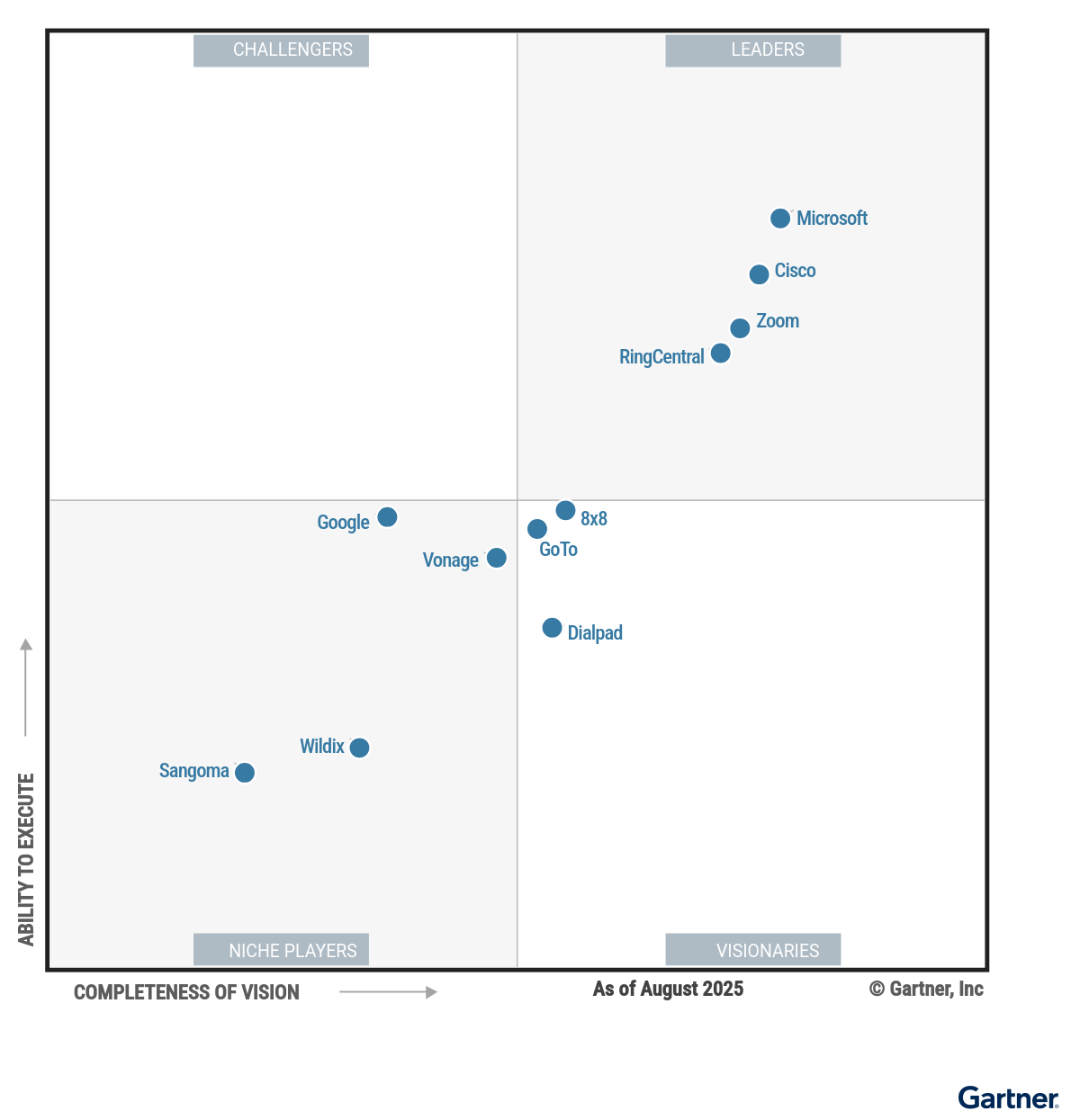

Magic Quadrant for Unified Communications as a Service

22 September 2025 - ID G00823063 - 46 min read

By Pankil Sheth, Megan Fernandez, and 2 more

UCaaS providers primarily offer telephony, meetings, messaging and contact center, and are trying to differentiate with AI capabilities that are mostly focused on customer-facing and collaboration features. This research helps heads of I&O select providers that align with their organizations’ needs.

Strategic Planning Assumptions

- By 2028, 90% of organizations will use their existing cloud office/collaboration platforms for enterprise telephony instead of specialized telephony platforms, which is a major increase from 30% in 2025.

- By 2028, enterprises will spend 50% lower than what they are spending now with their traditional telephony platforms.

- By 2028, organizations currently using specialist unified communications (UC) telephony platforms will cut down 70% of their existing UC as a service (UCaaS) licensing entitlements.

Market Definition/Description

Gartner defines unified communications as a service (UCaaS) as a multitenant, subscription-based service that is cloud-delivered. It provides business telephony features; public switched telephone network (PSTN) connectivity that enables inbound and/or outbound external calling; and collaboration features, such as messaging and meetings. UCaaS services can be consumed by end users with traditional handsets, desktop clients, web clients, meeting room systems and mobile apps.

UCaaS is used by organizations to securely communicate and collaborate — both internally and externally. It includes telephony, messaging and meetings. UCaaS providers may offer variations of each of the three core modes of communication and also offer a range of cloud contact center functionalities, either self-developed or through integration/partnerships with cloud contact center specialists.

Gartner’s definition of meetings for the UCaaS market mostly focuses on the capabilities for internal collaboration, work from home and external presentation meeting use cases. Other specialized use cases — such as webinar, remote support, distance learning and training — are often available from UCaaS offerings, but are not mandatory for inclusion in this research. These use cases are part of a separate market defined by Gartner (the meeting solutions market).

UCaaS is frequently sought by organizations as a replacement option that will enable them to outsource most of the maintenance, upgrade, support and management of premises-based UC to the UCaaS provider. With most providers, UCaaS is a co-managed service; however, the buyer’s share of the management is limited to simpler administrative tasks, such as move, add, change and delete (MACD).

Support for remote and hybrid workers, an important capability that buyers seek, is standard in UCaaS offerings today.

UCaaS vendors are expanding their offerings in two adjacent spaces. The first is basic, and involves mostly internal-facing, voice-only call center solutions that are usually bundled with the UCaaS offering at little/no additional cost. The second market involves artificial intelligence (AI)-enabled use cases for telephony, messaging and meetings. Gartner sees these two pursuits as attempts by vendors to differentiate their offerings in a highly commoditized market. Gartner observed a degree of GenAI normalization for meeting capabilities and, to a lesser extent, in telephony.

