Magic Quadrant for Search and Product Discovery

22 June 2026 - ID G00839916 - 44 min read

By Mike Lowndes, Sandy Shen, and 2 more

Search and product discovery solutions provide class-leading innovations, such as natural language processing, intent detection, algorithmic merchandising, and agentic integrations. Digital commerce leaders can use this research to improve engagement, conversion, and revenue without rebuilding entire commerce stacks.

Strategic Planning Assumption

By the end of 2027, at least one new AI-based conversational UI in search and product discovery (S&PD) will disrupt traditional search and browse UIs, penetrating at least 10% of a market worth nearly $18 billion in 2025.

Market Definition/Description

Gartner defines search and product discovery as applications that augment digital commerce solutions to facilitate navigation, filtering, comparisons and, ultimately, selection of products. They provide search (keyword, semantic and visual), merchandising (automation, configuration and curation of business rules) and product recommendations. These applications also provide catalog navigation (including SEO keyword automation and guided selling assistants). Personalization, optimization and analytics capabilities should also be available. Platforms are deployed as SaaS. They provide administrative tooling to enable digital commerce roles (merchandisers, content managers and search specialists) to support customer experiences via no-code. With the emergence of generative AI, conversational search and guided selling assistants are now appearing.

Search and product discovery applications can provide the digital customer journey from landing on a website or app to finding the correct product and adding to basket. Search results can be highly visual, using engaging layouts and multimedia. Content other than product information, such as educational information, compliance materials, customer reviews and related news may also be included in search results to engage customers and further support buying decisions.

Mandatory Features

The mandatory features for this market include:

- Product search (keyword)

- Semantic search support (natural language processing [NLP] and vector embeddings)

- Type-ahead/rich autocomplete

- Search analytics

- Results personalization

- Rule-based, curated and algorithmic merchandising

- Product recommendations (contextual, product substitution, complementary, etc.)

- Catalog navigation (browse) replacing a static taxonomy up to (but not including) product detail pages (PDPs)

Optional Features

The optional features for this market include:

- Advanced semantic search via natural language technologies, vector embeddings and/or graphs to understand query intent and map products to that intent

- Automated SEO content creation for product lists for category landing pages and subcategory product listing pages (PLPs)

- Productized integrations to digital commerce platforms

- Content search and other content types integrated with product search

- Optimization: A/B and multivariate testing (MVT) of ranking rules and merchandising

- Visual search

- Guided selling assistants and conversational discovery

- On-site retail media support

- Catalog enrichment/product data normalization

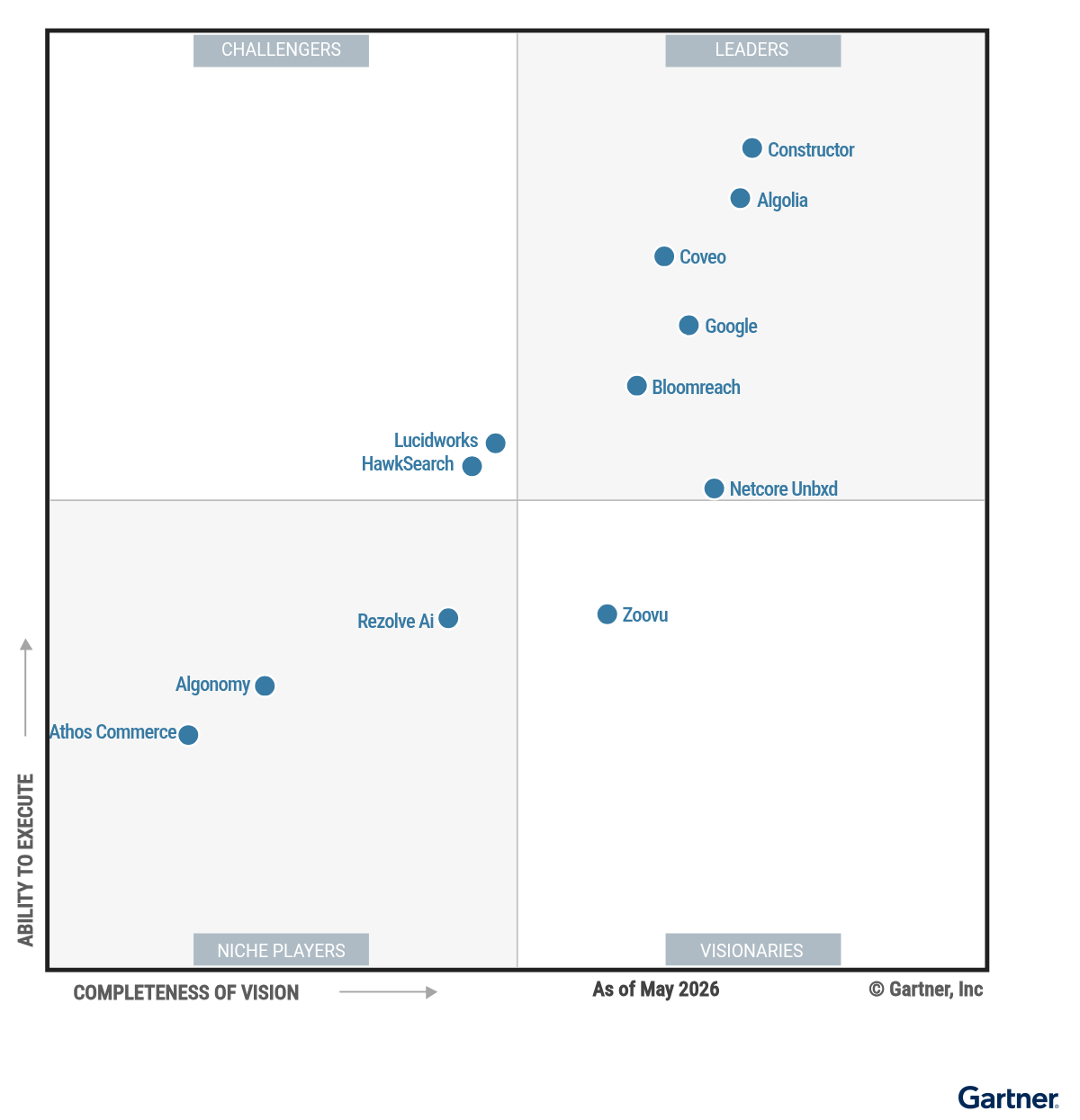

Magic Quadrant

Vendor Strengths and Cautions

Algolia

Algolia is a Leader in this Magic Quadrant. Headquartered in Palo Alto, California, its multitenant SaaS platform runs on Amazon Web Services (AWS) or Microsoft Azure and uses Google Cloud for some capabilities. Its capabilities are bundled into three modules: AI Search, Algolia Recommend, and Generative Guides for GenAI-based product finder capabilities. Pricing is based on API usage, with volume discounts available across three capability tiers. Limited free access is offered for developers.

