Magic Quadrant for AI Application Development Platforms

ARCHIVED

17 November 2025 - ID G00828116 - 42 min readBy Jim Scheibmeir, Mike Fang, and 2 more

Software engineering leaders’ top priority is to infuse AI into products. AI application development platforms streamline the process of building AI agents, assistants and multimodal applications. Use this evaluation to identify suitable vendors based on your organization’s needs.

Market Definition/Description

To provide clients with a more thorough evaluation of this market, we have replaced our Market Guide for AI Application Development Platforms with this new Magic Quadrant.

Gartner defines AI application development platforms as those that offer the required technology and workflows to design, build, test and deploy AI-embedded applications. These platforms provide access to foundation models and the capability to ground and place guardrails around them. Software engineering teams utilize these platforms to build AI applications, such as assistants, agents and multimodal applications.

Software engineering leaders face increasing pressure to incorporate AI into their products. AI application development platforms host the necessary tooling for enterprise developers to build AI assistants, agents and multimodal apps without extensive knowledge of machine learning. AI application development platforms focus on providing the features developers need to ground models with organizational knowledge. They also reduce risk by implementing responsible AI processes and guardrails within their AI-embedded applications. These platforms help scale the development of AI-embedded applications by offering governance, evaluation metrics and support throughout the application life cycle. Not every platform will offer access to first-party models or application-testing capabilities.

AI application development platforms support building the following types of applications:

- AI assistants leverage large language models (LLMs) to deliver functionality not obtained with traditional conversational AI technology. AI assistants enable improved Q&A support, new customer service and experience features, perform simple task automation and improved value outcomes.

- AI agents can plan and automate more complex tasks, make informed decisions, interact with their surroundings, orchestrate with other tools and AI agents. AI agents are semiautonomous or autonomous applications that may utilize a variety of AI techniques to identify patterns in their environment, make decisions, execute a sequence of tasks and generate outputs to achieve a defined goal.

- Multimodal applications combine multiple modalities (image, text, audio) to provide new experiences. Humanize and enhance the creativity of internal and customer communications, enabling hyperpersonalization. These nascent solutions utilize advanced natural language technologies (NLT), virtual assistants (VAs), graphic creation tools, computer vision, audio creation, and multimodal and emotional AI.

Mandatory Features

- Framework support for pro-code and low-code developers, enabling the authoring and enhancement of AI assistants, AI agents and multimodal applications

- Foundation model grounding capabilities to enhance accuracy and usefulness by utilizing organizational knowledge sources

- Guardrails that protect an organization’s reputation by reducing the risk of harmful material being entered into or generated by foundation models

- Model catalogs that offer access to leading commercial and open-source foundation models.

- Deployment capabilities for both cloud and hybrid runtime environments

- Governance capabilities for AI system auditing and monitoring

- Evaluations, prebuilt or custom, to assess the performance of the model or application

Common Features

- Security and risk management features, including data loss prevention, sandbox environments, identity and access management capabilities and more to protect enterprises and their customers

- AI router to direct prompts to LLMs and providers based on use case, performance, accuracy and cost

- AI gateway to provide additional rigor during LLM provider or model outages, ensuring business continuity and disaster recovery of AI applications

- Observability to track logs, tracing and metrics across the entire application stack

- Advanced foundation model grounding capabilities, such as knowledge graph, chunking and rerank

- Composability with other open-source or commercial offerings, such as multiagent framework, guardrail, observability and data grounding

- Emerging protocol support for communication across agents or to leverage shared tools and data sources

- Simulations used to mimic environments for AI agent development or operations, enabling optimization, what-if analysis and scenario planning to ensure the robustness of your AI applications

- Catalogs and marketplaces for tools, data sources, prebuilt agents, and other components

