Use the Coming GenAI Productivity Revolution to Rethink Your Microsoft Relationship

13 January 2026 - ID G00841877 - 13 min read

By Michael Silver, Joe Mariano, and 2 more

GenAI will spark a new wave of productivity suites from Microsoft, Google, and other vendors. SPVM leaders should seek to exploit a potential market shake-up as they approach their Microsoft contract renewals.

Insights at a Glance

IT SPVM leaders, trying to maintain flexibility and control costs, are frustrated with Microsoft’s changes in pricing, discounting, and contracting. These dynamics are reigniting interest in alternative products and vendors just as the productivity and collaboration suite market begins to undergo a critical change.

Gartner expects that GenAI will change how people work. Combined with customers unhappy with Microsoft’s pricing and contracts and looking for other productivity tools, this will lead to real competition for Microsoft 365 in three stages.

Gartner predicts that GenAI will result in viable competition to Microsoft 365 based on GenAI’s ability to change the way people work, combined with customers looking for alternatives because they are unhappy with Microsoft’s price increases and contracting changes (see Cut the Cost of Microsoft 365 License Renewals - Part 2).

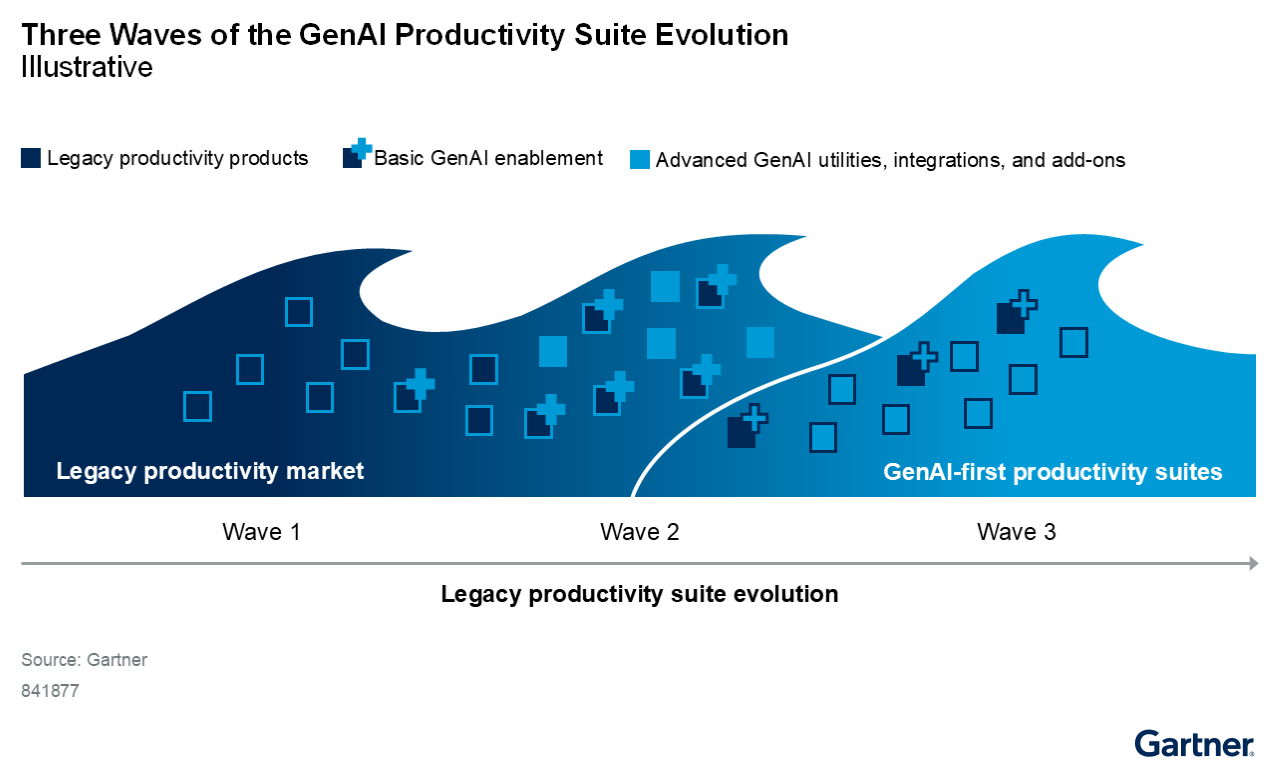

Gartner sees this happening over three waves of evolution:

- Wave 1 (2023 through 2027): GenAI functions are integrated into productivity tools, and users adapt them to their workflows. GenAI is changing the economics of switching from Microsoft to Google Workspace for organizations that want it for all users.

