Magic Quadrant for Decision Intelligence Platforms

26 January 2026 - ID G00827619 - 60 min read

By David Pidsley, Carlie Idoine, and 3 more

Decision intelligence platforms (DIPs) combine decision modeling, analytics, and AI to augment and automate decision making and drive business outcomes. Leaders responsible for decision intelligence can use these insights to invest in DIPs and boost their organization’s decision-centricity.

Strategic Planning Assumptions

By 2027, 25% of ungoverned decisions using large language models (LLMs) will cause financial or reputational loss due to human biases, insufficient critical thinking, and AI sycophancy.

By 2027, 50% of business decisions will have been augmented or automated by AI agents for decision intelligence.

By 2028, 25% of CDAO vision statements will become “decision-centric,” surpassing “data-driven” slogans, with human decision-making behaviors explicitly addressed to improve D&A value.

By 2030, explicitly modeled business decisions will be five times more trusted and 80% faster than ungoverned decisions, enabled by decision intelligence platform adoption.

Market Definition/Description

Gartner defines decision intelligence platforms (DIPs) as software to create decision-centric solutions that support, augment and automate decision making of humans or machines, powered by the composition of data, analytics, knowledge and AI. DIPs enable enterprises to collaboratively design and explicitly model decisions, orchestrate decision flow during execution at scale, and enable monitoring and governance of decision quality, while learning from actions and outcomes. Features can include a combination of rule- and logic-based techniques, machine learning, real-time event stream processing, business intelligence, multimodal data and analytics preparation, natural language, graph technology, optimization, simulation or AI agents for decision intelligence.

DIPs provide a solution to enhance how organizations make decisions, whether by humans or machines, individually or collectively. They address the growing challenge of making timely and accurate decisions in volatile, uncertain, complex and ambiguous ecosystems, for more demanding customers in disruptive, competitive and regulated markets. DIPs help by creating executable decision models that improve decision service composition and all-source intelligence to achieve better situational awareness, better recommendations or autonomous actions, tailored to specific decisions and outcomes. They can reduce the risk of poor decisions, allow organizations to anticipate change and respond more swiftly to opportunities at scale.

DIPs help an organization achieve the following outcomes:

- Improved decision making — With the ability to model decisions and orchestrate decision flows, DIPs make the decision making life cycle structured and transparent, and decision services more adaptive based on learning from their environment, leading to better outcomes.

- Increased efficiency — Augmenting and automating decision making at scale saves time and resources, utilizing prescriptive analytics so teams can focus on more strategic tasks.

- Enhanced collaboration — Collaborative decision modeling and execution help ensure interdependent and diverse perspectives are considered, leading to more comprehensive and trusted decisions.

- Better governance and accountability — The ability to explain, evaluate, govern and audit decisions ensures organizations can learn from past actions and continuously improve trust, safety and compliance with regulations.

DIPs offer a coherent, contextual, connected, compliant, cost-optimized, collaborative, and continuous approach to high-quality decision making in today’s complex world. By optimizing the use of data, AI and other technology, they drive decision quality and better business outcomes.

Mandatory Features

The mandatory features for this market are:

- Decision modeling — The capability to design explainable decision models from composite AI using a visual, low-code, decision-centric user interface to frame decisions with defined inputs, flow and outputs. It includes blueprints and decision network modeling to capture life cycle context, connectivity and continuity.

- Decision collaboration — The capability to improve human-AI delegation, minimizing friction between human and machine decision actors within teams, enterprises and ecosystems. It generates decision workflows, ethics and outcomes safeguards, guardrails and alerting thresholds for input/output monitoring and risk mitigation.

- Decision service composition — The capability to componentize decision flows and encapsulate tasks using modular, reusable components as decision services packaged for discovery. It includes integrating enterprise and partner system architectures and data ecosystems with an integration framework and programmatic access for composability.

- Decision execution — The capability to orchestrate and execute decision flows. It includes end-to-end decision life cycle management across development, testing and production environments, and various deployment options to ensure the reliable, scalable and efficient batch and real-time operations of decision services.

- Decision monitoring — The capability to view each decision, its model, logic, decision metadata and insight into the decision flow. It includes suggestions and alerts to implement safe and beneficial adaptations across the decision life cycle, involving humans in the loop as appropriate for learning and improving impact.

- Decision governance — The capability to apply governance principles to DI by logging, auditing and advancing decision making with an accountability framework for secure, safe, ethical, transparent, repeatable, outcome-led decisions; includes governing decisions as assets (model, logic, metadata): stewardship, policies and metrics.

Optional Features

The optionalfeatures for this market are:

- Rule- and logic-based techniques — The capability to capture organizational know-how, policies, procedures, standards, regulations and explicit knowledge as structured rules. Techniques include formal directives and expert heuristics or derivation from machine learning or optimization, controlled by analysts to ensure coherence.

- Machine learning techniques — The capability to extract insight and predict outcomes from high-dimensional datasets using statistical, computational and AI models that learn patterns and relationships. Techniques include supervised, semisupervised, unsupervised and reinforcement learning.

- Real-time event stream techniques — The capability to ingest data from streams with low latency for fast analytics and integration. Techniques include complex event detection and alerting to trigger or inform adaptive and continuous intelligence.

- Business intelligence techniques — The capability to model, analyze and visualize data via dashboards, reports and visualizations to support informed decision making. Techniques include empowering users to uncover patterns, predict trends, improve operations and collaborate on findings.

- Multimodal D&A prep techniques — The capability to unlock value from the spectrum of wide data in any format, language or image, sourced internally or externally. It deconstructs meaningful features of human-generated information for machines. It composes machine-generated data into context-enriched analysis for decisions.

- Natural language techniques — The capability to enable intuitive human-system communication by handling language aspects (pragmatic, semantic, grammatical, lexical). Techniques include generative AI and language processing methods to extract rules or policies, and parse, interpret and generate language, translations and summaries.

- Graph and knowledge techniques — The capability to represent and analyze highly connected data, such as relationships between entities, network nodes or data objects. Techniques include graph data management, ontologies and semantic networks, knowledge graphs, graph analytics or causal graphs.

- Optimization/simulation techniques — The capability to maximize benefits and manage trade-offs by finding optimal resource combinations under constraints via operations research. Techniques include linear, constraint, integer programming, evolutionary algorithms, what-if analysis or scenario planning to simulate environments and outcomes.

- AI agents for DI techniques — The capability to use agentic AI to improve speed, quality and adaptability of decision making. It includes AI agents’ (semi)autonomous role in decision modeling and composition, supporting, augmenting or automating decision service composition and execution, collaboration, monitoring and governance.