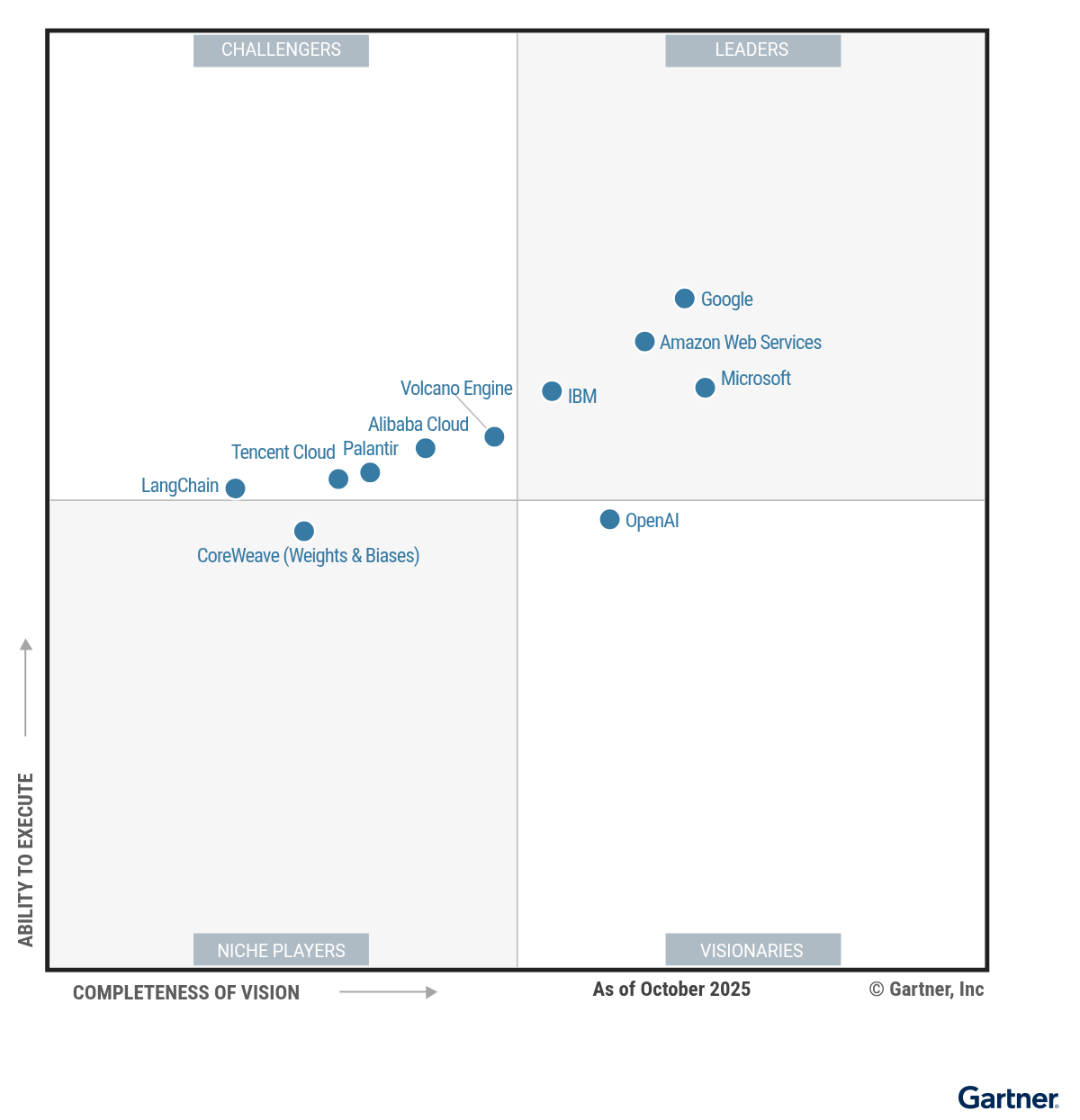

Magic Quadrant

Vendor Strengths and Cautions

Alibaba Cloud

Alibaba Cloud is a Challenger in this Magic Quadrant. It offers Alibaba Cloud Model Studio, which includes model APIs and fine-tuning services and tools including RAG, search, function calling and Model Context Protocol (MCP). Model Studio can be deployed on-premises or as a fully managed service.

Alibaba Cloud’s AI application development platform customers are mainly in China and the Asia/Pacific region. It plans to launch new data centers in South Korea, Malaysia, Thailand, the Philippines and Singapore. Its fastest-growing verticals are technology, financial services and automotive. In 2025, Alibaba Cloud introduced its agent development experience, which includes an MCP server with more than 50 tools and integrations. It also enhanced its Qwen family of open-weight models.

- Overall Viability: Alibaba, the parent company of Alibaba Cloud, generated more than $130 billion in revenue in FY25. For the quarter ended 30 June 2025, Alibaba Intelligent Cloud group’s revenue grew by 26%. The company’s massive scale and sustained growth provide a stable foundation for innovation and long-term customer confidence.

- Sales Execution/Pricing: Alibaba Cloud serves hundreds of thousands of paying customers, with significant growth in net new customers during the past 12 months. It offers flexible licensing options to help enterprises manage costs, and it offers free trials and inference credits to attract developers. Alibaba Cloud’s streamlined sales process results in deals closing in about two weeks on average.

- Business Model: Alibaba Cloud Model Studio combines flexible, consumption-based access to models, powerful application tools and robust infrastructure. Its model layer features self-developed and open-source Qwen models. The service layer offers additional models and tools like MCP to support building and deploying AI agents. Its platform layer provides the infrastructure and tooling needed to scale model development and AI application deployment.

- Market Responsiveness/Record: The vendor’s recent releases have not effectively differentiated Alibaba Cloud Model Studio from competing offerings, especially in terms of its cost management, and application deployment features. For example, Model Studio provides basic cost telemetry, requiring that developers track token usage to manage costs well.

- Customer Experience: Alibaba Cloud uses fewer customer feedback mechanisms than other vendors evaluated in this Magic Quadrant, which hinders its ability to gather insights and shape its product roadmap in alignment with evolving customer needs.

- Market Understanding: Alibaba Cloud needs to expand its partner program to better serve the horizontal and vertical needs of its current and future customers.

Amazon Web Services

Amazon Web Services (AWS) is a Leader in this Magic Quadrant. It offers Amazon Bedrock, a fully managed service that provides access to leading foundation models and tools that enable developers to build and deploy AI applications and agents.

AWS’ AI application development platform customers are global, with many residing in Europe and North America. It plans to expand in Saudi Arabia, Chile and the AWS European Sovereign Cloud. AWS’ fastest-growing verticals include healthcare and life sciences, telecommunications, and financial services. It recently released Strands Agents, a code-first, open-source Python SDK for building AI agents.

AWS AgentCore launched in July 2025, after the cutoff date for this research. Thus, it was not included in this year’s evaluation. Similarly, the New Zealand region was launched in September 2025.

- Vertical/Industry Strategy: AWS has developed the AWS Marketplace as a central hub for prebuilt AI agents that span numerous key industries. AWS, along with partners, has also added specialized models to Amazon Bedrock and Amazon SageMaker AI, such as TelClaude for telecom operational efficiency and Nova Premier for advanced multimodal media capabilities. The platform supports industry data formats like FHIR and OSDU, and enables model fine-tuning with solutions like AWS-GE HealthCare imaging models.

- Innovation: AWS has introduced Automated Reasoning (AR) checks as a new policy in Amazon Bedrock Guardrails to help mitigate AI hallucinations by validating the accuracy of content generated by foundation models against domain knowledge. AR checks use neurosymbolic AI, which combines neural networks with symbolic reasoning.

- Overall Viability: AWS is backed by its parent company, Amazon, which generated more than $630 billion in revenue with double-digit growth in FY24. Amazon continues to invest in AI R&D for internal use and within AWS services and technology. Enterprise customers can be confident about AWS’ ability to support innovation and remain viable in the long term.

- Marketing Strategy: AWS can be more outspoken about its specific vertical solutions at the corporate level. Customers in certain industries would benefit from broader communication on how AWS solutions are able to address their unique needs.

