers of all sizes, particularly in the finance, utilities and government sectors. Alibaba DHI offerings are global, but mostly deployed in China and Southeast Asia. Over the past year, Alibaba Cloud has added multiple AI capabilities, enabling customers to manage AI infrastructure, data processing, and training and inference workloads at their preferred locations. Alibaba Cloud DHI offerings are best suited for edge, hybrid cloud, AI/ML and sovereign use cases.

- Long-term commitment: Since launching Apsara Stack in 2015, Alibaba Cloud has steadily invested in private and hybrid cloud technologies, enabling it to support hybrid cloud use cases in China and, more recently, across Southeast Asia and other regions.

- Operational efficiency: Alibaba Cloud’s DHI products offer a unified operational platform, enabling both public and private cloud-centric customers to manage resources across cloud, edge, and on-premises environments from a single console.

- AI capabilities: Alibaba Cloud DHI products offer AI/ML tools and platform services, including AI Studio for Apsara Stack, enabling on-premises AI workloads. They also use proprietary Qwen LLM models to enhance operational efficiency with AI assistants.

- High cost of entry: Apsara Stack requires significant upfront investment and resources for private deployment, resulting in high initial costs. Cost efficiency is only realized after reaching a certain scale of usage, making it less suitable for midsize customers looking to replace VMware products with Apsara Stack.

- Market penetration outside of Asia: Despite gaining new customers in the Middle East, Africa and Europe in recent years, Alibaba Cloud’s DHI products still generate the majority of their revenue from China and Southeast Asia.

- Language limitation in global support: Alibaba Cloud DHI’s product interface, support documentation and online customer service functions are available only in Chinese and English.

Amazon Web Services

Amazon Web Services (AWS) is a Leader in this Magic Quadrant. AWS Local Zones bring AWS Cloud Region services to 35 metro areas; AWS Dedicated Local Zones support customer-specified deployments for exclusive use; and AWS Outposts provide fully managed on-premises infrastructure with a subset of AWS services. The Snowball offerings deliver compute and storage in remote or rugged locations with limited connectivity. AWS serves customers of all sizes worldwide across all verticals. Over the past year, the vendor has introduced Amazon EKS Hybrid Nodes for hybrid Kubernetes capabilities, launched second-generation Outposts racks to deliver enhanced performance and networking with Satellite Resiliency, and expanded Local Zones with new S3 storage classes and dedicated AI/ML compute options. AWS DHI offerings are best suited for customers wanting to deploy latency-sensitive and data-sensitive workloads in distributed locations.

- Large deployments: AWS has been selected for large deployments in North America, the Middle East and North Africa, and Latin America, driven by data residency and sovereignty requirements, resulting in multiple Outposts racks and Dedicated Local Zones implementations.

- Wide range of use cases: AWS’s DHI broad portfolio, which spans Local Zones, Dedicated Local Zones, Outposts, Snow offerings and container services (Amazon EKS Hybrid Nodes, Amazon EKS and ECS Anywhere), addresses a wide range of DHI use cases.

- Manageability: AWS DHI solutions such as Outposts are fully managed, with AWS handling delivery, installation, monitoring, updates and patching.

- Lack of awareness: Low awareness of AWS DHI offerings among non-AWS end users means heads of I&O rarely consider Outposts or Local Zones for modernizing on-premises infrastructure.

- Constrained disconnected operations: AWS Outposts now can support up to seven days of disconnected operations, but still has limitations when operated without service link connectivity to AWS Regions.

- Limited service offerings: AWS DHI offerings provide limited services compared with AWS Regions. AWS Outposts and Snow family devices do not offer SLAs.

Broadcom (VMware)

Broadcom (VMware) is a Leader in this Magic Quadrant. This evaluation focuses on its VMware DHI offering, VMware Cloud Foundation (VCF). VCF integrates compute, networking, storage, management and security to provide a platform for VMs and containers across on-premises, partner hyperscale cloud, and edge environments. Over the last year, the vendor introduced live patching for VCF components, automated deployment of management domains, and improved AI/ML workload support. Updates include global deduplication in vSAN Express Storage Architecture (ESA), enhanced data path in NSX, NVMe memory tiering, VPC integration, and vSAN-to-vSAN replication for snapshot-based data protection and recovery. Broadcom serves customers of all sizes and verticals across all geographies with VCF. VCF is a competitive offering for hybrid infrastructure management, edge computing and sovereign workload use cases.

