Magic Quadrant for Cloud ERP for Service-Centric Enterprises

13 October 2025 - ID G00826221 - 50 min read

By Robert Anderson, Johan Jartelius, and 4 more

Service-centric enterprises adopt cloud ERP applications to benefit from industry standard sets of process capabilities that produce better business outcomes. Application leaders should use this research to evaluate vendors of cloud ERP application suites as part of a composable ERP strategy.

Strategic Planning Assumptions

- By 2026, 85% of large ERP providers will have some agentic and generative AI (GenAI) capabilities in a preview, pilot or early adopter phase.

- By 2027, 62% of spending will be on ERP applications with AI capabilities, a major increase from 14% in 2024.

- By 2027, less than 10% of organizations that have implemented agentic AI within their ERP systems will have realized significant measurable value.

- By 2027, 60% of those replacing ERP applications will select software for their platform and business process orchestration capabilities, rather than for their transactional planning capabilities.

- By 2027, more than 50% of service-centric enterprises will look for an ERP-suite approach to meet their need for foundational capabilities.

Market Definition/Description

Gartner defines the market for cloud ERP for service-centric enterprises as a market for application technology that supports the automation of operational activities for service-centric (nonproduct) industries, including financial management, order-to-cash, source-to-pay, human capital management and other administrative capabilities. Cloud ERP for service-centric enterprises is delivered under a SaaS license model (with frequent mandatory updates), where application support, infrastructure provisioning and management are the responsibility of the vendor.

Broadly speaking, ERP solutions enable a variety of enterprisewide business processes, primarily those associated with systems of record and systems of differentiation. ERP solutions form the core systems that allow an enterprise to conduct business. For service-centric ERP solutions, process enablement covers a wide range of enterprise processes that include:

- Financial management system (FMS) functionality, including general ledger, accounts payable (AP), accounts receivable (AR) and financial planning.

- Order-to-cash (O2C) functionality, ranging from configure, price and quote (CPQ) to cash collection activities.

- Source-to-pay (S2P) functionality, which must cover at least e-sourcing, contract life cycle management, e-purchasing, AP invoice automation, supplier management, collaboration and payments.

- Human capital management (HCM) functionality, which must cover at least administrative HR capabilities, such as core HR data management, employee life cycle transactions and position management.

- Other administrative ERP functionality, to support typical service-centric activities, such as extended planning and analysis (xP&A), project management (for project-centric capabilities), service procurement and real estate lease management.

Mandatory Features

Must-have capabilities for this market include:

- Financial management system capabilities that provide visibility into an enterprise’s financial position through automation and process support for any activity that has a financial impact.

- Order-to-cash (O2C) capabilities that provide the framework for the financial supply chain that supports the mission of an organization to make money by providing services to customers. O2C integrates financial and operational processes within an organization, and must be robust for transactional support and analytics to coordinate enterprise operations.

- Source-to-pay capabilities, including the ability to pay for and manage supply of goods, services and people in support of delivery of revenue-generating services. Included are e-sourcing, contract management, e-purchasing, accounts payable, supplier engagement and collaboration, payments and procurement of services

- Human capital management functions that relate to administrative HR and talent management business requirements, including core HR data management, employee life cycle transactions, and position management.

Common Features

- Modular/Composable architectures displaying the ease with which the ERP can be deployed and integrated alongside other applications (cloud and on-premises) or platforms outside the primary ERP application suite to fulfill a composable ERP strategy. This includes the development for extension of the data model and/or functionality and the ability to consume, provide and exchange data/metadata.

- Advanced technology features associated with modern cloud solutions that include standard and generative AI, predictive analytics, hyperautomation and low-code development embedded in the applications or made available in the associated platform-as-a-service (PaaS) offering. Additionally, the solutions may offer configurable UI, mobile compatibility, contextualized secure data access and analytical reporting.

- Support/Systems Integrator (SI)/Methodology capabilities that address quality, cost, global availability and certification of professional services proved vital to driving deployment of ERP solutions for clients. Included are established partner networks, vendor certification programs and the capacity to support implementations that are properly aligned with the ERP vendor’s sales strategies and projections.

- Geographic coverage showcasing partner ecosystems and the ability to address languages and localization features provided by the vendor and/or partners.

- Complex corporate requirements, particularly for vendors targeting larger more complex enterprises, addressing the ability to manage multiple business units, multiple types of business, perform financial and operational consolidations within one instance of the suite, and provide reporting across various operating units and lines of business. This also includes the ability to manage major business processes across multiple business units.

- Sustainability functions that include ranking, reporting on and managing environmental, social and corporate governance initiatives natively within the suite.

- xP&A able to go beyond the financial organization’s use of financial planning and analysis (FP&A) and that is capable of merging financial and operational planning processes, allowing management to improve decisions and deliver better results across the enterprise.

- Ancillary capabilities, such as project management and professional services automation (for project-centric capabilities), subscription and recurring billing, service procurement and real estate lease management, may be offered optionally based on supported industries.