- Sales Strategy: AWS has an opportunity to complement its technical messaging with enhanced business value messaging for executive and line-of-business stakeholders. Providing these buyers with clearer connections between Amazon Bedrock’s capabilities and strategic business outcomes could help other personas with purchasing power better understand the platform’s business value.

- Business Model: Other vendors are more aggressive than AWS in terms of acquiring AI technologies and recruiting talent. AWS’ reliance on organic innovation and strategic partnerships may impact its advancement pace.

CoreWeave (Weights & Biases)

CoreWeave (Weights & Biases) is a Niche Player in this Magic Quadrant. It offers Weights & Biases, an AI platform it acquired in 2025. CoreWeave supports context engineering, evaluations, guardrails, observability, inference and deployment of AI models. It offers both a self-hosted and fully managed service offering.

The Weights & Biases product has global customers across North America, EMEA, Japan and the Asia/Pacific region. In 2025, CoreWeave released new observability capabilities within the Weights & Biases product, including tools for debugging, evaluating, monitoring and safeguarding AI agents.

CoreWeave expanded into reinforcement learning (RL)-based agent development with the acquisition of OpenPipe in September 2025. The Weights & Biases platform has recently added serverless RL to help enterprises post-train large language models on agentic tasks. These activities occurred after the cutoff date for this research and were not included.

- Vertical/Industry Strategy: CoreWeave has been expanding the breadth of its AI developer platform from AI training workloads to AI inference with the acquisition of Weights & Biases. The company is developing solution accelerators to help telecom companies modernize their contact centers, prebuilt AI agent evaluations for financial services, and no- and low-code workflows that help organizations move from prototype to production. CoreWeave’s strategy is to partner with leading model, framework and protocol providers.

- Sales Execution/Pricing: CoreWeave closes deals for its application development platform quickly — within two to six weeks on average — and it offers multiple license models and tiered service levels for flexibility. The company provides several free and trial programs, including a free tier for personal development and inference, bundled usage credits with Pro and Enterprise packages, and a forever-free offering for academic research.

- Marketing Execution: CoreWeave positions Weights & Biases as an end-to-end AI developer platform, emphasizing its speed, security and flexibility. It conveys these messages through sponsorships such as Aston Martin, ads at major third-party and computing events, high-profile partnerships, paid advertising, email campaigns, webinars, and content syndication. Its executive programs feature retreats with AI leaders.

- Product or Service: CoreWeave doesn’t offer its own agent framework and protocol. Instead, the company integrates with popular frameworks such as the OpenAI Agents SDK and protocols such as MCP. The company’s inference service, W&B Inference, supports only open-weights models. However, customers can work with any model — proprietary, open or custom — when using W&B Models and W&B Weave.

- Operations: CoreWeave has fewer industry and compliance certifications than other vendors evaluated in this Magic Quadrant.

- Customer Experience: In our customer reference survey, a few clients indicated they were looking for a new platform — more so than for other vendors included in this analysis. Additionally, the Weights & Biases platform did not show up as a consideration for customers of other tools. CoreWeave’s acquisition needs to focus on addressing these concerns and increasing industry visibility.

Google is a Leader in this Magic Quadrant. It offers Vertex AI, a unified AI development platform that includes Agent Builder, Model Builder and Model Garden. Its platform supports data preparation, model and agent development and runtime, and security and governance. It is typically used as a hosted solution on Google Cloud, although Vertex AI on Google Distributed Cloud supports both on-premises and edge deployments.

Google’s AI application development platform customers are global, with many in Europe and North America. Google is expanding in the Asia/Pacific region, especially in India, Japan, Korea, Singapore and Australia. Its fastest-growing industries are software and internet, telecom, and retail and consumer packaged goods. In 2025, Google introduced the Agent2Agent (A2A) Protocol.

Google recently introduced Gemini Enterprise, a platform for teams to build, scale and govern AI agents through a code, visual or chat interface, and the Agent Payments Protocol to enable secure payment transactions for agents.

- Innovation: In 2025, Google introduced the A2A protocol (since donated to the Linux Foundation), which enables agents from different developers and platforms to communicate and work together. The A2A protocol helps reduce vendor lock-in and create a more open AI agent ecosystem, enabling developers to orchestrate more complex workflows. Google also released Vertex AI on Google Distributed Cloud to support secure on-premises and edge deployments, which appeal to organizations with strict data sovereignty, security and privacy requirements.

- Overall Viability: Google’s parent company, Alphabet, generated more than $350 billion in revenue in FY24, and Google Cloud reported 30% growth for that year. Google is continuing to make large investments, such as the planned acquisition of Wiz, the hiring of Windsurf staff and continued R&D investments in Google DeepMind and global infrastructure, to drive continued AI innovation.

- Sales Execution/Pricing: Google’s license options are among the most flexible of any vendor in this assessment. Google supports developers with open-source tools such as its recently released Agent Development Kit. Google also provides promotions for startups, academic programs and other free trial plans to attract new users, and it has established strong implementation partner relationships with Accenture, Cognizant, Deloitte, Onix and Quantiphi.

- Business Model: Google’s business model for Vertex AI continues to rely primarily on a pay-as-you-go pricing structure. While it has introduced a subscription model for SaaS offerings and guaranteed AI model throughput, the rate at which it is transitioning to these new revenue streams risks losing competitiveness.

- Marketing Execution: Google’s market awareness is still maturing relative to its competitors. To help prospective customers understand and realize the value of its offerings, Google needs more targeted marketing campaigns to increase mind share and demonstrate effective conversion strategies.

- Customer Experience: Google Cloud customers were impacted by an outage on 12 June 2025 that Google addressed; it has since implemented measures for future prevention. Select customers reported below-average scores in Vertex AI’s deployment capabilities and governance.

IBM

IBM is a Leader in this Magic Quadrant. It offers watsonx, which includes watsonx.ai, watsonx.data, watsonx.governance, watsonx Orchestrate and its Agent Builder capability. IBM offers watsonx as a fully managed service hosted by IBM Cloud or via AWS Marketplace, or customers can self-host.

