Magic Quadrant for CSP 5G Core Network Infrastructure Solutions

22 September 2025 - ID G00826622 - 35 min read

By Peter Liu, Susan Welsh de Grimaldo, and 2 more

As 5G deployment shifts to stand-alone networks and cloud infrastructure, the 5G core market is evolving. Vendors offer innovative solutions with varied go-to-market strategies, leveraging AI, edge computing, and open APIs. Communications service provider CIOs can use this Magic Quadrant to assess 5G core providers.

Market Definition/Description

Gartner defines CSP 5G core network infrastructure solutions as a set of hardwares, software and services that form the intelligent control layer of the 5G network services. It enables communications service providers (CSPs) to deliver scalable, reliable, secure advanced connectivity and digital services to consumers and enterprise users. The 5G core is integral to a wide array of essential functions in the 5G network, encompassing access and mobility management, authentication, subscriber data management, policy control, network slicing and essential switching operations. This market covers CSPs’ deployment of 5G core solutions for the public 5G network.

A significant advancement from 4G evolved packet core (EPC), the 5G core network features service-based architecture and components like access and mobility management function (AMF), session management function (SMF) and authentication server function (AUSF), enabling better flexibility and efficient network management. It supports advanced functions like network slicing and effectively caters to diverse demands.

The use of 5G core offers multifaceted benefits, including enhanced connectivity, speed and personalized network performance. The most popular use cases include:

- Cloud-native design and service-based architecture (SBA), which offer enhanced flexibility and scalability, effectively catering to a wide range of users and devices, from individual consumers to small businesses and large enterprises.

- Network slicing, which helps create multiple virtual networks over a single physical and virtual infrastructure, allowing tailored connectivity solutions for diverse business needs, with different technical and commercial parameters including quality of service (QoS), latency and price, from emergency services to entertainment and industry-specific applications.

- Multiaccess edge computing (MEC) integration with the 5G core provides ultrareliable, low-latency services closer to the user to enable integrated communications and IT service.

Mandatory Features

- User plane function (UPF): Handles packet routing and forwarding, playing a key role in data transmission and internet connectivity for end-user devices

- Unified data management (UDM) and authentication server function (AUSF): Cloud-native subscriber data management and authentication supporting various identification methods and security protocols

- Access and mobility management function (AMF): Authentication and security mechanisms supporting various access types and handling mobility management

- Policy control function (PCF): Centralized policy management supporting quality of service, charging and access control across network functions

- Session management function (SMF): Advanced session establishment, modification and release capabilities supporting diverse services and applications

Common Features

- Network repository function (NRF): Service discovery and registration mechanism that enables network functions to discover and communicate with each other dynamically.

- Network exposure function (NEF): Securely exposes network capabilities to third-party applications and services through standardized APIs.

- Application function (AF): Enables interaction between application servers and the 5G core to request specific network resources or capabilities.

- Charging function (CHF): Manages charging and billing operations for network services and resources used by subscribers.

- Network data analytics function (NWDAF): An optional capability in the 5G core network for advanced data collection and analytics to enhance network management and efficiency.

- Network slice management function (NSMF): Manages the creation, modification, activation, deactivation and termination of network slices, which ensures that each slice meets the specific service requirements for which it is designed.

- Network slice selection function (NSSF): Enables selection of the appropriate network slice instance based on subscriber profile and service requirements.

- Service communication proxy (SCP): Manages signaling traffic by routing control messages between different network functions. SCP simplifies the signaling architecture, provides load balancing and ensures efficient communication within the network.

- Security edge protection proxy (SEPP): Provides security for signaling data and user data that is exchanged between different 5G network operators.

- Non-3GPP interworking function (N3IWF): Facilitates interworking between 5G networks and non-3GPP networks, such as Wi-Fi or other types of wireless networks, enabling seamless connectivity and service continuity across different network types.

- Cloud-native implementation: Support for containerized deployment in public cloud and/or private cloud environments with automated scaling and life cycle management.

- Service-based architecture (SBA): Cloud-native architecture with modular network functions that communicate via standardized APIs, enabling flexible service creation and management.

- Associate network management and services: Involves solution design, build, deployment and support. It also includes monitoring, provision and configuration, security enforcement, and troubleshooting to ensure efficient network operation and reliable connectivity.

- Multiple access technologies including legacy 2G/3G/4G networks and Wi-Fi: Simultaneously supports diverse radio access technologies (2G/3G/4G/Wi-Fi) through unified authentication, consistent policy enforcement and seamless mobility, enabling operators to modernize infrastructure while maintaining backward compatibility with legacy networks.

