Magic Quadrant for Enterprise Wired and Wireless LAN

18 May 2026 - ID G00839405 - 40 min read

By Mike Leibovitz, Christian Canales, and 1 more

The enterprise wired and wireless LAN market is increasingly defined by operational outcomes rather than features. Vendor innovation investments are focused on AI to deliver more secure and more autonomous networks that reduce operational effort and perform consistently over time.

Strategic Planning Assumptions

By 2030, 50% of organizations will use agentic network operations for tasks such as change validation and incident analysis, up from near 0% in 2025.

By 2029, 20% of enterprises will replace traditional NAC on campus LANs, using ZTNA or identity-based fabric controls instead, up from fewer than 2% in 2025.

Market Definition/Description

Gartner defines the enterprise wired and wireless LAN market as the infrastructure that enables secure connectivity across enterprise locations. This encompasses the hardware, software, and management capabilities required to deliver physical and logical network connectivity, enforce zero-trust security principles, and automate operations across campus, branch, and remote environments, including operational technology (OT) domains.

Enterprise wired and wireless LAN infrastructures solve the operational complexity of delivering secure, scalable connectivity across distributed enterprise environments. As organizations expand across campus, branch, remote, and operational technology domains, traditional network deployment and management approaches become too resource-intensive and inconsistent to meet business demands.

The offered capabilities address the business problem of fragmented network operations by unifying life cycle management (that is, provisioning, monitoring, policy enforcement, and incident response) into a single, software-driven system. This reduces manual effort, shortens resolution times, and improves compliance with governance and security requirements.

While hardware remains foundational, it is the infrastructure operations software (that is, automation, telemetry, and policy orchestration) that delivers the operational and business value enterprises seek.

Tangible outcomes include faster site turn-up, proactive issue detection and remediation, consistent user experience, and alignment of network operations with enterprise workflows through IT service management (ITSM) integration. Organizations also gain flexibility through cloud, on-premises, hybrid, and network as a service (NaaS) consumption models, enabling them to scale operations efficiently while maintaining control over data and performance.

Mandatory Features

The mandatory features of this market include:

- Unified Management: A single application — be it cloud, on-premises, or hybrid — that provides centralized visibility and control across wired and wireless infrastructure.

- Life Cycle Automation: Automation across all operational stages, including zero-touch provisioning for deployment and low-touch administration for ongoing operations.

- Access Security: A security application for authenticating users and devices, and for creating and enforcing access policies at the point of connection.

- Automated Campus Fabric: A network fabric architecture that enables automated device isolation, microsegmentation, and policy enforcement for all devices, including unmanaged or legacy Internet of Things (IoT) and OT.

- Real-Time Streaming Telemetry and Monitoring: Continuous generation of telemetry data from infrastructure components to support network optimization, troubleshooting, and issue resolution.

- Enterprise Workflow Integration: Integration with ITSM applications to automate incident handling, change management, and compliance reporting.

- API and Extensibility: Published, public APIs that expose functions for integration with third-party applications, enabling automation and data exchange.

- Enterprise-Grade Hardware Portfolio: A portfolio of hardware, including Ethernet network switches for all campus layers featuring high-density Power over Ethernet (PoE/PoE+/PoE++) and support for MACsec encryption. The portfolio must also include Wi-Fi-certified access points that support 2.4 GHz, 5 GHz, and 6 GHz radios.

Optional Features

The optional features for this market include:

- Universal Zero-Trust Network Access (UZTNA): A security model that enforces zero-trust principles for all local and remote users and devices through granular, adaptive access controls and microsegmentation.

- Behavioral Analytics: User and entity behavior analytics (UEBA) to monitor and analyze behavior patterns, informing security policy and operational decisions.

- Automated Threat Response and Containment: The ability to automatically respond to detected threats or known vulnerabilities (CVEs) by quarantining affected devices using the network fabric.

- Network Digital Twin for Change Validation: A virtual replica of the network used to simulate and validate changes, such as firmware upgrades, configuration updates, or security policy adjustments, before deployment.

- Agentic NetOps for Autonomous Operations: The use of AI agents, often leveraging domain-specific large language models (LLMs), to reason over telemetry and execute intent-based operational tasks.

- AI Network Assistant: A natural language interface, powered by a domain-specific LLM trained on network data, for conversational configuration, troubleshooting, and operational support.

- Configuration Drift Detection and Remediation: Tools that monitor for unauthorized or unintended configuration changes and enable automated rollback or remediation.

- AI-Enhanced Radio Resource Management (RRM): The application of AI to proactively optimize wireless network performance through dynamic radio tuning and interference mitigation.

- Client-to-Cloud Visibility: Integrated tools that provide hop-by-hop visibility and diagnostics from the end-user device to the application, across both LAN and WAN paths.

- Application Quality of Experience (QoE) Analytics: Analytics that measure the performance and usage of specific applications across Layers 4 through 7 to inform optimization and SLA tracking.

- Advanced Location Services: Collection and analysis of location telemetry from network infrastructure to enable indoor positioning and location-aware services.

- Data Sovereignty Controls: Deployment options that support data residency and sovereignty requirements through cloud, on-premises, or hybrid hosting models.

- Generative UI and Collaborative Dashboards: A contextualized or generative user interface that simplifies operations and enables shared, real-time visualization of network data.

- Multivendor Management: The ability to manage third-party or legacy network switches and access points.

- Flexible Licensing and Consumption Models: Support for subscription, perpetual, or usage-based licensing models, including NaaS offerings backed by SLAs.

Exclusions: It is important to note that this market definition does not encompass wired and wireless networking infrastructure devices primarily utilized to support adjacent markets, such as point-to-point wireless WAN offerings, industrial/ruggedized LAN equipment, or Wi-Fi hot spot services.

