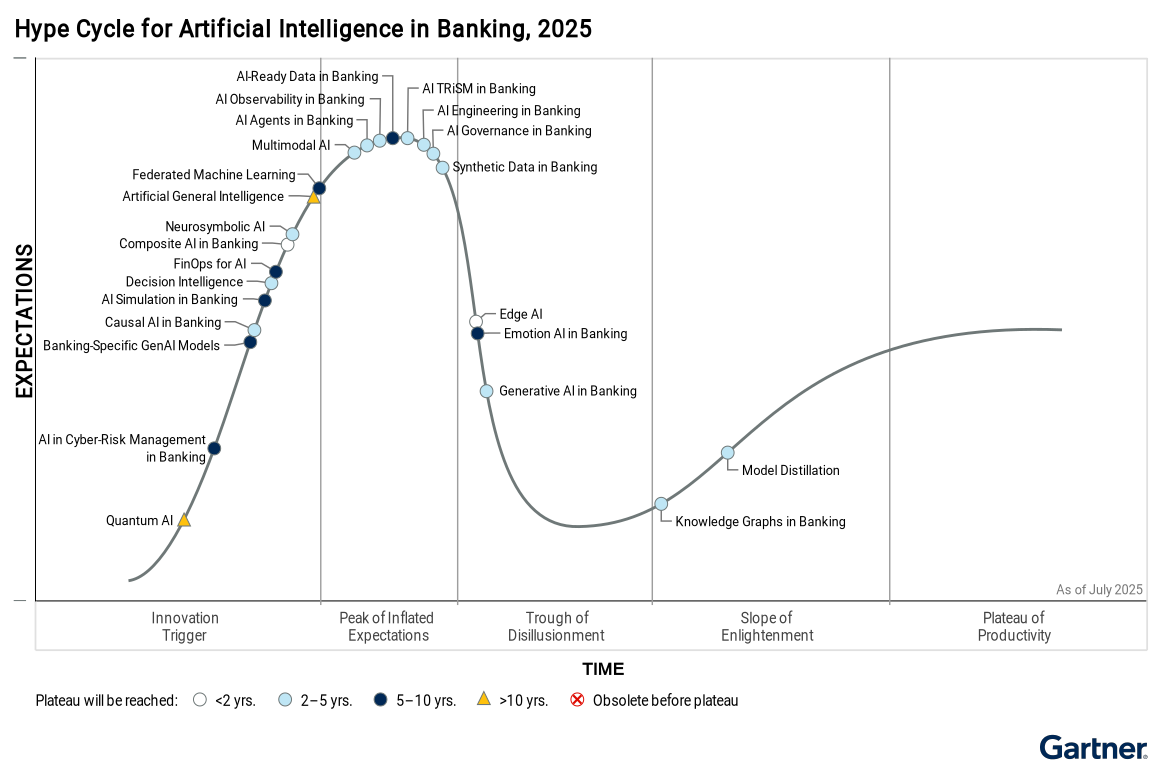

Hype Cycle for Artificial Intelligence in Banking, 2025

ARCHIVED

9 July 2025 - ID G00831999 - 105 min readBy Jasleen Kaur Sindhu

Banks are investing in AI deployment and governance to boost revenue, streamline operations, manage risk and enhance customer experience. This Hype Cycle helps banking CIOs identify high-impact AI trends and prioritize those with the most potential for near-term strategic gains.

Analysis

What You Need to Know

AI adoption continues to accelerate in banking, with 77% of banking CIOs reporting active or planned AI deployments in the current year, according to the 2025 Gartner CIO and Technology Executive Survey. As the broader AI landscape shifts from experimentation to scalable implementation, banks are also moving beyond pilots to embed AI into core operations.

This year’s Hype Cycle reflects a maturing understanding of AI’s potential and limitations. Generative AI (GenAI), while still prominent, is no longer the sole focus. Instead, attention is expanding to foundational enablers like AI-ready data, AI engineering, and AI governance — all critical for sustainable, scalable AI in banking. These shifts mirror broader industry trends, where GenAI has entered the Trough of Disillusionment, and the spotlight is now on operational readiness and responsible deployment.

For banks, this means a strategic pivot from chasing hype to building resilient AI ecosystems. Innovations such as AI agents, composite AI, and multimodal AI are gaining traction, but their success depends on robust data infrastructure, governance, and cost management — areas where banking CIOs must lead with discipline.

New entries like AI observability, FinOps for AI, and banking-specific GenAI models underscore the sector’s focus on transparency, financial efficiency, and domain-specific intelligence. Meanwhile, long-term innovations like quantum AI and artificial general intelligence (AGI) remain on the horizon, offering potential but requiring cautious, long-term investment strategies.

To stay competitive, banks must align AI initiatives with business outcomes, prioritize innovations with near-term value, and invest in the capabilities that will enable AI to scale responsibly and effectively across the enterprise.

The Hype Cycle

This Hype Cycle explores four critical themes essential for banking CIOs to maximize returns from their AI investments. These themes are:

AI foundational elements in banking: Includes the prerequisites necessary for successful AI implementation in banking, including underlying data preparation, engineering practices, computational approaches and cost management strategies. Relevant innovations are:

- AI engineering in banking

- AI-ready data in banking

- Banking-specific GenAI models

- Edge AI

- Federated machine learning

- FinOps for AI

- Multimodal AI

- Synthetic data in banking

Advanced AI techniques and capabilities in banking: Explores current and emerging AI techniques, capabilities and computational approaches that help with development of intelligent systems and processes in banking. Relevant innovations are:

- AI agents in banking

- Artificial general intelligence

- Composite AI in banking

- Generative AI in banking

- Knowledge graphs in banking

- Model distillation

- Neurosymbolic AI

- Quantum AI

Applied AI functionalities in banking: Focuses on the orchestration of multiple advanced AI techniques and capabilities to create new, human-centric functionalities and experiences in banking. These innovations enable intelligent simulations, emotion-aware interactions, advanced decision intelligence, and new approaches for cyber-risk security. Relevant innovations are:

- AI simulation in banking

- AI in cyber-risk security for banking

- Causal AI in banking

- Decision intelligence

- Emotion AI in banking

Responsible and ethical AI in banking: Focuses on ensuring AI systems are transparent, accountable and aligned with ethical standards. This involves managing risks, maintaining system observability and establishing governance structures to guide AI use in banking. Relevant innovations on this Hype Cycle are:

- AI governance in banking

- AI observability in banking

- AI TRiSM in banking

The Priority Matrix

The Priority Matrix is a companion to the Hype Cycle. It seeks to communicate some key attributes contained within the Hype Cycle, namely:

- How much value could an organization realize from the effective implementation of a particular technology?

- When will the technology be mature enough to help deliver expected value?

Two features of this Hype Cycle stand out:

- Almost all the innovations, except for Quantum AI, are high-benefit or transformational.

- Almost half of the featured innovations are expected to reach the Plateau of Productivity in five years or less. Artificial general intelligence (AGI) and quantum AI are the only two entries expected to take more than 10 years to reach mainstream adoption.

High-benefit innovations bring business efficiencies, but require ongoing training and education. Similarly, transformational innovations are game changers, but they require new skills and present high risk and reward.

To achieve practical efficiencies, it is crucial to prioritize innovations expected to achieve mainstream adoption within the next two to five years. Notable examples include the application of GenAI and AI agents, alongside robust AI governance and AI observability solutions.

It is important to recognize that, within the banking sector’s AI Hype Cycle, many innovations are currently at the Peak of Inflated Expectations. As such, banking CIOs must remain vigilant, continuously benchmarking their efforts against market developments to avoid being swept up in the prevailing hype. Investments should be grounded in a clear assessment of which innovations are most likely to deliver strategic or financial value in the context of their organization.

Quantum AI is also noteworthy. Although it is expected to take over a decade to reach mainstream adoption, it offers a unique competitive edge for banks. As validated techniques mature, quantum AI will provide distinct advantages across various industries. Specifically in banking, it will benefit use cases such as portfolio optimization, customer experience enhancement, and fraud prevention.