Algolia has a strong presence in North America and Europe, with some presence in APAC and LATAM. It serves a wide range of industries, primarily focused on the retail, wholesale, manufacturing, and services verticals. Roughly 50% of its clients are noncommerce.

Algolia’s roadmap includes investments in its Agent Studio, tools for monitoring agentic uses and multiagent memory, enhancements to its suite of AI assistants, and Search Autopilot for recommendations and results ranking.

- Innovation: Algolia is fully embracing the shift toward GenAI-powered and agentic discovery experiences, with investments in features supporting answer engine optimization (AEO) and the Universal Commerce Protocol (UCP). Organizations looking to modernize their on-site discovery strategies can use these tools to deliver intuitive and conversational experiences to their users.

- Market dominance: Algolia retains its dominance in terms of total customers and revenue, putting it in a good position to remain relevant and continue innovations as the market evolves.

- Indexing flexibility: The schemaless nature of the proprietary index eases ingestion of catalogs and other types of content, as it is not limited to strict or normalized formats.

- GenAI strategy: Algolia supports search via conversational UIs but does not offer a packaged large language model (LLM) solution of its own. This bring-your-own-LLM strategy may suit enterprise customers but may fail to meet the needs of organizations looking for packaged solutions.

- Pricing: Algolia’s product pricing offers limited modularity, and Gartner clients have indicated that the platform can become expensive as usage scales. This rigid pricing structure can unexpectedly increase the total cost of ownership (TCO) for growing organizations.

- Visual search: Algolia lacks native visual recognition, feature detection, and extraction capabilities of its own. Organizations with advanced visual search requirements must rely on third-party solutions.

Algonomy

Algonomy is a Niche Player in this Magic Quadrant. Headquartered in San Francisco, California, and Bangalore, India, its multitenant SaaS platform runs on a private cloud, complemented by some capabilities on Azure. It includes modules such as Find (search), Discover (browse), Recommend, Catalog Enrichment, and Agentic Commerce (chat). Pricing is primarily usage-based (charged by API calls for Find and Discover, user sessions for chat, and annual page views for Recommend).

Algonomy has a strong presence in North America and Europe and serves a range of industries, primarily midsize to large enterprise retail organizations.

Its roadmap includes investments in AI-generated dynamic faceting and sorting, real-time hybrid search with a shared embedding model, AI-based search configuration, native visual search and “shop the look,” and multimodal search.

- Innovation: Algonomy demonstrates responsiveness to future trends by investing in features like voice support and GenAI product discovery. Organizations looking to bolster their commerce strategies can leverage the platform’s AI capabilities to deliver features such as conversational discovery and visual recommendations to their users.

- Flexible pricing: The vendor’s usage-based pricing framework accounts for varying industry profiles (e.g., high-volume grocery versus low-volume luxury), regional indexing, and SKU counts, providing prospective buyers with the ability to scale costs appropriately for customer size.

- Native real-time personalization: Algonomy provides one-to-one personalization supported by an integrated, real-time customer data platform (CDP), using clickstream data, affinity metrics, and “wisdom of the crowd” to rerank results based on shopper behavior. This allows customers to deliver highly tailored shopping experiences that can improve user engagement and conversion rates.

- Sales strategy: Algonomy relies on a predominantly direct-sales channel and is only available on a single cloud marketplace. Because of this constrained growth and limited geographic presence, prospects outside of its core markets may face a lack of trained staff and implementation partners.

- B2B functionality: Algonomy lacks key capabilities such as AI-driven merchandising automation; the ability to boost, bury, or hide products via AI; sophisticated account-based pricing and segmentation; and product search by weight or pack size. This limitation can deter larger B2B customers that require these features to support complex operations.

- Manual merchandising and analytics tools: The platform lacks AI-driven automation for merchandisers, relying instead on manual rule management, boosting, and slider controls. Similarly, the analytics and A/B testing lack next best actions (NBAs), optimization algorithms, or an AI copilot, forcing merchandising teams to rely on manual processes that can hinder operational efficiency and campaign optimization.

Athos Commerce

Athos Commerce is a Niche Player in this Magic Quadrant. Headquartered in San Antonio, Texas, its multitenant SaaS platform runs on AWS and includes Site Search, Merchandising, Personalization, Analytics, and Predictive Product Bundling. Athos also sells a product data feed and syndication platform from its acquisition of Intelligent Reach. Pricing has three tiers, with the Expert tier offering the full AI platform for enterprises. It combines a fixed fee with usage rates based on domain, session, and catalog size.

Athos has a strong presence in North America and APAC (mostly Australia), with a customer base in EMEA due to its acquisition of Klevu in 2025. It serves a range of industries, primarily small and midsize businesses and midtier segments in the retail, brand, automotive, healthcare, and high-tech sectors.

Its roadmap includes investments in hybrid search, AI support for configuration, and visual search.

- Market responsiveness: Athos is on a multiyear journey to bring its next-generation platform vision to market and is releasing new features regularly. Its “search is the feed” strategy is highly relevant as product discovery shifts to AI platforms, social media, and marketplaces.

- Pricing and packaging: Athos provides a streamlined, packaged solution tailored for midtier retailers and brands. This straightforward approach allows prospective buyers to easily predict costs and adopt the platform without navigating complex purchasing agreements.

- Data sovereignty: Athos provides regional cloud hosting across North America, EMEA, and APAC, supporting data sovereignty (when required) and regional compliance.