IBM’s AI application development platform customers are global. IBM is expanding the reach of watsonx in North America and Europe via partnerships with AWS and Azure and by extending further within IBM Cloud. IBM’s fastest-growing verticals are financial services, government/public sector and professional services. In 2025, IBM launched the watsonx Orchestrate Agent Development Kit, a pro-code framework that allows developers to rapidly build, test and deploy AI agents.

- Marketing Execution: IBM is making strong structural investments in its marketing program. It targets software engineering leaders, developers and the C-suite with promotion of domain-specific solutions, especially those in customer care, HR, sales, banking and telecom. It leverages its Formula 1 and Wimbledon sports partnerships and its strong social media presence to attract new customers.

- Market Understanding: IBM demonstrates a comprehensive understanding of this market by addressing the key factor of openness. This is evidenced through its release of all Granite models as open weight, under the permissive Apache 2.0 license; its creation of the open-source BeeAI Framework; and a command-line interface that supports popular open-source AI agent frameworks.

- Business Model: IBM’s value proposition appeals to a wide range of customers, as it focuses on maintaining cost-efficiency, supporting AI agent technologies, enabling openness and prioritizing privacy. To support these outcomes, IBM runs sponsor programs, embeds product and independent software vendor partner solutions for insights, and uses technology to capture customer metrics.

- Customer Experience: Customer reference survey scores for observability and prebuilt agents were lower for IBM watsonx compared to other Leaders in this research.

- Offering (Product) Strategy: IBM’s multimodal capabilities within its watsonx offering lag behind most competitors in this research. Customers that have innovative or emerging use cases with avatars or digital humans must look elsewhere.

- Geographic Strategy: IBM watsonx’s current compliance certifications lag behind some vendors in specific regions.

LangChain

LangChain is a Challenger in this Magic Quadrant. It offers two open-source AI application frameworks, LangChain and LangGraph, and one commercial platform: LangSmith for agent evaluations, observability and deployment. LangChain offers a self-hosted, private cloud version of its products and a fully managed SaaS version.

LangChain’s customers are primarily in North America, and it is expanding in Europe. LangChain’s fastest-growing verticals include technology, financial services and retail. In 2025, LangChain released LangSmith Deployment (formerly called LangGraph Platform) for general availability. This paid offering is designed for enterprise development teams to deploy, scale and manage agent-based workflows in a stateful environment.

- Marketing Execution: LangChain effectively targets diverse technical buyers, especially AI engineers, platform engineers and AI development team leaders. The vendor consistently engages prospective customers through events, community engagement, paid channels and strategic partnerships, while maintaining a strong presence on streaming and social channels.

- Marketing Strategy: LangChain’s value proposition emphasizes reliability and faster delivery of agent-driven solutions. It also targets AI and platform engineers as top buyer personas. This strategy reflects a sharp awareness of evolving industry needs and resonates with technical audiences.

- Vertical/Industry Strategy: LangChain is executing a more verticalized field marketing strategy based on regional alignment, such as targeting financial services in New York and high tech in San Francisco.

- Product or Service: Compared to offerings of other vendors evaluated in this research, LangChain lags behind in terms of multimodal capabilities, cost optimization features, and the breadth and depth of its first-party model catalog and contributions.

- Operations: LangChain’s compliance certifications lag behind those of Leaders in the market, which will limit its appeal to customers in highly regulated industries that require CSA, PCI, FedRAMP or FISMA certifications.

- Sales Strategy: LangChain is not generating sufficient sales through its partner strategies, suggesting a need to strengthen or diversify its channel approach to effectively reach prospective customers. The vendor is also relatively slow at closing deals compared to competitors.

Microsoft

Microsoft is a Leader in this Magic Quadrant. Azure AI Foundry operates on a platform as a service (PaaS) business model designed for enterprise-scale AI applications. It monetizes through consumption-based pricing, offering both pay-as-you-go and provisioned throughput options.

Microsoft’s Azure AI Foundry customers are global. Azure AI Foundry is introducing additional data residency options in Indonesia, Malaysia and Spain, as well as additional options in U.S. Azure government environments. Microsoft’s fastest-growing verticals are healthcare, manufacturing, and retail and consumer goods. In 2025, Microsoft upgraded Azure AI Foundry Agent Service by adding MCP support, and it launched the Agent Factory framework for enterprise agent development.

- Product or Service: Microsoft’s open-source agent framework and Azure AI Foundry provide customers with advanced capabilities for AI orchestration and multimodal application development. The platform is expanding its model catalog and deployment options. With the release of the Foundry extension for Visual Studio Code, Microsoft has further improved the developer experience.

- Overall Viability: Microsoft continues to be a leading global technology company with extensive resources and a large customer base. The continuous growth of Azure, combined with Microsoft’s strategic investment in AI orchestration, underpin its ability to deliver long-term value and reliability.

- Marketing Execution: Microsoft positions Azure AI Foundry as a unified and trusted platform for building and deploying AI agents, emphasizing agentic workflows and observability. It effectively communicated its rebranding of Azure AI as Azure AI Foundry. Its Developer Audience campaign in early 2025 was especially effective at promoting the Azure AI Foundry developer tools, achieving 11.7 million impressions and record engagement across Microsoft and Azure channels.

- Customer Experience: Gartner Peer Insights reviews indicate that Azure AI Foundry received lower scores for service and support compared to other Leaders in this research. This could limit its appeal among prospective customers seeking high-touch support.

- Market Responsiveness/Record: Many of Microsoft’s compelling releases hinge on OpenAI’s technology, and these releases usually occur soon after OpenAI releases a similar model, API or capability. Customers that use competing clouds will look to OpenAI directly for new-to-market capabilities.

- Sales Execution/Pricing: Azure AI Foundry’s scores for pricing and flexibility and service and support in Gartner Peer Insights reviews are lower than other key vendors in this evaluation.

