Magic Quadrant for Finance and Accounting Business Process Outsourcing

24 June 2026 - ID G00839371 - 51 min read

By Jan Ambergen, Emily Connelly

With the rapid evolution of finance technology, outsourcing partners provide CFOs with opportunities to unlock innovation, streamline processes, and drive sustainable cost savings. CFOs can use these insights to assess F&A BPO providers’ capabilities in adopting advanced automation, analytics, and AI.

Market Definition/Description

Gartner defines finance and accounting (F&A) business process outsourcing (BPO) as the use of third-party outsourcing service providers to execute transactional finance processes, including purchase-to-pay (P2P), order-to-cash (O2C), and record-to-report (R2R). BPO service providers remotely connect to clients’ systems to carry out these operations. They can also offer proprietary or partnered process automation solutions to enhance transactional processing efficiency. F&A BPO services are typically delivered from global delivery centers.

F&A BPO providers deliver transaction processing services for P2P, O2C and R2R, leveraging advanced automation technologies. In addition to running these services, providers also offer innovative solutions and transformation expertise to enhance process efficiency and support the ongoing maturation of finance operations.

At a minimum, an F&A BPO provider processes finance activities via a remote connection to its customers’ existing systems. Providers employ the required staff, often located in global delivery centers, to deliver these services. Cost savings and efficiency gains are passed on to the buyer in the form of labor arbitrage.

Enhanced F&A BPO offerings that meet finance’s need for more automated transactional processing focus on providing process transformation expertise, often combined with proprietary or partnered process automation technologies, including the use of AI and machine learning (ML). Through agreements with F&A BPO providers, buyers can streamline finance processes, adopt automation technologies that reduce manual intervention, and reduce processing costs through both operational excellence and ongoing innovation.

Mandatory Features

The mandatory features for this market are:

- Connectivity solutions for providers to access clients’ existing systems.

- Offerings that cover two of the following three processes, including all associated subprocesses:

- Purchase-to-pay, including supplier or vendor master data management, purchase orders processing, invoice processing, payment selection, and accounts payable query support.

- Order-to-cash, including customer order management, customer master data management, billing invoice processing, credit and collection management, dispute resolution, cash allocation, and accounts receivable query support.

- Record-to-report, including financial journal entry management, period close management, statement processing, controls and compliance, and transaction analysis.

Optional Features

The optional features for this market include:

- Finance process automation technology solutions, either proprietary or partnered, for P2P, O2C, and R2R, which include workflows that embed the use of AI and ML capabilities.

- Finance process automation services, which involve the provider offering transformation expertise to manage transformation programs across P2P, O2C, and R2R.

- Predictive forecasting and reporting through advanced analytics, AI, and ML to deliver real-time insights, scenario modeling, and forward-looking financial analysis.

- Compliance and controls frameworks to ensure regulatory adherence, risk mitigation, and operational integrity across core finance functions.

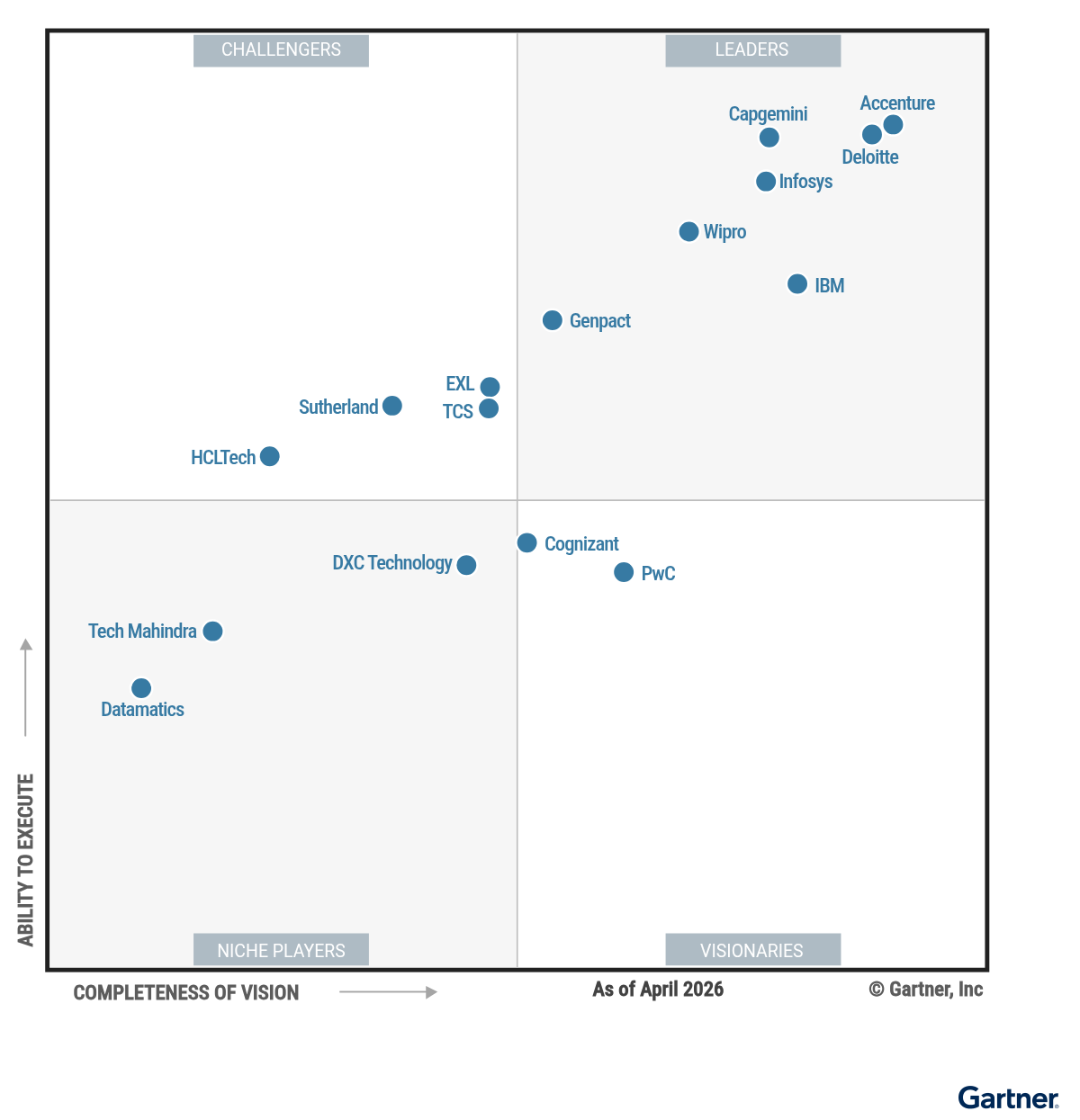

Magic Quadrant

Vendor Strengths and Cautions

Accenture

Accenture is a Leader in this Magic Quadrant. Of its 402 F&A BPO clients, 84% contract for P2P services, 71% for O2C services, and 74% for R2R services.

In the past year, Accenture has enhanced its integrated platform, SynOps, which acts as an integration and orchestration layer between finance process solutions and client ERP systems across multiple industries. The platform now includes a conversational generative AI (GenAI) layer to facilitate natural language conversation with clients. Accenture offers machine-reinvented process redesign, during which SynOps identifies which process steps can be executed by AI agents.

