Magic Quadrant for Sales Performance Management

6 July 2026 - ID G00841323 - 35 min read

By Sandhya Mahadevan, Steve Rietberg, and 2 more

SPM applications are a sales operations leader’s trusted partner in defining optimal territories and quotas, and administering compensation plans that incentivize the right behaviors. Use this research to compare vendors’ diverse approaches to meeting these objectives, then choose the most suitable one.

Market Definition/Description

Gartner defines sales performance management (SPM) as a suite of applications that automates the implementation and administration of incentive compensation plans for sellers, including associated territory and quota management (TQM). Vendors typically offer seat-based platform access for sellers, sales operations leaders, sales leaders and finance roles. Customers integrate SPM applications with their CRM tools and commercial systems for workflow and data connectivity, and for the delivery of seller-centric insights.

SPM automates and unites certain back-office sales processes, and are implemented to improve operational efficiency and incentive effectiveness. Sales operations leaders use SPM for territory and quota planning, especially at the beginning of their planning cycle, and for incentive payment calculations, reporting and analytics throughout the year. SPM increases efficiency and effectiveness in these functions as well as improving visibility, traceability and governance. SPM facilitates collaboration with cross-functional peers in implementing sales compensation plan governance. This is especially crucial for mature organizations with complex sales plans. SPM uses master data and hierarchies to organize territories that align with the business strategy and sales structure. They also enable consistent and accurate methods of deal attribution and compensation calculation.

Sales managers use SPM for measuring and motivating sellers, and leveraging real-time insights into sellers’ quota attainment. SPM also provides sellers with on-demand analytics for visibility into their compensation projections and calculation methods. Most vendors offer leaderboard reports as tools for motivating sellers and optimizing performance.

Mandatory Features

- Incentive calculation and payouts

- Commission expense accounting compliance

- Compensation budget planning

- Territory design and optimization

- Quota planning and governance

- Sales capacity planning

- On-demand, self-service analytics for sales

- Pay-performance analytics

- Risk and scenario modeling

- Compensation plan explainability

- Bidirectional integration and interoperability with major platforms (e.g., CRM, ERP and HCM)

- Administrator UI for noncoding business roles

- Multilanguage and multicurrency support

Optional Features

- Sales strategy planning

- Monte Carlo simulations

- Machine learning algorithms for planning

- Estimator widgets

- Gamification

- Sales forecasting

- Revenue intelligence

- Interoperability with sales platforms like revenue action orchestration (RAO) and revenue enablement platforms (REP)