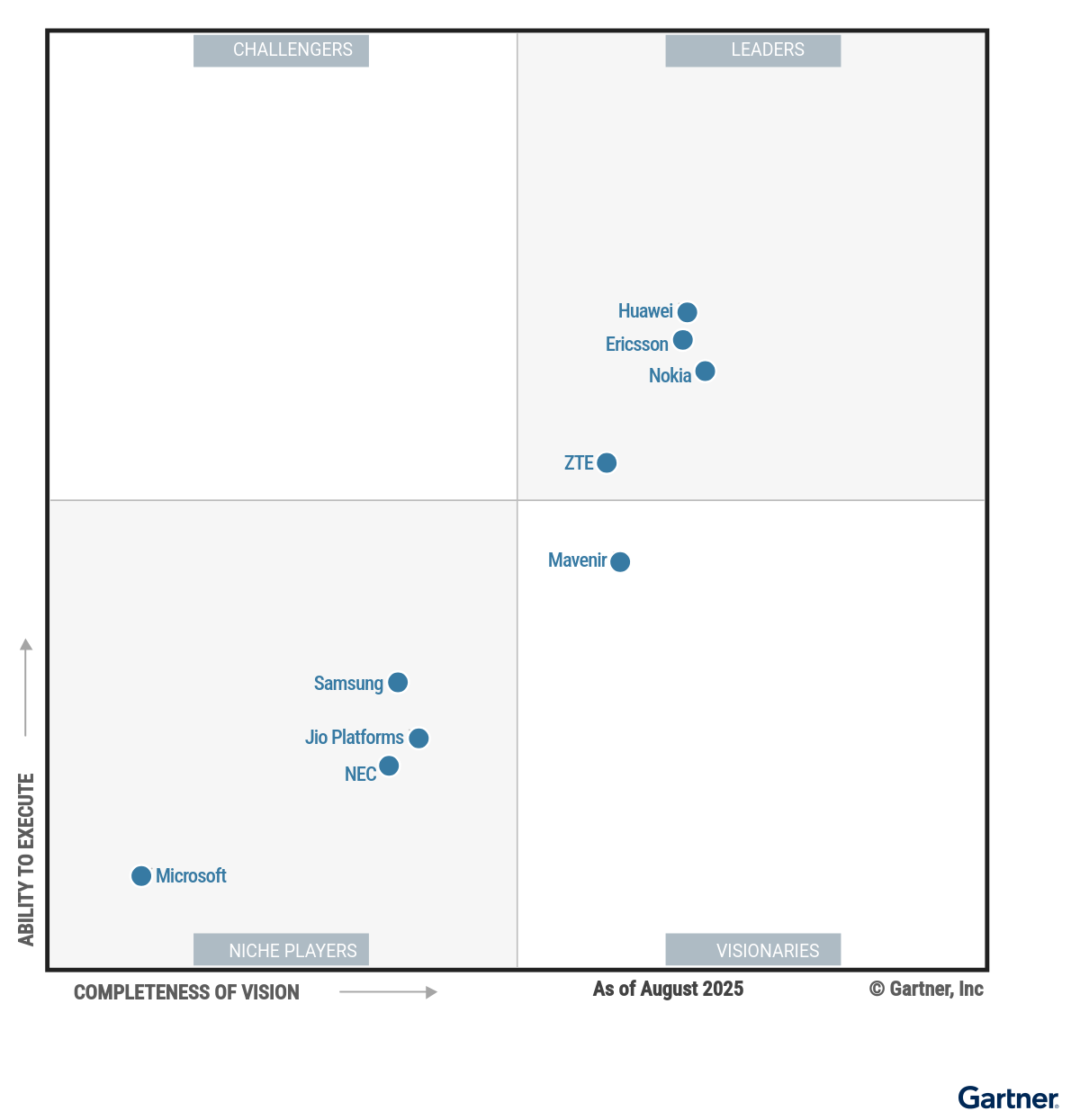

Magic Quadrant

Vendor Strengths and Cautions

Ericsson

Ericsson is a Leader in this Magic Quadrant. It is a multinational networking and telecommunications company headquartered in Stockholm, Sweden. Ericsson’s dual-mode 5G Core solution seamlessly integrates 4G Evolved Packet Core (EPC) and 5G core functionality through a cloud-native microservices architecture, providing comprehensive network convergence capabilities for both stand-alone and non-stand-alone deployments. The company serves global Tier 1 mobile operators across 180 countries with its reliable core network infrastructure. It maintains a strong market presence across the Europe, North America and Asia/Pacific regions.

Ericsson continues to invest in strategic evolution areas, including the development of a cognitive core that is powered by AI and autonomy, driving next-generation network automation, cloud-native architecture, high availability and energy efficiency, its Compact Packet Core, and 5G-Advanced capabilities to enable network monetization through open APIs and differentiated connectivity.

- Global customer base: Ericsson operates 60-plus live cloud-native core deployments serving premium Tier 1 operators across 180 countries. The company addresses diverse customer needs from mission-critical networks to nationwide communications service provider (CSP) infrastructure. Ericsson leverages its extensive radio access network (RAN) installed base for seamless end-to-end integration, with total cost of ownership (TCO) optimization, performance guarantees, reduced risk and unlocking the power of the network to drive innovation as key value drivers for CSP adoption.

- Product/service portfolio: Ericsson offers a well-integrated 5G core portfolio with broad functionality, including dual-mode 4G/5G core, comprehensive network functions, and multi-cloud compatibility across Amazon Web Services (AWS), Google Cloud, Microsoft Azure, Red Hat OpenShift, and VMware. The company’s preintegrated components and automated life cycle management simplify operations while providing industry-leading performance and reliability.

- Market execution: Ericsson leads the market with strong new customer acquisition and business model innovation. The company has won 5G core contracts from Tier 1 operators across the globe, including Airtel, Batelco, O2 (Telefonica), and XL Axiata in 2024. The company offers various business models, including subscription-based pricing that helps CSPs optimize costs and reduce upfront investments.

- Product strategy: Ericsson’s focus on mobile communications may slow its adoption and promotion of innovations and best practices from other technology domains, especially when compared with competitors that have broader portfolios that include Internet Protocol (IP), optical and data center capabilities.