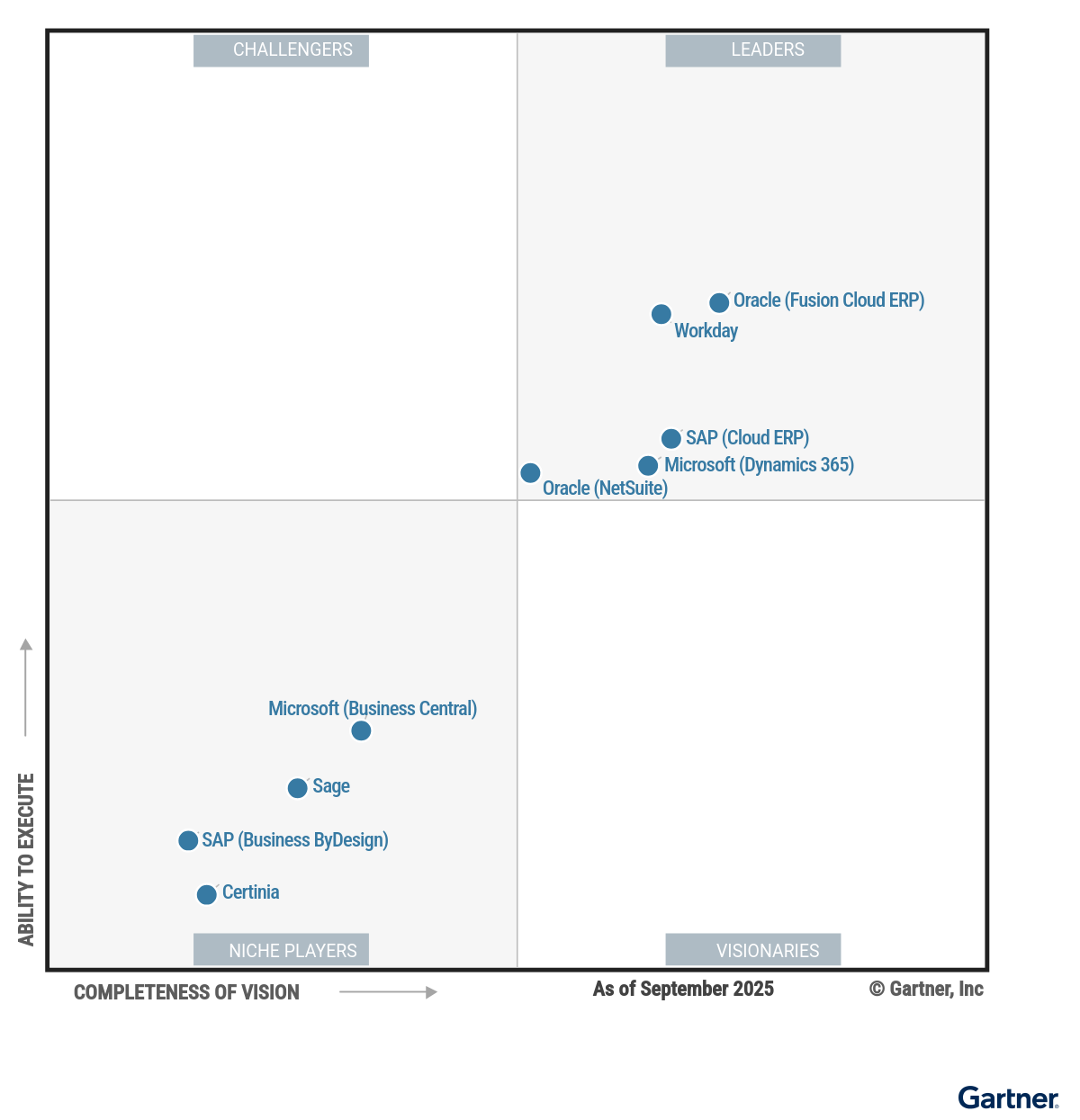

Magic Quadrant

Vendor Strengths and Cautions

Certinia

Certinia is a Niche Player in this Magic Quadrant. Its customer base is midsize to enterprise organizations primarily in the Americas, with a considerable presence in EMEA and a smaller share in the APAC region. The vendor offers a fully managed cloud solution, Financial Management (FM) Cloud, built on the Salesforce Platform. It focuses on financial management and professional services automation (PSA) for service-centric industries. Core human capital management (HCM) functionality is delivered via partnership with ADP.

Recent releases have focused on automating financial processes, like cash matching and bank reconciliation. The solution embeds Salesforce’s Einstein Discovery for predictive insights and has introduced GenAI for summarization and recommendations. However, creating custom AI agents may require separate Salesforce licensing, which could affect the total cost of ownership.

- Service-centric architecture: Certinia’s solution is purpose-built for service-based organizations, featuring a single-ledger architecture that enables unified customer records and real-time financial analysis. The general ledger natively supports complex corporate structures, including multientity, multibook, multicurrency, intercompany transactions, as well as dual charts of accounts. This solution provides robust financial management capabilities tailored for dynamic service environments and improves real-time visibility across business units.

- Platform extensibility and ecosystem: Certinia offers significant extensibility through low-code and no-code configuration options. This architecture facilitates seamless integration of Salesforce’s native AI and analytics tools. Clients benefit from flexible customization and access to a broad ecosystem of applications.

- Customer engagement model: Certinia uses a “swarm model” for customer support, engaging higher-level engineering expertise. Customer feedback is actively incorporated into product development, as seen in general ledger enhancements driven by nearly 2,000 community votes.

- HCM dependency: Certinia’s core HCM capabilities are not native and are delivered primarily through partnerships, most notably with ADP. Key functionalities are partner solutions, with integrated HR service management and an HR virtual assistant explicitly unavailable. This approach creates a functional gap for organizations seeking a single, comprehensive suite.

- Treasury functionality gaps: Organizations with complex treasury requirements will find notable gaps in Certinia’s current offering. Treasury and cash management functionality is listed as planned for the next 12 months but is not presently available in the application.

- Sustainability and ESG reporting: Certinia lacks out-of-the-box capabilities for sustainability and ESG reporting, which is increasingly important for enterprises focused on responsible business practices. Customization is required to add data to supplier records and to create ad hoc sustainability reports, potentially increasing implementation effort and cost.

Microsoft (Business Central)

Microsoft Dynamics 365 Business Central is a Niche Player in this Magic Quadrant. This solution is for enterprises in the lower midmarket segment. Clients are typically enterprises that generate less than $150 million in annual revenue in the Americas, EMEA and the APAC region. It is a fully managed cloud solution delivered from Microsoft Azure data centers that integrates with other Microsoft products, such as Microsoft 365, the Dynamics 365 CRM suite, SharePoint and Dataverse.

Business Central has native financial and operational capabilities. It relies heavily on partner solutions available on the Microsoft AppSource store for HR and more vertical solution capabilities.

Microsoft declined requests for supplemental information or to review the draft contents of this document. Gartner’s analysis is therefore based on other credible sources.

- Market momentum: Business Central customer adoption levels continue to grow consistently, with Microsoft reporting adoption by more than 45,000 customers. Growth can be attributed to a combination of factors, including its embedded AI capabilities, wide partner network and a number of clients migrating from Microsoft Navision and Great Plains due to end-of-life support concerns.

- AI-enabled Copilot: Business Central has incorporated Microsoft Copilot and AI-enabled capabilities in the suite. Compared with other solutions that target small and midsize businesses (SMBs), Business Central’s AI roadmap vision and execution is above average.

