Market Guide for Retail Media Networks

4 August 2025 - ID G00814194 - 20 min read

By Greg Carlucci

Retail media networks provide a significant opportunity for both advertisers and retailers to leverage shopper purchasing and digital behaviors to drive increased sales. CMOs can use this research to understand the retail media market dynamics and key trends shaping the future of commerce media.

Overview

Key Findings

- New data privacy constraints that limit cross-site tracking and ad targeting are driving CMOs and their teams to seek alternative methods of online targeting and measurement. Logged-in, informed and consented retail shopper data presents a significant resource for both targeting and measurement, especially when combined with retail sales for closed-loop measurement.

- CMOs and their teams are slowed by the increasingly fragmented and labor-intensive nature of performance advertising across multiple retail media networks. Furthermore, advertising inventory on RMNs is often more expensive, which means advertisers must weigh the benefits of reaching highly valuable audiences at a higher cost against reaching larger, less precisely targeted audiences at a lower cost per impression.

- Retail media’s proximity to sales and complicated legacy relationships with brick-and-mortar retail partners attracts more C-suite members’ attention compared to other media channels. Due to this, RMNs require a significant investment of finite data and analytics resources to prove their value.

Recommendations

To ensure a successful advertising program across RMNs, CMOs must:

- Quantify the potential costs and revenue of each RMN on offer by deploying zero-budgeting analysis of current retail partners, identifying priority partners and media costs.

- Prioritize retailers with developed data offerings by evaluating their media and data capabilities as a whole, including investment measurement capabilities that include media costs and conversion.

- Carefully structure and develop your teams’ skills in strategic performance marketing specific to RMN advertising; if necessary, use agency partners for additional bandwidth.

- Implement a data-driven advertising strategy that utilizes clean room technologies to securely activate first-party data across off-site channels such as Google, Meta and OTT platforms. This approach enables precise audience targeting while expanding your retail media network footprint beyond owned properties.

Market Definition

Gartner defines retail media networks as packaged retail website search, display, app, in-store assets and other digital advertising opportunities (e.g., ad impressions) that are sold to brands and advertisers. Retailers leverage media networks to execute their unified retail commerce strategy and to develop new lines of revenue, while advertisers aim to increase their exposure to and influence the behavior of retail shoppers at or near the final point of purchase.

RMNs offer retailers supplemental revenue from their owned digital and physical assets and datasets. RMNs let companies buy branding and conversion-oriented ads at or near the final point of purchase — which stands out as its unique selling proposition.

Retailers build RMNs to aggregate audiences of shoppers across commerce websites, apps, and digital assets in physical stores into media opportunities for advertisers. These media opportunities, including search listing ads, product ads (display and video) and audio, are purchased by advertisers through direct insertion orders or digital buying methods like programmatic real-time auctions. Marketing and technology leaders at retailers develop these advertising exchange capabilities internally or partner with ad technology platforms, such as with demand- and supply-side partners, to offer their media for sale in a scalable and cost-efficient way. In addition to their value as media opportunities, retailers can assemble these audiences into valuable data segments by historical browsing and purchase behavior, which can be used to improve both on-site personalization and targeting.

The common use-case scenarios or business problems addressed by retail media networks include:

- An urgent need to create advertising solutions that don’t rely on third-party data, including cookies. RMNs enable retailers and brand advertisers to leverage first-party data to target and measure mutually beneficial advertising opportunities to consumers, brands and retailers without the use of cookies.

- The monetization of retailers’ audience and first-party consumer behavior and purchase data. Retailers own vast amounts of first-party data they collect directly from customer interactions and purchases across digital and physical assets. The data can be used to create personalized experiences and provide targeted advertising opportunities on both owned assets and, with the proper privacy-enhancing technology, third-party media.

Must-Have Capabilities

The must-have capabilities for retail media networks include:

- The creation of advertising opportunities (e.g., ad impressions) on a retailer’s owned digital and/or physical properties.

- The sale of advertising opportunities to brands and advertisers across digital and/or physical properties.

- Manual measurement and reporting capabilities for analysis of campaign results.

Standard Capabilities

Standard capabilities for retail media networks include:

- Integration with digital and/or unified retail commerce and other key platforms (e.g., merchandising inventory management, CDP, CRM and ERP).