In 2026, Accenture plans to further integrate advanced technologies such as ML, agentic AI and GenAI into financial processes. Clients will benefit from capabilities such as on-demand closing and reporting for R2R, as well as autonomous forecasting for areas such as customer payment behavior in O2C, all supported by human-in-the-loop validation.

- AI-enabled technology ecosystem: Accenture provides a portfolio of AI-enabled finance products. This includes agentic-led reconciliation and variance analysis on balance sheet accounts in the R2R process; and Collector’s Copilot, which prioritizes customer accounts with real-time data and detects promises-to-pay and disputes in the O2C process. These solutions accelerate automation efforts while helping clients improve their working capital.

- Process innovation: Accenture has established structured ideation and reinvention mechanisms through a comprehensive library of practical playbooks and technology assets, known as the Reinvention Console. Clients benefit from validated ideas and reusable technology accelerators, reducing the time required during pilots and rollouts.

- Transition strategy: Accenture applies its 360 Value Framework at the start of each engagement to assess the client’s process maturity against predefined best-in-class practices to identify tailored improvement opportunities within the specified scope of services aligned on with clients. This assessment establishes a baseline for ongoing process maturity development, and minimizes the risk of post-transition contract disputes.

- Technology integration: Accenture’s strategy relies on a complex ecosystem of proprietary assets and partner platforms. Clients that do not have dedicated IT resources to help govern service delivery and improvement initiatives might face extended integration timelines and possible adjustments to their existing enterprise architectures.

- Business model: Accenture does not always clearly communicate how existing client processes are advancing to higher maturity levels. Clients should discuss with the provider how change management will be used to drive increased adoption of process automation solutions.

- Contract flexibility: Clients’ feedback highlights long lead times in contract negotiations and challenges when requesting changes to original process scopes. Clients should evaluate this provider’s change request and scope change terms during proposal review processes.

Capgemini

Capgemini is a Leader in this Magic Quadrant. Of its 481 F&A BPO clients, which include clients inherited through the WNS acquisition, 88% contract for P2P services, 83% for O2C services, and 73% for R2R services.

Over the past year, Capgemini has continued embedding GenAI into its technology solutions to monitor process KPIs and analyze the root causes of service quality issues. Clients reported up to 30% faster close cycles and a significant reduction in manual interventions as a result.

In 2026, the integration of WNS will be a critical priority for Capgemini. Since the acquisition closing date of 17 October 2025, Capgemini has aligned and strengthened governance structures that promote client engagement and relationship protection throughout the technology and service delivery integration process.

- Secure AI-enabled operations: Capgemini adopts a risk-focused approach, supported by domain-embedded controls from its BPO operations to address key threats associated with AI technology. It has implemented secured data access, advanced risk controls, and specialized AI security guardrails to mitigate risks such as data leakage, model manipulation, and insecure AI adoption.

- Transformation capabilities: Capgemini offers comprehensive, evidence-based process transformation design services by using process mining and a target operating model design engine that can produce execution-ready roadmaps. The implementation risks associated with these changes are closely linked to the recommendations provided.

- Value delivery model: Capgemini employs integrated value governance within its delivery model to ensure outcome-focused engagements. A Business Outcome Officer and a Value Realization Office ensure that baseline objectives from the outset of the engagement remain embedded throughout engagement delivery, enhancing accountability to maintain progress against predefined objectives.

- Client segmentation: Larger enterprises are prioritized in Capgemini’s F&A BPO strategy, resulting in a less diversified client base compared with most providers in this research. CFOs of small and midsize businesses (SMBs) requiring customized support should inquire about how the WNS acquisition has influenced this strategy.

- Build-operate-transfer (BOT): While Capgemini provides BOT capabilities, its experience is more limited than other Leaders in this Magic Quadrant. Prospective clients considering a BOT engagement are encouraged to discuss these capabilities in detail and review client references.

- Delivery model: The acquisition of WNS further enhances Capgemini’s global delivery coverage, although the workforce is concentrated in Asia/Pacific. Clients seeking nearshore solutions should evaluate regional staffing commitments to ensure time zone alignment and stakeholder engagement.

Cognizant

Cognizant is a Visionary in this Magic Quadrant. Of its estimated 215+ F&A BPO clients, 75% contract for P2P services, 50% for O2C services, and 45% for R2R services.

In the past year, Cognizant upgraded its accounts payable (AP) invoicing processing platform, ServiceNow APO, by integrating agentic AI technology to enable touchless processing and using GenAI for invoice extraction and automated exception handling. This reduces processing time while minimizing reliance on manual interventions.

In 2026, Cognizant plans to further enhance its process automation advisory services with the stated objective of increasing client adoption of new technologies and AI process solutions delivered as part of the BPO engagement.

- Process innovation: Cognizant uses innovation assistant Bluebolt, along with global innovation studios, to create an enterprise-scale co-innovation and upskilling ecosystem that sources, prototypes, and scales client ideas. Clients benefit from prioritized access to pilot programs and prototyping resources, enabling them to keep pace with new AI-driven innovation opportunities.

- Market adaptability: Cognizant’s product and services strategy anticipates the impact of AI by developing process technology solutions for regulatory oversight, data sovereignty, and data security. In preparation for a reset of global delivery models, it is pioneering advanced learning and training models for new staff. As a result, clients will benefit from improved compliance, enhanced data protection, and accelerated onboarding and upskilling of employees.

- Delivery model: Cognizant provides a range of delivery options — including nearshore, offshore, and BOT — along with industry-specific blueprints designed to support regional compliance and expedite implementations. Clients have the flexibility to customize proximity, governance, and sector-focused solutions to accelerate engagement launches while ensuring adherence to local regulatory standards.

- Pricing model: Cognizant offers traditional pricing structures for most clients, with limited outcome-based KPIs. Clients should ensure that provisions for technology and process innovation are included in their contract agreements.

- Change request: The process for handling change requests and complaints does not include defined response times or standardized operational SLAs for all requests, and it varies on the nature of the request. Clients should proactively discuss how change requests and escalations will be managed to prevent challenges with planning and governance effectiveness.

- Technology portfolio: Cognizant’s portfolio of proprietary and partner products across multiple domains does not appear cohesive. Clients should assess Cognizant’s integration governance, data flow ownership, and total cost of ownership strategies during evaluations to avoid unnecessary complexity and ensure a cohesive, sustainable technology architecture.

Datamatics

Datamatics is a Niche Player in this Magic Quadrant. Of its 91 F&A BPO clients, 70% contract for P2P services, 30% for O2C services, and 25% for R2R services.

In the past year, Datamatics has introduced agentic solutions that create and send dunning letters and collection reminders, and perform cash applications to increase O2C process efficiency. The provider has also introduced AI-driven credit risk scoring to strengthen risk management.

In 2026, Datamatics plans to establish a center of excellence specifically for logistics clients, providing specialized O2C and R2R offerings. Clients will benefit from specialized bill-of-lading processing and intercompany accounting services.

- Innovation fund: Datamatics offers clients an innovation fund to support enhancements to its proprietary solutions. This enables clients to benefit from an improved proof-of-concept approach before enhancements are scaled to production.