- Product strategy and go-to-market (GTM): Athos is fundamentally a renamed Searchspring, with integration features from Klevu; most existing customers are still on one of the previously branded, geographically separated products. The slow migration of clients to its rebranded platform creates confusion over the GTM, leaving prospective buyers with uncertainty regarding the unified product roadmap.

- Complex implementations: Athos is mainly focused on midtier retailers and brands. As a result, the platform may not be suitable for customers with complex requirements or those requiring sophisticated B2B search capabilities.

- Limited advanced search capabilities: Athos is still developing its hybrid (combining keyword and vector embedding support) and visual search solutions. Organizations that require strong, multilingual natural language understanding, intent detection, or image-based search out of the box need to carefully consider the capabilities available.

Bloomreach

Bloomreach is a Leader in this Magic Quadrant. Headquartered in Mountain View, California, its multitenant SaaS platform runs on AWS and Google Cloud and includes modules such as Search, Categories, Recommendations, Conversational Agent, and Web Personalization, bundling its AI capabilities onto Loomi AI. Pricing is tiered and scale-based, determined by a combination of monthly unique visitors and indexed document count, rather than API consumption limits.

Bloomreach has a strong presence in North America and EMEA. It serves a range of industries, primarily upper midmarket and enterprise organizations in the retail and B2B manufacturing sectors.

Its roadmap includes investments in a full-page conversational search experience, profile-based one-to-one personalization utilizing CRM data, autonomous self-optimizing search agents, LLM-based query understanding, and agentic integrations.

- Global operations: The vendor’s expansive ecosystem allows customers to easily integrate the platform into their existing architecture while benefiting from flexible procurement options. Supported by a global partner network, Bloomreach centers its strategy on integration with digital commerce platforms and co-selling with system integrators (SIs), data warehouses, and major cloud hyperscalers (including availability on AWS and Google Cloud).

- Innovation: Bloomreach is committed to enhancing AI and agentic capabilities with investments in conversational MCPs for agentic apps, check-out integrations with PayPal and Shopify, and an agentic orchestration layer that treats search, catalog, and content as intelligent tools.

- Merchandising and B2B capabilities: Bloomreach maintains comprehensive catalog and merchandising tooling, including visual merchandising, conditional slotting, and dynamic category management. It also natively supports robust B2B features, such as SKU part search, product variant grouping, and complex unit-of-measure conversions.

- Complex pricing model: Pricing is scale-based, requiring a complex pricing matrix, with AI tools, visual search, and content search treated as paid add-ons rather than bundled features. While this might provide flexibility for enterprise buyers, it may be more complex for those seeking more packaged solutions.

- AI/algorithmic merchandising: The platform leans on curated manual merchandising of results, which can potentially hinder operational efficiency and increase manual workload. However, using vector search brings some AI merchandising functionality.

- Narrow AI feature set: Bloomreach’s vision for AI-driven capabilities, the Loomi.ai intelligence layer, is not yet clearly reflected in the breadth of features supported for S&PD. It powers hybrid search integration but is otherwise currently limited to a guided selling assistant, analytics assistant, AI recommendations, and autosegmentation. This disconnect means that prospects should carefully consider the vendor’s AI roadmap for S&PD features versus that of other leaders.

Constructor

Constructor is a Leader in this Magic Quadrant. Headquartered in San Francisco, California, its multitenant SaaS platform is cloud-agnostic but typically runs on AWS or Google Cloud. Modules include Search, Autosuggest, Browse, Collections, Recommendations, Quizzes, and Retail Media. Pricing is a flat subscription fee, and invoicing is driven by forecast API calls, which are determined through a multiweek proof of concept to estimate usage and immediate ROI.

Constructor has a strong presence in North America and Europe and is growing in other regions. It serves a range of industries, typically global retail organizations and a growing number of B2B customers.

Its roadmap is one of the most comprehensive found in this research, including investments in agentic readiness, query pipeline refinement, personalization, merchandising, and AI assistants.

- Growth and momentum: Constructor has expanded its vertical coverage beyond its historical focus on large enterprise retailers, enabling support for a broader range of industry requirements and organizations.

- Core search innovation: Constructor layers its Discovery Reasoning Engine over a hybrid AI query pipeline to provide clear explanations for its ranking and relevance outputs. Alongside its ROI-oriented optimizations and AI assistant investments, Constructor’s innovation in core search capabilities remains strong.

- Retail media integration: The end-to-end Retail Media platform is unique in this research. For organizations looking to manage extensive sponsored product merchandising, including the selling of placements, this native capability may be attractive.

- Premium price: Constructor’s platform is among the most expensive in this research. While it may have differentiating features, pricing can be an issue for some organizations.

- Integration and personalization: The platform’s strict focus on commerce search means that integration of different content types and experiences falls below that of some of the broader platforms in this research. The “zero first-party data” approach can restrict the advanced personalization strategies typically enabled by native or adjacent CDPs, though Constructor can accept external signals once customers are authenticated and consenting.

- Conversational UI: Though Constructor fully supports natural language search, it has yet to show full integration of a conversational UI option into the main search experience or provide the adaptive experiences that some competitors offer.

Coveo

Coveo is a Leader in this Magic Quadrant. Headquartered in Quebec City, Canada, its Coveo for Commerce is a multitenant SaaS platform that runs on AWS and includes modules such as Coveo Search, Product Listing, Recommendations, and Merchandising Hub as part of its base package. Pricing is a consumption-based, query-per-month model for its base package, with add-ons charged as a percentage of the base cost (except the conversational modules, which have a consumption-based pricing structure).

Coveo has a strong presence in North America, followed by Europe, with a small presence in APAC. It typically serves customers with more than $1 billion in online sales in the manufacturing, retail, and high-tech distribution.

Its roadmap includes investments in the agentic space, with capabilities around autonomous agents in the merchandising process. It also includes expanding agent-to-agent orchestration and interoperability features and improving other core search capabilities around advanced query understanding and multimarket search support.

- Breadth of capabilities: Coveo offers a wide range of features across Search, Merchandising, Recommendations, Analytics, and Optimization, making it suitable for diverse client needs.

- Market responsiveness: Coveo’s versionless platform ensures all customers are on a single codebase, with multiple daily deployments and frequent releases that deliver regular updates and patches.

- Strong vertical coverage: Coveo serves B2C and B2B clients almost equally, supporting a wide range of use cases across industry verticals and along the customer journey.