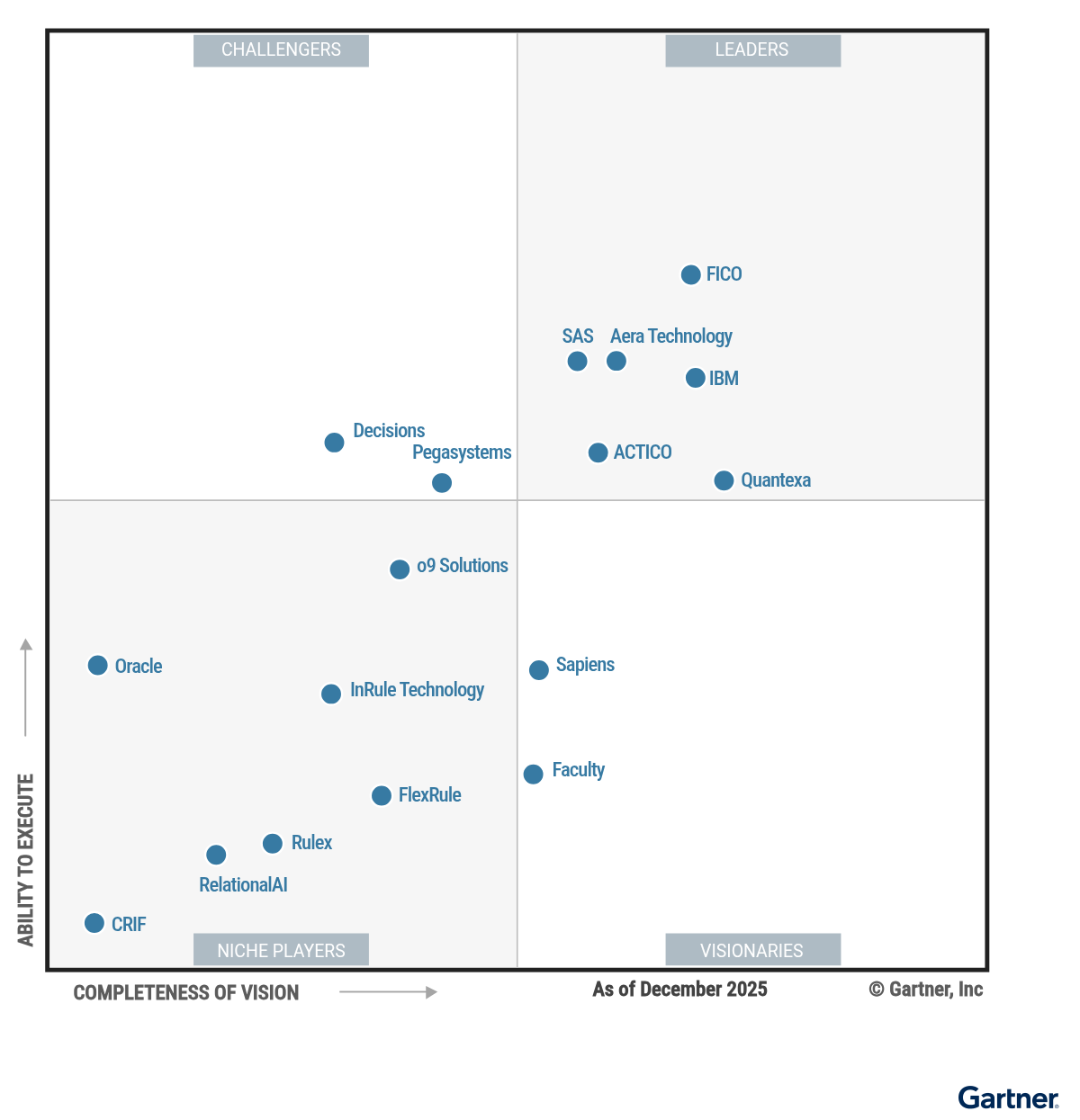

Magic Quadrant

Vendor Strengths and Cautions

ACTICO

ACTICO is a Leader in this Magic Quadrant. It is a private company founded in 2015, headquartered in Friedrichshafen, Germany. Its operations focus on EMEA, serving large organizations in banking and investment services, and insurance. ACTICO was acquired by Keensight Capital in March 2025. Its Decision Platform delivers decision automation, enabling systems to act autonomously, with human oversight only when needed. In 2026, ACTICO plans to launch GenAI-driven decision optimizations, an AI agent for financial data standardization, and explainable AI automation with governance for regulated industries.

- Market Responsiveness/Record: ACTICO demonstrates rapid delivery of new versions and enhancements, supporting alignment with evolving requirements. Consistent execution of roadmap commitments, reinforced by mechanisms for monitoring customer needs and inclusion of mandatory features, provides buyers with confidence in timely product evolution.

- Sales Strategy: ACTICO has differentiated sales approaches for diverse buyer personas, enabling easier engagement across IT and business stakeholders. A broad partner network and combined direct and channel models, supported by dedicated sales resources, help address multiple use cases and enterprise segments.

- Overall Viability: ACTICO’s strong profitability and sustained R&D investment reduce risk for long-term adoption. Consistent revenue growth, an industry-leading customer base, and continued innovation reinforce its strategic commitment to the platform.

- Customer Experience: ACTICO faces challenges in delivering a consistently positive experience, as some clients report low satisfaction with platform capabilities and delivery compared with other vendors. Limited evidence of business value through ROI metrics or case studies may make it harder for buyers to justify investment.

- Marketing Strategy: ACTICO’s lower marketing spend compared with competitors may limit brand visibility and customer engagement. Its misalignment with expected market evolution over the next two to five years creates uncertainty for long-term positioning.

- Marketing Execution: ACTICO’s limited visibility across external search metrics and low presence in Gartner-related inquiries and search may hinder brand awareness. Minimal evidence of innovative marketing methods, such as community engagement or event participation, raises concerns about its ability to influence market perception in an AI-first search era.

Aera Technology

Aera Technology is a Leader in this Magic Quadrant. Founded in 2017, this private company is headquartered in Mountain View, California, U.S., with operations primarily in North America and EMEA. It serves large organizations in manufacturing and natural resources, and oil and gas, typically in supply chain and operations teams. Aera has raised $263 million in funding. Aera Decision Cloud delivers audited decision automation, enabling systems to act while humans review later. In 2026, Aera plans innovations including autonomous agent teams that self-assemble for decisions, learning and governance agents to optimize policies and enforce compliance, and multidimensional simulation integrated with agentic AI.

- Sales Execution/Pricing: Aera Technology’s flexible pricing and contract terms, combined with proofs of concept (PoCs) and trials, support value realization during presales. Larger deal sizes, longer contract durations, and growing customer adoption across regions reinforce strong commercial execution.

- Market Understanding: Aera Technology shows strong vision and a differentiated roadmap, positioning it well for first-time or replacement buyers. Deep awareness of enterprise needs and competitive dynamics reinforces its ability to anticipate evolving client requirements.

- Marketing Strategy: Aera Technology has clear, consistent messaging on long-term market direction, which strengthens buyer confidence. Significant marketing investment, focus on large enterprises, and ability to quantify business benefits reinforce its strong go-to-market execution.

- Overall Viability: With heavy platform investments, Aera Technology’s lack of profitability to date and average revenue growth may raise concerns about long-term financial stability. Its concentration of customers in manufacturing and natural resources, and oil and gas, combined with fewer customers across other industries than vendors in this market, shows a narrower growth profile. Gartner inquiries indicate some supply chain leaders struggle with managing Decision Cloud platform costs, which prospective buyers should verify.

- Geographic Strategy: Aera Technology shows limited regional focus, with below-average presales investment and a minimal presence in South America and APAC (Australia). Reliance on global partners in North America and EMEA, rather than region-specific ecosystems, may restrict its ability to scale geographic coverage effectively.

- Innovation: Aera Technology’s September 2024 to 2025 feature releases show limited differentiation, offering broadly available capabilities that further strengthen its platform rather than new and distinctive advantages. Prospective buyers should verify measurable outcomes, live reference customers, and roadmap maturity, particularly for agentic decision modeling and learning features, to avoid hype risk.

CRIF

CRIF is a Niche Player in this Magic Quadrant. Founded in 1988, this private company is headquartered in Bologna, Italy, with operations primarily in EMEA. It serves large and midsize organizations in banking and investment services, and insurance. Its StrategyOne platform delivers approved decision augmentation, where systems act but require explicit human approval. CRIF’s vision includes natural language agents that generate complete decision processes, business intelligence chatbots for conversational insights and what-if analysis, and optimization chatbots that enable governed, no-code changes to decision strategies.

- Market Responsiveness/Record: CRIF demonstrates timely delivery of roadmap commitments through targeted updates, including real-time variable storage, audit trails, and optimized decision tables. These enhancements support mandatory features critical to the decision life cycle.

- Business Model: CRIF plans to transition from custom delivery to composable, ready-to-use solutions with AI agents, GenAI, and multicloud deployment. This evolution, supported by a strong roadmap, reflects its commitment to future enterprise needs.

- Overall Viability: CRIF’s financial stability, strong companywide revenue, and growing StrategyOne footprint reduce risk for long-term adoption. A sizable enterprise customer base in EMEA reinforces confidence in continued support and market presence.

- Marketing Execution: CRIF’s limited brand recognition and weak visibility for StrategyOne make it difficult for prospects to find targeted information, including through AI-driven search. Only a small proportion of CRIF customers have adopted StrategyOne as direct users, and low engagement indicators such as poor search metrics, minimal Gartner inquiries, and lack of participation in influential forums suggest the vendor is not effectively using modern marketing methods to build awareness or trust.