- DHI offering maturity: Broadcom’s DHI solution is consolidated into a single comprehensive product, VCF, which has been in the market for well over five years.

- Widespread expertise: VMware solutions are widely adopted around the world, giving many professionals a strong foundation in VMware and increasing the availability of talent.

- Hybrid cloud traction: VMware was one of the first vendors implementing hybrid cloud deployments, establishing robust partnerships with all major hyperscale public cloud providers and many regional sovereign cloud providers, enabled by VCF license portability.

- License changes: VMware’s transition from perpetual licensing to a subscription-based model, along with recent product restructuring, has resulted in increased costs. This has resulted in a significant number of Gartner clients considering reducing or eliminating their reliance on VCF.

- Lack of communication and support: A growing number of Gartner clients have expressed negative experiences communicating with VMware sales personnel and not receiving prompt support service.

- Limited data services: VMware VCF does not have advanced data services for unstructured data compared to other market leaders.

Google is a Visionary in this Magic Quadrant. Google’s primary DHI solution, Google Distributed Cloud (GDC), includes several deployment options. One is GDC software only, which delivers a Kubernetes experience based on Google Kubernetes Engine (GKE). Another is GDC connected, which supports low-latency edge workloads with connectivity to Google Cloud. The third option is GDC air-gapped, which is designed for highly secure, isolated environments without connectivity to Google Cloud. Google provides centralized global fleet management through a cloud-based console, while also supporting local management capabilities. In the past year, Google has enhanced DHI by extending advanced AI (Gemini, Vertex AI, Agentspace), expanding NVIDIA GPU support, and introducing features like Cross-Cloud Network and GKE fleet management. Google’s DHI solutions serve large enterprises, service providers, and midsize organizations across global markets, focusing on edge use cases in retail and manufacturing, and sovereign deployments in regulated sectors like the public sector and defense.

- Strong AI/ML capabilities: The GDC air-gapped solution is well-positioned to bring Google’s AI stack, including the delivery of its Vertex AI, Gemini, and Gemma models, directly to on-premises and edge locations.

- Sovereign cloud: GDC demonstrates strategic market understanding by rapidly advancing its on-premises AI roadmap and securing major public sector contracts for national sovereign cloud initiatives, and collaborating with both technology companies and global service delivery partners.

- Enhanced security: GDC is built on zero-trust principles, enforcing a default-deny network posture, enabling microsegmentation, and using strong IAM with RBAC and ABAC for secure authentication and authorization across hybrid and air-gapped environments.

- Early DHI maturity: GDC is a relatively new entrant in the hybrid cloud space, and its ecosystem, which includes third-party integrations, partner support, customer references and use-case coverage, is not yet as extensive as those of market leaders.

- Inconsistent hybrid operations: GDC DHI manages VMs differently from Google’s public cloud, using KubeVirt and local control planes, which may require different tools and processes than those used with Google Compute Engine (GCE). GDC connected rack does not support virtual machines.

- Lack of advanced services availability: Google-managed AI capabilities like Gemini and Agentspace are not uniformly available across all GDC offerings and currently are in preview or slated for future releases, limiting immediate deployment.

Huawei

Huawei is a Niche Player in this Magic Quadrant. This evaluation is focused on HUAWEI CLOUD Stack Online (HCSO) and CloudPond, which use the same architecture, services and APIs from Huawei’s public cloud. Huawei also provides HUAWEI CLOUD Stack and FusionCube for on-premises deployment options. Outside China, the vendor continues to grow DHI customers in Southeast Asia, the Middle East, Latin America and Europe, primarily serving midsize to large organizations in the government, financial, manufacturing and carriers sectors. Over the past year, the vendor further enhanced its operation and management platform with LLM argumentation to improve customer satisfaction, and improved its AI workloads running at the edge. Huawei DHI offerings are a good fit for container, AI/ML and sovereignty workloads that span on-premises and edge locations.

- Solution scalability: Huawei DHI products offer flexible, fully managed deployment options across IaaS, PaaS and SaaS, supporting everything from edge setups to large-scale rollouts. This versatility appeals to government, enterprise and telecom customers needing private or sovereign cloud solutions.