Artificial general intelligence (AGI) is another innovation expected to take more than a decade to achieve mainstream adoption. In the short term, banking CIOs should remain cautious of the hype surrounding AGI, which often fuels fears and unrealistic expectations about the current capabilities of AI. In the long term, AI capabilities will continue to evolve, with or without AGI, influencing banks through developments such as the emergence of machine customers and autonomous business operations.

Priority Matrix for Artificial Intelligence in Banking, 2025

| Benefit | Years to Mainstream Adoption | |||

|---|---|---|---|---|

| Less Than 2 Years | 2 to 5 Years | 5 to 10 Years | More Than 10 Years | |

Transformational | ||||

High | ||||

Moderate | ||||

Low | ||||

Source: Gartner (July 2025)

On the Rise

Quantum AI

Analysis By: Chirag Dekate, Soyeb Barot

Benefit Rating: Low

Market Penetration: Less than 1% of target audience

Maturity: Embryonic

Definition:

Quantum AI is an embryonic field of research emerging at the intersection of quantum technologies and AI. Quantum AI aims to exploit unique properties of quantum mechanics to develop new and more powerful AI algorithms that deliver better than classical performance, potentially resulting in new types of AI algorithms designed to run on quantum systems.

Why This Is Important

Quantum AI is an area of active research. Once commercialized, quantum AI could potentially help in:

- Enabling organizations to use quantum systems to address advanced AI analytics faster while using a fraction of the resources used in conventional AI supercomputing.

- Developing new AI algorithms that exploit quantum mechanics to deliver capabilities beyond ones that can be executed on classical systems.

- Unlocking disruptive applications that include drug discovery, energy industry and logistics.

Business Impact

While the business impact of the embryonic quantum AI field today is low, when validated techniques mature, quantum AI will enable competitive advantage across industries; for instance:

- Life sciences: Transform drug discovery by shortening timelines, lowering costs and improving outcomes.

- Finance: Optimize portfolios, minimize risk and improve fraud detection systems.

- Material science: Revolutionize energy transportation, manufacturing and create new revenue streams by discovering new materials.

Drivers

- Progress is steady in scaling quantum systems and improving error correction schemes.

- Hype around quantum technologies is driving more businesses and researchers to explore the intersection of quantum and AI.

- The accelerated pace of innovation in quantum systems (including a larger volume of higher quality qubits, and greater stability and reliability of quantum systems) is driving greater interest in applicability in areas, including quantum AI.

- Access to quantum computing as a service is lowering the barrier to entry, encouraging greater collaboration among researchers and enabling exploration of new algorithms and techniques.

- Governments and enterprises globally are increasing funding for quantum (and quantum AI) research, resulting in accelerated innovation.

- The halo effect of increased hype around GenAI is driving new focus on alternative research techniques, including quantum AI, that could potentially deliver new disruptive results.

- Universities and training programs are developing programs and curricula to develop a quantum-ready workforce.

Obstacles

- Hardware limitations: Current quantum systems, while getting stabler, are still error-prone and inherently noisy, limiting their utility and impact on practical quantum AI.

- Algorithm limitations: While several quantum AI algorithms have been proposed, very few have been vetted and proven, and they are nowhere close to being enterprise-ready.

- Cost: Despite their limited utility and widespread accessibility, rapidly evolving noisy intermediate-scale quantum (NISQ) systems are relatively expensive, which could inhibit research and development efforts needed to devise quantum AI algorithms.

- Scalability of systems: Scaling quantum systems to the level necessary for enterprise-ready quantum AI continues to be a major technical hurdle.

- Compute paradigms: Integrating traditional data and analytics pipelines with quantum is inherently challenging because quantum systems operate on a fundamentally different paradigm both from a data representation perspective and from a compute (non-von Neumann model) perspective.

User Recommendations

- Prioritize investments in AI and GenAI over any quantum AI investments. Quantum AI is too nascent to warrant focused investments and unlikely to yield material gains in the next two to three years.

- Partner with local universities by sponsoring academic research as a means of derisking your quantum AI investments and create a university-to-industry talent pipeline.

- Create a quantum AI opportunity radar that enables you to track progress of underlying technologies and quantum AI algorithms, enabling you to maximize value creation as the embryonic field of quantum technologies evolves.

- Diversify quantum use cases beyond a narrow AI context into other domains including materials simulations, search, optimization and other emerging algorithmic domains.

Sample Vendors

Amazon Web Services; Google; IBM; IonQ; Microsoft; Multiverse Computing; Pasqal; SandboxAQ

Gartner Recommended Reading

AI in Cyber-Risk Management in Banking

Analysis By: Lopa Sinha

Benefit Rating: Transformational

Market Penetration: 1% to 5% of target audience

Maturity: Emerging

Definition:

AI in cyber-risk management optimizes processes by analyzing data and providing predictive insights for real-time decision making. AI in cyber-risk management in banking enhances control implementation, identifies deficiencies and scales risk monitoring through automated compliance validation and issue detection.

Why This Is Important

AI in cyber-risk management in banking can:

- Analyze banking data such as transactions to flag suspicious activities, thus minimizing financial losses.

- Ensure adherence to law by mapping controls, automating checks and flagging noncompliance.

- Predict potential vulnerabilities or attack patterns based on historical data and emerging trends.

- Automate routine processes, risk management and incident responses.

- Support applications such as AI agents to orchestrate policy drafts and risk assessment.

Business Impact

With digital transformation, banks generate massive amounts of data across transactions, user sessions and third-party and cloud services. AI reduces dependency on manual operation while increasing effectiveness of security operation. AI also helps stress-test the resilience of critical banking processes by simulating attack paths and proactively identifying business impact. By parsing and correlating millions of events in real time, it enables banks to build automated incident management processes.

Drivers

AI transforms cybersecurity risk management in banking from static, reactive and siloed processes into data-driven, time-sensitive and integrated defenses, and it enables these drivers:

- The increasing prevalence of advanced and AI-powered cyberthreats, including advanced persistent threats (APTs), AI-powered phishing and sophisticated malware, is a primary driver compelling banks to adopt AI for real-time threat detection and response.

- Improvements in the accessibility and applicability of AI and GenAI technology are making these solutions more practical for banking institutions to deploy.

- The necessity for enhanced detection and prevention capabilities across various security domains, such as behavior analytics to identify fraud and insider threats and facilitate adaptive access and authentication, is driving AI adoption.

- The need exists to improve security operations efficiency and effectiveness by enabling security operations center (SOC) teams to prioritize critical alerts. Another improvement approach is to enhance the prioritization and risk scoring of open and self-identified issues to effectively manage cyber risk. Both of these drive the leveraging of capabilities potentially enhanced by AI.

- Strategic forecasting and resource allocation in cybersecurity budgeting, utilizing predictive analytics that consider emerging threats, organizational data and industry trends to anticipate future risks and propose best next actions and optimal security investments, promotes use of AI-driven approaches.

- Maintaining continuous compliance and dynamically managing security policies that align with existing and evolving regulations, industry standards and business-relevant emerging threats are challenges. They drive the need for capabilities like dynamic policy tailoring and comprehensive analysis of policy control gaps, which AI can support.

- The need to manually analyze cyber issues with complex data landscapes while dealing with a shortage of talent is a formidable task without AI augmentation.

Obstacles

- Many core banking systems and mainframes may be incompatible with AI tools. Retrofitting AI into legacy systems will require costly overhaul or custom middleware.

- AI accuracy declines without unified, clean data; however, data relevant to banking security is generally scattered across legacy systems, third-party SaaS and on-premises and cloud infrastructure.

- AI-driven cyber-risk management solutions often require access to sensitive data, such as network logs, user behavior patterns and security incident reports, increasing privacy and security concerns.

- AI algorithms are susceptible to biases inherent in the training data, which can lead to inaccurate recommendations. This creates hesitation among risk owners and cyber-risk teams to trust and further adopt these technologies.

- Cost is a barrier, particularly for small and midsize banks with limited IT capabilities.

