Magic Quadrant for Customer Journey Analytics & Orchestration

23 March 2026 - ID G00843109 - 44 min read

By Christopher Sladdin, Daniel O'Sullivan, and 1 more

The increasing complexity of customer journeys risks detracting from CX and loyalty, and impacts growth and cost management. Leaders should use this Magic Quadrant to identify best-fit customer journey analytics and orchestration solutions for real-time analysis, prioritization and orchestration.

Market Definition/Description

Gartner defines customer journey analytics and orchestration (CJA/O) as solutions that track and analyze how customers and prospects interact with an organization across multiple channels over time. These solutions subsequently enable organizations to prioritize and orchestrate real-time improvements to the customer experience in multichannel journeys throughout the end-to-end customer life cycle.

The journey lens provided by CJA/O solutions offers insights by combining cross-channel interaction data with transactional, voice of the customer (VoC), and customer profile data on a time axis. Other types of analysis, when used in isolation, cannot achieve this. This enables data-driven predictions at scale and experimentation with multichannel interventions that can be robustly verified as driving increased customer satisfaction, retention, and lifetime value.

CJA/O solutions support three main use cases:

Analysis

- Understanding complex multichannel customer journeys

- Identifying opportunities by analyzing areas where customers get stuck or abandon journeys entirely

- Visualizing common journeys using Sankey diagrams and journey maps

Prioritization

- Using insights to prioritize design/process changes and decisions

- Integrating VoC and other data to correlate action with service priorities and metrics

- Accessing immediate feedback regarding the impact of decisions and process changes

Orchestration

- Designing next best actions to orchestrate customer journeys in real time

- Serving customers with alerts or notifications based on the context, segment or other factors

- Optimizing individual journeys to deliver the best outcome for the customer and the business

While some solutions offer limited customer journey mapping capabilities— where the business outlines the intended/ideal journey through workshops, etc. — they are not the core focus of CJA/O tools. Gartner covers customer journey mapping technologies separately (see Innovation Insight: Customer Journey Mapping Technology).

Mandatory Features

- Gathering data from source systems/channels is the ability to ingest data from different internal systems and multiple channels of engagement (such as a website, chatbot, retail store, live chat, phone, etc.). The ability to ingest data must be source-system-agnostic (for example, data cannot be limited to only digital channels), although vendors may additionally choose to provide dedicated connectors to specific solutions.

- Journey visualization enables organizations to observe customers’ journeys across all channels and touchpoints, both at a macro level (i.e., for a group of customers) and at an individual customer level. This commonly takes the form of a Sankey diagram. These visualizations may require user input or may be generated dynamically.

- Deterministic customer identity matching connects customer records based on specific known identifiers (e.g., a user ID, phone number, etc.). This is required for tracking individual users across multichannel journeys. Vendors may connect to other services in the organization to access identity data.

- Journey prioritization and outcome management capabilities enable users to understand the business and customer impact of journeys and potential improvements, enabling data-driven journey management, and value storytelling.

- Journey orchestration capabilities enable organizations to intervene in a customer’s journey in near real-time. This feature uses rules or predictive analytics and machine learning to identify where to intervene in journeys to optimize customer and/or business outcomes. This could include automating customer-facing actions (such as generating a communication or tailoring website messaging based on their profile data) or internal actions (such as generating an alert).

Optional Features

- Probabilistic customer identity matching is the use of statistical methods to match individual users where reliable identifiers (e.g., a user ID) are not available. Algorithms are used to assign a likely match based on data such as location, device, user behavior and other factors.

- Journey mapping capabilities allow users to expand on current-state journey visualizations or propose future-state journey designs, incorporating additional depth regarding, for example, customer expectations, questions, pain points, opportunities, and associated processes and technologies. These may be designed within the vendor’s solution or via an integration to a third-party journey mapping solution.

- Customer segmentation capabilities allow users to analyze, prioritize, and orchestrate journeys for different groups of customers, with groupings derived from journey insights or broader enterprise data.

- VoC integration enables customer feedback gathered from surveys or other collection methods to be overlaid on top of journey visualizations. This data is used to identify customer expectations and experiences at key journey stages.

- Real-time agent assist capabilities surface customer journey data in real time to service agents, providing actions and recommendations to help them steer customers toward positive outcomes.