- Process transformation: Datamatics has launched process advisory services that use maturity assessments to evaluate each client’s current state. Based on these assessments, it develops a process transformation roadmap aligned with the client’s business objectives.

- Transition support: Datamatics delivers auditable knowledge capture and transition governance through stakeholder workshops, version-controlled standard operating procedures (SOPs), and real-time transition dashboards. This reduces single-person dependency and accelerates stabilization for customers during onboarding.

- Innovation: Datamatics has limited technology partnerships, which may affect the development of domain- and industry-specific technology solutions. Clients should pressure-test how their technology roadmap fits within Datamatics’ technology capabilities and innovation plans.

- Change request: The process of handling change requests and complaints does not include defined response times for routine requests. Clients should proactively discuss how change requests and escalations will be managed to prevent challenges with planning and governance effectiveness.

- Process adoption: Client adoption of more complex subprocesses within Datamatics’ contract portfolio varies, with lower implementation rates reported for areas such as dispute management relative to credit assessment and automated cash application in O2C, and fixed asset accounting in R2R. Clients should evaluate existing capabilities against their targeted outsourcing service scopes.

Deloitte

Deloitte is a Leader in this Magic Quadrant. Of its 735 F&A BPO clients, 70% contract for P2P services, 65% for O2C services, and 75% for R2R services.

In the past year, Deloitte has expanded its integrated performance platform, Ascend, by adding agentic AI capabilities to streamline the financial close process through a period-end closing steps dashboard that provides real-time visibility and orchestration.

In 2026, Deloitte plans to expand AI investments in Zora AI Perform to support various finance processes with touchless processing. For example, in P2P, the technology supports autonomous data extraction and workflow. Clients will benefit from lower processing costs through autonomous vendor invoice processing with minimal human involvement.

- Technology ecosystem: Deloitte provides an extensive technology ecosystem, including proprietary tools, hyperscalers, process mining, and prebuilt ERP connectors that embed integrated automation, rich process analytics, and near-real-time controls. Clients benefit from reduced integration lead times and improved operational visibility across finance processes.

- Process innovation: Deloitte, with its Lights Out Finance concept, drives innovation in every engagement through dedicated innovation funds, defined proof-of-concept cycles, and flexible gain-share or co-funding models. Clients benefit further from clear measures of success and aligned incentives for scaling process innovations.

- Delivery model: Deloitte’s delivery model can accommodate the unique operating constraints of geographically complex clients by capturing distinct cultural, linguistic, time zone, and regulatory needs. This coverage remains essential for activities in which significant global task-level exceptions can undermine technology automation opportunities.

- Technology integration: Deloitte’s proprietary platforms can create implementation and integration complexity for clients that prefer an accelerated technology roadmap. Clients should mitigate these challenges by aligning provider and internal IT teams early to co-determine integration and governance strategies.

- AI-enabled operations: Deloitte’s AI risk management framework is developing alongside the rapid evolution of AI technology. Clients adopting advanced technology should discuss how risks such as data leakage, model manipulation, hallucinations, and data sovereignty are being addressed and monitored throughout the engagement life cycle.

- Change request: Deloitte’s process for managing change requests and complaints have varied response times based on complexity and impact. Clients should proactively clarify timelines for handling change requests and escalations to ensure effective planning and governance.

DXC Technology

DXC Technology is a Niche Player in this Magic Quadrant. Of its 100 F&A BPO clients, 86% contract for P2P services, 68% for O2C services, and 64% for R2R services.

In the past year, DXC Technology has introduced the Avanta Agentic AI processing platform, designed to automate end-to-end vendor invoice processing. The platform uses Maestro, a digital coordinator, to orchestrate AI agents, thereby creating capacity between these agents, which increases productivity and efficiency in the P2P process.

In 2026, DXC Technology plans to enhance its technology offerings by integrating modular agentic AI capabilities across all enablement and productivity tools, with a particular focus on invoice processing and reconciliations. Clients will benefit from tailor-made solutions using the modular approach and reduced processing costs in these high-volume processes.

- Vertical/industry capabilities: DXC Technology targets multiple industry verticals with specialized industry-specific solutions. For example, clients can use e-invoicing capabilities to communicate with governments and benefit from e-invoicing platforms using prebuilt formats that minimize the need for customization.

- Market adaptability: DXC Technology anticipates an accelerated shift away from traditional physical delivery centers in the F&A BPO market, an emerging trend that is often underacknowledged among other providers. DXC is preparing for delivery model virtualization by introducing a digital workforce approach, offering clients more flexible service delivery options that are more resilient to disruptions.

- Delivery model: DXC Technology offers a flexible global delivery model that supports nearshore services, balancing proximity, language, cost, and service maturity. Clients can adapt their delivery footprint over time, allocating work between offshore and nearshore locations as business requirements and automation maturity evolve.

- Build-operate-transfer (BOT): DXC Technology has limited references for BOT models. Clients interested in these hybrid BPO structures should request pilots, references, and contractual safeguards before committing to these services.

- Pricing model: DXC Technology offers traditional pricing structures for most clients, with limited incorporation of outcome-based KPIs. The application of advanced technologies such as AI increasingly demands these models to foster innovation and support new process adoption.

- Innovation funds: DXC Technology provides innovation funds to only a select group of clients, which can limit technology adoption. Clients should not assume that innovation POCs or advanced technology deployments are included by default, and should specifically negotiate for funded pilot programs.

EXL

EXL is a Challenger in this Magic Quadrant. Of its 205 F&A BPO clients, 80% contract for P2P services, 82% for O2C services, and 75% for R2R services.

In the past year, EXL has further enhanced its AI capabilities by combining its Digital Finance Suite — its proprietary operating platform — with EXLerate.AI, its agentic AI toolkit, to deliver industry-specific solutions across R2R, P2P, and O2C. Examples include fraud detection for the healthcare industry, customer onboarding for the banking industry, and specialized accounts payable workflows for claims processing in the insurance industry.

In 2026, EXL plans to expand its AI agents by creating domain-trained copilots that integrate with clients’ systems of record, enabling faster deployment and improved efficiency. These will support expansion into industry use cases, including media reconciliations and reinsurance receivables, while enabling AI-supported, straight-through processing for account reconciliations and invoice processing. Additionally, EXL will continue investments in EXLData.ai, its advanced agentic data management solution, which leverages processing agents to transform structured and unstructured data into AI-ready formats. Clients will benefit from reduced processing times and improved process effectiveness and decision making, enabled by high-quality, contextualized data.

- Vertical/industry strategy: EXL delivers vertical-specific technology and process solutions for P2P, O2C, and R2R. Clients in the insurance and healthcare industries, for example, benefit from prebuilt AI solutions for industry-specific accounting processes, payment integrity, and revenue cycle management.

- Data management: EXL employs EXLData.ai, standardized common data models, and data visualization and reconciliation services that harmonize data across ERP and auxiliary systems. This minimizes data fragmentation during transitions and ensures auditable, reconciled finance data for downstream workflows and reporting.

- Transition support: EXL collaborates with clients through co-creation, conducting joint workshops to align on business outcomes, assess risks, and develop measures of success. This approach enables clients to begin engagements at the right process maturity level while establishing a flexible delivery model that can adapt to changing volumes and requests.