- Telecom proficiency and partner networks: Huawei’s expertise in low-latency networks, supported by long-standing global carrier partnerships, enriches the hybrid cloud experience and drives customer growth.

- End-to-end solution: Huawei offers a self-developed hardware and software DHI solution, significantly improving deployment, operations and cost efficiency.

- Supply chain constraints: U.S. sanctions on Huawei continue to affect its global supply chain and ecosystem development, leading to concerns among prospective customers and, in some cases, limiting its consideration as an option in the global market.

- NVIDIA AI compatibility issue: Huawei DHI solutions lack support for the NVIDIA-based ecosystem when customers choose hardware-integrated solutions.

- Lack of transparency: Publicly available information on Huawei’s DHI products is relatively limited. Key details are lacking, such as hardware compatibility lists, user manuals and the regions where services are available.

IBM

IBM is a Challenger in this Magic Quadrant. This evaluation focuses on its IBM Cloud Satellite hybrid cloud management solution, IBM Fusion HCI System, and Red Hat OpenShift Virtualization, which supports containers and virtual machines. IBM also provides the Power Virtual Server and Power Private Cloud deployment options. IBM is a global provider, and its clients tend to be large and midsize enterprises across all verticals. Since last year, IBM has added content-aware storage to enhance retrieval-augmented generation (RAG) capabilities, as well as Fusion Control Tower, which enables the management of containerized, virtualized and AI applications from a single control plane. IBM’s DHI offering is well-suited for AI workloads and container deployments.

- IBM Power Virtual Server: IBM provides its IBM Power customers with a cloud-like experience for their Power workloads. IBM Power Virtual Server (PowerVS) and IBM PowerVS Private Cloud enable customers to run applications on IBM Power-based logical partitions on IBM Cloud or in the customer’s data center.

- Strong AI/ML integration: IBM is integrating AI/ML through its range of solutions, adding watsonx data support and additional NVIDIA GPUs to Fusion HCI, Red Hat AI platforms and its own Granite models, as well as inference support on IBM Power systems.

- Comprehensive vertical support: IBM delivers cloud solutions tailored for regulated industries, such as financial services and healthcare, through IBM consulting, removing the need for additional system integrators and providing a single contract to the end user.

- Loosely integrated portfolio: IBM has a broad portfolio of products, but they are not tightly integrated. Navigating the portfolio’s different interfaces and required skillsets remains complex.

- Virtualization support: IBM’s DHI product offerings continue to leverage Red Hat OpenShift Virtualization to support management of x86 virtual machines. It is still a relatively new technology and is not as proven for running large-scale production workloads and implementations.

- Networking limitations: Unlike every other vendor in this Magic Quadrant, IBM does not support IPv6 addressing and routing in all of its DHI offerings.

Microsoft

Microsoft is a Leader in this Magic Quadrant. In late 2024, Microsoft replaced Azure Stack HCI with Azure Local. This evaluation focuses on Azure Local and Azure Arc. Azure Local is a hyperconverged solution that can be managed at customer locations using the Azure Arc framework. The latter provides a unified way to manage customer environments and extends the Azure platform to on-premises, multicloud and edge environments. Microsoft’s DHI vertical market targets encompass a wide array of organizations and industries; the provider’s top priorities include manufacturing/industrial and retail across all business sizes. Over the past year, Microsoft has added AI services on Azure Local, enabling generative AI and ML at the edge; an Azure Arc multicloud connector for AWS; and the deployment of AI models on Azure-Arc-enabled Kubernetes. Microsoft DHI is best-suited for multicloud, hybrid infrastructure management and edge use cases.

- Centralized management plane: The combination of Azure Local and Azure Arc enables centralized control, life cycle automation, and visibility across distributed infrastructure assets, including VMs, Kubernetes clusters and databases, regardless of where they are hosted.

- Brand recognition: Both Microsoft and Azure together have brand names that are known for their on-premises-to-cloud solutions and services that span much of the globe, and have licensing that is attractive to many vertical markets. This makes them a natural shortlist candidate for customers seeking a DHI solution.