- Integration: Although Ericsson has multicloud strategies and a good track record of third-party cloud infrastructure integration, the company was perceived as less flexible that some competitors when integrating with third-party clouds. Its full-stack preference may raise concerns about integration challenges and increased costs for CSPs pursuing best-of-breed, multivendor strategies.

- AI innovation: While Ericsson demonstrates AI capabilities in core products, competitors lead with more comprehensive AI strategies, including agentic networks and AI-native architectures. This may limit the company’s competitiveness and innovativeness in the evolving AI-driven 5G monetization market.

Huawei

Huawei is a Leader in this Magic Quadrant. It is a global information and communications technology (ICT) provider headquartered in Shenzhen, China. Huawei’s 5G AI Core Network provides a convergent 5G core supporting mobile networks ranging from 2G to 5G-Advanced (5G-A) in a microservices architecture, with integrated AI and autonomous operation capabilities. The company serves major CSPs in most regions, with large-scale deployments in China and select Tier 1 CSP customers across the Asia/Pacific, Middle East, Europe, Latin America and Africa regions.

Huawei continues to invest in its two-phase AI evolution strategy, from 5G-A Intelligent Core to Agentic Core networks, with a primary focus on its Intelligent Personalized Experience (IPE) solutions, 5G-Advanced capabilities, AI-driven autonomous operations, Telco Intelligent Converged Cloud (TICC) and comprehensive B2B solutions across vertical markets.

- Product strategy and innovation: Huawei is a technological leader in the 5G core market, spearheading 5G-Advanced standards development and innovative technologies, supported by substantial R&D investment. This enables rapid commercialization of advanced 5G core features. The company pioneers AI-native 5G core architecture with autonomous operations through agentic AI and digital twins.

- Large-scale deployment and service: Huawei’s 5G core enables large-scale deployment in China. The scalable architecture handles high traffic volumes and massive user bases, backed by Huawei’s Global Technical Service, providing intelligent operations, network optimization, and comprehensive professional services. Deployments extend to operators across the Middle East, Asia/Pacific, Europe, and other regions with demonstrated network and operational reliability.

- Network slicing and monetization: Huawei 5G core delivers end-to-end network slicing with traffic-to-slice monetization through its IPE solution and Network Data Analytics Function (NWDAF)-centered intelligence for real-time user experience optimization. This allows CSPs to create dedicated service instances for specific use cases, optimizing resource allocation and enabling experience-based business models.

- Geopolitical challenges: Geopolitical challenges and security concerns surrounding Huawei’s network portfolio continue to impact its market presence and growth opportunities in North America, parts of Europe, and certain Asia/Pacific regions. These also create uncertainty regarding access to advanced technologies, such as GenAI, and the potential for global collaboration.

- Public cloud partnerships: Huawei prioritizes its own cloud platform capabilities and, unlike its competitors, it lacks extensive public cloud partnerships with major providers like AWS, Google Cloud, and Microsoft Azure. CSPs seeking comprehensive multicloud deployment options may need to evaluate whether the vendor’s approach aligns with their cloud strategy requirements and vendor diversity objectives for hybrid or multicloud architectures.

- Business model flexibility: Huawei’s flexible subscription models currently lack the clarity and standardization needed to fully optimize costs for CSPs. The limited business model flexibility impacts Tier 2 operators and mobile virtual network operators (MVNOs), hindering their ability to leverage “start-small, pay-as-you-grow” models for efficient resource allocation and cost optimization.

Jio Platforms

Jio Platforms is a Niche Player in this Magic Quadrant. It is an Indian multinational technology company and a subsidiary of Reliance Industries, headquartered in Mumbai, India. Jio Platforms’ 5G Combo Core solution integrates 4G and 5G functionality through a cloud-native microservices architecture, offering dual deployment versions: Jio 5G Hyperscale for large-scale traffic and Jio 5G Hyperlite for enterprise and private network deployments. The company operates India’s largest 5G stand-alone (5G SA) network and maintains a strong domestic presence while pursuing global expansion.

Jio Platforms continues to invest in key growth areas, including AI/ML-driven network automation, digital transformation SaaS business models, strategic partnerships with global cloud providers, and aggressive international expansion strategies.

- Large-scale 5G core deployment in India: Jio Platforms operates a nationwide 5G SA network in India with 170 million subscribers as of December 2024, utilizing cloud-native microservices with 4G/5G interworking and network slicing. This provides CSPs with a reference implementation for substantial subscriber loads and service capabilities.

- Strong financial viability supporting R&D innovation: Jio Platforms has secured strategic investments from Google, Meta, and Qualcomm, providing substantial financial backing for R&D and technology development. This enables sustained innovation in 5G core technologies and accelerated development cycles.

- Software development and ecosystem integration: Jio Platforms utilizes software development capabilities with digital ecosystem integration across its JioFiber, JioTV, JioCinema and JioSaavn services. This enables CSPs to access deployment options and diversified revenue streams through integrated digital services.

- Limited global brand recognition: Despite active industry engagement, Jio Platforms’ brand recognition and market presence outside India remain emerging, with limited experience in legacy 3G/4G networks in international markets. CSPs outside India may be concerned about Jio’s service, support, and integration capabilities, particularly for legacy infrastructure and regional resource availability.