Mandatory Features

Enterprise telephony features: This functionality must be supported through physical IP phones, physical analog phones; analog devices (e.g., fax machines and fire alarm panels); desktop apps; web apps; or mobile apps. It must include at least the following features:

- Emergency calling services with notifications connectivity to the PSTN.

- Survivability

- Basic internal or external calling

- Call forwarding

- Call transfer

- Shared-line call appearances

- Voicemail

- Call logging

- Call recording

- Encryption

- Account codes

- Hunt groups

- Queues with announcements

- Attendant consoles (for receptionists)

- Delegation (for administrative assistants)

- Auto attendants

- Interactive voice responses (IVR) for self-service

- Hot desking (used in shared workspaces)

Meeting functionality: These features must be accessible via desktop app, mobile app, web app or meeting room systems. They must include at least the following features:

- Multiparty audio/video conferencing with content sharing (screen and application sharing)

- In-meeting messaging

- File sharing

- Customizable layouts

- Closed captioning

- Meeting summaries

- Recording

- Virtual backgrounds

- Breakout session support

- Reactions and other social engagement features

Messaging features: The following capabilities must be included, at a minimum:

- The ability to enable users to exchange richly formatted instant messages (IMs) with emojis, images, file attachments and links in real time.

- Support for personal messaging for 1:1 communication (also known as “chat”), as well as team messaging for groups using conversational user experiences.

- Support for presence and status indicators that allows users to view the availability and status of other users and resources in their organizations.

Common Features

Software apps: These enable access to all of the communication modalities and collaboration features from a consistent user experience across endpoints. UCaaS providers offer desktop, web and mobile apps for smartphones and tablets, as well as software extensions/plug-ins that integrate with business applications, such as calendars, email and CRM solutions.

Contact center: UCaaS vendors commonly have two offerings:

- An integrated contact center can be self-developed by the UCaaS provider, often relying on the same platform that delivers UCaaS telephony services. This offering is typically less costly.

- UCaaS vendors can enter into technology partnerships with other market-leading, third-party contact center vendors to offer best-in-class services under the same contract, but not their own technology stack. This offering is typically more costly.

The above approach employing two offerings enables UCaaS vendors to provide basic, internal-facing IT help desk call centers at little or no additional cost within the UCaaS licensing.

Quality of service (QoS) monitoring: Buyers expect UCaaS providers to include at least a basic level of QoS monitoring and reporting, along with advanced features, such as dashboards with graphical representations of the following:

- Details of the performance of the underlying data networks being used to deliver UCaaS

- Trending reports with threshold-crossing alarms

- Suggestions on corrective actions

- Features to identify root cause

APIs: These include features to support the customization, development or integration of discrete UC features, such as voice and video, meetings, messaging and management, administration or reporting, and analytics. Integration options commonly include:

- Contact centers

- Marketplaces

- Collaboration applications

- Workstream collaboration

- Plug-in or extension integrations for leading cloud business applications

- Communication platform as a service (CPaaS) for digital business application integrations

- Integration with business analytics and AI features

AI-enabled features: With the advent of generative AI (GenAI) and other types of AI (e.g., machine learning), organizations have begun exploring AI-based features in UCaaS platforms. This includes such optional features as:

- Conversation summary for PSTN/internal calls

- AI receptionist

- Agentic functionalities mainly focusing on admin and maintenance for the UCaaS platform

- Suggesting next best actions, based on the conversation

- Automatic creation of reminders for follow-up, based on the conversation

- Alerting based on voicemail transcripts and voicemail summarization

Magic Quadrant

Vendor Strengths and Cautions

8x8

8x8 is a Visionary in this Magic Quadrant. It offers 8x8 Work (for telephony, meetings and team messaging), 8x8 Contact Center and 8x8 CPaaS capabilities. It is preferred mostly by midsize enterprises looking for advanced telephony capability bundled with contact center as a service (CCaaS) solutions. It also serves large organizations in certain verticals, although less often. Its customers are mostly based in North America and Europe. Despite the enhancements last year, there is still an opportunity to improve its meetings and workstream collaboration capabilities, which most enterprises today focus on when selecting a UCaaS platform.

The vendor’s latest enhancements include 8x8 Intelligent Directory (an AI autoattendant), 8x8 Engage (offering omnichannel capabilities), partnering with NICE to deliver advanced contact center solutions tailored for large enterprises, and 8x8 Intelligent Customer Assistant (a self-serve automation capability).

- 8x8 is well-positioned to deliver feature-rich, telephony-centric UCaaS capabilities to organizations that have adopted Microsoft Teams or other cloud office tools for messaging and meetings.

- 8x8 is one of the few UCaaS providers evaluated in this Magic Quadrant offering a mature native contact center platform, which is most suitable for organizations in the small and midsize (SMB) segment. (Large contact center organizations require more mature customer service and AI capabilities than what 8x8 offers.)

- Gartner Peer Insights reviews and Gartner client interactions highlight the product’s intuitiveness, simplicity and ease of use for both users and admins. They also indicate good value at competitive pricing.

- 8x8 has seen consistently sluggish growth for its UCaaS business in the past couple of years, as well as mixed performance for its business outside North America. Multinational organizations considering 8x8 must look at its regionwide capabilities and sales support to determine whether it can meet their needs.

- 8x8 has been losing market visibility among the Gartner client base mostly due to changes in the communication culture and customer preferences, as well as its UCaaS offering being telephony-led and not collaboration-first.

- Almost all other vendors in this research offer integrated solutions with contact center and Microsoft Teams, eroding 8x8’s first-mover advantage. Its integrated contact center and AI offering may not be a good fit for independent or integrated large-scale CCaaS deployments.

Cisco

Cisco is a Leader in this Magic Quadrant. Webex by Cisco offers telephony, messaging, collaboration, meetings, devices and contact center. It is preferred by large multinational UCaaS buyers in highly regulated sectors, and by customers that prioritize integrated management, vendor-provided software and hardware, AI capabilities, and observability. Gartner observes lower Webex adoption in the SMB segment, with buyers seeking the lowest-priced solution.

Cisco’s latest enhancements include Webex Calling Customer Assist (a lightweight contact center), Webex AI Codec (AI-based audio enhancement supporting bit rates of 1.6 Kbps to 6.0 Kbps), AI Assistant, AI-generated Vidcast (AI video generation from PDFs or PowerPoint) and AI-generated Slido polls and quizzes.

- Cisco has continued to invest in AI for customer experience, employee productivity, audio/video intelligence and management portals. AI-driven features provide real-time summaries, enable multilingual support and enhance the meeting experiences with AI Assistant, gesture recognition and immersive video features.