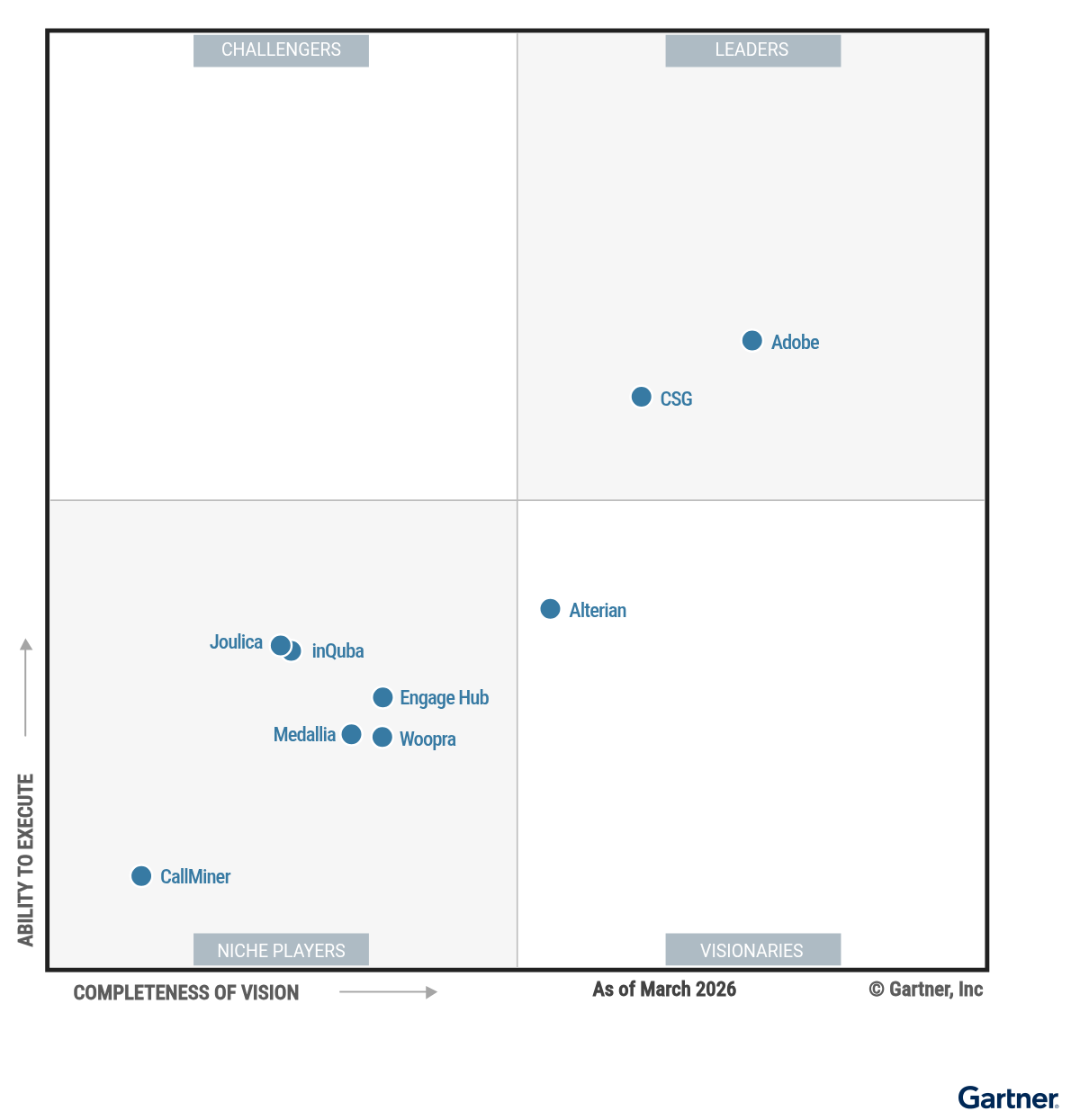

Magic Quadrant

Vendor Strengths and Cautions

Adobe

Adobe is a Leader in this Magic Quadrant due to its strong product capabilities and its role and industry expertise. Its Adobe Customer Journey Analytics and Adobe Journey Optimizer products are best-suited for B2B account management and sales, and B2C-focused marketing campaign management. It has a global reach but is focused in North America and EMEA. Customers tend to be midsize to large enterprises in financial services, retail, healthcare, high-tech, manufacturing, travel and hospitality, and media and entertainment.

Its roadmap focuses on increased agentic- and predictive AI solutions to support nontechnical users and extend orchestration workflows, enhanced loyalty program orchestration, expanded channel support and analytics for journeys in conversational channels.

- Comprehensive product offering: Adobe’s solutions combine analytical strength with deep design-focused owned-channel, paid media and internal orchestration capabilities. The platform also has a strong focus on prioritization and outcome, and ROI management.

- B2B journey management: Adobe recently launched B2B editions of its products to support multistakeholder customer journey analytics and orchestration (CJA/O). It provides comprehensive oversight of multistep buyer journeys, including steps undertaken with resellers or partners, enabling organizations to analyze and orchestrate targeted engagement, not just at the broad account level, but also for specific roles and buying groups.

- Broader platform integration: While Adobe’s products are highly capable as stand-alone solutions, their interoperability with other applications in the Adobe Experience Cloud enhances their capabilities, particularly for customer data management and orchestration.

- Technical proficiency required: Adobe’s configurability and complexity require significant technical skill to use, which increases the need for Adobe or partner-provided professional services.

- Pricing complexity: Gartner clients have called out Adobe’s pricing strategy for a lack of transparency. Its product bundles and associated pricing are perceived as complex, and the potential for future price changes as AI features roll out creates further buyer uncertainty.

- Sales cycle length: Adobe’s complex pricing structures and its comparatively limited support in helping customers evaluate its products result in some of the longest sales cycles, on average, among the vendors in this research. Adobe does not offer free trials or outcome-based contract terms, and proofs of concept to properly evaluate the platform are offered by sales on a case-by-case basis and may require paid services to support.

Alterian

Alterian is a Visionary in this Magic Quadrant due to its focus on innovation and product differentiators. Its Real-Time CX Platform provides company-data-driven CJA/O, while its Journey Insight capabilities enable users to compare their journeys with competitors’ through large third-party datasets. It operates primarily in North America, with partners in EMEA and the Asia/Pacific region. Customers tend to be midsize to large enterprises in the retail, financial services, telecom, utilities, healthcare, travel and service provider industries.

Its roadmap focuses on providing deeper insight into consumer journeys that involve third-party AI platforms, increasing AI assistance in its platform, and several smaller capability and UI refinements.

- Solution-focused market insight: Alterian understands its customers’ challenges and needs, focusing on roles such as marketing and customer experience (CX) strategists. It tailors its messaging and advances solutions that quickly connect to prospects’ and customers’ real concerns.

- Addressing adoption barriers: Alterian’s comparatively low-cost Journey Insight capabilities leverage large third-party datasets to provide brand and competitor journey analysis. Organizations can use this data to design and optimize first-party journeys. This offers an alternative starting point for organizations where access or ability to integrate company-owned data is challenging in the short term.

- Focus on innovation: Alterian spends significantly more of its revenue on R&D than any other vendor, resulting in a suite of valuable product and service improvements, and confidence in the deliverability of its short-term roadmap.

- Engagement reach: Despite Alterian’s strong understanding of its target market, its visibility among target customers and prospects remains somewhat limited. Its investments in marketing and outreach through events, research, campaigns and case studies are modest.

- Regional support: The vast majority of Alterian’s customer base and recent growth are in North America. While the vendor has some resources, partners and data residency options in Europe and the Asia/Pacific region, prospects based outside North America should probe its ability to provide adequate onshore or nearshore capabilities and services.