- Offering (Product) Strategy: CRIF’s low R&D investment limits innovation and leaves major gaps in decision execution, monitoring, and foundational capabilities needed for the decision life cycle. Weak support for advanced techniques like graph and knowledge models, AI agents, multimodal data preparation, real-time streaming, and natural language forces customers to rely on external tools, reducing differentiation across use cases.

- Sales Strategy: CRIF’s small pool of dedicated sales resources, limited partner network, and underdeveloped channel strategy make it difficult to engage diverse enterprise personas and combined IT-business buyers. The absence of robust indirect channels and partnerships means prospects must build the business case and drive adoption internally, reducing momentum across complex organizations.

Decisions

Decisions is a Challenger in this Magic Quadrant. Founded in 2010, this private company is headquartered in Virginia Beach, Virginia, U.S., with customers primarily in North America. It serves midsize and large organizations in healthcare, banking and investment services, insurance, and manufacturing and natural resources. Decisions has raised $50 million in funding. It merged with ProcessMaker in November 2025. Its platform delivers audited decision automation, where systems act and humans routinely review later. In 2026, Decisions plans to introduce tools that enhance developer and expert collaboration, improve visibility into live environments for safer updates, and allow customers to build custom AI agents with strong security and auditing controls.

- Overall Viability: Decisions demonstrates financial stability with consistent revenue growth and strong profitability. Significant R&D investment and a strategic focus on its Decisions platform reinforce long-term commitment and market competitiveness.

- Business Model: Decisions’ platform shows strong alignment between the vendor’s core business and this market. This signals long-term stability, continued investment, and strategic platform focus.

- Sales Strategy: Decisions tailors its sales approach to diverse IT and business buyer personas, emphasizing decision automation as a core value proposition. A robust channel strategy, extensive partner network, and dedicated DIP-focused sales resources enable broad market reach and large-scale implementations.

- Customer Experience: Short tenure among customer-facing staff in sales, customer service, R&D, and IT, combined with limited demonstrable ROI evidence or measurable business outcomes in case studies compared with peers, may reduce buyer confidence in the vendor’s ability to sustain long-term relationships. Decisions shows less flexibility than competitors in contract negotiations with limited detail on core clauses.

- Marketing Strategy: Decisions’ marketing messaging lacks clarity and forward-looking differentiation, making it difficult for prospects to understand how its approach stands apart in this emerging market. The strategy appears reactive with limited evidence of unique positioning or innovation, which may undermine buyer confidence in its long-term vision.

- Market Understanding: Decisions lacks clear competitive differentiators and a strong vision for evolving priorities such as decision automation and advanced AI capabilities. Its roadmap emphasizes a low-code automation platform with incremental infrastructure improvements and aligns more with adjacent market competitors than with shaping future decision intelligence needs, which may limit its ability to lead in this market.

Faculty

Faculty is a Visionary in this Magic Quadrant. Founded in 2014, this private company is based in London, U.K., with operations primarily in EMEA. Faculty serves midsize and large organizations in government and healthcare. It has raised $53 million in funding. In January 2026, Accenture announced its intention to acquire Faculty. Its Frontier platform delivers approved decision augmentation, where systems act but require explicit human approval. In 2026, Faculty plans to introduce a “Return-on-Decision” framework to automatically track the business impact of each decision made on Frontier, and tools that make it easier for customers to build and deploy decision solutions quickly without reliance on forward-deployed engineering efforts.

- Sales Execution/Pricing: Faculty attracts new customers through presales support and commercial flexibility to reduce adoption risk. Its predictable, scalable pricing model with subscription, modular domains, and outcome-linked options, combined with negotiation agility and multiyear commitments, provides competitive terms and a clear path for expansion across functions and geographies.

- Market Understanding: Faculty combines a visionary roadmap with strong awareness of customer needs and competitive dynamics. It differentiates through computational twins and anticipates future requirements for AI safety, human-AI collaboration, prescriptive analytics, and scenario planning. This approach positions its Frontier platform to influence market evolution and deliver transformative decision making at scale.

- Vertical/Industry Strategy: Faculty maintains its focus on targeted sectors, particularly life sciences. Its ecosystem of partnerships with hyperscalers, healthcare platforms, and global system integrators extends reach, streamlines integration, and embeds its platform into critical industry workflows.

- Product or Service: Faculty’s Frontier platform has limited depth and quality of critical capabilities expected in this market. Low adoption within its own customer base and gaps in decision analysis, decision engineering, and decision science use cases, along with missing capabilities for real-time streaming, multimodal data preparation, and traditional knowledge graph techniques, raise concerns about its ability to deliver a comprehensive and competitive platform.

- Geographic Strategy: Faculty lacks a clear and consistent regional focus, with limited presales investment and minimal emphasis on region-specific partnerships or ecosystems. Organizations operating outside EMEA should validate the availability of localized resources and partner networks to avoid gaps in deployment and ongoing support.

- Market Responsiveness/Record: Frontier’s mechanisms for monitoring and responding to customer needs include customer advisory boards, usage analytics, and continuous deployment practices, but appear weak and inconsistently applied, with limited measurable impact on platform evolution. The quality of mandatory DIP feature releases last year remain underwhelming, raising questions about its ability to sustain innovation and meet evolving customer expectations.

FICO

FICO is a Leader in this Magic Quadrant. Founded in 1956, this public company is headquartered in Bozeman, Montana, U.S., with customers primarily in North America and EMEA. It serves large and midsize B2C organizations in banking and investment services. Its FICO Platform delivers autonomous decision automation, where systems act without human review unless needed. In 2026, FICO plans to introduce dynamic profiling to maintain a real-time digital twin of decision data, decision agents that can self-test and monitor performance against business goals, and a marketplace that makes it easier for customers and partners to create and share decision-centric solutions.

- Overall Viability: FICO demonstrates strong financial health through consistent profitability, significant revenue, and sustained growth. Substantial R&D investment relative to platform revenue and proven customer retention across industries reinforce its long-term commitment and market leadership.

- Business Model: FICO operates a well-defined, forward-looking business model that emphasizes ecosystem growth through a platform-led strategy and strategic partnerships. Its strong financial foundation, supported by consistent profitability and substantial growth funding, reinforces long-term stability and the ability to invest in innovation.

- Innovation: FICO delivers advanced real-time decisioning and simulation capabilities supported by a foundation model that enables domain-specific GenAI and AI automation for regulated environments. Its patented technologies for explainability, bias mitigation, and AI agent-based architectures reinforce leadership in trustworthy, autonomous decision intelligence.

- Sales Execution/Strategy: FICO’s consumption-based pricing model can become complex as usage scales across dimensions such as transactions, storage, and add-on features. Buyers should carefully model projected consumption and contract terms to avoid unexpected cost variability and ensure predictability for budgeting.

- Market Understanding: FICO’s broad view of its competitive landscape compares its platform to adjacent technologies rather than focusing on DIPs. It competes in new and existing client deals with credit scoring, fraud and crime prevention, optimization engines and CRM solutions. By serving adjacent needs, it is misaligned with some DIP critical capabilities that its customers frequently use and expect greater knowledge and awareness of.

- Vertical/Industry Strategy: FICO’s approach remains heavily concentrated in banking and credit risk, with other industries addressed mainly through contract frameworks and partner-led solutions rather than differentiated platform capabilities. Organizations outside banking should validate whether upcoming roadmap extensions, such as enterprise fraud and customer management, deliver the innovation and independence they require.

FlexRule

FlexRule is a Niche Player in this Magic Quadrant. Founded in 2016, this private company is headquartered in Melbourne, Australia, with customers primarily in North America and EMEA. It serves large and midsize organizations across multiple sectors. FlexRule Open delivers audited decision automation, where systems act and humans routinely review later. In 2026, FlexRule plans to introduce tools to manage all decision-related assets under strong governance, a familiar spreadsheet-style interface for training and building decision models, and extensions that improve collaboration between humans and AI agents for complex, evolving decision contexts.