- Cisco is one of few vendors evaluated in this Magic Quadrant offering a fully self-developed portfolio that includes UCaaS, CCaaS and CPaaS software, as well as hardware (such as IP phones, headsets, cameras, meeting systems, gateways, analog telephone adapters and session border controllers). Its end-to-end approach enables greater integration and support.

- Cisco employs an effective vertical strategy, integrating its platform with leading industry-specific applications and addressing specialized requirements and sector-specific certifications, tools and standards. This approach enables customers to more efficiently comply with regulated and complex industry mandates.

- Webex’s robust feature set comes with added complexity, particularly for organizations without existing Cisco expertise. Initial setup and configuration and ongoing management (especially when integrating with legacy Cisco on-premises infrastructure or third-party business applications) require more expertise, effort and time than competing solutions.

- Gartner clients in the SMB segment report that Cisco’s competitors offer lower prices as well as licensing that is easier to understand, evaluate and negotiate.

- Some Cisco customers indicate a preference for utilizing collaboration capabilities from alternative UCaaS providers or from vendors in adjacent software markets that offer integrated collaboration tools. As a result, the value proposition of the comprehensive Webex UCC suite may be diminished for organizations that prioritize collaboration features available from other platforms.

Dialpad

Dialpad is a Visionary in this Magic Quadrant. Its portfolio includes telephony, meetings, messaging, contact center and sales capabilities delivered through the Dialpad Connect, Dialpad Support and Dialpad Sell service bundles. It supports a diverse range of organizations but is particularly strong among SMBs seeking integrated UCaaS/CCaaS-lite capabilities. It operates primarily in North America and Asia. It may not meet the needs of organizations with advanced call routing or customization requirements.

Dialpad’s latest enhancements include its Ai Live Coach with feedback and next best actions, the expansion of AI and real-time transcription support to eight languages, and AI-driven call purpose categorization for analytics and insights.

- Dialpad’s solution is well-suited for organizations seeking intuitive, AI-infused UCaaS capabilities. The unified Dialpad interface and consistent user experience across devices and applications make the solution straightforward and easy to use.

- Dialpad services are generally easy to procure, with transparent pricing across service bundles. The onboarding and implementation processes are streamlined, requiring minimal change management and enabling a seamless customer transition.

- Dialpad continues to expand its market reach through integration with the Google Customer Engagement Suite and new Google Workspace Marketplace incentives. Customers can use Google Cloud Platform spend allocations toward Dialpad services.

- Dialpad’s solution may not meet the needs of organizations with niche or highly customized requirements. Some Gartner Peer Insights reviews cite limited call routing capabilities and basic analytics and reporting features. The vendor also has fewer value-added reseller and system integrator partners with expertise in delivering specialized configurations and integrations.

- Dialpad’s historical differentiation through AI-enabled summarization, customer satisfaction (CSAT) and conversation analytics capabilities has diminished because these features have become standard across most UCaaS/CCaaS-lite solutions, limiting the provider’s unique value proposition.

- Dialpad’s meeting functionality continues to lag behind its competitors. The solution lacks support for survey/polling, live translation, breakout rooms, online meeting storage integration, support for large meetings (over 1,500 users) and full HD video resolution (currently capped at 720 pixels).

Google is a Niche Player in this Magic Quadrant. Its offering comprises Google Meet, Google Chat and Google Voice. It is preferred by midsize organizations, or by organizations with basic telephony needs that have adopted Google Workspace (common in academia, the public sector and nonprofits).

Google’s latest enhancements include AI-driven real-time translation; Gemini AI for meeting recaps; enhancements to noise cancellation and automatic lighting adjustment; call routing enhancements with multilevel autoattendants and ring groups; e-discovery for call, text and voicemail records; and deeper Google Workspace integrations. It has also improved mobile app functionality and accessibility as well as its security features.

Google declined requests for supplemental information about this document. Gartner’s analysis is therefore based on other credible sources.

- Google’s integration of UCaaS capabilities within the broader Google Workspace suite provides access to messaging, meeting, calling and collaboration features directly within familiar applications. This approach is intended to support adoption and enhance the overall user experience. Customer feedback regarding these integrations has generally been positive.

- Google has invested heavily in AI. Its Gemini platform has been integrated across the product portfolio, including UCaaS. Because AI capabilities will likely become a higher priority for UCaaS buyers, this integration may enhance Google’s value proposition.

- Organizations that are already utilizing Google Workspace may benefit from a lower total cost of ownership (TCO) when adopting Google’s UCaaS capabilities, because a range of UC features are included within existing Workspace entitlements.

- Google’s basic telephony offering may not fully address the needs of organizations with operational communications needs, or those in sectors with industry-specific or regional regulatory obligations (such as healthcare, financial services, manufacturing and government). These industries are likely to have unique requirements in support of their regulatory obligations.

- Google’s availability SLA target for all Workspace services — including Meet, Chat and Voice — is 99.9%. This is lower than the targets offered by leading providers in this research, and in the UCaaS market in general.

- Google’s pace of innovation has been more gradual than that of the leading UCaaS competitors. Others have introduced meetings, contact center, messaging and calling enhancements more rapidly than Google has over the past 12 months.

GoTo

GoTo is a Visionary in this Magic Quadrant. Its product, GoTo Connect, provides telephony, meeting, messaging and contact center capabilities. It is particularly well-suited for cost-conscious small or midsize businesses and distributed enterprises seeking streamlined communications functionality. It operates primarily in North America, with an expanding footprint in Latin America and select regions of Europe. It lacks a broad ecosystem of partners for custom integration and collaboration capabilities compared with some other vendors evaluated in this Magic Quadrant.

Recent product developments include the introduction of AI Receptionist, enhancements to GoTo’s AI-driven quality management capabilities, and the extension of quality management and coaching features to all customer-facing employees.

- GoTo Connect is easy to set up and use. The solution is noted by Gartner clients and in Peer insights reviews for its ease of initial configuration and intuitive features and capabilities.

- GoTo differentiates itself through ease of engagement. It has primarily adopted a direct sales and support model, transacting most business directly with customers. Its in-house support is consistent and accessible, and available 24/7. Gartner Peer Insights feedback indicates that GoTo is regarded as approachable and easy to work with.

- GoTo Connect is generally affordable, offering a strong value proposition for businesses looking for low-cost communications services.

- GoTo may not meet the requirements of large enterprises with expansive multicountry operations due to its limited geographic presence in the Asia/Pacific region, Europe and the Middle East.