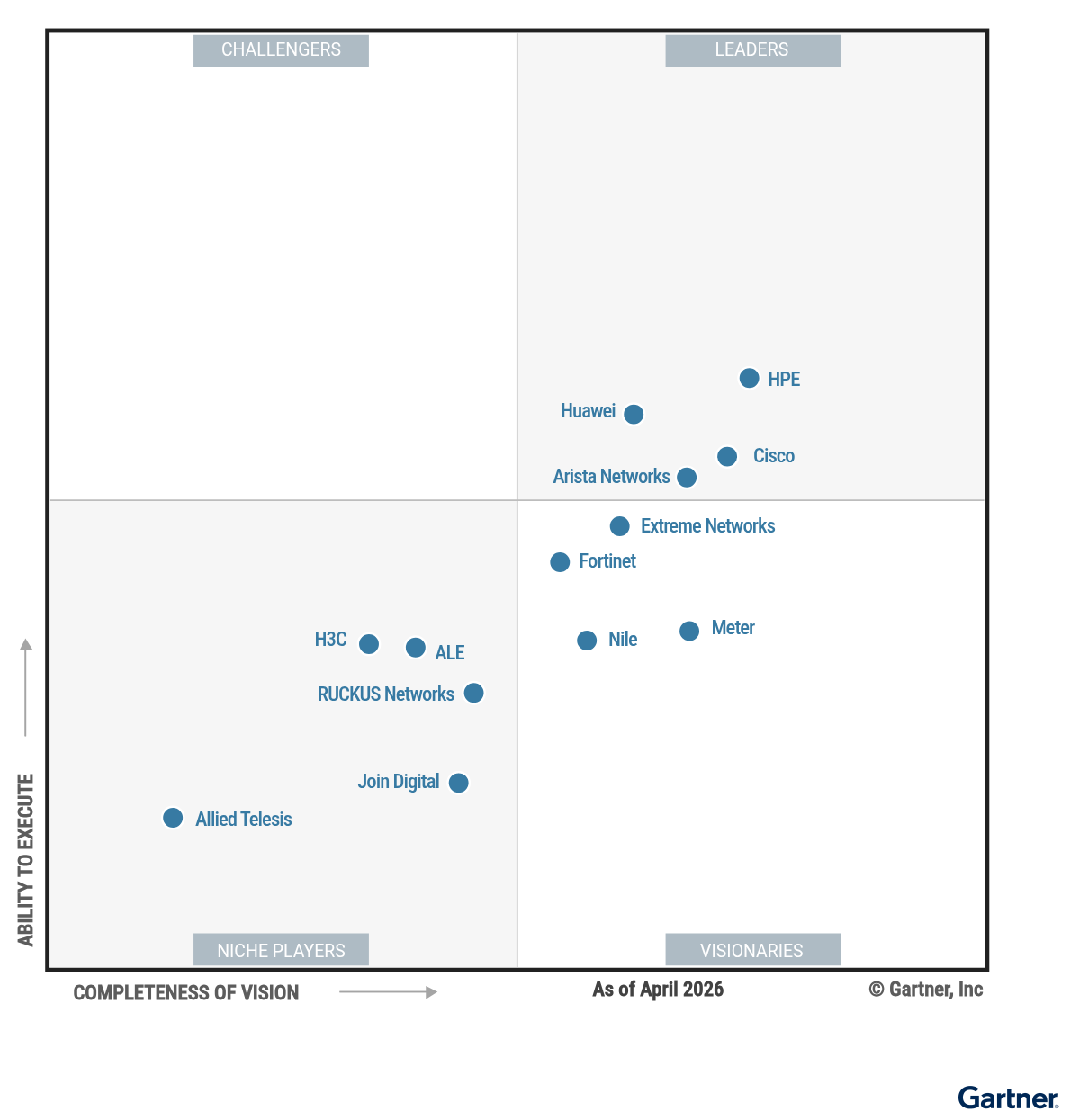

Magic Quadrant

Vendor Strengths and Cautions

ALE

Alcatel-Lucent Enterprise (ALE) is a Niche Player in this Magic Quadrant. The company offers an enterprise wired and wireless LAN portfolio that includes OmniSwitch Ethernet switches, OmniAccess Stellar wireless access points and the OmniVista management platform. The portfolio supports cloud-based, on-premises and hybrid management, with campus segmentation and identity-based policy enforcement for IT, IoT and OT devices. ALE serves enterprises and public-sector organizations, focusing on transportation, healthcare, government and education, with the strongest customer adoption in Europe. Gartner expects ALE to continue investing in AI-assisted networking capabilities to improve operational workflows and efficiency.

- Campus segmentation focus: ALE delivers identity-driven segmentation across wired and wireless campus access for environments where access control and policy enforcement are primary requirements.

- Regulated and industrial environment fit: ALE executes effectively in transportation, healthcare and government environments that prioritize compliance, deterministic behavior and controlled change.

- Licensing flexibility: ALE offers flexible commercial models, including perpetual licensing alongside subscriptions, with capabilities such as NAC included at no additional cost.

- AI operational scope: AI capabilities are primarily delivered through guided, human-validated workflows, with selective closed-loop execution.

- Cloud deployment choice: Cloud delivery supports a more limited set of providers rather than multiple hyperscalers.

- Geographic concentration: Enterprise campus LAN adoption remains strongest in Europe, which may require additional validation of service and support consistency outside core markets.

Allied Telesis

Allied Telesis is a Niche Player in this Magic Quadrant. The company provides an enterprise wired and wireless LAN portfolio that includes Ethernet switches, wireless access points and centralized management through OneConnect, Vista Manager EX, the Autonomous Management Framework Plus (AMF Plus), the AMF-Security Controller and Autonomous Wave Control (AWC). Enterprise adoption is most common in healthcare, education and government environments, with execution that is strongest in the Japanese market. Gartner expects Allied Telesis to continue investing in cloud-based management and AI-assisted networking capabilities.

- Single-OS campus management: Allied Telesis operates wired and wireless LAN infrastructure on a single network operating system with centralized management through Vista Manager EX, supporting standardized configuration and life cycle management.

- Vertical environment fit: The portfolio supports security and segmentation requirements found in regulated environments such as healthcare, education and government.