- Market Responsiveness/Record: FlexRule demonstrates strong agility by consistently delivering new capabilities ahead of many competitors, enabling faster adoption and innovation for customers. Its Open platform maintains high release quality with patented support for stateful, context-aware decision flows and full DMN Level 3 conformance.

- Market Understanding: FlexRule combines a strong vision with a forward-looking roadmap that helps organizations transition from BI to DI. Its decision-centric approach, grounded in low-code principles and open standards, enables adaptive, participatory models while minimizing lock-in risk. Deep market awareness of competitive positioning in new and replacement scenarios further supports its ability to anticipate trends and guide customers toward future-ready operating models.

- Offering (Product) Strategy: FlexRule’s Open platform emphasizes decision-centric design with robust rule and logic modeling to enable precise, adaptable decision flows. Its API-first architecture and strong decision service composition support operationalization, integration, and governance across diverse environments, accommodating code-first, low-code, and no-code approaches for flexibility and scalability.

- Overall Viability: Despite operating for a decade, FlexRule remains small in scale with fewer than 30 employees, limited functional depth, and few dedicated R&D staff. Low revenue, few customers, and reliance on organic growth in overseas markets without external funding are possible concerns about its ability to accelerate growth and sustain long-term investment.

- Vertical/Industry Strategy: FlexRule’s broad vertical approach, limited ecosystem partnerships, and incremental roadmap progress in vertical/industry sectors may reduce alignment and long-term fit for organizations with specialized requirements. Sparse evidence of measurable outcomes and generally low satisfaction further create uncertainty around reliability.

- Sales Execution/Pricing: FlexRule’s pricing structure and sales approach may limit flexibility for organizations seeking scalable adoption. Short contract durations, smaller deal sizes, and constrained negotiation options require careful evaluation to avoid cost misalignment and long-term value constraints.

IBM

IBM is a Leader in this Magic Quadrant. Founded in 1911, this public company is headquartered in Armonk, New York, U.S., with globally diversified operations. It serves large and midsize organizations in banking, insurance, communications, and more. IBM Decision Intelligence platform, Cloud Pak for Data, and Cloud Pak for Business Automation deliver audited decision automation, where systems act and humans routinely review later. In 2026, IBM plans to add tools that measure the business impact of decisions, integrate advanced optimization for complex planning, and introduce an agentic assistant that enables decision creation, management, and updates.

- Market Responsiveness/Record: IBM demonstrates strong agility by delivering platform capabilities ahead of market trends, including natural-language-driven decision automation, agentic integration, and advanced simulation tools that accelerate adoption and reduce time to value. Consistent execution of roadmap commitments and feature releases, such as composite AI support, GenAI-assisted modeling, and enhanced decision governance, reflects a clear focus on responsiveness to evolving customer needs.

- Market Understanding: IBM demonstrates a strong strategic vision supported by a robust roadmap and deep awareness of competitive dynamics, enabling organizations to plan confidently for complex, long-term workflows. IBM’s experience in agent orchestration and clear differentiation of the DIP market from adjacent analytics and data science segments positions it to guide customers toward future-ready decision intelligence strategies.

- Geographic Strategy: IBM leverages a well-developed global ecosystem of major system integrators and specialized regional partners to provide localized expertise and compliance support. Continued investment in regional presales resources ensures tailored engagement and smoother deployments across diverse markets.

- Sales Execution/Pricing: IBM’s pricing flexibility and sales engagement may pose challenges for organizations with complex buying teams. Limited negotiation options and slower customer acquisition across regions suggest prospective buyers should verify alignment with budget and scalability needs.

- Business Model: IBM’s limited emphasis on this market within its broader business priorities may constrain long-term investment and innovation. This creates uncertainty for organizations seeking sustained advancement in decision intelligence capabilities.

- Vertical/Industry Strategy: IBM’s recent enhancements focus on broad platform upgrades rather than deeply tailored solutions for specific industries. This may limit differentiation for organizations seeking strong vertical alignment and industry-specific capabilities.

InRule Technology

InRule Technology is a Niche Player in this Magic Quadrant. Founded in 2002, this private company is headquartered in Chicago, Illinois, U.S., with operations primarily in North America and EMEA. It serves organizations of all sizes across government, banking and investment services, healthcare, insurance, manufacturing and natural resources, and retail. The InRule Decision Platform delivers autonomous decision automation, where systems act without human review unless needed. In 2026, InRule plans to offer a unified platform that combines rules, process automation, machine learning, and AI; launch a marketplace for prebuilt integrations and accelerators; and extend its composite AI approach with explainability reports to meet regulatory requirements.

- Sales Execution/Pricing: InRule combines transparent, decision-execution-based pricing with flexible SaaS and on-premises deployment options to align costs with usage and support scalability. Strong presales engagement through PoCs and trials, along with bundled training and professional services, helps organizations validate ROI early and reduce implementation risk.

- Marketing Strategy: InRule targets large and midsize enterprises through a focused go-to-market approach, supported by significant investment in marketing channels and compelling customer success stories. Highlighting decision governance and measurable outcomes such as cost savings, efficiency gains, and improved engagement helps InRule communicate differentiated value and build credibility with prospective buyers.

- Sales Strategy: InRule employs a focused sales approach with dedicated resources aligned to both IT and business buyer needs across DIP use cases. Its strong direct sales model, supported by a specialized team and partner ecosystem, targets regulated, high-volume enterprises and CIO-led buying committees to deliver compliance, agility, and a tailored buying experience.

- Market Responsiveness/Record: InRule’s mechanisms for monitoring and responding to customer needs appear limited, and roadmap commitments are not consistently met. Feature launches and early releases demonstrate activity, but they don’t clearly establish sustained responsiveness or early market leadership.

- Business Model: Although InRule positions its Decision Platform as central to unified decision intelligence with AI and governance, its approach shows limited evolution and heavy reliance on this single market. With this narrow focus, as market dynamics shift, lack of planned business model evolution may constrain its adaptability and growth. Private ownership by a single equity firm will likely influence its strategic priorities.

- Vertical/Industry Strategy: Although InRule references industry-specific accelerators and templates, its Decision Platform has limited scope, primarily generic components and a few starter projects. This fragmented approach and lack of a well-defined roadmap may limit its ability to deliver differentiated value for complex or highly regulated sectors.

o9 Solutions

o9 Solutions is a Niche Player in this Magic Quadrant. Founded in 2009, this private company is headquartered in Dallas, Texas, U.S., with operations primarily in North America and EMEA. It serves large and midsize organizations in retail, manufacturing and natural resources, and communications, media and services, typically in supply chain functions. o9 Solutions has raised $411 million in funding. Its o9 Digital Brain platform delivers autonomous decision automation, where systems act without human review unless needed. In 2026, o9 Solutions plans to enable faster decision synchronization across functions, automate high-volume processes for “touchless” execution, introduce AI agents trained on knowledge graphs to assist managers, and provide tools for post-decision analysis to explain performance and improve outcomes.

- Customer Experience: o9 Solutions ensures reliability and operational stability through robust technical support and clearly defined SLAs. Its ability to drive measurable business value, including improved forecasting accuracy, cost reduction, and enhanced supply chain performance, demonstrates commitment to helping organizations achieve transformative results.

- Geographic Strategy: o9 Solutions supports global operations through a network of regional partnerships and ecosystems, complemented by significant investment in presales resources across major regions. Its clear regional focus and localized expertise enable smooth implementations and alignment for organizations operating internationally, while maintaining strong coverage in North America and EMEA.

- Marketing Strategy: o9 Solutions demonstrates a strong go-to-market approach focused on enterprise engagement, supported by significant investment in marketing channels. This strategy, combined with sustained growth and above-average R&D investment, positions it as a stable and innovative provider committed to long-term product evolution.

- Product or Service: The o9 Digital Brain platform has significant improvement opportunities across critical capabilities for decision analysis, execution, and collaboration. Organizations with advanced requirements for integrated workflows, governance, and human-AI collaboration may face operational challenges and require additional configuration or third-party elements to achieve outcomes they would expect of any DIP.