- GoTo has a relatively limited application marketplace and partner ecosystem. Its solution may be less suitable for organizations with extensive customization needs, particularly those outside of its core verticals of automotive, education and healthcare.

- GoTo’s contact center and meetings capabilities may not be sufficient for organizations that require extensive feature sets such as advanced quality management; integrated AI capabilities designed for customer support; and digital channels, including self-serve capabilities required by mid- to large-scale contact center organizations.

Microsoft

Microsoft is a Leader in this Magic Quadrant. Its product, Microsoft Teams, offers telephony, messaging and meetings. A Teams Premium subscription also includes the Queues app, a lightweight voice-only call center and other advanced meeting capabilities. As a UCaaS solution, Teams is preferred by organizations already invested in it for other uses requiring lightweight telephony capabilities. Its operations are geographically diversified, and customers represent all business sizes, industries and geographies. Teams continues to lack a full-fledged, native in-app contact center functionality.

The vendor’s latest enhancements include Teams AI agents with Interpreter and Facilitator capabilities (currently under public preview); context gathering before call transfer in Teams, using Copilot; monitor, whisper and barge capabilities in the Queues app; and Teams Phone extensibility for Dynamics 365 Contact Center.

- As a UCaaS solution, Teams continues to be preferred by organizations already using it for collaboration, due to its relatively low TCO, its tight integration with other UCaaS vendors and its ease of use.

- Microsoft is one of few UCaaS vendors suitable for multinational organizations requiring telephony capabilities in cloud-difficult geographies — such as India, the Middle East and some parts of the emerging Asia/Pacific market. This is due to its wide reach, sales and service support, and extensive regional telecom carrier partnerships through Direct Routing and Operator Connect.

- Microsoft provides a strong AI foundation for all its offerings, including telephony, meetings, and chat. Although its AI enablement currently focuses more on meetings than telephony, it still has more value-added AI capabilities across the portfolio.

- Microsoft has yet to improve on its admin and endpoint management capabilities through the GUI, along with other advanced telephony features. Gartner clients and Gartner Peer Insights reviews indicate this is a challenge for telephony-heavy organizations in industries such as healthcare, law, retail and hospitality.

- Although Microsoft introduced an independent contact center solution, Dynamics 365 Contact Center, last year, it is not provided along with Teams. The native Teams contact center, with external-facing capabilities provided along with Teams, still remains a pain point for organizations planning to bundle UCaaS and CCaaS from one vendor.

- Teams’ collaboration capabilities are increasingly seen as competition for its own telephony adoption, as many users no longer require a UC or UCaaS telephony platform due to changes in communication culture and increased mobility use.

RingCentral

RingCentral is a Leader in this Magic Quadrant. It offers RingEX and RingCX, which deliver integrated telephony, messaging, meetings and contact center capabilities. It serves organizations of all sizes, especially those requiring advanced telephony capabilities and an integrated UCaaS and/or lite CCaaS. Most of RingCentral’s customer base is located in North America, but it also has a strong presence in Europe. It may not be ideal for price-sensitive small businesses looking for easy-to-implement, “good enough” bundled capabilities.

RingCentral’s latest enhancements include AI Receptionist, with conversational AI; AI Assistant for real-time meeting notes, transcription and summarization capabilities; and Branded Caller ID for recognizable outgoing customer communications.

- RingCentral continues to infuse innovative AI capabilities throughout its service portfolio, providing differentiated employee experience capabilities, such as AI Receptionist and others, to organizations focused on customer-facing roles and lightweight call center functionality.

- RingCentral supports an extensive range of third-party applications, including over 500 prebuilt integrations and tools for use in various unique industries. This enables it to support UCaaS buyers with customized configurations.

- The RingEX solution is frequently noted by Gartner clients as offering intuitive, feature-rich telephony. Notable strengths include seamless call transfer to mobile devices and simplified integration with third-party applications.

- RingCentral’s service and support can be difficult to navigate, with some customers reporting delays in response time and issue resolution.

- Gartner clients cited challenges related to renewals with RingCentral, especially higher pricing and an inability to use the existing UCaaS entitlements from previous contracts.

- While RingCentral’s UCaaS/CCaaS value proposition continues to advance, RingEX’s capabilities remain primarily voice-centric. RingCX’s native advanced analytics and digital engagement features are less feature-rich and need to evolve for large-scale contact centers, but RingCentral’s partnership with NiCE can bridge the gap here.

Sangoma

Sangoma is a Niche Player in this Magic Quadrant. Its product, Sangoma UC, supports telephony, video meetings, messaging, CCaaS, software-defined WAN and CPaaS. Around 90% of Sangoma’s UCaaS customers are located in North America. They are primarily small and midmarket organizations, especially in healthcare and retail, seeking UCaaS bundled with lite CCaaS and CPaaS. Sangoma also offers managed IT services, 5G, VPN and data networking.

Sangoma’s latest enhancements include verticalizing solutions and forging key partnerships, which notably enhance its sector-specific value in healthcare, hospitality and retail. It introduced AI-driven support tools such as ASK Sangoma, revamped its service protocols and enhanced its GenAI platform.

- Sangoma’s UCaaS offering is competitively priced and offers several adjacent services, including CCaaS, CPaaS, and managed software-defined WAN and security solutions, enabling the vendor to be a “one-stop shop” for some SMBs.

- Sangoma is one of few vendors evaluated in this Magic Quadrant with a complete UCaaS solution that includes both cloud services and hardware (such as desk phones, headsets and survivable branch appliances). Hybrid deployments are also possible, combining Sangoma’s on-premises and cloud solutions.

- Sangoma is distinguished by its particularly high customer retention rate. It provides managed services and dedicated customer onboarding teams to help customers. It also extends this program to SMBs, which other providers may not do.

- Sangoma has a very limited presence outside North America. As a result, its cloud and hybrid UC offerings may not be a fit for organizations with a significant presence in geographic locations other than North America.

- Sangoma offers full public switched telephone network (PSTN) replacement in fewer countries than most other vendors, which may affect organizations with broader international requirements. Full PSTN replacement is important to ensure seamless global communication and compliance with local telephony regulations. Additionally, Sangoma’s limited language support and lack of automated transcription features may present challenges for users seeking advanced collaboration and accessibility tools.

- Sangoma’s brand recognition is low among Gartner clients. As the UCaaS market continues to consolidate, vendors with better-established brands continue to see increased adoption at the expense of lesser-known competitors.

Vonage

Vonage is a Niche Player in this Magic Quadrant. It offers Vonage Business Communications (VBC) for telephony, messaging, and meetings; CPaaS; and Vonage Fusion, which brings CCaaS, UCaaS and AI into one intelligent platform, streamlining engagement across midmarket and enterprise customers. It integrates CRM platforms, including Salesforce. Vonage has a strong presence and customer base in North America, but a limited presence in Europe, the U.K., and the Asia/Pacific region.