- Limited direct sales relationships: Alterian has limited investment in a direct sales route to market. It prefers to go to market via partners instead. These partners, including consultancies and other professional services organizations, can help clients interpret and apply customer journey insights to maximize their ROI, but at an additional cost to the client.

CallMiner

CallMiner is a Niche Player in this Magic Quadrant due to its limited CJA/O capabilities and focus. Its main product is a conversation analytics and CX automation solution. CJA/O is provided as part of this solution through two specific product components, Analyze and Outreach. It is best-suited for existing customers, or service functions with a high volume of conversational interactions. It operates primarily in North America and Europe, and is growing in the Asia/Pacific region. Customers tend to be large enterprises, often in banking, financial services and insurance, healthcare, and professional services.

It plans to expand agentic AI from journey discovery to automated analytics and guided actions from an AI assistant. Beyond this, its roadmap for CJA/O is unclear.

CallMiner declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- Ease of access: CallMiner offers enterprise-ready support for the customer service and support and CX functions. Existing or new customers to CallMiner — in particular, their Analyze product — may find that it offers easier-than-usual access to CJA/O capabilities than others, given their availability within the broader conversation analytics solution.

- Regulatory support: CallMiner offers a number of data residency options to meet regional and industry-specific requirements. Additionally, it is certified in or compliant with a range of international regulations.

- Marketing execution: CallMiner effectively promotes the need for journey analytics through a library of articles and FAQs that frame CJA/O within the context of service and support operations. It shows how journey analytics can improve understanding of customer behavior and enhance service CX outcomes.

- Product/service: The vendor has made minimal investments in CJA/O capabilities in recent years, resulting in limited capabilities in a number of key areas for buyers, including journey visualization and analysis, deterministic and probabilistic customer identity matching, and orchestration.

- Market positioning: CallMiner anchors its go-to-market and sales messaging around conversation analytics and CX automation capabilities such as agent coaching, fraud detection and compliance, rather than CJA/O. It offers limited resources, documentation and marketing materials related to CJA/O capabilities, making it difficult for prospects to fully assess its product features and capabilities against those of other vendors in the market.

- Market reach: CallMiner’s CJA/O capabilities are offered only as part of its broader platform. This narrow focus restricts the vendor’s reach largely to customer service and support teams. Although CallMiner has a large potential audience among existing customers, it is not a viable option for most buyers seeking a CJA/O solution.

CSG

CSG is a Leader in this Magic Quadrant due to its strong go-to-market capabilities and market responsiveness. Its CSG Xponent platform is best-suited for marketing teams that need extensive orchestration capabilities and rely on intricate rule-based or AI-driven logic. Its operations are mostly focused in North America, with a small presence in EMEA, and its customers tend to be large enterprises in the financial services, insurance, healthcare, utilities and telecom industries.

Its product roadmap focuses on introducing hybrid AI agent orchestration within deterministic journeys, a digital twin of the customer to support enhanced journey simulation, and AI-assisted journey configuration.

- Market vision: CSG understands the market’s growing need for real-time, intent-aware interventions and governed AI productivity, requiring what it describes as a unified “journey operating system.” It has therefore focused its roadmap on investments in agentic, natural-language journey creation and intelligent omnichannel routing that adapts to customer intent.

- Pre- to postsales support: CSG has streamlined the process for customers to articulate their journey obstacles and aspirations (prepurchase) and subsequently achieve ROI (postpurchase). Its standardized sales and success methodology includes templates for identifying and calculating potential value, and guided implementation support for proving value in five postacquisition journeys before scaling further.

- Pricing balance: CSG offers a strong balance of simplicity and flexibility in its pricing and bundles. It provides predictable pricing through flat, annual SaaS platform fees plus pay-per-use communication fees for outbound orchestration (e.g., per SMS or email sent). It also offers outcome-based pricing for customers that want a stronger commitment to ROI at the expense of some predictability.

- Ongoing acquisition: CSG is currently being acquired by the NEC Group — a significant Japanese IT corporation — which creates some uncertainty for customers and prospects about the longer-term viability of the CSG Xponent platform. There are, as yet, no publicly communicated plans regarding the future of the solution; however, Gartner has noted that some capabilities overlap between CSG’s platform and Netcracker, an existing NEC subsidiary, which could indicate future consolidation.

- Product/service: The platform is either lacking capabilities or is overly reliant on complex workflow configuration to support customer segmentation, prioritization and outcome management, voice of the customer (VoC) integration, and B2B and account-based journey management. This limits its suitability for a number of common CJA/O use cases.

- Regional presence: CSG’s customer base is skewed toward North America, with only a minimal presence in Europe and no presence in other regions. Prospects outside of North America should scrutinize its ability to provide adequate support for their needs.

Engage Hub

Engage Hub is a Niche Player in this Magic Quadrant because of its relatively small footprint and limited resources for scaling its marketing and sales pipeline. Its platform is best-suited for customer service and support or end-to-end CX. Its operations are mostly focused in Europe, with a smaller presence in North America and Latin America, and its customers tend to be midsize to large high-volume and regulated enterprises in financial services, utilities, telecom, the public sector and retail.

Engage Hub’s product roadmap focuses on enhancements to its customer journey visualization capabilities, AI-driven insights to support logic-based orchestration, and AI monitoring and adjustment of journeys and outcomes.

- AI capabilities: Engage Hub is notable for its strong AI-supported solution capabilities, including the native ability to deploy customer-facing conversational AI channels. It has invested heavily in agentic AI, enabling users to configure complex multiagent workflows that execute end-to-end automations through the orchestration layer.

- Regulated industries support: Engage Hub has demonstrated its suitability for a range of regulated sectors, including government. The platform has specialized features such as the RegSolv tool for compliance tracking, PCI DSS-compliant payment orchestration and advanced security authenticators.