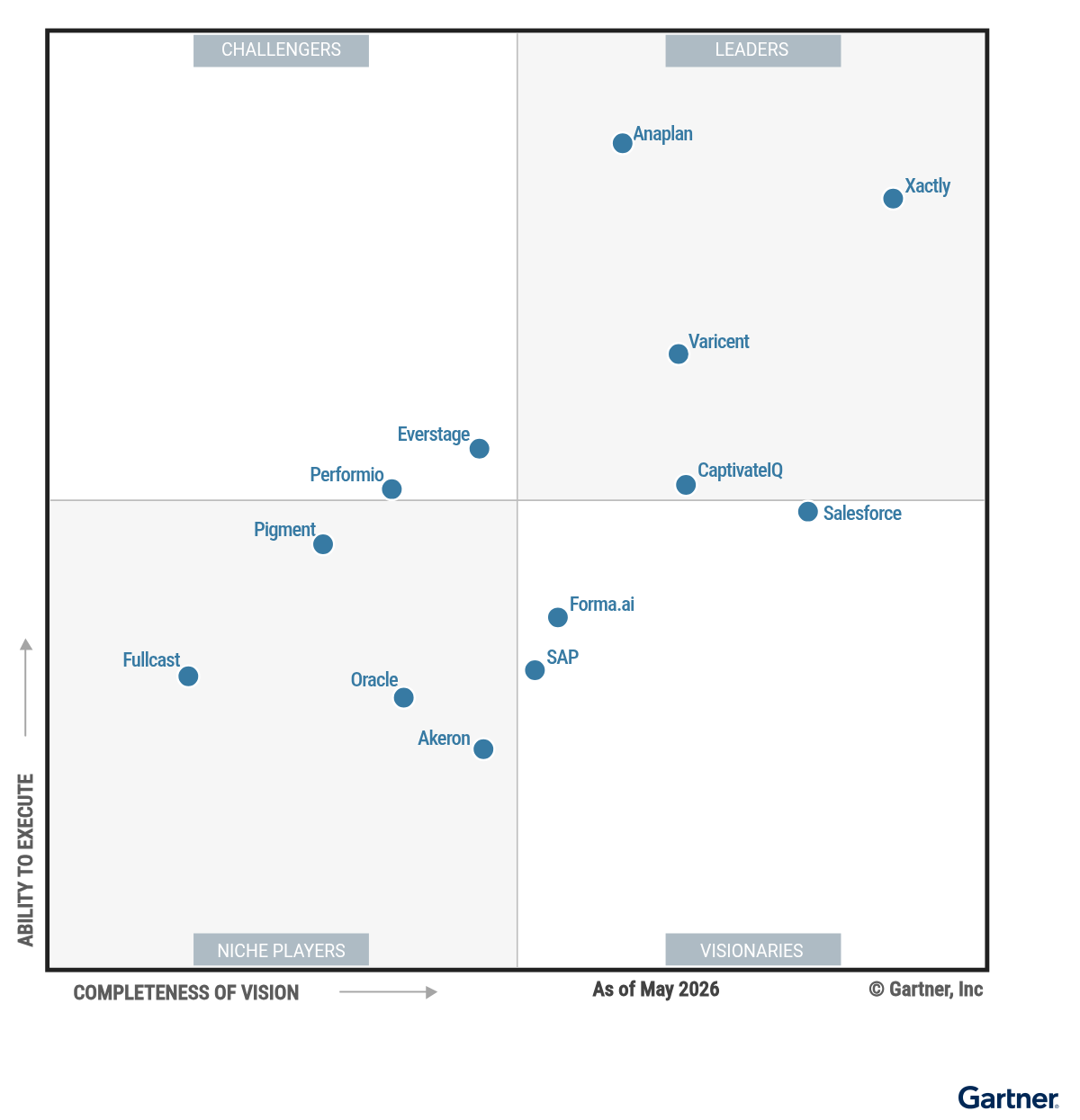

Magic Quadrant

Vendor Strengths and Cautions

Akeron

Akeron is a Niche Player in this Magic Quadrant, based on its uneven geographic presence and focus on specific verticals. Its cloud-native platform, Vulki by Akeron, covers the full life cycle of sales and nonsales incentive compensation management (ICM), including territory and quota planning, calculation, analytics, dispute handling, and data integration.

Its recurring SaaS model is priced per payee, with partner-led professional services. Akeron serves customers in several verticals, and has a notable presence in consumer packaged goods (CPG), financial services and luxury retail.

Since late 2025, it has launched Akyba, a governed AI agent center with bring-your-own-large-language-model (LLM) architecture. It also launched a real-time, on-demand calculation engine and Vulki DataFlow, an explainable data integration layer.

- AI governance: Akyba’s agent-based, human-in-the-loop architecture and bring-your-own-LLM approach directly address enterprise concerns around trust, auditability and vendor lock-in. This positions Akeron as one of the more AI-forward SPM vendors, while maintaining the governance and control required by large enterprises.

- Partnerships: Akeron’s exclusive SPM presence on the Microsoft Marketplace, its MACC-aligned procurement model, and active co-selling with Microsoft reduce purchasing friction and accelerate deal cycles. Complementary delivery through Accenture and Huron Consulting Group further strengthens its implementation capacity.

- Intuitive UX and mobile experience: Akeron delivers a strong user experience, with an intuitive interface tailored for both administrators and sellers. Its mobile capabilities are well-suited for field sales scenarios, enabling sellers to effectively manage tasks and access key information on the go.

- Ongoing investment cycle: As a recently established vendor, Akeron remains in a deliberated investment phase focusing on geographic and go-to-market (GTM) expansion. It is smaller in scale and global footprint than long-established incumbents.

- No public sector presence: Akeron does not serve the public sector, so it is not suitable for the government, state-owned or public organizations.

- Narrow value proposition: Akeron’s value proposition places more focus on operational efficiency, with comparatively less emphasis on the broader sales strategy, performance elevation, and decision support expected by buyers seeking transformational SPM platforms.

Anaplan

Anaplan is a Leader in this Magic Quadrant, based on the maturity of its planning product and its revenue performance management (RPM) framework. Its suite runs on a single codebase and data layer, with an integrated user experience across account segmentation and scoring, GTM capacity, territory and quota planning, ICM, and sales forecasting.

Anaplan’s SaaS model uses value-based pricing based on the number of use cases and company size, rather than seat count. Typical customers include large-scale enterprises.

Recent updates have focused on Anaplan CoModeler for AI-assisted model building, custom agent creation and domain-specific agents, supported by a unified data foundation. It expects to offer a full ICM application, additional agents and prebuilt connectors in 2H26.

- Enterprise credibility: With a revenue base over $1 billion and a large global enterprise customer footprint, Anaplan has strong market relevance and brand recognition among CxOs, making it easier to get stakeholder buy-in.

- Broad application portfolio: Anaplan’s SPM capabilities extend beyond incentives into adjacent processes such as AI-guided segmentation, capacity planning, forecasting, and revenue orchestration. This breadth underpins a differentiated RPM focus.

- Mature partner ecosystem: A well-established ecosystem of global system integrators, advisory firms, and application-building partners enables the delivery of complex transformation programs at scale.

- Operational complexity: Anaplan’s flexibility and modeling power can translate into lengthier implementations and dependency on highly technical resources. This can increase total cost of ownership for some customers, particularly those that extend beyond out-of-the-box capabilities.

- Risk of underutilization: Customers that deploy Anaplan for a single use case fail to fully leverage its broader RPM capabilities that connect planning and decision making across cross-functional teams. This can reduce business agility and dilute perceived ROI.

- Unconventional pricing model: Anaplan’s value-based pricing differs from conventional SPM models by structuring around use cases, company size and seat count, which can require buyer education to map relevant capabilities to spend and ROI.

CaptivateIQ

CaptivateIQ is a Leader in this Magic Quadrant, based on the strength of its core capabilities. Its cloud-native SPM software focuses on ICM and sales planning, built on a unified modeling platform. Its real-time modeling engine, SmartGrid, enables flexibility as well as auditability and scalability.

The subscription-based SaaS is priced per payee or planning instance, with add-ons for advanced analytics, AI, compliance and services. Industries served include technology, financial services, insurance, manufacturing, and business services.