OpenAI

OpenAI is a Visionary in this Magic Quadrant. It includes first-party models, reasoning models, image models provided via the Images API, speech models, core language capabilities and APIs. The OpenAI platform is available as ChatGPT SaaS offerings and as a developer API platform (Responses API, Images API, Embeddings, Models) and is also consumed via partner clouds such as the Azure OpenAI service and other partner channels.

OpenAI’s customer base remains strong in North America but is now broadly distributed across Europe and Asia, reflecting global expansion. OpenAI’s fastest-growing verticals are financial services, healthcare and life sciences, and public sector.

In August 2025, OpenAI released GPT-5, which includes built-in reasoning and a greater focus on agentic AI and coding. This release was after our research cutoff date and was not included.

- Marketing Execution: OpenAI expanded the reach of its marketing initiatives in 2025, including significant messaging in Indonesia, India, Brazil, Europe, Japan and Singapore. Its campaigns included a high-profile Super Bowl ad to drive ChatGPT adoption, and its DevDays conference tweet was viewed more than 1.6 million times.

- Marketing Strategy: OpenAI has expanded its cobuilding approach with the OpenAI Pioneers Program. OpenAI has also established mind share among developers by providing early beta access to its offerings and sponsoring developer events and education initiatives.

- Business Model: OpenAI offers a broad portfolio of models and solutions that are bundled in a single platform. Its frontier model pricing is competitive and appeals to customers of all sizes and across industries.

- Overall Viability: OpenAI’s enterprise-grade support structure is leaner than peers, which may pose scaling considerations for some customers. While OpenAI’s growth and revenue channels are notable, the company may face exposure to macroeconomic volatility.

- Customer Experience: OpenAI does not operate a formal customer advisory board. The company experienced two API incidents in June 2025, which were followed by targeted reliability improvements. OpenAI was one of two vendors in this assessment for which customer survey respondents indicated they were looking at alternative platforms.

- Operations: OpenAI has fewer industry compliance certifications compared to other vendors in this assessment, especially for the defense industry

Palantir

Palantir is a Challenger in this Magic Quadrant. It offers the Palantir Artificial Intelligence Platform (AIP), which is bundled with Palantir Foundry as a unified offering. Palantir AIP and Foundry are provided as SaaS and can be hosted in private clouds on hyperscaler partners.

Palantir’s AI application development platform customers are mainly in North America, and it is expanding in the U.S., Korea, Japan and the Middle East. Palantir’s fastest-growing verticals are defense and intelligence, manufacturing, and healthcare. In 2025, Palantir announced AI Forward Deployed Engineer, which will provide fleets of agentic engineers across the life cycle of AI application development.

- Sales Execution/Pricing: Palantir offers flexible pricing options to suit a range of customers, with subscription and enterprise plans that provide various levels of support. The company engages prospective customers through a free developer plan and open-source tools.

- Vertical/Industry Strategy: Palantir maintains a strong presence in defense and intelligence, outpacing its competitors in this industry. The healthcare sector, Palantir’s second fastest-growing vertical, is also notable, as Palantir software supports a large segment of U.S. hospital beds.

- Innovation: Palantir’s Foundry Ontology technology and processes give it an edge on retrieval-augmented generation (RAG) implementations and security within AI application development. The visual aspects of the Palantir AIP development environment are intuitive and ease the cognitive burden for developers.

- Sales Execution/Pricing: Palantir’s partnerships contribute a smaller proportion of revenue compared to the Leaders in this Magic Quadrant, which may indicate future challenges in reaching new customers.

- Marketing Strategy: Palantir operates on a lower marketing budget, with fewer marketing staff compared to many other vendors in this market. Palantir’s lean marketing approach will make it difficult to differentiate its offerings as customer expectations and competition increase.

- Customer Experience: Palantir does not operate a formal customer advisory board. Customer reference survey responses indicated concerns with AIP’s ease of deployment and implementation and the affordability of the platform.

Tencent Cloud

Tencent Cloud is a Challenger in this Magic Quadrant. It offers the Tencent Cloud Agent Development Platform. It offers capabilities for grounding, agentic workflow and multiagent, resource monitoring and management, plug-ins and evaluations. Tencent offers self-hosted versions of its products for on-premises use and a SaaS offering.

Tencent Cloud’s AI application development platform customers are mainly in China, and it plans to expand in the broader Asia/Pacific region, Europe and the Middle East. Tencent Cloud caters to midsize enterprises. Its fastest-growing verticals include retail (e-commerce), healthcare and education. In 2025, Tencent Cloud added memory and context for its AI agents, as well as deployment enhancements for reliability and speed.

- Operations: Tencent Cloud sustained higher operational stability than many vendors, backed by a large number of dedicated support personnel. It also maintains key industry compliance certifications such as SOC, NIST, HIPAA, PCI and ISO.

- Overall Viability: Tencent reported $91.9 billion in revenue in FY24, representing an 8.4% increase over FY23. The company’s scale and resources provide a stable foundation for innovation and customer confidence.

- Marketing Execution: Tencent Cloud concisely communicates the benefits of its platform, including its wide array of MCP plug-ins and tools and its agent capabilities. The company builds credibility and appeals to prospective clients with customer case studies and testimonials, large-scale summits, high-frequency online live broadcasts, and third-party endorsements. Tencent Cloud strategically targets C-level executives, business leaders and software engineering leaders.

- Market Responsiveness/Record: Tencent Cloud’s methods for detecting and responding to changing market conditions are limited, raising concerns about its agility and ability to stay ahead of emerging trends.

- Business Model: Tencent Cloud plans to maintain its current business model over the next 12 months, with a more gradual pace of change compared to leading vendors. Similarly, Tencent’s value proposition does not effectively differentiate the company from competitors, as it misses in communicating impactful statements about technology, process and investment.

- Product or Service: Tencent Cloud has delivered limited features within its platform compared to other vendors in this research, especially in terms of cost management (its AI gateway and model routers are lagging).