- Business Model: o9 Solutions’ stated plans emphasize product and feature innovation like agentic AI, “decision replay,” and its APEX Digital Operating Model, but offer limited clarity on its broader business model evolution. This may create some uncertainty about how quickly innovations translate into measurable customer outcomes and vendor roadmap as market dynamics shift.

- Sales Execution/Pricing: o9 Solutions’ limited traction in acquiring new customers across regions beyond the supply chain domain and weak presales engagement, including PoCs and trials, may slow validation and onboarding for prospective clients. Pricing often requires proactive negotiation and careful expectation management to avoid misalignment with budget and scope.

Oracle

Oracle is a Niche Player in this Magic Quadrant. Founded in 1977, this public company is headquartered in Redwood Shores, California, U.S., with globally diversified operations. It serves large organizations across industries. Its entry into the DIP market is Oracle Cloud Infrastructure (OCI), which includes Integration and Analytics Cloud to deliver decision recommendations, where systems suggest actions and humans choose whether to use them. This evaluation excludes AI Data Platform (released October 2025), Fusion Analytics, and other application-layer analytics. In 2026, Oracle plans to help customers create AI-driven decision models with governance, enable agentic AI systems that automate processes end to end, and support decision-centric agents with its Autonomous AI Lakehouse architecture.

- Overall Viability: Oracle is a financially robust organization with consistent investment in research and development, providing it a reliable foundation for its solution portfolio. Solid year-over-year growth and a broad customer base reinforce stability, though limited visibility into market-specific revenue, customer growth, and R&D allocation may require prospective buyers to verify platform-specific commitments.

- Geographic Strategy: Oracle demonstrates strong global engagement through service provider partnerships and regional alignment through cloud infrastructure partnerships for regions, supported by presales investment across major markets. This approach with large system integrators provides localized expertise and resources, enabling smooth deployments and compliance for globally distributed organizations.

- Marketing Execution: Oracle achieves strong market visibility through initiatives like global events and strategic partnerships. High-profile research on decision making and technology reinforces its ability to deliver clear messaging while highlighting measurable business impact.

- Sales Execution/Pricing: Oracle’s limited negotiation flexibility and pricing transparency in this market may make cost predictability challenging, particularly given modest deal sizes and mixed perceptions of overall competitiveness. Its presales engagement, including PoCs and trials, is relatively constrained, which can slow validation and onboarding for prospective customers.

- Business Model: While Oracle’s business model is mature and stable, the DIP market segment represents a very small portion of it. Its current messaging and narrative don’t demonstrate sufficient market focus, clarity, and consistency that signal a longer-term perspective for DIP customer needs. Customers should seek explicit commitments around investment, roadmap clarity, and measurable outcomes before making decisions.

- Innovation: Oracle’s innovation efforts appear fragmented. Its initiatives broadly tie to automation and AI, and aren’t purpose-built for decision intelligence capabilities. Limited differentiation within the DIP market and reliance on adjacent technologies may create uncertainty for buyers about whether Oracle’s roadmap will deliver sustained, differentiated advancements in this market.

Pegasystems

Pegasystems is a Challenger in this Magic Quadrant. Founded in 1983, this public company is headquartered in Waltham, Massachusetts, U.S., with operations primarily in North America and EMEA. It serves large organizations in banking and investment services, insurance, communications, media and services, retail, and healthcare. Its Pega Infinity Platform delivers autonomous decision automation, where systems act without human review unless needed. In 2026, Pegasystems plans to introduce AI agents that monitor model health and recommend strategy improvements, tools that give partners faster ways to package and deliver solutions, and real-time insights to help clients optimize decisions and improve engagement outcomes.

- Marketing Execution: Pegasystems demonstrates strong visibility through leading web search performance, high engagement in Gartner inquiries and searches, and use of social media, industry forums, and multimedia campaigns. Its event-driven engagement and strong brand recognition reinforce market influence and accessibility for prospective buyers.

- Marketing Strategy: Pegasystems’ messaging emphasizes its large enterprise customers’ success in achieving business goals like revenue growth, improved retention, and efficiency gains, as well as its own success through consistent execution that results in strong financial performance and sustaining R&D investment.

- Vertical/Industry Strategy: Pegasystems demonstrates a clear commitment to industry-specific innovation through a roadmap that introduces agentic AI automation, real-time intelligence, and hyperpersonalization tailored to its target verticals. Its strong ecosystem of strategic partnerships and verticalized data models for the Pega Infinity Platform enables repeatable, industry-focused solutions that accelerate transformation and deliver measurable business outcomes.

- Market Responsiveness/Record: Customer feedback indicates that Pegasystems’ responsiveness to evolving decision intelligence demands has been inconsistent, with limited evidence of timely roadmap execution and mechanisms to adapt. Being overindexed on CRM and CX use cases, combined with a lack of aggressive pursuit of first-time or migrating DIP customers, creates uncertainty about Pegasystems’ ability to maintain competitive momentum in the evolving DIP market.

- Offering (Product) Strategy: Low investment in mandatory features across the decision life cycle may slow innovation and limit critical capability enhancements in Pegasystems’ platform. Gaps in decision-centric UI and decision services, along with limitations in graph analytics, business intelligence, and decision governance, constrain decision observability and adaptability.

- Business Model: As market dynamics shift, limited business model evolution and slight misalignment between the market and Pegasystems’ operating model may restrict its ability to adapt for DIP use cases.

Quantexa

Quantexa is a Leader in this Magic Quadrant. Founded in 2016, this private company is headquartered in London, U.K., with operations in EMEA, North America, and APAC. It serves midsize and large organizations in banking and investment services, government, insurance, and communications, media and services. Quantexa has raised $400 million in primary funding, including $114 million in March 2025. The Quantexa Decision Intelligence Platform primarily provides advisory decision support and recommendations for human approval. In 2026, Quantexa plans to launch a unified AI layer for contextual insights, strengthen its trusted data foundation with its real-world context layer, expand its Q Assist natural-language interface, and simplify deployment through cloud and marketplace solutions for faster time to value.

- Sales Execution/Pricing: Quantexa is gaining significant net new customers globally by offering scalable pricing options that align with diverse engagement and automation needs through value-based and consumption-based models. Its structured presales support, combined with strong negotiation flexibility and multiyear contracts, ensures predictable costs and alignment with business objectives.

- Vertical/Industry Strategy: Quantexa demonstrates strong industry alignment through a clear vertical roadmap, deep partnerships, and tailored capabilities. These investments enable organizations in regulated sectors to accelerate time to value and operationalize decision intelligence at scale.

- Market Understanding: Quantexa demonstrates a strong strategic vision for DI that enables organizations to move from analytics to actionable outcomes that improve transparency and scalability. Its market awareness and competitive differentiators position it well to capture greenfield opportunities and displace incumbents as demand accelerates.

- Customer Experience: Customer reference survey feedback indicates inconsistent satisfaction with critical capabilities, placing the Quantexa Decision Intelligence Platform among lower-scoring vendors for overall customer experience and delivery. Shorter employee tenure in customer-facing and technical roles, combined with indirect or estimated ROI claims in case studies and product gaps in decision automation, optimization and simulation capabilities, may impact continuity, support quality, and time to value.

- Marketing Strategy: Quantexa’s product marketing does not consistently convey differentiated value and often misaligns with the enterprise persona of its customer base, making it difficult for prospects to judge fit from promotional materials. Relatively low channel investment compared to peers may require prospects to rely on direct engagement to validate capabilities and ensure alignment with organizational priorities.

- Marketing Execution: In social media follower counts, Quantexa holds a midtier position in the DIP market and minimal Gartner analyst inquiry engagement from Quantexa’s prospects and clients may reduce third-party validation and market influence. Prospective buyers may find it challenging to access independent perspectives compared with competitors that maintain deeper market-specific relationships.