Recent upgrades include Catalyst, an AI-enhanced modeling layer, as well as expansion of its no-code plan builder, natural language plan explanations and real-time what-if modeling. In May 2026, CaptivateIQ announced a suite of three SPM agents and a Model Context Protocol (MCP) server.

- ICM and RevOps: CaptivateIQ offers dual configuration paths where administrators can design plans using guided blueprints or build custom logic from scratch. Its focus on data modeling, powered by the SmartGrid engine, offers flexibility to ingest as-is data from a variety of sources without extensive IT involvement.

- AI strategy: The modeling add-on, Catalyst, supports tangible outcomes such as anomaly detection, forecasting, natural language plan explanations and workflow automation, rather than generic copilots. This approach reinforces trust and usability in compensation and planning processes.

- Partner-led GTM: A growing ecosystem of specialist SPM partners enables CaptivateIQ to scale enterprise delivery and maintain a largely variable cost structure. For customers, this supports a compelling ROI and rapid time to value.

- Scalability: Compared to larger platforms, CaptivateIQ operates at a smaller revenue and customer scale. This may raise concerns for highly risk-averse, global enterprises seeking long-established vendors with extensive resources and a global footprint.

- Perceived complexity from feature expansion: Customer feedback suggests that CaptivateIQ’s growing feature richness may, in some cases, reduce the simplicity, ease of implementation and maintainability that historically differentiated the platform.

- ICM-centric value proposition: CaptivateIQ’s messaging remains heavily centered on cost reduction, process efficiency and operational transparency, with less focus than other vendors on broader chief sales officer (CSO) priorities such as strategic sales planning, performance elevation and revenue growth optimization.

Everstage

Everstage is a Challenger in this Magic Quadrant, based on a growing customer base and its focus on optimizing the seller experience. It positions itself as an “AI-first” company, with no-code builders and agentic AI embedded directly into various SPM workflows and analytics.

Pricing for its recurring SaaS model is seat-based, with tiers based on volume and modules. Typical customers include midmarket and enterprise organizations.

Recent investments have focused on enterprise scalability and incorporating AI as an operational layer. Its roadmap focuses on expanding its territory and quota planning offerings, in addition to configure, price and quote (CPQ), to form a unified revenue execution platform.

- Seller experience: Everstage’s UI simplicity, mobile experience and real-time earnings visibility help reduce shadow accounting while improving seller trust, engagement and motivation.

- Growth momentum: Year-over-year growth sustained over two years, positive customer feedback, and frequent rip-and-replace wins against other market-leading incumbents indicate Everstage’s strong go-to-market execution and customer trust.

- Unified revenue execution: By integrating ICM, territory and quota planning on a shared data foundation, Everstage aligns with the broader RevOps convergence trend and increasing buyer preference for platform consolidation across the revenue life cycle. Its Databooks module provides flexible data integration.

- Scalability: Everstage is a relatively new entrant, compared to established SPM leaders and large platform vendors. This may present concerns for highly risk-averse enterprises that prioritize product extensibility, vendor scale, longevity and a global footprint.

- Reporting and analytics maturity: Everstage’s self-service analytics capabilities are still maturing. This can increase clients’ reliance on guided workflows and support resources, particularly for advanced analysis, until newer GenAI-driven builder experiences fully mature.

- Risk of increased complexity: Everstage’s evolution toward a broader, integrated RevOps platform introduces a risk of increased complexity, which could erode the simplicity and ease of use that initially set the platform apart and fueled early adoption.

Forma.ai

Forma.ai is a Visionary in this Magic Quadrant, because of its thought leadership and its AI-native user experience. Its SPM software uses predictive modeling to help customers quantify the revenue impact, cost and risk of incentive decisions. Forma.ai facilitates the Sales Comp Think Tank, a peer-to-peer community of enterprise sales comp leaders.

Pricing for Forma.ai’s SaaS model is subscription-based, but evolving toward usage- and value-aligned constructs tied to data scale, simulation intensity and decisioning workflows. Typical customers include upper midmarket and large enterprise organizations across industries.

It recently integrated SeaMonster into its SPM product; this is an acquisition that enables Forma.ai to offer activity tracking, sales process mapping and activity-based incentives.

- Differentiated AI strategy: Forma.ai’s ML-powered scenario modeling and predictive simulation capabilities extend beyond traditional calculation engines, enabling customers to assess behavioral, cost, and revenue impacts prior to plan rollout.

- Rapid growth and validation: Sustained high growth rates, Deloitte Fast 50/Fast 500 recognition, and expanding adoption among large-enterprise customers indicate strong market relevance and momentum, particularly in complex, data-intensive SPM environments.

- Thought leadership forums: Forma.ai’s thought leadership forums help it stay ahead of evolving compensation trends and shape how leaders incorporate SPM into strategic decision making.

- Focused SPM product scope: Forma.ai is primarily focused on territory, quota and ICM. Organizations seeking a broader suite spanning adjacent revenue operations workflows may require integrations with additional vendors.

- Complex value narrative: Forma.ai’s enterprise-oriented positioning, simulation-driven approach and emphasis on advanced analytics may require higher data literacy and technical skills.

- Evolving pricing model: Forma.ai declined to share pricing information for this research, but some Gartner clients report that a lack of pricing transparency introduces procurement complexity and difficulty in estimating usage.