- Innovation: EXL grows its technology portfolio primarily through internal development, strategic technology partnerships, and partial investments in technology scale-ups. It is less reliant on full scale-ups acquisition than its peers, and clients should confirm that their technology ambitions align with EXL’s innovation strategy.

- Talent retention: EXL’s workforce attrition is high relative to the speed of its internal technology adoption. Clients should inquire about staff retention strategies and the availability of skilled resources.

- Innovation capabilities: EXL offers innovation capabilities to all clients in its core offering, with additional dedicated funding mechanisms for exploratory technology use cases included in 25% of contracts. Clients should explicitly discuss with EXL how optional funded pilot programs can be incorporated into their agreements.

Genpact

Genpact is a Leader in this Magic Quadrant. Of its 380 F&A BPO clients, 71% contract for P2P services, 68% for O2C services, and 74% for R2R services.

In the past year, Genpact has continued the expansion of its GenpactNext advanced technology strategy by integrating agentic AI solutions into its P2P, O2C, and R2R processes. In the P2P process, for example, its Agentic AP Suite resolves nearly 100% of data anomalies and duplicate payments. This solution improves risk management and increases processing efficiencies by 70% through automated responses to user queries.

In 2026, Genpact plans to expand its agentic AI portfolio within the R2R process by introducing reconciliation and intercompany agentic solutions to accelerate process innovation. It also aims to maximize the use of AI Maestro, an AI workbench and agentic orchestration engine. Clients will benefit from a faster close cycle and a significant reduction of cost to serve resulting from these new solutions.

- Human-AI collaboration readiness: Genpact uses the Agentic Operations Readiness Accelerator (AORA) framework to prepare its workforce for human-AI collaboration by evolving roles, enhancing processes, and embedding responsible AI governance. The framework uses adaptive assessments to map employees’ domain expertise and the data skills required for new agentic solutions to inform certification and specialized learning paths. This ensures that employees can effectively supervise and guide AI solutions.

- Business model: Genpact operates the largest network of delivery centers, supporting a strategy of initially rebadging clients’ workforce at the start of engagements before gradually transitioning activities to its main delivery hubs. Clients benefit from the reduced risks of institutional knowledge loss that are enabled by this approach.

- Pricing model: Genpact incorporates outcome-based KPIs in more than 60% of its contracts and offers agentic AI pricing structures oriented around predefined outcomes. This approach emphasizes trust and alignment around targeted client outcomes, differentiating it from traditional models.

- Innovation funds: Genpact offers innovation funds to 100% of its clients, with 35% of them opting to avail themselves of these funds. Clients should not assume that innovation POCs or advanced technology deployments are included by default and should specifically discuss how these funded pilot programs, which incentivize technology adoption, can be incorporated into their contract.

- Client segmentation: Although Genpact is pursuing workforce investments to target other segments, small and midsize businesses are less represented compared with other providers. These businesses should discuss Genpact’s approach for offering scalable solutions and tailored support specific to their segment.

- Change request: The process of handling change requests beyond predefined SLAs and statements of work does not include defined response times or a standardized operational approach. Clients should proactively discuss how SLA change requests will be managed to prevent challenges with planning and governance effectiveness.

HCLTech

HCLTech is a Challenger in this Magic Quadrant. Of its 85 F&A BPO clients, 60% contract for P2P services, 70% for O2C services, and 45% for R2R services.

In the past year, HCLTech has upgraded its invoice-to-pay platform by integrating EXACTO, a patented GenAI intelligent document processing solution. EXACTO enables the autonomous processing of invoices, contracts, and other P2P documents, including both structured and unstructured content, moving its end-to-end process toward near-autonomous processing.

In 2026, HCLTech plans to invest in ML, agentic and GenAI capabilities across P2P, O2C, and R2R processes, including NLP-based dispute resolution for P2P, continuous close for R2R, and predictive collections from O2C. Clients will benefit from enhanced process-level assurance and improved process-level insights.

- O2C technology solutions: HCLTech excels in delivering a comprehensive suite of O2C technology solutions, enhanced with AI capabilities. It offers agentic solutions from order entry and cash application, using data to analyze credit risk and predict client cash inflow.

- Regional workforce: HCLTech has one of the most diverse regional workforces among providers and maintains one of the lowest attrition rates in the industry. Clients benefit from a stable team that can address distinct cultural, linguistic, time zone, and regulatory requirements. This broad coverage is essential for activities where significant global task-level exceptions could otherwise undermine technology automation opportunities.

- Service agreement: Based on market trends, HCLTech co-creates service delivery agreements with clients, jointly defines SLAs, and uses a controlled change request process. This approach gives clients clearer, measurable expectations and reduces ambiguity during and after transition.

- Industry strategy: HCLTech serves a limited number of clients across various industries, and its initiatives to develop industry-specific solutions in sectors such as life sciences and media and entertainment are still in the early stages. Clients with sector-specific deployment needs should request examples of industry solutions to evaluate their relevance.

- Business continuity plan (BCP): While HCLTech’s BCP is tested to evaluate readiness, the specifics regarding backup site arrangements for service continuity are unclear. Prospective clients are advised to verify detailed BCP provisions to ensure uninterrupted business operations.

- Innovation funds: HCLTech offers innovation funds only in large multiyear contracts when it is commercially justified, which can limit technology adoption. Smaller clients should not assume that innovation POCs or advanced technology deployments are included by default, and should specifically negotiate for funded pilot programs.

IBM

IBM is a Leader in this Magic Quadrant. Of its 341 F&A BPO clients, 63% contract for P2P services, 40% for O2C services, and 34% for R2R services.

In the past year, IBM has enhanced its capabilities for the P2P process by integrating agentic AI capabilities. This solution offers a persona-based engagement layer for business users, delivering data insights and business value through NLP queries.

In 2026, IBM plans to advance its agentic solutions to support plain-language data queries across both transactional processes and judgment-based tasks. Clients will benefit from reduced processing costs in high-volume areas and strengthened enterprise risk management.

- Transformation capabilities: IBM has an extensive proprietary and partner technology ecosystem to support complex process transformation initiatives. This provides clients with reliable execution, and established transfer models for multidelivery locations or high complexity process transformation priorities.

- Process innovation: IBM combines its integrated portfolio of process redesign, process intelligence, and AI tools to accelerate the transition from POC to production. Clients have the opportunity to participate in pilot projects, enabling them to prototype future-state processes.

- Transition support: IBM offers a centralized Transition Accelerator Kit that leverages structured process documentation using watsonx and GenAI for knowledge capture, creating fast, audit-ready process documentation. This reduces reliance on subject matter experts while accelerating onboarding cycles and transition phase compliance.

- Technology integration: IBM has a complex technology ecosystem, which can be perceived as requiring significant integration efforts as it includes multiple proprietary assets, third-party tools, and recent acquisitions. Clients should mitigate these challenges by aligning provider and internal IT teams early to co-determine integration and governance strategies.

- Pricing model: IBM’s clients’ adoption of contracts with outcome-based KPIs remains limited compared with other Leaders in this Magic Quadrant, despite IBM offering a range of pricing structures. Clients are encouraged to discuss with IBM how costs associated with advanced technologies, including AI, are incorporated into commercial agreements.