- Wave 2 (2025 through 2029): Multiple vendors release GenAI components designed to replace, accelerate, and optimize work processes.

- Wave 3 (2028 through 2035): These vendors, components, products, and technologies will mature, get acquired, or go defunct, and, longer term, resurface in a new generation of AI-first productivity and collaboration suites. AI-first productivity and collaboration suites will be characterized by a massive redesign, with new user interfaces, content types, and document formats. For Microsoft, this may represent an innovator’s dilemma, where they must decide how to respond to competitive products that strive to offer radically improved interfaces and functions, potentially at the expense of compatibility and familiarity.

Gartner predicts that through 2027, GenAI and agent use will create the first true challenge to Microsoft productivity tools in 30 years, prompting a $58B market shake-up.

IT SPVM leaders should use uncertainty and market upheaval in their negotiations with Microsoft to maintain discounts and flexibility.

Strategic Planning Assumption

Through 2027, GenAI and agent use will create the first true challenge to mainstream productivity tools in 30 years, prompting a $58B market shake-up.

Through 2029, a majority of Microsoft-centric organizations will spend 30% to 50% more on Microsoft software and SaaS every three years without having budgeted for such a significant increase.

Issue Context

Microsoft dominates the productivity market with Microsoft Office and Microsoft 365, owning an estimated 88% share of the enterprise productivity product market.1 Yet, CIOs and their leadership teams cite escalating frustration with rising costs for what many consider a commodity product. Gartner predicts that through 2029, a majority of Microsoft-centric organizations will spend 30% to 50% more on Microsoft software and SaaS every three years without having budgeted for such a significant increase, due to increasing prices, decreasing programmatic and discretionary discounts, and Microsoft’s currency pricing adjustments (see Unlock Negotiated Microsoft Discounts With Strategic Products, Cut the Cost of Microsoft 365 License Renewals — Part 1, and Cut the Cost of Microsoft 365 License Renewals - Part 2).

IT leaders have faced this frustration before, but the ability to create a net positive business case to move from Microsoft 365 to an alternative productivity product has historically been elusive:

- IT leaders have been reluctant to run a mixed environment, which would require user profiling, platform governance, and significant employee enablement and support with interoperability or version control problems, significantly increasing TCO. Limited integration between so-called best-of-breed products also increases digital friction.

- Few organizations are able to migrate every user to a non-Microsoft-Office solution. At least some users will require Excel or Word because of functional or advanced compatibility issues, resulting in a mixed product environment.

- Microsoft’s bundling of the productivity suite with the Windows OS, client access licenses for server workloads, Entra ID for identity management, and its enterprise management and security (EMS) licenses forces the business case to account for more than productivity.

Gartner clients report that they are interested in alternatives but feel locked into Microsoft 365. What will it take for competition to upset the market dynamics? GenAI (and agentic AI) enable new functionality and change the economics of alternative products based on the AI features vendors are including. In the long term, it will create a new, more level playing field for competition and spark a new generation of AI-first productivity suites (see figure 1).

Impact Brief

GenAI’s Impact on the Productivity Suite Market

- Developing new content today increasingly begins with GenAI taking vast amounts of content and synthesizing it in myriad ways, rather than starting with a blank canvas. Editing frequently involves having AI continually rewrite content rather than the author doing it manually.

- A host of providers, including Anthropic, Asana, Canva, ClickUp, Context.AI, Google, Grammarly, Microsoft, Notion, OpenAI, Perplexity, Zoho, and others already offer GenAI services that compete for organizations’ productivity suite budgets. Others, like xAI, believe they can replace the productivity suite and its apps with prompts and agents.

- Gartner predicts that, over time, differentiated AI capabilities included in a raft of new products will become more important to productivity suites than compatibility with legacy documents. As legacy formats and compatibility decline in importance, barriers to entry will decrease, and competition will increase.