Fullcast

Fullcast is a Niche Player in this Magic Quadrant, due to its recent entry but growing momentum in SPM. Its modules span territory and quota planning, capacity planning, routing, forecasting, ICM and revenue intelligence. It synchronizes GTM plans with CRM workflows and integrates with Salesforce, ServiceNow, NetSuite and AWS.

Pricing for the cloud-native SaaS is transitioning to a value- and usage-based approach. Typical customers include midmarket and large enterprise organizations with distributed sales teams.

Fullcast recently invested in consolidating its platforms and unifying the full GTM planning life cycle, while reducing total cost of ownership. It plans to expand agentic automation and evolve from a modular toolset into a fully integrated GTM operating system.

- SPM consolidation vision: Fullcast offers a unified platform, reducing fragmentation across RevOps, sales and finance. This supports a strong consolidation narrative, aligning with enterprise priorities to reduce total cost of ownership and simplify tech stacks.

- Targeted acquisitions: Recent acquisitions across forecasting, ICM, analytics and AI-driven workflow/content tooling have accelerated product breadth and roadmap velocity. The company’s investment in agentic AI positions it competitively as embedded intelligence becomes standard in RevOps platforms.

- Clear, minimalist UI: Fullcast delivers a streamlined user experience designed around seller workflows, enabling ease of use and supporting strong adoption.

- Limited ICM feature set: Many of its features are not as extensive as those of other vendors in this Magic Quadrant, and its Microsoft-Excel-like administrative UI is not as modern as the UIs of other vendors in this Magic Quadrant.

- Capability gaps: Certain end-user capabilities, such as mobile experience, dispute resolution workflows and advanced approval processes, remain in development. These gaps may impact seller adoption and satisfaction.

- Diluted focus: Fullcast’s positioning across the RevOps OS, as well as SPM, revenue intelligence and AI-driven GTM workflows can create messaging complexity across different members of an enterprise buying group.

Oracle

Oracle is a Niche Player in this Magic Quadrant. It offers SPM capabilities as part of Oracle Fusion Cloud, rather than as a stand-alone SPM solution. Capabilities span ICM, territory management, quota management, forecasting and analytics.

SPM components are licensed as SaaS through recurring subscriptions. Typical customers include complex, global organizations, and are often customers of Oracle’s broader CX suite.

Recent SPM innovation has centered on embedding GenAI and agentic capabilities into its CX suite, significantly modernizing its UX (Redwood), and more tightly integrating data across the Fusion Cloud suite.

Oracle declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- Capacity for complexity: Oracle is well-suited for complex, global organizations with multicurrency, multientity plans and date-effective rules, hierarchical crediting, approval workflows, and fully traceable calculation logic, including in highly regulated industries.

- Cloud EPM’s scalability: Oracle Sales Planning is built on the Cloud EPM platform, bringing mature enterprise planning capabilities to quota setting, forecasting and scenario modeling. This is particularly advantageous for organizations standardized on Oracle’s data and analytics stack.

- Long-term stability: Oracle offers the scale and longevity of a single strategic vendor with global support, extensive R&D investment, and aligned roadmaps across CX, EPM, ERP and HCM. This makes it a lower-risk choice for large, long-term transformation programs.

- Platform approach: Oracle delivers SPM capabilities as part of the Oracle Fusion platform, rather than as a stand-alone point solution. Organizations seeking highly specialized functionality for compensation or sales planning use cases may prefer vendors focused exclusively on SPM.

- Implementation overhead: Gartner clients, especially those with complex compensation structures, often report a steep learning curve and reliance on system integrators for deployment and customization. This can extend time-to-value and increase total cost of ownership.

- User experience: Oracle’s user interface prioritizes consistency with the broader Fusion Cloud Applications suite. Persona-based optimization caters toward the payee user experience, which may prevent role-specific optimization for compensation administrators and RevOps users.

Performio

Performio is a Challenger in this Magic Quadrant, due to consistent execution, rapid expansion and high customer satisfaction. Its SaaS SPM platform includes a flexible data model and a structured Plan Builder for RevOps and finance teams. Its MCP server connects compensation data and plan logic to enterprise AI tools.

Pricing is subscription-based, with implementation services and optional premium support. Typical customers include midmarket and enterprise organizations across industries.

It has a close integration and resell partnership with LINEN Cloud to expand its ICM offering while maintaining a modular approach. It is also adding AI capabilities, including an AI Admin Assistant, AI-driven implementation acceleration and a sales coach.

- AI roadmap: Performio applies AI to high-impact operational challenges. Capabilities such as the AI admin assistant, AI-driven implementation agents and MCP server integration reflect a pragmatic, outcome-oriented approach.

- Strong customer model: Performio’s high retention rates, multiyear prepaid contracts and profitability reflect a value-driven approach that delivers measurable ROI and fosters long-term customer commitment.

- Strong global presence: Performio has a strong position in Asia/Pacific and is expanding its footprint in North America and Europe.

- Narrow value proposition: Performio’s capabilities and messaging are heavily oriented toward the needs of compensation administrators, with less focus on supporting strategic sales decision making. This limits its appeal to senior sales leaders.

- Implementation timelines: Customer feedback suggests that Performio’s deployment cycles are longer relative to lighter, midmarket-focused SPM solutions.

- Gaps in risk, forecasting, integration: Performio’s capabilities in risk detection and management, predictive forecasting, and integration and data connectivity are still maturing.