- Traditional ad sales methods like shopper marketing partnerships and insertion orders.

- Self- or managed-service digital ad platforms to enable the buying of ads and campaigns.

- Automated dashboards for reporting on campaign results that update within a set time frame.

Optional Capabilities

Optional capabilities for retail media networks may include:

- Real or near-real time ad buying and campaign serving via programmatic technology.

- Precise optimization and buying levers, such as targeting by return on ad spend, profitability and inventory stock levels.

- Data collaboration capabilities to integrate with ad and marketing technology companies for the packaging of aggregate and first-party audience data for both on- and off-site targeting.

- Live dashboards for real-time reporting and analysis.

Market Description

The retail media network market is centered around significant growth, technological advancements, evolving roles for various players and a push toward integrated consumer experiences.

Explosive Growth and Diversification of Retail Media Networks

Retail media advertising spend is projected to reach $130 billion by 2028, an increase of $68 billion in 2025.1 The market’s explosive growth in media spend is driven by existing media network expansion of off-site advertising as well as new entrants leveraging their rich customer data and purchase history to position themselves as media suppliers, which significantly increases the available ad inventory.

New media networks are emerging from industries beyond traditional retail, including:

- Financial institutions, such as Chase Media Solutions, PayPal Ads

- Travel and hospitality organizations, such as MARRIOT MEDIA, United Airlines (Kinective Media)

- Delivery services, such as Uber Eats, DoorDash, Gopuff

- Quick service stations, such as 7-Eleven, Wawa, Casey’s

Pioneers like Amazon continue to expand their pool of owned-and-operated inventory on platforms such as Prime Video, Twitch, Amazon Music and IMDb, reaching 130 million U.S. households.2 In addition, Amazon has partnered with Roku to create the largest connected TV (CTV) network, which reaches an estimated 80 million U.S. CTV households.3 Amazon has also created new partnerships with streaming providers like The Walt Disney Company to enable them to reach customers on their platforms that include Hulu, ESPN and Disney+.4

Advancements in Data, Technology and Measurement

New data privacy constraints (which allow users to limit tracking) and the phasing out of third-party cookies are driving CMOs and their teams to seek alternative online targeting and measurement methods. First-party data — specifically logged-in, informed and consented retail shopper data — represents a significant opportunity for both targeting and closed-loop measurement, directly linking ad spend to retail sales.

Retail media networks are increasingly providing self-service models and AI-powered optimizations for advertisers. This helps advertisers manage media investments with in-house teams and allows them to leverage ad-tech partners for measurement, providing more direct control over KPIs like return-on-ad-spend (ROAS), total revenue and profit. RMNs are maturing to provide detailed reporting, ranging from end-of-campaign summaries to near-real-time dashboards, supporting transparency and ROI analysis.

Privacy-enhanced data integrations (such as data clean rooms) are vital for enabling sophisticated on- and off-site targeting. Mature RMNs are forming external data partnerships to enable targeting on social media and streaming TV, which is increasingly valuable as privacy laws tighten.

Evolving Roles and Standardization Efforts

Retailers are gaining confidence in their new identity as media suppliers — a significant shift that requires developing internal capabilities, including marketing technology and strategic expertise.

Ongoing standardization efforts by industry bodies like the Interactive Advertising Bureau (IAB) are aiming to simplify the buying and measurement of ad inventory on RMNs.5 Standard ad units like display, sponsored search and sponsored product ads are becoming more broadly available via demand-side platforms (DSPs) as retailers partner with supply-side partners (SSPs) and ad networks.

Marketing agencies are expanding into retail media, leveraging technology to provide competitive optimization and measurement services as advertisers expand beyond traditional consumer goods companies.

Rise of Omnichannel Experiences

Shoppers flock to channels most convenient to them, often combining digital and physical experiences (such as using a mobile phone while in-store). This necessitates an integrated approach to advertising across online, mobile and in-store touchpoints. For more on omnichannel experiences, see How to Bridge Digital and Physical Customer Experiences.

Advancements in physical in-store and shopper marketing capabilities as well as new digital signage opportunities are expanding media opportunities for advertisers.