- The cost and packaging of GenAI is likely to evolve over time, with providers moving fee-based features into a no- or low-cost tier, potentially making lower-cost products more suitable. More costly, higher-level tiers are also likely to emerge.

How Microsoft’s Contracting Changes Will Impact Organizations’ Productivity Suite and AI Plans

Rising costs associated with Microsoft contract renewals are prompting some organizations to reconsider alternative productivity suites. This is driven by factors such as:

- Decreased discounts at each renewal cycle.

- Price increases for many Microsoft 365 components, notably in March 2022 and July 2026.2

- Elimination of volume discount bands for online products for renewals after 1 November 2025.

Furthermore, to get a desired level of discount, Microsoft customers are often required to buy more than they feel they need and enter multiyear commitments with amendments that eliminate the flexibility to reduce quantities. This limits organizations’ abilities to respond to changing market conditions.

Implications

Background

The harshest critics of Microsoft Office would say that many of its improvements over time have been evolutionary, not revolutionary, and the way most people work in 2025 has not fundamentally changed since Office 4.3 was released in 1994.

But if Microsoft Office were truly a commodity, it would be easy to replace, and it wouldn’t dominate share of the market. For most users, there are and have been suitable replacement products available at a lower or even no cost. However, most organizations that have successfully deployed alternatives have found that some percentage of users, often including the legal and finance departments, need the visual fidelity (the formatting and pagination of the document do not change) or the full capability and compatibility with Microsoft products, including Excel formulas and macros, etc., afforded only by using the Microsoft product.

A little over 20 years ago, open source software, led by Linux and (at the time) Sun’s StarOffice, challenged Microsoft’s desktop dominance. Gartner experts sum up their product strategy as compatible enough and cheaper. But compatible enough was rarely good enough, cheaper didn’t provide sufficient ROI, and in most organizations, they barely made a dent.

About five years later, Google began competing with its Workspace suite and ChromeOS. Google did better by focusing on features that Microsoft lacked, namely the ability to work collaboratively on documents. But compatibility could be problematic, and Microsoft eventually added sufficient collaborative features to keep most of its market share.

Based on the high migration cost, questionable savings, and the added complexity of managing a mixed environment, Gartner advised that to achieve a positive return, organizations considering alternatives must seek to gain a business advantage from the new features by changing the way people work, and not just to save money on the tools.

Saving money has historically not been a sufficient reason to move off Microsoft Office. A major discontinuity in the market that fundamentally changes how people work would be required to challenge Microsoft’s dominance. Generative AI is that discontinuity.

Gartner believes that the biggest problem past competitors had was that they didn’t transform (or even sufficiently change) how people worked. Gartner’s position has long been that Office’s place in the market would not be successfully challenged by products that were compatible enough and cheaper. Rather, a major discontinuity in the market that fundamentally changed how people work would be required. GenAI is that discontinuity.