Pigment

Pigment is a Niche Player in this Magic Quadrant, based on its relatively young ICM offering and uneven geographic presence. Its SPM is configured as a fully integrated planning capability that connects territory and quota planning, capacity tracking, forecasting, and ICM through a single, shared data model.

Pricing for Pigment’s SaaS is subscription-based, with three main levers: a platform fee, use-case fees and role-based user licenses. AI capabilities are monetized through a credit pool introduced in 2026. Typical customers include large enterprises.

Pigment is investing heavily in agentic AI (e.g., the Modeler, Analyst, and Planner Agents) to accelerate model creation, automate analysis, and enable continuous, governed planning cycles.

- Integrated platform: Pigment differentiates itself through its ability to natively connect SPM with financial planning and analysis (FP&A), workforce, and broader enterprise planning processes. This cross-functional integration drives strong executive-level alignment across CFO, CRO and COO stakeholders, while increasing platform adoption and retention through embedded, multidomain use.

- Agentic AI capabilities: Pigment’s Modeler, Analyst, and Planner Agents position AI as an embedded platform capability rather than an overlay.

- Partner ecosystem: A mature, system-integrator-led delivery model enables Pigment to support large SPM and planning transformations with accelerated time-to-value.

- ICM maturity and capabilities: Pigment is a newer entrant in ICM, relative to long-established specialist vendors. Some highly specialized compensation edge cases may require additional configuration and/or services support, depending on the customer’s plan design.

- Limited international footprint: Pigment’s strongest commercial and delivery presence is currently in North America and select European markets (notably France, U.K./Ireland and DACH). Organizations with formal in-region hosting or data residency requirements (including APAC) should validate these needs during evaluation, when required.

- Smaller operational scale: Pigment’s dedicated SPM organization is smaller than some long-established SPM specialists. Organizations with specialized support or delivery requirements should validate expectations during the evaluation process.

Salesforce

Salesforce is a Visionary in this Magic Quadrant, due to its holistic approach to the seller experience and agentic innovation. As a native extension of the larger CRM platform, Salesforce SPM includes sales planning, territory and quota management, enablement, mapping, AI-driven insights and ICM capabilities.

Pricing is subscription-based per user per month. SPM capabilities are available à la carte or as part of bundled offerings. Typical customers include large sales enterprises.

Upcoming capacity planning capabilities will support top-down allocation and bottom-up validation. A planned commission agent will provide sellers with instant earnings transparency, automated dispute resolution and proactive deal coaching.

- Integrated platform: Salesforce SPM is embedded within the CRM system of record, enabling planning, execution, enablement and compensation to operate on a unified data layer. This closed-loop architecture keeps all data within the secure boundary of the CRM, eliminating the “integration tax” of third-party stacks while mitigating the risks of data silos and manual entry errors.

- Global partner ecosystem: A large global network of certified partners, combined with the targeted SPM Rapid Start program, enables Salesforce to deliver SPM implementations at scale across industries and geographies. This ecosystem reduces implementation risk and supports consistent time-to-value for enterprise deployments.

- AI foresight: As AI capabilities gain adoption, Salesforce maintains its differentiation by embedding SPM within Agentforce Sales. It also announced Salesforce Headless 360 to extend Salesforce functionality to wherever sellers choose to work.

- Limited to Salesforce customers: Salesforce SPM is a native extension of the Salesforce platform. Planning and mapping capabilities are not viable for customers of other CRM platforms. Only ICM capabilities are available for non-Salesforce customers.

- Disjointed ICM/planning experience: The integration of acquired SPM assets (e.g., Spiff) with Salesforce’s broader sales planning and revenue workflows is still evolving. This may result in fragmentation or additional integration effort, particularly for capacity planning.

- High AI maturity requirement: Salesforce’s agentic AI capabilities require high data hygiene and deep tech-stack consolidation for peak effectiveness. Organizations with disconnected data silos or those unprepared to integrate with Data 360 will struggle to realize the full ROI of these advanced capabilities.

SAP

SAP is a Visionary in this Magic Quadrant, due to its ability to handle highly complex business models and compensation plans. Its cloud-native SPM platform is vendor-neutral and designed to centralize sales planning, territory and quota management, ICM, performance analytics, and AI-driven insights into a single system of record.

SAP’s SaaS model is subscription-based, typically priced by payee or record volume. Typical customers include upper midmarket and large enterprises in incentive-driven or regulated industries.

SAP’s latest cloud-native release includes a unified seller UX and a redesigned admin UX. Recent releases include the Joule AI assistant, enabling conversational access to commissions and performance insights. It has also enhanced its quota modeling and low-code data integration.

- Analytics and AI: SAP offers a sophisticated suite of analytics, and SAP Joule embeds generative and agentic AI across incentive design, planning, scenario modeling, dispute management and seller transparency.

- Global partner ecosystem: SAP’s extensive global system integrator and partner network enables large, multicountry deployments and supports industry-specific accelerators. This ecosystem strengthens SAP’s ability to deliver complex SPM transformations across regions and verticals at scale.

- Enterprise macro priorities: SAP’s positioning around suite consolidation, extensibility, sovereign cloud options and regulatory compliance aligns closely with enterprise priorities in cost-conscious, highly regulated and complex operating environments.

- Seller and admin UX: Gartner clients often perceive SAP’s SPM as less intuitive and more complex for day-to-day workflows and rapid plan iteration. This may impact adoption among RevOps teams seeking higher agility and ease of use.