Vonage’s latest enhancements include expanding its fixed mobile convergence capabilities to support native dialing on both iOS and Android devices, and adding GenAI capabilities such as advanced virtual assistants, knowledge bots, and AI-driven transcription and summarization. It plans to add agentic AI capabilities as well as live translation and transcription.

- Vonage Fusion consolidates UCaaS, CCaaS and AI functions into a single platform, simplifying management for organizations. Its integration with major business tools supports efficient workflows and helps users address customer needs more effectively.

- Vonage has a strong, vertically focused approach for healthcare, finance, retail and manufacturing, including tailored campaigns and integrations. It also offers a broad set of industry-relevant compliance certifications, supporting the regulatory and privacy requirements of customers in highly regulated sectors.

- Vonage has a track record of providing excellent implementation and customer support. Gartner Peer Insights reviews frequently laud the vendor for its excellent customer experience through quick issue resolution and an easy-to-use platform.

- Vonage primarily focuses on the SMB segment and so is less frequently considered by large, global enterprises. Few large-scale Gartner clients report considering it when sourcing UCaaS.

- Vonage’s meetings capability supports a maximum of 200 participants per meeting. It also falls short in its webinar capabilities and advanced external-facing meetings requirements, restricting its adoption among organizations requiring a collaboration-centric UCaaS platform.

- Vonage’s operations and growth in the past couple of years have been mainly concentrated in the U.S. As a result, customers outside the U.S. have reported difficulties with support.

Wildix

Wildix is a Niche Player in this Magic Quadrant. Its product, x-bees, offers telephony, meetings and conferencing. The solution is purely channel-driven and was designed to serve knowledge workers, but mainly is suitable for organizations with heavy frontline worker and customer-facing roles. Wildix’s primary market is Europe. It has a limited presence elsewhere, although it is expanding in North America. It still does not offer a collaboration-centric UCaaS solution, which has lately been the main focus for customers selecting UCaaS solutions.

The vendor’s latest enhancements include expansion of its global sales engineering team outside Europe, the introduction of a sales training academy (a new partner onboarding tool), and native CRM integration enhancements with Salesforce and HubSpot.

- Wildix’s solution is primarily designed for customer-facing and frontline worker roles and industries. It offers strong AI-based capabilities for contact-center-lite operations along with UCaaS solutions, but is mostly focused on customer-facing functions.

- Unlike other telephony specialist UCaaS vendors struggling with growth, Wildix shows consistently strong growth in its UCaaS business. In the past year, it managed to expand beyond its core European market — mostly in North America, but also a little in the Asia/Pacific region.

- Wildix shows a strong organizational culture, which is reflected in its high employee retention and satisfaction. Its culture also contributes to company growth and supports the geographical expansion it is planning for the coming years.

- Wildix primarily supports customer service use cases along with the traditional telephony part, rather than collaboration use cases. This may become a challenge in the future because customers’ decision making is largely influenced by collaboration-specific capabilities rather than telephony, except in specific industries where the collaboration capabilities provided by Wildix may not meet the needs of those organizations.

- Garner Peer Insights reviews show some challenges around stability and audio call quality, as well as around the intuitiveness of the administration and management portal.

- Wildix has low brand awareness among Gartner clients seeking UCaaS solutions. This may make it difficult for Wildix to attain market share and could affect its overall growth.

Zoom

Zoom is a Leader in this Magic Quadrant. Its offering includes telephony, meetings, messaging and contact center. It is preferred by large organizations; those with preexisting Zoom contracts for meetings only; and those in government, education, financial services and healthcare. Zoom has less UCaaS adoption among small organizations, retail organizations and organizations that do not seek collaboration.

Zoom’s latest enhancements include a customizable AI Companion, agentic AI capabilities that automate tasks and expanded functionality within platforms such as Microsoft Teams. It has also released a unified workspace for the full conversation-to-completion journey and new purpose-built vertical solutions for various industries.

- Zoom’s bundled contact center features a simplified setup experience and receives positive feedback from customers for ease of configuration and ongoing management. It also offers native AI capabilities such as automated intent discovery, autotraining, message translation and real-time agent guidance.

- Zoom’s consistent focus on service and support is frequently noted in its high ratings in Gartner Peer Insights reviews. Users share positive feedback regarding the vendor’s support experience, including project implementation, integrations and ongoing operational support.

- Zoom has developed a comprehensive Trust Center and invested heavily in security, privacy, industry standards, compliance, regulatory certifications and attestations, including a specialized Zoom for Government offering that supports the Federal Risk and Authorization Management Program (FedRAMP) and Department of Defense Impact Level 4 (DOD IL4). It has high adoption rates in highly regulated industries such as government, healthcare and financial services.

- Zoom’s licensing strategy has changed more rapidly than the industry average in the past few years. Renewing customers may be presented with updated bundled licenses for Zoom Workplace that include additional entitlements compared with previous agreements, but these may cost more and include unnecessary features.

- Zoom has expanded its portfolio to include Zoom Calendar, Zoom Docs, Zoom Mail and workforce management solutions. As a relatively new entrant in these adjacent markets, it may not yet be competitive against established vendors, and the level of investment in these new offerings may affect its overall financial performance.

- Zoom’s user experience is effective for those utilizing a broad range of its features. However, some Gartner clients have observed that additional functionalities make the user experience more challenging for those who mostly leverage Zoom for meetings.

Inclusion and Exclusion Criteria

To qualify for inclusion in this Magic Quadrant, providers must meet the following criteria.

Self-developed UCaaS core software:

- UCaaS provider must self-develop the core software for calling/telephony.

- UCaaS provider must self-develop the core software for desktop apps, mobile apps and web clients (all of them, not just one or two).

- UCaaS provider must self-develop the core software for meetings (audioconferencing, video-,conferencing and web conferencing).

- UCaaS provider must self-develop the core software for messaging.

- UCaaS provider must self-develop the core software for administrative portals.

- UCaaS provider must offer a bundled contact center that is seamlessly integrated into the UCaaS solution.

- Contact center may be self-developed or may source from a technology partner.

- UCaaS provider must offer quality of service (QoS) monitoring that is seamlessly integrated into the UCaaS solution

- QoS monitoring may be self-developed or may be sourced from a technology partner.

Provider operator core:

- UCaaS provider must operate (i.e., manage, monitor, support and upgrade) the core UCaaS software platform for calling/telephony, messaging, meetings and admin portal.