- Familiarity with Azure: For customers familiar with or moving to Azure as their preferred cloud provider, the Microsoft DHI solution allows them to use the Azure services and management capabilities, tools, APIs, and SDKs as if their resources are running directly in Azure.

- Product depth: Azure Local does not have a breadth of offerings that cover a significant range of DHI use cases, such as large on-premises deployments or lightweight edge.

- Integration concerns: Some customers have indicated that assembling a comprehensive, unified solution from multiple Microsoft products requires significant effort compared with employing a single-stack solution. In addition, some Gartner clients have reported postinstallation instability.

- Limited disconnected operations: While Azure Local can run disconnected for 72 hours, the capability to remain disconnected and air-gapped for longer periods is currently only in public preview.

Nutanix

Nutanix is a Leader in this Magic Quadrant. This evaluation focuses on Nutanix Cloud Platform (NCP), which is a unified, software-defined hybrid cloud platform designed for centralized management of applications and data across various environments. Nutanix is a global provider, with its focus primarily on large enterprise customers. Public sector, financial services and healthcare are Nutanix’s primary verticals focus. Over the past 12 months, Nutanix added support for Dell PowerFlex and Pure Storage FlashArray over NVMe/TCP, as well as Cloud Native AOS, a software solution that extends Nutanix’s enterprise storage and data services to Kubernetes and cloud-native bare-metal environments. It also introduced Nutanix Enterprise AI (NAI), a centralized inferencing platform for deploying and managing a wide range of generative AI models and inference endpoints securely. NCP is suited to sovereign workloads, hybrid infrastructure management and edge multicloud use cases.

- Comprehensive single product: NCP is the sole unified Nutanix DHI offering. This provides a single-stack hybrid cloud solution that includes a viable hypervisor alternative to VMware ESXi. This single-stack approach delivers an integrated DHI solution, thereby avoiding the undesired complexity related to integrating multiple offerings.

- Operational consistency: Nutanix Cloud platform provides an identical operational model for applications and data, whether they are deployed at edge locations, in private data centers, or across major public clouds like AWS, Azure and Google Cloud.

- Advanced data services: NCP incorporates a scale-out distributed storage architecture with comprehensive data services, including snapshots, disaster recovery and encryption.

- Limited cloud-first traction: Nutanix has not created significant sales traction with DHI prospects who have a “cloud-first” mentality and consider cloud providers as being the innovators in this market. This causes those prospects to avoid considering Nutanix Cloud Platform as a potential DHI solution.

- Negative price perception: Nutanix has never been positioned as a low-price leader, and some prospective customers may choose other lower-priced options.

- Small company size: Some Gartner clients have indicated that they have not chosen Nutanix because of the vendor’s size, believing that larger-scale providers in the DHI space present less risk.

Oracle

Oracle is a Leader in this Magic Quadrant. This evaluation focuses on Oracle Cloud Infrastructure (OCI) Dedicated Region, Oracle Alloy, Oracle Compute Cloud@Customer, Oracle Roving Edge Infrastructure and Oracle’s multicloud services. The core capability of Oracle in this market is its ability to provide the full scope of OCI public cloud services on-premises, for partners to deliver, or in other public clouds. Oracle is a global provider and its DHI customers tend to be large enterprises with significant investments in other Oracle products.

Oracle’s DHI solutions serve a broad range of industries, including government, financial services and telecom providers. Over the past year, Oracle has added Dedicated Region25, which enables a full OCI cloud region in three racks, as well as GPU expansions for OCI Dedicated regions and Oracle Alloy. Oracle’s DHI solution is suitable for users with data sovereignty or local deployment requirements and users who need access to Oracle Database services in a multicloud environment.

- Sovereign operations: Oracle provides a wide variety of sovereign options that deliver the full scope of cloud services for dedicated, sovereign and partner-operated regions. This provides a choice for customers under strict regulatory and data privacy laws.

- Enhanced networking for AI: OCI is built on a high-speed, RDMA-based network that is well-suited to AI-style applications. This architecture is replicated in its DHI products, enabling sovereign AI solutions.

- Strong multicloud support: Oracle embeds its own Exadata-based managed database services directly into selected regions of Microsoft Azure, AWS and Google Cloud (GCP), and provides high-performance, direct-connect networking links with no additional egress fees to Azure and GCP.