- Simplified administration: Allied Telesis aligns its offerings for organizations that prioritize simplified day-to-day administration and predictable operations.

- Cross-domain visibility: End-to-end telemetry and assurance across wired and wireless LAN domains are limited, constraining root cause analysis.

- AI operational scope: AI-assisted features focus on guided configuration and troubleshooting rather than predictive analytics or remediation.

- Geographic concentration: Enterprise LAN adoption remains concentrated in Japan, limiting suitability for organizations seeking global execution.

Arista Networks

Arista Networks is a Leader in this Magic Quadrant. The company participates in the enterprise wired and wireless LAN market with Ethernet switching, wireless access points and the CloudVision platform for LAN operations. Arista primarily serves large enterprises, with strongest adoption in North America, and continues to expand campus deployments beyond its historical data center customer base. Gartner expects Arista to continue investing in AI-assisted LAN operations and in scaling sales and field execution.

- Operational coherence: Arista delivers wired and wireless campus networking through the CloudVision platform with integrated policy visibility and network detection and response capabilities.

- Assurance-led AI: Arista has delivered AI-assisted LAN operations focused on change validation, digital-twin testing, and AVA-based diagnostics across wired and wireless environments.

- Financial stability: Arista’s strong financial position and growing enterprise campus installed base support continued investment in its portfolio.

- Campus market awareness: Enterprise buyers frequently associate Arista with data center networking, resulting in lower initial awareness of its campus LAN offerings.

- Large enterprise alignment: Arista’s campus LAN portfolio is primarily aligned to large enterprises and may be less attractive for price-sensitive or smaller campus refresh cycles.

- Global adoption: Enterprise campus LAN adoption remains strongest in North America, which can limit familiarity and consistency of execution in other regions.

Cisco

Cisco is a Leader in this Magic Quadrant. The company participates in the enterprise wired and wireless LAN market through its Cisco Switching and Cisco Wireless portfolios, supported by cloud-based, on-premises and hybrid management platforms. Cisco serves large global enterprises across all major regions, with particularly strong penetration in North America and EMEA, and broad adoption across public-sector, financial services, healthcare, higher education and large commercial enterprises. Gartner expects Cisco to continue investing in AI-assisted LAN operations and in advancing platform integration across its portfolio.

- Integration progress delivered: Cisco has improved integration between Cisco Switching and Cisco Wireless across Catalyst and Meraki management, enabling increasingly consistent LAN operations across historically separate portfolios.

- Common AI foundation: Cisco has centralized its enterprise LAN portfolio around an AI-driven operating model based on a common IOS-XE foundation and Deep Network Model, supporting more consistent insight, validation and operator-initiated automation.

- Scale sustains execution: Cisco’s scale, enterprise installed base and global partner ecosystem support sustained execution of its converged wired and wireless LAN roadmap.

- Buying complexity: Gartner clients report increased purchasing complexity during enterprise LAN refresh cycles, particularly when transitioning between Meraki and Catalyst.

- Portfolio messaging: As Cisco integrates its enterprise LAN portfolio, some Gartner clients report less clarity around how traditional Meraki and Catalyst branding maps to offerings during refresh evaluations.

- Uneven AI delivery: Some elements of Cisco’s AI-driven LAN strategy are not yet consistently available across the enterprise LAN portfolio, limiting near-term operational impact for some customers.

Extreme Networks

Extreme Networks is a Visionary in this Magic Quadrant. The company participates in the enterprise wired and wireless LAN market with a campus-focused portfolio centered on Extreme Platform ONE, which integrates Ethernet switching, wireless access points, fabric networking and centralized LAN operations. Extreme primarily serves enterprise campus environments across North America and EMEA, with adoption most common in government, education, healthcare, manufacturing and retail organizations that prioritize high-density access and policy-centric operations. Gartner expects Extreme to continue investing in Extreme Platform ONE and AI-assisted LAN operations.

- High-density campus focus: Extreme focuses primarily on enterprise campus networking, aligning its strategy, portfolio and execution around high-density wired and wireless access for campus deployments.

- Platform ONE direction: Extreme has established Extreme Platform ONE as a unified, cloud-based control plane that integrates telemetry, policy, analytics and workflows, and underpins its expanding AI capabilities.

- Commercial flexibility: Extreme’s universal licensing and hardware model provides flexibility and predictability during campus refresh and upgrade cycles.

- Platform convergence ongoing: Extreme continues to operate both ExtremeCloud IQ and Extreme Platform ONE, which can slow the pace of feature maturity and coherence.

- AI operational scope: Extreme’s AI networking capabilities focus on diagnostics and guided assistance rather than closed-loop or autonomous LAN operations.

- Platform market visibility: Extreme Platform ONE positioning has limited visibility among Gartner enterprise clients, reducing awareness during campus LAN evaluations.

Fortinet

Fortinet is a Visionary in this Magic Quadrant. The company participates in the enterprise wired and wireless LAN market with an offering built around its Security Fabric architecture, including Ethernet switching and wireless access points that can be integrated with FortiGate firewalls through FortiLink. Fortinet serves midsize and large enterprises globally, with a strong installed base in North America, EMEA and the Asia/Pacific region. Fortinet’s enterprise LAN deployments are most common in industries such as retail, manufacturing, healthcare, financial services and government, where integrated security enforcement is a primary design requirement. Gartner expects Fortinet to continue investing in AI-assisted LAN operations and in extending FortiAIOps capabilities across its enterprise LAN portfolio.

- Security-led LAN differentiation: Fortinet approaches the campus LAN as an extension of enterprise security, with networking tightly aligned to policy enforcement.

- Security Fabric integration: Fortinet’s Security Fabric spans campus LAN, WAN and SASE, enabling consistent operations across networking and security domains.

- Distributed environment alignment: Fortinet aligns particularly well with distributed enterprises, branch environments and OT-adjacent use cases, where uniform security enforcement and consistency are prioritized.