- Contact center may be operated by the UCaaS provider or by a technology partner.

- QoS monitoring may be operated by the UCaaS provider or by a technology partner.

- Compute, storage and networking infrastructure for back-end UCaaS services can be operated/managed by the UCaaS provider or by a technology partner (e.g., infrastructure as a service [IaaS] partner, telecom partner) user base.

User base:

- UCaaS provider must have a total user base of at least 850,000 paying users with telephony entitlements and domestic calling plans.

- Twenty or more current customers must each have 2,500 or more paying users with enterprise telephony feature entitlements and calling plans for domestic PSTN calling.

Revenue:

- UCaaS provider must have a minimum of $100 million yearly in UCaaS recurring revenue as of 31 December 2024. UCaaS recurring revenue is revenue that is directly connected to monthly or yearly recurring charges for UCaaS licenses/seats, and excludes one-time charges (OTCs) for consulting services, implementation services for new customers, hardware, etc. Gartner requires a letter of attestation from an appropriate finance executive certifying that the minimum revenue requirements have been met.

Geographic serving area and user base split:

- Definition of regions:

- Region 1 — North America: U.S. and Canada

- Region 2 — Europe: the U.K., Ireland, Iceland and Western Continental Europe (Andorra, Austria, Belgium), U.K., Ireland, Iceland, Western Continental Europe (Andorra, Austria, Belgium, France, Germany, Liechtenstein, Luxembourg, Monaco, Netherlands, Portugal, Spain, Switzerland, Italy), Scandinavia (Denmark, Norway, Sweden)

- Region 3 — the Asia/Pacific region: Must include three of the following: Australia, New Zealand, India, Hong Kong, Singapore, Japan and China

- Region 4 — Latin America: Mexico, Central America and South America

- UCaaS provider must have 25,000 or more paying users with telephony entitlements and domestic PSTN calling plans in two or more of the above-defined regions; for example, more than 25,000 users in Region 1, and more than 25,000 users in Region 2.

- UCaaS provider must have 1,000 or more paying users with telephony entitlements and domestic PSTN calling plans in one-third (different region than previous criteria) of the above-defined regions; for example, more than 1,000 users in Region 3.

Sales and support:

- UCaaS provider must have 75 or more directly employed sales and support staff in two (or more) of the above-defined regions. For example: more than 75 directly employed staff in Region 1 and more than 75 directly employed staff in Region 2.

Customer Interest Indicator (CII):

- UCaaS provider must rank among the top providers in Gartner’s CII, as defined by Gartner for this Magic Quadrant. Data inputs used to calculate the Gartner CII factor in a balanced set of measures, including:

- Inquiry volume

- Gartner Peer Insights competitor mentions in reviews

- Twitter and LinkedIn followers

- Gartner.com search volume

- Google trends

- Web traffic analysis

- Overall CII score and ranking

Evaluation Criteria

Ability to Execute

Gartner analysts evaluate providers on the quality and efficacy of their processes, systems, methods and procedures. These factors enable their performance to be competitive, efficient and effective. They positively affect revenue, retention and reputation, in relation to Gartner’s view of the market.

Product/Service

This refers to the core goods and services that compete in and/or serve the defined market. This includes current product and service capabilities, feature sets, skills, etc. This can be offered natively or through OEM agreements/partnerships, as defined in the Market Definition and detailed in the subcriteria.

Key components include:

- UC functionality

- Voice services/telephony

- Personal and team messaging

- Meetings

- Contact center

- Mobility services, desktop and mobile apps

Overall Viability

This includes an assessment of the organization’s overall financial health, as well as the financial and practical success of the business unit. We view the likelihood of the organization being able to continue to offer and invest in the product, as well as the product position in the current portfolio.

Key components include:

- Corporate financial health

- Corporate commitment to UCaaS

- Recurring revenue trends

- Retention of existing customers

- New adoption and customer base trends

Sales Execution/Pricing

This is an assessment of the organization’s capabilities in all presales activities and the processes, resources and structures that support them. These include deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Key components include:

- Conversion rates for sales of full-spectrum UC

- Conversion rates for sales of partial UC services (telephony only, for example)

- Direct sales

- Indirect sales via channel partners

Market Responsiveness and Track Record

This is an assessment of the ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the provider’s history of responsiveness to changing market demands.

Marketing Execution

This criterion assesses the clarity, quality, creativity and efficacy of programs designed to deliver the provider’s message to influence the market, promote the brand, increase awareness of products, and establish a positive identification in the minds of influencers and buyers. This mind share can be driven by a combination of publicity, promotional activity, thought leadership, social media, referrals and sales activities.

Customer Experience

This is an assessment of the products and services and/or programs that enable customers to achieve anticipated results with the products evaluated. Specifically, these include quality buying experiences and interactions, technical support, and/or account management and support. They may also include ancillary tools, customer support programs, availability of user groups and SLAs.

Key components include:

- Procurement experience/ease

- Customer admin portal experience

- Account management

- Technical assistance tools

- Customer support experience

Operations

This criterion assesses the ability of the organization to meet goals and commitments. Factors include the quality of the organizational structure, skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | High |

Market Responsiveness/Record | Medium |

Marketing Execution | Medium |

Customer Experience | High |

Operations | Low |

Source: Gartner (September 2025)

Completeness of Vision

Gartner analysts evaluate providers on their ability to convincingly articulate logical statements about the market’s current and future direction, innovation, customer needs and competitive forces, in light of Gartner’s view of the market.

Market Understanding

This is an assessment of the ability to understand customers’ current and future needs and translate them into products and services. It considers the extent to which vendors show a clear vision of their market, listen, understand customer demands, and can shape or enhance market changes with their added vision.

Key components include:

- Completeness of UCaaS offering across the main pillars: calling, meeting, messaging, contact center and management

- Complementary professional, support, life cycle/change management and managed services

- Track record of UCaaS functionality and services offerings

- Roadmap to evolve the above to anticipate the market’s future needs

Marketing Strategy

This refers to clear, differentiated messaging consistently communicated internally and externalized through social media, advertising, customer programs, demand generation and positioning statements.

Sales Strategy

This refers to a sound strategy for selling that uses the appropriate networks, including direct and indirect sales, marketing, service, and communication. It also includes partners that extend the scope and depth of market reach, expertise, technologies, services and the vendor’s customer base. The use of targeted incentive programs to entice new customers and retain existing ones is also assessed.

Offering (Product) Strategy

This is an assessment of an approach to product development and service delivery that emphasizes the following as the map to current and future requirements:

- Market differentiation

- Functionality

- Methodology

- Features

It also includes the design, logic and execution of the organization’s business proposition to achieve continued success.