- Microsoft stack integration: Microsoft-centric customers may benefit from Business Central integration with other Microsoft offerings, such as Microsoft 365, Power BI, Teams and Power Platform.

- Cost and ease of maintenance: Customers report a heavy dependence on partner solutions/add-ons to cover themes like localization and reporting, plus industry-specific capabilities. That arrangement leads to variable customer feedback on cost and ease of maintenance.

- Horizontal ERP strategy: The horizontal (as opposed to industry-vertical) approach of Business Central requires customers to consider AppSource as an essential element in fulfilling their particular business needs. This approach is particularly true with respect to areas such as professional services, construction and nonprofit industries. The number of multiple offerings, some of them with apparently overlapping features, is a challenge, according to customer feedback.

- HR functionality: HR capabilities are still considered too simple, and there are visible gaps, such as in payroll capabilities. Customers that want a comprehensive suite will need to rely on solutions that have prebuilt integrations with Business Central available in AppSource.

Microsoft (Dynamics 365)

Microsoft Dynamics 365 is a Leader in this Magic Quadrant. It is a fully managed cloud SaaS solution delivered from Microsoft Azure data centers. Many ERP components are natively developed, but its partner solutions enable industry-specific capabilities. It serves midsize to large service businesses, primarily in EMEA, the Americas and the APAC region.

Recent announcements include the introduction of Microsoft 365 Copilot for Finance for tasks including reconciling accounts, variance analysis, project staffing recommendations, forecasting cash flow and automating repetitive financial processes. Microsoft also provides Copilot Studio, so customers can build their own assistants and agents. It has introduced process mining tools for optimizing business processes within the ERP and has also enhanced its capabilities to help predict customer payments, cash flow and demand forecasting. In 2026, Microsoft Dynamics 365 plans to invest further in agentic AI.

- AI prowess: Microsoft Dynamics 365’s embedded AI capabilities, through Copilot, are superior to others in the market to support business functions critical to service-centric organizations. Microsoft’s Power Platform now supports building custom agents that can interact with Dynamics 365 ERP data and processes.

- Mid-to large-scale FMS: Microsoft’s core financial management solution is integrated into Microsoft Dynamics 365 customer engagement applications, Teams, Microsoft 365 and Power Platform. AI-driven insights help finance teams identify trends, anomalies and opportunities for cost savings and revenue growth.

- Microsoft Azure capabilities: Azure Cloud Platform’s capabilities give Dynamics 365 built-in integrations with a rich set of enterprise-class platform services, such as Microsoft Fabric, Microsoft Power BI, Power Apps and Dataverse.

- Global and complex customer references: Global and complex enterprises report difficulty finding references for implementing Microsoft Dynamics 365 on a large scale. Microsoft plans to make the solution more attractive to these customers by increasing automation support for complex financial consolidations. Large-scale deployments or high transaction volumes may require careful performance optimization.

- HR functionality: Microsoft remains relatively untested for HR capabilities in organizations with more than 1,000 employees. In 2024, Microsoft released recruiting and service management capabilities and filled some previous gaps in career planning and succession management. However, organizations with global payroll requirements or that require advanced capabilities, like high-volume recruiting or skills management, may need to seek out additional independent software vendor partners.

- Complex customization: Although Dynamics 365 offers rich customization capabilities, customers have told Gartner that leveraging the solution’s complex capabilities often requires advanced technical skills and deep platform knowledge. Customers requiring substantial tailoring to fill functional gaps or to extend complex applications may need skilled developers or consultants.

Oracle (Fusion Cloud ERP)

Oracle Fusion Cloud ERP is a Leader in this Magic Quadrant. It is a modular and configurable SaaS solution for upper-midmarket and large enterprise, service-centric organizations. Its clients are spread across the Americas, EMEA and the APAC region. This fully managed cloud solution runs in Oracle data centers or in an Oracle Cloud at Customer tenant.

It provides the extensive ERP capabilities required by many service industries, while integrating third-party solutions for customers adopting composable architecture for specialized capabilities. Oracle continues to invest in AI capabilities, including its Oracle AI Agent Studio and the continuous release of embedded AI use cases.

- Technology platform: Oracle has strong application and data integration via Oracle Integration Cloud (OIC), in addition to extension development and AI-enabled capabilities through the Oracle Cloud Infrastructure (OCI)-based platform strategy and the evolving Redwood User Experience.

- Market and product positioning: Oracle Fusion’s recommended implementation journeys focus on process standardization, which helps customers seeking transformative cloud initiatives. Its Oracle Cloud implementation methodology, the Oracle True Cloud Method, provides a standardized methodology and combines Oracle Guided Learning along with accelerators that offer recommendations directly within the application during implementation.

- AI and Agent Studio: Oracle has delivered GenAI and agentic AI use cases across the Fusion portfolio, with over 1,000 customers said to be using them in production. Its new AI Agent Studio enables customers to build custom agents or extend prebuilt agent templates, including the ability to test agents’ behaviors prior to production and create multiagent orchestrations for more complex workflows.

- Global partner delivery consistency: Delivery-quality consistency may be variable outside North America, particularly in multicountry rollouts. Some Gartner clients report that global partners, including those offering local regulatory expertise, still lack the depth of Oracle Fusion experience found in local markets. Oracle and its partners are investing in regional capability development and standardized delivery models to improve consistency and reliable global outcomes.

- Oracle ERP on-premises functional parity: Gartner interactions with clients still show on-premises Oracle ERP customers have concerns about gaps between Oracle Fusion and their existing, often customized solutions. Existing on-premises Oracle ERP customers should assess and balance their objectives for functional parity against the longer-term value of continuous innovation.

- Industry-specific focus: Some customers and prospects within priority industries (e.g., healthcare, financial services) report a visible gap between the future vision and what is currently available. Oracle has stated that it will continue to invest in industry-specific innovation with the goal of aligning product capabilities to key vertical segments’ evolving needs.

Oracle (NetSuite)

Oracle NetSuite is a Leader in this Magic Quadrant. It offers a robust ERP suite tailored for service-centric enterprises from startups to upper midmarket organizations. Most of its clients are in the Americas, the U.K. and ANZ, with more limited adoption in broader Europe and APAC. This platform is a fully managed cloud SaaS solution, running on Oracle Cloud Infrastructure (OCI) to harness innovations that enhance the ERP experience.