- AI operational scope: Campus LAN operations are currently delivered through guided, human-in-the-loop workflows rather than closed-loop or autonomous automation.

- Firewall-centric control plane: In Fortinet’s primary architecture LAN telemetry and automation are anchored to the FortiGate control plane, which can constrain independent evolution of autonomous LAN operations.

- LAN positioning: The campus LAN is primarily positioned as part of the cybersecurity portfolio, which can reduce visibility among Gartner clients during LAN-first evaluations.

H3C

H3C is a Niche Player in this Magic Quadrant. H3C participates in the enterprise wired and wireless LAN market with a portfolio that includes Ethernet switching, wireless access points, campus segmentation capabilities and centralized LAN management through its AD-Campus architecture and Cloudnet platform. The company’s portfolio includes AI-assisted capabilities delivered through its LinSeer assistant. H3C primarily serves large enterprise customers in the Asia/Pacific region and supports on-premises and cloud-based deployment models. Gartner expects H3C to continue investing in AI-assisted networking capabilities and high-bandwidth campus switching.

- Centralized campus control: H3C delivers centralized management, integrated segmentation and troubleshooting capabilities that support large, policy-driven campus environments.

- Broad campus design: H3C aligns its campus LAN offerings to a wide range of design requirements, including fiber-to-the-desk and fiber-to-the-access-point architectures used to support physical security and scale.

- Sustained regional scale: H3C’s scale and continued investment in enterprise infrastructure support ongoing development and delivery of its campus LAN portfolio within its core regional markets.

- High Asia/Pacific concentration: Enterprise LAN adoption remains concentrated in China and select Asia/Pacific markets, limiting suitability for globally standardized deployments.

- AI operational scope: H3C’s AI-assisted networking capabilities are most effective for specific tasks, with more limited effectiveness in complex, end-to-end troubleshooting scenarios.

- Execution outside core markets: Service delivery, support quality and escalation processes can vary outside H3C’s primary regions, requiring buyers to validate consistency.

HPE

Hewlett Packard Enterprise (HPE) is a Leader in this Magic Quadrant. HPE participates in the enterprise wired and wireless LAN market through two networking portfolios: HPE Aruba Central and HPE Mist, both offered as enterprise campus LAN solutions following HPE’s acquisition of Juniper Networks. HPE operates Aruba Central and Mist as distinct enterprise LAN platforms connected by a common AI engine, Marvis, enabling buyers to select the platform that aligns with their architectural and operational preferences. The Aruba Central portfolio includes Ethernet switching, wireless access points, network access control and centralized LAN operations with an emphasis on on-premises management, while the Mist portfolio provides cloud-managed wired, wireless LAN, indoor location and NAC operations. HPE serves large global enterprises and public-sector organizations across North America, EMEA and the Asia/Pacific region. Gartner expects HPE to invest in integration across its enterprise LAN portfolios while advancing AI-assisted LAN operations.

- Enterprise buyer alignment: HPE aligns its enterprise wired and wireless LAN strategy closely with buyer demand for platforms that emphasize AI operations for assurance, automation and security at scale.

- Dual enterprise platforms: HPE offers two mature enterprise LAN platforms, HPE Aruba Central and HPE Mist, each capable of supporting large wired and wireless campus deployments via a common AI engine.

- Investment scale: HPE’s financial strength, global enterprise customer base and broad channel reach support sustained investment across its enterprise wired and wireless LAN portfolio.

- Platform selection required: HPE operates HPE Aruba Central and HPE Mist as parallel enterprise LAN platforms, requiring buyers to make a deployment choice that carries operational implications.

- Adoption decision scrutiny: Some Gartner clients that are new to HPE increase diligence during evaluations to validate roadmap and longer-term operational fit.

- Evaluation effort increased: While HPE provides positioning guidance for both HPE Aruba Central and HPE Mist enterprise campus platforms, there is additional evaluation effort required for buyers.

Huawei

Huawei is a Leader in this Magic Quadrant. The company participates in the enterprise wired and wireless LAN market through its CloudCampus architecture, including CloudEngine campus switches, AirEngine wireless access points and centralized LAN operations delivered via iMaster NCE-Campus. Huawei serves large enterprises, governments and public-sector customers in the Asia/Pacific region, the Middle East, Africa, Latin America and parts of Europe, where its enterprise networking portfolio is commercially available and supported. Gartner expects Huawei to continue investing in AI-assisted networking capabilities embedded within its campus LAN portfolio.

- Closed-loop automation: Huawei has implemented closed-loop analytics and AI-driven automation across both wired and wireless campus LAN environments, enabling policy-driven autonomous assurance and remediation workflows that extend beyond reactive diagnostics.

- Integrated campus architecture: Huawei delivers a full enterprise wired and wireless LAN portfolio through its CloudCampus architecture, integrating switching, Wi-Fi, campus segmentation, AI-driven operations and zero-trust security.

- Feature delivery pace: Huawei demonstrates strong execution in delivering new campus LAN capabilities, particularly in Wi-Fi sensing, Smart Anomaly Detection (SmartAD), AI-assisted operations, security automation and policy enforcement.

- Market availability: Huawei’s enterprise LAN offerings are unavailable in some regions due to regulatory, legal and geopolitical restrictions.

- Regional commercial variation: Country-specific sales, contracting and support models may result in uneven procurement experiences and execution consistency.

- Technical positioning: Huawei’s enterprise LAN positioning remains technology-centric, which can reduce resonance during evaluations focused on business outcomes.

Join Digital

Join Digital is a Niche Player in this Magic Quadrant. The vendor participates in the enterprise wired and wireless LAN market through its Graphite cloud-native operations platform, delivered primarily via a NaaS model and also available as a self-managed offering. Join Digital sources wired switches and wireless access points from open ecosystem partners, with differentiation centered on centralized operations, automation and service delivery rather than proprietary network operating systems. Join Digital primarily serves North American midsize and large enterprises with deployments commonly associated with commercial real estate, enterprise office environments and use cases requiring integration with IoT systems. Gartner expects Join Digital to continue investing in enhancements to its service-led operational capabilities as well as improvements to its Graphite platform, bringing more functional control into the software layer and relying less on specific hardware capabilities.