- Limited brand awareness: OCI is not yet automatically considered by prospective DHI customers unless they are already invested in Oracle Exadata implementations.

- Lacks a native GenAI model: OCI is focused on delivering large-scale compute services for AI model builders and partnerships with high-profile AI companies to deliver industry-leading models. If OCI falls behind on its technical capabilities, it risks losing these customers, who are driving large capital investments.

- Perception concerns: Gartner clients have raised concerns regarding Oracle’s historic behavior and, recently, the denials and delays in disclosure of the breach of Oracle Cloud Classic.

Tencent Cloud

Tencent Cloud is a Niche Player in this Magic Quadrant. This evaluation is focused on Cloud Dedicated Cluster (CDC) and Cloud Dedicated Zone (CDZ). These are distributed cloud solutions that extend public cloud solutions to on-premises and edge locations. The vendor also offers Tencent Cloud Enterprise as a private cloud solution, and Tencent Cloud-native Suite (TCS) for container management and GPU orchestration. Tencent Cloud’s DHI offerings provide private and hybrid cloud solutions for large traditional enterprises in China, and also support Chinese businesses expanding abroad in the internet, manufacturing and finance sectors. Over the past year, the vendor has improved resilience capability and added AI inference on the edge into its DHI products. Tencent Cloud DHI is suitable for edge, hybrid and sovereign workloads.

- Investment commitment: Tencent Cloud has invested in DHI products in recent years, with a focus on reducing both customer operational efforts and network latency through DHI solutions, as well as optimizing upfront investment requirements for Tencent Cloud Enterprise products.

- Infrastructure-neutral: Tencent Cloud Enterprise and the TCS solution can operate on customers’ existing infrastructure, provided it meets the minimum configuration requirements. This makes it a practical option for customers who prefer to reuse their current infrastructure for the technology solution replacement.

- Consistent experience: As an extension from public cloud, Tencent Cloud delivers CDC and CDZ products to the customer’s desired location. CDZ has the same cloud product as Tencent’s public cloud. This DHI solution uses a public cloud management console to maintain a consistent customer operational experience.

- Limited public cloud footprint: Tencent Cloud’s CDC and CDZ products are available only in regions where Tencent’s public cloud is present. The limited public cloud global footprint restricts the expansion of Tencent’s DHI offerings.

- Lack of momentum outside of China: Most of Tencent Cloud DHI’s revenue comes from China, while overseas revenue is mainly driven by Chinese enterprises expanding abroad. Tencent Cloud lacks clear customer and planning strategies for DHI products across different regions and industries.

- Redundant features: Some of Tencent Cloud’s DHI offerings have redundant features and the company lacks a unified design strategy across its DHI product portfolio.

Inclusion and Exclusion Criteria

Inclusion Criteria

To qualify for inclusion, providers:

- Must sell a DHI offering aligning to the DHI market definition. All mandatory features must be generally available as of 1 May 2025.

- Must show evidence of 60 enterprise customers deploying products in distributed hybrid infrastructure scenarios or must have reported over $50 million in ARR contract value as of 1 May 2025.

- Must show evidence that all DHI production customer deployments are across on-premises and at least one hyperscale strategic public cloud environment (see Magic Quadrant for Strategic Cloud Platform Services). For hyperscale cloud providers, there should be evidence of on-premises or edge DHI deployment and software providers or full-stack HCI vendors, as well as evidence of the deployment of a DHI offering in the hyperscale strategic public cloud.

- Must have at least 10 production customers per region in on-premises data centers in at least four out of seven global regions (North America, Europe, Asia/Pacific [excluding China], Latin America, China, Middle East and Africa).

- Must have the following business capabilities:

- Be the primary developer and IP owner of the software components of DHI (control plane and hypervisor), with an exception of open-source-based products. If any part of the technology is based on open source, the vendor should be one of the top 10 open-source project contributors.

- Have 24/7 DHI customer support (including phone support). There must be an English-language localization of the contract, service portal, documentation and support.

- Have a managed service minimum DHI availability of not lower than 99.9%.

- Must have these technical capabilities relevant to Gartner clients:

- Ability to deploy and operate the DHI where the customer prefers, including on-premises, at the edge or colocated.