- Implementation costs and duration: SAP’s enterprise-grade flexibility and governance come with inherent trade-offs. Partner-led implementations in particular can require longer timelines and higher investment, delaying time to value.

- Pricing complexity: SAP’s pricing structure, often involving volume-based tiers, can be difficult for customers to forecast and compare.

Varicent

Varicent is a Leader in this Magic Quadrant, based on strong customer reception to its product across all SPM use cases. Its platform covers sales planning (capacity, territory, quota), ICM, seller insights and native data orchestration. It is designed to serve as a system of record and execution for revenue performance.

Its hybrid SaaS pricing model focuses on value rather than number of seats, with AI monetized through consumption-based “impact” and “assist” credits. Typical customers include large enterprises and upper midmarket organizations with complex commercial models across industries.

It recently launched several purpose-built AI assistants and agents for extract, load and transform (ELT), planning, research, and seller inquiry handling.

- AI integration: Varicent’s AI assistants and agents for plan configuration, scenario modeling, inquiry resolution and ELT pipeline development have been well-received by customers for their utility and ease of use.

- Data integrations: Varicent offers a unified architecture where sales planning and incentives share a common data and logic foundation. Its native ELT capabilities further strengthen this position by embedding data ingestion, validation and observability directly within the SPM platform, reducing reliance on external tooling and improving data integrity.

- Scalable ecosystem: Strong system integrator relationships and a strategic partnership with Workday expand access to large transformation programs and support globally distributed enterprise deployments at scale.

- Premium pricing profile: Varicent’s enterprise-grade capabilities require higher pricing, which may make it less practical than lower-cost or more narrowly scoped SPM alternatives, particularly for price-sensitive segments.

- Enterprise-focused complexity: The platform is less suited to SMB or early-stage organizations, given the complexities of deployment and maintenance.

- Learning curve: Varicent’s depth in governance, data modeling and workflow configuration can increase onboarding effort and reliance on specialized expertise, especially in large, highly regulated or operationally complex environments.

Xactly

Xactly is a Leader in this Magic Quadrant, based on the depth of its AI strategy and the extensibility of its product. Its Intelligent Revenue Platform is designed to orchestrate the entire revenue planning life cycle, unifying territory and quota planning, capacity planning, ICM, forecasting, expense accounting, benchmarking, and analytics on a single data model.

The cloud-native SaaS is priced as a per-user subscription, with usage-based expansion options for extensibility and advanced AI. Typical customers include enterprise-grade organizations that operate complex GTM structures at scale.

Xactly recently launched MCP capabilities and piloted Xactly Intelligence Studio, allowing users to build and deploy their own specialized agents.

- Benchmarking assets: Xactly’s proprietary 20-year benchmarking dataset represents a durable competitive advantage, enabling AI-driven recommendations for quotas, territories, capacity, and incentives that can be sliced by filters such as org size or vertical.

- Composable, extensible platform: Through its Extend and Intelligence modules, and its emerging marketplace, Xactly enables customers and partners to build custom workflows, applications, and AI agents without sacrificing governance.

- Strong viability: Xactly’s business model demonstrates strong financial resilience. This enables sustained investment in R&D and product innovation, while maintaining stability through changing macroeconomic conditions.

- Platform complexity: Some Gartner clients report that Xactly introduces a perceived “black-box” layer between their organization and the underlying solution, limiting transparency into logic and calculations.

- UX perception: Xactly’s user interface is viewed by Gartner clients as less intuitive than newer, design-led competitors, making it more difficult to gain consensus for buying teams with UX-focused stakeholders.

- Complex pricing: Xactly’s pricing structure, including multiple tiers, add-ons and usage-based expansion, can be harder for buyers to evaluate, compared to simpler per-seat or per-payee models, potentially introducing friction in procurement processes.

Inclusion and Exclusion Criteria

For inclusion in this Magic Quadrant, vendors must meet all of the following baseline requirements:

- The vendor must have had a generally available (GA) SPM product in the market for at least two years (i.e., GA on or before 29 February 2024).

- The vendor must deliver all mandatory capabilities defined in the SPM market definition.

- Note: Vendors may still qualify if mandatory capabilities are delivered via add-ons or separate integrated products, provided they are commercially available and commonly deployed with the SPM offering.

In addition, vendors must meet at least two of the following three criteria to demonstrate sufficient market relevance and momentum:

- Achieve at least 20% growth in their SPM business over the prior calendar year (2025 vs. 2024).

- Add more than 15 net-new SPM customers (logos) during calendar year 2025.

- Have at least five live SPM deployments within the past 12 months (February 2025 through February 2026), each supporting 1,000 or more payees.

Vendors that do not meet all baseline requirements or fail to satisfy at least two of the three momentum criteria above are excluded from this research.

Evaluation Criteria

Ability to Execute

Product/Service: Specifically, we looked for the strength of critical capabilities offered by the vendor, its ability to integrate with customers’ stacks, and the relevance of its customer case studies.

Overall Viability: Specifically, we looked for product profitability, revenue and customer growth, and planned investments in corporate functions.

Sales Execution/Pricing: Specifically, we looked at the vendor’s current and planned pricing, its product bundling strategy, and its contract durations and values.

Market Responsiveness/Record: Specifically, we looked at the vendor’s major and minor release schedules, perceived market trends, and detected market changes.