Market Direction

In 2025, 30.6% of the total marketing budget across all industries went to paid media — an 11% increase on gross media spend as a proportion of company revenue year over year.6 Media networks have significantly proliferated in the last several years, forcing CMOs to manage a more fragmented media buying process that requires outside help, like agencies or ad-tech measurement solutions.

As paid media spend and retail media network spend increases, retailers are incorporating RMN investments into their broader business and cooperative marketing agreements. Retailers are learning how to build advertiser relationships, marketing technology to manage privacy and audience-building capabilities.

In addition to paid media and retail media spend increases, consumer goods companies are trying to allocate and balance retail media ad spending against traditional, trade promotion spend. As these can directly conflict, consumer goods companies must carefully examine RMNs where retailers can collaborate to maximize profit from trade spend on products versus where profit on ad spend can be maximized through retail media advertising.

Given these forces shaping the market, established RMNs are continually adapting their strategies. In addition to determining their team’s capabilities and prioritizing retailers for RMN ad investment, CMOs must consider following market shifts that will impact both RMNs and the broader digital advertising ecosystem.

Intensified Competition and Pressure on Value Proposition

Established RMNs are experiencing increased competition entering the market. The surge in available ad inventory means established networks are no longer the sole providers of highly valuable first-party data with direct access to purchasing audiences.

In response to additional retail media network launches, “walled garden partnerships” between retailers and major ad platforms (like Google and Meta) are blurring the value proposition of individual RMNs, as advertiser targeting capabilities become more homogenized across different platforms:

- Google continues to expand partnerships with retailers like Costco and other media networks to enable advertisers to identify retail buyers using Google’s Display & Video 360 (DV360) DSPs.7

- Meta expanded its API connection to retail media networks, allowing advertisers to target audiences from retail networks like Best Buy on their platform.8

Imperative for Advanced Data and Measurement Capabilities

Established RMNs are prioritizing and enhancing their first-party data offerings, ensuring ethical collection and use with explicit consent, especially as third-party cookies are phased out.

Despite advancements in reporting, many retailers lack a full self-service reporting model with closed-loop measurement. There is a critical need for investment in robust closed-loop measurement capabilities. This investment enables advertisers to directly tie RMN ad spend to on- and off-site sales outcomes, providing detailed, near-real-time reporting.

Established RMNs are accelerating the development of their technology stacks and media capabilities to facilitate effective ad buying and data leverage (including privacy-enhanced integrations like data clean rooms) to enable sophisticated on- and off-site targeting. This helps address the ongoing challenge of measurability, particularly for off-site media. Clean rooms (which are typically reserved for advertisers with large media budgets and addressable audiences) allow brands to identify customers purchasing their products at retailers more seamlessly across walled gardens.

Adaptations of service models and internal capabilities retailers are fully embracing their new role as media suppliers and developing the necessary internal marketing technology and strategic expertise to operate effectively in this capacity.

These retailers are strategically offering a mix of campaign management routes, including advanced self-service models with AI-powered optimizations, retailer-managed services for brands requiring strict control and seamless integration for performance/specialist agencies. This approach is catering to diverse advertiser needs, from those with in-house teams to those that rely on agency partners.

Strategic Investment in Omnichannel Experiences and New Monetization Opportunities

To capture a larger share of brand dollars, established RMNs are innovating beyond performance features. They are introducing new branding and partnership opportunities that appeal to brands seeking to reach audiences moving away from traditional advertising channels like linear TV or print and into connected TV and over-the-top (OTT) advertising.

Embracing Standardization and Interoperability

To simplify the buying process for advertisers and attract more spend, retailers are actively participating in and adopting industry standardization efforts (such as IAB guidelines) for ad units and measurement.

Retail media advertising inventory has become more broadly available via DSPs, and they are fostering partnerships with SSPs and ad networks. This is making retail media easier to buy and measure across existing advertiser tools.

Market Analysis

Retail Media Advertising Expands Beyond the Consumer Goods Industry

Retail media advertising was historically most beneficial for consumer goods organizations, but their appeal has expanded to more nonendemic industries as rich customer data and precise targeting lure more advertisers onto these networks. For example, customers purchasing diapers at retailers could be targeted with ads from financial institutions offering education savings plans or healthcare organizations that offer services to find pediatricians.