NetSuite has expanded its embedded GenAI capabilities beyond its initial Text Enhance feature. The strategy includes a broader portfolio of tools, such as NetSuite Expert for contextual help, Prompt Studio for creating custom AI-driven workflows, and a forward-looking roadmap centered on its AI-optimized experience and NetSuite Virtual Support Assistant.

- Unified cloud platform: NetSuite delivers a fully integrated suite of ERP, CRM, e-commerce and professional services automation applications. This unified approach eliminates data silos, ensures seamless process integration and provides a single source of truth for all business operations.

- 360-degree dashboards: Oracle dashboards integrate diverse data points to offer a holistic perspective on crucial business relationships. This functionality ensures reporting and insights are readily accessible across consolidated, subsidiary and detailed transactional levels. NetSuite Analytics Warehouse leverages machine learning algorithms to process customer data, generating predictions, forecasts and classifications.

- Infrastructure: OCI delivers improved performance, scalability and security, while also providing access to Oracle’s portfolio of enterprise cloud solutions — including Autonomous Database, Analytics Cloud, and Integration Cloud.

- Contracting and cost: Compared to other market competitors targeting midsize businesses, NetSuite’s pricing is at the higher end. Its pricing model also varies based on user count, data volume, infrastructure and support tiers; this flexibility may introduce risk due to overly complex contractual terms. NetSuite recently introduced lower-cost, task-specific user licenses for roles requiring limited access, such as approvals or warehouse functions.

- Resource management: NetSuite enables customers to manage internal employee resources and availability, but does not currently provide specific capabilities to support oversight of third-party workers. This limitation may pose challenges for organizations needing comprehensive resource management. Businesses aiming to handle both internal and external personnel will need to consider supplementary third-party solutions.

- Transparency into AI customer adoption data: NetSuite has chosen not to break out specific customer adoption data for its AI and GenAI use cases, which are embedded in existing workflows. Sharing more insights into the adoption and real-world impact of these advanced AI features will help prospective clients fully understand the benefits of Oracle’s AI capabilities provided to NetSuite and its customer base.

Sage

Sage is a Niche Player in this Magic Quadrant. Sage Intacct is a fully managed cloud solution targeted at lower-midmarket customers with some traction also in upper-midsize organizations. Its clients are mainly in North America, but are also in the U.K., Australia, South Africa, France and Germany. Focused on financial management applications, it includes a planning solution, with capabilities developed in-house. For other capabilities in many areas, Sage relies on partner solutions.

Sage recently introduced Sage Copilot to boost insights, improve forecasting and streamline bookkeeping, with features like Variance Analysis, automated invoice processing, and GL Outlier Detection.

Sage declined requests for supplemental information or to review the draft contents of this document. Gartner’s analysis is therefore based on other credible sources.

- Financial management: Sage offers a strong financial management solution targeted at lower-midsize organizations, but with the capacity to scale upward when accounting processes are not overly complex. It offers solid multientity and multicountry global consolidation capabilities. New accounts payable (AP) automation capabilities include AI-driven, multiline general ledger coding. Other enhancements include AP invoice matching with line-level variance notifications, support for complex legal business structures, and synchronizing financial transactions between businesses.

- Support for project-driven organizations: Sage has introduced a Professional Services Automation solution that offers AI-powered project resource management. It includes a project intelligence dashboard that enables project managers, grant managers and administrators to track key performance indicators.

- Improved industry focus: Sage has gained traction in the construction industry as the financial management component of Sage Construction Management. It also supports not-for-profit organizations by connecting operational and financial processes, adding fundraising via DonorPerfect, and supports multientity consolidation and regulatory compliance for the healthcare industry.

- Concentration in North America: Sage has a limited presence outside of North America, despite expanding into key English-speaking markets around the world. It also has expanded into France and Germany. This may still limit some multinational companies faced with compliance and localization requirements.

- Procurement and HR strategy: Sage does not offer a complete source-to-pay solution. It depends on partners to fill the gap in delivering procurement as part of its core finance capabilities. With HR, it doesn’t offer native capabilities for benefits administration, career and succession management, or HR service management.

- Financial planning capabilities: Sage Intacct Planning is fully integrated with its core accounting solution and is sufficient for smaller organizations. Those requiring complex modeling, sophisticated reporting and complex integrations may find it limiting. Sage is working on performance improvements, but organizations should ensure that it supports the full range of their requirements.

SAP (Business ByDesign)

SAP Business ByDesign is a Niche Player in this Magic Quadrant, primarily catering to midmarket organizations. Its clients are in the Americas, APAC and EMEA, which is the largest market for this offering. It has a broad set of capabilities; however, customers must frequently depend on partner solutions for additional functional areas.

ByDesign is considered “fully mature” by SAP. Future updates will only focus on compliance, legal updates, capabilities that uphold SAP product standards and improvements to already supported functionality. Enhancements are delivered through integration with the SAP Business and Technology Platform (SAP BTP) and through partners. Consequently, customers may need to subscribe to specific SAP BTP or third-party services for additional functionality.

SAP will delist SAP Business ByDesign from 20 April 2026, making it no longer available for new customers. Existing customers can continue to use the software and can buy additional licenses until further notice by SAP.

- Extensibility: Customization through low-code tools lets businesses efficiently tailor solutions. AI and ML services enhance operational efficiency, while partners can develop unique, industry-specific capabilities to align with regional demands.

- Industry-specific solutions: Midsize enterprises aiming for quick implementation without extensive process design can benefit from various prebuilt functionalities and processes created by SAP and its partners that address diverse industry needs. Notable industries include professional services, nonprofit, public sector and construction.

- Service provider ecosystem: SAP Business ByDesign has built a robust ecosystem of service providers, offering extensive industry expertise to assist customers with their implementations.

- Product roadmap: As SAP prioritizes SAP Cloud ERP as its strategic focus, Business ByDesign will no longer be offered for sale starting in 2Q26. Currently, there is no easy out-of-the-box migration path to move from SAP ByDesign to S/4HANA Cloud, Public Edition (aka SAP Cloud ERP).