RelationalAI

RelationalAI is a Niche Player in this Magic Quadrant. Founded in 2017, this private company is headquartered in Berkeley, California, U.S., with operations primarily in North America and EMEA. It serves large organizations, often Snowflake Data Cloud customers, in banking and investment services, communications, media and services, and retail. RelationalAI has raised $145 million in funding, including $22.5 million from Snowflake Ventures and AT&T Ventures, as announced in December 2025. Its Decision Intelligence Platform delivers approved decision augmentation, where systems act but require explicit human approval. In 2026, RelationalAI plans to offer cost-efficient fine-tuning of open-source LLMs, an AI assistant that accelerates decision modeling using relational knowledge graphs, and an analyst-friendly interface to visualize data and semantics together.

- Customer Experience: RelationalAI shows strong commitment to customer success through reliable technical support backed by contractual SLAs, ensuring predictable performance and responsiveness. Its flexibility in contract negotiations and experienced product support teams helps it build long-term relationships and consistent delivery.

- Innovation: RelationalAI demonstrates strong innovation by integrating relational knowledge graphs, neurosymbolic reasoning, and data cloud capabilities, enabling organizations to open and unify data and analytics for scalable, cost-effective decision intelligence adoption.

- Business Model: RelationalAI’s business model is anchored by its Decision Intelligence Platform and “Rel” decision agent, which is central to it delivering differentiated value in the decision intelligence platform market. Significant funding and a strategic partnership with Snowflake reinforce its ability to scale and innovate effectively.

- Product or Service: RelationalAI’s platform lacks many foundational decision intelligence capabilities, including decision modeling, collaboration, governance, and monitoring. Its code-only approach and features gaps across the decision life cycle may limit suitability for organizations seeking a complete, enterprise-ready solution.

- Vertical/Industry Strategy: RelationalAI shows no evidence of vertical-specific investment, with no roadmap, partnerships, or templates to support vertical or industry requirements. This absence may limit suitability for organizations seeking domain-focused solutions or prebuilt decision blueprints.

- Sales Strategy: RelationalAI has a small dedicated sales team, a limited partner network, and an underdeveloped channel approach. Its sales strategy shows minimal differentiation for buyer personas and use cases, which may reduce its ability to extend market reach and align with diverse enterprise requirements.

Rulex

Rulex is a Niche Player in this Magic Quadrant. Founded in 2007, this private company is headquartered in Genoa, Italy, with operations primarily in EMEA and North America. It serves large organizations in manufacturing, banking and investment services, and wholesale trade. Rulex has raised $2.2 million in funding. Its Rulex Platform delivers reversible decision augmentation, where systems act unless a human rejects the decision afterward. In 2026, Rulex plans to make its cloud services automatically adjust computing resources to handle changing workloads, improve data inspection and audit during decision flow execution, and deliver reusable interface templates that accelerate the creation of decision-centric applications.

- Sales Execution/Pricing: Rulex provides strong presales support through PoC engagements and 30-day trials, reducing evaluation risk for buyers. Flexible pricing models and contract terms, combined with clear value for money, support adoption across multiple geographies.

- Vertical/Industry Strategy: Rulex delivers industry-tailored solutions through a roadmap focused on vertical-specific enhancements and a strong partner ecosystem for domain expertise. Its partner-led growth model, including alliances and certification programs, accelerates implementation and expands delivery capacity for faster time to value.

- Customer Experience: Rulex consistently delivers strong customer outcomes, supported by high satisfaction ratings and responsive support teams. Its flexibility in engagement and commitment to long-term relationships help ensure confidence throughout the decision intelligence journey.

- Marketing Execution: Rulex’s limited brand visibility and weak use of digital channels may hinder market influence and buyer engagement. Low search metrics and minimal analyst presence create uncertainty for prospects seeking accessible information.

- Innovation: Rulex’s recent innovation efforts have focused on adding features such as a proprietary optimization solver and a decision-centric UI, but these have not significantly differentiated its platform from competitors and lack patents. Its roadmap, aimed primarily at usability and closing capability gaps (rather than driving breakthrough advancements), may slow progress toward meeting emerging decision intelligence requirements.

- Marketing Strategy: Rulex’s marketing approach lacks clarity and consistency. Its limited channel investment and messaging relies heavily on technical language rather than clearly articulating differentiated value or practical outcomes. These factors may make it harder for buyers to assess the vendor’s long-term vision and scalability.

Sapiens

Sapiens is a Visionary in this Magic Quadrant. Founded in 1982, this private company is headquartered in London, U.K., with customers of its Sapien Decision platform primarily in North America. It serves large organizations in banking and investment services, and insurance. Sapiens was acquired by Advent in December 2025. Its Decision platform delivers autonomous decision automation, where systems act without human review unless needed. In 2026, Sapiens plans to introduce tools that let businesses customize and manage AI-driven decision workflows, add features to monitor decisions against KPIs and recommend improvements, and enhance its modeling capabilities with interactive, GenAI-powered tools that make building and updating decision models faster and easier.

- Market Responsiveness/Record: Sapiens demonstrates strong agility in addressing evolving market needs by rapidly delivering GenAI-driven decision modeling and advanced visualization features. Its ability to translate customer feedback into high-quality enhancements within weeks helps clients stay ahead of industry trends.

- Innovation: Sapiens demonstrates strong innovation with GenAI capabilities that convert natural language requirements into decision models and merge machine learning outputs with business rules for transparency and control. Its roadmap emphasizes adaptive workflows, KPI-driven optimization, and interactive modeling, enabling faster time to market and enterprisewide accessibility for decision automation.

- Vertical/Industry Strategy: Sapiens demonstrates strong industry alignment through a clear vertical roadmap delivering tailored innovations for sectors such as mortgage and insurance. Specialized accelerators and deep ecosystem partnerships enable speed, flexibility, and measurable business impact for decision intelligence initiatives.

- Overall Viability: Sapiens’ Decision platform-specific annual revenue and year-over-year growth are comparatively low, and it doesn’t show market leadership in customer numbers. Its R&D financial investment in its Decision platform is comparatively low. This raises concerns about its ability to scale resources and maintain competitive momentum in this market, which could affect long-term support and ecosystem strength for its Decision platform.

- Sales Strategy: Sapiens’ reliance on a selective direct sales model with a small team may limit accessibility for organizations outside its high-value criteria. A narrow channel strategy and limited partner network could constrain market reach and flexibility for new prospects.

- Geographic Strategy: Sapiens’ Decision platform’s geographic strategy remains heavily concentrated in North America, which may limit localization and responsiveness for regional needs. Global delivery often depends on extending North American resources rather than dedicated local investments.

SAS

SAS is a Leader in this Magic Quadrant. Founded in 1976, this private company is headquartered in Cary, North Carolina, U.S., with globally diversified operations. It serves large and midsize organizations in banking and investment services, insurance, healthcare, and government. SAS Viya delivers reversible decision augmentation, where systems act unless a human rejects the decision afterward. In 2026, SAS plans to expand its focus on trust and transparency to make AI-powered decisions more explainable, auditable, and reliable, with a model governance framework, industry-specific AI agents, and enhanced simulation, monitoring, analytics, and compliance features, for responsible and regulated AI deployment.

- Overall Viability: SAS demonstrates strong financial health and sustained growth, supported by strong profitability and industry-leading revenue performance. Continued investment in R&D and consistent year-over-year expansion reinforce confidence in its ability to innovate and support SAS Viya for the long term.

- Geographic Strategy: SAS maintains an extensive global footprint enabled by a mature partner ecosystem and region-specific enablement programs. Its multilingual product support, regional compliance certifications, and flexible cloud deployment models allow its customers to operate Viya in accordance with local regulatory, data sovereignty, and operational requirements.

- Vertical/Industry Strategy: SAS demonstrates a strong and sustained commitment to industry alignment, with experience in sectors such as financial services, healthcare, and manufacturing. Its roadmap delivers deep vertical capabilities through prebuilt AI models, compliance-ready workflows, and dedicated AI agents for high-value use cases such as fraud detection, anti-money laundering, and supply chain optimization, supported by an extensive ecosystem of strategic partnerships and alliances that accelerate time to value and reduce implementation risks.

- Sales Execution/Pricing: SAS offers trials and flexible deployment options, but its pricing and contract negotiation practices remain less flexible compared to competitors. Organizations seeking customized enterprisewide pricing may require earlier alignment with SAS sales teams to ensure cost predictability and transparency.