- Ability to deploy and operate the DHI in one or more hyperscale public clouds.

- Vendor-developed DHI control plane that provides a secure, automated and integrated capability for onboarding, operating, life cycle management of infrastructure and supporting the distributed infrastructure across on-prem and in the public cloud..

- Ability to address four out of six use cases defined in the companion Critical Capabilities research.

Exclusion Criteria

Offerings are excluded from this Magic Quadrant if they are exclusively marketed and sold as container management infrastructure products and can’t accommodate virtual machine infrastructure. In addition, offerings are excluded that do not have an ability to deploy full DHI services in the hyperscale public cloud.

Honorable Mentions

Gartner tracks more than 20 vendors in this market. Nine vendors met the inclusion criteria for this Magic Quadrant, but the exclusion of a vendor does not mean that the vendor and its products lack viability. Following are two noteworthy vendors that did not meet all the inclusion criteria for distributed hybrid capabilities, customer numbers and regional requirements, but could still be suitable for clients, depending on their specific deployment patterns.

Red Hat: Red Hat OpenShift, in conjunction with OpenShift Virtualization, forms a cohesive solution that merges the capabilities of containers and virtual machines within a unified platform. This software-defined solution offers deployment flexibility, extending its reach to various customer-preferred locations, such as the edge, public cloud or data center environments.

SUSE: SUSE Virtualization (based on the open-source Harvester project) is SUSE’s HCI solution based on Kubernetes and KVM technologies, extending Rancher’s enterprise container management platform with virtualization management. SUSE Virtualization operates on bare metal and offers integrated virtualization and storage, supporting both virtual machines and containerized environments. When used together, Rancher and SUSE Virtualization streamline Kubernetes cluster management with multicluster control and flexible infrastructure support in the data center that can also extend to edge locations for practical application modernization.

Evaluation Criteria

The Ability to Execute criteria for this Magic Quadrant are as follows:

Product or service: This criterion covers the assessment of vendor capabilities to deliver and differentiate features and functionality supporting most market use cases, diversification of customer use across the vendor’s portfolio and the scope of issues impacting customer experience.

Overall viability: This criterion covers the assessment of a vendor’s key financial, staffing and customer base growth metrics.

Sales execution/pricing: This criterion covers the assessment of a vendor’s success in the market. Considerations include results of new versus repeat business, growth of new DHI customers and changes in customer investments. Adaptations to sales and presales efforts and levels of pricing transparency are also considered.

Market responsiveness/record: This criterion evaluates the vendor’s ability to deliver DHI products and capabilities that are first-to-market and differentiating compared to the competition, while also continuing to meet market demands and gaps in their portfolio.

Marketing execution: This criterion evaluates the vendor’s ability to create mind share, expand to new markets and build a sales pipeline in the DHI market.

Customer experience: This criterion assesses the vendor’s ability to demonstrate ongoing client satisfaction, implement improvements and offer distinctive customer support capabilities. This also focuses on how the vendor is perceived in the market, and how well its marketing programs are recognized. The evaluation focuses on how well the vendor is able to influence and shape perception in the market through marketing activities and thought leadership that drives awareness. An additional indicator for this criterion is how often Gartner clients inquire about a specific vendor in terms of capabilities/reputation or in a shortlist evaluation process.

Operations: This criterion looks at the ability of the vendor to meet goals and commitments. Factors include quality of the organizational structure, skills and relationships, and the vendor’s ability to meet SLAs. Considerations include partnerships with other technology providers, outages that affect customers and SLA adherence.

Ability to Execute

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | High |

Sales Execution/Pricing | High |

Market Responsiveness/Record | Medium |

Marketing Execution | Low |

Customer Experience | High |

Operations | Low |

Source: Gartner (September 2025)

Completeness of Vision

The Completeness of Vision criteria for this Magic Quadrant are as follows:

Market understanding: This criterion evaluates the ability of the vendor to understand customer requirements, align those requirements to its products and services, and evolve its product vision, based on its own established perspectives of the market’s direction.

Marketing strategy: This criterion evaluates the clarity of the vendor’s marketing vision that highlights competitive differentiation and an understanding of personas engaged in solution selection.