- Service industry partner add-ons: Although SAP provides many of the administrative and operational ERP capabilities required by service-centric industries, customers may experience additional licensing fees for these add-ons and customer-specific solutions.

- Articulated future strategy: SAP is encouraging existing customers to transition to SAP Cloud ERP, while urging partners to enhance their skills for SAP Cloud ERP. However, this message contributes to rising concerns and speculation regarding the future direction of SAP Business ByDesign, leaving stakeholders uncertain about its long-term viability.

SAP (Cloud ERP)

SAP Cloud ERP (formerly S/4HANA Cloud, Public Edition), is a Leader in this Magic Quadrant. SAP’s cloud ERP portfolio includes both public and private cloud options, but only SAP S/4HANA Cloud Public Edition met the inclusion criteria to be evaluated in this research. This product has a global reach and is targeted at midmarket, large and global enterprises. SAP Cloud ERP is sold directly and primarily as a commercial bundle via implementation partners’ channels and has been recently positioned by SAP sales in both RISE and GROW journeys. It is a multitenant SaaS cloud solution and has financial management, O2C, HR, indirect procurement and vendor management capabilities.

Industry verticalization and preconfigured best practices are available for multiple service-centric industries, with additional scenarios via the SAP portfolio. Tighter integration with SAP Analytics Cloud provides more comprehensive and advanced analytical capabilities. SAP recently introduced an AI digital assistant, Joule, and Microsoft Copilot integration, along with Fiori AI-assisted summarization features.

- Modern technology portfolio: SAP Cloud ERP is part of a technology portfolio that includes an associated cloud platform (SAP BTP) offering capabilities to deliver modern customization and integration.

- AI and GenAI: SAP is moving forward with its AI capabilities strategy. Offerings, such as Joule, alongside partnerships with other technology vendors (e.g., Microsoft), will help customers envision how to leverage ERP-embedded AI.

- Global partner support: SAP has one of the most extensive implementation partner networks in the market. This network supports SAP’s presence across multiple geographies and types of customers, enabling customers with a global footprint to consider this solution as a strong contender.

- Cross-functional complexity: SAP Cloud ERP requires separate deployment of stand-alone applications, such as SuccessFactors for HR, as these capabilities are not native to the core platform. Application leaders should account for the operational overhead of managing disparate user experiences and integrations, which may increase administrative burden and complexity, particularly for midsize organizations.

- Live customers in complex organizations: Most live customers are lower and midsize or tier-two organizations. Notable exceptions exist, but SAP’s go-to-market strategy primarily focuses on midsize businesses. Larger global customers should scrutinize this solution against their requirements to ensure it can meet their needs.

- Pricing: Customers looking to adopt embedded AI capabilities or SAP BTP features may find it challenging to understand how their total cost of ownership will be affected by the associated consumption of data and/or messages. This concern is key for customers that anticipate relying heavily on AI-enabled capabilities or extensions created in SAP BTP. SAP recently introduced a new persona-based bundling strategy aimed at reducing complexity.

Workday

Workday is a Leader in this Magic Quadrant. The Workday Suite is aimed at upper-midmarket, large and global organizations. Nearly three-quarters of its customers are in North America, with others in EMEA and APAC. Its native cloud solution focuses on advancing AI capabilities, enhancing UX and expanding its financial and HCM suites.

Workday plans to continue expanding globally into professional services, tech and media, retail and hospitality, financial services, government, education, and healthcare. As part of its next generation of AI, Workday Illuminate, it is developing more AI use cases, including automating transactions, querying data and surfacing insights through its Ask Workday interface. Workday also expanded its developer tools and APIs and acquired Flowise, a low-code platform, to further expand its AI agent building capabilities. Additionally, it is investing in its Agent System of Record strategy for managing and governing agents like digital workers.

- Unified data core: Workday unified data core is fully harmonized across its ERP suite and enhances built-in analytics and AI capabilities. Having a unified data core enables business functions to integrate better because data silos are eliminated, improving operational efficiency and decision-making for users.

- HR capabilities: Workday Human Capital Management is one of the leading HR solutions in the ERP market. Workday has enhanced talent acquisition technology through the development of AI-enabled talent discovery and job recommendations, both of which are intended to increase the efficiency of recruiting operations.

- User experience: Workday customers cite high satisfaction with customer support in addition to an active user community and its highly collaborative approach to product development. Additionally, they rate Workday’s user-friendly interface highly, stating that it helps drive strong adoption.

- Global support: Workday lags other Leaders in geographic reach, which is critical for large global enterprises headquartered outside of North America. Recently, Workday decided against building some of its own global payroll capabilities and instead invested in a partner strategy with Global Payroll Connect. Prospective buyers should review the offering and Workday’s localization capabilities to decide if they sufficiently meet their needs.

- Partner ecosystem: Workday continues to invest in expanding its partner network, but this ecosystem can be thin in specialized industries or emerging regional markets compared to its leading competitors. New Workday customers should evaluate partner capabilities to ensure they are sufficient to meet their needs.

- Native recurring billing management: Workday partners for B2C usage-based billing, and it recently released Workday Revenue Center, which expands support for B2B usage-based billing. Prospective buyers should determine whether these offerings meet their requirements versus other available third-party solutions.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

No vendors were added to this Magic Quadrant.

Dropped

No vendors were dropped from this Magic Quadrant.

Inclusion and Exclusion Criteria

To qualify for inclusion, providers need to deliver a suite of cloud-based, service-centric ERP applications

that include the following criteria.

Product Capabilities

- Financial management functionality — General ledger, accounts payable, accounts receivable, fixed assets, cash management and financial planning.

- Order-to-cash — Provide a substantial component of functionality by vertical as described in the vendor questionnaire.

- HCM — Provides administrative HR capabilities such as core hr data management, employee life cycle transactions, and position management. May also include payroll and benefits administration. It should also provide support to talent management, including a minimum of three of the following functions: recruiting, onboarding, performance and goals management, career and succession management, learning management, and compensation management. It is expected that the aforementioned functions support employee and manager self-service via browser and mobile application.

- Source to pay (S2P) — Includes e-sourcing, contract management, e-purchasing, AP invoice automation, supplier management, collaboration and payments (can involve supplier master data), order confirmations, and changes through a network or portal.