CMOs should prioritize retail media networks based on cost, reporting and performance as emerging retail media networks are beginning to make their audiences available in ad exchanges that no longer require ad hoc campaign building (see Figure 1). Leverage this market guide and other resources, like Gartner’s digital commerce research, to demonstrate ways RMNs can prove marketing’s value (see How CMOs Can Prove Marketing’s Value Using Digital Commerce).

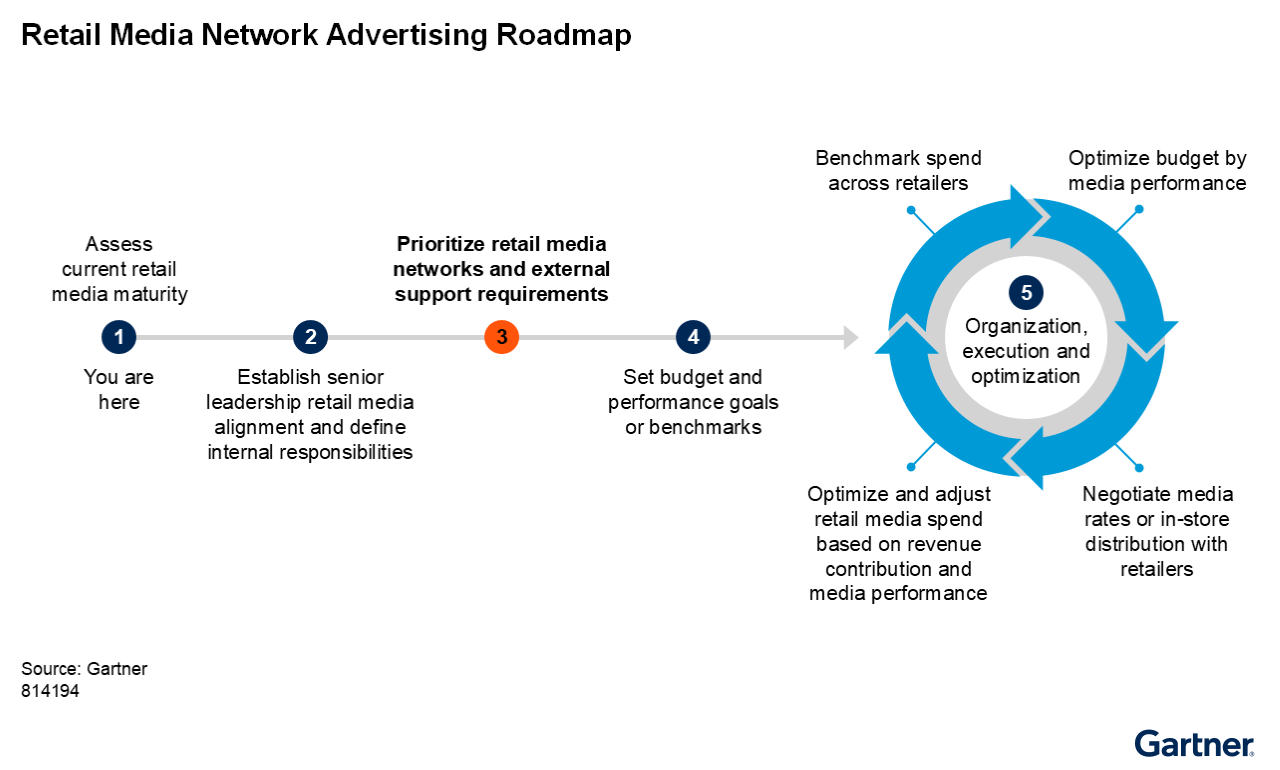

Many of the same skills and technologies utilized to manage search and display advertising are also involved in managing retail media. Brand CMOs starting from scratch on RMNs can jump-start their teams’ maturity by leveraging their experience in advertising, commerce and media technologies that enable media buying, measurement, optimization and audience segmentation (see Maturity Model for Retail Media Network Advertising).