- Approach to roadmap: Engage Hub takes a two-part approach to building its product roadmap: 50% is based on direct customer feedback (obtained through customer interactions, journey tracking and formal market research), and the other 50% is reserved for features that anticipate broader market trends.

- Market visibility: Engage Hub has limited market visibility due to underinvestment in marketing and sales. Its CJA/O thought leadership and blogs are often outdated, and it has limited presence at events. This can make it hard for prospects to discern whether its capabilities suit their needs. Gartner has noted increasing recognition of this challenge, with Engage Hub looking to invest more heavily in market outreach in the year ahead.

- Sales/onboarding length: Engage Hub has some of the longest sales cycles, on average, among the vendors in this research. It attributes an increase in customer onboarding timelines over the past year to heightened scrutiny of its AI capabilities. Its limited in-house sales resources may also lead to increased purchase friction.

- Size of customer base: Engage Hub’s revenue depends heavily on a small number of large customer accounts. While this may currently enable highly attentive customer-vendor relationships, customers’ relative importance and the quality of dedicated support could dissipate as the customer base grows.

inQuba

inQuba is a Niche Player in this Magic Quadrant due to its small footprint and product maturity gaps. Its Customer Journey Management product is best-suited for customer service and support use cases. Its operations are predominantly based in EMEA, with a small, but growing, presence in the Asia/Pacific region. Customers tend to be midsize to large enterprises concentrated in the banking, finance and insurance, and investment service industries.

inQuba’s product roadmap includes expanded agentic AI capabilities, improved journey profitability and lifetime value attribution, expanded support for orchestration via WhatsApp, enhanced capabilities to handle erroneous data, and architecture updates to support elastic scaling.

- Breadth of support: Despite its smaller customer base, inQuba has successfully demonstrated how its solution can support a variety of functions and enterprise sizes. The vendor is particularly notable for its success in supporting highly regulated industries.

- Pricing strategy: inQuba uses a straightforward pricing approach that simplifies the buying process and contributes to a shorter-than-average sales cycle for new customers. The platform is sold as a stand-alone solution with a flat annual platform fee. Outcome- or risk‑reward-based pricing is available as an alternative. Implementation and premium support services are offered as separately priced add-ons.

- Sales innovation: inQuba offers targeted pricing/feature bundles tailored to specific use cases to help smaller customers adopt CJA/O at a lower cost and in less time. It also runs Journey Accelerator Workshops that fast-track business cases and clarify the benefits of CJA/O, thus shortening sales cycles.

- Time to value: inQuba’s heavy dependence on professional services contributes to slower onboarding timelines compared to other vendors in this research. Because the platform requires significant upfront professional services and longer deployment times, customers should evaluate inQuba’s risk-reward or outcome-based pricing model during procurement.

- Product maturity: While inQuba’s roadmap and priorities align with the broader market direction, the vendor overlooks other foundational requirements to improve broader product capabilities, such as enhanced integration of VoC in journey analysis views, owned-channel orchestration and journey governance.

- Persona/role resources: Compared to the Leaders in this Magic Quadrant, inQuba offers fewer resources tailored to the buyer needs of specific roles or personas (e.g., marketing, CX, customer service leaders). Prospects should request specific case studies that demonstrate the vendor’s ability to support role-specific KPIs and use cases.

Joulica

Joulica is a Niche Player in this Magic Quadrant due to its small customer base and heavily analytics-focused offering. Its Customer Journey Analytics platform is best-suited for organizations looking to layer customer journey analytics on top of existing infrastructure (e.g., AWS, Google, Salesforce, Zoom). Its operations are mainly focused in North America, with a smaller presence in Europe. Its customers are primarily midsize enterprises in banking, finance and insurance, construction and real estate, and professional services.

Its product roadmap focuses on further expansion of its data integrations, the addition of agentic AI analytics, enhancements to its orchestration capabilities and the ability to benchmark customer journey KPIs.

- Megavendor alliances: Joulica maintains a strong partner strategy, working with vendors such as AWS, Google, Salesforce and Zoom. Its emphasis on journey analytics as a stand-alone capability makes it a natural fit for organizations that want a dedicated customer journey analytics offering to integrate with their existing platforms and architectures, which may handle broader orchestration.

- Investment in marketing: Joulica is investing in targeted prospect and customer outreach to strengthen its market position. Its focus on role- and segment-specific messaging, and the appointment of a new CMO, underscore this shift.

- Sales and retention strategy: Despite still having a comparatively small footprint in the market, Joulica has more than doubled the size of its customer base over the past three years, while maintaining customer retention rates of over 95%. It plans to triple its investment in sales resources over the coming year and to increase spending on customer success and professional services to support continued growth.

- Innovation strategy: Despite spending a significant percentage of its revenue on R&D, Joulica takes a slower, more reactive approach to innovation. For example, it has only recently begun to invest in its own native orchestration capabilities — several years behind its competitors.

- Market vision: Joulica’s planned investments show a lack of differentiated vision for the CJA/O market. There is no mitigation plan provided for disruptive trends, such as the shift to third-party conversational journeys (e.g., those undertaken via ChatGPT) or for the significant risk of a partner developing CJA/O capabilities to independently offer customer experience as a service (CXaaS).

- Off-the-shelf industry support: Joulica lacks industry-specific platform features and pre- or postsales resources. Instead, its platform offers generalized features that customers must tailor to their vertical. Prospects should take advantage of Joulica’s free proofs of concept to ensure the platform can be adapted to meet industry-specific needs.

Medallia

Medallia is a Niche Player in this Magic Quadrant due to its unclear market positioning and limited product investment. It offers CJA/O through a combination of its VoC platform, Medallia Experience Cloud (MEC), and the Medallia Experience Orchestration (MXO) add-on. It is best-suited for existing customers of the broader MEC platform, or organizations willing to move other VoC efforts to MEC. It has a global presence and its customers span most industries, with particular concentrations in financial services, travel, hospitality and entertainment, and retail.

Its product roadmap includes an AI insights assistant, B2B account profiles, agentic messaging and automated scoring of friction in omnichannel journeys.