- Business Model: SAS’s broad analytics and AI strategy reflects only moderate prioritization of decision intelligence, framing diverse analytics insights and outputs as “decisions” and offering freemium DI capabilities. This approach may create uncertainty about its future roadmap, investment focus, and how DI fits into SAS’s business model. When evaluating Viya, discuss long-term DI roadmap alignment.

- Innovation: Although SAS Viya describes progress and ambition, key DI capabilities such as GenAI-driven decision modeling, agentic AI frameworks, and enhanced governance are still maturing, remain in development, or are not broadly available. Reliance on proprietary approaches may introduce integration complexity and require significant organizational readiness or incremental adoption to realize intended benefits.

Inclusion and Exclusion Criteria

This Magic Quadrant research uses the same inclusion criteria as its companion Critical Capabilities for Decision Intelligence Platforms. To qualify for inclusion in this research, vendors had to meet the following criteria:

- General Availability: Product(s) evaluated should be generally available on 1 September 2025. General availability (GA) is defined as something a vendor’s clients have in a production environment, rather than something they are testing or evaluating. GA doesn’t make any assertions about quality, rather that the product is generally available for sale/use and is fully supported. Betas with limited distribution (e.g., invite only, limited user numbers) or finite duration (e.g., expiry date for use) are not generally available.

- Market Definition: The product(s) must meet the Market Definition defined above.

- Cross-Industry: The customer base for production deployment of the product since 1 January 2024 through 31 December 2024 must include paying customers for the product(s) in at least three of the following industries: Banking and Investment Services; Communications, Media and Services; Education; Government; Healthcare; Insurance; Manufacturing and Natural Resources; Oil and Gas; Power and Utilities; Retail; Transportation; and Wholesale Trade. See Note 1: Vertical Industries.

- Customer Interest: Vendor ranks among the Top 21 for the Customer Interest Indicator (CII) as defined by Gartner. CII was calculated using a weighted mix of internal and external inputs that reflect Gartner client interest, vendor customer engagement, and vendor customer sentiment between 1 January 2024 and 31 July 2025.

Honorable Mentions

This market is larger than only the vendors included in this Magic Quadrant, so there are many platforms that may be of relevance to readers. We encourage Gartner clients to use our Toolkit: Decision Intelligence Platform Feature Checklist and make inquiries with the authors to discuss these and other notable vendors, not all of which are included in the following list.

- Corridor Platforms: Notable for AI in regulated financial services with strong governance and explainability. This year, it did not meet our customer interest and cross-industry inclusion criteria.

- Cloverpop: Its DIP focuses on human+AI collaboration and serves as a decision “system of record” for structured decision workflows. This year, it did not meet our customer interest inclusion criterion.

- Frontline Systems: Analytic Solver (widely used in Excel) and RASON cloud platform for optimization, simulation, machine learning and rules. This year, it did not meet our customer interest criterion.

- Microsoft: Microsoft Fabric includes Real-Time Intelligence, Fabric IQ, ontology, graph, digital twins, and autonomous AI operations agents. It integrates Power Automate, Foundry, Purview, Copilot Studio and Teams. This year, it did not meet our market definition inclusion criterion.

- OpenRules: Long-standing open-source vendor appealing to organizations seeking standards-based, flexible rule-based decisioning. This year, it did not meet our customer interest inclusion criterion.

- Palantir: Foundry offers custom-built decision intelligence solutions for complex, custom-made enterprise requirements. This year, it did not meet our market definition inclusion criterion.

- Rainbird: For repeatable, deterministic AI in high-volume, policy-driven, compliance-heavy workflows requiring logic-based defensibility and auditability. This year, it did not meet our customer interest inclusion criterion.

- Sparkling Logic: SMARTS platform combines business rules, decision analytics, dynamic questionnaires, AI, and ModelOps for agile decision automation. This year, it did not meet our customer interest inclusion criterion.

- Trisotech: Digital Enterprise Suite aligns with DIP standards and orchestrates business decisions with processes and cases. This year, it did not meet our customer interest inclusion criterion.

- XpertRule Software: Delivers a domain-specific DIP for decision automation across manufacturing, healthcare, and financial services. This year, it did not meet our customer interest inclusion criterion.

Evaluation Criteria

Ability to Execute

The Ability to Execute criteria used in this Magic Quadrant are as follows.

Product/Service: The capabilities, features, and overall quality of the core goods and services that compete in and or serve the defined market. Our evaluation focused on: (1) Critical Capabilities for Decision Intelligence Platforms score; (2) overall rating of delivery and execution with the vendor; and (3) proportion of unique customers receiving the entire portfolio of products.

Overall Viability: The organization’s overall financial health, as well as the financial and practical success of the relevant business unit. This includes the likelihood that the organization can continue to offer and invest in the product, as well as the product’s position in the organization’s portfolio. Our evaluation focused on: (1) annual revenue; (2) year-over-year growth; (3) market-specific customer growth and retention; (4) resource growth and utilization; and (5) R&D investment.

Sales Execution/Pricing: The organization’s capabilities in all presales activities and the structures that support these activities. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel. Our evaluation focused on: (1) presales support; (2) deal size; (3) average contract duration measured in months/years; (4) number of net new customers across geography; (5) analyst perception of pricing/value for money spent (from contract reviews, customer survey, social media, and inquiries when possible); (6) pricing model/pricing and contract flexibility; and (7) typical implementation times.

Market Responsiveness and Track Record: The ability to respond, change direction, be flexible, and achieve competitive success as opportunities develop, competitors act, customer needs evolve, and market dynamics change. This includes the provider’s history of responsiveness to changing market demands. Our evaluation focused on: (1) quality of product releases/updates; (2) number of product releases/updates per year; (3) time to market for new product versions and enhancements (with examples) as measured by idea to beta testing and then beta testing to general availability; (4) mechanisms for monitoring and responding to customer needs; and (5) analyst perception of roadmap promises being met.

Marketing Execution: The ability to deliver clear, high-quality, creative, and effective messaging via publicity, promotional activity, thought leadership, social media, referrals, and sales activities. This includes the organization’s ability to influence the market, promote the brand, increase awareness of products and establish a positive reputation among customers. Our evaluation focused on: (1) market visibility, such as innovative marketing methods to engage user communities, participation in events, etc.; (2) brand name recognition/customers’ familiarity with product or vendor; (3) ease of finding specific/targeted market-related information on the vendor’s website and other sources; (4) external search metrics (e.g., Google); (5) effective utilization of brand channels, social media, web, industry analysts forums, TV/radio commercials, online blogs/video, community forums, academic institutions, and peer networks; and (6) Gartner presence (client inquiry volume, search analytics).

Customer Experience: The degree to which a vendor’s products, services, and programs enable customers to achieve their desired results. This includes the quality of supplier/buyer interactions, technical support or account support, as well as ancillary tools, customer support programs, availability of user groups, and service-level agreements. Our evaluation focused on: (1) overall satisfaction with the provider’s capabilities and delivery; (2) quality of technical support; (3) flexibility and adaptability in negotiating final contracts; (4) the extent that the software developed by the vendor achieved the benefits expected; and (5) customer and employee retention.

* Not Rated for this Magic Quadrant — Operations: This criterion, which typically evaluates the ability of the organization to meet its goals and commitments, the quality of its organizational structure, skills, experiences, programs, and systems that enable the organization to operate effectively and efficiently, was not included in this inaugural Magic Quadrant for this market, as the operations of product, sales, marketing, and customer service team were instead evaluated within their respective criteria.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | High |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | High |

Marketing Execution | High |

Customer Experience | Medium |

Operations | NotRated |

Source: Gartner (January 2026)

Completeness of Vision

The Completeness of Vision criteria used in this Magic Quadrant are as follows.

Market Understanding: The ability to understand customer needs and translate that understanding into products and services. Vendors with a clear vision of the market listen to and understand customer demands, and they can shape or enhance market changes with their vision. Our evaluation focused on: (1) vision and strategic focus; (2) competitive differentiators and awareness; and (3) market knowledge.