What’s Changed

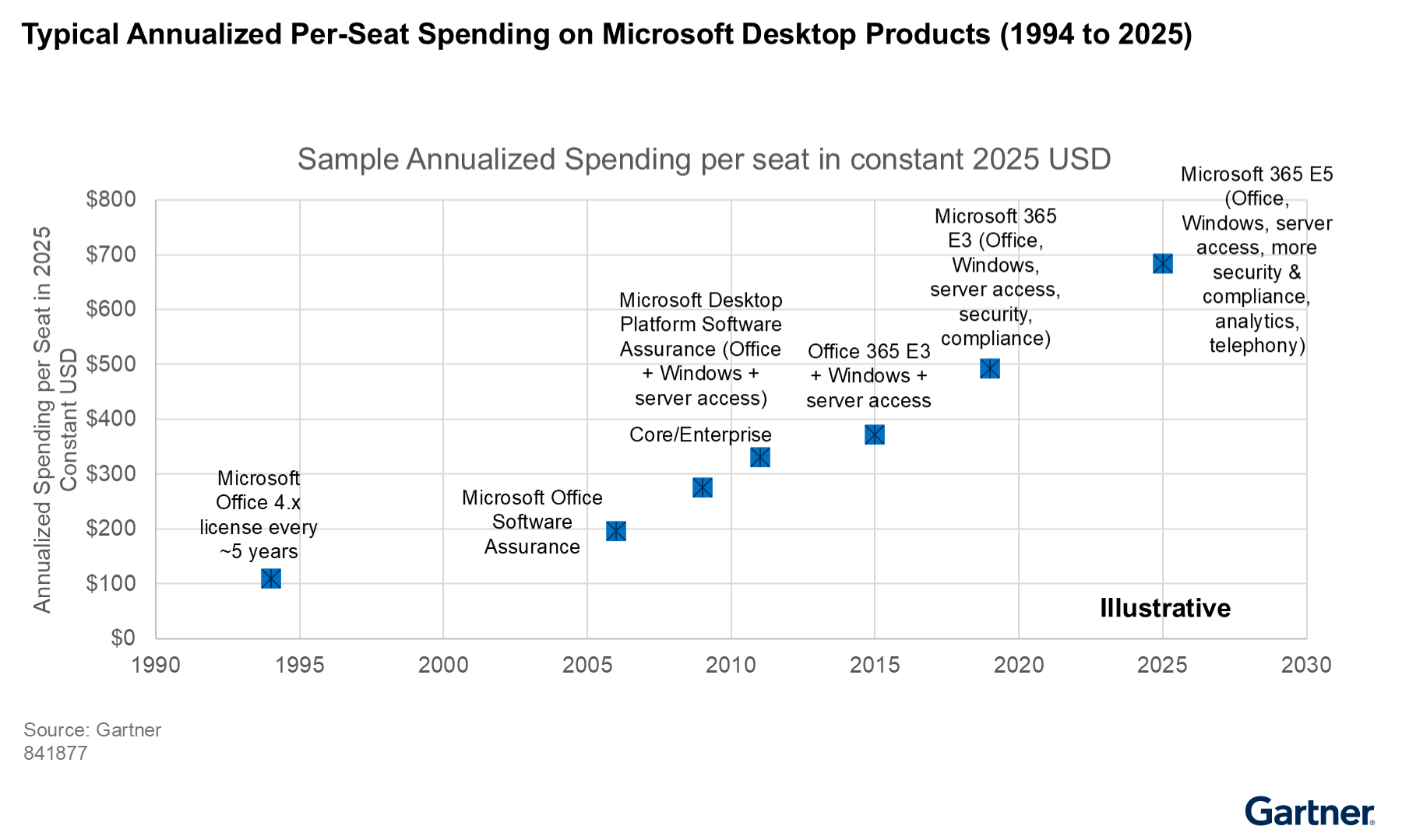

Over the past three decades, Microsoft has systematically transitioned organizations from infrequent perpetual license purchases to ongoing maintenance, to subscription models, such as Office 365 and subsequently Microsoft 365 E3 and E5. This evolution has significantly expanded both organizational reliance on Microsoft products and overall expenditure. While the value has increased as larger bundles with more products were purchased, typical annual spending increased approximately sixfold during this period (see Figure 2), from around $50 per device per year in 1994 ($110 in 2025 constant USD) to almost $700 per user per year in 2025.3 As the cost per seat has increased, even a small percentage rise equates to a significant impact on the budget, necessitating heightened scrutiny during renewal negotiations.

Lately, Gartner experts have seen a resurgence of organizations seeking alternative productivity products as they face increasing renewal costs for Microsoft contracts, often by 30% to 50% every three years and often without a significant increase in features.

There are two main differences that increase the likelihood that alternative productivity products will be more successful than in the past:

- Organizations seeking to provide every user with a fully functional GenAI product are discovering that the economics have shifted, and Google Workspace — which offers Gemini to all users by default — can provide significant savings compared with the additional expense of purchasing Microsoft 365 Copilot for all M365 users. This economic advantage is proving compelling enough for some enterprises to justify and pursue a transition to Google Workspace.

- We are on the precipice of a GenAI revolution in productivity suites, as AI has the potential to enable a total reinvention of those solutions. Cluttered user interfaces full of buttons and menu items are likely to be rendered obsolete. Long, tedious, and error-prone formulas and macros will be created and managed automatically. New document types that include many different types of content, AI agents, and prompts are likely to emerge, along with new formats to efficiently store, manage, and search them.

All of these advances could erode the competitive advantages Microsoft has had with Office.