- Customer experience: The process for handling customer complaints doesn’t include clear response times and lacks proactiveness. In contracts, other providers enforce strict response times and use AI-enabled early warning systems. Clients should confirm how IBM manages complaints and escalations to avoid challenges with planning and governance effectiveness.

Infosys

Infosys is a Leader in this Magic Quadrant. Of its 181 F&A BPO clients, 55% contract for P2P services, 50% for O2C services, and 30% for R2R services.

In the past year, Infosys launched the Infosys Intelligent Close Platform, a platform with AI technology designed to autonomously deliver close activities through outlier detection, automated journal entry posting, and reconciliation, as part of its Topaz Platform. Clients benefit from this platform as it enables a faster and error-free close.

In 2026, Infosys plans to further expand its AI-driven process technology deployment by delivering agentic solutions to support O2C overdue management, P2P vendor invoice processing, and continuous close in R2R.

- Technology ecosystem: Infosys offers a broad portfolio of proprietary, AI-enabled finance products complemented by an extensive partner ecosystem. In the R2R process, its Ledger Intelligence assurance solution uses embedded ML to detect anomalies and deliver alerts. Clients benefit from improved proactive controls that strengthen financial reporting assurance.

- Build-operate-transfer: Infosys has one of the highest BOT track records among all providers, supporting clients seeking BPO transformation experience. Clients benefit from transition methodologies, technologies, and transformation capabilities that support predictable timelines for establishing these client-focused delivery centers.

- Process innovation: Infosys combines its integrated portfolio of process redesign, process intelligence, and AI tools in innovation programs, and incorporates AI-enabled knowledge capture into its engagements. Clients can rapidly prototype and validate POCs to shorten stabilization of new processes and convert retained knowledge quickly.

- Delivery model: Infosys has a limited number of delivery centers in the Americas compared with other Leaders. Clients with significant global task-level exceptions may find that technology automation opportunities are limited as a result. They should discuss how their cultural, linguistic, time zone, and regulatory requirements will be addressed during provider evaluations.

- Client segmentation: Infosys has the highest concentration of clients in the large enterprise segment. It has recently started to focus on the SMB market, but solutions for non-large enterprise companies may be less diversified, and SMBs should confirm the availability of scalable solutions and customized support to ensure their needs are addressed.

- Change requests: The process for handling change requests and complaints includes long response times. Clients should confirm how Infosys manages change requests and escalations to prevent challenges with planning and governance effectiveness.

PwC

PwC is a Visionary in this Magic Quadrant. PwC did not disclose its number of clients, but its managed services cover P2P, O2C, and R2R services. PwC is the fastest growing service provider in this Magic Quadrant.

In the past year, among other AI investments, PwC has launched Outcomes Hub, an enterprise AI command center that orchestrates finance workflows and features advanced natural language chatbot functionality.

PwC declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- Technology ecosystem: PwC demonstrates a strong mergers and acquisitions track record to expand its finance managed services unit. Its latest acquisition of Kunai has strengthened its services for the financial industry by offering new technology solutions for payment networks.

- Delivery centers: PwC supports clients globally through its network of delivery centers, complemented by a worldwide local presence to handle high-complexity finance tasks while maintaining region-specific expertise.

- Integrated platform: PwC’s Outcomes Hub is a managed services platform that acts as an orchestration layer for agentic AI solutions supporting finance processes, including invoice processing, payment approvals, and reconciliations.

- Client feedback: PwC doesn’t disclose how it gathers client input to improve engagement-level delivery and satisfaction. Clients should seek references to assess the effectiveness of their client partnerships when coordinating on service delivery improvements and customization requests.

- Pricing model: PwC’s clients’ adoption of contracts with outcome-based KPIs remains undisclosed. Clients are encouraged to discuss with PWC how costs associated with advanced technologies, including AI, are incorporated into commercial agreements.

- Technology partnerships: While PwC discloses technology alliances on its website, it is unclear which partners are included in its managed services offerings due to limited client testimonials. Clients are advised to engage PwC directly to clarify which partner solutions are available as part of the managed services portfolio, and to ensure these align with their own technology strategies.

Sutherland

Sutherland is a Challenger in this Magic Quadrant. Of its 127 F&A BPO clients, 47% contract for P2P services, 64% for O2C services, and 61% for R2R services.

In the past year, Sutherland has formalized the client success leader role to enhance orchestration and accountability across client transformation initiatives, including AI. While process transformation and innovation have been part of Sutherland’s engagement model, this role ensures that transformation programs are closely aligned with client objectives and that value is sustained throughout the contract period.

In 2026, Sutherland plans to build solutions that strengthen risk, controls, and compliance across transactional finance processes to cover emerging priorities related to AI governance, data integrity, and regulatory change. Clients will benefit from new risk management safeguards.

- Transition support: Sutherland uses Epiplex in the start phase of the transition. Epiplex translates natural language, video, and draft documentation in standard operating procedure (SOP) creation and other onboarding materials. This enables shorter transition windows, faster new-hire productivity ramp-ups, and reduced handover risks.

- Process innovation: Sutherland uses structured co-creation and governance mechanisms, such as Joint Innovation Council and Think Tank, to involve clients in process innovation. These forums enable clients to actively shape process transformation plans.

- Pricing model: Sutherland has one of the highest outcome-based pricing structure adoption rates among providers in this market. This approach emphasizes trust and alignment around targeted client outcomes, differentiating it from traditional models.

- Strategic engagement: Sutherland’s approach to business reviews is primarily focused on delivering incremental operational improvements, with less emphasis on broader strategic topics relevant to senior leadership. Clients seeking more strategic engagement should proactively communicate their expectations and guide meeting agenda preparations to ensure that higher-level business objectives and priorities are addressed during reviews.

- Client segmentation: Sutherland varies the inclusion of automation and licensing across its client base, with larger accounts receiving priority. Small and midsize prospective clients with a turnover below $1 billion should confirm the availability of automation tools, licensing, and expected outcomes, as these factors can significantly impact cost, timelines, and achievable ROI.

- Technology roadmap: Sutherland outlines its future advanced technology capabilities as multiyear roadmap targets. These roadmaps feature AI capabilities that are already in use among other Challengers, such as revenue leakage solutions. Clients should verify the status of current innovation deployments to pressure-test their operationalization timelines and associated investment commitments.

TCS

TCS is a Challenger in this Magic Quadrant. Of its 300 F&A BPO clients, 95% contract for P2P services, 70% for O2C services, and 70% for R2R services.

In the past year, TCS has enhanced its Cognix platform by integrating agentic AI solutions across P2P, O2C, and R2R processes. These innovations improve end-to-end orchestration, generate insights, and increase the efficiency of financial statement creation, and its quality. For example, the provider’s R2R process platform now leverages GenAI and agentic AI for performance journal management and predictive journal entry creation.

In 2026, TCS plans to further expand its agentic AI capabilities across high-volume tasks, including vendor and client dispute resolution steps, as well as in judgment-intensive activities. Clients will benefit from reduced processing costs in high-volume areas and improved working capital.

- Technology ecosystem: TCS has introduced agentic agents, GenAI query capabilities, and automation across financial workflows, such as compliance reporting and assurance. Clients benefit from these new capabilities, which support accelerated analysis and improved quality of regulatory reporting.