Market Execution: Specifically, we looked for marketing budget, marketing headcount, and recent marketing campaign success.

Customer Experience: Specifically, we looked for the vendor’s typical customer time to value, customer experience measurement and customer support offerings.

Operations: Specifically, we looked for operational or compliance certifications, leadership changes, and recent merger or acquisition activity.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | Medium |

Marketing Execution | Low |

Customer Experience | High |

Operations | Low |

Source: Gartner (July 2026)

Completeness of Vision

Market Understanding: Specifically, we looked at the vendor’s perceived competitors, its potential competitors and planned investments in differentiators.

Market Strategy: Specifically, we looked at the vendor’s top buyers or ideal customer profiles, its demand-sensing approaches, and the evolution of its marketing strategy.

Sales Strategy: Specifically, we looked at the evolution of the vendor’s sales strategy, its channel strategy, and its planned focus on new versus existing customers.

Offering (Product) Strategy: Specifically, we looked at the vendor’s planned product enhancements, responsiveness to customer feedback, and product strategy priorities.

Business Model: Specifically, we looked at the organization’s current business model, planned changes to the business model, and changes to licensing/pricing models.

Vertical/Industry Strategy: Specifically, we looked for specific verticals targeted by the vendor, its planned growth in specific verticals, and planned changes to vertical strategy.

Innovation: Specifically, we looked at the vendor’s most innovative roadmap items, its recently released innovations and its vision for AI development.:

Geographic Strategy: Specifically, we looked at the vendor’s fastest-growing sales geographies, its planned changes to geographic strategy, and the most impactful region-specific standards impacting its SPM product.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | Medium |

Marketing Strategy | Low |

Sales Strategy | High |

Offering (Product) Strategy | High |

Business Model | Low |

Vertical/Industry Strategy | Medium |

Innovation | Medium |

Geographic Strategy | Low |

Source: Gartner (July 2026)

Quadrant Descriptions

Leaders

Leaders combine tenure and scale with a clear, opinionated vision for how SPM should operate in an AI-native era: Decisions are anchored in proprietary data assets, not heuristics, and executed on unified or tightly governed platforms that connect planning, incentives and execution. They deliver rich capability without overwhelming the user, and support multiple interaction modes (spreadsheet, workflow and AI assistant). Their AI is embedded, not bolted on: Assistants and agents take action within workflows, enabling users to move from insight to execution (e.g., adjusting plans, resolving inquiries, rebalancing territories) in a governed, auditable manner.

Buyers should treat Leaders as strategic platforms and choose based on operating model fit and data advantage, not feature checklists. Evaluate how deeply AI is integrated into transactional workflows, whether the platform unifies plan-to-pay on a common data model, and how easily users can act on recommendations. Large, complex organizations will benefit from ecosystem depth and scalability, while others may prioritize speed, usability and domain strength in ICM. In all cases, the decisive factors are quality of underlying data, ability to drive measurable outcomes (productivity, accuracy, cycle time), and flexibility in how users operationalize the system and interact with it day-to-day.

Challengers

Challengers deliver strong execution in core ICM with a focus on flexibility, reliability, and seller-centric usability, often rooted in a pragmatic, “get the job done” approach to SPM. They tend to emphasize transparency, accuracy and operational efficiency, particularly in compensation administration. Challengers apply AI selectively to high-friction tasks like onboarding, dispute resolution and admin productivity. Compared to Leaders, their architectures are less opinionated around end-to-end transformation and more aligned to traditional SPM constructs, with primary interaction still anchored in tabular and workflow-driven experiences. Many combine deep domain specialization with emerging platform ambitions, but remain earlier in proving scaled breadth, ecosystem depth and advanced analytics maturity.

Buyers should consider Challengers when prioritizing dependable ICM execution, faster deployment and improved seller experience over full platform consolidation. These vendors are well-suited for organizations that want to modernize compensation processes without committing to a broad RevOps transformation, or that value configurability and operational control within a defined scope. Trade-offs to assess include reliance on partners for adjacent capabilities (e.g., planning), maturity of self-service analytics, and ability to scale globally. In practice, Challengers often provide strong ROI in core use cases, but buyers should evaluate how far the solution can extend as requirements evolve beyond compensation into integrated planning and revenue orchestration.

Visionaries

Visionaries present a clearly differentiated, forward-leaning view of AI-driven SPM, often grounded in strong engagement with the sales operations community and a thought-leadership-led GTM approach. Their strategies emphasize agent-based workflows, continuous planning and broader RevOps convergence, aligning closely with where the market is heading. Visionaries demonstrate a strong AI-forward vision, but have not yet fully operationalized or scaled that vision within their SPM offering.

Buyers should consider Visionaries when they prioritize strategic alignment with the future of SPM and are prepared to adopt new operating models ahead of the mainstream. These vendors suit organizations with higher AI maturity and change appetite, where innovation and differentiation outweigh the need for fully proven scale and depth today. However, the trade-off is execution risk: Buyers must rigorously assess current product maturity, delivery capability and timeline to value, ensuring that roadmap ambition can translate into tangible, near-term outcomes, not just long-term potential.

Niche Players

Niche Players demonstrate deep strength in specific industries, use cases or organizational segments, often delivering highly tailored capabilities that address well-defined customer needs with precision. Their positioning reflects deliberate focus, rather than underperformance: Many intentionally prioritize vertical depth, specialized workflows or targeted customer segments over broad platform expansion. As a result, they may score lower on both vision and execution in a broad market context — not due to lack of capability, but because their strategies emphasize fit-for-purpose solutions rather than end-to-end SPM transformation or AI-led redefinition of the category.

