Magic Quadrant for Data and Analytics Governance Platforms

6 January 2026 - ID G00828171 - 59 min read

By Anurag Raj, Guido De Simoni, and 1 more

A data and analytics governance platform helps organizations design and enforce governance policies for data and its derived assets across its life cycle. D&A leaders should explore and adopt these capabilities to meet end users’ demand for streamlined, scaled, and automated governance decision making.

Strategic Planning Assumptions

By 2027, 60% of data governance teams will prioritize governance of unstructured data to deliver GenAI use cases and improve decision quality in organizations.

Through 2028, 80% of S&P 1200 organizations will relaunch a modern, D&A governance program, based around a trust model.

Market Definition/Description

A data and analytics governance platform is a set of integrated business and technology capabilities that help business leaders and users develop and manage a diverse set of governance policies and enforce those policies across business and data management systems. These platforms are unique from data management in that data management focuses on policy execution, whereas D&A platforms are used primarily by business roles — not only or even specifically IT roles — for policy management.

Data and analytics (D&A) leaders who are investing in operationalizing and automating the work of D&A governance should evaluate this market. The work of D&A governance primarily includes policy setting and policy enforcement, and collaborates with data management (policy execution). Use cases are employed across numerous governance policy categories and multiple business scenarios and asset types (data, KPIs, analytics models). The intersection of use-case/business scenarios, policy categories and assets to be governed is then used to identify the technology capability. These capabilities may share similar names across policy categories, but may not mean the same thing, or may be used differently by various governance personas. For example, data classification in a data security implementation would be quite different from a data classification effort for creating trust models, which would be based on lineage and curation.

Mandatory Features

The must-have features for this market include:

- Policy-setting solution: Operationalize, serve, and automate the work of data and analytics governance stakeholders involved in setting policies (governance board, data owners) using:

- Information policy representation (high level): Model, store and access (for state and/or persistence) a business representation of the governance policies being enforced, with integration and links to business rules enumerated in the various applications.

- Organization and role models: Set up organizational models and associated user IDs with key roles across the various workflows and the intersection of work related to policy setting and policy enforcement. An example is setting up models that tag real people to data elements, tasks, workflows, rules and more.

- Workflow management: Support and automate governance workflows with capabilities including business process modeling, data flow modeling and documentation, and support for analytics key performance indicators (KPIs) and other benchmarking efforts to monitor business impact of D&A governance.

- Policy enforcement solution: Operationalize, serve and automate the work of data and analytics governance stakeholders involved in enforcing policies (business data stewards, analytics stewards) using:

- Business glossary: Develop and use a glossary in support of policy analysis and development. It includes the ability to support taxonomies and ontologies to address semantic variations. This expands from business glossaries to identifying relationships between data elements, synonyms and (preferably) support ontologies and semantic relationships (business metadata), and is part of broader data cataloging capability.

- Data lineage and impact analysis: Identify data provenance using the depth and breadth of data lineage. Data lineage must be broad because it must audit and, wherever needed, infer all the steps, applications and transformations that any data element has gone through from its original source to all the possible endpoints, including AI models. The capability is also leveraged to identify the impact of a change on any metadata element. It must be deep to allow for drilling down or analyzing to the finest level of detail, such as column-level or transformation logic.

- Orchestration/automation: Align data governance with modern data management practices and technologies. Leveraging AI/ML, active metadata, GenAI, AI agents, these capabilities automate and optimize key functions like data quality, integration, cataloging and insight generation, ensuring that data is accurate and relevant. In data governance, “augmented” means using active metadata and AI and machine learning (ML) to enhance decision making and enforce policies effectively. These capabilities also support data democratization, enabling nontechnical users to participate in data processes while maintaining governance standards.

- User interface (UI) for stewardship: Support the skills and needs of a variety of stakeholders involved in policy enforcement, including business data stewards and analytics stewards, and provide them with collaborative workflows. Address a variety of users with an interface that is easy to use and engaging to interact with. The UI should enhance the experience that users have while interacting with the solution/product and ensure that different personas find the appropriate virtual environment in which to work. It should also create a collaborative experience.

- Task management: Set up, assign and reassign tasks across the organizational roles involved in policy setting, enforcement (including exception management) and external roles/users. Management tools such as dashboards and work-to lists are provided to monitor the status of tasks.

- Rule management (low level): This capability automates the enforcement of business rules that are tied to data elements and associated metadata. It supports dedicated interfaces for the creation of, and the order of execution and links with, information stewardship for effective governance.

- Connectivity/integration: Provide facilities for loading (import) and exporting metadata, including roles, in a fast, efficient and accurate manner in conjunction with other third-party tools. These facilities provide a communication backbone for the bidirectional flow of metadata between the central repository and the data sources or other participating/consuming applications downstream. The solution should support interoperability and, potentially, harmonization of metadata.

Common Features

The common features for this market include:

- Data catalog: Inventory, curate and query multistructured data and its derived assets. The inventory capabilities are enabled by machine learning (ML) and automatic detection of relationships with other data assets. The catalog capability extends to provide marketplace experience to curate certified data products backed by data contracts.

- Data dictionary: Manage technical metadata about data elements that are being used or captured in a database, information system or as part of a research project. This capability is associated with a metadata repository, and is used to perform analysis using metadata. Organizations can also use repositories to publish information about reusable assets, which enables users to browse metadata during life cycle activities such as design, testing and release management.

- Data classification: Organize data by relevant categories so that it may be used and protected more efficiently. On a basic level, the classification process makes data easier to locate and retrieve. Data classification is particularly important for risk management, compliance, data security and trust.

- Data profiling and visualization: Conduct statistical and business-rule-based analysis of diverse datasets (ranging from structured to unstructured data and from internal to external data) to give business users insight into the quality of data and enable them to identify data quality issues.

- Match, link, merge (entity resolution): Use a variety of traditional and new approaches, such as rules, algorithms, metadata and ML, to match, link and merge related data entries within or across diverse datasets.

- Governance model management: Review, edit, explore and otherwise interrogate various models (data, policy, rule, organizational, etc.) and various states and conditions over time as relevant for governance work.

- Security (on the platform itself): Provision certain data security policies through data risk assessment and orchestration of data security controls that are available on the governance platform. The controls enact data access privileges, audits or monitoring to enable certain levels of security provision by the platform.

- Tag management: Enable enrichment through user tagging of content or automatic detection, such as personally identifiable information/data (PII or PID). This capability should also provide context (such as tagging and rating) to enable data analysts, data scientists, data stewards and other data consumers to identify and integrate access to additional relevant datasets for the purpose of enhancing business value.

- Analytics models: Govern the iterative advanced analytics and AI models by capturing versioning models and reports and promoting them from development to testing to production environments.

- Data observability: Provide insight into the health of an organization’s data landscape, data pipelines and data infrastructure by continuously monitoring, tracking, alerting, analyzing and troubleshooting incidents to reduce and prevent data errors or downtime. This capability tells not only what went wrong, but also why, and assesses the impacts. Data observability improves reliability of data pipelines by increasing the ability to observe changes, discover unknowns and take appropriate actions.