Not all RMNs are the same, however, and proficiency with one retailer does not necessarily indicate success across others. On the retailer capability side, key differentiators include data portability, measurement options, media buying across different channels and campaign optimization capabilities (like connecting ad spend to new incremental customers or habitual buyers, networkwide frequency controls and ad suppression for shoppers that previously converted).

Reach Customers Across Multiple Channels

The essential difference between RMN advertising and other media channels is the ability to buy products featured in ads natively on the brand website, in the app or within a physical store. The targeting is also based on purchase-level data, not just digital behaviors like website browsing history. In comparison, think about what it’s like to view an ad on other media channels. Display advertising, for example, can include content and products that were previously viewed by the shopper (such as remarketing and retargeting). When the viewer clicks on the ad, it will take them back to where they originally viewed the content or product and away from the website they were browsing.

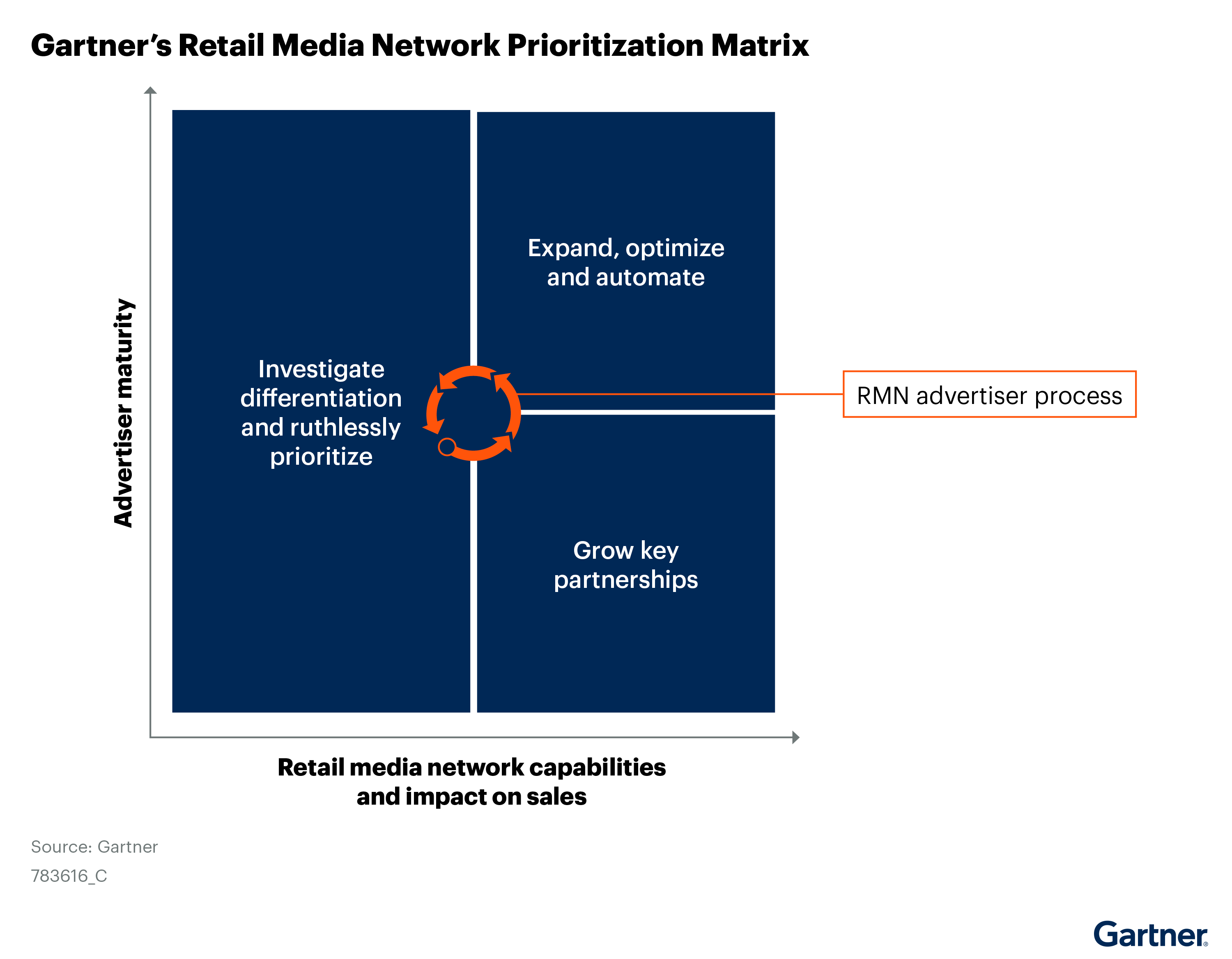

The marketing team’s maturity and a retailer’s capabilities lend themselves to a grid that can help CMOs prioritize RMNs for investment of both budget and time (see Figure 2). Regardless of team maturity (shown on the y-axis), RMNs with less reach and fewer capabilities (the x-axis) should be ruthlessly prioritized and only invested in if they offer distinct audiences or novel technologies that improve campaign profitability.

Like other forms of performance advertising, RMNs have an inverse relationship between team maturity and the level of bandwidth necessary to achieve success. Once key retail partners and digital channels are identified, CMOs should focus on building their team’s capacity to maximize the potential brand impact and revenue with those partners. Once RMN advertising teams have sufficiently mastered the campaign levers of key retail media partnerships, CMOs should focus on expanding existing relationships, developing new measurement opportunities for further optimization and leveraging automation to free bandwidth. That extra bandwidth can then be reinvested to identify new, differentiated partners and tools to drive additional growth.