Of course, Microsoft will likely respond to price competition quickly, resetting the economic equation in No. 1, and Microsoft has already made several adjustments:4

- Microsoft integrated Copilot Chat into Microsoft 365 Apps, a function that previously required a paid M365 subscription.

- Microsoft announced that Copilot for Sales, Copilot for Service, and Copilot for Finance, which had each cost $20 PUPM in addition to Microsoft 365 Enterprise’s $30, will be included at no additional charge starting 1 October 2025.

- Microsoft 365 Copilot’s price will decrease by 40% for education customers, from $30 PUPM to $18 PUPM starting 1 December 2025.

While customers currently paying original prices for these products may be able to get some concession from their Microsoft account teams, programmatically, they will not be able to get any prepaid monies back and will have to remember to true-down the product at their next anniversary. IT SPVM leaders who accepted a nonreduction amendment in exchange for a discount will pay the negotiated price through the expiration of their agreement.

Microsoft faces the difficulty of responding to price competition without upsetting customers who made significant multiyear commitments at higher prices.

The coming GenAI productivity suite revolution will be more complex for both organizations and Microsoft to respond to, as vendors jockey for position with new innovations and identify ways to create new lock-in points to create sustainable competitive advantage. For Microsoft, this represents an innovator’s dilemma: how aggressively will Microsoft compete with AI-first productivity products that have fundamentally different feature sets or monetization models, which could jeopardize Office’s dominance and revenue?

Actions

- Prepare for a new generation of personal productivity suites by facilitating innovation and maintaining governance for employees who want to be adventurous and try new products. Monitor developments and track the evolution of new standards.

- Negotiate discounts and flexibility into Microsoft contracts using market uncertainty as leverage. Shorten commitments if discounts on longer terms are not sufficient to protect you if business conditions decline, divestitures occur, prices or features of GenAI products change, or you decide to switch to other AI products.

Cautions

- Organizations will lose negotiating leverage with Microsoft or other vendors if their real preferences and intentions are disclosed.

- Organizations risk adopting a patchwork of tools that hinders effective collaboration and degrade the digital employee experience.

- Organizations that adopt a product that gets acquired or goes defunct could result in higher costs, the need to change strategy, or difficulty extracting or migrating IP from the tool. Ensure you have methods to move, retain, and secure critical information from defunct platforms.

1 Productivity Suites Revenue Breakout, Worldwide, 2023. Productivity suites revenue breakout: The market revenue of 88% listed represents our estimate of value and usage, not figures reported or provided by the vendors, of both SaaS and legacy on-premises software. They do not include consumer (nonbusiness) revenue.

We divide office suite revenue among the markets in which they are a part to provide useful market sizing and product comparisons. The vendors do not report revenue at a component level. However, an estimated allocation is necessary to report on the total market size for those affected markets, as well as to compare Microsoft’s and Google’s relative strengths against stand-alone players. (Examples are Google Drive versus Dropbox, and Microsoft SharePoint as a content services platform versus OpenText’s content services.)

Revenue breakouts are informed by analysts’ client conversations and, in the case of Microsoft 365, with additional input from a survey of component usage. In the case of Google Workspace, revenue is split between office suites and content collaboration platforms (for the Google Drive component). Revenue for Microsoft Office products and Microsoft 365 is split among six categories based on an assessment of usage.

3 Based on Gartner historical cost and usage tracking during client inquiries.

4 On 10 September 2025, Microsoft announced that Copilot for Sales, Copilot for Service, and Copilot for Finance, which had cost $20 PUPM and required a $30 PUPM M365 Copilot license, would be included in M365 Copilot at no additional charge starting 1 October 2025 Moving sales, service, and finance to the frontier with Microsoft 365 Copilot, Microsoft 365 Blog.

On 15 October 2025, Microsoft announced that starting 1 December 2025, educational institutions would be able to purchase M365 Copilot subscriptions for $18.00 PUPM, a 40% discount from its original cost New AI experiences and academic offering for Microsoft 365 Copilot, Microsoft Education Blog.

In August 2025, Microsoft enabled Copilot Chat in Microsoft 365 Apps, a function which previously required a paid M365 Copilot subscription Copilot in apps for work, Microsoft 365 Copilot.