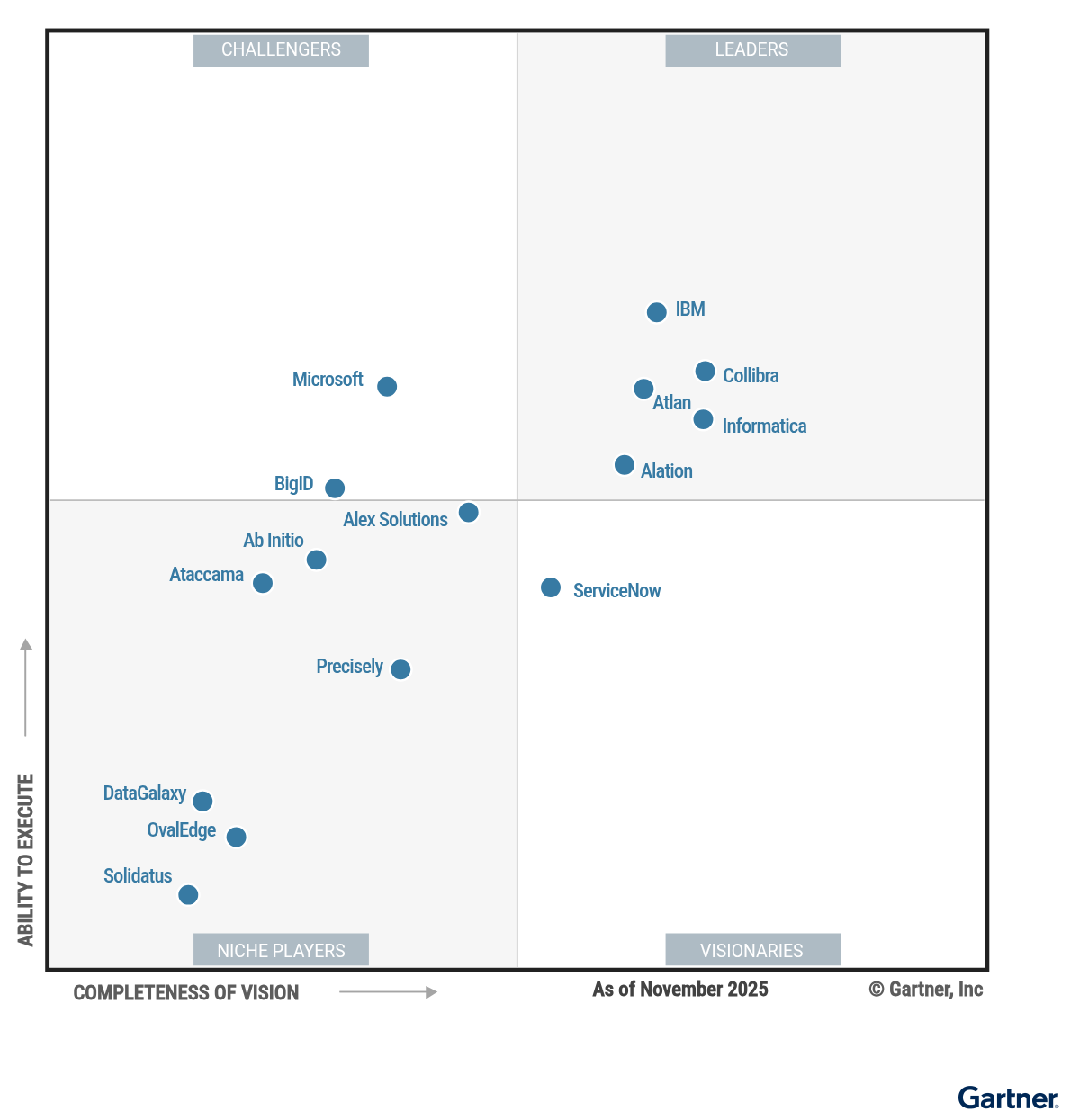

Magic Quadrant

Vendor Strengths and Cautions

Ab Initio

Ab Initio is a Niche Player in this Magic Quadrant. It is headquartered in Massachusetts, U.S. Its D&A governance platform is the Data Platform/Metadata Hub, which is offered as a flexible deployment option across various environments, including cloud, on-premises, virtual machines, containers and cloud marketplaces. The platform encompasses user context and personas, semantic terms and ontologies, operational information, catalog, lineage, marketplace, semantic rules, controls, and agentic AI instructions. Ab Initio has more than 250 global customers, the majority of which are located in North America and Europe. Ab Initio’s operations are geographically diverse, with customers across sectors, including financial services, telecom, and healthcare. Ab Initio is notable for its metadata-driven design and data integration. These features can help support governance by improving data consistency and traceability. It has stable financials, positive customer feedback, and plans to further develop AI capabilities, self-service options, and easier deployment.

- Mature, Unified Platform: Ab Initio provides a metadata-driven data management platform that includes data integration and data quality as enablers for data governance, making it highly suitable for complex and regulated enterprise environments.

- Agentic AI Framework and Innovation: Its Agentic AI framework leverages active metadata for managing, monitoring, and controlling data processes with minimal manual intervention, while adapting governance actions based on the specific context of data and workflows.

- Long-Term Stability: As a privately held, profitable company with no long-term debt and a subscription-based revenue model, Ab Initio maintains long-term stability and strong customer relationships.

- Evolving Marketing Strategy: Ab Initio does not have broad market understanding, given its historically referral-based and technology-led strategy. To ramp up its current relatively lower brand awareness and market share, Ab Initio is moving to a more direct marketing and partner-led approach, which may impact product support and the overall engagement model.

- Limited Sales and Services Partnership: The company focuses on direct software sales, with a relatively less extensive sales and service partner ecosystem, which may be suitable for regulated industries with targeted and complex support requirements. However, it may not be suitable for enterprises requiring broad, standardized services.

- Change Risks: Ab Initio’s roadmap includes significant changes, such as a redesigned UI for business users and a new platform as a service (PaaS) offering, introducing execution risk as it adapts to broader user needs and cloud-native deployments.

Alation

Alation is a Leader in this Magic Quadrant. It is headquartered in California, U.S. Its data and analytics governance platform includes: Data Catalog (foundation of the Agentic Data Intelligence Platform), Data Governance, Data Quality, Data Lineage, and Analytics and Data Products Marketplace. These offerings are available as SaaS options in the AWS cloud or can be deployed in an infrastructure as a service (IaaS) configuration on AWS, Google Cloud and Microsoft Azure. The products can also be installed on-premises or in private cloud environments. Alation has over 650 customers, most of which are located in North America. Its customer base is primarily concentrated in the financial services and manufacturing sectors. Alation stands out for delivering a flexible, AI-driven platform for data governance and productization, enabling organizations to automate and scale trusted data management in an evolving market.

- Open and Portable Architecture: Alation’s platform is designed to avoid vendor lock-in. It emphasizes data sovereignty and flexibility, allowing customers to maintain control over their data environment.

- AI-Driven Governance: Alation’s platform is developing AI agents for policy management, providing features like instant data quality checks, behavioral analysis, and proactive resolution, which automate and streamline some governance tasks.

- Operational Excellence: Alation has improved its operations with a focus on resource optimization, expanding customer base, and leveraging a broad partner ecosystem with major technology providers (e.g., Snowflake, Databricks, AWS, Google, Microsoft), supporting integration and interoperability across modern data and analytics environments.

- Cloud-First Module Availability: Advanced modules like Data Quality and Data Products Marketplace are only available out of the box for Alation Cloud Service users. Customer-managed (on-premises) deployments would require additional resources for enablement, integration, and ongoing maintenance to access similar capabilities.

- Evolving Policy Declaration Capabilities: While Alation’s current policy enforcement features have improved with Policy Center and Workflow Center modules, its native policy declaration at the data product level is still maturing compared to best-in-class competitors.

- Upskilling/Adoption Challenges: Adoption of advanced features such as the Data Products Builder may present challenges related to organizational change management and upskilling. While Alation has invested in training resources, customers should anticipate the need for dedicated effort and planning to ensure successful uptake and effective use of these capabilities.