- AI tools often don’t plug and play with existing SOAR, SIEM, IAM or risk management platforms.

User Recommendations

- Strategically position AI as a core technology for banking enterprise resilience, specifically by leveraging it to improve security operations benchmarks like mean time to detect (MTTD) and mean time to respond (MTTR). This demonstrates the tangible value of AI in strengthening the organization’s defensive posture.

- Align strategic goals such as customer engagement by connecting real-time threat mitigations to brand trust and operational uptime.

- Quantify cyber-risk exposure with AI-enhanced scenarios to calculate potential loss across data breaches, ransomware and other compromises.

- Leverage AI to map regulatory requirements and ensure technology usage aligns with compliance standards to reduce future audit gaps.

- Develop a comprehensive data strategy that addresses critical considerations like data quality, accessibility, security and privacy, which are foundational for compliant AI deployment in banking.

- Avoid implementing duplicate AI functions across different tools and platforms. Establish a clear reference architecture for AI deployment.

Sample Vendors

Cisco (Splunk); IBM; LexisNexis Risk Solutions; Microsoft; NICE; Palo Alto Networks; ThreatQuotient; Tufin; Visa (Featurespace); Zscaler

Gartner Recommended Reading

Banking-Specific GenAI Models

Analysis By: Sudarshana Bhattacharya

Benefit Rating: High

Market Penetration: Less than 1% of target audience

Maturity: Emerging

Definition:

Domain-specific GenAI models are tailored to specific industry, business function or workflow needs. They enhance accuracy, privacy and compliance while minimizing hallucinations and prompt engineering. Built from scratch or fine-tuned on domain data, these models outperform general-purpose models on targeted use cases. In banking, these models are trained on specific financial data providing deep contextual understanding, enhancing accuracy and regulatory compliance for financial tasks.

Why This Is Important

While general-purpose models perform well across a broad set of applications, they may fall short for many banking applications that require domain-specific data and knowledge. GenAI models tailored to banking and investment services are growing and can improve alignment and trustworthiness with industry use cases while delivering more accurate, compliant and contextualized responses. Through targeted training, these models can lower hallucination risks associated with large models.

Business Impact

Banking-specific GenAI models:

- Outperform general-purpose models on domain-specific tasks by understanding financial language, context and nuances, while maintaining robust model benchmarks.

- Increase precision by reducing hallucination and inaccuracies through banking-specific dataset training.

- Accelerate GenAI project deployment in banks by providing a more advanced starting point with RAG, chain of thought and fine-tuning.

- Offer greater compliance and trust with banking regulations, which increases adoption within the industry.

Drivers

- The proliferation of open-source foundation models: The banking sector is capitalizing on open-source GenAI models for domain-specific solutions. Capital One’s Chat Concierge tool, built on Llama and integrated into car dealership websites, facilitates vehicle comparisons, explores financing options, offers trade-in estimates and assists in scheduling test drives.

- Increased specialization in GenAI model use: AI models are increasingly trained on private, organization-specific financial data that is not available in open-source models. This exclusive data allows for focused training, which enables models to excel in specialized tasks like customer service automation (Ally Bank), document analysis, financial forecasting and advisory services. As a result, banking-specific GenAI models offer precision and efficiency by using proprietary data and sidestepping the extensive customization needed with general-purpose solutions.

- Enhanced data privacy: Banking-specific GenAI models address challenges of confidentiality and privacy when handling PII data.

- Reduced hallucination: Transparent and proprietary training data creates a narrower knowledge base, which reduces unexpected outputs.

- Growing interest in domain-specific AI agents: The current hype around agentic AI — systems that can autonomously plan, reason and take actions — is fueling rapid growth in domain-specific GenAI models. As banks realize the value of specialized agents for processes like portfolio management, which require deep understanding of market trends, they push strongly to use tailored models optimized for those verticals, combining general AI capabilities with domain-specific expertise.

Obstacles

- Compliance and security: Open-source models may conflict with the bank’s internal IT standards, posing compliance threats from bad actors.

- Model proliferation and reduced versatility: Optimizing models like robo advisors and customer assistants for specific tasks limits their broader applicability. On the other hand, increasing the numbers of models complicates governance and management.

- Model maintenance: Managing domain-specific models requires frequent updates to avoid drift and adds operational complexity to the model risk management process.

- Data scarcity and quality: Domain-specific models require high-quality, relevant data, which is often scarce because of the prevalence of legacy systems in banking. Data silo and data quality issues require data cleanups that make model training challenging.

- Computational cost and in-house expertise: Banks have challenges in hiring and retaining skilled AI engineering and DevSecOps resources because of the technology sector’s competitive salaries and benefits.

User Recommendations

- Gather representative, high-volume and high-quality data for model pretraining to encompass all possible scenarios like lending, risk management, fraud detection, customer service, compliance or competitive differentiation.

- Establish life cycle management practices like model drift and data drift monitoring to avoid model degradation and ensure continuous compliance with regulatory or industry standards.

- Inquire about intended use cases and transparency details, such as training data size, quality, relevance, domain knowledge tests and data privacy measures, when evaluating banking-specific AI models. Assess accuracy benchmarks on real-world banking tasks.

- Assess the model for regulatory and ethical compliance by examining its model card, benchmarks and metrics, and confirm the vendor’s domain expertise in banking to ensure it understands the industry’s unique challenges.

Sample Vendors

AI4Finance Foundation; Ant Group; Broadridge; BUSINESSNEXT; Squirro

Gartner Recommended Reading

Causal AI in Banking

Analysis By: Benjamin Seesel, Priyanka Shukla, Ben Yan, Leinar Ramos

Benefit Rating: High

Market Penetration: 1% to 5% of target audience

Maturity: Emerging

Definition:

Causal AI identifies and utilizes cause-and-effect relationships to go beyond correlation-based predictive or generative models and toward AI systems that can prescribe actions more effectively and act more autonomously. It includes different techniques, such as causal graphs and simulation, that help uncover causal relationships to improve decision making. A deeper understanding of events is critical for several banking functions, such as customer engagement, operations and risk management.

Why This Is Important

Causal AI goes beyond correlation-based generative and predictive approaches to help understand the underlying factors that cause an outcome, so banks can take proactive, targeted actions. Banks can use causal AI in many ways, such as to analyze customer behavior and predict future needs, identify loan default drivers, improve financial forecasting, detect fraud or understand how new events or policy changes will impact business outcomes.

Business Impact

Causal AI helps banks:

- Devise data-driven customer engagement and retention strategies, driving revenue growth

- Improve credit risk assessment and prediction of default by differentiating between correlation and causation

- Identify the root cause of disruptions in business processes, improving operational efficiency and cost saving

- Unlock the power of explainable and understandable AI, enabling reliable augmentation and autonomy in AI-driven decision making, even in changing economic and competitive environments

Drivers

- AI — in particular agentic AI — systems increasingly need to act autonomously, particularly for time-sensitive and complex use cases (such as fraud detection and credit assessment). This will only be possible if AI understands what impact actions will have and how to make effective interventions.

- Limited data availability for certain use cases requires more data-efficient techniques like causal AI, possibly combined with synthetic data. Causal AI leverages human domain knowledge of cause-and-effect relationships to bootstrap AI models in small-data situations.

- Growing complexity in banking and continuously evolving regulatory, competitive and technological landscapes requires more robust AI techniques. Correlation-based AI models, trained with historical data, are brittle and lose accuracy when faced with gradual, let alone disruptive, changes. Causal structure changes much more slowly than statistical correlations, making causal AI more robust and adaptable in fast-changing environments.

- Banks face significant pressure to ensure transparency, explainability and interpretability in decisions made by AI systems. Causal AI can help explain why the model arrived at a particular decision.

- Generative AI (GenAI) can accelerate causal AI implementation. GenAI is emerging as an aid to explore documents and other data sources for existing causal knowledge. This can then be used to generate candidate causal graphs, which, while still requiring human validation or completion, may reduce time-consuming manual work.