Leverage Owned Data for Better Targeting

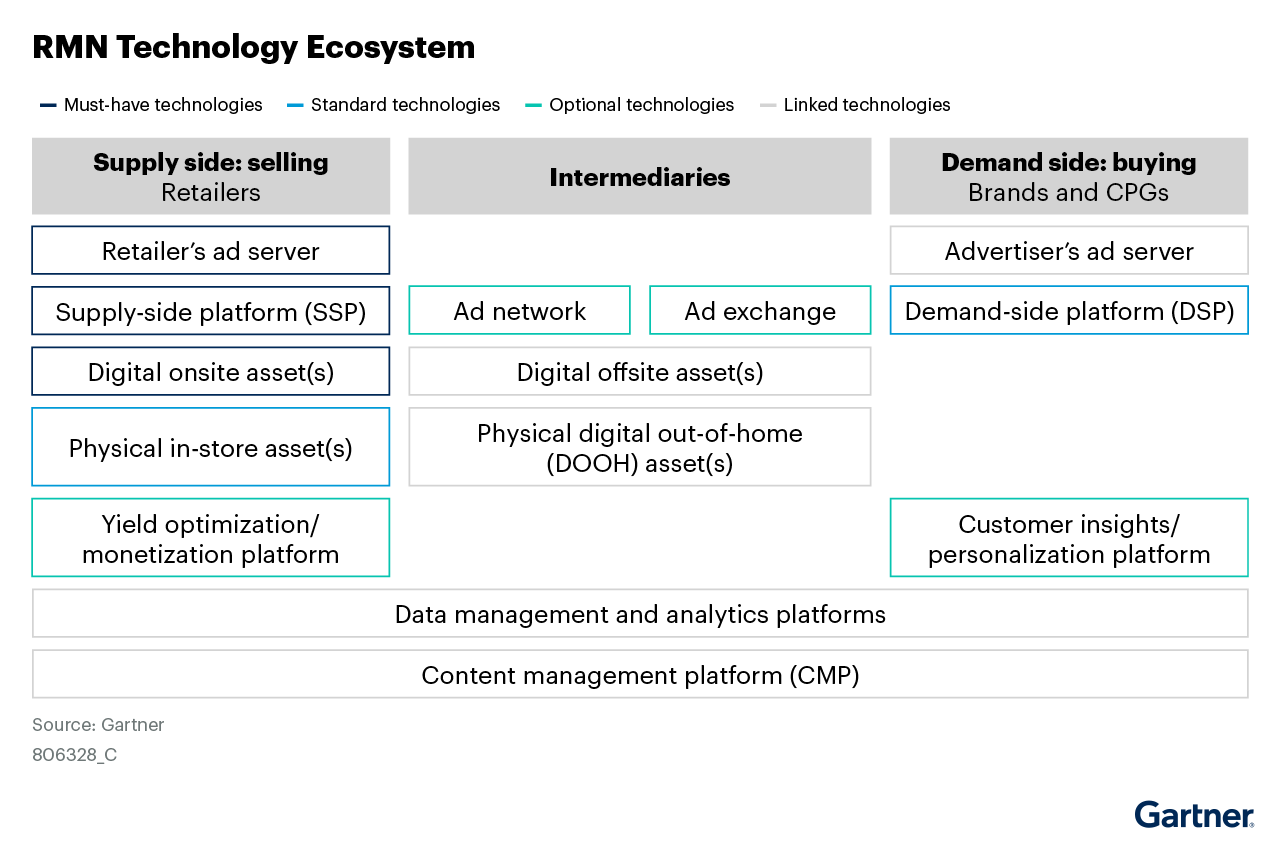

Owned customer data from your brand website, email lists or loyalty programs can be leveraged to improve advertising targeting. Such improvements include creating look-alike audiences of your existing customer base, including or removing existing customers from campaigns and improving the ability to track performance. Clean room technologies allow brands and retailers to match user IDs by leveraging hashed Personally identifiable information (PII) like email, names, phone numbers and device IDs (see Figure 3).

Data capabilities are a key differentiator for many retailers, from the facilitation of measurement to the enablement of retail shopper and sales data for both on- and off-site targeting. Ideally, CMOs should determine their team’s or their agency service provider’s level of data maturity and match it to that of their retail partners. Capabilities like data clean rooms with live data dashboards may be out of reach for some teams and retailers now, but they can be included in a tech roadmap to determine their completeness of vision within the space.

The logged-in and consented data from shoppers browsing and buying on their digital and in-store properties can be leveraged in ways that add value to existing media targeting and measurement capabilities. Sourcing and utilizing consumer data for marketing is becoming increasingly difficult as major web browsers phase out third-party tracking cookies and privacy regulations tighten restrictions on first-party data collection.

Retail shopper data (with opted-in consent) can be leveraged with data-collaboration technologies to fill some of the targeting and measurement gaps (see Optimize Paid Media Spend by Mastering Ad Targeting). CMOs can leverage this retail data via privacy-enhanced resolution capabilities (like data clean rooms) to target shoppers on external media such as connected TV and social media.