- Vertical/Industry strategy: TCS’ client portfolio spans all major industries, with specialized technology solutions integrated in most of its service offerings. For example, clients in the healthcare industry benefit from inventory accruals tied to clinical batch and traceability data.

- Transition support: TCS embeds AI-enabled transition intelligence via its Cognix platform to autonomously capture and document client process knowledge. Clients benefit from an evidence-based, current-state view; standardized playbook; and control points to ensure effective transition management.

- Technology integration: TCS’ technology ecosystem offers a range of both partnership-based and proprietary solutions across end-to-end processes. Clients should discuss how to achieve straight-through processing functionality, and align on any proprietary solution dependencies during and after engagements.

- Build-operate-transfer: While TCS offers frameworks to support BOT engagements, its experience in this area is limited compared with Leaders. Prospective clients considering a BOT engagement are encouraged to request client references to receive assurance on TCS’ BPO capabilities.

- Innovation funds: TCS offers innovation funds to its clients, but the inclusion of these funds in contracts lags behind leading providers in this market. Clients should ensure that innovation POCs or advanced technology deployments are included by default, or negotiate outcome-based contracts with dedicated innovation funds to improve technology adoption.

Tech Mahindra

Tech Mahindra is a Niche Player in this Magic Quadrant. Of its 102 F&A BPO clients, 80% contract for P2P services, 80% for O2C services, and 40% for R2R services.

In the past year, Tech Mahindra has introduced TechM Orion, an ecosystem of agentic AI solutions featuring prebuilt and configurable AI agents spanning several industry verticals. For example, clients in the financial services industry benefit from ready-to-deploy solutions such as anomaly and suspicious payment detection, which improves risk management, or reconciliation across multiple ERP systems in the R2R process, which eliminates manual errors.

In 2026, Tech Mahindra will continue to expand the use of NLP, intelligent document processing, and GenAI copilots, prioritizing highly manual tasks such as automating invoice extraction, coding, and reconciliations. Clients will benefit from lower processing costs and improved accuracy through autonomous processing of vendor invoices with minimal human involvement.

- API-enabled connectivity: Tech Mahindra uses an API-first, platform-led architecture with prebuilt connectors and agentic AI assets to connect to clients’ ERP systems. This facilitates heightened straight-through processing by pushing insights and automations across P2P, O2C, and R2R processes back into source systems.

- Transformation capabilities: Tech Mahindra offers process transformation services and uses AceFin to establish process maturity baselines, model SLAs, assess controls, and generate transformation scenarios. Clients receive aligned SLAs and clearly documented transformation pathways, reducing time by 30%-40% during the design phase.

- Transition support: Tech Mahindra uses AI-integrated discovery and process intelligence technology to capture process knowledge during transitions. This is especially beneficial for clients operating in a fragmented, multi-ERP environment as it reduces reliance on subject matter experts and enables faster, lower-risk transitions.

- Delivery model: Tech Mahindra’s global delivery resources are highly concentrated in Asia/Pacific delivery centers. Clients with significant global task-level exceptions may find that technology automation opportunities are limited as a result. They should discuss how their cultural, linguistic, time zone, and regulatory requirements will be addressed during provider evaluations.

- Innovation funds: Tech Mahindra’s use of dedicated innovation funds with clients is limited, which can hinder new technology adoption. Clients should not assume that innovation POCs or advanced technology deployments are included by default, and should specifically negotiate for funded pilot programs.

- Technology roadmap: Tech Mahindra’s technology roadmap is lagging compared with other providers, with many featured capabilities already in use elsewhere, such as agentic solutions for supporting fraud detection. Clients should verify the status of current innovation deployments to pressure-test their operationalization timelines.

Wipro

Wipro is a Leader in this Magic Quadrant. Of its 244 F&A BPO clients, 67% contract for P2P services, 56% for O2C services, and 43% for R2R services.

In the past year, Wipro has launched Wipro Intelligence, a unified platform that integrates process-level automation, process orchestration, and performance analysis capabilities. Wipro has also launched WINGS (Wipro Intelligent NextGen Services), an execution engine that uses agentic AI capabilities to optimize workflows in finance activities. For example, in the R2R process, AI agents autonomously schedule close activities, automate reconciliations, and post journal entries.

In 2026, Wipro plans to introduce Quantum Finance, an algorithmic approach that enables large-scale and complex calculations to be completed within seconds. Clients will benefit from faster access to process-level data analytics and reporting insights.

- Process innovation: Wipro embeds co-innovation and funding mechanisms (Value Management Office, Wipro Innovation Network, Rapid Accelerator, and a stated contract innovation fund) to operationalize POCs. This governance and committed funding model helps clients to pilot, validate, and scale innovations with joint ownership and fewer budgetary barriers.

- Pricing model: Wipro offers a broad pricing portfolio that includes outcome-based and AI pricing structures oriented around predefined outcomes. This approach emphasizes trust and alignment around targeted client outcomes, differentiating it from traditional models.

- Innovation: Wipro frequently acquires companies to strengthen its offerings across domains and industries. Its acquisition of Harman’s Digital Transformation Solutions business unit strengthened its AI development capabilities for finance processes, such as improved invoice processing and user dashboards for better customer experience.

- Technology integration: Wipro’s strategy for how its proprietary assets and partner platforms integrate with clients’ existing architectures remains unclear. Clients should discuss how straight-through processing functionality is achieved to ensure interoperability and effective management of technology version updates.

- Technology adoption: Adoption of advanced technologies, such as low-code application platforms, chatbots, and conversational AI, within Wipro’s client base is not as high as among some other Leaders. Considering the growing significance of these technologies, clients should evaluate how Wipro’s offerings align with their specific needs and match their finance technology maturity.

- Delivery model: Wipro’s global delivery resources are highly concentrated in Asia/Pacific delivery centers. Clients with significant global task-level exceptions may find that technology automation opportunities are limited as a result. They should discuss how their cultural, linguistic, time zone, and regulatory requirements will be addressed during provider evaluations.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

- PwC

- DXC Technology

Dropped

- Conduent

- WNS

Inclusion and Exclusion Criteria

In addition to Gartner client relevance, as determined by analyst expertise and opinion, providers needed to meet the following criteria to qualify for inclusion:

Each provider is required to meet one of the following (in USD constant currency):

- Have attained a minimum revenue of $200 million (or the equivalent in another currency) from F&A BPO services in the last 12 months ending 30 September 2025, or

- A minimum annual revenue of $25 million from F&A BPO services and an average annual growth rate of 10% over the last two years ending 30 September 2025.

Each provider is required to meet all of the following:

- The service must meet the requirements outlined in the Market Definition section.

- Must offer F&A BPO services to a minimum of five clients in at least five of the following major industries:

- Education

- Energy & utilities

- Financial services

- Government

- Healthcare

- Information technology

- Life sciences

- Manufacturing

- Media & entertainment

- Professional services

- Retail

- Telecommunication

- Transportation & logistics

- Must have F&A BPO delivery centers in at least three of the following four regions:

- Asia/Pacific

- EMEA

- Latin America

- North America

Evaluation Criteria

Ability to Execute

Gartner evaluates providers’ Ability to Execute by using criteria that assess their products or services, overall viability, sales execution and pricing, market responsiveness and track record, operations and customer experience. Analysts use these criteria to evaluate providers’ abilities to compete and be effective in the market by satisfying and retaining customers, while embedding innovative new service capabilities that help clients keep pace with finance process and market-level changes.