- Service-led operations: Join Digital’s NaaS model enables low-touch LAN operations for organizations seeking to reduce internal operational effort.

- Flexible consumption: Join Digital provides a stand-alone SaaS offering for self-managed LAN deployments, alongside a managed NaaS option supporting wired-only, wireless-only or unified environments.

- Operational experience: Service workflows and AI-assisted capabilities benefit from insights gained operating live enterprise environments at scale.

- Portfolio alignment: Join Digital’s open-standard approach may be less aligned to organizations that require vertically integrated campus networking architectures.

- Evolving self-managed capabilities: Join Digital’s self-managed capabilities are still evolving and may lack the LAN management capabilities required for some enterprises at campus scale.

- Enterprise visibility: Join Digital has lower visibility among Gartner enterprise clients and is less frequently evaluated in campus LAN procurement processes.

Meter

Meter is a Visionary in this Magic Quadrant. Meter participates in the enterprise wired and wireless LAN market through a subscription-based NaaS offering that combines networking hardware, software, connectivity, security and operations through a single cloud-managed system. The offering supports fully managed, co-managed and customer-operated deployment models while remaining delivered as a service. Meter primarily serves enterprises with distributed locations in North America, including retail, logistics and office environments. Gartner expects Meter to continue investing in AI-assisted LAN operations and enterprise security capabilities as it expands market adoption.

- Single-system architecture: Meter delivers the campus LAN as a tightly integrated system in which networking hardware, software, connectivity and operations are designed, deployed and managed as a unified environment rather than as discrete components.

- Production-derived automation: Meter embeds AI and a production-informed digital twin into its platform, using live operational telemetry to validate configuration changes and automate workflows with lower operational risk.

- Low-touch operations: Meter targets organizations seeking to materially reduce day-to-day network operations burden, supporting managed, co-managed and self-managed models without reverting to traditional management complexity.

- Full-stack adoption: Meter’s offering requires adoption of its full integrated stack, limiting suitability for organizations that seek multivendor flexibility or independent selection of LAN components.

- Segmentation architecture: Meter’s current LAN segmentation may be less fitting for organizations that require fabric-based segmentation across multiple sites.

- Enterprise visibility: Meter has lower visibility among Gartner enterprise clients and is less frequently shortlisted for campus LAN evaluations.

Nile

Nile is a Visionary in this Magic Quadrant. Nile participates in the enterprise wired and wireless LAN market through a secure NaaS offering delivered via a subscription model that includes switches, wireless access points and a cloud-managed operations platform. The offering is delivered as an operationally complete service that includes hardware, software, licensing, ongoing operations, and identity-centric access and segmentation applied by default. Nile primarily serves midsize and large enterprises across North America, with an expanding presence in Europe, Asia and the Middle East that seek to modernize or replace campus LAN environments using a service-based delivery model. Gartner expects Nile to continue investing in autonomous, AI-assisted LAN operations and in expanding its NaaS service capabilities to support broader enterprise adoption.

- Identity-centric LAN security: Included with its NaaS offering, Nile applies identity-based access control and segmentation by default across the LAN, enforcing least-privilege access without requiring separate NAC platforms or VLAN and ACL configuration.

- Consumption model: Nile delivers an outcome-based service, integrating wired and wireless infrastructure, segmentation, security and operations with a financially backed SLA.

- Hands-off automation: Nile supports automated assurance and optimization across the network life cycle through centralized telemetry and a continuously updated network digital twin.

- Full-stack adoption: Nile’s NaaS is best-suited to customers adopting a unified wired and wireless LAN and may be less well-aligned for organizations seeking long-term independent operation of LAN components.

- Device-level customization: Nile standardizes switch and access point configuration and management, which may reduce direct device-level control compared with traditionally operated LANs.

- Enterprise visibility: Nile has lower visibility among Gartner enterprise clients compared with incumbent vendors.

RUCKUS Networks

RUCKUS Networks is a Niche Player in this Magic Quadrant. The company offers enterprise wireless and wired LAN infrastructure, with centralized management delivered through RUCKUS One offering cloud-based and on-premises options. RUCKUS has a global footprint with strongest enterprise adoption in North America and EMEA, primarily serving hospitality, multiple-dwelling units, education housing and large public venues, where reliable wireless performance is a primary requirement. Gartner expects RUCKUS to continue strengthening business execution with ongoing investment in AI-assisted operations and targeted vertical solutions.

Belden announced its intention to acquire RUCKUS Networks from Vistance Networks on 30 April 2026. At the time of this evaluation and publication, however, Belden and RUCKUS Networks operated as separate legal entities. Gartner will provide further insight as more details become available.

- Wireless-first campus fit: RUCKUS designs its campus portfolio around wireless LAN as the primary access layer to deliver reliable WLAN service in dense environments.

- Guest and transient usage: The portfolio is commonly deployed in environments such as hospitality, venues, MDUs and education, where guest and short-lived access are a central operational requirement.

- AI-assisted WLAN operations: RUCKUS delivers AI-assisted wireless operations focused on WLAN optimization, monitoring and troubleshooting within its platform.

- AI operational scope: Support for some campuswide operational use cases may be more limited, particularly across wired environments.

- Support consistency varies: Gartner clients report variability in support delivery, requiring buyers to perform added diligence.

- Enterprise visibility: RUCKUS has lower visibility among Gartner enterprise clients and is less frequently considered during campus LAN evaluations.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

No vendors were added to this Magic Quadrant.