Buyers should consider Niche Players when requirements are tightly scoped, industry-specific or aligned to a particular functional need where these vendors have proven expertise. They can offer strong value, faster alignment and differentiated domain support within their focus areas. However, organizations seeking a unified platform, extensive ecosystem support or a roadmap toward integrated, AI-driven SPM should assess the limitations of this specialization. The key decision factor is fit: Niche Players are best chosen when their strengths map directly to the buyer’s priorities, rather than as a foundation for broad, future-oriented transformation.

Context

The SPM market is evolving from a narrowly focused compensation administration category into a broader, cross-functional performance and planning domain anchored in RevOps principles. Buyers increasingly expect SPM platforms to enable integrated decision making across sales, finance, HR and IT, supported by AI capabilities, trustworthy data and scalable architecture.

The market is characterized by three primary vendor archetypes.

- Pure-play SPM vendors offer deep expertise in incentive compensation and seller performance management. These vendors typically provide greater flexibility in compensation modeling and faster innovation aligned with CSO priorities. However, they often rely on integrations for adjacent planning, HR, or financial data capabilities, and their support for enterprisewide data and AI strategies varies.

- Enterprise application suite vendors position SPM within broader CRM, ERP or HCM ecosystems. These solutions appeal to large enterprises seeking shared data models, centralized governance and embedded workflows. Trade-offs can include reduced specialization in complex compensation scenarios and less adaptability to rapidly evolving GTM models.

- Planning platform vendors originate from financial or workforce planning markets and extend into SPM with strengths in modeling, forecasting and scenario analysis. These platforms often resonate with RevOps and finance stakeholders, but may lack mature compensation administration capabilities or deep seller-level usability, requiring careful assessment for sales-led use cases.

Pricing models vary and influence scalability and economics. Seat-based pricing offers predictability but limits expansion, while consumption-based models provide flexibility with added governance requirements. Outcome-based pricing is in the early stages of maturity and requires high trust and metric clarity.

Key decision factors for SPM buyers include:

- The specific performance or planning gaps being addressed

- Compatibility with the existing technology stack and its capacity for data and AI workloads

- The primary buyer persona and stakeholders driving the initiative

- Alignment with the vendor’s point of view on SPM and planning

- Current data maturity and organizational data, technology, and AI literacy

- Engagement model with IT and system integrators

- Complexity, scale, user population and flexibility requirements

Market Overview

CSOs increasingly view SPM as a strategic, cross-functional capability rather than a back-office function. SPM platforms shape selling behavior, resource allocation, and execution strategy, and organizations expect them to support integrated decision making across sales targets, financial budgets and workforce capacity. As a result, vendors are expanding beyond compensation administration to serve finance, HR and IT stakeholders alongside sales leadership. This evolution raises the bar for scalability, data integrity and governance.

SPM buyers focus on a few key elements to differentiate vendors in the market:

AI Infrastructure and Decision Augmentation

Vendors vary significantly in their AI maturity. Some are augmenting legacy architectures with AI assistants, but this approach limits scalability, explainability and trust. Others are investing in AI-native platforms with embedded data pipelines, context awareness and prescriptive decision support.

CSOs are beginning to differentiate vendors based on their ability to move beyond insight generation toward decision augmentation — delivering early warning signals, scenario modeling, and guidance that informs compensation design, territory coverage, and quota allocation. Deep CRM and human resources information system (HRIS) integration continues to be a baseline expectation.

Vendor Point of View on SPM and Planning

Vendors increasingly differentiate through their points of view on what SPM should enable — ranging from sales execution enablement to RevOps orchestration and enterprise planning. These philosophies directly influence roadmap priorities, workflow design and the flexibility of compensation models.

As sales roles become more specialized and GTM motions more dynamic, CSOs are prioritizing platforms that support continuous plan iteration, modeling, and trade-off analysis, rather than static, annual compensation administration.

Data Governance

CSOs increasingly recognize that friction in SPM arises from poor data hygiene and constrained infrastructure. Latency, manual reconciliation, and downstream errors erode trust in compensation outcomes and analytics. Vendors are therefore differentiating through varying levels of support for data preparation, transformation and governance.

At the same time, demand is rising for greater transparency and explainability at the seller and frontline manager levels. As interest in AI-driven insights and automation grows, trust, governance and clear ROI are emerging as purchasing criteria alongside innovation.

Presence in Adjacent Markets

The SPM market continues to converge with adjacent domains, such as sales planning, territory and quota management, and forecasting. CSOs increasingly favor platforms with integrated capabilities that reduce operational friction and improve consistency across the revenue life cycle. Differentiation is shifting from feature depth in ICM toward the ability to support holistic performance management, from planning through execution.

However, broader ecosystem reach introduces trade-offs, as vendors balance end-to-end coverage with depth in sales-specific use cases.

Acronym Key and Glossary Terms

| CPQ | Configure, price and quote |

| CRM | Customer relationship management |

| CX | Customer experience |

| ERM | Enterprise resource management |

| ERP | Enterprise resource planning |

| HCM | Human capital management |

| ICM | Incentive compensation management |

| LLM | Large language model |

| SPM | Sales performance management |

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.