Alex Solutions

Alex Solutions is a Niche Player in this Magic Quadrant. It is headquartered in Melbourne, Australia. Its data and analytics governance platform includes: Unified Data Intelligence Platform, Data Hub, OpenMetaHub (OMH), Intelligent Connectors, Alex AI Guru, and Enterprise Reporting and Analytics (ERA). These offerings are available on-premises and in the cloud. In the cloud, they can be deployed as managed services and software as a service (SaaS). Alex Solutions has over 60 customers globally, with the majority located in APAC and North America. Its customer base is primarily concentrated in the financial services and manufacturing sectors. Alex Solutions stands out for a comprehensive, automated metadata governance platform that makes AI and data analytics trustworthy, scalable, and compliant, especially for enterprises in regulated sectors.

- Unified Governance Platform: Alex Solutions offers a unified platform where all governance features (lineage, quality, connectors, policy management) are native and integrated. This enables dynamic, automated, and explainable data governance at scale, setting Alex apart from more fragmented or passive solutions.

- Effective Integrations/Operationalization: Alex integrates seamlessly with enterprise tools, such as Jira, Snowflake, and Databricks, embedding governance directly into operational workflows. This ensures governance is proactive, with features like automated impact analysis and policy enforcement within daily business processes.

- Scaling Governance Enforcement: The platform supports natural language policy drafting, reusable governance playbooks, and real-time dashboards for compliance. Automated enforcement and alignment between business policies and technical execution help enterprises scale governance efficiently.

- Market Agility: Alex Solutions prioritizes regulated, compliance-driven industries over horizontal expansion to achieve targeted adoption and outcomes in these sectors. This cautionary growth strategy limits its ability to rapidly horizontal scale in the market compared to other vendors.

- Evolving Cloud-Native Focus: Alex’s platform offers robust on-premises capabilities, particularly valued in regulated markets. Broader cloud-native and SaaS-first delivery options is an area of continued expansion as customer preferences evolve.

- Evolving Governance Marketplace/Playbook Ecosystem: The Alex Data Playbooks are a competitive differentiator for sharing and discovering reusable governance assets, including executable workflows. However, the marketplace UI and curation of underlying assets is still evolving for better discoverability and adoption.

Ataccama

Ataccama is a Niche Player in this Magic Quadrant. It is headquartered in Ontario, Canada. Its primary D&A governance platform, Ataccama ONE, is available for cloud and on-premises use. It has about 270 active customers, most of which are based in EMEA and North America. These customers are predominantly from the finance, insurance, and manufacturing sectors. Ataccama ONE stands out for its focus on data quality, MDM offering, and AI agent for automation, along with capabilities for governing unstructured data.

- Data Profiling/Visualization: Ataccama ONE provides strong core data quality functions, including the ability for users to define and execute custom profiling rules, with strong AI/ML automation support for different data quality workflows.

- Unstructured Data Quality: Ataccama’s data quality capabilities such as quality checks and approval processes, can extend to documents-based unstructured data via Document AI, though remediation is primarily manual. The platform profiles data, extracts attributes and structures them to apply quality rules and includes reporting on unstructured data quality issues in its profiling reports and quality dashboards.

- Sales Execution Pricing: Ataccama has a lenient pricing approach, offeringing unlimited, free “consumer users” licenses with comment and view access to the platform. They do not have additional charges for metadata assets including policies, rules, etc.

- Workflow Management: Ataccama has limitations in its workflow management capabilities, lacking a native business process modeling capability to design and visualize workflows and processes. There are also limited out-of-the-box, role-specific user interfaces for stewardship.

- Inadequate Self-Service Customization: A relatively small portion of Ataccama’s platform customization is done by customers themselves. The rest relies on Ataccama or independent consultants.

- Sales Strategy: Ataccama targets regulated industries for its sales, but it has limited out-of-the-box support for policy modeling for industry and geographic regulations, and does not provide prepackaged rules or policy engines for AI-specific regulations.

Atlan

Atlan is a Leader in this Magic Quadrant. It is headquartered in San Francisco, U.S. Its product (also Atlan) is a cloud-first, AI-native single platform offering a metadata control plane for streamlined and real-time governance across data, analytics, and, increasingly, AI models. It has over 300 customers, the majority of which are in North America, and its customers tend to be technology, professional, and financial services, healthcare and education, and consumer and industrial. Atlan stands out in its focus to deliver AI-native governance through context (metadata)-based ecosystem partnerships, agentic stewardship and orchestration of enterprise agentic systems.

- Future-Proofed Architecture: The core architecture of Atlan’s “metadata lakehouse” is built on Apache Iceberg’s open table format, which allows for scalable, unified metadata cataloging for structured, semistructured and unstructured data. From a governance perspective, this allows for trusted, query-able and auditable metadata for automation, event-driven and real-time policy enforcement across diverse scenarios and systems.

- Vision for Ecosystem-Led Innovation: Leveraging the metadata lakehouse, the Atlan App Framework provides a structured toolkit and a marketplace to help developers, customers, and partners build, deploy, and share a wide range of applications, including custom connectors, data quality apps, and governance agents. While newly launched, it demonstrates the continued focus to facilitate and accelerate collaboration within and across AI-native enterprises using their platform for automated governance.

- Market Presence and Growth: Gartner client inquiries suggest that customers perceive Atlan as a modern, innovative, advisory-oriented organization, which has enhanced its market presence and sales momentum. This is reflected in its relatively higher customer and revenue growth vs. competitors.

- Missing Advanced Data Quality and MDM Capabilities: Atlan doesn’t natively provide advanced data profiling, entity resolution, and data quality analytics and workflows but leverages external packages and partners, such as Great Expectations, Monte Carlo, Anomalo, and Ataccama. However, Atlan’s new data quality studio is available and being further developed for more advanced data quality capabilities, currently only for Snowflake and Databricks environments.

- Deployment Limitations: Although Atlan provides secure agents for on-premises interaction and connectivity with its cloud-based services, it’s primarily offered as a cloud-managed SaaS and PaaS solution that’s delivered on major cloud providers’ containerized services. This limits options for organizations seeking traditional on-premises or privately managed deployments.

- Relatively Limited Large-Enterprise Experience: Nearly three-fourths of Atlan’s customers are SMB and midsize organizations from AI-forward and relatively less regulated industries. A small number of Peer Insights and customer interaction data mentioned reduced performance at large-scale deployments.

BigID

BigID is a Challenger in this Magic Quadrant. It is headquartered in New York, U.S. Its product, BigID Next, provides a single integrated platform to combine data, analytics and AI governance with a focus on data security and privacy policy enforcement and execution. It has around 350 customers, most of which are based in North America. Those customers span multiple industry verticals, particularly in regulated environments. BigID is known in the data security technology space for data loss prevention, privacy management, and AI risk and security management. As organizations are removing silos across security, risk, AI, and D&A governance operating models, the platform stands out for supporting an integrated governance model.

- Data Discovery and Classification: BigID Next offers broad coverage of out-of-the-box connectors across different data sources, particularly for semistructured and unstructured data sources. It supports text chunking, vector embedding, search, classification, metadata extraction, and enrichment of unstructured content. These are crucial capabilities for governing the AI development life cycle that competitors in the traditional D&A governance space are enhancing.

- AI Risk Management: The platform provides a framework for AI risk management (including data-related risks) that covers detection, prioritization, mitigation, monitoring, validation, compliance and transparency, with strong support for human oversight. The human oversight is augmented by embedded AI assistants that help prioritize risks, suggest remediations, and recommend stewardship actions.

- Diverse Persona Support: Given BigID’s intention to integrate siloed governance efforts, it provides out-of-the-box UI support for a broad set of governance-related personas, including data stewards, line of business leaders, AI/ML teams, privacy officers, and compliance and legal teams.

- Product and Partnership Strategy: BigID’s dominant product strategy is to enrich and complement existing catalog and/or governance tools (e.g., Collibra, Alation, Purview) through its centralized metadata hub. However, as it expands its focus from privacy/security to include the D&A governance office as a buyer, users should carefully evaluate whether BigID’s evolving product, marketing, and partnership strategies will fully meet their needs as a primary platform for D&A governance.