- The next step in AI requires causal AI. Current deep learning models, in particular large language models (LLMs) and “reasoning” models for GenAI and AI agents, have limitations in terms of reliability. A composite AI approach that complements, for example LLMs with causal AI — in particular, causal knowledge graphs — offers a promising avenue to bring AI to a higher level, especially helpful in use cases such as fraud management, AML and customer authentication.

Obstacles

- Causality is not trivial. Not every phenomenon is easy to model in terms of cause and effect, with many factors potentially being relevant. Causality might be delayed, circular, unknown or hard to validate, despite the growing use of AI for causal discovery.

- Identifying a complete list of causal factors is difficult in today’s banking landscape, which is impacted in unpredictable ways by geopolitical risks, macroeconomic uncertainties and widely varying regulations around the world.

- Causal AI requires high-quality data, but data in banking is often siloed, disparate and not AI-ready.

- Even when models appear to function well, flawed assumptions about cause and effect can lead to incorrect or risky conclusions.

- Top causal AI use cases in banking, such as fraud prevention and credit and liquidity risk assessment, carry significant regulatory, operational and reputational risk if the causal AI model is flawed.

- Limited experience, skill sets and technical knowledge with enterprise-scale applications make it difficult for banks to scale causal AI pilots to larger and more complex causal models.

User Recommendations

- Run proofs of concept (POCs) to understand how causal AI complements existing AI approaches, including machine learning (ML), GenAI, agentic AI, and impact reliability and transparency.

- Use causal AI when more augmentation and automation is required. Examples include use cases such as next best action advisory tools, credit risk assessment, fraud detection, portfolio optimization and loan origination.

- Select different causal AI techniques based on the complexity of the use case, including ML or LLMs for causal discovery, causal rule inferencing, causal graphs, Bayesian networks or simulation.

- Educate your AI teams on how causal AI differs from correlation-based AI and the full range of applicable techniques if you plan to scale causal AI following a successful POC.

- Involve domain experts across lines of business, such as retail and commercial banking and wealth management, as applicable, in causal AI initiatives to help create, maintain or validate causal models.

Sample Vendors

Actable AI; Bayes Server; causaLens; Causality Link; Geminos; Howso; Parabole.ai; Scalnyx; Vizuro; Xplain Data

Gartner Recommended Reading

AI Simulation in Banking

Analysis By: Jasleen Kaur Sindhu, Leinar Ramos

Benefit Rating: High

Market Penetration: 1% to 5% of target audience

Maturity: Adolescent

Definition:

AI simulation is the combined application of AI and simulation technologies to jointly develop AI agents and the simulated environments in which they can be trained, tested and sometimes deployed. It includes both the use of AI to make simulations more efficient and useful and the use of a wide range of simulation models to develop more versatile and adaptive AI systems. AI simulation has a wide application in banking, from stress-testing market scenarios to simulating new fraud categories.

Why This Is Important

AI simulation has a wide-ranging application in banking. By combining AI and simulation, banks can model new risk and market scenarios to optimize investment decisions and improve predictive insights. New fraud scenarios can be simulated to strengthen the existing fraud detection capabilities. Banks can improve customer and competitor intelligence by simulating customer preferences to new products or marketing campaigns, including developing new credit products that minimize customers’ default risk.

Business Impact

AI simulation can enable banks to:

- Optimize investment strategies and evaluate risk exposure by simulating different and new financial scenarios.

- Use stress-testing scenarios for financial crime prevention.

- Onboard frontline staff faster on how to respond to different scenarios through situational simulation training.

- Enhance custom retention strategies and new product development pipelines.

- Reuse simulation environments to train future AI models.

Drivers

- Limited availability of AI training data: The scarcity in available AI training data is increasing the need for synthetic data techniques such as simulation. This is particularly critical for fraud prevention or credit decision making that requires a diverse balanced dataset. Generative AI (GenAI) and agentic AI implementations will further necessitate the need for more training data.

- Data privacy requirements: AI simulation allows banks to safely generate and share data, without compromising customers’ personally identifiable information (PII) with fintechs and technology providers.

- IT testing: By automating and optimizing testing processes, AI can significantly speed up quality assurance and engineering testing cycles, enabling quicker releases and updates.

- Regulatory compliance: Simulation offers a unique opportunity for banks to run and model millions of market scenarios. Banks can run stress tests and avoid large-scale market contagions, optimize capital allocations and ensure regulatory compliance.

- Innovation opportunities: With the rise in digital banking, banks now have greater access to customer data. AI simulation can further enhance banks’ ability to use this data to experiment and innovate. For instance, creating novel customer-facing applications that provide financial coaching to customers, or using AI agents to simulate and test customer preferences.

- Increasing number of sophisticated cyber and fraud attacks: This is driving the usage of AI and simulation-generated synthetic data to identify new risk types and fraud scenarios. For example, banks are using synthetic data to identify new variables and clusters to improve the accuracy of their fraud detection models.

- AI reusability: Banks will increasingly deploy hundreds of AI models, which requires a shift in focus toward building persistent, reusable environments where many AI models can be trained, customized and validated. Simulation environments are ideal since they are reusable and scalable, and enable many AI models to be trained at once.

Obstacles

- Talent scarcity: A lack of awareness and skills among AI practitioners to use simulation techniques can be a major obstacle.

- High cost: Using AI simulation can be expensive for most banks; additional investment is required to improve accuracy of the simulated output.

- Gap between simulation and reality: Simulations can only emulate — not fully replicate — real-world systems. Given this gap, AI models trained in simulation might not have the same performance and accuracy.

- Lack of explainability: Banks need to ensure that users can understand, explain and trust the results generated through AI simulations. Further, the combination of AI and simulation techniques can result in more complex pipelines that are harder to test, validate, maintain and troubleshoot.

- Data quality and availability: AI simulation relies on good quality and quantity of data. This requires integrating data from disparate sources and legacy systems and removing underlying biases, which might be a challenge for most banks.

User Recommendations

- Start with tried and tested business applications, such as stress-testing market scenarios or investment portfolios, where AI simulation has proven to be a success.

- Ensure AI simulation models comply with regulations related to data and model privacy, fairness, transparency and explainability. Invest in techniques and tools to build trust.

- Create synergies between AI and simulation teams, projects and solutions to enable a next generation of more adaptive solutions for evermore complex use cases. Incrementally build a common foundation of more generalized and complementary models that are reused across different use cases, business circumstances and ecosystems.

- Prepare for the combined use of AI, simulation and other relevant techniques, such as graphs, natural language processing (NLP) or geospatial analytics, by prioritizing vendors that offer platforms that integrate different AI techniques (composite AI) and simulation.

- Identify skills and competencies required to train or hire AI talent.

Sample Vendors

Altair Engineering; The AnyLogic Company; FICO; FNA; Microsoft; NVIDIA; Simudyne; Zenarate

Gartner Recommended Reading

Decision Intelligence

Analysis By: David Pidsley, Pieter den Hamer, Erick Brethenoux

Benefit Rating: Transformational

Market Penetration: 5% to 20% of target audience

Maturity: Emerging

Definition:

Decision intelligence (DI) is a practical discipline that advances decision making by explicitly understanding and engineering how decisions are made, and how outcomes are evaluated, managed and improved via feedback. By digitizing and modeling decisions as assets, DI bridges the insight-to-action gap to continuously improve decision quality, actions and outcomes. DI is technology-agnostic and applies decision-centric frameworks like observe, orient, decide and act (OODA) and Gartner DI (GDI).

Why This Is Important

Agentic AI and generative AI (GenAI) hype, regulatory pressures on decision automation, and recent global crises have exposed the fragility of business processes and the predigital, implicit and suboptimal ways of decision making that remain incumbent. DI is positioned beyond the trigger, poised to address these challenges by making decisions more explicit, optimal, adaptable and auditable.

Business Impact

- Faster, higher quality decisions that are consistent, compliant and cost-effective while being complex, contextual and continuous, thus driving agility in facing opportunities and threats in domains like banking, healthcare and supply chain.

- Enduring, effective, efficient, explainable and ethical enterprisewide DI execution enhances timely stakeholder outcomes.