Medallia declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- VoC integration: Medallia’s core focus on MEC gives it deep expertise in unified VoC capabilities. This extends to its product, where it enables cross-functional CX teams to combine CJA/O with VoC insights to identify drivers of customer outcomes and sentiment.

- Ease of adoption: Many leading CX organizations are already Medallia customers, and the ability to deploy MXO as an add-on has the potential to significantly simplify adoption by reducing integration friction and the need for vendor management.

- Industry focus: Medallia shows an expansive vertical strategy, offering dedicated and tailored solutions across more than a dozen specific industries, including financial services, healthcare, retail, automotive and the public sector. The vendor invests heavily in industry-specific resources, providing specialized market research, targeted playbooks and compliance-ready tools, such as tailored government cloud environments.

- Market positioning: Medallia offers a relatively capable CJA/O product for its target markets, yet its public positioning is inconsistent. It often frames its technology as complementary to other vendors’ solutions — for example, positioning itself as a strategic partner to Adobe — which creates uncertainty for buyers evaluating Medallia as a stand-alone CJA/O provider.

- Sales strategy: Until recently, MXO was available as a stand-alone solution. However, the vendor has since decided to offer this product only as an add-on for its existing customer base, which limits the product’s potential reach and reduces flexibility in pricing and bundling options.

- Product investment: Medallia has invested only minimally in promoting and advancing the capabilities of its MXO solution over the past year. This reduces the product’s visibility in the market beyond Medallia’s existing customer base and raises questions about its long-term future and viability.

Woopra

Woopra, an Appier company, is a Niche Player in this Magic Quadrant due to its shifting functional and geographic focus and unclear platform direction. Its platform, which can be used alone or as part of Appier’s broader marketing suite, is best-suited for organizations that are looking to optimize marketing campaign journeys or that already leverage other Appier solutions. Recent strategic shifts have moved the vendor’s focus away from small and midsize enterprises in North America and toward large enterprises in the Asia/Pacific region.

Its product roadmap emphasizes agentic AI capabilities designed to enhance journey insight discovery and action. It also plans to offer probabilistic identity matching capabilities.

- Support for emerging touchpoints: Woopra is adapting its platform to handle complex new touchpoints by expanding its event models to capture conversational AI intents, building machine-operable APIs for safe bot-to-bot interactions and embedding privacy-by-design governance to navigate decentralization.

- Market responsiveness: Woopra has a strong customer feedback collection and improvement loop, with a deep understanding of the challenges customers experience with CJA/O and its platform. It has plans — some already delivered — to mitigate these concerns.

- CX: Woopra eschews traditional paid professional services in favor of comprehensive onboarding, unlimited working sessions and dedicated customer success engineers, included at no additional cost within the Pro and Enterprise packages. This support model accelerates time to value, particularly for those in Woopra’s core retail and e-commerce markets, by guiding users through prebuilt, industry-specific playbooks.

- Long-term roadmap: Having been acquired by Appier, Woopra is shifting its product strategy from a stand-alone offering to an embedded “intelligence layer” within Appier’s broader marketing suite. This creates uncertainty about Woopra’s long-term independent roadmap. While Woopra remains available as a stand-alone solution, prospects should evaluate whether they will need to purchase additional Appier products to access advanced capabilities for their orchestration needs.

- Strategy change: The shift in Woopra’s target audience signals a significant change in strategy. Existing customers in North America may see less support as its resources move to the Asia/Pacific region, and Asia/Pacific prospects should verify its ability to support a market where it has not yet proven itself.

- Functional focus: Over the past year, Woopra’s messaging has shifted away from CJA/O toward a more singular focus on agentic AI. Its traditional focus on broad, cross-functional playbooks has narrowed to prioritize marketing as the primary use case. This creates ambiguity about the product’s future focus and viability for use cases beyond marketing AI.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Dropped

- Genesys, previously featured in Gartner’s Market Guide for Customer Journey Analytics and Orchestration after its 2021 acquisition of Pointillist, a CJA/O platform. Genesys recently announced the deprecation of Pointillist (effective July 2026), consolidating its resources and innovation on the Genesys Cloud Journey Management functionality. As of 15 January 2026, Genesys’ data capture capabilities are not source-system-agnostic, lacking the ability to ingest third-party data, so it does not meet this year’s inclusion criteria. Genesys expects to support this capability as of March 2026.

- Qualtrics, previously featured in Gartner’s Market Guide for Customer Journey Analytics and Orchestration after its 2021 acquisition of Usermind, a customer journey analytics and orchestration platform. It is no longer included in our market coverage as it no longer publicly markets CJA/O as a capability on its website, and research indicates these features are no longer available in its Experience Management (XM) platform.

Inclusion and Exclusion Criteria

CJA/O capabilities can be found in many forms across a range of different use-case-specific technologies. The vendors listed in this Magic Quadrant do not comprise an exhaustive list of vendors in this market. To qualify for inclusion in the Magic Quadrant for Customer Journey Analytics & Orchestration, vendors were required to meet the following criteria:

- Customer journey analytics and orchestration must be publicly marketed as a product or feature on the vendor’s website.

- The product must meet Gartner’s market definition for CJA/O platforms. Specifically, the platform must directly (i.e., not through another vendor product) support all five of the following capabilities:

- Data capture — The solution must be able to ingest data from different internal systems and multiple channels of engagement (such as a website, chatbot, retail store, live chat, phone, etc.). The ability to ingest data must be source-system-agnostic (for example, data cannot be limited to only digital channels), although vendors may additionally choose to provide dedicated connectors to specific solutions.

- Journey visualization — The solution must be able to visualize a customer’s journey across all of the multiple channels and touchpoints ingested, both at a macro level (i.e., for a group of customers) and at an individual customer level. These visualizations may require user input or may be generated dynamically.

- Deterministic customer identity matching — The solution must be able to connect customer records based on specific known identifiers (e.g., a user ID, phone number, etc.) in order to track individual users’ multichannel journeys. Solutions may connect to other services in the organization to access identity data.