Volcano Engine

Volcano Engine is a Challenger in this Magic Quadrant. It offers Volcano Ark, an AI application development platform that includes HiAgent, PromptPilot and veRL. Volcano Ark is a cloud-SaaS managed offering with subscription, enterprise unlimited and pay-as-you-go licensing.

Volcano Engine’s AI application development platform customers are mainly in China. It plans to expand more across the Asia/Pacific region and establish a presence in the Middle East and Europe. Its fastest-growing verticals are technology companies, including device manufacturers and robotics, and retail (e-commerce). In 2025, Volcano Engine introduced Intent-Driven Agent Creation, which translates user intent directly into a testable and potentially deployable service.

- Business Model: Volcano Engine offers standardized product capabilities and flexible pricing options, including usage-based billing for public cloud and options for subscription or perpetual licenses in private deployments. The company primarily relies on a direct sales channel that closes deals within weeks on average. It also prioritizes customer success by ensuring project delivery, launch and retention.

- Innovation: Volcano Engine’s open-source reinforcement learning (RL) framework, veRL, enables the open-source community to fine-tune vertical-specific models. veRL is also integrated into Volcano Ark, which provides customers with advanced RL capabilities through a simple, low-code workflow.

- Geographic Strategy: Volcano Engine plans to deepen its presence in Southeast Asia and expand its geographic focus beyond the Asia/Pacific region. It will enter the Middle East and establish a foundational presence in Europe. Its strategy includes deploying regional cloud infrastructure for low latency and data sovereignty, building local sales and support teams, and localizing models and compliance frameworks.

- Sales Execution/Pricing: Volcano Engine’s partnerships contribute a smaller proportion of revenue relative to what its competitors achieve through robust channel partner strategies, which will hamper its ability to reach new customers.

- Marketing Execution: Volcano Engine’s messaging does not sufficiently emphasize critical topics such as security, time to value and cost optimization. Much of its marketing activity focuses on China, limiting global brand awareness and engagement with customers in other regions.

- Market Understanding: Volcano Engine’s current approach to demand sensing is insufficiently developed, suggesting a need for improved techniques to anticipate and respond to emerging customer needs and market shifts.

Inclusion and Exclusion Criteria

Inclusion Criteria

To qualify for inclusion, providers need to:

- Meet Gartner’s Market Definition of AI application development platforms

- Demonstrate a go-to-market strategy for its AI application development platform aiding in the development of AI assistants, AI agents and multimodal applications with pro-code capabilities

- Sell their AI application development platform with no requirement to purchase or subscribe to any other product or platform

- Target software engineers/software developers as a core user persona

- Enable software engineers/software developers to build AI applications directly and not mandate the use of vendor- or partner-provided professional services

- Implement each of the following use cases:

- Building AI assistants

- Building AI agents

- Building multimodal applications

Providers must also meet one of the following criteria:

- Derive at least $100 million annual revenue in FY24 from their AI application development platform

- Have at least 500 unique paid customer organizations or logos subscribed, not individual users

In addition, providers must operate and support at least 10 paying enterprise customers in three or more of the following geographies:

- North America

- Latin/South America

- Europe

- Middle East

- Africa

- Asia/Pacific

- China

Lastly, the provider must rank among the top 25 organizations in the Customer Interest Indicator (CII) defined by Gartner for this Magic Quadrant. The CII was calculated using a balanced set of measures, including Gartner customer search, inquiry volume or pricing requests; frequency of mentions as a competitor to other vendors in this Magic Quadrant; and scores and frequency of mentions, as measured on Gartner Peer Insights.

Exclusion Criteria

We excluded vendors that:

- Require professional services along with their AI application development platform

- Do not meet the mandatory features described in the Market Definition

- Emphasize no-code within their primary marketing channels, or have a go-to-market strategy focused on low-code application platforms or primarily serving business users.

Honorable Mentions

Airia. Airia’s Enterprise AI Orchestration Platform is designed for building and managing AI agents, assistants and multimodal applications. The platform offers no-code and low-code tools and APIs for developers to streamline the creation and deployment of intelligent workflows. Core capabilities include guardrails, evaluations, observability, cost optimization, and a model catalog supporting both open-source and commercial models. Airia did not meet the inclusion criterion for targeting software engineers/software developers as a core user persona.

Cohere. Cohere’s North is an enterprise AI platform that enables organizations to automate tasks, streamline workflows and access enterprise data efficiently. North provides AI agents that can be customized and integrated with different business tools and data sources. The platform is designed for secure deployment in private or on-premises environments and includes security and admin controls. Cohere did not meet the inclusion criteria for revenue.

CrewAI. CrewAI is an Agent Management Platform (AMP) designed for building, orchestrating and managing AI agents and multiagent workflows. It enables organizations to design “Crews” of autonomous agents and “Flows” of governed automations that work together across data, APIs and business systems. CrewAI offers integrated observability, RBAC, audit logs and cloud/on-prem deployment, to help companies move from experimentation to production. CrewAI did not meet the inclusion criteria for revenue.

Dify. Dify offers commercial and open-source community edition platforms for building and managing AI applications, focusing on LLMOps and agent-based workflows. It provides tools for prompt engineering, dataset management and application deployment through a user-friendly visual interface. Dify supports integration with various LLMs and REST APIs, enabling developers to create and operate AI solutions either in the cloud or on-premises. Dify did not meet the inclusion criteria for revenue.

H2O.ai. H2O.ai’s H2O AI Cloud is a platform that allows users to build, deploy, monitor and share machine learning models and AI applications. H2O AI Cloud provides tools for automated ML, including feature engineering, model validation and tuning. H2O.ai also offers H2O Wave, an open-source framework for developing AI applications. H2O.ai did not meet the inclusion criteria for revenue.