Sales strategy: This criterion evaluates the vendor’s ability to establish and update a sales strategy that aligns with company goals and customer interest. Factors also include the vendor’s ability to reach customers directly and expand coverage through its network of partners.

Offering (product) strategy: This criterion evaluates the vendor’s product planning, emphasizing its alignment to shortcomings, commitment to differentiation and improvement of existing capabilities.

Business model: This criterion evaluates the vendor’s strategies to sustain its business in the market.

Vertical/industry strategy: This criterion evaluates the vendor’s strategy to direct its product offerings, its alignment with industry-specific technology providers and its resources to meet specific vertical market requirements.

Innovation: This evaluates the plans to bring future differentiated capabilities to market that will enhance the vendor’s ability to interact with customers and drive business. This criterion evaluates the vendor’s strategy for reinvestment and its differentiating innovations in product design and capabilities, introduction of new technologies, third-party partner relationships, integration, and overall differentiation in the DHI market.

Geographic strategy: This criterion evaluates the vendor’s strategy to direct resources, skills and product offerings to meet needs across most major geographies.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Medium |

Sales Strategy | Medium |

Offering (Product) Strategy | High |

Business Model | Medium |

Vertical/Industry Strategy | Low |

Innovation | High |

Geographic Strategy | Medium |

Source: Gartner (September 2025)

Quadrant Descriptions

Leaders

Leaders distinguish themselves by offering a service suitable for strategic adoption and having an ambitious roadmap. They can serve a broad range of use cases. However, they do not excel in all areas, may not necessarily be the best providers for a specific need and may not serve some use cases at all. Leaders in this market have appreciable market share and many referenceable customers supporting multiple geographies, verticals and deployment models.

Challengers

Challengers are well-positioned to serve some current market needs. They deliver a good service that is targeted at a particular set of use cases, and they have a track record of successful delivery. However, they might not adapt to market challenges quickly enough or do not have a broad scope of ambition. These vendors have the potential to establish themselves across the broader global market, but have not yet done so.

Visionaries

Visionaries are typically vendors that focus on strong innovation and product differentiation, with the potential to significantly disrupt the market if execution improves. Their services are still emerging, and they have many capabilities in development that are not yet generally available. Although they may have many customers, they might not yet serve a broad range of use cases well or may have a limited geographic scope.

Niche Players

Niche Players in the DHI market may be excellent providers for particular use cases or in regions where they operate, but they should ultimately be viewed as specialist providers. They often do not serve a broad range of use cases, deployment models or customer segments, or have a broadly ambitious roadmap. Some may have solid leadership positions in markets adjacent to this market, but have developed only limited global DHI capabilities.

Context

Heads of I&O aspire to modernize their IT infrastructure through the integration of innovative technologies, while embracing the principles of cloud-native platform engineering. Heads of I&O embarking on the journey of DHI that spans on-premises, cloud and edge domains should consider the following recommendations:

- Strategic direction: Craft a comprehensive hybrid platform strategy that aligns with their organization’s long-term objectives, integrating on-premises, cloud and edge components cohesively.

- Use case, workload analysis and prioritization: Conduct an in-depth analysis of their workloads and applications. Review their needs and applicability for a DHI platform, and analyze performance, capacity metrics, SLAs and data requirements specific to each environment.

- Strategic vendor collaborations: Forge partnerships with DHI vendors offering unified solutions across the spectrum of on-premises, cloud and edge, ensuring full-stack infrastructure alignment and DHI solution applicability for the majority of use cases.

- Security and regulatory compliance: Implement robust security evaluation for DHI solutions, taking into account their unique requirements for data sovereignty, compliance, and access controls to ensure both agility and security.

- Leveraging edge advantages: Harness the capabilities of DHI edge solutions to streamline latency-sensitive tasks, elevating performance and delivering enhanced user experiences at the source by enabling centralized management and standardized solution delivery.

- Resource management: Evaluate DHI control plane resource management and orchestration tools that enable hybrid cloud management across all deployment domains. Pay special attention to integration with existing systems and the capability to create infrastructure as code by leveraging available DHI management APIs.

- Comprehensive testing and validation: Prioritize comprehensive testing and validation of their distributed hybrid setup, identifying and addressing potential performance bottlenecks, integration and operational intricacies. Pay special attention to the ability for the DHI solution to function disconnected from the cloud control plane.