- Journey prioritization and outcome management — The solution must enable organizations to assess the business and customer impact of journeys and potential improvements.

- Journey orchestration — The solution must enable organizations to intervene in a customer’s journey in near real time. Journey orchestration can be rule-based or leverage predictive analytics and machine learning to identify where to intervene in journeys to optimize customer and/or business outcomes. This could include automating customer-facing actions (such as generating a communication) or internal actions (such as generating an alert).

- The CJA/O product version being evaluated must have been generally available as of 15 January 2026.

- The CJA/O product must be in production use by both B2B and B2C (or B2B2C) company use cases.

- The provider must have a presence in at least two of the following regions: North America, Latin America, EMEA, Asia/Pacific.

Evaluation Criteria

Ability to Execute

Product/Service: We specifically looked at the vendor’s performance in each of the critical capabilities defined in the Critical Capabilities companion research. We also assessed the vendor’s own views of suitability to deliver against four function-specific use cases: B2B sales and account management, customer service and support, end-to-end CX management, and marketing campaign management. Also considered were plans to address product weaknesses.

Overall Viability: We specifically looked at the size and focus of the vendor’s customer portfolio, market-specific customer growth and retention, and resource growth and utilization. Also assessed was the strategic alignment of the vendor’s CJA/O offering within the broader portfolio of the organization/parent company (where relevant), as well as the impacts of any ongoing mergers or acquisitions, and any other drivers of viability.

Sales Execution/Pricing: We specifically looked at direct and indirect sales revenue and customer growth; pricing clarity, flexibility, affordability, value for the money spent and innovation; and typical contract terms. Also assessed was the vendor’s success at securing cross-functional sales that target multiple functional use cases.

Market Responsiveness/Record: We specifically looked at mechanisms for monitoring and responding to customer needs and evidence of listening to, adapting to and aligning with customer needs and market trends. Also assessed was the quality of recent product releases/updates, as well as recent issues that have negatively impacted CX and how the vendor responded to them. We also looked at how the product roadmap is communicated and updates are adopted by customers.

Marketing Execution: We specifically looked at evidence of brand awareness, perception and strength, and evidence of the vendor’s marketing presence and thought leadership, including through events, blogs, whitepapers, case studies, webinars and other media. Also assessed were recent marketing messages and campaigns.

Customer Experience: We specifically looked at overall satisfaction with the provider’s capabilities and delivery; the presence of a mature CX business capability; the speed of and obstacles to customer onboarding; and the availability, adoption and success of customer success and professional service offerings.

Operations; We specifically looked at overall resourcing and the use of AI agents; compliance with and participation in regulatory or certification frameworks; geographic spread and support; and support for data residency requirements.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | High |

Market Responsiveness/Record | Medium |

Marketing Execution | Medium |

Customer Experience | High |

Operations | Low |

Source: Gartner (March 2026)

Completeness of Vision

Market Understanding: We specifically looked at how vendors listen to current customer demands, understand how those needs will evolve in future and adapt their roadmap accordingly, and how vendors demonstrate a grasp of current competitors and any overlap with adjacent software markets. Differentiation (product, business practices, customer experience) was also assessed.

Marketing Strategy: We specifically looked at vendor perceptions of brand awareness in the CJA/O market; strong articulation of the ideal customer profile; and positioning to meet the needs of current ideal customer profile and new customer target segments.

Sales Strategy: We specifically looked at whether the vendor has a value-based selling strategy, and how it flexes its sales strategy for different target customer profiles/personas/functions, as well as its ability to sell cross-functional CJA/O implementations (e.g., for marketing and customer service combined). We also assessed whether product and service bundling and pricing is clearly articulated and designed to meet the needs of customers, and whether total cost of ownership (TCO) is easy to predict. The availability of POCs, free trials, outcome-based pricing, and support with business case development and value definition was also considered, as were anticipated changes to sales strategies and pricing or licensing models in the coming year.

Offering (Product) Strategy: We specifically looked for role-based and use-case-driven R&D investments that keep pace with customer expectations, as well as a clear, forward-thinking roadmap for the coming year that focuses on delivering features of high value to most of the vendor’s customer base. Architecture, platform scalability and UI/UX investments were also assessed.

Business Model: This criterion was not assessed in this Magic Quadrant. All vendors offer a SaaS-based product offering.

Vertical/Industry Strategy: We specifically looked at platform capabilities to support specific verticals/industries; vendor understanding of vertical/industry-specific trends, and plans to address these to support customers; sales and marketing to support industry requirements and use cases; and vendor strength in specific industries.

Innovation: We specifically looked for evidence of investment in R&D; the vendor’s outlook on the longer-term future of the market and plans to mitigate the impact of likely trends; and product innovation, in particular to incorporate new technologies. We also looked for customer experience and operational innovation in new forms of training, education, events, licensing and organizational changes.

Geographic Strategy: This criterion was not assessed in this Magic Quadrant, given the potential for SaaS solutions to be leveraged internationally. The split of vendors’ customer bases across geographies, and support for these customers, was assessed separately via other criteria.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | Medium |

Marketing Strategy | Medium |

Sales Strategy | High |

Offering (Product) Strategy | High |

Business Model | NotRated |

Vertical/Industry Strategy | Low |

Innovation | High |

Geographic Strategy | NotRated |

Source: Gartner (March 2026)

Quadrant Descriptions

Leaders

Leaders demonstrate strong execution across multiple functional use cases and deliver meaningful business outcomes through enterprise-grade CJA/O capabilities. They show consistent roadmap momentum, have a clear market vision, and have the operational maturity, CX and market presence to support cross-functional deployments at scale. Leaders are often the vendors against which other providers measure themselves.

Challengers

Challengers have a more focused CJA/O strategy and more comprehensive platform than Niche Players. They have the size and product capabilities to compete worldwide, but they might not be able to provide a compelling vision. Challengers execute well across multiple functional use cases and sizes of business. There are no Challengers in this year’s Magic Quadrant.