Huawei Cloud. Huawei Cloud’s ModelArts is a suite of tools for building, training and deploying machine learning models and AI-embedded applications. ModelArts features automated ML, data labeling and model management, with support for a wide range of frameworks. ModelArts is designed for both beginners and advanced users, providing a visual interface and scalable infrastructure for AI development. Huawei Cloud did not meet the inclusion criterion for operating and supporting at least 10 paying enterprise customers in three or more geographies.

Live Tech. Live Tech’s DST EAC is an integrated development environment designed to support both data scientists and software engineers in creating and deploying AI workflows. DST EAC features drag-and-drop interfaces for building flows related to classification, summarization and code generation, powered by OpenAI APIs. DST EAC comes with ready-to-use templates for prompt engineering, allowing organizations to set up and customize LLM and agentic solutions. Its flexible deployment model enables AI solutions to be packaged as containers and deployed on-premises or in the cloud. Live Tech did not meet the inclusion criteria for revenue.

WRITER. WRITER’s platform allows enterprises to build, activate and supervise custom AI agents. It provides a collaborative workspace for software engineers and business stakeholders to iterate AI agent development. WRITER’s platform includes purpose-built LLMs, multiagent orchestration, integration with existing business systems and a library of over 100 prebuilt agents. WRITER did not meet the inclusion criteria for revenue.

Evaluation Criteria

Ability to Execute

Product or Service. We specifically looked for critical capabilities applied to the use cases of software engineers developing AI agents, AI assistants and multimodal applications.

Overall Viability. We specifically looked for revenue, profit, customer growth and satisfaction; platform investments; employee and customer geographic distribution; and company size.

Sales Execution/Pricing. We specifically looked for new client logos and current client contract growth; license models and adjustments to them; and customer satisfaction regarding costs and negotiations.

Market ResponsivenessRecord. We specifically looked for release notes and platform updates, the provider’s analysis of market trends, and open-source investments.

Marketing Execution. We specifically looked for significant changes to messaging, campaign success, social media impact and marketing investments.

Customer Experience. We specifically looked for customer success metrics and methods implemented to capture and improve customer experience; customer support; and how customer experience is incentivized within the vendor’s organization.

Operations. We specifically looked for staffing; customer impacting incidents and retrospectives; and platform security and compliance.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | High |

Marketing Execution | Low |

Customer Experience | Medium |

Operations | Medium |

Source: Gartner (November 2025)

Completeness of Vision

Market Understanding. We specifically looked for strategic investments, demand sensing capabilities, competitive analysis and understanding of market disruption.

Marketing Strategy. We specifically looked for updates to marketing strategy, platform messaging and persona targeting.

Sales Strategy. We specifically looked for sales strategy updates, new client/current client growth, customer feedback regarding pricing and negotiations, and license and pricing models.

Offering (Product) Strategy. We specifically looked for product/platform roadmap, near-term product/platform priorities and incorporation of customer feedback.

Business Model. We specifically looked for a value proposition, an understanding of owners/investors/shareholders and planned updates to the business model.

Vertical/Industry Strategy. We specifically looked for regulations addressed, vertical/industry customer success and areas of vertical/industry focus.

Innovation. We specifically looked for patent activity recently delivered, planned innovation, and R&D investment and management.

Geographic Strategy. We specifically looked for region-specific regulation support, completed/planned updates to geographic support strategy and alignment of strategy to growth.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Low |

Sales Strategy | Low |

Offering (Product) Strategy | High |

Business Model | Low |

Vertical/Industry Strategy | Medium |

Innovation | High |

Geographic Strategy | Medium |

Source: Gartner (November 2025)

Quadrant Descriptions

Leaders

Leaders provide mature offerings that meet market demand and have demonstrated the vision necessary to sustain their market position as requirements evolve. The hallmark of Leaders is that they focus on and invest in their offerings to the point where they lead the market and can affect its overall direction. As a result, Leaders can become the vendors to watch as you try to understand how new market offerings might evolve.

Leaders typically possess a large, satisfied customer base (relative to the size of the market) and enjoy high visibility within the market. Their size and financial strength enable them to remain viable in a challenging economy.

Leaders typically respond to a wide market audience by supporting broad market requirements. However, they may fail to meet the specific needs of vertical markets or other more specialized segments.

Challengers

Challengers have a strong Ability to Execute but may not have a plan that will maintain a strong value proposition for new customers. Larger vendors in mature markets may be positioned as Challengers because they choose to minimize risk or avoid disrupting their customers or their own activities.

Although Challengers typically are of significant size and have significant financial resources, they may lack strong vision, innovation or an overall understanding of market needs.

Challengers can become Leaders if their vision develops. Over time, large companies may fluctuate between the Challengers and Leaders quadrants as their product cycles and market needs shift.

Visionaries

Visionaries align with Gartner’s view of how a market will evolve, but their ability to deliver against that vision is less proven.

For vendors and customers, Visionaries fall into the higher-risk-higher-reward category. They often introduce new technology, services or business models, and they may need to build financial strength, service and support, and sales and distribution channels.

Whether Visionaries become Challengers or Leaders may depend on if customers accept the new technology or the vendors can develop partnerships that complement their strengths. Visionaries are sometimes attractive acquisition targets for Leaders or Challengers.

Niche Players

Niche Players do well in a segment of a market, or they have a limited ability to innovate or outperform other vendors in the wider market. This may be because they focus on a particular functionality or geographic region, or because they are new entrants to the market.

For end users, assessing Niche Players is more challenging than assessing vendors in other quadrants. Some could make progress, while others do not execute well and may not have the vision and means to keep pace with broader market demands.

A Niche Player may be a perfect fit for your requirements. However, if it goes against the direction of the market — even if you like what it offers — then it may be a risky choice because its long-term viability will be threatened.

Context

As enterprises accelerate their adoption of AI-driven digital transformation, software engineering teams are increasingly moving from fragmented, single-purpose technologies to AI application development platforms. These platforms empower software engineering teams to design, build, test, deploy and govern AI-embedded applications — such as assistants, agents and multimodal solutions — at scale, without requiring deep machine learning expertise.