- High-End Pricing and Complexity: BigID’s pricing model tends to be on the higher end compared to competitors. Instead of flat-rate pricing, the platform’s pricing is customized around factors like the number of data sources, applications involved, deployment type, and support requirements, which can lead to a higher cost.

- Scaled Deployment: Sixty percent of BigID’s customer base is large enterprises with potentially huge data footprints. BigID Express for SMBs is a lighter version that excludes add-on apps and advanced features that would require further configuration.

Collibra

Collibra is a Leader in this Magic Quadrant. It’s dually headquartered in New York, U.S., and Brussels, Belgium. Collibra has over 700 active customers across more than 50 countries. Its unified governance platform includes Collibra Data Governance, Collibra AI Governance, Collibra Data Catalog, Collibra Data Lineage, Collibra Data Quality & Observability, Collibra Data Privacy, and Collibra Protect. Its deployment options are predominantly SaaS cloud-based, but also include PaaS, IaaS, multicloud, private cloud, FedRAMP cloud, and hybrid environments. Collibra has made two significant acquisitions (which were not integrated with the core platform at the time of this evaluation) to improve its platform-native capabilities — Deasy Labs for unstructured data governance and Raito for data access capabillities.

- Strong Market Understanding: The platform’s vision is to offer end-to-end governance, serving as a single control and context plane for managing data and AI assets with native core modules, including data quality and observability and AI governance. Its focus is to address modern governance requirements including unstructured data, data products, and AI.

- Deep Ecosystem Partnership: Collibra has a strong partnership network with major technology providers and system integrator partners such as AWS, Google, Infosys and Snowflake. It provides native integrations with more than 100 different data environments or applications, including bidirectional integration with the SAP environment.

- Unified Platform for Data and AI Governance: Collibra’s dedicated AI Governance module, built on the core governance module, caters to governing AI models, including third-party or embedded models. The module acts as a governed model registry, documenting models with their metadata and providing automated policy enforcement support for key regulatory and compliance checks.

- Customization and Implementation: Achieving operational maturity and tailoring the platform to an organization’s specific metadata model, roles, and workflows require significant investment. Client interaction and Peer Insights data indicate that successful implementation typically requires substantial external effort, with 40% of customization generally performed by independent consultants.

- Feature Parity Based on Deployment: Collibra’s managed SaaS offering on AWS and GCP is the most feature-rich and up-to-date deployment. Customers deploying outside AWS or GCP, or using self-hosted models, should be aware that native support and the latest functionalities, including those which are AI-powered, may be limited compared to the primary SaaS offering.

- Current Scope of SaaS Data Quality Module: The SaaS-based data quality and observability module, as part of the unified platform, is a new offering at an added cost over the base platform. The module is not a full suite data quality tool, and many features, such as monitoring of streaming data, remediation support, and deduplication, are not currently supported.

DataGalaxy

DataGalaxy is a Niche Player in this Magic Quadrant. It is headquartered in Lyon, France. Its integrated data governance solution consists of DataGalaxy Metadata Hub and DataGalaxy Strategy Hub, which focus on realizing value from governance and data management activities through an intuitive UI. DataGalaxy has 200 active customers, and its customer base exists mostly in EMEA. Those customers primarily fall within the public sector as well as the financial services and insurance industries. Its product strategy focuses on providing an intuitive platform with automation to enable users to realize fast time to governance value.

- Innovation in Governance: DataGalaxy has launched its value governance platform, which goes beyond traditional control and compliance governance by enabling users to align governance to business objectives, track value of data products, and personalize and monitor business-related KPIs.

- Customer Experience: DataGalaxy’s comprehensive training and support services create a positive customer experience. Its customers report the platform is simple and intuitive, but it offers in-person and online training worldwide and does not price differently for support levels.

- Workflow Management: DataGalaxy offers many workflow management capabilities, including translation between rules stored in the repository and the user interface. Its many out-of-the-box collaboration workflows include external data acquisition, publishing certified data assets and data products.

- Unstructured Data Governance: DataGalaxy doesn’t currently offer cataloging and governance support (such as lineage tracking, tagging, parsing, and classification) for unstructured data.

- Data Profiling and Observability: The platform does not provide adequate profiling, monitoring, and detection capabilities, such as creation and execution of user-defined rules, scheduled execution of profiling processes, and anomaly detection. DataGalaxy does not provide native observability capabilities.

- Overall Viability: Due to the nature of the platform, DataGalaxy’s growth strategy is targeting new customers rather than expanding existing customer contracts. Most of its customer base consists of small or midsize enterprises, possibly limiting its ability to expand, and it relies on resell partners more heavily than other vendors in this market do.

IBM

IBM is a Leader in this Magic Quadrant. It is headquartered in New York, U.S. IBM has global operations in 170 countries across various sectors, including regulated industries. IBM’s data and analytics governance strategy centers on watsonx, with key D&A governance platform offering being watsonx.data intelligence and watsonx.governance for AI governance. Its focus is delivering on autonomous data product curation and agentic AI-powered governance, and unifying governance of structured and unstructured data.

- Architectural Strength: watsonx is an open, integrated data and AI platform built for hybrid environments and powered by an intelligent metadata layer. The rationalization and integration of modules within the watsonx portfolio for data management, governance, and AI model development are designed to accelerate AI adoption while ensuring strong governance and compliance.

- Unified Governance Platform Experience: The new system integrator watsonx.data intelligence platform provides a more cohesive experience that has preintegrated modules of IBM Knowledge Catalog, Manta Data Lineage, and Data Product Hub. The shared metadata layer of the platform with watsonx.governance for AI enabling integration to manage governance across both data and AI assets, supports unified oversight and compliance.

- Innovation: IBM has executed many innovative use cases relevant for governance tasks including agentic assistant for task management support, unstructured data curation and lineage support, and advanced anomaly detection through historical stability checks.

- Feature Differences: The platform’s functional capabilities are inconsistent across SaaS and software (on-premises or self-managed) deployment, and across different product packaging. For example, users of IBM Knowledge Catalog Standard do not have access to rule management and data protection features that are available in the new watsonx.data intelligence platform.

- Migration Challenges: The current customers of IBM InfoSphere moving to the new platform (watsonx.dataintelligence) face potential technological challenges (e.g., metadata loss, re-establishing integrations and preserving workflows), lack of change management and learning support, and new resource unit-based licensing. Achieving the same functionality may require manual intervention and use of IBM’s provided migration tools.

- Limited Applicability for Smaller Organizations: IBM solutions often require significant customizations performed by IBM and independent consultants. Client interactions suggest that skilled IT professionals are essential for successful deployment and scaling. IBM’s platform is frequently perceived as being complex and best suited for large enterprises, though the introduction of a SaaS solution may help reduce those concerns going forward.

Informatica

Informatica is a Leader in this Magic Quadrant. It is headquartered in California, U.S. Its data and analytics governance platform is Informatica Intelligent Data Management Cloud (IDMC). IDMC is a cloud-native SaaS solution supporting multicloud environments such as AWS, Azure, GCP and Oracle. Informatica has 5,000+ customers for all its products that span 80+ sectors. It operates globally, with a significant presence across North America, EMEA, and APAC, and a strong focus on supporting customers worldwide through partnerships with major cloud providers and global system integrators. Informatica has a comprehensive platform that centralizes management and governance for all data types, including structured data, unstructured data, and AI assets. It offers neutral ecosystem support across major clouds, persona-friendly interfaces, and advanced automation through its CLAIRE engine and agentic capabilities. Informatica delivers effective governance features, fine-grained controls, and robust scalability, backed by financial growth and customer success.