Visionaries

Visionaries deliver innovative and potentially market-changing solutions, but they struggle to meet the needs of all organizations due to geographic limitations, company size constraints and/or specific product limitations. They have strong potential to influence the direction of the market, but are limited in terms of execution and/or track record.

Niche Players

Niche Players sometimes offer the best solutions for the needs of organizations of a particular size or industry, considering the price-to-value ratio of their solutions. But they may lack specific functionality; focus support on fewer functions, industries or regions; or lack the investment required to scale their customer base.

Context

This Magic Quadrant is designed to help buyers with the decision-making process regarding a CJA/O platform, providing details on the market and vendor capabilities that align with your business problems and technical concerns. Your shortlist should be determined by the complexity and scale of your requirements. This Magic Quadrant is not designed to be the sole tool for creating a CJA/O vendor shortlist. Use it as part of your due diligence, in conjunction with discussions with Gartner analysts and other customer journey management research, including the associated Critical Capabilities for Customer Journey Analytics & Orchestration.

Gartner clients shouldn’t assume that a CJA/O Leader vendor is always the best fit for their company. Differences in product offerings, innovation and go-to-market strategies vary by vendor. Therefore, every provider in this Magic Quadrant, no matter its placement, may be a best fit for a client, and clients should explore how that diversity meets their business needs. Gartner clients should follow a deliberate RFP process when selecting a CJA/O platform vendor. The RFP process aligns the buying team around the value for the purchase, creates consensus for the selected vendor and helps ensure support for the implementation.

Gartner recommends focusing on the following factors when procuring and implementing a CJA/O platform:

- Functional and cross-functional fit: To maximize the value you derive from your CJA/O solution, you should seek a solution that can support a variety of cross-functional use cases, rather than focusing on product fit for a single function. The needs of each participating function should be gathered and the anticipated value and outcomes evaluated to ensure alignment with business objectives and expectations. A representative of each participating function should be involved in the vendor evaluation and decision-making process to ensure functional and use-case needs are evaluated. You can leverage Gartner’s BuySmart™ tool to help you compile requirements and assess vendor suitability as a team (see Note 1).

- AI governance: With AI (including agentic) increasingly embedded in CJA/O tools, buyers should assess how these solutions fit their data, AI governance and operating model needs, or if the AI can be configured to meet their requirements.

- Reference customers: Always delve into the prospective vendor’s customer base to explore exactly what is being delivered and the outcomes achieved. Look beyond the size of the deployment (number of users) to include the types of feedback, analysis and action being taken from it. Ask about client retention and tenure rates, along with efforts to improve customer experience.

- Selection criteria: Beyond functional considerations, closely scrutinize the vendor’s data architecture, administration layer, UX, associated analytics and professional services organization (both technical and business-oriented). With increased emphasis on adhering to data privacy regulations, you must also understand how data will be stored, which team members will have access to it and how it will be used.

- Professional services: Consider the extent to which you will require professional services — both during onboarding and in longer-term use of the CJA/O solution — to maximize ROI, and factor this into your TCO calculation.

- Roadmap and innovation: Ask vendors for their roadmap, including how they intend to mitigate broader market trends (see below), upcoming product releases and investment in improving the customer experience (e.g., customer success, pricing and bundling, training materials, etc.). Ensure that the direction the vendor is headed in aligns to your business needs, and doesn’t just meet your immediate needs, but also will enable you to grow to meet your three-year plan going forward.

Magic Quadrants are snapshots in time. To be impartial and to complete our analysis, we stop our data collection efforts at a specific time for all vendors. For this Magic Quadrant, the product/service capabilities needed to be in production and generally available in mid-January 2026 to be considered in our evaluation.

Market Overview

The market for customer journey analytics & orchestration is maturing but remains fluid. While it may appear a significant gap exists between the Leaders in this Magic Quadrant and the Visionaries and Niche Players, this is predominantly driven by the Leaders’ operational maturity and larger market presence. Product capability differences between vendors in different quadrants can be much smaller.

Evolving Vendor Landscape

A healthy cohort of stand-alone vendors continues to compete effectively, even as broader suite providers embed or increasingly build CJA/O capabilities into their solution stacks.

But while it previously seemed likely that the market would further consolidate and CJA/O would be included as a capability within broader suite solutions, that outcome now feels less certain. Some suite vendors have exited the CJA/O market in the past year, others have de-emphasized and repackaged their CJA/O capabilities, while still others are accelerating their integration as part of a wider CXaaS vision.

A further shift this year is the growing divergence in functional orientation across vendor offerings. Every vendor that participated formally in this year’s Magic Quadrant claimed to be able to support all four functional use cases we presented — B2B sales and account management, customer service, end-to-end CX management, and marketing campaign management. However, in practice, their customer bases and roadmaps often reflect deeper strength in one or two functions, rather than the enterprise as a whole.

This divergence creates meaningful differences in suitability for cross‑functional deployments, which Gartner views as essential for realizing the full value of CJA/O. As highlighted in this year’s Critical Capabilities research, organizations increasingly expect these tools to support end‑to‑end, shared-journey priorities. Vendors that can demonstrate credible cross‑functional capability, rather than function‑specific depth alone, are better-positioned to meet those expectations.

Buyer Confusion With Adjacent Technologies

Many vendors use terminology related to journey management and analysis interchangeably (see Distinguishing Customer Journey Management, Mapping, Analytics and Orchestration). This confusion leads to downstream challenges: mis-scoped RFPs, poorly aligned stakeholder expectations, mismatches between buyer needs and vendor strengths, and under-realization of value once implementations begin. We strongly encourage clients to review:

- The Market Definition in this Magic Quadrant for CJA/O

We also regularly observe confusion among clients as to whether they really want a CJA/O solution or whether they are conflating these tools with adjacent technologies. In particular, we observe the following common areas of overlap.