- Risk is mitigated through accurate, trustworthy, fair, privacy-protective and scalable decision-centric operationalization of AI to augment and automate decisions.

- Adaptability of decisions as assets strengthens decision governance and outcome predictability.

Drivers

- Dynamic business complexity: Unpredictable disruptions, chaotic environments and accelerating pace of digital competition demands near real-time decision models that can adapt. Decision services can be powered by the composition of multimodal data analysis, data science, optimization, expert knowledge and other AI techniques.

- Decision silos: DI curtails fragmented, localized and implicit decisions that undermine organizational efficacy and efficiency. It also addresses the demand for cross-functional alignment on decisions as assets, the need for harmonization on which action should be taken following a business decision, and outcome optimization that balances global efficiency and local adaptations.

- Deluge of dashboards not driving action: Despite proliferation of “data-driven” tools and interfaces, most of which fail to connect insights to actions, dashboard development delays create decision latency, ambiguous outcomes and inability to perceive a decision’s impact harming organization efficiency.

- Human-AI delegation and distrust: AI adoption requires transparent, auditable decision models to address ethical concerns and ensure accountability. Automating human decisions has promoted disquiet and requires monitoring.

- Regulatory scrutiny: Data protection, AI and socio-environmental mandates compel explicit decision documentation for tighter compliance, risk awareness and mitigation. Explicit decision modeling and decision stewardship drive the analysis, management and control of the operational processes and observations needed to enforce decision governance policies and standards applied to decisions as assets.

- Availability and innovation of enabling technologies: Convergence of rule engines, simulation and optimization in DI platforms practically enables DI prototypes and pilots to become scalable DI implementations.

- GenAI acceleration of DI: Enriched context awareness via LLMs is accelerating composite AI model development for low-code/no-code business decision analysts and pilots of agentic decision automation.

Obstacles

- Business stakeholder apathy, limited urgency and low cultural readiness, ineffective change management, and lack of DI skills and AI literacy hinder adoption.

- Bridging the insight-to-action gap to improve outcomes requires a decision-centric vision beyond the data-driven dogma and the data-to-insight workflow. Technology centricity overlooks psychological and sociological factors in decision making.

- Weak collaboration, inadequate operating, delivery and organizational models (i.e., a DI center of excellence), and disconnected decision-making silos hamper DI effectiveness. Even advanced cross-silo DI practitioners struggle to impartially reconsider key decision flows.

- Unselective or overly enthusiastic adoption of decision automation introduces risks, including unintended consequences, loss of context and bias amplification. This undermines trust in DI and limits effective use of DI platforms.

User Recommendations

- Define and model critical decisions involving resource allocation, uncertainty or competing alternatives. Use these as pilots to build DI momentum and demonstrate value for enterprisewide adoption.

- Inventory repetitive, high-impact decisions and their key inputs. Adopt decision-centric modeling by articulating outcomes, decision logic, alternative courses of actions and required observations to drive continuous learning, improvement and transparency.

- Maximize decision quality, resilience and traceability through cross-functional DI fusion teams, fostering collaboration and alignment across departments. Delegate decision-making authority to those with the most relevant expertise and context.

- Upskill staff in decision modeling, prescriptive analytics and optimization. Investigate the roles of decision engineers, decision scientists and decision stewards. Experiment with agentic, GenAI and other composite AI, and DecisionOps to support organizationwide decision centricity and excellence.

Gartner Recommended Reading

FinOps for AI

Analysis By: Jim Hare, Adam Ronthal, Andrei Razvan Sachelarescu

Benefit Rating: High

Market Penetration: 1% to 5% of target audience

Maturity: Emerging

Definition:

FinOps for AI is the application of financial operations best practices to help organizations increase visibility and manage the costs of AI services to ensure efficient usage and deliver maximum business impact. Using FinOps to track and measure AI spend and usage is crucial for optimizing costs, ensuring financial accountability and maximizing ROI.

Why This Is Important

Cost poses one of the greatest near-term threats to AI and GenAI success. AI workloads, especially in cloud environments, often use expensive GPU-based compute infrastructure and consume tokens in unforeseen ways, leading to unpredictable expenses if not monitored properly. Deploying and managing AI solutions generates other costs, including development, governance and change management. Using FinOps to track and measure AI spend and usage is crucial for optimizing costs, ensuring financial accountability and maximizing ROI.

Business Impact

FinOps helps businesses optimize AI spend by providing real-time cost visibility and control, enabling teams to allocate resources efficiently and prevent budget overruns while also preventing underprovisioning that can cause downtime or slowdowns. FinOps for AI also enhances collaboration between finance, engineering and operations teams, ensuring that AI investments align with business objectives while ensuring cost-efficiency. Using FinOps practices, organizations can maximize the ROI of AI initiatives and leverage cost-saving opportunities such as reserved instances, workload automation/optimization and usage-based pricing models.

Drivers

- AI adoption, especially AI applications and GenAI, is contributing to a spike in cloud costs for most enterprises. Hidden costs and unpredictable invoices make it difficult for organizations to deploy AI more broadly.

- Tracking AI costs and usage scaling is complex due to fluctuating computational demands, variable AI service pricing, hidden infrastructure costs and exponential scaling of model training and inference across users and applications.

- Organizations new to AI and/or the cloud are unlikely to be prepared for AI cost volatility and will need to adjust their legacy operating models and budget practices by adopting FinOps for AI. Many organizations face challenges in tracking and measuring AI costs against concrete business benefits.

- Engineering teams are often immature in their use of AI services and the many dynamic layers needed to achieve ongoing cost-effectiveness.

- The total cost of ownership (TCO) of AI use cases can differ from the cost of traditional software applications with fixed costs and purpose. Continuous training, switching to newer models, specialized infrastructure like GPUs and differences in processing costs for specific data types (text, image, video, audio) are part of ongoing AI costs.

- Many AI models and services are based on consumption pricing models and may be purchased in many versions or variants.

- Pricing may also fluctuate based on a variety of factors such as usage, model choice, accuracy and performance guarantees. The velocity of pricing volatility requires continuous and active assessments of price/performance and accuracy.

Obstacles

- Implementing FinOps for AI is challenging because of AI workloads’ unpredictable and dynamic nature and the complexity and variety of cost factors that make cost estimation, budgeting and optimization more challenging compared with traditional cloud operations.

- Balancing performance and cost-efficiency is difficult because AI models often require specialized compute infrastructure resources, GPUs and large datasets that can lead to excessive cloud spending if they are not monitored and optimized effectively.

- Many organizations struggle with cross-functional collaboration among finance, operations and engineering teams, as aligning AI-specific cost insights with business objectives requires a cultural shift and enhanced visibility into AI-driven expenditures.

User Recommendations

- Track the TCO of using AI: Implement real-time tracking of total running costs, including cloud, infrastructure and labor costs. Use tagging and cost allocation strategies to assign expenses to specific AI projects or departments. Assign budgets to AI-related resource and service groups, and trigger cost alerts when consumption exceeds budget goals.

- Optimize AI spend and workloads: Track AI spend across packaged and custom SaaS, AI-leveraging commercial models (tokens via API calls), and compute from hosted models.

- Understand the pros and cons of buying versus building models: Closed models built by model providers may be considered more expensive at first glance, but they reduce delivery time, upfront development costs and the need for more expensive skills. Build models for truly strategic types of use cases.

- Embrace an agile approach to model switching: Regularly compare models in use with alternative options to see whether the same or better accuracy can be achieved at lower cost.

- Invest in making data AI-ready: Control data preparation and processing costs by investing in data cleansing and curation to produce smaller training and retrieval-augmented generation datasets of higher quality.

- Implement proactive cost management controls and guardrails: Integrate real-time anomaly detection and alerts with demand-throttling options to guard against unexpected cost spikes.