In May 2025, Salesforce entered into an agreement to acquire Informatica. The acquisition closed 18 November 2025.

- Comprehensive Coverage/Integration: Informatica’s platform supports diverse data sources across on-premises and cloud environments. Informatica has strong partnerships with major hyperscalers, ensuring broad compatibility and seamless integration for enterprises.

- AI-Powered Automation/Augmented Capabilities: Informatica leverages unified metadata and advanced AI engines (CLAIRE Copilot, CLAIRE GPT) for predictive and GenAI, enabling recommendations and natural language queries that promise to help clients with aspects of automated data governance.

- Financial Viability/Market Responsiveness: Informatica shows robust financial health, consistent revenue growth, and significant investment in innovation, with a flexible consumption-based pricing model and rapid adaptation to GenAI and governance trends.

- Adoption and Change Management: While IDMC’s PaaS model streamlines deployment, organizations with limited data governance maturity may require additional support and change management to fully realize the platform’s value and best practices.

- Operational Resilience in Multicloud Environments: Informatica’s broad cloud hosting strategy generally mitigates risks from shifting partner priorities, but operational disruptions, such as major cloud provider outages, could impact service availability. Customers should evaluate Informatica’s failover and disaster recovery capabilities to ensure business continuity.

- Product Strategy Post Acquisition: Given the recent acquisition by Salesforce, Informatica’s product roadmap, and go-to-market and sales strategy may change.

Microsoft

Microsoft is a Challenger in this Magic Quadrant. It is headquartered in Washington, U.S. Its platform, Purview, is a unified SaaS-based data governance platform built on Azure. It offers data cataloging, quality management, security, and compliance capabilities across cloud, on-premises and hybrid environments. Despite being a relatively new offering in the market, Purview has a large global customer base that spans diverse industries primarily driven by adoption in its broad Azure, Fabric, and Microsoft 365 client base. Purview invests in building an open, extensible governance (including security) platform offering augmented by AI and geared toward less technical users, which has been its traditional user base. Microsoft reports that 75% of its Microsoft 365 Copilot customers use Purview.

- Governance Within Microsoft Ecosystem: Purview is well-integrated with both Microsoft 365 and the Azure environment and continues to work on deeper integration. This enables unified data governance, cataloging, security, and compliance across these platforms, which might be preferred by Microsoft-first organizations.

- Overall Viability: Customer interactions and secondary research suggest a relatively higher number of customers, driven primarily by Purview’s bundling into Azure deals at competitive pricing. Its broad partner network and advisory services allow for higher market mind share and capture.

- Security and Risk Management: Purview provides robust security and risk management features, including granular access controls, sensitivity labeling, audit logging, and native data loss prevention across Microsoft 365 services, Azure, and Microsoft Fabric, which will be suitable for CDAOs’ and CISOs’ security-oriented D&A governance program.

- Product Immaturity: As a relatively new offering in this market compared to other vendors, Purview’s current product maturity lags behind others, particularly in supporting knowledge graph, data product curation and governance, workflow management, automation, data profiling, entity resolution, and unified experience between product modules.

- Platform Extensibility: While Purview’s strategy is to be a unified governance platform for all data (not just Microsoft data), it still has to strengthen third-party integrations with a broader set of out-of-the-box connectors and ecosystem partnerships compared to other vendors in this market.

- Pricing: The pricing is primarily based on a pay-as-you-go (PAYG) model, with costs based on the number of assets curated in the catalog and the processing units used. Increased curation and use of advanced features can lead to higher costs. Some broader security and compliance features, such as Insider risk management, data security posture management, and audit, are available through Microsoft 365 E5/E5 compliance add ons, rather than the Purview Data Governance PAYG model, depending on the data source, which may add to overall cost.

OvalEdge

OvalEdge is a Niche Player in this Magic Quadrant. It is headquartered in Georgia, U.S. The OvalEdge platform enables customers to catalog datasets, define business glossaries, trace data lineage, monitor quality, enforce data access policies, and monitor and enforce privacy and compliance policies with competitive pricing. OvalEdge has over 200 customers, primarily in the North America and EMEA regions. Its customers are mostly in the finance, technology, and healthcare/services industries. OvalEdge’s most notable release in the past 12 months is its askEdgi AI chatbot, which customers can use to identify and analyze data.

- Connectivity/Integration: OvalEdge offers 150 native connectors. These connectors include relational database management systems, analytics and reporting platforms, ETL/ELT platforms, and file systems and content repositories.

- Sales Execution/Pricing: OvalEdge offers flexibility in deal sizes, with various modules that can be added as the governance program scales. This makes governance less complex for those who are just getting started, while still maintaining capabilities for customers who are more advanced in their governance practices.

- Workflow Management: OvalEdge offers native business process modeling through a visual diagram for users to design the governance workflow. There are also workflows that are extended to unstructured data, including the ability for viewer-level users to provide feedback on metadata attributes for unstructured data in the catalog.

- Geographic Strategy: OvalEdge’s growth may be restricted by its limited local geographic presence and customer base, which is mostly in EMEA and North America.

- Analytics Models: The platform has limited capabilities to govern advanced analytics models. It does not include risk assessment, bias detection, regression testing, or drift detection, and does not demonstrate the fitness of data for AI use cases. It also does not integrate with environments and tools used for developing AI models (such as DSML platforms and MLOps tools).

- Data Profiling and Visualization: OvalEdge does not natively support profiling or quality capabilities for unstructured data. It also lacks the ability to configure user-defined rules and execute profiling analysis, and to analyze trends in profiling results over time.

Precisely

Precisely is a Niche Player in this Magic Quadrant. It’s headquartered in Massachusetts, U.S. Its data and analytics governance platform is the Precisely Data Integrity Suite, which is a SaaS solution. Precisely’s Data Integrity Suite has a global reach with 150 customers across the U.S., Australia, France, Germany, Singapore, India, Poland, and Brazil. The platform provides unified governance capabilities on a shared metadata foundation to enable trusted outcomes across hybrid environments. Future focus involves prioritizing automated metadata curation, an agentic ecosystem, AI assistant/chat interfaces, extending governance to unstructured data, and data catalog federation and a knowledge graph deployment utilizing AI/ML for autonomous policy enforcement.

- Single, Integrated Suite: Precisely’s solution uses a modular architecture to unify essential capabilities like governance, quality, observability, integration, enrichment, and geospatial intelligence on a shared metadata foundation. This holistic approach with seamless integration differentiates Precisely from competitors’ solutions and accelerates time to value.

- Hybrid Deployment and Mainframe Specialty: Precisely offers a deployment model with a hybrid approach where agents, managed from the cloud, connect and interoperate with data systems residing in other environments. Their strong core enterprise systems support, especially for organizations reliant on mainframe data access and governance, is facilitated through these agents.

- Business-Friendly Design: The platform offers a business-friendly design and user interface that lessens the technical learning curve and accelerates time to value. Its AI/ML augmentation, such as several newly delivered AI-generated descriptions for technical and business assets, reduces manual effort for data stewards and improves catalog clarity.

- Limited Unstructured Data Support: Precisely’s capabilities are largely restricted to structured and semistructured data. Customers who rely heavily on documents, emails, or multimedia content for governance and analytics may find these areas unsupported by the solution’s native functionality.

- Rule Management Limitations: The platform’s rule management capability lags behind competitors. For example, it doesn’t currently support natural-language-based rule generation, version control, rule management for unstructured data, and DataGovOps principles.

- Bidirectional Metadata Exchange and Policy Support Gaps: Automated bidirectional synchronization of metadata with third-party tools and out-of-the-box policy engines for AI-specific regulations (such as the EU AI Act) are not currently available.