Dropped

The following vendors were dropped from this Magic Quadrant:

- Juniper Networks

- TP-Link

Inclusion and Exclusion Criteria

To qualify for inclusion, providers must:

- Demonstrate relevance to Gartner clients and adherence to the Market Definition’s mandatory requirements for the enterprise wired and wireless LAN market by offering both hardware and software, specifically:

- Enterprise Ethernet switching hardware

- Enterprise Wi-Fi access point hardware

- Enterprise LAN operations software (campus network applications): cloud, on-premises or hybrid offerings that provide centralized management, security and automation across the wired and wireless infrastructure

- Ensure required hardware and software are commercially available by 31 December 2025, including:

- Hardware: Enterprise Ethernet switches and Wi-Fi access points, plus any optional appliances

- Software: Enterprise LAN operations software (campus network applications)

All components must be publicly orderable, listed on a publicly published price list, in inventory and

available for shipment by the cutoff date. Capabilities becoming generally available after 31

December 2025 influences only the Completeness of Vision axis.

- Meet the following revenue and growth threshold requirements:

- Have customers in at least three of the following regions: North America, EMEA, Asia/Pacific (including Japan) and Latin America, with no more than 70% of annual revenue generated in any single region

- At least USD $200 million in annual enterprise wired and wireless LAN revenue and at least 200 enterprise customers using the offered products from 1 January 2025 to 31 December 2025

or

- At least USD $10 million in annual enterprise wired and wireless LAN revenue for the same period (2025) and 50% year-over-year growth

- Provide enterprise LAN operations software (campus network applications) that delivers unified discovery, configuration, policy enforcement, monitoring, real-time telemetry and automation across wired and wireless infrastructure, with integration into IT operations workflows.

- Offer integrated access security and segmentation, including authentication of users and devices and policy-based isolation for guest, IoT, and OT devices, with automated remediation capabilities.

Honorable Mentions

- TP-Link: This vendor has relevant technology and is investing in this market.

- Ruijie Networks: This vendor has relevant technology and is investing in this market.

Evaluation Criteria

Ability to Execute

Product or Service: We evaluate each vendor based on its overall enterprise wired and wireless LAN offerings, inclusive of both hardware and software. This assessment considers the breadth and depth of wired and wireless LAN functionality and the range of enterprise use cases supported. Specific functionality areas assessed include: wired LAN hardware portfolio, wireless LAN hardware portfolio, LAN infrastructure management, campus segmentation, zero-trust enforcement, guest connectivity, and AI and agentic automation.

Overall Viability: We assess the vendor’s overall financial health and its ability to sustain investment across marketing, sales, product development, and support, as well as the likelihood of continued commitment to growing and supporting its enterprise wired and wireless LAN business.

Sales Execution and Pricing: We assess the vendor’s pricing strategy and the effectiveness of its direct and indirect sales motions. This primarily includes an evaluation of pricing and licensing models offered to enterprise customers, including transparency, simplicity and perceived value. Sales execution considerations include the vendor’s go-to-market structure, sales enablement channel effectiveness, and consistency of execution across regions.

Marketing Execution: We assess the effectiveness of the vendor’s marketing programs, including the clarity, consistency and reach of its messaging across owned and external channels such as websites, events and digital media. This criterion emphasizes how well vendor messaging resonates with enterprise buyers, communicates differentiation and reinforces relevant outcomes. We also consider whether marketing investments are appropriate for the vendor’s scale and whether they translate into market awareness and consideration.

Market Responsiveness and Track Record: We assess the vendor’s ability to deliver relevant capabilities in alignment with evolving enterprise requirements, relative to competitors. This includes a review of the vendor’s historical responsiveness to changing market demands, delivery of planned capabilities and ability to address product limitations. While this assessment is primarily focused on product execution across hardware and software, it also considers alignment with broader market and architectural trends.

Customer Experience: We assess the full customer experience across presales and postsales engagement. This includes customer feedback related to evaluation, deployment, daily operations, hardware and software quality, and technical support. We also consider how the vendor manages customer experience at scale, including support structures, customer success programs and broader organizational practices that influence long-term satisfaction.

Operations: For this Magic Quadrant, operational execution was not directly evaluated, as it was determined to be less central to the primary technology and decision criteria for enterprise wired and wireless LAN buyers in this market.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | High |

Marketing Execution | Medium |

Customer Experience | Medium |

Operations | NotRated |

Source: Gartner (May 2026)

Completeness of Vision

Market Understanding: We assess the vendor’s ability to understand current and emerging enterprise wired and wireless LAN requirements. This includes awareness of operational, security and experience challenges that enterprises are seeking to address, as well as insight into how these needs are evolving. This increasingly considers how vendors distinguish between baseline AI-assisted capabilities (such as reactive diagnostics and recommendations) and emerging agentic approaches. We also evaluate the vendor’s self-awareness regarding its strengths and limitations, and its understanding of the competitive landscape and alternative approaches available to enterprise buyers.

Marketing Strategy: We evaluate the vendor’s ability to influence the future direction of the market through its messaging and marketing programs. This includes the strategy to invest in marketing and deliver concise, relevant and consistent forward-looking messages aligned to enterprise buyer personas.

We assess whether the marketing strategy is positioned to raise awareness, generate demand and establish thought leadership, and whether it effectively communicates differentiated value tied to enterprise outcomes.

Sales Strategy: We evaluate the vendor’s strategy for using direct and indirect sales channels, along with related investments, to acquire new customers and expand adoption within existing enterprises. This includes assessing how clearly and consistently the vendor articulates a sales approach that resonates with enterprise buyers, as well as how effectively it adapts sales motions and pricing approaches in response to evolving market and technology transitions.

Offering (Product) Strategy: We evaluate the vendor’s wired and wireless LAN product strategy, including key areas of focus and the most impactful planned enhancements on its roadmap. This assessment emphasizes the value of roadmap plans to target enterprise customers, the breadth of customers impacted and the timeliness of delivery relative to market needs. We also assess whether the vendor is addressing material gaps in its current offering. This criterion focuses on the vendor’s most consequential enterprise plans, not an exhaustive review of all roadmap items.

Business Model: We evaluate the design, logic and execution of the vendor’s business model to support sustained growth and long-term success. This includes alignment across positioning, packaging and pricing strategies, and how effectively the business model supports cloud, hybrid and on-premises deployment and consumption options in ways that align with enterprise expectations.