AI application development platforms help to reduce cognitive load and tooling overhead for developers. Furthermore, these platforms support standardized governance and faster time-to-value for AI initiatives through reuse in approaches, skills and artifacts. While the core function of these platforms is to streamline the creation of AI-embedded applications, vendors are increasingly distinguishing themselves by supporting complex agentic workflows and multimodal capabilities. Over the past year, leading vendors have expanded their offerings to include MCP server building and hosting, model routing, AI gateways, and observability tools for monitoring and compliance.

Software engineering leaders should prioritize platforms that deliver governance and cost optimization across the entire life cycle of AI applications and enable effective collaboration between software engineering, data science and business teams. To maximize ROI and minimize risk, select platforms that provide strong guardrails, grounding and observability features, ensuring that AI applications are accurate, secure and compliant.

As the market continues to evolve, regularly reassess platform choices to ensure alignment with changing business needs, regulatory requirements and emerging AI capabilities.

Market Overview

The AI application development platform market is growing rapidly, as software engineering leaders across industries seek to embed advanced AI capabilities into their organization’s products and operations. Indeed, building AI capabilities into apps/establishing AI engineering is a top priority (41%) identified in the Gartner Software Engineering Survey for 2025. Gartner estimates the size of the AI application development platform market to be above $5.2 billion in 2025, with a staggering annual growth rate of more than 30%.

AI application development platforms provide teams with a wide array of capabilities that streamline the process of building, testing, deploying and governing AI assistants, AI agents and multimodal applications. Buyers are increasingly seeking solutions that offer broad model catalogs, grounding capabilities, guardrails and observability, which help ensure the accuracy, safety and compliance of AI applications. While enterprises are looking for more vertical accelerators, such as prebuilt AI application templates for domains or models trained for particular industries, this is an area where the market has not yet matured.

Nonetheless, these platforms enable development teams to automate workflows at scale, connect previously siloed data and collaborate with data science teams, all of which is driving strong demand.

In 2025, several trends impacted the direction of the market, including:

- The introduction of Model Context Protocol and Agent2Agent Protocol standards. These protocols provide standardization that enable agents to communicate across different platforms and connect to external data sources.

- Increased focus on managing the AI agent life cycle. Platforms are providing more robust frameworks for continuous evaluation of agent performance, stricter guardrails and deep observability into their reasoning processes, including advances in short- and long-term memory technology for AI agents.

- New regulations such as the EU AI Act and California’s SB 53. National governments and regulatory bodies are enacting strict data residency and processing mandates.

- The rise of agent experience (AX). Front-end development markets and strategies will be reshaped. Traditional human-centric UI demand will shrink as stripped-down, agent-optimized graphical interfaces take precedence. UX and front-end service providers must pivot toward building hybrid and agent-centered interaction models.

- Enhanced fine-tuning and grounding techniques beyond retrieval-augmented generation. According to the 2025 Gartner AI in Software Engineering Survey, fine-tuning is the most commonly used approach for grounding or customizing generative AI models, selected by 80% of respondents, compared to RAG at 45%.

- The rise of open-weights and open-source offerings. Providers such as Alibaba Cloud, Meta and OpenAI are releasing open-weights models, while developers are building prototypes with popular open-source, pro-code AI agent frameworks including AG2, LangGraph and CrewAI. However, these efforts are impeded by significant challenges related to achieving the requisite security and scalability necessary for successful enterprise deployment. In the 2025 Gartner AI in Software Engineering Survey, a significant number of respondents indicated using AI application development platforms (73%) over pro-code AI agent frameworks (25%).

- The heightened need for application security. Software engineering teams need robust controls for input/output filtering, prompt injection defense and data governance to ensure the safety and quality of AI applications.

Vendors are differentiating themselves in terms of multimodal support, compliance certifications, first-party model development, inference capabilities and flexibility in licensing. As software engineering leaders evaluate AI application development platforms, they should seek vendors that excel in these areas of differentiation and effectively support their geographic coverage, development personas and enterprise infrastructure.

In the near term, we expect vendors will continue investing in features that reduce operational complexity, enhance security and promote responsible AI deployment. By 2027, end users should expect to see more innovation for models and AI applications at the edge and application development opportunities across more devices and robotics.

Gartner Software Engineering Survey for 2025. The survey was conducted to provide a comprehensive understanding of the current landscape in software engineering. It aims to identify the demand for various roles, essential skills and upskilling strategies within the software engineering organization. It explores the integration of AI in software engineering workflows, their leadership experiences and prior roles of the current leaders. It also assesses their budget expectations, team structures, organizational outcomes and priorities. The survey was conducted online from October through December 2024 among 400 respondents from the U.S. (n = 320) and U.K. (n = 80). Qualifying organizations operated in multiple industries (excluding the IT software industry involved in the development of commercial software and the education sector) and reported enterprisewide revenue for fiscal year 2023 of at least $250 million or equivalent. Qualified participants were highly involved in managing software engineering/application development teams and the activities they perform. Disclaimer: The results of this survey do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.

2025 Gartner AI in Software Engineering Survey. This study was conducted to explore the adoption of AI within software engineering functions, focusing on two key areas: the use of AI tools (e.g., AI code assistants, AI code agents) throughout the software engineering life cycle (SDLC); and the development of AI-powered solutions (or AI engineering) within software engineering functions, along with their contribution to business outcomes. The research was conducted online from 29 April through 25 June 2025 among 299 respondents from North America (n = 150), EMEA (n = 104) and Asia/Pacific (n = 45). Quotas were established for company sizes and for industries to ensure a good representation across the sample. Organizations were required to be either piloting or using AI tools in SDLC for less than four years, and either piloting or having built AI solutions in their software engineering functions. Respondents included both leaders and individual contributors from software engineering functions, each with at least one year of tenure at their current organization. All respondents were involved in decision making or directly engaged in using AI tools or building AI solutions within their software engineering functions. Disclaimer: The results of this survey do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.