- Limited global ecosystem and partner integration: Jio’s core solution has fewer validated partnerships with global system integrators, cloud providers, and specialized telecom vendors compared with established players. CSPs requiring extensive third-party integrations should evaluate the maturity and availability of Jio’s partner ecosystem.

- Limited market maturity and track record: Launched in 2022, Jio’s 5G core lacks a proven deployment history across diverse markets and use cases outside India. This may lead to concerns about deployment uncertainties, performance validation challenges, and limited reference cases for vendor evaluation and due diligence processes.

Jio Platforms declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

Mavenir

Mavenir is a Visionary in this Magic Quadrant. It is a privately owned network software provider headquartered in Richardson, Texas. Mavenir’s cloud-native 5G core provides an end-to-end software solution. The company offers complete 5G core network functions, which also support 4G, 3G/2G, Wi-Fi, and fixed-mobile convergence on the same cloud-native architecture. The company operations span multiple regions, with clients ranging from Tier 1 CSPs to enterprises. Mavenir has achieved notable commercial success and continues expanding into private networks, defense applications, and satellite connectivity. It recently made significant progress in voice-over-NB-IoT calls in nonterrestrial network (NTN) mode.

Mavenir’s future focus is on autonomous operations, multicloud deployment agility, AI-powered network optimization, 5G-Advanced capabilities, enterprise solutions for public safety and utilities, and core SaaS and is aimed at delivering innovation as a service for B2B2X markets.

- Cloud-native leadership: Mavenir demonstrates true cloud-native architecture with platform-independent, decoupled network functions supporting Kubernetes deployment across multiple platforms (e.g., AWS EKS, Red Hat OpenShift, and VMware Tanzu). The solution offers 3rd Generation Partnership Project (3GPP) service-based architecture compliance and AI/ML integration for network scaling, and it eliminates legacy technology dependencies.

- Market execution: Mavenir demonstrates good market execution across various segments, serving diverse CSPs from large and small to incumbents and “greenfield” providers. The company offers flexible options — from single network functions to turnkey solutions, with perpetual, annual, or network-as-a-service models — maintaining a strong presence in Europe and North America.

- Software adaptability: Mavenir demonstrates deep CSP market understanding through platform-independent, decoupled network functions running on any deployment model. The company’s continuous integration/continuous delivery (CI/CD) DevOps-based releases reduce deployment time while supporting flexible deployment across centralized, distributed, and hybrid cloud environments.

- Financial and resources: Although Mavenir’s recent recapitalization, debt elimination, and renewed focus on core business are positive, the workforce reductions over two years — though reportedly outside 5G core — raise concerns around delivery capacity and financial stability. CSPs may require additional validation of Mavenir’s long-term stability and support capabilities.

- Scale deployment: Although Mavenir has diversified its customer base, it lacks experience in large-scale deployments compared with market leaders. This may be a concern of CSPs who require comprehensive deployment and operational support for critical infrastructure that serves large subscriber bases.

- Geographic presence: Mavenir is expanding coverage into regions like the Middle East, but its service delivery and local presence in emerging markets and Asia/Pacific remain limited compared with market leaders. The company lacks extensive on-ground presence and partnerships that are essential for localized support in key growth markets.

Microsoft

Microsoft is a Niche Player in this Magic Quadrant. It is a multinational software and communications technologies company headquartered in Redmond, Washington. It offers 5G mobile core products, including Affirmed UnityCloud and Azure Operator 5G Core (AO5GC), to selected Tier 1 CSPs in the EU, Middle East and U.S.

Microsoft has reconsidered its telecommunications strategy, with AO5GC remaining only in limited preview mode while the company ceases active new customer acquisition and reduces R&D investment in the product. This strategic pivot focuses on AI investments and cloud platform services, positioning Microsoft as a preferred platform partner for established telecom vendors, rather than a direct competitor in the 5G core market.

- Hyperscale cloud infrastructure: Microsoft leverages Azure’s global footprint and web-scale architecture to provide CSPs with proven cloud deployment capabilities across private, public, and hybrid environments, enabling rapid 5G core implementations

- Ecosystem integration: Microsoft has the potential to enable CSPs to offer converged services by integrating 5G core with Microsoft 365, Microsoft Teams and Azure AI services, creating unique revenue opportunities from enterprise customers seeking seamless business application connectivity.

- Cloud-native microservices architecture: Microsoft’s 5G core utilizes containerized web-scale microservices architecture with full Azure integration. This enables disaggregated cloud-centric deployment models that provide service agility and flexibility.

- Strategic retreat: Microsoft’s withdrawal from active 5G core development demonstrates telecommunications is no longer a priority. CSPs requiring dedicated telecom innovation face uncertainty about long-term product support.

- Limited investment: Reduced investment constrains Microsoft’s ability to deliver advanced features like sophisticated policy orchestration and carrier-grade network slicing, creating functional gaps for complex requirements.

- Vendor lock-in: Microsoft’s platform-first approach prioritizes Azure integration over vendor-neutral flexibility. CSPs requiring multicloud deployment may find Microsoft’s Azure-focused strategy limiting for operational autonomy.

Microsoft declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

NEC

NEC is a Niche Player in this Magic Quadrant. It is a prominent ICT vendor headquartered in Tokyo, Japan. The company offers the NEC 4G/5G Converged Core, a fully cloud-native converged mobile packet core that integrates 4G EPC with 5G core functionality. The architecture leverages Control and User Plane Separation (CUPS) with strong third-party control plane (C-Plane) interworking experience, enabling flexible advanced user plane function (UPF) deployment centrally or at edge locations. NEC has demonstrated proven large-scale deployment experience with NTT DOCOMO since 2021 and maintains a strong AWS partnership. The company’s solution supports multiplatform deployment across on-premises and public cloud environments, with autoscaling features.