- Other administrative ERP — Supports service-centric industries, such as expanded planning and analysis (xP&A), project management (for project-centric capabilities), planning, services procurement and real-estate lease management.

Market Presence

- The vendor must have at least 750 organizations with annual revenue/expenditures/funding of more than $75 million in production using the ERP application. Each organization must be live with at least three of the components (modules) of operational ERP — including finance, HCM and procurement. Vendors must be prepared to provide evidence of sufficient in-production customers. If a vendor chooses not to disclose this information, Gartner may use its own market research, as well as insights from public sources, to judge that vendor’s eligibility for inclusion and viability.

- These 750 organizations must be managing at least $150 million annually through the ERP suite. The annual revenue of a parent organization cannot be used when only a smaller subsidiary uses the cloud service as a lower-tier ERP.

- The vendor must actively sell and market the cloud service (and have live users of the cloud service in the qualifying revenue ranges) outside of its home region. Gartner defines regions as the following: Americas, EMEA or APAC. At least 25% of the cloud service revenue must be from outside of the vendor’s home region.

- The vendor must have at least $125 million in booked subscription and support revenue for the ERP suite cloud service only (that is, excluding any revenue from on-premises, hosted, managed cloud service or other deployment models) from January 2024 through December 2024 (or whichever 12 months accounting period most closely aligns with that period). Unrealized recurring revenue may not be included. If a vendor chooses not to disclose revenue information, Gartner may use its own market research, as well as insights from public sources, to judge that vendor’s eligibility for inclusion and viability.

Cloud Service Attributes

The ERP suite must be deployed as a cloud service, meeting the following attribute definitions.

- Responsibility:

- The vendor must manage all technology infrastructure either in its own data centers or in third-party data centers.

- The vendor must implement upgrades as part of the cloud service, not a third party or managed service provider.

- Licensing and technology:

- The cloud service must be licensed on a subscription basis or metered pay for use.

- Users cannot have a contract that is only for them (except for minor adjustments), nor can they be provided with a version different to that offered to other cloud customers.

- The cloud service must use internet technologies. Use of internet files, formats and identifiers are necessary for delivery of cloud service interfaces.

- Computing resources used to support the cloud service should be scalable and elastic in near-real-time rather than based on dedicated hardware/infrastructure.

- Customization:

- Modification of source code should not be possible. Configuration via citizen developer tools and extension via a platform as a service (PaaS) — by partner, vendor or user is allowed.

- Pace of Change:

- A single code line is used for all customers of the cloud service to allow rapid deployment of new functionality by the vendor.

- The vendor must deliver at least two upgrades containing new functionality per annum to all users of the cloud service and control the pace of the update cycle. All customers must be on the current upgrade version before the release of the next upgrade version — this requirement applies to the specific partner solutions that supplement the core mandatory set of features highlighted in the previous sections.

- The vendor must offer self-provisioning capabilities for the service (at least for development and test instances) without involvement of its own staff.

- The technology used to deliver the service must be shared by multiple customers to create a pool of resources from which elasticity can be delivered.

These inclusion criteria relate to a cloud service based on a single code line with a unique user interface and data model. For vendors offering multiple cloud ERP suites each with its own code line, each solution must meet the identified inclusion criteria (that includes any partner solution that is part of the mandatory features for consideration in this research); for example, each cloud ERP suite must have at least 750 organizations in a production environment.

This Magic Quadrant reflects Gartner’s definition of “composable ERP.” We define this as an adaptive technology strategy that enables the foundational administrative and operational digital capabilities for an enterprise to keep up with the pace of business change. This strategy delivers a core of composable applications and, as a service, software platforms that are highly configurable, interoperable and flexible to adapt to future modern technology.

Consequently, if a vendor’s cloud ERP suite consists of capabilities from different code lines, that vendor will be included in the Magic Quadrant provided its solution:

- Has predefined workflow integrations.

- Uses vendor-supported integration technologies.

- Is positioned as a component of a broader “solution,” rather than as a stand-alone product in the vendor’s portfolio, and the vendor has users of the full solution in production.

The inclusion criteria are the specific attributes that a provider must have to be included in this Magic Quadrant.

Honorable Mentions

The following vendors did not qualify for inclusion in this Magic Quadrant, but nevertheless merit consideration by enterprises with specific needs in certain industries or regions:

- Infor: This vendor did not satisfy the criteria for the minimum number of organizations (with revenue exceeding $75 million) in production using the ERP application and for having at least 25% of cloud service outside its home region. Infor’s go-forward market strategy is to focus on healthcare, financial services, HCM and the public sector in North America.

- Ramco Systems: This vendor did not satisfy the criterion for minimum yearly booked revenue ($100 million) from its cloud service ERP suite.

- TOTVS: This vendor focuses on Latin America and did not meet the criterion for selling cloud solutions outside its home region.

- Unit4: This vendor did not satisfy the criterion for selling the cloud solutions outside its home region.

- Yonyou: This vendor focuses on the APAC region and did not satisfy the criterion for selling cloud solutions outside its home region.

Evaluation Criteria

Ability to Execute

Gartner assesses vendors’ Ability to Execute by evaluating the products, technologies, services and operations that enable them to be competitive, efficient and effective in this market, and that benefit their revenue, client satisfaction and retention, and general reputation.

Each provider’s Ability to Execute is judged by its success in fulfilling its promises, using the following criteria:

- Product or service: This criterion assesses the product offerings that compete in the defined market. These may be offered natively or through original equipment manufacturer agreements and partnerships, as defined in the market definition/description section and detailed in any subcriteria. This Magic Quadrant evaluates functional capabilities in all areas defined in the market definition/description section, support for the needs of midsize, large and global enterprises, and the ease with which the cloud service can integrate with other cloud/on-premises applications.

- Overall viability: This criterion includes an assessment of the vendor’s overall financial health, as well as the financial and practical success of the relevant business unit. It considers the likelihood of the vendor continuing to offer and invest in its product, as well as the product’s position in its portfolio.

- Sales execution/pricing: This criterion assesses the vendor’s abilities in all presales activities and the structure that supports them. Included here are deal management, pricing and negotiation, presales support, and the sales channel’s overall effectiveness. Each vendor is also evaluated on its ability to sell ERP.