- Regional support limitations: The majority of Coveo’s client base and staff are in North America and Europe, with some presence in APAC (mostly Australia and New Zealand). Organizations in other regions should confirm available support and references.

- Pricing complexity and add-ons: Coveo’s pricing model and commerce add-ons can increase the TCO and cause customers to exceed usage estimates. While product modularity may be attractive to organizations with complex requirements, it may not suit those looking for more packaged solutions.

- Lengthy and costly deployments: Deployments often take longer and cost more than average for this market, typically requiring specialized SIs, which can delay time to value.

Google is a Leader in this Magic Quadrant. Headquartered in Mountain View, California, its Gemini Enterprise for Customer Experience is a single-tenant or multitenant SaaS platform on Google Cloud. Its search and product discovery solution is part of Gemini Enterprise for Customer Experience, which includes AI Commerce Search, a Shopping agent, and CX Agent Studio. Pricing is based on query volumes for commerce search and conversational sessions for the Shopping agent and Agent Studio.

Google has a global presence and serves a range of industries, typically retail industries with customers of all sizes.

Its roadmap includes investments in merchant UIs for real-time pricing and inventory, agent suggestions on product pages, and advanced analytics for shopping agent.

- Unified experience and journey: The solution dynamically invokes product grid or conversational experience based on user intent, and the Shopping agent supports a multichannel experience across the full buying journey, spanning product discovery, purchase, and service. This allows customers to offer one agent for all customer-facing use cases.

- AI models and shopping graph: Google uses several AI models for relevance, ranking, and personalization, and supports text, image, video, and voice in 40 languages. It leverages its shopping graph of 40 billion products and real-time Google Search signals for catalog enrichment and product ranking, delivering highly contextualized and relevant results.

- Growth: Google’s S&PD product query volume has seen significant year-over-year (YoY) growth, coming from both existing and new customers. Such growth can provide prospects with confidence in the product’s long-term viability.

- Retail focus: The solution primarily serves the retail industry, despite having customers in other verticals such as healthcare, financial services, and hospitality. Prospective buyers outside of retail must ascertain the suitability of the product for industry-specific needs.

- B2B search: The solution has limited functionality for B2B, such as variant grouping, SKU substitution, and catalog segmentation by role or business unit. B2B organizations may have to rely on customizations or third-party extensions, which may increase costs and time to value.

- AI merchandising: While the solution increased the options for manual controls over the previous year, it is built with AI-at-the-core merchandising with no support for integrated A/B testing. This can be a challenge for organizations preferring sophisticated manual merchandising configurations.

HawkSearch

HawkSearch is a Challenger in this Magic Quadrant. Headquartered in Des Plaines, Illinois, its SaaS platform runs on AWS and includes modules such as AI-Powered Search, Product Discovery, Recommendations, Merchandising Controls, Analytics, and Developer Tools. Pricing is consumption-based and takes into account the number of API calls per month, records, and attributes. The use of smart search features and units of measure for conversation modules are also separate pricing parameters.

HawkSearch has a strong presence in North America, with a smaller presence in Europe. It serves a range of industries, typically midmarket to enterprise organizations in the manufacturing, distribution, and life sciences sectors.

Its roadmap includes investments in AI, such as a B2B search assistant, analytics assistant, and agentic commerce. HawkSearch is also planning on improving its native experimentation capabilities.

- B2B focus: HawkSearch specializes in complex B2B verticals with tailored Industry Accelerators, offering prebuilt synonym dictionaries and dimensional setups for sectors like electrical, plumbing, HVAC, and automotive.

- Transparent pricing: HawkSearch offers modular pricing with a standard rate calculator, giving prospects clear investment details, implementation steps, and available add-ons.

- B2B AI alignment: HawkSearch’s AI features respect B2B rules for entitlements, pricing, and inventory. These robust features support complex B2B search experiences.

- Proof of scale: HawkSearch mainly serves mid- to lower-enterprise B2B verticals, resulting in a smaller market footprint. Organizations in larger enterprise segments or different industries may find the platform lacks the proven scale or out-of-the-box capabilities needed to support their unique requirements.

- Global support: HawkSearch’s client base and staff are primarily in North America. Prospective customers in other regions may face challenges with localized support and regional references.

- Limited partner ecosystem: HawkSearch relies on a small group of integration partners with trained personnel. This limitation can restrict prospective customers’ options for deployment and potentially delay implementation.

Lucidworks

Lucidworks is a Challenger in this Magic Quadrant. Headquartered in San Francisco, California, its multitenant, single-tenant, or hybrid SaaS platform runs on Google Cloud and AWS. It includes modules such as Neural Hybrid Search, Lucidworks AI, Signals, and Studios. Pricing is subscription-based, determined by query volume, API calls, SKU count, index scale, or search volume.

Lucidworks has a strong presence in North America, with small bases in EMEA, LATAM, and APAC. It serves a range of industries, typically midsize to large enterprise organizations in the retail, finance, and manufacturing sectors.

Its roadmap includes investments in enhanced part number search, UI Studio, advanced ETL indexing, Commerce Studio, and Conversational Q&A AI Agent. It also includes long-term GenAI initiatives, such as “Luci,” a context-preserving AI shopping assistant, Agentic Commerce workflows, AI-driven catalog intelligence, and autonomous relevance optimization.

- Enterprise deployments: Lucidworks leverages a large enterprise-focused direct sales team and global partner ecosystem to give customers the customization and scalability needed for complex enterprise requirements.

- Geographic presence: Lucidworks maintains a global partner ecosystem across North America, LATAM, Europe, and China, with a robust sales channel strategy that prioritizes enterprise alignment, technical collaboration, and partner-supported delivery to address commerce search and discovery programs at scale.

- Strong B2B capabilities: Lucidworks excels in B2B scenarios, featuring robust support for entitlements, part and partial part number searches, product grouping, and measurement unit conversions. Its Dynamic Index keeps index sizes small by injecting customer-specific pricing and inventory availability at query time rather than preindexing every permutation.

- Product packaging: Lucidworks blends its product with a service-led approach. While this appeals to organizations with complex objectives, it is less suitable for those seeking a more packaged, out-of-the-box solution.