Vertical Strategy: We assess the vendor’s strategy for directing investment, product capabilities and dedicated resources to meet the needs of enterprises within specific industry segments. This includes evaluating the relevance of industry-specific offerings and the degree to which the vendor aligns its approach to the operational and regulatory requirements of targeted vertical markets.

Innovation: We evaluate the vendor’s plans to drive market innovation by introducing differentiated capabilities that deliver new enterprise value or address existing challenges more effectively. This assessment primarily emphasizes future innovation rather than current in-market capabilities. Innovation may span multiple areas, including product, pricing, go-to-market approaches and use-case expansion. We assess whether planned innovations are differentiated, credible and capable of shifting enterprise expectations or prompting competitive response, rather than representing incremental feature evolution.

Geographic Strategy: We assess the vendor’s strategy for sustaining and expanding enterprise adoption on a global basis. This includes evaluating how well the vendor addresses regional requirements through appropriate investments in localized support, documentation, services and product user interfaces, and whether its approach is credible and scalable across geographies.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Medium |

Sales Strategy | Medium |

Offering (Product) Strategy | High |

Business Model | Medium |

Vertical/Industry Strategy | Medium |

Innovation | High |

Geographic Strategy | Low |

Source: Gartner (May 2026)

Quadrant Descriptions

Leaders

Leaders demonstrate a strong ability to address current enterprise requirements while also influencing how buyer expectations and market priorities evolve over time. Leaders deliver mature, comprehensive offerings that support multiple enterprise use cases today and establish clear strategic direction that shapes future adoption patterns and evaluation criteria.

Leaders typically set the reference architectures, operational models or capability expectations that competitors respond to and buyers increasingly demand, translating vision into delivered capabilities through sustained execution. They benefit from strong visibility among customers and prospects, a sizable installed base, financial strength, and global presence, enabling them to scale innovation and shape market direction. Leaders continue to invest actively in their wired and wireless LAN portfolios but may not fully address the needs of more specialized segments, such as narrowly defined verticals, geographies or highly specific use cases.

Challengers

Challengers demonstrate a proven ability to meet current enterprise requirements in the market. Challengers typically have strong visibility among prospective buyers, a sizable installed base, financial strength and offerings that effectively support multiple enterprise use cases.

However, a Challenger’s strategy or roadmap is often narrower in scope or slower to reflect evolving market expectations compared with Leaders, making it less likely to shape or redefine the market’s direction. In some cases, larger vendors in mature markets are positioned as Challengers because they prioritize predictability and execution over aggressive innovation, choosing to minimize disruption for their existing customers or operating models.

Visionaries

Visionaries demonstrate a strong alignment with how the market is expected to evolve and often introduce new ideas, approaches or capabilities that address emerging use cases or long-standing enterprise challenges.

While Visionaries may present compelling strategies and roadmaps, they typically lack a consistently proven Ability to Execute at scale across the full set of enterprise requirements. This may be reflected in a more limited installed base, lower visibility among buyers, partial geographic coverage or incomplete breadth of capabilities. As a result, Visionaries often represent a higher-risk, higher-reward option for enterprises aligned with their direction and tolerance for execution variability.

Niche Players

Niche Players may be a strong fit for specific enterprise requirements. They typically focus on defined portions of the market, such as particular use cases, geographies, vertical industries or technology specializations.

While Niche Players ship viable offerings within their areas of focus, they have not demonstrated the ability to drive broader market direction or sustain execution across the full enterprise market. Limitations often become apparent outside their core focus, such as in breadth of functionality, geographic reach, customer coverage or scalability. These constraints can reduce their ability to address a wider range of enterprise needs or adapt as requirements evolve. However, for customers with requirements that align closely with Niche Players’ strengths, these vendors can represent an appropriate and effective choice.

Context

The enterprise wired and wireless LAN market is increasingly defined by operational outcomes. Infrastructure investment decisions are evaluated less by deployment success and more by how networks behave over time, including reliability in production, change safety and the consistent enforcement of zero-trust security across environments. As a result, enterprises are shifting from buying hardware and features to committing to outcomes that must be delivered and sustained over the full life cycle of the LAN.

This shift introduces tension between traditional hardware refresh drivers and rising expectations for software-driven operations. LAN switching and wireless hardware generally meets enterprise performance requirements, but hardware alone is not sufficient to meet buyer expectations. Value is determined by management, automation, telemetry and assurance capabilities, particularly their ability to reduce operational effort and risk.

In practice, operational outcomes are delivered by how infrastructure and software work together, not by the individual components alone. Some vendors will continue to innovate in hardware, silicon and network software in ways that expose richer telemetry and enable deeper interaction with management and automation. Client inquiry volume reflects high expectation and interest for AI capabilities and hands-off operations. Clients consistently describe self-driving networks as a desired destination, but one they expect to reach incrementally rather than through instant automation.

Most enterprise LAN offerings now include AI assistants that support task-oriented, reactive workflows such as diagnostics, correlations and recommendations. These tools are increasingly becoming viewed as baseline capabilities. In contrast, agentic NetOps represents a shift toward goal-based outcomes, where software agents reason over the network state, pursue defined objectives and act within guardrails to achieve operational intent.

Interest in hands-off operations is paired with skepticism about trust and control. Clients frequently question how consistently software driven actions will perform at scale, how decision boundaries will be enforced and how accountability can be maintained as responsibility shifts from human operators to agentic software.

As advances in AI software accelerate capability delivery, this skepticism is increasingly tied to operational coherence. The rate of capability delivery is expected to exceed most enterprises’ ability to absorb operational fragmentation. Vendor differentiation is therefore emerging around how offerings introduce new capabilities through a single, intelligible operating experience or deliver them across multiple operational surfaces.

Vendors that provide a consistent place to operate the network, with shared workflows, policy and validation, are better-positioned to translate innovation into usable outcomes. Where capabilities are delivered across multiple operational surfaces, adoption slows even when individual features are strong.