ServiceNow

ServiceNow is a Visionary in this Magic Quadrant. It is headquartered in California, U.S. Its primary platform is the data.world Enterprise Data Catalog & Governance Platform that plans to operate within the larger context of the ServiceNow data control tower vision following the July 2025 acquisition of data.world. With 74 office locations in 33 countries, ServiceNow offers support and training worldwide. Its customers are mostly based in North America, followed by EMEA and APAC. The current focus is for deepening data.world’s bidirectional integration with ServiceNow to enhance task management and agentic applications.

- Workflow Orchestration: ServiceNow’s unification of its governance platform with its workflow automation capabilities is a strategic strength that enables actionable, closed-loop governance. It supports the principle “govern once, enforce everywhere” by pushing policies down to execution systems like data warehouses and BI tools.

- Knowledge Graph/Semantic Foundation: The platform is natively built on a knowledge graph that allows it to model policies, governance roles, and governed data assets as nodes and connections. This provides flexibility and ensures semantic consistency throughout the data ecosystem.

- AI-Driven Automation: The platform leverages AI (including GenAI) to automate and democratize governance through capabilities such as natural language interaction, automated notification, and query translations.

- Product Offering Limitations: The platform is currently only available as a cloud-based service managed by the vendor in AWS. It does not support on-premises installation or offer perpetual licensing, and customers must use the subscription model in the cloud.

- Limited Unstructured Data Governance Support: The platform focuses primarily on governing structured and semistructured metadata, with limited support for unstructured data governance.

- Product Strategy Post Acquisition: Given that data.world is actively being integrated into ServiceNow’s offerings, the overall product and sales strategy as a stand-alone governance platform may change.

Solidatus

Solidatus is a Niche Player in this Magic Quadrant. It is headquartered in the U.K. The Solidatus platform offers data lineage, catalog, governance, and management solutions. Solidatus’ operations are focused in North America and EMEA markets. Its customers are large and complex organizations predominantly in the banking and securities industries. Its product implementations are equally managed by internal resources and external implementation partners. Solidatus’ roadmap projects the addition of AI capabilities such as incorporating agents in metadata creation, curation and activation, and new industry use cases beyond the financial services industry through its partnerships.

- Product Strategy: Solidatus has a collaborative approach to feature development, including co-developing agents with its customers to ensure alignment of features with customer priorities and augmentation requirements.

- Data Lineage: Solidatus provides data lineage at a granular level and is designed to manage lineage across complex environments. It includes a modeling capability that simulates proposed changes and their implications before implementing in production.

- Analytics Models: The platform provides capabilities for model governance, including detection of schema drift and data drift with impact analysis, UI for managing AI model documentation, lineage, and a dashboard for reporting on KPIs related to model governance.

- Reliance on Independent Consultants: Solidatus’ platform customization relies heavily on independent consultants, with a minority being done by customers themselves. Its customers report limited connector capability as well.

- Data Profiling and Visualization: Solidatus is a metadata platform with limited ability to perform tasks related to profiling and visualization natively. The platform requires integration with other solutions to support a full range of governance activities.

- Solution complexity: The platform takes longer to implement compared to peers’ platforms. It is less suitable for organizations early in their governance journeys that are seeking a quick lightweight approach to establishing their governance capabilities.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

BigID: BigID met the inclusion criteria this year and was added.

Microsoft: Microsoft met the inclusion criteria this year and was added.

Dropped

Global Data Excellence: Global Data Excellence did not meet the inclusion criteria of “impact” based on the Customer Interest indicator (CII) identified by Gartner for this Magic Quadrant. The CII shows the market momentum for the vendor in this market.

Anjana Data: Anjana Data did not meet the inclusion criteria of “impact” based on the Customer Interest indicator (CII) identified by Gartner for this Magic Quadrant. The CII shows the market momentum for the vendor in this market.

Quest Software: Quest erwin (previously erwin by Quest) was excluded from this year’s Magic Quadrant because Quest was in the midst of making a strategic pivot for its product and brand during the evaluation period. The focus on being a broad data management platform for AI doesn’t fit the market description prima facie.

Inclusion and Exclusion Criteria

To qualify for this body of research vendors must meet the following requirements:

General availability (GA)

Offer stand-alone platform solutions that are positioned, marketed, and sold specifically for general-purpose data and analytics governance applications. Vendors that provide several D&A governance product components must demonstrate that these are integrated and collectively meet the full inclusion criteria for this Magic Quadrant. The platforms must demonstrate the capabilities as available in GA from June 2025.

Product or service capability

Policy setting operationalization and augmentation through a set of capabilities:

- Information policy representation

- Organization and role model

- Workflow management

Policy enforcement operationalization through a set of capabilities:

- Business glossary

- Data lineage and impact analysis

- Orchestration/automation:

- User interface (UI) for stewardship

- Task management

- Rule management (low level)

Connectivity and integration with operational and analytical data systems.

Support augmentation and automation of at least five capabilities through AI/ML (including NLP based on LLM support), knowledge graph, and active metadata.

Capability in large-scale deployment (in terms of number of concurrent users and data volume) via architectures that can support concurrent users and applications. All deployment types should support capabilities listed above. Vendors must showcase at least 10 large-scale deployments (>than 500 users/>50 data sources/>1,000 data assets).

The solution is intentionally geared primarily toward nontechnical users involved in governance work. They are supported by end-user functionality for the following types of users: business data stewards, analytics stewards (stewards operationalizing governance in analytics pipelines), data scientists, business intelligence analysts, citizen users, data architects, data quality analysts, data engineers, database administrators, and data integration analysts.

Support integration and interoperability with other data management and governance-related solutions such as metadata management, master data management, data quality, data security platforms, and AI governance platforms from third-party tools.

Demonstrate in at least three business scenarios how the platform operationalizes and automates policy setting, policy enforcement, and policy execution (in conjunction with existing data management technologies).

Performance

Maintain an installed base of at least 50 production paying customers (different companies/organizational entities/logo) for their flagship data governance solution (not just individual smaller modules or capabilities). The customers must be running in production for at least one month.

Provide direct sales and support operations, or a partner providing sales and support operations in at least two of the following regions: North America, LATAM, EMEA, and Asia/Pacific.

Impact

Rank among the top 25 organizations in the Customer Interest Indicator (CII) identified by Gartner for this Magic Quadrant. CII was calculated using a weighted mix of internal and external inputs that reflect Gartner client interest, vendor customer engagement, and vendor customer sentiment in the last 18 months.

Data inputs used to calculate D&A governance market momentum included a balanced set of measures:

- Gartner.com search

- Inquiry volume

- Frequency of mention in PI competitors

- Google trends search index

- Number of followers on Twitter and LinkedIn

- Average visits/month: web traffic analysis

Geographic coverage

The customer base for production deployment must include paying customers in multiple countries (at least five) and in two or more regions (North America, LATAM, EMEA, and Asia/Pacific).

Industry coverage

The customer base must be representative of at least three or more industry sectors (different logos).

Honorable Mentions

Global Data Excellence (GDE): While GDE is dropped in this year’s evaluation on account of low market momentum, its DEMS-NIXUS platform provides a strong governance product offering that is grounded in the fundamentals of data sovereignty, semantic and linguistic AI, and ethical data management, focusing on specific domains of business and operational excellence, crisis management, and defense.

Amazon Web Services (AWS): AWS provides governance functionality across its environment through an integrated solution portfolio (instead of a stand-alone platform) that includes Amazon SageMaker Catalog (cataloging, discovering, and curating), AWS Glue, and Amazon SageMaker (its main data management platform with built-in governance). AWS doesn’t meet the inclusion criteria for platform extensibility across diverse data systems and cloud environments.

Google: Google’s Dataplex Universal Catalog is a unified governance solution for the Google Cloud environment integrated into BigQuery. Google doesn’t meet the inclusion criteria for platform extensibility across different cloud environments. Google partners with third-party vendors such as Collibra and Informatica for multicloud use cases.