- Weak native personalization: The platform’s personalization is simple, relying heavily on “wisdom of the crowd” and general trending signals rather than delivering sophisticated, one-to-one personalized experiences.

- No AI copilot for merchandisers: The absence of an AI assistant within the Commerce Studio or Analytics Studio results in merchandisers having to manually manage rules and processes rather than having AI assist and automate their workflows.

Netcore Unbxd

Netcore is a Leader in this Magic Quadrant. Headquartered in San Mateo, California, its multitenant SaaS solution can run on AWS, Google Cloud, and Azure. It offers modules such as Search, Browse, Recommendations, Catalog Enrichment, Visual Search, and AI Agents. Pricing is based on the number of modules, websites, API calls, SKUs, languages, and conversations, with add-on modules and services costing extra.

Netcore has a strong presence in North America and a growing presence in EMEA and Asia. It serves a range of industries, typically retail and wholesale/distribution verticals and midsize to upper-midsize organizations.

Its roadmap includes investments in adaptive product detail pages, context graphs to link product attributes with use cases, and digital persona simulation.

- Expanding global footprint: Netcore saw double-digit growth for customers and revenue in 2025 and has increased its presence in EMEA and LATAM. This sustained growth provides prospects with increased assurance of the vendor’s stability and its ongoing commitment to expanding its global footprint.

- Portfolio approach: The vendor offers a broad portfolio that extends product discovery and insights into multiple direct and indirect channels, enabling better control of the branded experience and investment ROI.

- Agentic capabilities: Netcore offers multiple agentic capabilities for customers, including shopping and stylist agents, and merchandisers doing promotions, enrichment, data explanation, insights, and integration with AI (answer engine) platforms.

- Limited industry focus: Netcore primarily serves midsize to upper-midsize organizations. It has clients in the retail, automotive, and service sectors, and to a lesser extent in B2B wholesale and distribution. Organizations outside these verticals may not find enough references in their industries.

- Complex pricing: Pricing is based on the number of storefronts, API calls, SKUs, and languages, with AI agent costing based on conversations. Other Netcore product modules use different metrics such as message volumes and a one-off enablement cost for quizzes. Prospects may have difficulty estimating TCO.

- AI enablement: While AI is used across a broad set of capabilities such as intent detection, search, ranking, and recommendation, the product requires manual configurations of models and strategies to be used in each case, and assessing the combination of multiple factors’ impact on search performance is not straightforward.

Rezolve Ai

Rezolve Ai is a Niche Player in this Magic Quadrant. Headquartered in London, England, and New York, its Brain Commerce platform is a single- or multitenant SaaS platform that can be deployed on AWS, Google Cloud, or Azure. In addition to Discovery AI, Rezolve also offers Conversational AI, Enrich AI, AEO/generative engine optimization (GEO), and Location Services. Rezolve pricing is based on monthly API query volume, with three pricing tiers to meet diverse customer needs.

Rezolve has a strong presence in Europe, followed by North America and APAC. It serves customers with online sales below $500 million and is expanding in the enterprise segment, typically organizations in the retail industry vertical. Rezolve made six acquisitions in 2025, including ViSenze (visual search and recommendations) and Crownpeak (Digital Experience Platform and Search from Fredhopper).

Its roadmap includes investments in Agentic Merchandising, integration into agentic protocols such as Agentic Commerce Protocol and UCP, and unifying merchant experiences across its acquired products.

- Global presence: Rezolve’s recent acquisitions have expanded its regional footprint, ensuring customers in all major markets benefit from improved support and accessibility.

- Expansion of digital commerce capabilities: Rezolve’s strategic acquisitions in 2025 and 2026 underscore its commitment to the digital commerce sector. The broader solution portfolio offers customers a range of discovery and transactional capabilities across the user journey.

- Strong retail focus: Rezolve’s primary customer base is retail, and its latest acquisitions have further strengthened its capabilities around merchandising and visual search, driving higher adoption rates compared to other evaluated vendors.

- Fragmented product portfolio: Rezolve’s portfolio includes multiple search platforms, such as Fredhopper, which is mostly EMEA-based, and GroupBy, which is mostly NA-based, ViSenze (APAC), and Advanced Commerce. This geographically fragmented product portfolio will require careful integration by Rezolve, and organizations should proactively assess roadmap, interoperability, and support risks to avoid future platform migration challenges.

- Product scope: Rezolve primarily serves the retail sector and is expanding into B2B, health, and fan engagement. Organizations in other industries, especially complex B2B and industrial distribution, should seek relevant customer references and clarify the product roadmap for nonretail use cases.

- Limited system integration ecosystem: Rezolve has a small pool of SI partners. Customers should request references and be prepared to collaborate directly with Rezolve’s product teams or rely on internal resources for implementation.

Zoovu

Zoovu is a Visionary in this Magic Quadrant. Headquartered in Boston, Massachusetts, its multitenant SaaS solution runs on Azure and includes modules such as Search Studio, Conversation Studio, Configuration Studio, Advisor Studio, and Data Platform. Pricing uses a credit-based system, driven by SKUs, query volumes, sessions, and skills. Zoovu acquired XGEN AI, an AI search and recommendations engine in May 2026. This was after the research deadline and does not form part of this assessment.

Zoovu has a strong presence in Europe and North America and serves a range of industries, typically in manufacturing, retail, and high-tech verticals.

Its roadmap includes investments in avatar and voice tools, GEO tools, and conversational insight, vibe merchandising, and experience building.

- Data enrichment: Zoovu has a product ontology spanning more than 17,000 product categories and 50,000 attributes and uses internet data and AI to enrich the catalog for both structured and unstructured data. This is a key capability supporting relevance and recommendations.

- Product finder: The capability can be dynamically invoked based on user intent, with the ability to show compatible products/bundles and real-time pricing/availability specific to an account or location. Quiz questions can be generated by AI and served in a dynamic order based on user behavior, improving add-to-cart and conversion rates.

- Growth in search: Zoovu has grown its search revenue to be close to its product finder business, which was the primary focus and revenue-generating product of the company. This expanded focus provides prospects with confidence in the vendor’s growing expertise as an end-to-end S&PD provider.