NEC’s strategy emphasizes open architecture and best-of-breed integration with 3GPP-standardized interfaces, AI/ML integration for vertical industries, and global market expansion through strategic partnerships, including AWS and OREX SAI for international reach beyond its strong domestic Japanese market presence.

- Proven AWS partnership: NEC demonstrates deep AWS integration with verified 5G core deployment on Graviton3 processors, claiming a 72% power consumption reduction over Graviton2. The strategic AWS partnership includes managed services, joint solution development, and certified professional engineers, providing CSPs with enterprise-grade cloud capabilities and sustainability benefits.

- Advanced UPF: NEC’s high-performance UPF leverages CUPS architecture with third-party C-Plane interworking experience, enabling flexible central or edge deployment. The solution delivers upload/download speed improvements and quality-of-experience enhancement while supporting open standards and best-of-breed integration, which has been validated through large-scale commercial deployment with NTT DOCOMO since 2021.

- Industry-centric strategy: NEC’s vision focuses on transitioning from layered, centrally aggregated networks to horizontal distributed networks that co-create new business with industries. The strategy emphasizes network slicing for verticals, hybrid cloud deployment, and API monetization to maximize value-added services rather than just data consumption.

- Dependency on partners for execution: NEC’s niche portfolio strategy, which specializes in a subset of the 5G core functionality, requires reliance on partners for advanced end-to-end solutions. It creates an execution dependency that can increase integration complexity and limit direct market control.

- Limited global market presence: NEC’s market impact is concentrated in APAC, particularly Japan, with limited global competitive success. CSPs with international operations may encounter inconsistent support quality and gaps in local expertise across regions.

- Restricted legacy network support: NEC’s core supports legacy 2G/3G networks only through packet gateway (PGW) interfaces, limiting migration options. CSPs with significant legacy infrastructure may require additional vendor solutions, increasing migration complexity and costs.

Nokia

Nokia is a Leader in this Magic Quadrant. It is a multinational telecommunications and technology company headquartered in Helsinki, Finland. Nokia’s 5G core portfolio delivers fully cloud-native microservices architecture for seamless multigenerational network support, providing end-to-end solutions for both CSP and enterprise deployments through unified core networks and autonomous networks platforms. The company serves global Tier 1 operators with proven infrastructure, maintaining strong market presence across North America, Europe, Asia/Pacific, Latin America, and the Middle East and Africa.

Nokia continues to invest in a monetization-focused strategy for 5G use cases, cloud-native platforms and core SaaS, secure infrastructure operations, intelligent automation capabilities, and AI-powered engineering solutions.

- Product strategy: Nokia offers a comprehensive 5G core portfolio featuring embedded AI/ML, energy efficiency optimization and advanced network slicing capabilities. The company delivers portfolio completeness across multigenerational networks (2G/3G/4G/5G/fixed) with automation leadership and its Network Exposure Function APIs, enabling new monetization opportunities beyond traditional connectivity. In addition, Nokia demonstrates good AI integration with autonomous operations, including AI-enabled agents and GitOps-based intent configuration.

- Business model innovation: Nokia leads with comprehensive business model flexibility that spans traditional licensing, subscription, core SaaS, and managed services, combined with any-cloud deployment capabilities across AWS, Google Cloud, Microsoft Azure and Red Hat platforms. This ecosystem partnership approach with live-customer validation enables CSPs to optimize both business models and deployment architectures based on specific capital expenditure (capex)/operational expenditure (opex) requirements, while supporting seamless evolution from legacy to cloud-native operations.

- Ecosystem and geographic strategy: Nokia maintains one of the largest 4G and 5G installed bases globally. In addition to global presence, Nokia demonstrates strong market execution with regional adaptation strategies tailored to specific market needs. The company also maintains strong developer community engagement through its Core User Group, as well as its Network Exposure Function APIs, enabling CSPs to monetize 5G through B2B2X opportunities while reducing operational complexity.

- Product strategy: Although Nokia demonstrates strong multicloud compatibility, its use of Red Hat as the primary reference platform may raise concerns for CSPs who prefer non-Red Hat platforms regarding integration complexity and support optimization for their non-Red Hat platforms.

- Investment and workforce: Nokia’s overall R&D spending in 5G trails behind other market leaders, and the company’s workforce reduction potential (October 2023 announcement of up to 16% reduction over three years) raises concerns about development speed, technology advancement, and service and support capabilities.

- Market execution: Nokia’s 5G core positioning faces competitive pressure because competitors with stronger RAN portfolios and market share can more effectively cross-sell core technologies and offer integrated end-to-end solutions.

Samsung

Samsung is a Niche Player in this Magic Quadrant. It is a multinational conglomerate headquartered in Suwon, South Korea, with Samsung Electronics managing the network business. The company offers a cloud-native 5G core solution featuring microservices architecture, dynamic orchestration and CI/CD capabilities, supporting 4G, 5G non-stand-alone (NSA), and 5G SA on a common platform with 3GPP Release 16 compliance.