A dog food brand selling at a grocery chain wants to use the grocer’s shopper data to target their ads toward dog food shoppers who haven’t purchased recently. With the help of an SSP and/or customer data platform, the grocer can load segments of shoppers, which then appear as targetable segments on a DSP. The dog food brand selects the segment, pays a premium to target those shoppers across the DSP (typically a flat cost-per-mile [CPM] or percentage of media) and prioritizes streaming TV. Dog food shoppers who haven’t purchased in the last week watch a free, ad-supported TV app on their connected TV and are served an ad for the dog food brand.

If those shoppers return to the store and make a purchase, the grocer can then provide that data back to the DSP, providing a closed-loop report to the dog food brand to calculate the cost of that customer acquisition.

As the market matures and the industry standardizes ad formats and measurement capabilities, expect retail media to be easier to both buy and measure across existing advertiser tools like DSPs. Advancements in physical in-store and shopper marketing capabilities (like foot-traffic identification, immersive experiences and new digital signage opportunities) will also increase the media opportunities for advertisers.

Lastly, expect retailers to introduce new branding and partnership opportunities that expand upon the performance features present in retail media today as they compete for brand spend. Brands with robust media and advertising programs may be able to leverage these opportunities to reach new or returning audiences that increasingly buy their way out of traditional advertising channels like linear TV, print or digital via ad blockers.

Representative Vendors

The vendors listed in this Market Guide do not imply an exhaustive list. This section is intended to provide more understanding of the market and its offerings.

The vendors listed in this Market Guide do not imply an exhaustive list. This section is intended to provide more understanding of the market and its offerings.

These retailers were selected to provide a reference list featuring a breadth of retail media networks based on digital commerce maturity, campaign management models, geography and industry focus (see Table 1). While there was no minimum threshold of monthly web visitors for their primary commerce and RMN websites (like retailer.com), priority was given to retailers with at least 5 million visitors per month.