- Customer support limitations: Zoovu primarily supports customers via sales and technical support teams without a formal customer success role for all customers. Go-live readiness service, implementation support, and ongoing optimization services all cost extra. Customers with a small budget that expect extensive guidance during implementation and ongoing operation should plan accordingly.

- Geographic presence: Most of Zoovu’s customers are in Europe, North America, and Australia, where its implementation partners are based. Prospective customers in other regions may face challenges with the level of support needed to meet requirements.

- AI merchandising: Ranking is mostly driven by product attribute scores with manual configuration of rules and ML-based behavior signals, while the copilot offers guidance but lacks the ability to execute tasks. The lack of full back-office automation can force customers to rely on manual workarounds to identify opportunities or NBAs.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

No vendors were added to this Magic Quadrant.

Dropped

- FactFinder

- Nosto

- Yext

Inclusion and Exclusion Criteria

In addition to Gartner client relevance, as determined by analyst expertise and opinion, providers need the following to qualify for inclusion:

- Offer a minimum of one software as a service (SaaS) search and product discovery solution that is actively being sold.

- The search and product discovery solution must meet the market definition and stated functionality.

- The search and product discovery solution must support over 60 current production customers as of February 2026.

- Vendors must have onboarded more than 10 new production customers to their search and product discovery solution in calendar year 2025.

- The search and product discovery solution must serve customers in more than one unique industry sector. To qualify, the vendor must have a minimum of 5% of search and product discovery production customers in the sector.

- The search and product discovery solution must serve customers in more than one region. To qualify, the vendor must have a minimum of 5% of search and product discovery production customers outside their home region.

Honorable Mentions

The following vendors were considered for this evaluation but failed to meet the inclusion criteria due to low overall market awareness and market share.

Doofinder

Doofinder is an EMEA-based S&PD vendor providing modules, including AI Search, AI Assistant, Product Recommendations, Quiz Maker, and Category Merchandising, with productized integration into BigCommerce, PrestaShop, Magento Open Source, Shopify, and WooCommerce. Doofinder provides a fast, plug-and-play search and discovery platform for the midtier that requires no coding, with natural language processing for intent understanding, one-to-one personalization, visual and voice search capabilities, and search analytics.

Fast Simon

Fast Simon is a North America-based S&PD vendor providing AI-powered search, merchandising, personalization, visual discovery, and conversational commerce capabilities. The platform integrates with Shopify, Adobe Commerce (Magento), BigCommerce, and WooCommerce, and supports both no-code deployment and composable commerce implementations through APIs and SDKs. Fast Simon leverages shopper behavioral signals, catalog data, and real-time inventory availability to support natural language and multimodal search, automated merchandising, personalization, and AI shopping assistants. Fast Simon primarily serves midmarket and enterprise retailers.

Luigi’s Box

Luigi’s Box is an EMEA-based, S&PD vendor with six product modules: Search, Recommender, Product Listing, Shopping Assistant, Conversational Discovery, and Analytics, with productized integrations into digital commerce platforms including Shopify, Shopware, Adobe Commerce (Magento), WooCommerce, PrestaShop, BigCommerce, and commercetools. Its Search module combines keyword matching with vector-based hybrid search, while Conversational Discovery and the Shopping Assistant add natural language, dialogue-led product discovery and guided selling. The platform offers AI and natural language processing (NLP) capabilities, including optimizations for European languages, and supports both self-service and guided integration for the midtier and enterprise. It also extends into agentic commerce, exposing search and discovery to external AI agents via the MCP.

Voyado

Voyado is an EMEA-based vendor that also sells CRM, personalization, and loyalty products as part of its Agentic Suite. Voyado Product Discovery includes modules for intelligent site search and browse, product recommendations, personalized product discovery, algorithmic and agentic merchandising, category listings, and retail media. There are productized integrations into Adobe Commerce, BigCommerce, Centra, commercetools, Salesforce Commerce Cloud, Scayle, Shopify, and Shopware. Voyado provides a retail-trained AI that analyzes complex retail logic, balancing intent with critical business constraints like profit margins, stock levels, and product life cycles for larger retailers.

Evaluation Criteria

Ability to Execute

Gartner analysts evaluate providers on the quality and efficacy of the processes, systems, methods, or procedures that enable vendor performance to be competitive, efficient, and effective, and to positively impact revenue, retention, and reputation within Gartner’s view of the market.

Product or service: The core goods and services that compete in and/or serve the defined market. This includes current product and service capabilities, quality, feature sets, and skills. This can be offered natively or through OEM agreements and partnerships as defined in the Market Definition and detailed in the subcriteria. Representative analysis components include:

- Demonstration of product capabilities

- RFI responses on the product or service

- API scope and usage by customers

- Peer Insights data

Overall viability (of the business unit, finances, strategy, and organization) and financials: Viability includes an assessment of the organization’s overall financial health as well as the financial and practical success of the business unit. It weighs the likelihood that the organization will continue to offer and invest in the product as well as the product’s position in the vendor’s current portfolio. Representative analysis components include:

- Corporate growth trends in revenue and profitability

- Digital commerce search and discovery product growth trends in revenue and profitability

- Customer growth trends

- Global customer presence

Sales execution and pricing: The organization’s capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel. Representative analysis components include:

- Gross merchandise value segmentation

- Average deal size

- Pricing approach, flexibility, and simplicity

Market responsiveness and track record: The ability to respond, change direction, be flexible, and achieve competitive success as opportunities develop, competitors act, customer needs evolve, and market dynamics change. This criterion also considers the provider’s history of responsiveness to changing market demands. Representative analysis components include:

- Product enhancements delivered due to customer request

- Frequency of enhancements

Customer experience: The products and services and/or programs that enable customers to achieve the anticipated results with the products evaluated. Specifically, this includes quality supplier-buyer interactions, technical support, and account support. This may also include ancillary tools, customer support programs, availability of user groups, and service-level agreements. Representative analysis components include:

- Peer Insights data

- The availability and quality of support and online training

- The scope of customer success programs

Marketing execution: Marketing execution was not rated because for this market it does not help buyers when considering an S&PD product.