Samsung’s All-in-One-Box” Compact Core is a product made for small-scale enterprises to easily deploy 5G networks with lower operating costs. The “All-in-One-Box” Compact Core supports CUPS (CP and UP separation) architecture for edge computing and multicloud environments. The company has operational experience with large-scale 5G SA deployments across South Korean operators (such as KT, SK Telecom, and LG Uplus) and Japanese operator KDDI.

Samsung continues advancing edge computing integration, AI-driven optimization, and CognitiV NOS (Network Operations Suite) capabilities.

- Commercial-scale deployment experience: Samsung has operational experience with Korean telcos (KT, SK Telecom, LG Uplus), Japan’s KDDI, and TELUS in Canada. Samsung’s 5G SA core supports KDDI’s nationwide network and SK Telecom’s next-generation 5G core trials, providing CSPs with reference implementations and operational insights from live networks.

- Multicloud support: Samsung supports public clouds — such as AWS, Azure, and Google Cloud platforms — and container platforms such as Wind River and Red Hat. This enables CSPs to avoid vendor lock-in and optimize deployment costs. In addition, Samsung uses Intel’s Data Plane Development Kit (DPDK) technology to optimize UPF performance.

- PaaS integration: Samsung’s open-source PaaS integrated with CognitiV NOS provides CSPs with an effective automation platform for accelerated 5G service delivery and standardized management.

- Fewer investments in 5G core technology: Samsung primarily focuses on RAN technology and allocates comparatively fewer resources to 5G core solutions. This may limit the strategic investments and development priorities needed for global 5G core market expansion.

- Limited global market presence, as well as brand awareness: Samsung’s 5G core capabilities are well-proven in South Korea and Japan, but its market penetration and brand recognition elsewhere are not as strong as its competitors.

- Partner dependencies: Samsung’s portfolio is less comprehensive than the Leaders in this research and relies on partners to provide full-stack 5G core solutions, rather than providing in-house capabilities. This may raise concerns of fragmented accountability and integration complexity, especially for CSPs looking for single-vendor responsibility.

Samsung declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

ZTE

ZTE is a Leader in this Magic Quadrant. It is an ICT technology solution provider headquartered in Shenzhen, China. ZTE’s 5G Common Core provides converged support for all mobile generations and fixed access services on a unified platform, built with 5G-service-based architecture and cloud-native microservices technologies. The solution incorporates network intelligence with NWDAF as the core component. The company has a strong presence in its home market, and serves all Tier 1 Chinese operators. It also has good presence in Asia/Pacific, Africa and Latin America.

ZTE continues to invest in 5G-Advanced capabilities, with a primary focus on AI-driven transformation through NWDAF-centered network intelligence, containerization and CI/CD deployment practices, energy-efficient green UPF technology, and strategic partnership expansion across public clouds and open-gateway platforms. These capabilities are not limited to operating on ZTE’s Tulip Elastic Cloud System (TECS) platform; the company is also committed to operating on more global cloud platforms.

- Large-scale deployment: ZTE’s 5G Common Core operates in high-scale networks across Tier 1 Chinese operators and select international markets without sustained service-level outages. The converged core supports multiaccess technologies (2G/3G/4G/5G and fixed access), enabling CSPs to achieve network reliability for massive subscriber bases while preserving legacy investments.

- Product offering: ZTE offers a strong portfolio supporting 3GPP Release 18/19 features, including time-sensitive networking (TSN), IoT-NTN, and NWDAF-based network intelligence. The company provides diverse solutions, including iCube for rapid deployment, and prepackaged solutions for small CSPs and private networks, enabling differentiated services and new monetization opportunities.

- AI-driven enhancements: ZTE’s Automatic Integration Center, big data platform, and uSmartInsight enable end-to-end life cycle management via CI/CD. This reduces costs and enhances automation for CSPs. It’s AI-UPF solution offers built-in LM (large model) for intelligent service identification, key quality indicator (KQI) measurement, load prediction, and network congestion forecasting.

- Geopolitical challenges: ZTE faces challenges in securing 5G contracts outside China due to ongoing geopolitical issues and security concerns about its network equipment. This limits its market exposure in regions such as North America, parts of Asia, and Europe.

- Public cloud partnerships: Although ZTE 5G Common Core supports third-party cloud platforms such as Red Hat and has a good track record of commercial deployment, The company has not yet built strong partnerships with major global cloud providers, which affects its go-to-market strategy, especially as CSPs increasingly prioritize public cloud or multicloud deployment.

- Market execution: ZTE’s heavy reliance on the Chinese market (68% of revenue) limits global diversification and creates vulnerability to regional conditions. The company faces competitive challenges due to limited business model flexibility and smaller 5G market share outside China.

Inclusion and Exclusion Criteria

To qualify for inclusion, a vendor must meet the criteria below:

- The vendor must provide generally available 5G core solutions that include, at a minimum, UPF, AMF, SMF, PCF and UDM functions. These functions can be developed in-house or provided through third-party partners.

- The vendor’s 5G core solutions must have a general availability (GA) date on or before 31 December 2024.

- The vendor must have at least one commercial deployment with a communications service provider (CSP) by 31 December 2024, excluding trials and testing.

- Major events like mergers and acquisitions (M&A) up to 31 December 2024 will be counted for scoring; those occurring after this date until final scoring will be recorded but not evaluated.