Sample Vendors

Airia; Exostellar; FinOps Foundation; Finout; Flexera; IBM

Gartner Recommended Reading

Composite AI in Banking

Analysis By: Moutusi Sau, Erick Brethenoux, Pieter den Hamer

Benefit Rating: Transformational

Market Penetration: More than 50% of target audience

Maturity: Early mainstream

Definition:

Composite AI, or hybrid AI, refers to the combined application (or fusion) of different AI techniques to improve the efficiency of learning and expand the level of knowledge representations. It broadens AI abstraction mechanisms and provides a platform to solve a wide range of banking problems effectively. In banking, the ability to deeply contextualize data is applied in areas like detecting fraud, adhering to compliance or constructing a 360-degree customer view.

Why This Is Important

Composite AI recognizes that no single AI technique is a panacea. It aims to combine connectionist AI approaches, like machine learning (ML) and deep learning, with symbolic and other AI approaches, like rule-based reasoning, graph analysis or optimization techniques. A single technique can rarely solve banking problems. Integrating the strengths of different techniques can bring in nuances to the solution. Thus, composite AI is at the center of the generative AI (GenAI), decision intelligence (DI) and agentic AI markets.

Business Impact

With its emphasis on customer trust and responsibility to regulations, composite AI is critical to the banking industry being able to safely employ GenAI. We’ve seen a combination of techniques, including AI agents or ML models, conduct all regulated tasks around GenAI implementation. By cross-verifying results from multiple AI methods and models, composite AI can lead to more accurate predictions and fewer errors, which is crucial in risk-sensitive areas like credit scoring and fraud detection.

Drivers

- Enhancing financial crime prevention: Composite AI significantly augments existing rule-based systems with methods like behavioral, network and login analysis. For AML, it utilizes composite methods like knowledge graphs, label propagation, clustering and computer vision. It also aids the know-your-business process by analyzing transactions to uncover patterns revealing connected organizations and potential money-laundering activities.

- Simulating and future-proofing the business: Agent-based modeling, identified as the next wave of composite AI, uses multiple agents to represent actors in the ecosystem. This allows banks to simulate complex situations like financial crises or how investors interact during emergent behaviors. Agents will be able to determine the best AI tools for specific problems.

- Deepening customer hyperpersonalization: Composite AI facilitates truly personalized customer experiences by combining various AI methods to analyze diverse customer data, including transactions, interactions, preferences and sentiments. This ranges from tailored product recommendations to personalized financial advice.

- Addressing data scarcity with synthetic data creation: Enterprises are now complementing scarce, raw historical data with synthetic data created using composite AI techniques. Methods such as knowledge graphs and generative adversarial networks (GANs) generate this synthetic data, which is increasingly valuable for use cases like fraud detection and customer-facing applications.

- Increasing strategic advantage of GenAI: The acceleration of GenAI is actively driving the research and adoption of composite AI models. Such models are described as the foundation of the digital innovation platforms that are becoming prevalent across banks.

Obstacles

- Data scientists as decision makers: Applying multiple AI methods together is still in its early days. Ultimately, banking data scientists decide how to combine AI methods, which prevents applications from scaling fast.

- Lack of talent to leverage multiple AI methods: Hiring someone with data science experience is still expensive in banking, and getting talent to leverage multiple methods is still uncommon.

- Trust and risk barriers: The AI engineering discipline is also starting to take shape, but only mature banks have started to apply its benefits in operationalizing AI techniques. Organizations must first address security, ethical model behaviors, observability, model autonomy and change management practices across the combined AI techniques.

- Deploying ModelOps: The ModelOps domain in banking remains fragmented with multiple tooling. A robust ModelOps approach is required to efficiently govern composite AI environments and harmonize them with other areas, such as DevOps and DataOps.

User Recommendations

- Work with banking leaders to identify projects, including credit decisioning or fraud detection, in which an ML-only approach is inefficient or doesn’t work well. This includes cases where enough data is not available or when the pattern cannot be represented through current ML models.

- Capture domain knowledge and human expertise in areas like front office or risk management that require context for data-driven insights by applying decision management with business rules and knowledge graphs, in conjunction with ML and/or causal models.

- Capture domain expertise within banking areas like lending, credit decisioning workflows to provide context for data-driven insights by applying decision management with business rules and knowledge graphs, in conjunction with ML and/or causal models.

- Accelerate the development of DI projects by encouraging experimentation with GenAI, which in turn will accelerate the deployment of composite AI solutions.

Sample Vendors

4Paradigm; ACTICO Group (ACTICO); Aera; FICO; Frontline Systems; IBM; Indico Data; SAS; Simudyne

Gartner Recommended Reading

Neurosymbolic AI

Analysis By: Erick Brethenoux, Afraz Jaffri

Benefit Rating: High

Market Penetration: 5% to 20% of target audience

Maturity: Emerging

Definition:

Neurosymbolic AI is a form of composite AI that combines probabilistic reasoning methods and symbolic systems to create more robust and trustworthy AI models. This fusion enables the combination of probabilistic models with logic-based techniques (such as rules and knowledge graphs) to enable AI systems to better represent, reason and generalize concepts. This approach provides a reasoning infrastructure for solving a wider range of business problems more effectively.

Why This Is Important

Neurosymbolic AI addresses limitations in current AI systems, such as incorrect outputs, lack of generalization to a variety of tasks and an inability to explain the steps that led to an output. The neurosymbolic approach leads to more powerful, versatile and interpretable AI solutions and allows AI systems to reason through more complex tasks. Generative AI systems are starting to leverage neurosymbolic methods to overcome their reasoning shortcomings.

Business Impact

Neurosymbolic AI will have an impact on the efficiency, adaptability and reliability of AI systems used across business processes. The integration of logic and multiple reasoning mechanisms brings down the need for ever larger AI models and their supporting infrastructure. These systems will rely less on the processing of huge amounts of data, making AI agile and resilient. Neurosymbolic approaches can augment and automate decision making with less risk of unintended consequences.

Drivers

- Neurosymbolic AI addresses the limitations of large reasoning models (LRMs), which are still plagued with a lack of symbolic abstraction when exclusively based on deep learning techniques.

- The need for explanation and interpretability of AI outputs is especially important in regulated industry use cases and in systems that use private data.

- Understanding the meanings behind words, not just their arrangement (semantics over syntax), is an increasing priority in systems that deal with real-world entities to ground meaning to words and terms in specific domains.

- The set of tools available to combine different types of AI models is increasing and becoming easier to use for developers and end users. The dominant approach is to chain together results from different models (composite AI) rather than using single models.

- The integration of multiple reasoning mechanisms necessary to provide agile AI systems eventually leads to adaptive AI systems, notably through blackboardlike mechanisms.

- Agentic AI advances also participate in advancing neurosymbolic methods, while agents using various composite AI techniques collaborate to solve problems.

Obstacles

- Most fundamental neurosymbolic AI methods and techniques are being developed in academia or industry research labs. Despite the increased availability of tools, implementations in business or enterprise settings are still limited.

- No agreed-upon techniques exist for implementing neurosymbolic AI, and disagreements continue between researchers and practitioners on the effectiveness of combining approaches, despite the emergence of real-world use cases.

- The commercial and investment trajectories for AI startups allocate almost all capital to deep-learning approaches, leaving only those willing to bet on the future to invest in neurosymbolic AI development.

- Currently, despite increasing exposure, popular media and academic conferences do not give as much exposure to the neurosymbolic AI movement as compared to other approaches (such as generative AI).

User Recommendations

- Adopt composite AI approaches when building AI systems by using a range of techniques that increase the robustness and reliability of AI models. Neurosymbolic AI approaches will fit into a composite AI architecture.

- Dedicate time to learning about neurosymbolic AI approaches, and to identifying use cases that can benefit from applying these approaches.

- Invest in data architecture that can leverage the building blocks for neurosymbolic AI techniques, such as knowledge graphs and agent-based techniques.

- Consider neurosymbolic AI architectures when the limitations of generative AI models prevent their implementation in the organization.

- Educate developers on the potential of neurosymbolic models by exploring the capabilities of neurosymbolic approaches while building learning AI agents.