Operations: Operations was not rated because vendor operational models are very similar, leading to little differentiation.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | High |

Sales Execution/Pricing | High |

Market Responsiveness/Record | High |

Marketing Execution | NotRated |

Customer Experience | High |

Operations | NotRated |

Source: Gartner (June 2026)

Completeness of Vision

Gartner analysts evaluate providers on their ability to convincingly articulate logical statements. This includes current and future market direction, innovation, customer needs, competitive forces, and how well they map to Gartner’s view of the market.

Market understanding: The ability to understand customer needs and translate them into products and services. Vendors show a clear vision of their market. They listen, understand customer demands, and can shape or enhance market changes with their added vision. Representative analysis components include:

- The scope of the digital commerce search and discovery offering

- Track record of meaningful enhancements

Sales strategy: A sound strategy for selling that uses the appropriate networks, including direct and indirect sales, marketing, service, and communication. This includes partners that extend the scope and depth of the vendor’s market reach, expertise, technologies, services, and customer base. Representative analysis components include:

- Partner strategy

- Locations and span of sales team

Offering (product) strategy: An approach to product development and delivery that emphasizes market differentiation, functionality, methodology, and features as they map to current and future requirements. Representative analysis components include:

- The product roadmap vision

- Product roadmap details

- Differentiation of the search and product discovery vision

Vertical or industry strategy: The strategy to direct resources (sales, product, development), skills, and products to meet the specific needs of individual market segments, including verticals. Representative analysis components include:

- The scope of current industry-specific functionality

- The scope of planned industry-specific functionality

- The span of customers across industry verticals

Innovation: Direct, related, complementary, and synergistic layouts of resources, expertise, or capital for investment, consolidation, defensive, or preemptive purposes. Representative analysis components include:

- Planned capital investment in digital commerce search and discovery technology

- The ability to leverage cloud-native capabilities

- The use of emerging technology

- Adherence to modern architectural paradigms

Geographic strategies: The provider’s strategy to direct resources, skills, and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels, and subsidiaries, as appropriate for that geography and market. Representative analysis components include:

- The span of geographic locations

- The span of partner network

- Revenue and customers across geographies

Marketing strategy: Marketing strategy was not rated because for this market it does not help buyers when considering an S&PD product.

Business model: Business model was not rated because the business models are very similar, leading to little differentiation.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | NotRated |

Sales Strategy | Medium |

Offering (Product) Strategy | High |

Business Model | NotRated |

Vertical/Industry Strategy | Medium |

Innovation | High |

Geographic Strategy | Medium |

Source: Gartner (June 2026)

Quadrant Descriptions

Leaders

Leaders demonstrate the ability to provide a depth and breadth of functionality at scale. They deliver capabilities across multiple industries and business models. They provide sales and support services both directly and through an ecosystem of application, service, and integration partners. They innovate new products and product functionality, investments inside and outside core S&PD, and programs that improve customers’ ability to succeed. Leaders tend to be mature in a market, and also have financial, technical, and organizational viability, and consistently feature in Gartner clients’ evaluations of vendors. They often set the competitive benchmark against which other vendors measure themselves, but may not always have the most leading-edge technology.

Challengers

Challengers provide functionality that may have a narrower scope than Leaders in relation to serving the total addressable market, but do scale well within their scope. Challengers may focus on fewer industries, geographies, or business models. These vendors have a solid customer base, but they may not be the most innovative, or may only invest in innovation that is key to their target markets. They use their research and development resources, access to investment, profits, and market reputation to attract customers and execute well. Challengers often focus on a perceived high-growth or high-value sector of the market. They often invest heavily in technology to meet the needs of their target customers, and they have robust feature sets for the customers they serve.

Visionaries

Visionaries demonstrate the ability to disrupt through innovative approaches to S&PD. They may incorporate new technologies or architectural approaches into their products, use creative pricing strategies, or focus on a narrow market segment. They often win new customers quickly because they have identified an underserved niche in the market — one not addressed by Leaders or Challengers. Visionaries often have modern offerings but have yet to win large numbers of customers, and they often lack resources compared with larger companies. They also often have smaller partner networks and act as fast movers. Visionaries are often funded by venture capital or private equity companies, which provide the capital that enables them to invest in technology, sales, and marketing resources for continued progress.

Niche Players

Niche Players address a narrow band of the market, defined by industry, digital gross merchandise value (GMV), company size, region, technology capability, or a combination of these characteristics. They frequently provide cost-effective packaged solutions that are easy to use within the boundaries of complexity. They often target smaller or emerging-market opportunities, or smaller end-user companies. Niche Players often lack geographical or transactional scale, and attract a significantly smaller range of technology, implementation, or service partners. They lack the financial viability of Leaders and Challengers. Like Visionaries, Niche Players are often funded by venture capital or private equity companies, which provide the capital that enables them to invest in technology, sales, and marketing resources for continued progress.

Context

Buyers of S&PD products are either looking to replace a native search capability within a digital commerce platform or find a superior product to one they already have. They are looking to deliver and support a unique, compelling, and consistent customer experience (CX) across many channels, now including external and internal AI agents. Buyers are seeking more flexible and nimble implementations and postimplementation extensions that enable accelerated time to market, reduce the total cost of ownership, and deliver desirable digital business outcomes.

Increasingly, organizations are also looking for support for catalog enrichment, especially for natural language search and AEO, support for AEO itself via APIs and MCP, and emerging AI platform protocols.

The evaluation criteria emphasize the requirements for viability, future success, architectural vision, innovation, and breadth of capabilities — all of which provide essential context for buyers determining the best-fit vendor for their needs.

Ultimately, however, each buyer’s requirements are different. Organizations should match their own requirements for functionality, industry expertise, technology, and cost to the vendors’ offerings by using the companion Critical Capabilities for Search and Product Discovery to rank vendors’ products for each use case by weighting criteria to their needs.

Market Overview

Demand for differentiating S&PD continues to grow, especially with the shift toward GenAI platforms and the return of conversational commerce. A dedicated S&PD product is often seen as a relatively cost-effective way to provide optimal digital customer experiences in the path to purchase — without fully replacing an incumbent digital commerce or digital experience platform. S&PD helps organizations meet the demands of today’s B2B and B2C buyers.

Since the last round of research, indexes have become unified (both keyword and vector embeddings) to power natural language search and retrieval-automated generation (RAG) for many LLM-based GenAI use cases such as conversational commerce, and the need to power AEO has become paramount.