Product or service, sales execution and pricing, customer experience, and operations criteria are particularly important. These criteria highlight providers’ ability to offer proven process automation solutions and transformation methodologies, as evidenced by robust client testimonials and customer satisfaction data. This increases CFOs’ confidence in providers’ Ability to Execute core finance processes independently. Providers must be able to do so with a high degree of accuracy and demonstrate outcomes against the predetermined service levels agreed on with clients.

A comprehensive portfolio of process automation solutions, transformation methodologies, and operational capabilities enables the expansion and enhancement of services within the finance domain, all with the same provider. Services must be priced transparently and with a high degree of accuracy, and be structured in a way that incentivizes continuous innovation.

The criteria for overall viability, as well as market responsiveness and track record, assess whether providers have sufficient funding levels to continuously develop their products, paired with the ability to respond to customers’ changing needs in this market.

The criteria for marketing execution was not rated, as it does not deliver unique, value-differentiating insights to clients evaluating BPO services.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | High |

Market Responsiveness/Record | Medium |

Marketing Execution | NotRated |

Customer Experience | High |

Operations | High |

Source: Gartner (June 2026)

Completeness of Vision

Gartner assesses providers’ Completeness of Vision by using criteria to assess their market understanding, offering (product) strategy, innovation, geographic strategy, vertical and industry strategy, and business model. Analysts also evaluate providers’ understanding and articulation of how they exploit market forces, such as clients’ rising end-to-end process automation ambition, and emerging workforce needs, to create new opportunities for themselves and their clients.

Market understanding, offering (product) strategy, and innovation criteria are particularly important. These criteria highlight providers’ ability to clearly articulate a roadmap for transforming finance operations. By offering advanced process technology solutions with extensive AI capabilities, clients can shift away from heavy human dependency and move toward intelligent and highly automated process workflows. Outcomes expected by clients should include a reduction in the total cost of operations, along with improvements in service quality and compliance.

Business model, vertical/industry strategy, and geographic strategy criteria address a provider’s ability to respond to clients’ demands and deliver value to organizations of different complexities, industries, or geographies.

The criteria for marketing strategy and sales strategy were not rated as they do not offer meaningful, differentiating insights for prospective clients.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | NotRated |

Sales Strategy | NotRated |

Offering (Product) Strategy | High |

Business Model | Medium |

Vertical/Industry Strategy | Medium |

Innovation | High |

Geographic Strategy | Medium |

Source: Gartner (June 2026)

Quadrant Descriptions

Leaders

Leaders are adopting an AI-first approach to enhance clients’ process maturity, and global service delivery efficiency. By continuously deploying benchmarking and diagnostics on process-level cost and efficiency, AI solution prevalence, manual work reduction, and engagement service quality, Leaders demonstrate how labor-centric managed services can be transformed to technology-centric models with minimized human dependencies. Additionally, Leaders use integrated performance platforms to help clients evaluate providers’ performance and identify improvement opportunities in real time, while also demonstrating how process maturity advancements delivered by the provider are reducing processing costs.

Leaders have enhanced the digital skill sets of their workforce, enabling them to effectively use existing advanced technology solutions, while building new capabilities. The integration of AI agents as “digital colleagues” into their advanced technology portfolio further increases service delivery efficiency, particularly for routine and labor-intensive tasks.

By integrating ML, AI agents and GenAI technology into their service delivery, Leaders have increased the number and type of individual activities within finance’s end-to-end processes that are now well-suited for outsourcing. These expanded AI capabilities are enabling fully autonomous execution of discrete tasks within end-to-end process workflows — common use cases range from automated vendor invoice data extraction and customer dispute management, to reconciliations and journal entry automation. Leaders supplement these capabilities by offering a broad span of both proprietary and partnership-developed solutions, relative to other providers, as part of their technology ecosystems. This approach addresses clients’ technology ambitions and requirements while simultaneously reducing lock-in concerns.

A Leader may become a Challenger unless it continuously revisits, reprioritizes, and expands its AI innovation roadmap, with the future-state objective of enabling fully autonomous service delivery across end-to-end processes. Conversely, a Leader may become a Visionary if it doesn’t address AI-associated data sovereignty, security, and technology lock-in risks that can otherwise hinder client adoption of new solutions.

Challengers

Challengers excel in their Ability to Execute via the breadth of their industry-specific coverage and offerings, and the speed and flexibility of their outsourcing transition strategies. Challengers frequently co-create transition strategies with their clients, and consistently apply AI-enabled solutions to facilitate rapid knowledge capture of those clients’ processes. Challengers are also responding to clients’ demand for enhanced nearshore service delivery to support client-specific coverage and regulatory nuances.

Challengers generally service large client bases through customizable technology solutions, both proprietary or developed via external partnership networks. Their advanced technology solutions — spanning process mining, ML, AI agents, GenAI, and intelligent process workflows — often compete with those of Leaders in this market.

However, Challengers may lack the ability to articulate a clear roadmap for transitioning finance operations from a reliance on human-performed tasks to intelligent, highly automated process workflows. Additionally, the inclusion of innovation funds in client contracts is lower compared with providers in the Leaders quadrant.

A Challenger may become a Leader if it demonstrates exceptional insight into the market’s direction, as well as the ability to continue developing and delivering innovative, differentiating solutions in the future. Alternatively, a Challenger may become a Visionary or a Niche Player by sacrificing growth and focusing on developing innovative, differentiating and/or segment-specific features and capabilities.

Visionaries

Visionaries keep ahead of emerging F&A outsourcing service delivery innovations. Visionaries invest in and rapidly seek to elevate the effectiveness of the AI solutions they pilot and deploy, aiming to accelerate the evolution of their F&A BPO services from primarily labor-centric to primarily technology-centric offerings. Visionaries enable this evolution via robust and often proprietary process-level transformation and innovation methodologies that help clients to more quickly identify opportunities to innovate services through new technology adoption.

Visionaries also focus on developing new AI agents that offer clients greater flexibility to adapt delivery models in response to the evolving priorities of finance organizations.

However, Visionaries’ proprietary technology solutions are sometimes not integrated cohesively into a robust overall product portfolio that is easy for different F&A BPO client demographics to use. This can increase lock-in risks and hinder client adoption. Additionally, Visionaries may demonstrate limited service delivery agility, making it critical for clients to negotiate closely with providers to tie pricing models to tangible outcomes, and to ensure that formal response processes to change requests get formally embedded into engagement governance mechanisms.

A Visionary may become a Leader when it develops its go-to-market capabilities, generates strong growth, and demonstrates that it can nurture partnerships that complement its strengths. Alternatively, a Visionary may become a Niche Player if it over-indexes on ensuring full service excellence across discrete, isolated processes that are widely available throughout the F&A BPO market.

Niche Players

Niche Players demonstrate reliable process expertise spanning the core finance tasks in P2P, O2C, and R2R. They may also offer effective process technology solutions within specific finance subprocesses, industry sectors, or geographic regions.