Evaluation Criteria

Ability to Execute

Gartner analysts evaluate providers on the quality and efficacy of the processes, systems, methods, or procedures that enable D&A governance platform provider performance to be competitive, efficient, and effective, and to positively impact revenue, retention, and reputation within Gartner’s view of the market.

Product or Service: The capabilities, features, and overall quality of the core goods and services that compete in and or serve the defined market. Our analysis focused on the following areas (the list is not exhaustive): score, feedback on product capabilities, depth/breadth of capabilities, differentiated D&A GP product, support for the emerging needs of the market including for unstructured data governance, trust models, data product governance, and AI.

Overall Viability: The organization’s overall financial health, as well as the financial and practical success of the relevant business unit. This includes the likelihood that the organization can continue to offer and invest in the product, as well as the product’s position in the organization’s portfolio. Our analysis focused on the following areas (the list is not exhaustive): year-over-year growth (for overall vendor and for the product in the market), profitability, R&D investment, and customer perception of future viability.

Sales Execution/Pricing: The organization’s capabilities in all presales activities and the structures that support these activities. This includes deal management, pricing and negotiation, presales support and the overall effectiveness of the sales channel. Our analysis focused on the following areas (the list is not exhaustive): number of net new customers, quality of sales-related activities, pricing model/pricing and contract flexibility.

Market Responsiveness and Track Record: The ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve, and market dynamics change. This includes the provider’s history of responsiveness to changing market demands. Our analysis focused on the following areas (the list is not exhaustive): customer base, new customer acquisition, product release frequency and impact, ability to sense and adapt to changing market, and vendor track record.

Marketing Execution: The ability to deliver clear, high-quality, creative, and effective messaging via publicity, promotional activity, thought leadership, social media, referrals, and sales activities. This includes the organization’s ability to influence the market, promote the brand, increase awareness of products, and establish a positive reputation among customers. Our analysis focused on the following areas (the list is not exhaustive): Gartner presence (client inquiry volume, search analytics), social media presence, brand name recognition/customer’s familiarity with product or vendor, and range of programs to increase product profile.

Customer Experience: The degree to which a vendor’s products, services, and programs enable customers to achieve their desired results. This includes the quality of supplier/buyer interactions, technical support, or account support, as well as ancillary tools, customer support programs, availability of user groups, and service-level agreements. Our analysis focused on the following areas (the list is not exhaustive): overall satisfaction with the provider’s capabilities and delivery, flexibility and adaptability in negotiating final contracts, product SLAs, service-level support, and its pricing and implementation time.

Operations: The ability of the organization to meet its goals and commitments. This includes the quality of its organizational structure, skills, experiences, programs, and systems that enable the organization to operate effectively and efficiently. Our analysis focused on the following areas (the list is not exhaustive): reliance on ecosystem partners, M&A activities, certification to improve market reach, implementation tools/programs to support customer success, number of implementation resources, and locations and number of implementation partners.

Ability to Execute

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | High |

Marketing Execution | Medium |

Customer Experience | High |

Operations | Medium |

Source: Gartner (January 2026)

Completeness of Vision

The evaluation covers current and future market direction, innovation, customer needs, and competitive forces, as well as how well they correspond to Gartner’s view of the market.

Market understanding: The ability to understand customer needs and translate that understanding into products and services. Vendors with a clear vision of the market listen to and understand customer demands, and they can shape or enhance market changes with their vision. Our analysis focused on the following areas (the list is not exhaustive): understanding of market trends, thought leadership and market knowledge, and competitive differentiators.

Marketing strategy: The ability to clearly communicate differentiated messaging, both internally and externally, through social media, advertising, customer programs, and positioning statements. Our analysis focused on brand messaging, user group support, revenue dedicated to marketing, etc.

Sales strategy: The ability to create a sound strategy for selling that uses the appropriate networks, including direct and indirect sales, marketing, service, and communication. This includes partnerships that extend the scope and depth of a provider’s market reach, expertise, technologies, services, and their customer base. Our analysis focused on overall sales strategy, number of D&A GP sales resources and geographic distribution, number of countries with D&A GP sales resources, and number of sales channels/partners for D&A GP.

Offering (product) strategy: The ability to approach product development and delivery in a way that meets current and future requirements, with an emphasis on market differentiation, functionality, methodology, and features. Our analysis focused on (the list is not exhaustive): incorporation of market trends in product strategy, differentiated product capabilities, focus on user experience, and new or planned product features.

Business model: The design, logic and execution of the organization’s business proposition. Our analysis focused on the following areas (the list is not exhaustive): vendor commitment to D&A GP market, business/D&A GP product value proposition, business model evolution, partnership/ecosystem, and M&A strategy.

Vertical/industry strategy: The ability to strategically direct resources (sales, product, development), skills, and products to meet the specific needs of verticals and market segments. Our analysis focused on the following areas (the list is not exhaustive): number of industries with active customers, dedicated resources for specific industry/verticals, and differentiated product capabilities for specific industry/verticals, including regulatory support and certifications specific to industry verticals.

Innovation: Marshaling of resources, expertise, or capital for competitive advantage, investment, consolidation, or defense against acquisition. Our analysis focused on the following areas (the list is not exhaustive): quality of product roadmap and execution/delivery of previous product roadmap.

Geographic strategy: The ability to direct resources, skills, and offerings to meet the specific needs of regions outside the provider’s home region, either directly or through partners, channels, and subsidiaries.

Our analysis focused on the following areas (the list is not exhaustive): number of regions with existing customers, number of regions and offices supporting D&A GP, training support, and support for geography relevant regulations.

Completeness of Vision

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | High |

Sales Strategy | Medium |

Offering (Product) Strategy | High |

Business Model | Medium |

Vertical/Industry Strategy | Low |

Innovation | High |

Geographic Strategy | Medium |

Source: Gartner (January 2026)

Quadrant Descriptions

Leaders

Leaders are vendors that are considered to have a strong ability to execute their strategies and a clear vision for the market and its dynamic evolution. They provide near-comprehensive and integrated solutions that meet customer needs in policy operationalization and automation, and have a proven track record of successful implementations. Leaders are often seen as industry innovators, and they typically have a relatively large customer base or strong market momentum. For this market, we have noticed an increase in the number of Leaders compared to the previous year that have been able to commensurately scale their vision with execution. Given the dynamic nature of this market, the Leaders should be viewed as not necessarily meeting all the demands of the market from a product perspective, but have the vision, resources, and commitment to respond to the market demands.

Challengers

Challengers are vendors that have the ability to execute their strategies effectively, but may lag in understanding the vision for the market compared to Leaders or Visionaries. They offer competitive solutions and have a strong market mind share, but they may not be currently as innovative or forward-thinking as the Leaders. Challengers may be strong competitors in the market. For this emerging market, our analysis showed there are two Challengers — both new entries to this market. One, having leveraged its existing customer base with attractive licensing to scale execution, and another leveraging its security offerings to capture the broader D&A governance market.

Visionaries

Visionaries are vendors that have a clear vision for the market and offer innovative solutions. They are often seen as forward-thinking and capable of driving change in the industry, based on innovation trends. Visionaries may have unique features or capabilities that differentiate them from other vendors but may still need to demonstrate their ability to execute their strategies effectively. In this year’s evaluation, we found only one Visionary, owing to scaled operation and execution on its innovation roadmap, with two Visionaries of last year’s evaluation moving to the Leaders space.

Niche Players

Niche Players provide specialized capabilities that cater to specific customer needs, but may not have the same breadth or depth of offerings or/and market presence in this market. The focus could still be in the data management area rather than data and analytics governance or on specific segments of the customer base (for example, large, regulated industries) or policy type (for example, data quality). The majority of the vendors fall in this quadrant due to the emerging nature of the market.