Marketing Strategy: The ability to clearly communicate differentiated messaging, both internally and externally, through social media, advertising, customer programs, and positioning statements. Our evaluation focused on: (1) market visibility; (2) go-to-market approach; (3) messaging and narrative clarity and consistency; (4) channel investment; and (5) customer service and product support process quality.

Sales Strategy: The ability to create a sound strategy for selling that uses the appropriate networks, including direct and indirect sales, marketing, service, and communication. This includes partnerships that extend the scope and depth of a provider’s market reach, expertise, technologies, services, and customer base. Our evaluation focused on: (1) differing sales strategies for target customer profiles/personas; (2) dedicated sales resources size and positioning; (3) channel strategy; and (4) partner network size.

Offering (Product) Strategy: The ability to approach product development and delivery in a way that meets current and future requirements, with an emphasis on market differentiation, functionality, methodology and features. Our evaluation focused on: (1) support for new delivery models and usage of market-specific tools; (2) product portfolio breadth and depth; and (3) investment levels in critical capabilities.

Business Model: The design, logic, and execution of the organization’s business proposition. Our evaluation focused on: (1) significance and alignment of Magic Quadrant market to overall business; (2) venture capital (VC) or market cap funding / to annual revenue; and (3) business model evolution.

Vertical/Industry Strategy: The ability to strategically direct resources (sales, product, development), skills, and products to meet the specific needs of verticals and market segments. Our evaluation focused on: (1) clear and consistent vertical focus; (2) vertical/industry-specific product roadmap; and (3) vertical/industry-specific partnerships/ecosystem.

Innovation: Marshaling of resources, expertise, or capital for competitive advantage, investment, consolidation, or defense against acquisition. Our evaluation focused on: (1) use of newer technologies including automation, smart machines, etc.; (2) clear indications of the vendor’s future outlook toward innovation (product or business model innovation); and (3) number of market-specific patents and trademarks.

Geographic Strategy: The ability to direct resources, skills, and offerings to meet the specific needs of regions outside the provider’s home region, either directly or through partners, channels, and subsidiaries. Our evaluation focused on: (1) region-specific presales investment; (2) region-specific partnerships/ecosystem; and (3) clear and consistent region focus.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Medium |

Sales Strategy | Medium |

Offering (Product) Strategy | High |

Business Model | Low |

Vertical/Industry Strategy | Medium |

Innovation | High |

Geographic Strategy | Low |

Source: Gartner (January 2026)

Sources of information that informed Gartner’s evaluation of vendors by these criteria are in the Evidence section.

Quadrant Descriptions

Leaders

Leaders combine strong execution with a clear, forward-looking vision for decision-centric architectures. They deliver comprehensive capabilities across the decision life cycle — modeling, orchestration, monitoring, and governance — while integrating advanced AI techniques such as generative AI and agentic AI. Leaders typically offer composable architectures, low-code/no-code interfaces, and robust governance frameworks that meet regulatory and enterprise requirements. They demonstrate consistent roadmap delivery, strong financial viability, and the ability to scale across industries and geographies. Leaders also invest heavily in innovation, embedding optimization, simulation, and explainability to support trusted automation at scale.

Challengers

Challengers excel in execution and often have a strong installed base or proven success in adjacent markets such as business rule engines or workflow automation. They typically offer reliable, mature platforms with solid decision modeling and execution capabilities but may lag in innovation or differentiation compared to Leaders. Many Challengers focus on incremental enhancements rather than transformative features like agentic AI or advanced simulation. Their vision for decision intelligence may be less comprehensive, with limited emphasis on emerging trends such as autonomous agents or multimodal decision flows. While they provide stability and predictable delivery, customers should validate long-term roadmap commitments to ensure alignment with evolving decision-centric strategies.

Visionaries

Visionaries demonstrate a strong understanding of where the market is heading and often lead with innovative concepts such as agentic AI, GenAI-driven modeling, and decision-centric orchestration. They prioritize advanced capabilities like simulation, optimization, and contextual decision flows, aiming to redefine how enterprises embed decision intelligence. However, Visionaries may lack the scale, maturity, or breadth of capabilities needed for enterprisewide adoption today. Their offerings often appeal to organizations seeking cutting-edge features and early adoption of emerging technologies; however, customers should assess execution risk and ensure these innovations translate into measurable business outcomes.

Niche Players

Niche Players typically focus on specific industries, regions, or decision types, offering specialized capabilities or lightweight platforms that address targeted use cases. They may provide strong rule-based modeling or domain-specific templates but often lack depth in advanced AI techniques, composable architectures, or global scalability. Many Niche Players are evolving from traditional decision management suites or business rule engines, extending their offerings to include decision intelligence features. While they can deliver value for organizations with narrow requirements or regulated environments, customers should evaluate their ability to support broader decision-centric strategies and long-term innovation.

Context

Decision intelligence platforms (DIPs) have shifted from niche adoption to a late-stage emerging market, becoming a strategic enabler for organizations of any size, geography, and industry seeking agility, resilience, and measurable business impact. This Magic Quadrant evaluates vendors on their ability to deliver decision-centric architectures that combine explicit decision modeling, AI-driven augmentation and automation, and governance at scale. Demand is accelerating so that being decision-centric will surpass data-driven in the vision statements of leaders responsible for DI, and explicitly modeled decisions will be much more trusted and much faster than ungoverned decisions.

Four trends dominate this market’s evolution:

- Agentic AI and GenAI integration: Vendors are embedding LLM-powered AI agents and GenAI to accelerate decision modeling, automate workflows, and enable adaptive, context-aware execution. Roadmaps emphasize autonomous agents and natural-language-driven modeling. Other techniques like simulation capabilities are on the rise to support proactive decision optimization.

- Governance and trust as differentiators: As decisions become more automated, organizations must enforce auditable guardrails, explainability, and compliance. Vendors investing in decision governance, bias detection, and policy enforcement will lead in regulated and high-risk environments.

- Composable and ecosystem-driven architectures: Platforms are evolving toward API-first, modular designs that integrate with data clouds, analytics, and process automation ecosystems. This supports scalability, low-code extensibility, and industry-specific accelerators for faster time to value.

- Some longer-existing vendors have evolved their DIP offering by combining or extending techniques already supported in their decision management suites or business rule engines, signaling a convergence of legacy decisioning capabilities with modern AI-driven approaches. Packaged suite providers are also adding DIP capabilities within their solution offering.

Leaders responsible for DI should:

- Prioritize governance and explainability: Select platforms with strong decision monitoring, audit trails, and compliance-ready features to mitigate risk and build trust in AI-driven decisions.

- Evaluate agentic AI and GenAI capabilities pragmatically: Insist on measurable outcomes (e.g., cycle-time reduction, KPI lift) and production references before committing to AI agents or natural language modeling.

- Match platform strengths to use cases: Decision analysis favors no-code modeling and monitoring; decision engineers require composable architectures and real-time execution; decision science demands advanced ML and simulation; stewardship needs governance and explainability.

- Plan for scalability and integration: Choose platforms with API-first architectures, low-code extensibility, and hybrid deployment options to future-proof investments.

- Leverage vertical accelerators: For regulated or specialized sectors, prioritize vendors offering domain-specific templates and compliance workflows to reduce implementation risk and accelerate ROI.

Market Overview

The demand for DIPs has never been higher. The adoption of decision intelligence (DI) has grown along with the increasing complexity of decision making. DI is defined as a practical discipline used to improve decision making by understanding and engineering how decisions are made and how outcomes are evaluated, managed, and improved by feedback.

The influx of disruptions, competition, and digital business, and a plethora of regulations has forced decisions and decision making to be more coherent, contextual, connected, compliant, cost-optimized, collaborative, and continuous (see Innovation Insight: Decision Governance Mitigates Risks of Generative AI Agents).

In fact, the 2024 Gartner CDAO Agenda Survey found that of organizations surveyed:

- 33% have already deployed DI.

- 17% committed to have deployed within six months.

- 19% were considering deployment in six to 12 months.

- 25% were investigating doing so in 12 to 24 months.

- Only 7% said they had no interest in deploying it.