By embracing these recommendations, heads of I&O can confidently steer their organizations through the intricacies of distributed hybrid infrastructure, seamlessly integrating on-premises, cloud, and edge environments to drive operational excellence and strategic success.

Market Overview

The distributed hybrid infrastructure (DHI) market was formed to address the needs of heads of I&O to deploy standardized infrastructure platforms for any deployment scenario. DHI solutions attract customers who want a cloud IaaS solution without PaaS. This includes compute, whether based on virtual machines, bare metal or containers; storage; and network services. DHI can be deployed where the customer prefers, whether on-premises, in the public cloud or on the edge.

The DHI market has emerged at the convergence of two trends: the adoption of distributed cloud solutions, extending public cloud services to noncloud environments; and the deployment of full-stack software-defined platforms or hyperconverged solutions in public cloud environments.

In this evolving market scenario, organizations are strategically recalibrating their approach, considering a diverse range of options at their disposal. Cloud-inspired on-premises solutions offer a compelling distributed hybrid infrastructure avenue. Currently, these software solutions, which facilitate smooth integration with existing infrastructures, are being deployed on public clouds, contributing to the development of robust hybrid cloud architectures. This hybrid framework facilitates centralized control across an array of environments, encompassing on-premises, public cloud and edge infrastructure. The inherent orchestration and management capabilities of these solutions address the intricate operational needs of modern businesses.

Simultaneously, the assessment extends to the realm of distributed public cloud IaaS. Innovative solutions from all hyperscale public cloud providers are redefining boundaries, extending the reach of public cloud services. By venturing beyond conventional limits, these solutions empower organizations to deploy public cloud services in diverse, noncloud locations. This decentralized approach aligns with the escalating demand for computing resources that are both decentralized and centrally controlled.

The market’s defining attributes revolve around the distribution of the entire infrastructure stack, highlighting an emphasis on centralized control and comprehensive management across an array of diverse infrastructure environments. This landscape also encompasses pivotal hybrid functionality, facilitating seamless deployment across on-premises, public cloud and edge infrastructure domains.

Heads of I&O have a growing strategic interest in sovereign cloud capabilities, and DHI has emerged as a key enabler in delivering them. Sovereign cloud demands local control over data, infrastructure, and operations to meet national security and compliance requirements. DHI enables this by supporting cloud-like deployments within national borders, across on-premises, public cloud and edge environments.

With centralized orchestration and policy enforcement, DHI ensures consistent governance and security across distributed infrastructure. It allows organizations to maintain data residency while leveraging modern cloud capabilities. Integration with local providers and regulatory frameworks further strengthens its role in sovereign cloud delivery.

Recently, special emphasis has been on the ability to rely on DHI products to enable AI-capable infrastructure delivery. AI workloads require flexible, high-performance environments that can handle intensive compute, large datasets and real-time processing.

DHI enables organizations to run AI training on powerful compute platforms and inference close to data sources, improving efficiency and reducing latency. It also tackles data gravity by allowing compute to operate near the data, minimizing transfer costs and supporting compliance.

Centralized orchestration simplifies the complexity of managing distributed AI models, offering unified control, life cycle management and scalability. DHI platforms also integrate AI-specific hardware and frameworks, streamlining deployment and performance optimization.

In short, DHI provides the infrastructure agility and intelligence needed to support AI at scale, making it a strategic enabler for modern enterprises.

Vendor placement on the Magic Quadrant for Distributed Hybrid Infrastructure is based on Gartner’s view of a vendor’s performance against the criteria noted in this research. In addition, placement is heavily influenced by more than 1,200 Gartner client inquiries and one-on-one meetings regarding distributed hybrid cloud solutions, end-user surveys, Gartner conference kiosk surveys, Gartner conference session polling data, Gartner Research Circle polls, and Gartner Peer Insights.

The included vendors submitted comprehensive responses to Gartner’s Magic Quadrant survey on this topic, which were used as the basis for subsequent vendor briefings and follow-up meetings, product demonstrations and correspondence.

Additionally, this research drew input from other Gartner analysts, industry contacts and public sources, such as U.S. Securities and Exchange Commission filings, as well as articles, speeches, published papers and public domain videos.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.