Vertical/Industry Strategy

This is an assessment of the strategy to direct resources (e.g., sales, product and development), skills and products to meet the specific needs of individual market segments, including verticals.

Innovation

This criterion assesses the direct, related, complementary and synergistic layouts of resources; expertise and capital for investment, consolidation, defensive or preemptive purposes.

Geographic Strategy

This is an assessment of the provider’s strategy to direct resources, skills and offerings to meet the specific needs of locations outside the “home” or native geography, directly or through partners, channels and subsidiaries, as appropriate for each given geography and market.

Key components include:

- Ability to deliver full PSTN replacement in multiple global regions and countries

- Localization/country homologation (including supported languages in end-user apps, admin portals and audible announcements)

- Local/regional sales and support

- Local currency contracting/billing

- In-region data center and point of presence (POP) locations to enable data sovereignty and enhance performance

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Medium |

Sales Strategy | High |

Offering (Product) Strategy | High |

Business Model | Low |

Vertical/Industry Strategy | Medium |

Innovation | High |

Geographic Strategy | High |

Source: Gartner (September 2025)

Quadrant Descriptions

Leaders

Leaders have mature UCaaS portfolios. They have comprehensive and integrated UCaaS solutions that address the full range of market needs, have a proven ability to serve large organizations, and have a commitment to three or more geographical markets. They have defined migration and evolution plans for their products in core UCaaS areas, and are using their solutions to acquire new customers, expand their geographical footprint and innovate in new functional areas.

Challengers

Challengers have the ability to deliver UCaaS to large organizations. They have yet to become Leaders because their UCaaS solutions lack some elements. Their customer support is still evolving, they do not offer differentiated services or most of their users deploy only certain aspects of UC.

Visionaries

Visionaries have an ambitious vision of the future and are making significant investments to develop unique technologies. Their services are still emerging, and they have many capabilities in development that are not yet generally available. Although Visionaries may have many customers, they might not yet serve a broad range of use cases well.

Visionaries are close to delivering — or are already delivering — differentiated UC functionality or services, but have not yet established themselves in the enterprise market. This may be due to an inability to support multiple large customers, a lack of proven ability to support panregional UCaaS deployments or limited brand-name recognition. Some providers may be Visionaries because of only one or two shortcomings, such as inconsistent customer service.

Niche Players

Providers may be Niche Players for a variety of reasons. For some, it may be because of limited brand recognition or because they lack a robust marketing ability to sell beyond their home region. For others, it may be because their customers are using only a limited amount of UC functionality, their feature set may be weak in certain areas or their customer service may be inconsistent.

Context

Cloud-based UC services have become the standard in most regions, except in certain telecom-regulated areas such as the Middle East, Africa and some less-developed parts of the world. This widespread adoption is driven by the functional and commercial advantages that cloud UC offers over traditional, premises-based solutions. Leading UC vendors have developed distributed, resilient, multitenant solutions delivered via the cloud. Meanwhile, vendors with existing on-premises UC customer bases continue to support these legacy products — primarily in regulated regions — but are no longer investing in new features or innovation, as demand for on-premises solutions continues to decline.

Gartner expects that many legacy premises-based UC solutions will be discontinued over the next five years, as vendors encourage migration to UCaaS. In developed regions, some vendors have already stopped selling new licenses for premises-based UC systems. UCaaS offers superior desktop and mobile user experiences, enhanced mobile capabilities, improved performance and analytics dashboards, advanced collaboration features, and more robust management portals, compared to legacy on-premises solutions.

Additionally, cloud UC solutions require significantly less effort, time and expertise from customer administrators. While premises-based UC demands engineering-level skills to manage, UCaaS is much simpler. As a result, heads of infrastructure and operations almost always prefer UCaaS.

SMBs

With few exceptions, UCaaS has long been the preferred UC deployment model for organizations with fewer than 1,000 employees, which were among the earliest adopters. Exceptions typically include organizations with 500 to 999 employees that:

- Do not anticipate a need for modernizing business communications or collaboration within the next three years

- Possess the expertise to manage on-premises infrastructure

- Maintain such infrastructure at a TCO that is lower than prevailing UCaaS market rates

However, this last scenario is increasingly rare among Gartner clients, and most vendors evaluated in this Magic Quadrant primarily serve this segment.

All SMBs should consider cloud solutions, as the market has become highly competitive, the TCO is generally lower than alternatives and the cost of maintaining on-premises systems continues to rise each year. Innovation in cloud UC is robust, and few organizations wish to continue self-managing legacy infrastructure.

Large Enterprises

Large enterprises — those with 1,000 to 5,000 users — are well-suited to UCaaS. Many of the vendors evaluated in this Magic Quadrant are suitable choices for such organizations,and have long lists of customer references to prove it. Many UCaaS providers that operate in a single global region (and are, therefore, not featured in this research) can also be good options, assuming the buyer only operates in the same region.

Some large enterprises may operate in a hybrid model of vendors for different architectures. Gartner has seen these types of enterprises start deploying collaboration-centric platforms, such as Teams, for a majority of their users and use a telephony specialist vendor such as RingCentral, 8x8 and Dialpad for a small number of users who need more-advanced telephony features. Some of these organizations may migrate the majority of employees to the cloud, but use premises-based infrastructure in countries with restrictive regulatory requirements or unsuitable data network connections.

Very Large Enterprises

During the past few years, the adoption of UCaaS among the largest segment of anything more than 5,000 users has become the default desired option.

Very large enterprises that continue to invest in premises-based UC (including ongoing maintenance and support agreements, upgrades, and patching) should be aware that vendors are allocating minimal R&D budgets to this technology. If organizations buy a new system today, they are unlikely to see significant innovation or enhancements during a typical five- to eight-year product life cycle. Most future enhancements (such as AI, mobility, analytics and advanced UX) will only be available on UCaaS platforms. Nonetheless, premises-based deployments will persist for reasons of regulation and the unavailability or unsuitability of UCaaS in specific regions.

Market Overview

Gartner’s view of the market is highly influenced by transformational technologies and approaches to meeting the future needs of end users. It does not focus solely on the current market needs.

Gartner has observed a significant decline in the traditional use of telephony services across organizations. Many enterprises are actively rightsizing their telephony footprint to realize cost savings, enhance the digital employee experience, and minimize redundancy in capabilities and features across their existing UC platforms.

In recent years, leading UCaaS providers have increasingly prioritized the integration of AI capabilities within their platforms. These everyday AI enhancements are primarily aimed at improving collaboration-oriented use cases, such as meetings, conferencing and team messaging. Additionally, there is a growing emphasis on leveraging AI for select customer-facing telephony applications, further enhancing the overall user experience.