- Market responsiveness/record: This criterion assesses the vendor’s ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customers’ needs evolve and market dynamics change. The market for cloud ERP suites is dynamic, so this criterion addresses the vendor’s ability to respond to users’ needs and demands. This includes its responses to the demands of delivering service-centric ERP applications in the cloud, which pose new challenges for vendors and users.

- Marketing execution: This criterion assesses the clarity, quality, creativity and efficacy of programs designed to convey the vendor’s message, influence the market, promote a brand, increase awareness of products and establish a positive identification in customers’ minds. Vendors can create this “mind share” by combining publicity, promotions, thought leadership, social media use, referrals and sales activities.

- Customer experience: This criterion assesses the vendor’s products, services and programs in terms of how they enable customers to achieve expected results with the products evaluated. Considerations include the quality of technical support for vendor-buyer interactions and account support. Also assessed is the vendor’s ability to make its marketing vision a reality and help teams complete the transition from on-premises to cloud deployment.

- Operations: This criterion assesses the vendor’s ability to meet its goals and commitments. Factors include the quality of the organizational structure, skills, experiences, programs, systems and other means that enable the organization to operate effectively and efficiently. In particular, we analyze the vendor’s ability to deliver a robust and reliable cloud service, as well as its associated support and service capabilities (whether provided directly or through partners).

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | High |

Market Responsiveness/Record | High |

Marketing Execution | Medium |

Customer Experience | High |

Operations | High |

Source: Gartner (September 2025)

Completeness of Vision

Gartner assesses vendors’ Completeness of Vision by evaluating their ability to articulate their perspectives on the market’s current and future direction, anticipate customer needs and cloud technology trends, and address competitive forces.

Each vendor’s Completeness of Vision is judged on its understanding and articulation of how market forces can be exploited to create new opportunities for itself and its clients, using the following criteria:

- Market understanding: This criterion assesses the vendor’s ability to understand customers’ needs and relate those needs to products and services. Vendors with a clear vision of their market listen to and understand customers’ demands and can shape or enhance the market. We analyzed vendors’ understanding of how the market for service-centric ERP suites is shifting to the cloud and what that means for functional capabilities.

- Marketing strategy: This criterion looks for clear, differentiated messaging that is communicated consistently both internally and externally through social media, advertising, customer programs and positioning statements. We analyzed how effective a vendor’s marketing strategy was at raising awareness of its offering in this new and evolving market.

- Sales strategy: This criterion looks for a sound strategy for selling that uses appropriate networks, including direct and indirect sales, marketing, service, and communication networks. It also assesses any partners that extend the scope and depth of the vendor’s market reach, expertise, technologies, services and customer base.

- Offering (product) strategy: This criterion looks for an approach to product development and delivery that emphasizes market differentiation, functionality, methodology and features in light of current and likely future requirements.

- Business model: This criterion assesses the suitability of the design, logic and execution of the vendor’s business proposition in terms of the likelihood of achieving continued success.

- Vertical/industry strategy: This criterion assesses the vendor’s strategy to direct resources (e.g., sales, product and development), skills and products to meet the specific needs of individual market segments, including industries. Each vendor was assessed on its strategy for service-centric industries.

- Innovation: This criterion assesses direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or preemptive purposes. In particular, we analyzed each vendor’s strategy for using cloud delivery, AI, user experience and platform services as a way of bringing innovation to ERP functions and processes.

- Geographic strategy: This criterion assesses the vendor’s strategy for directing resources, skills and offerings to meet the needs of areas outside its home region, either directly or through partners, channels and subsidiaries, as is appropriate for that region and market. We evaluated each vendor’s strategy for providing the localizations and translations required to support multinational and global organizations. We also assessed each vendor’s global go-to-market approach.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Medium |

Sales Strategy | High |

Offering (Product) Strategy | High |

Business Model | Low |

Vertical/Industry Strategy | Medium |

Innovation | High |

Geographic Strategy | High |

Source: Gartner (September 2025)

Quadrant Descriptions

Leaders

Leaders demonstrate a market-defining vision for supporting and advancing service-centric ERP systems and processes in the cloud, with particular strength in core financial management. They consistently execute this vision through products, services and go-to-market strategies, along with solid customer service and support. Leaders maintain a strong and expanding global presence, serving a wide range of organizations across industries and regions while servicing enterprises of different sizes. They have multiple proofs of successful deployments by customers in their home region and elsewhere. Their offerings are characterized by deep and broad ERP functionality, scalable and composable architectures and ongoing innovation, particularly in AI and automation. Leaders’ extensive partner ecosystems further enable successful business transformation and support complex customer requirements.

Organizations should also be aware that Leader’s offerings may introduce complexity in implementation, require careful evaluation of vertical-specific capabilities, and necessitate close attention to contract terms and pricing models. Specific vertical market needs or other, more specialized segments, might be better addressed by Niche Players. Similarly, Leaders may also be too complex to deal with or too costly to be considered in less complex functional scenarios.

Challengers

Challengers have greater market presence than Niche Players and Visionaries. They may have developed a substantial presence in one area of the market, but they lack a sufficiently broad vision to execute consistently and more widely in the market. They tend to have a viable and proven cloud service, but they focus on a specific size of enterprise or selection of industries.

Challengers can become Leaders if they develop their vision for, and focus on, this market. Large companies may move between the Challengers and Leaders quadrants as their product cycles shift and market needs change.

Visionaries

Visionaries understand how the organization is changing as it moves to a service-centric cloud ERP system. They have a good vision for technology and functionality, but are limited in terms of their Ability to Execute or to demonstrate a track record. Their solutions attract enterprises that want to move service-centric capabilities aggressively to the cloud, and they may have some differentiating functional capability. Visionaries are typically limited in terms of market presence, geographic presence outside their home region, and the market’s awareness of them and their products. Hence, user organizations should closely evaluate the extent of Visionaries’ presence in their industry segment and region.

Visionaries may become Challengers or Leaders, depending on how they strengthen their go-to-market capabilities and whether they can develop partnerships that complement their strengths.