Vendor Selection

Representative Media Network Vendors

Retailer | Solution Name | HQ |

7-Eleven | Gulp Media Network | U.S. |

Albertsons Companies | Albertsons Media Collective | U.S. |

Amazon | Amazon Ads | U.S. |

ASOS | ASOS Media Group | U.K. |

Belk | Belk Media Network | U.S. |

Best Buy | Best Buy Ads | U.S. |

Boots | Boots Media Group | U.K. |

Carrefour Group | Carrefour Links Unlimitail | France |

Casey’s | Casey’s Access | U.S. |

Cdiscount | Cdiscount Advertising | U.K. |

Chase | Chase Media Solutions | U.S. |

CVS | CVS Media Exchange | U.S. |

DoorDash | DoorDash Ads | U.S. |

eBay | eBay Ads | U.S. |

E.Leclerc | ConsoRegie | France |

Expedia Group | Expedia Group Media Solutions | U.S. |

Instacart | Instacart Ads | U.S. |

Intermarché * | Infinity Advertising | France |

Klarna | Klarna For Business | U.S. |

Kroger | Kroger Precision Marketing (KPM) | U.S. |

Loblaw | Advance | Canada |

Lowe’s Media Network | Lowe’s Media Network | U.S. |

Macy’s | Macy’s Media Network | U.S. |

MARRIOTT MEDIA | MARRIOTT MEDIA | U.S. |

Nordstrom Media Network | Nordstrom Media Network (NMN) | U.S. |

Target | Roundel | U.S. |

Tesco | Tesco Media | U.K. |

The Home Depot | Orange Apron Media | U.S. |

PayPal | PayPal Ads | U.S. |

Uber | Uber Advertising | U.S. |

Ulta Beauty | UB Media | U.S. |

United Airlines | Kinective Media | U.S. |

Walgreens | Walgreens Advertising Group | U.S. |

Walmart | Walmart Connect | U.S. |

Wayfair | Wayfair Advertising | U.S. |

Wawa | Goose Media Network | U.S. |

*Infinity Advertising is a joint venture between Intermarché and the Casino Group. | ||

Source: Gartner

Market Recommendations

To develop their RMN strategy to drive commercial growth, CMOs must:

- Prioritize retailers that offer features like prospecting new customers, networkwide frequency control and ad suppression when audiences convert. Keep an eye on the shopping experience and take note of details like ad visibility, competitive separation and contextual relevance as well as retailer investment in new technologies like supply-side platforms.

- Evaluate their marketing team’s maturity, bandwidth and technology to manage RMN advertising and determine which campaign management choices will help reach their goals.

- Focus on retail media partners, data strategies and tools (like data clean rooms) to optimize targeting precision and reach by combining first-party data with on- and off-site media opportunities.

1 Retail Media Ad Spending Forecast H1 2024, EMARKETER.

4 Amazon Ads and Disney Advertising Announce Strategic Integration to Increase Ad Relevancy and Deliver Commerce Insights for Advertisers, Amazon Ads.

5 Final IAB/MRC Retail Media Measurement Guidelines Available for Download, Interactive Advertising Bureau (IAB).

This survey explored top-line marketing budgets with the goal of understanding how changing customer journeys, pressures from the C-suite and cost challenges affect marketing’s spending priorities and channel effectiveness. Conducted online from January through March 2025, the research included 402 respondents from North America (n = 202), the United Kingdom (n = 97) and Europe (n = 103; including France, Germany, Belgium, Denmark, Finland, Netherlands, Norway and Sweden). Participants were required to be involved in decisions related to setting or influencing marketing strategies/planning, aligning marketing budgets/resources, or leading cross-functional programs and strategies with marketing. Seventy-seven percent of the respondents represented organizations with annual revenue of $1 billion or more. The respondents came from a diverse range of industries: manufacturing (n = 52), financial services (n = 50), insurance (n = 43), consumer products (n = 43), healthcare (n = 42), travel and hospitality (n = 37), IT and business services (n = 36), retail (n = 36), pharma (n = 32), and media (n = 31). Disclaimer: Results of this survey do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.

Note 1: Gartner’s Initial Market Coverage

This research provides Gartner’s initial coverage of the market and focuses on the market definition, rationale for the market and market dynamics.