Customer Journey Mapping Technologies

Vendors like Cemantica, JourneyTrack, Smaply and TheyDo offer specialized tools for mapping customer journeys (through stakeholder input and AI-driven analysis of VoC surveys, transcripts and focus group interviews), visualizing the current state and designing future-state journeys that span various touchpoints. But they do not ingest channel event data and stitch it together based on common customer identifiers, or provide real-time orchestration capabilities, as CJA/O tools do (see Innovation Insight: Customer Journey Mapping Technology).

For clarity: CJA/O tools, at present, do not support journey mapping capabilities. We believe adding these capabilities (or dedicated integrations to tools that offer them) would significantly increase the value of, and lower barriers to adoption for, CJA/O tools.

Digital, Web and Product Analytics Tools

Vendors like Amplitude, Contentsquare, Pendo and Quantum Metric analyze digital product behavior, but they are not designed to ingest the full spectrum of digital, physical and analog customer interactions that define end‑to‑end journeys — a mandatory feature for inclusion in this market. This distinction is critical; customer journeys do not happen solely within digital products, so relying on these tools for end-to-end journey analysis will provide only a partial view as compared to true CJA/O vendors (see Market Guide for Product Analytics).

Multichannel Marketing Hubs (MMHs)

Vendors like Adobe, Braze, Insider, Salesforce, and SAP support the orchestration and delivery of personalized marketing campaigns across owned and paid channels through outbound engagement, content generation, and campaign automation. While MMHs increasingly incorporate journey‑aware capabilities and real-time decision making, their primary purpose is to execute digital-marketing-led communications, not to analyze or optimize end‑to‑end customer journeys.

Organizations that treat MMHs as substitutes for CJA/O risk narrowing their understanding of journeys to the marketing domain and overlooking upstream or downstream operational drivers that materially impact customer experience and business outcomes. (See Magic Quadrant for Multichannel Marketing Hubs.)

Demand Patterns

Demand for CJA/O continues to grow across industries and functions, but the nature of that demand is diverging. Buyers should consider how organizations of a similar size to their own are approaching CJA/O:

- Large enterprises increasingly expect CJA/O to demonstrate cross-functional value, linking insights and customer engagement across marketing, service, sales and enterprise CX. This reflects the trend of senior marketing leaders, customer service and support leaders, and enterprise CX teams all reporting active or expanding use of journey analytics. Large enterprises also place greater emphasis on governance, explainability, and the ability to tailor AI‑enabled analysis and orchestration to their data, policies and operating models.

- Midsize organizations more commonly deploy CJA/O to support a single function first and limit the scope to the most critical channels and journeys. They use modular packaging and existing suite relationships (where offered) to reduce cost and accelerate time to value. However, there is a trade-off: Vendors with strong function-specific capabilities may serve these deployments well, but may not be positioned to support cross-functional expansion later.

- Both segments continue to scrutinize ROI. Many organizations seek clearer links between journey improvement and business outcomes, greater flexibility in commercial models, and reduced dependency on professional services as they scale their programs. These factors contribute to more selective vendor evaluation.

Recent Changes

Expansion of AI

In the past year, AI has been the driving force behind vendors’ roadmaps for both journey analysis and orchestration. Embedded assistants for journey analysis and autogenerated insight narratives are now common, and embedding agentic AI in orchestration is in most vendors’ near-term roadmaps (or, for CSG and Engage Hub, already delivered). We have also noted continued expansion in owned-channel orchestration capabilities, and a doubling-down in vendor messaging about “real-time” journey analysis and orchestration capabilities.

Shifting Cost of Ownership and Importance of Time to Value

To make CJA/O more accessible and address buyer concerns about ROI, some vendors have adjusted their pricing models from consumption-based to modular licensing or value-based, or to include CJA/O alongside broader software suites. However, new AI investments threaten this pricing stability, as vendors may layer in additional consumption-based models to recoup costs and grow revenue.

Such pricing additions increase the pressure on vendors to accelerate time to value. Vendors have traditionally relied on professional services to support users in configuring the platform, analyzing journeys and building orchestration workflows, and they market these services as value-add. But these services also significantly increase TCO. Now, demand for such support is likely to increase, but few vendors are focusing on how to reduce this dependency or enable faster time to value to offset the rising TCO.

Future Direction

Over the next few years, the CJA/O market will be shaped most significantly by two related shifts:

- The rise of conversation-first journeys — As customers increasingly interact through chat, messaging, voicebots, multimodal assistants and generative AI (GenAI) interfaces, organizations will need analytics and orchestration capabilities that interpret journeys through intent‑ and interaction‑level signals, rather than clickstream sequences alone.

- The migration of journeys into third-party channels — Organizations will increasingly need ways to monitor and shape portions of the journey that unfold outside their own digital perimeter, including in agentic commerce, generative engine optimization (GEO) search results, third‑party GenAI tools, and social or multimedia environments, where data is difficult to obtain.

Several vendors have begun responding by integrating conversational context into journey visualizations and orchestration logic, and by using AI‑derived summaries to surface intent and sentiment within conversational flows. But most vendors remain primarily focused on company-owned channels, with limited ability to analyze or influence third-party journey moments.

As conversational channels and external ecosystems proliferate in customer journeys, CJA/O providers must adapt quickly to remain the system of intelligence for understanding and improving customer journeys. If they can’t adapt fast enough, that role will shift to adjacent markets evolving at greater speed.

This is the first version of the Magic Quadrant for Customer Journey Analytics & Orchestration. It replaces the Market Guide for Customer Journey Analytics & Orchestration.

Acronym Key and Glossary Terms

| AI | artificial intelligence |

| CJA/O | customer journey analytics and orchestration |

| CX | customer experience |

| CXaaS | customer experience as a service |

| GenAI | generative AI |

| TCO | total cost of ownership |

| VoC | voice of the customer |

Note 1: Gartner BuySmart™

The Gartner BuySmart™ tool helps guide you through technology evaluations with templates containing requirements and scorecards to help you select the best providers for your needs. Using a connected workflow, BuySmart enables you to conduct thorough evaluations to invest confidently. See the BuySmart template designed for Customer Journey Analytics & Orchestration.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.