Sample Vendors

Franz; Google DeepMind; IBM; Microsoft; RelationalAI; Wolfram|Alpha

Gartner Recommended Reading

Artificial General Intelligence

Analysis By: Pieter den Hamer, Philip Walsh

Benefit Rating: Transformational

Market Penetration: Less than 1% of target audience

Maturity: Embryonic

Definition:

Artificial general intelligence (AGI) is the (currently hypothetical) capability of a machine that can match or surpass the capabilities of humans across all cognitive tasks. In addition, AGI will be able to autonomously learn and adapt in pursuit of predetermined or novel goals in a wide range of both physical and virtual environments.

Why This Is Important

With AI’s growing sophistication — including the recent advances in generative AI (GenAI) and agentic AI — a growing number of AI experts have shortened their predicted timelines for achieving AGI in the future or view AGI as no longer purely hypothetical. A clear, shared definition of AGI is necessary for evidence‑based governance and realistic expectations. Achieving AGI would be a transformative tipping‑point with profound consequences for productivity, employment, geopolitical power, legal, ethical and cultural norms — and society at large.

Business Impact

In the near term, anticipation of AGI fuels both overly optimistic expectations and existential fears, skewing investment, distorting trust and accelerating the emergence of new AI regulations. Over the longer horizon, the question of who builds and controls AGI — or other forms of increasingly powerful AI — looms large. Many experts see public stewardship as essential, a prospect that could upend private advantage and redraw entire markets.

Drivers

- Recent advances and growing interest in multimodal large language models (LLMs), so-called reasoning models and AI agents drive considerable hype about AGI. The massive scaling of deep learning and the availability of huge amounts of data and compute power largely have enabled these advances.

- AI’s further evolution toward AGI, as defined here, is increasingly complemented by other partially new approaches, such as knowledge or causal graphs, world models, adaptive AI, embodied AI, composite and neurosymbolic AI, and likely other innovations yet unknown.

- A number of AI vendors are openly discussing and actively researching the field of AGI, creating the impression that AGI lies within reach. However, their definitions of AGI vary greatly and are often open to multiple interpretations. Moreover, other leading AI vendors and experts have dismissed AGI as hype, urging focus on the real impact of AI’s growing capabilities.

- Humans’ innate desire to set lofty goals is also a major driver for AGI. At one point in history, humans wanted to fly by mimicking bird flight. Today, airplane travel is a reality. The inquisitiveness of the human mind, taking inspiration from nature and from itself, is not going to fizzle out.

- People’s tendency to anthropomorphize nonhuman entities also applies to AI-powered machines. The humanlike responses of LLMs and the reasoning-like capabilities of recent AI models have fueled this tendency. Although many philosophers, neuropsychologists and other scientists consider this attribution highly uncertain or going too far, it has created a sense that AGI is within reach or at least is getting closer. In turn, this has triggered massive media attention, several calls for regulation to manage the risks of AGI and a great appetite to invest in AI for economic, societal and geopolitical reasons.

Obstacles

- Little scientific consensus exists on the meaning of “human intelligence.” Any claims about AGI are hard to validate in the face of the enormous complexity of the human brain and mind and such a limited understanding of them.

- Unreliability, lack of transparency and limited abstraction and reasoning of pattern-based capabilities in current AI are not easy to overcome with deep learning’s intrinsically probabilistic approach. More data or more compute power for ever-bigger models is unlikely to resolve these issues, let alone to achieve AGI. To realize (and control) AGI will require further technological innovations. Therefore, AGI as defined here is unlikely to emerge in the near future.

- If AGI materializes, autonomous actors likely will emerge that, in time, will be attributed with full self-learning, agency, identity and perhaps even morality. This will open a bevy of considerations about AI’s legal rights and trigger profound ethical and even religious discussions. AGI also brings the risk of negative impacts on humans, from job losses to a new, AI-triggered arms race and more. A serious backlash may result, and regulations to ban or control AGI are likely to emerge in the near future.

User Recommendations

- Engage with stakeholders to address excessive optimism or unwarranted pessimism, and create or maintain realistic expectations around AGI. Ground AI strategy in concrete business problems rather than speculative AGI forecasts. Recalibrate the AI portfolio periodically as AI capabilities evolve, while leveraging the complementary strengths of human and artificial intelligence.

- Stay apprised of scientific and innovative breakthroughs that may indicate AGI’s possible emergence; however, be aware of the broad range of definitions and views regarding AGI, some strict and some less strict. Meanwhile, keep applying current AI to learn, reap its benefits and develop practices for its responsible use.

- Assess whether AI systems truly meet their specific use-case needs, rather than relying on generic measures of intelligence.

- Prepare for emerging AI regulations and promote internal AI governance to manage current and emerging AI risks. Because although AGI as defined here is not a reality now, current AI already poses significant risks regarding ethics, reliability and other areas.

Sample Vendors

Aigo; Amazon; Anthropic; Butterfly Effect; DeepSeek; Google; Microsoft; OpenAI

Gartner Recommended Reading

Federated Machine Learning

Analysis By: Tong Zhang, Bart Willemsen, Svetlana Sicular

Benefit Rating: High

Market Penetration: Less than 1% of target audience

Maturity: Emerging

Definition:

Federated machine learning (FedML) is a decentralized approach to machine learning that enables multiple clients to collaboratively train a shared model without sharing their raw data, enhancing privacy and overcoming data transfer constraints. This process involves clients performing local training on their data and sending updates to a central server, which aggregates these updates to refine the global model.

Why This Is Important

FedML highlights an important innovation in (re)training ML algorithms in a decentralized environment without disclosing sensitive business information. It enhances model personalization and contextualization by allowing local data processing in smartphones, softbots, autonomous vehicles or Internet of Things (IoT) edge devices. It also facilitates organizations to build collaborative learning models across data silos.

FedML unlocks access to diverse datasets, improving model accuracy and robustness while overcoming challenges related to data gravity and sovereignty.

Business Impact

FedML offers transformative benefits across industries by enabling collaborative machine learning while preserving data privacy and security. It allows organizations to enhance model accuracy and operational efficiency without transferring sensitive data, reducing costs and ensuring compliance with data regulations. FedML is applicable in sectors such as healthcare, finance, telecommunications, IoT and manufacturing, providing solutions for diagnostics, fraud detection, network optimization and personalized services. It also facilitates training and fine-tuning AI agents and large language models using private data.

Drivers

- The proliferation of privacy and legislative regulations requires protection of local data. FedML is one type of solution to protect data privacy.

- The training of AI agents and LLMs requires the use of private, distributed datasets without exposure.

- Growth of edge computing and IoT requires data processing and model training directly and in real time on distributed devices, reducing the need for data centralization.

- Exploding data volumes and data gravity make large-scale data transfers challenging, but FedML can resolve these challenges by processing data locally and avoiding the need for centralization.

- Collaboration is essential for organizations to gain valuable data insights FedML facilitates this collaboration by enabling shared model training without directly exchanging sensitive or proprietary data.

- Centralized architectures of machine learning have certain limitations, including scalability, power consumption and latency issues. FedML can be one effective solution to address these challenges.

- Advancements in enabling technologies, such as differential privacy and blockchain, extend the adoption of FedML by enhancing privacy and facilitating decentralized coordination.

Obstacles

- FedML adoption is hindered by lack of awareness, trust issues, incentive design, collaboration and infrastructure maturity, requiring comprehensive solutions for enterprise integration.

- Enabling FedML requires a complex pipeline that integrates capabilities across DataOps, ModelOps, deployment and continuous tracking/retraining, necessitating a high degree of implementation maturity.

- Creating a new, more accurate and unbiased central model from local model improvements can be nontrivial, as the diversity or overlap between local learners and their data may be hard to assess and may vary greatly.

- Diverse device capabilities cause challenges like stragglers and client dropout, necessitating asynchronous training and adaptive algorithms to handle variability in computation and connectivity.

- FedML’s model updates can leak sensitive information, requiring privacy-enhancing technologies like differential privacy and secure multiparty computation to safeguard against inference attacks.

- Ensuring equitable model performance across diverse clients is challenging due to statistical heterogeneity, necessitating fairness-aware algorithms to address disparities during training and aggregation.