However, Niche Players often lack broader attributes, such as an in-depth market understanding or a well-defined product strategy. Their ability to innovate or surpass other providers is generally constrained by the substantial investment needed to compete across the full spectrum of the F&A BPO market.

When Niche Players do innovate, they typically apply new proprietary technology to the subprocesses, geographies, and market segments with which they are familiar. Their smaller client base enables them to showcase self-service finance workflows effectively and to provide flexible knowledge transfer methodologies. Their business models emphasize delivering value through insights from transactional finance data.

Potential clients might assume that providers in other quadrants are better suited for their strategic finance agendas. But Niche Players can be a good choice for clients requiring narrow service expertise across discrete transactional subprocesses, geographies, or industry verticals, as well as clients seeking tailored knowledge transfer and transition support solutions.

Niche Players can move to the Visionary quadrant by developing compelling process and technology innovation roadmaps that facilitate the transition toward autonomous service delivery. Niche Players may shift into the Challenger quadrant by expanding the breadth of their sector-specific offerings and services.

Context

F&A BPO providers are increasingly enhancing their services by leveraging proprietary or third-party technology ecosystems. Their focus is on advancing process maturity for clients by deploying advanced technologies, such as ML, AI agents and GenAI, which reduce the dependency on human labor. This results in greater processing efficiencies and lower processing costs. To stay aligned, both providers and clients must concentrate on maintaining an up-to-date transformation roadmap and effectively managing the technology ecosystem.

The following recommendations will help you identify the F&A BPO provider best suited to your organization’s needs:

- Adopt flexible contract structures to support innovation. While FTE-based contracts offer a starting point, the market is rapidly shifting toward hybrid and flexible models that incorporate transaction-based pricing, fixed fees, and gain-share arrangements. Contracts should include provisions for periodic review and adjustment, enabling the integration of new technologies and process improvements as they mature. It is essential for clients to define with providers a baseline of outcome-based KPIs for each service, ensuring that pricing and provider incentives are directly linked to measurable business outcomes such as cycle time reduction, error minimization, and working capital improvement.

- Evaluate providers’ ability to support process maturity innovations. Agree at the start of the engagement the percentage of service fees allocated to an innovation fund for risk-free POC initiatives. This will enable more rapid adoption of new technologies. Additionally, determine the frequency of benchmarking and co-creation engagements to ensure accountability, and maintain influence on process transformation strategies. Throughout the contract term, discuss and update process transformation roadmaps based on the latest insights in process technology.

- Shift to nearshore models with advanced technology integration. As technology development accelerates, impacting the processing of transactional activities in low-cost countries, providers are contemplating a shift from offshore delivery models to nearshore locations. This transition involves replacing basic transactional activities with advanced technology. Clients should:

- Predefine flexibility mechanisms within providers’ delivery models as technology sophistication progresses.

- Pressure-test providers’ workforce retention and reskilling strategies to accelerate the development and embedding of advanced process technology solutions.

Market Overview

The finance and accounting business process outsourcing (F&A BPO) market is rapidly deploying advanced technologies — including AI, generative AI and AI agents — across finance’s P2P, O2C, and R2R processes. These technologies facilitate enhanced process ideation, innovation, and execution, transforming F&A BPO from a labor-centric to a technology-centric market. According to Gartner’s Forecast Analysis: Business Process Services, Worldwide, spending on F&A BPO services will show a compound annual growth rate of 2.4% over the period of 2024 to 2028, reaching $20.5 billion in 2028.

Market Trends

F&A BPO transforms from a labor-centric to a technology-centric market: Clients’ demand for and adoption of advanced technologies such as AI, GenAI, and AI agents is rising year on year. When paired with F&A BPO providers’ growing investments in, and production and application of, AI, these trends are accelerating the F&A BPO market’s shift from a predominantly labor-centric to a predominantly technology-centric market. All providers in this market today have AI use cases spanning P2P, O2C, and R2R, and most have capabilities across all three. However, the volume and sophistication of these capabilities will vary. Introducing AI solutions for vendor invoice processing, cash application, and duplicate payment detection are now standard across the market, and providers routinely offer integrated performance platforms that can deliver insights to clients on service- and process-level performance, as well as associated improvement opportunities. Capabilities to support tasks such as reconciliations and narrative reporting in R2R are also maturing rapidly. Consequently, these technologies are effectively reducing human dependence across traditionally labor-intensive activities.

Providers must reshape expectations as emerging AI capabilities outpace client readiness: Providers’ emerging technology capabilities can reshape F&A BPO service delivery expectations. Process transformation services that can reduce costs, enhance productivity and efficiency, improve compliance, and even generate insights are now routinely incorporated into contracts and SLAs. However, these capabilities often outpace clients’ readiness to accept new AI solutions due to perceived risks related to data sovereignty and security, hallucinations, provider lock-ins, and technology integration issues. Providers that tackle this reticence head-on will capture disproportionate market share. Most notably, providers are differentiating themselves via the combined span of proprietary and partnership-driven technologies being developed and used for BPO service delivery. Providers that offer a strong balance of both are most likely to address individual clients’ tailored technology ambitions and requirements while simultaneously reducing lock-in concerns.

New capabilities are balanced against continued delivery model investments: F&A BPO clients expect increasingly customized and flexible service delivery options, which providers continue to balance against the growing shift to predominantly technology-centric service delivery. Market appetite for nearshoring options, global coverage, and industry-level specialization, as well as build-operate-transfer (BOT) arrangements, continue to hold steady. This is due to three factors: clients’ current AI readiness, the increasingly tailored service arrangements that clients expect amid providers’ rising AI and process transformation capabilities, as well as individual clients’ regulatory, language, and time-zone coverage requirements. Providers today continue to differentiate themselves based on the depth and breadth of workforce specialties, and location- and industry-specific services that they can offer. A case in point is BOT, wherein providers can distinguish themselves by offering a combination of fully transferable center creation, as well as hybrid models in which they maintain operational oversight after centers have been built.

Outcome-based pricing becomes the norm: The market is increasingly defaulting to offering pricing models with outcome-based KPIs. All providers are willing to underwrite parts of delivery risk through outcome or gain-share contracts. This also leads to fluidity in pricing constructs due to the significant gulf in potential impact that clients can experience through outcome-based arrangements, which are often cited as delivering over 50% gains in process efficiency but are currently still targeted around highest-feasibility outcomes. Efficiency gains are capped at levels that providers are comfortable committing to, above which a gainshare structure is feasible. This change reflects buyer demand for accountability, and broader market patterns indicate that providers that can offer increased transparency through measurable benefits, such as process cycle time or error reductions, gain more rapid competitive traction.

Acronym Key and Glossary Terms

| BOT | build-operate-transfer |

| BPaaS | business process as a service |

| BPO | business process outsourcing |

| CFO | chief financial officer |

| EMEA | Europe, the Middle East, and Africa |

| ERP | enterprise resource planning |

| F&A | finance and accounting |

| FP&A | financial planning and analysis |

| FTE | full-time equivalent |

| GenAI | generative AI |

| ML | machine learning |

| O2C | order-to-cash |

| P2P | purchase-to-pay |

| PO | purchase order |

| R2R | record-to-report |

| SMB | small and midsize business |

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.