At present, AI does not constitute a primary area of interest for end users and is not widely perceived as a principal differentiator among UCaaS vendors. Nevertheless, Gartner anticipates that the demand for AI-enabled meeting functionalities will grow in the future, as the technology continues to mature and its benefits become more apparent to end users. From a telephony perspective, the applicability of AI-driven capabilities is currently more relevant to particular user groups — primarily those in customer-facing positions — rather than to the broader organizational user base.

AI has emerged as a prominent area of focus for nearly all the vendors included in this research. Despite the increased investment and attention from vendors, demand for AI-oriented use cases within the UCaaS sector has remained relatively limited among Gartner clients. Consequently, AI capabilities are not yet regarded as a fundamental requirement for organizations selecting a UCaaS provider, except in specific scenarios that involve customer-facing roles.

Beyond their core offerings of meetings, conferencing and chat, UCaaS providers are also expanding their portfolios to include adjacent capabilities. Notably, many have begun to offer integrated solutions for contact centers and CPaaS. This strategic expansion enables providers to address a broader range of enterprise communication needs and positions them as comprehensive solutions for UC and customer engagement.

Furthermore, a number of vendors have begun to introduce lightweight call center functionalities in conjunction with their core UCaaS offerings, frequently at little or no additional cost. These features are predominantly intended to support internal IT help desks or basic call center operations, representing a strategic initiative to address a wider spectrum of communication and support requirements within enterprises.

Team Messaging and SMS

UCaaS providers have extended the capabilities of team messaging and workstream collaboration services by adding generative AI for drafting messages or replies and chat summarization, integrating business applications, integrating file-sharing services, adding bot frameworks, and providing connectivity to mobile SMS messaging services from desktops, web clients and mobile apps.

Meetings

UCaaS platforms are rapidly evolving with embedded generative AI features such as real-time transcription, translation, meeting summarization and sentiment analysis, significantly enhancing meeting productivity and reducing administrative workload. AI assistants are streamlining scheduling and postmeeting tasks, while platform convergence integrates UCaaS with CCaaS and CPaaS. Infrastructure upgrades, including 5G adoption and faster platform architectures, are delivering improved performance and reliability, especially for mobile and large-scale meetings.

Looking ahead, meeting technologies are poised to become even more intelligent and immersive. Advancements in AI will enable real-time coaching, automated follow-ups and predictive insights that anticipate participant needs and optimize collaboration.

APIs, CPaaS and App Marketplaces

A capability that has seen increasing market demand is the integration of UC capabilities with business applications that make workflows more efficient. Examples of such integration include CRM applications, workforce management, contact center applications, workgroup applications, IT service management applications, and line-of-business applications. Some UCaaS providers have extended their offerings to include CPaaS. This enables the consumption of “atomized” UC capabilities (for example, the ability to send an SMS or initiate a call) by other applications that are enhanced by integrating and enabling communications services.

Reporting and Analytics Dashboards

UCaaS offerings provide administrative tools that visualize availability, failures, performance, diagnostics, usage, user adoption and other key performance indicators. Dashboard reporting can be measured and displayed on multiple levels, such as call, user, business unit and location.

UCaaS offerings share key characteristics with other cloud services, such as shared infrastructure and management tools, per-user/per-month pricing, and scalable capacity without hardware procurement. Leading providers use multitenant, microservices-based architectures, often leveraging public cloud platforms (e.g., Amazon Web Services, Microsoft Azure, Google Cloud Platform, Oracle) or their own data centers. UCaaS applications are distributed across regional or global service nodes, with some workloads processed in traditional data centers to optimize performance and user experience. Providers manage development, operation and updates of these platforms directly.

Modern UCaaS platforms have greatly improved administrative capabilities by offering centralized dashboards for managing users, devices, licenses and security policies from a single interface. Automation in provisioning, onboarding and device configuration streamlines operations, reducing errors and speeding up service delivery. Enhanced security and compliance features, including AI-driven protocols and real-time monitoring, are especially beneficial for organizations in regulated industries, while cloud-native flexibility allows IT teams to scale services easily for hybrid and remote workforces.

For end users, UCaaS platforms now deliver a unified experience by integrating messaging, voice, video and collaboration tools within one interface, minimizing the need to switch between apps and boosting productivity. AI-powered features such as live call sentiment analysis, postcall summaries and predictive analytics further enhance user engagement and support proactive communication. The emphasis on mobile-first design ensures that users have full access to platform functionalities on smartphones and tablets, while customizable interfaces and feedback loops continuously improve usability.

These advancements are driven by broader technology trends, including the pervasive use of AI and automation for intelligent routing and quality scoring, the adoption of 5G for high-quality real-time collaboration (including AR/VR tools), and seamless integration with business applications like CRM and project management systems. Together, these trends are transforming UCaaS platforms into comprehensive, intelligent hubs for modern workplace communication and collaboration.

The widespread shift to hybrid and remote work across all industries has driven sustained demand for UCaaS. UCaaS enables seamless communication and collaboration on desktop and mobile apps, offering experiences and features comparable to desk phones, but with added convenience and no extra cost. The market has become increasingly collaboration-focused, reflecting users’ growing preference for meetings and messaging tools over traditional telephony. Over the past five years, communication culture has evolved, with users favoring mobile devices and collaboration apps for both internal and external interactions, rather than relying on UCaaS telephony features.

However, certain user roles continue to require traditional telephony features and functionality, and UCaaS telephony has become increasingly focused on serving these specific needs. The telephony market has largely plateaued in terms of feature innovation, while users are rapidly embracing advancements on the collaboration front. Notable enhancements include automatic meeting summarization, recommendations for next best actions, in-meeting language translation, advanced sound suppression and improved quality of experience over unmanaged networks.

Although CCaaS is not the core focus of this research, strong links exist between UCaaS and CCaaS, because SMB organizations often purchase them together. A separate market exists for stand-alone CCaaS offerings aimed at larger (typically with more than 250 agents), higher-volume and more-complex contact centers. These include those, for example, with requirements around workforce engagement and management capabilities, interaction analytics, more intricate and deeper integrations with CRMs and line-of-business applications, and more advanced features.

During the past two years, many UCaaS providers have started offering lightweight, call-center-related capabilities to bridge the gap of providing basic call center capabilities at almost no additional cost. Some UCaaS providers develop and operate their own CCaaS services with all the advanced contact center capabilities, whereas others have partnerships with leading CCaaS vendors that enable them to bundle CCaaS with their UCaaS offerings.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.