Across client interactions, a consistent set of priorities shapes enterprise LAN decisions:

- Modernization without increased operational burden. Enterprises seek to reduce hands-on troubleshooting, simplify change workflows and limit reliance on specialized expertise, particularly across distributed campus and branch environments.

- Lower-risk vendor commitments. Evaluation emphasizes roadmap continuity, architectural stability and the likelihood of disruptive migrations, especially amid consolidation or acquisition activity.

- Practical zero-trust execution. Organizations aim to extend identity-anchored access control and segmentation across wired, wireless and nonuser devices without introducing brittle designs or excessive operational overhead.

- Clear operational value from AI. Buyers look for evidence that AI capabilities improve diagnostics, change confidence or remediation speed rather than simply enhancing visibility.

- Intentional architectural differentiation by site. Enterprises reassess when fabric-based designs are justified and when simpler, internet-centric coffee shop models are sufficient, aligning investment to business impact and risk tolerance.

These priorities are reinforced by market dynamics. Enterprise LAN spending is expected to continue growing through 2026 and into 2027, driven primarily by replacement activity and technology transitions rather than new greenfield installations (see Forecast: Enterprise Network Equipment, Worldwide, 2024-2030, 1Q26). This means that many organizations will make material decisions under time pressure, with limited opportunity to revisit architecture or operating models until the next replacement cycle. The consequences of these decisions extend well beyond the immediate refresh window.

At this stage of a mature enterprise LAN market, innovation is increasingly concentrated around a smaller set of known outcomes focused on highly secure and more autonomously operated enterprise networks. In this market, vision is no longer evaluated as a broad set of ideas, but by how directly it will shape delivered capabilities.

Market Overview

Enterprise wired and wireless LAN purchasing continues to be driven primarily by refresh cycles. However, differentiation among vendors is increasingly influenced by how networks are operated and maintained over time rather than by speed of the deployment. Switching and Wi-Fi hardware capabilities generally meet enterprise requirements, and buyer evaluation now places greater emphasis on operational reliability, change safety and consistent security enforcement.

As a result, enterprise buyers increasingly evaluate LAN platforms as long-term operating environments rather than isolated infrastructure purchases. Client interactions consistently emphasize outcomes such as reduced time to identify issues, lower configuration drift and predictable change execution. Platforms that simplify operations and reduce operational risk tend to receive greater consideration than those that emphasize incremental feature delivery.

Operational Coherence

Operational coherence has become an important point of differentiation in the market. Vendors that deliver management, assurance, automation and security through a single operational interface are generally easier for enterprises to absorb and operate. Where capabilities are distributed across multiple management tools or control planes, adoption often slows, even when individual features are competitive. As a result, enterprises tend to adopt closed-loop and automated capabilities incrementally, favoring policy-bounded and scenario-specific execution.

This dynamic affects buyer confidence in automation and software-driven capabilities. Enterprises are typically more hesitant to rely on automation when operational workflows are fragmented or governance is unclear. As software capabilities continue to expand, the ability to introduce new functionality without increasing operational complexity is increasingly important.

AI-Assisted Operations and Agentic NetOps

AI-assisted LAN operations are now common across enterprise platforms and are increasingly viewed as baseline capabilities. Most offerings provide assistant-based functionality that supports diagnostics, event correlation and recommendations in response to operator input. These capabilities deliver value when they reduce troubleshooting time or improve operational visibility.

Closed-loop automation in enterprise LANs today is typically policy-bounded and use-case-specific rather than continuously autonomous. While several vendors demonstrate advanced validation and closed-loop workflows, only a small subset deliver materially hands-off operations across day-to-day LAN management.

Agentic NetOps represents a more advanced operational approach in which software agents reason over network state and carry out actions within defined guardrails. Current enterprise adoption remains limited and focused on specific use cases such as change validation, incident analysis and configuration drift detection. While interest is increasing, concerns related to trust, governance and accountability continue to constrain broader autonomous operation.

Zero-Trust Execution on Campus Networks

Zero-trust principles continue to influence campus LAN design and evaluation, although challenges are primarily operational rather than functional. Identity-based access control and segmentation capabilities are widely available across the market. However, many organizations encounter difficulty integrating these controls into routine LAN operations without increasing administrative effort.

Differences among vendors are more apparent in how access control and segmentation are implemented and maintained across wired, wireless and nonuser devices. Enterprises increasingly evaluate whether security controls function consistently during common activities such as onboarding, troubleshooting and network change.

Differentiated Architectures by Site

Enterprises are increasingly tailoring LAN architectures based on site requirements rather than applying uniform designs across all locations. Many office and branch environments adopt simpler, internet-centric designs that emphasize manageability and efficiency. In contrast, regulated, OT-adjacent and mission-critical environments continue to require architectures with higher levels of segmentation and control.

This reflects broader buyer behavior in which architectural complexity and operational rigor are aligned to business risk and site importance rather than applied universally.

Market Implications

Enterprise LAN spending is expected to remain closely tied to refresh cycles, with many purchasing decisions made under time constraints and limited opportunity for rearchitecture before the next upgrade.

As a result, enterprises place increasing weight on the long-term operational effects of platform decisions.

Innovation in this market is concentrated around improving security posture, reducing operational effort and introducing greater levels of automation while maintaining control and predictability. Differentiation among vendors is increasingly driven by the ability to deliver consistent operational outcomes over time rather than by the breadth of available features.

To inform this research:

- Gartner analysts conducted approximately 1,500 discussions on the topic of wired and wireless LAN and associated technologies with clients/prospects in 2025 (i.e., client inquiry, conference one-on-ones).

- All vendors in this research responded to a request for information (RFI) regarding current and planned capabilities, and a video submission following a script that demonstrates current product capabilities.

- Gartner analysts reviewed relevant reviews from Gartner Peer Insights.

- Gartner analysts reviewed publicly available information, including blogs, product specification sheets and financial information regarding vendors and products in this market.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.