The digital commerce search market — valued at approximately $17.41 billion in 2025 — continues to experience rapid growth, driven by increasing demand for personalized search experiences and the rising popularity of digital commerce.1

Market Evolution

Relevance as a primary driver of results ranking has become highly commoditized and is not enough on its own. Personalized relevance — which uses customer behavior data in aggregate (sometimes called “wisdom of the crowd”) and real-time clickstream data — has been the standard and minimum expectation, but we are seeing an accelerated shift toward intent detection (which can include these signals) as the primary driver of improved outcomes. Despite its limitations for product search, keyword search (keyword matching) was the dominant search technology for many years. This was enhanced by NLU/NLP-based semantic search, which captures the meaning of multiword and natural language queries and returns more accurate results. Traditional NLP, such as named entity recognition, is still used, especially when paired with a knowledge graph of the search domain (e.g., a product catalog) to support inference and query reformulation for more accurate results.

Over the last year, rapid AI-driven innovation has occurred, and the market is currently reacting to the impact of GenAI platforms (answer engines), mostly around the introduction of MCP servers, GEO/AEO support, and the integration of conversational UIs to product discovery (and the wider customer journey).

Driven by the growing adoption of LLMs, graph, and vector databases — the market is projected to maintain a compound annual growth rate of 11.1% from 2025 to 2033, reaching $40.48 billion by 2033.1

Vector search (which refers to mathematically derived closeness of potential results to query intent) has become a foundational capability and a basic expectation in S&PD products, providing further improvements to semantic search. Hybrid search refers to the blending of this approach with keyword matching and graph, which also powers RAG for LLM-based use cases. Some vendors now pulled these separate data types into a unified index.

Other key market shifts contributing to the evolution of S&PD include:

- GenAI UI: Many vendors have experimented with new GenAI-based conversational UIs for discovery. Widely established and accepted patterns remain elusive. The whole industry is approaching an inflection point in the evolution of new discovery UIs (see GenAI Product Discovery Requires a New Digital Commerce UX). New UIs are hard to establish, and certain large vendors are likely to lead the way to general acceptance of hybrid visual and conversational discovery UIs.

- Guided selling assistants: Gartner has consolidated a fragmented set of use cases into guided selling assistants, a customer-facing offering that enables self-service product discovery and recommendations (see Hype Cycle for Digital Commerce, 2026). These may be separate customer journeys from a core search experience (typically at the category or even product level), but we increasingly expect them to be integrated into the core discovery experience.

- GenAI and agentic commerce: The emergence of conversational answer engines such as ChatGPT, Google Gemini, and Perplexity.ai, and the use of these platforms to discover products, is increasingly replacing traditional web search engines and even digital commerce catalogs. This shift from answer engine to agent may present an existential threat to the existing S&PD market and the traditional worldwide web of “pages.” However, at present, the majority of traffic to commerce sites and subsequent transactions are handled by human interaction, not AI agents. Organizations that need to provide and retain control over optimal first-party customer experiences and data will require discrete, brand-level S&PD experiences to reflect the new answer engine capabilities, at least in the medium term.

- SEO evolution into GEO and AEO: With product category and detail pages (PDPs) becoming landing pages, recommendations and other discovery elements must be optimized within those page types. These also need to become better at providing the content underpinning GenAI: SEO becomes GEO, AEO, and agent-oriented content (AOC), as content descriptions become more natural language and descriptive for easier LLM consumption. As GenAI platforms themselves crawl and interact with websites, having better product data will also remain critical.

- Catalog enrichment: Poor catalog data remains a problem for S&PD clients, particularly in B2B environments. While Gartner’s best practice places the management and enrichment of product data firmly in the product information management function, we recognize this is not always possible and does not always lead to improved search retrieval outcomes. Several S&PD vendors now include product catalog enrichment capabilities as part of their offerings.

- Algorithmic merchandising AI: This is increasingly automating merchandising, especially by using customer behavior and product conversion data. However, many organizations still seek to retain curated/visual merchandising as an important tool, as AI has yet to access business strategy, tactics, or the contents of warehouses.

- Retail media networks: The growth of retail media networks is impacting S&PD by requiring the facilitation of sponsored product placements. While curated merchandising can cover some of these requirements manually, organizations are increasingly seeking automation for sponsored product placements, integration with third-party network APIs, and the ability to auction placements.

- Live proof of concept (POC): Most organizations now demand to run some form of S&PD product A/B test as a POC, using tags to capture customer search data against an incumbent solution or against direct competitors. We now evaluate vendors’ ability to support this capability.

- Free API calls: More recently, many vendors have abandoned charging for subsequent autocomplete and search-as-you-type API calls, as this pricing model proved unpopular. Now, only the first query letter or letters (depending on the algorithm) are used to determine pricing.

Acronym Key and Glossary Terms

| API | Application programming interface |

| ARR | Annual recurring revenue |

| AWS | Amazon Web Services |

| B2B | Business to business |

| B2C | Business to consumer |

| CDP | Customer data platform |

| CMS | Content management system |

| CX | Customer experience |

| DACH | Germany, Austria and Switzerland |

| DXP | Digital experience platform |

| GMV | Gross merchandise value |

| GTM | Go to market |

| ISV | Independent software vendor |

| KPI | Key performance indicator |

| LLM | Large language model |

| MACH | “Microservices, API-first, cloud-native SaaS, headless” — the tagline of the MACH Alliance, an industry body dedicated to promoting this approach |

| NER | Named entity recognition |

| NLP | Natural language processing |

| PIM | Product information management |

| POC | Proof of concept |

| S&PD | Search and product discovery |

| SaaS | Software as a service |

| SKU | Stock keeping unit |

| SMB | Small and midsize business |

| UI | User interface |

This Magic Quadrant is based on primary and secondary research by Gartner. This research drew on, but was not limited to:

- Gartner Peer Insights reviews for “S&PD” posted during 2025 and the first three months of 2026

Other sources include:

- Recorded briefings and demonstrations in which the vendors provided Gartner with insights into their products’ capabilities

- Feedback about vendors and their products captured during thousands of conversations, and other interactions with users of Gartner’s client inquiry service in 2025 and the first three months of 2026

- Generally available sources of information

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.