Evaluation Criteria

Ability to Execute

To evaluate a vendor’s Ability to Execute, Gartner considered the following criteria:

- Product/Service: Core goods and services that compete in and/or serve the defined market. This includes current product and service capabilities, quality, feature sets, skills, and more. This can be offered natively or through OEM agreements/partnerships. The emphasis is on advanced technological capabilities, strict adherence to 5G standards, scalability, interoperability, robust security features, and flexible support for diverse cloud environments and usage scenarios.

- Overall viability: Includes an assessment of the organization’s overall financial health, as well as the financial and practical success of the business unit. This also includes Gartner’s view of the likelihood of the organization continuing to offer and invest in the product as well as the product position in the current portfolio.

- Sales execution/pricing: The organization’s capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

- Market responsiveness and track record: Ability to respond, change direction, be flexible, and achieve competitive success as opportunities develop, competitors act, customer needs evolve, and market dynamics change. This criterion also considers the provider’s history of responsiveness to changing market demands.

- Market execution: The clarity, quality, creativity, and efficacy of programs designed to deliver the organization’s message in order to influence the market, promote the brand, increase awareness of products, and establish a positive identification in the minds of customers. This “mind share” can be driven by a combination of publicity, promotional activity, thought leadership, social media, referrals, and sales activities.

- Customer experience: Products and services and/or programs that enable customers to achieve anticipated results with the products evaluated. Specifically, this includes quality supplier/buyer interactions, technical support, or account support. This may also include ancillary tools, customer support programs, availability of user groups, and service-level agreements.

- Operations: The ability of the organization to meet goals and commitments. Factors include the quality of the skills, experiences, programs, systems, and other elements that enable the communications service providers (CSPs) to operate effectively and efficiently.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | Medium |

Overall Viability | Medium |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | Medium |

Marketing Execution | Medium |

Customer Experience | Medium |

Operations | Medium |

Source: Gartner (September 2025)

Completeness of Vision

To evaluate Completeness of Vision, Gartner considered the following criteria:

- Market understanding: Ability to understand customer needs and translate them into products and services. Gartner considers whether vendors show a clear vision of their market — listen, understand customer demands, and shape or enhance market changes with their added vision. In addition, the ability to see 5G core in the wider context of CSPs’ overall transformation and monetization strategies is of particular importance, provided this insight is reflected directly in the product roadmap and design of the vendor.

- Market strategy: Clear, differentiated messaging consistently communicated internally, and externalized through social media, advertising, customer programs, and positioning statements. Gartner evaluates the alignment of the vendor’s 5G core marketing strategy with its current market position and its overall 5G core portfolio strategy, including a market segment focus.

- Sales strategy: A sound strategy for selling that uses the appropriate networks, including direct and indirect sales, marketing, service, and communication. Gartner also analyzes vendor partnerships based on the scope and depth of market reach, expertise, technologies, services, and customer base. This includes business models, pricing strategy, and distribution channels for different use scenarios.

- Offering (product) strategy: An approach to product development and delivery that emphasizes market differentiation, functionality, methodology, and features as they map to current and future requirements. This encompasses innovation, differentiation, and considerations such as product performance, architecture, scalability, and portfolio comprehensiveness.

- Business model: The design, logic, and execution of the organization’s business proposition to achieve continued success. Important aspects include value proposition, revenue models, customer segmentation, and distribution channels.

- Vertical/industry strategy: The strategy to direct resources (sales, product, and development), skills, and products to meet the specific needs of individual market segments, including verticals.

- Innovation: Direct, related, complementary, and synergistic layouts of resources, expertise, or capital for investment, consolidation, or defensive or preemptive purposes. This encompasses ongoing demonstration of technological expertise and leadership, allocation of adequate R&D budget, involvement in and contribution to 5G-core-related standardization and associated technologies, and facilitation of ecosystem partner support. This also includes fostering co-innovation through collaborative initiatives with partners, customers, academic institutions, and other stakeholders.

- Geographic strategy: The provider’s strategy to direct resources, skills, and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels and subsidiaries, as appropriate for that geography and market.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | Medium |

Marketing Strategy | Medium |

Sales Strategy | Medium |

Offering (Product) Strategy | Medium |

Business Model | Medium |

Vertical/Industry Strategy | Medium |

Innovation | Medium |

Geographic Strategy | Medium |

Source: Gartner (September 2025)

Quadrant Descriptions

Leaders

Leaders distinguish themselves by offering services suitable for strategic adoption and having an ambitious roadmap. With a comprehensive portfolio, they can address a broad range of use cases, though they may not excel in all areas or be the best for specific needs. Leaders in this market have significant market share, numerous referenceable customers, strong service and support capabilities, and good customer references.

Challengers

Challengers are well-positioned to serve specific market needs with targeted services. They deliver reliable and effective solutions for particular use cases and have a proven track record of successful delivery. However, they are not adapting to market challenges sufficiently or quickly, and often lack a broad, ambitious vision. This can limit their ability to expand beyond their current offerings and address a wider range of customer needs.

Visionaries

Visionaries have an ambitious vision of the future and are making significant investments in the development of unique technologies. Their offerings are still emerging, and they have many capabilities in development that are not yet generally available. Although they may have many customers, they might not yet serve a broad range of use cases well or may have a limited geographic scope.

Niche Players

Niche Players may be excellent providers for particular use cases or in regions in which they operate, but they should ultimately be viewed as local or specialist providers. They often do not effectively serve a broad range of product portfolios, nor do they have a broadly ambitious roadmap. Some may have solid leadership positions in markets adjacent to this market, but have developed only limited capabilities.