Context

D&A governance platforms are a composite market that continues to grow. The data management-related segments (database management system [DBMS], data integration, data quality, master data management, metadata management, DataOps, and data observability) grew by 12.9% to $133 billion in 2024. D&A governance platforms also represent roughly a $2 billion market in 2024, with current and forecast market growth well above other data management-related segments.

The D&A governance platform primarily serves business stakeholders for scaled policy management while integrating with data management technologies (storage, integration, DataOps) to complete the governance workflows. This means that besides being a unified, business-friendly platform for policy management for the broadest types of policies, it must have connectivity and metadata sharing (at least unidirectional) with business applications, legacy systems, data management technology stack, and analytics stack. The choice of data governance platform and the capabilities to prioritize should complement the current and planned data management architecture (see How to Align Data Management to Accelerate Data Governance).

The use case scenarios for D&A governance influence the decision about platform choice. The governance use cases are ever-growing and can be fleshed out through the intersection of key dimensions, such as:

- Governance Planes: Operational planes to govern data used in transactional systems (for example, in ERP or CRM) or analytical planes to govern data in analytical (and even experimental) systems such as in lakehouse, analytics, and business intelligence platforms.

- Policy Types: Quality, security, privacy, ethics, life cycle management, or definitions and models (refer to Define Comprehensive D&A Governance Policies to Drive Efficiency).

- Asset to Be Governed: Structured data, unstructured data, KPIs and reports, data products, AI models (including agents), etc.

- Governance Personas to Be Supported: Data owners, governance board members, business and analytics stewards, data scientists, data product managers, etc.

Because this is a dynamic market with new demands from emerging use cases, vendor capabilities will vary and gaps will be common, making identifying and prioritizing use cases even more essential. Overall, the market demonstrates multiple gaps including the level of stewardship support, cohesive experience across multiple modules catering to different use cases and policy types, value tracking, and custom integrations often requiring external consultants. However, the market direction is promising and gradually working toward filling those gaps, primarily due to increased focus on D&A governance programs due to AI ambitions.

However, the biggest prerequisite for ensuring ROI from such platform investment is the maturity of the D&A governance operating model. The platform only scales and streamlines existing governance decision making and workflows. Yes, it can recommend governance gaps to be filled, but largely the modeling of workflows and people assigned to own the workflows should be mature and engaged enough to interact with the capabilities provided by the platform. The biggest faltering point of such investments are often when governance platforms are frontloaded in designing a D&A governance program (see How to Design an Effective Data and Analytics Governance Operating Model).

The operating model of D&A governance is also evolving with time, particularly with AI being the most dominant focus for different governance practices, including data governance. The siloed operations of governance mechanisms (e.g., legal, security and compliance, privacy, record retention, AI risk) are beginning to coalesce or at least be forced to collaborate more to ensure AI governance.

This means that D&A governance platform selection will bring in additional stakeholders’ considerations to ensure complementarity or fulfillment of others’ priorities. The vendors in this market are also responding to this need by building partnerships or native capabilities in disciplines beyond their traditional market (see Market Overview).

Market Overview

Organizations often use a variety of specialized, stand-alone solutions for D&A governance, such as data security, privacy, quality, and retention. This leads to overlapping capabilities, higher costs, and integration challenges without added business value. Data management itself is evolving, with new approaches like active metadata, data fabric, and data mesh helping connect data silos and automate governance execution through machine learning and semantic models. Similarly, business applications such as ERP and CRM/CDP are also evolving their capabilities that overlap with governance platform capabilities. This has led to significant confusion, exacerbated by lack of common language across different stakeholders to align siloed governance and data management operations.

Scaled AI adoption has put tremendous pressure on D&A leaders to automate and streamline governance. Unfortunately, vendor hype and messaging has added to the pressure and created more confusion. Many vendors in the data management space claim they can “automate governance.” These claims are hyperbolic. At best, they can automate specific tasks such as entity discovery and remediation. The Leaders must adapt to new platforms aligned to their emerging use cases. Vendors respond in different ways: Some integrate or acquire solutions, while others remain niche, leading to ongoing market changes.

Two major issues persist: unclear use cases and requirements between vendors and users, and a lack of user-friendly stewardship solutions for business roles that are increasingly getting diversified. Different departments use governance tools differently, but business involvement is crucial for success, even if D&A governance is being implemented over ERP or over the data warehouse or ABI platform. There’s growing demand for unified governance platforms that manage policy setting, execution, and enforcement, with trust models improving data quality and transparency.

Overall, the data and analytics governance platform market is still developing, with many players and evolving capabilities as noted in the next section.

Innovation

Significant movements in the market have impacted the positioning of vendors. Evolving foundational capabilities and the changing nature of D&A governance that create demands for new capabilities play a significant role in these movements. While last year’s trends of AI-driven automation, commodification, and convergence continue, they’ve been put in high gear due to AI-driven innovation, including AI agents.

The top trends for this market (discussed below) are:

- Unstructured data governance

- Horizontal market consolidation

- Overlap with adjacent metadata and data management markets

- Consumerization 2.0

- Trust models

- Agentic governance enforcement

- AI governance

Unstructured Data Governance

Traditionally, D&A governance platforms have focused on structured and, to some extent, semistructured data. However, demands for AI-ready data have pushed vendors to quickly ramp up their capabilities to govern unstructured data. This is reflected in the way they’ve built connectors for unstructured data sources, tracking lineage, parsing, classification and chunking capabilities, and vectorizing capabilities. The pace at which vendors have been able to incorporate unstructured data governance has been one of the key differentiators.

Horizontal Market Consolidation

Narrower governance capabilities targeting specific personas (CISO, risk, legal), policies (security, privacy) or data type(s) (master data, unstructured data) are increasingly being incorporated as native platform capabilities through development, acquisitions or tighter ecosystem partnerships. This is primarily driven by the end-user’s interest in collapsing a siloed governance operating model into one, leveraging a single technology platform to model and enforce different types of policy, primarily to aid AI governance.

Overlap With Adjacent Metadata and Data Management Markets

Besides the consolidation of governance solutions, there is also a broader trend of convergence in data management platforms (see Future of Data Management Markets: Converged Data Management Platforms Drive Tool Consolidation). While this consolidation includes multiple data management technology verticals, one of the scenarios of consolidation of capabilities is of metadata management and data governance tools (for both policy management and execution). Most vendors evaluated in this Magic Quadrant are also in metadata management solutions. However, governance is only one of the use cases for metadata application. The focus areas of metadata management vendors vary across different use cases that span both data management and data governance, but the challenge for that segment is that the actual use case and use roles are totally different.

Several considerations distinguish a data management-oriented metadata management vendor and a governance-oriented metadata management vendor, including persona focus (governance support is more for nontechnical personas), extensibility (governance solution needing to span multiple data management systems as opposed to solely a single environment), policy management focus (as opposed to policy execution focus). Both types of vendors are doing parts of “managing metadata,” but they are not both doing “metadata management” in the same way. Additionally, D&A leaders should be aware of the emerging data management platforms market category and avoid investing in duplicated technology capabilities. The Market Guide for Data Management Platforms shows several vendors operate in both the D&A governance platforms and data management platforms market categories.

Consumerization 2.0

Last year, the platforms extended their marketplace capabilities to reposition its basic data catalog to insights catalog that casual users can intuitively interact with to search for data products and insights. The platforms have further enriched and expanded these capabilities, including agentic product creation from the platform for product owners, development environment for developers, and, most importantly, connectivity to business applications’ AI agents. The commodification aspect (primarily for AI agents) has brought the business applications and D&A governance market closer, leading to two significant acquisitions of governance vendors by established business applications players — Salesforce of Informatica, and ServiceNow of data.world.

Trust Models