User Recommendations

- Focus on FedML for scenarios where data decentralization is required by privacy regulations, competitive sensitivities or logistical challenges, leveraging its advantage in creating decentralized smart services with diverse user data.

- Use centrally pretrained models to start FedML processes, capturing general patterns and focusing federated rounds on fine-tuning and personalization with local data.

- Begin with small pilot projects or simulations to gain experience and understand algorithm and framework nuances before large-scale deployments.

- Establish governance, trust and incentive mechanisms early to facilitate partnerships with suppliers, customers or peers, enhancing operational efficiency and product offerings through shared insights.

- Implement strategies to prevent excessive divergence from the global model, using central reference models or algorithms like FedProx to maintain cognitive cohesion.

Sample Vendors

Alibaba Group; Devron; Eder Labs; FedML; Google; Intel; NVIDIA; Owkin; WeBank; WithSecure

Gartner Recommended Reading

At the Peak

Multimodal AI

Analysis By: Nick Ingelbrecht, Sushovan Mukhopadhyay, Yogesh Bhatt

Benefit Rating: Transformational

Market Penetration: 1% to 5% of target audience

Maturity: Adolescent

Definition:

Multimodal AI models are trained with multiple types of data (also known as modalities) simultaneously, such as images, video, audio and text. This enables them to create a shared data representation to improve performance in different tasks. At runtime, they can handle more than one modality, either in their inputs, their outputs or both.

Why This Is Important

Multimodal AI adds significant new technology capabilities such as greater accuracy to existing software. It spurs new specialized applications, enables new use cases such as visual question answering of image frames, manufacturing optimization, and fraud detection in banking and finance, and creates new value outcomes. The physical world and the data it generates are inherently multimodal. By integrating and analyzing diverse data sources, a more comprehensive evaluation of complex environments and tasks can be achieved compared with unimodal models, helping users make sense of the world and opening up new avenues for AI applications.

Business Impact

Gartner forecasts that:

- Over the next five years, multimodal AI will become increasingly integral to capability advancement in every application and software product across all industries.

- By 2027, 40% of generative AI (GenAI) solutions will be multimodal (text, images, audio and video), up from 1% in 2023.

Drivers

Multimodal AI adoption will generate cross sector transformational opportunities. Key drivers include:

- A paradigm shift from traditional, linear processes to dynamic, AI-driven systems where humans and machines collaborate seamlessly. And further evolution of agentic AI will involve increasing integration with multimodal AI techniques to handle the complexity and richness of real-world data and tasks.

- Recent AI breakthroughs, particularly in the realm of large language models (LLMs) and vision language models (VLMs), are highly relevant to multimodal AI. These advancements have catalyzed a renaissance in natural language processing and computer vision.

- Intelligent applications, by their nature, are context-rich and designed to adapt to constantly changing scenarios. This makes multimodal AI a crucial component for their development and evolution.

- World models are a significant driver for multimodal AI because they inherently require the ability to process and understand information from various modalities to accurately represent and simulate the complexity of the real world.

- Broader availability of AI/GenAI multimodal models, both proprietary and open-source, lowers the barriers to entry and adoption via AI marketplaces.

- There is a demand for multimodal domain-specialized models in areas such as healthcare, where multimodality extends or enriches use cases.

Obstacles

Multimodal AI is powerful in understanding and processing from various modalities, but faces several primary obstacles to adoption:

- Integrating diverse data types — such as text, images, audio and video — is challenging due to differences in format and time stamps, risking inaccurate interpretations. Multimodal AI models are complex, combining various modality-specific subnetworks, which can obscure transparency and explainability.

- Architectural complexity, increased data volume and the need for data fusion lead to inference latency, hindering reliable operation where immediate decision making is crucial.

- Dataset bias originates from leveraging training datasets like text, images, videos and speech, which may inadvertently reflect societal or cultural biases. This can result in making unfair or inaccurate predictions/decisions.

- Handling sensitive data across modalities increases breach risks and privacy violations. This complicates compliance with regulations like General Data Protection Regulation (GDPR) or Health Insurance Portability and Accountability Act (HIPAA), as multimodal AI exposes new attack surfaces and heightens privacy risks with diverse data types.

User Recommendations

Organizations looking to implement multimodal AI should:

- Identify AI use cases where multimodal AI can enhance business value beyond unimodal AI foundation models.

- Run pilots with off-the-shelf multimodal models to demonstrate not only technical feasibility but the business value.

- Build a strong model evaluation by assessing the quality of relationships between modalities such as comparing generated captions from images to ground-truth labels/descriptions.

- Prioritize building or accessing robust data infrastructure supporting the collection, storage and processing of diverse data types (text, images, audio and video).

- Build or acquire expertise to handle the technical complexities of processing and integrating multimodal data with legacy and existing workflows.

- Create or extend AI governance strategies and policies to address challenges with multimodal datasets and ensure compliance.

- Incorporate multimodality into technology roadmaps and create migration paths for multimodal AI in systems procurement or product development plans.

Sample Vendors

Aimesoft; Google; Hugging Face; Jina AI; Meta; Midjourney; NVIDIA; OpenAI; Stability AI; TwelveLabs

Gartner Recommended Reading

AI Agents in Banking

Analysis By: Jasleen Kaur Sindhu, Lopa Sinha, Sophia Palmstedt

Benefit Rating: High

Market Penetration: 5% to 20% of target audience

Maturity: Emerging

Definition:

AI agents are autonomous or semiautonomous software entities that use AI techniques to perceive, make decisions, take actions and achieve goals in their digital or physical environments. In banking, AI agents offer new opportunities to automate workflows requiring complex decisioning such as fraud investigation, sales, trade financing and lending. Governance, however, remains crucial for mainstream adoption of AI agents in the banking industry.

Why This Is Important

Banks are beginning to explore AI agents but have made less progress than other industries. Unlike GenAI assistants, AI agents have the ability to make decisions and take actions for complex tasks. Banks are currently considering AI agents for internal operations like HR, IT, risk and compliance, and customer service, but they also present opportunities to augment complex processes such as lending and fraud investigation.

Business Impact

- Hyperpersonalized banking experiences that adapt based on customer behavior, spending pattern or lifestage.

- Real-time anomaly investigation with self-improving AI agents trained on evolving fraud patterns.

- Continuous monitoring of compliance postures to flag policy violations in real time.

- Improved employee productivity by removing or reducing time spent on tedious, complex banking processes such as account opening, statement processing, reconciliation and settlement.

Drivers

- Early implementations in banking: Banks are beginning to implement AI agents from simple applications to complex systems. BNY Mellon uses multiagent architecture for tailored sales recommendations, enhancing client interactions. Capital One’s proprietary AI agent tool assists car buyers. Top use cases reported include IT support, call center support and internal administrative tasks like HR.

- GenAI breakthroughs: Advances in reasoning models, large action models (LAMs) and domain-specific small language models enhance the planning of complex actions and banking industry-specific implementations.

- Data-rich landscape: Banking’s extensive customer and financial data and complex decision-making processes offer opportunities for AI agents to automate operations and improve delivery.

- Multimodal understanding: AI’s ability to use vision, audio and language allows for flexible agents, reducing development time and effort for automation.

- Composite AI, including neurosymbolic models: Advances in planning and problem-solving models enable complex AI agents. These agents use diverse AI practices for forecasting, decision making and planning. For instance, Digital Credit Union’s AI agent aids fraud investigation by gathering relevant account information, summarizing details and sharing insights with business units.

Obstacles

- Potential negative impact on employees working alongside AI agents, risking increased job security fears.

- Workflows that can be fully automated by AI agents in banking are not yet feasible. Governance challenges and the need for oversight will likely delay the adoption of fully autonomous AI systems.

- AI agents can suffer from issues like hallucinations, lack of traceability and explainability, which can complicate compliance and lead to incorrect decisions.

- Many banks operate with outdated legacy systems and fragmented data silos. Poor quality data can lead to suboptimal decisions by AI, reducing its effectiveness.