Context

This Magic Quadrant evaluates communications service provider (CSP) 5G core infrastructure vendors and assesses their execution in 2024 alongside future development plans. This evaluation is time-sensitive because vendors and markets evolve.

Readers should not use this Magic Quadrant in isolation as a tool for selecting vendors and products. They should treat it as one reference point among the many required to identify the most suitable vendor and product. When selecting a 5G core solution, they should use this Magic Quadrant in combination with the companion Critical Capabilities research and other Gartner reports. We also recommend using Gartner’s client inquiry service.

In addition, Gartner also advises readers to assess and evaluate vendors beyond this list based on your own needs:

- Evaluate at least two 5G core infrastructure vendors to ensure service continuity and facilitate smooth negotiations.

- Assess each vendor’s willingness to collaborate with other stakeholders, including competitors, to support the CSP’s network modernization goal.

- Perform a business value assessment to determine alignment with the CSP’s primary business objective.

Market Overview

The 5G core market is experiencing rapid transformation as operators accelerate stand-alone (SA) deployments. GSA (Global Mobile Suppliers Association) data shows 154 operators have launched 5G SA services globally, representing 24.7% of operators investing in 5G licenses as of January 2025.

Market Evolution and Monetization

Although building large-scale networks that provide broadband connectivity remains the primary business model for 5G core deployments, communications service providers (CSPs) still prioritize performance, capacity, resilience, multigeneration support, and simplified operations for fast and cost-effective rollouts.

In the meantime, the market has evolved beyond initial connectivity deployments toward sophisticated monetization platforms. CSPs are increasingly leveraging 5G core capabilities for network monetization beyond consumer Enhanced Mobile Broadband (eMBB), including fixed wireless access (FWA), enterprise solutions, satellite connectivity, and massive IoT deployments. This shift is driving demand for cloud-native architectures that support advanced features like network slicing, dynamic resource allocation, and multiaccess edge computing integration.

The integration of artificial intelligence and machine learning, and the ability to orchestrate AI/ML capabilities through the Network Data Analytics Function (NWDAF), is becoming a key differentiator. Open APIs and edge computing solutions are gaining traction, allowing CSPs to offer more tailored services and tap into new revenue streams.

Competitive Landscape and Market Dynamics

The market demonstrates consolidation around established players, with newcomers facing significant barriers to compete in public 5G core networks. Traditional leaders maintain market dominance through comprehensive portfolios and proven execution capabilities, making entry challenging for new vendors.

Key market trends include:

- AI integration acceleration: Heavy investment in AI-native capabilities from all vendors, with solutions evolving from add-on features to core differentiators

- Business model innovation: Shift toward subscription-based, usage-based, and outcome-based pricing models, with vendors offering flexible commercial arrangements from single-network-function licensing to turnkey network-as-a-service solutions

- Network slicing for enterprise: Network slicing, enabling operators to address new B2B use cases with improved SLA and security, that is becoming central to enterprise service differentiation and private network deployments

- 5G-Advanced development: Evolution toward RedCap, enhanced positioning capabilities, and next-generation features preparing foundation for 6G transition and improved enterprise use cases

- NTN/satellite growth: Nonterrestrial networks gaining prominence, with 77 publicly announced partnerships between operators and satellite vendors across 43 countries, primarily for rural coverage expansion

Technology Innovation and Cloud-Native Transformation

Cloud-native architecture has become table stakes for market participation, with 72% of new deployments adopting cloud-native approaches, according to vendor deployment data. The market is seeing convergence toward microservices architectures, containerization, and CI/CD deployment practices. Yet, significant variation in specific tools exists across vendors. Vendors are further differentiating through automation capabilities, with solutions like intent-driven 5G core automation and zero-touch operation becoming competitive advantages.

Innovation focuses on:

- Data-driven 5G core with NWDAF implementation for intelligent network insights and predictive analytics

- AI-powered operations and engineering with foundation models enabling autonomous network management

- Cloud-native platforms and SaaS delivery models from innovation-as-a-service to full commercial B2B2X offerings

- Security-hardened infrastructure with rapid vulnerability responses for enterprise and government applications

- 5G-Advanced capabilities, including RedCap evolution and enterprise WAN solutions for public safety, utilities, and defense sectors.

Vendors differentiate through comprehensive partnership ecosystems and specialized vertical market focus.

Market Challenges and Future Outlook

Despite strong growth momentum, the market faces several challenges. Geopolitical factors continue to influence vendor selection, particularly affecting Chinese vendors’ market access in certain regions. Additionally, the complexity of 5G SA implementations requires new operational skill sets and significant infrastructure investments, creating adoption barriers for some CSPs. In addition, network resilience concerns following multiple service-impacting outages is increasing.

The market is also experiencing pricing pressure as CSPs seek to optimize return on investment. This is driving innovation in commercial models, with successful vendors offering transparent pricing structures, subscription-based licensing, and value-based pricing tied to customer success metrics.

Looking forward, the market is positioned for continued growth that is driven by enterprise 5G adoption, private network deployments, and emerging use cases in Industry 4.0, autonomous vehicles, and smart cities. Vendors demonstrating technical innovation, commercial flexibility, and strong execution capabilities are best-positioned to capitalize on these opportunities, while the market increasingly rewards specialization and customer-focused solutions over traditional vendor relationships.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.