Niche Players

Niche Players offer service-centric ERP capabilities, but are limited in their Completeness of Vision and Ability to Execute, and may not have the full footprint of capabilities. Instead of a strong cloud technology vision, some may offer narrower cloud platform capabilities or industry focus. Although they do sell and market these applications on a stand-alone basis, this is neither their focus nor part of their primary go-to-market strategy. Consequently, they typically have a weaker vision for business transformation needs than do Leaders and Visionaries. They may also target specific industries or company sizes with deeper functionality (e.g., several Niche Players focus on project-centric and midsize enterprises).

A Niche Player may be suitable for some customers’ requirements, and all Niche Players in this Magic Quadrant should be considered viable contenders. Prospective customers of a Niche Player should assess how well-aligned that vendor is with the market’s direction and their potential business strategic direction. A Niche Player may be a risky choice if this assessment shows it is not following the trends of a specific industry or market.

Context

ERP is among the top items on the list of application projects approved in budgets during the past two years. Evaluating and selecting vendors to fulfill business and technical requirements is the key to successful ERP journeys. In 2025, Gartner’s client inquiry data shows a continued and rising interest for AI-enabled strategies and composable ERP when selecting modern cloud ERP solutions. Offsetting this heightening interest, however, more than half of ERP leaders participating in Gartner’s 2024 Enterprise Application Leaders Signature Survey stated aligning business and applications strategies remains a top challenge when evaluating these solutions.1

While transformative capabilities and technology are being rolled out in cloud ERP, the business remains insufficiently engaged to decipher its usefulness with respect to business objectives and strategy. That’s because many business leaders still perceive ERP as “software,” as opposed to a set of practices for managing and optimizing enterprise resources. ERP leaders must view their evaluations of modern cloud ERP and associated emerging technologies as a joint effort between IT, business stakeholders and process leaders as they guide their organizations to successfully adopt a service-centric cloud ERP solution (see What IT Leaders Must do to Avoid Disappointing ERP Initiatives).

As IT and business participants evaluate service-centric cloud ERP solutions, they should be aware that the two trends of AI and composable ERP will support the basis of their ability to deliver increasing layers of business value beyond traditional solutions.

Vendors have recognized a large, untapped demand for transactional automation and are rapidly introducing AI features that address the ERP processes common to most companies. Gartner predicts that by the end of 2025, AI assistants will be embedded in almost every enterprise application, and by 2026, 85% of large ERP providers will have some agentic and GenAI capabilities in preview, pilot or early adopter phase.2 In the future, ERP applications will do much of the work that is now done manually and will assist users as they navigate complex processes and make decisions. Gartner forecasts that 62% of 2027 spending will be on ERP applications with AI capabilities, a major increase from 14% in 2024.3 These applications will also pull together data from throughout the enterprise to create new levels of insight. AI agents will be able to make autonomous decisions and act independently without manual user intervention. Ultimately, a very large share of tasks currently performed by employees will instead be performed by autonomous AI agents working in conjunction with each other (see Innovation Insight: AI Is on the Cusp of Reshaping ERP).

Application leaders evaluating service-centric cloud ERP solutions must also understand and be prepared to evaluate the technologies and frameworks that underpin a composable strategy. Gartner predicts that by 2027, 60% of organizations replacing ERP applications will select software for the platform and business process orchestration capabilities, rather than for the software’s transactional planning capabilities.4 This is because composable ERP strategies and associated vendor platforms enable both technical flexibility and continuous improvement, as well as a stable foundation for embracing emerging automated capabilities. Organizations must employ responsive, composable approaches that continue to evolve in order to remain future-ready.

Composable ERP strategies keep growing in interest among organizations that realize flexibility and agility in their strategy are a requirement to support an increasingly volatile business landscape. Composable architecture and modular software increase ERP users’ ability to “compose” their business processes and optimize their use of enterprise resources. This approach increases the importance of ensuring ERP vendors’ business process orchestration, integration and data management capabilities are thoroughly evaluated (see Navigate 10 Ugly Truths of Composable ERP).

Additional emerging technologies and capabilities, such as adaptive experience and decision intelligence, are also affecting forward-looking, service-centric ERP evaluations. Adaptive experience provides the ability to tailor workflows, interfaces and functionalities to the needs, preferences and behaviors of different users or business scenarios. Decision intelligence integrates advanced analytics, AI and data-driven insights into ERP solutions to support and enhance business decision-making and improve competitive advantage. These emerging technologies reflect today’s more complex, multivendor ERP technology landscape, and they often differ in terms of adoption, maturity and benefit. When evaluating solutions, ERP leaders must analyze them against their business requirements and plan for their adoption now, because the changes associated with them eventually will be significant. In many cases, these solutions will lay the foundation for even greater change in the future. To assist in this process, Gartner covers a full range of these technologies and capabilities (see Hype Cycle for ERP, 2025).

ERP can significantly increase organizations’ chances of ERP success by evaluating highly configurable and composable service-centric cloud ERP solutions capable of harnessing modern AI and other emerging technologies that are well-aligned with business strategy and deliver tangible benefits.

Market Overview

Service-Centric Cloud ERP Market Remains Strong

The ERP market continues to represent a significant portion of the enterprise applications market. According to Gartner’s analysis, the 2024 ERP software market grew 11.3% to $66 billion (from $59 billion). Cloud ERP adoption, GenAI and agentic AI messaging, as well as a cautious macroeconomic environment, influenced the market’s growth. Most providers saw a positive but lower rate of growth due to the ongoing macrochallenges that affected the global economy in 2024. Administrative ERP capabilities (e.g., HCM software and financial management software [FMS]), which are especially critical to service-centric organizations, represent nearly 90% of ERP revenue (see Market Share Analysis: ERP Software, Worldwide, 2024).

The service-centric cloud ERP market is robust, with a multitude of vendors providing competitive solutions for both midsize and large organizations. While no single vendor holds a dominant position overall, a few key vendors supply the majority of new and existing solutions for large organizations. For midsize organizations, numerous vendors offer products, some specializing in particular geographies or sectors within the service industry. However, these solutions may not possess the same breadth and depth of functionality as those designed for larger organizations.

The vendors in this Magic Quadrant all actively sell and market service-centric ERP to midsize and large organizations on a stand-alone basis, even if they have a broader ERP suite offering. Although some vendors sell opportunistically to small businesses, this Magic Quadrant does not cover service-centric ERP solutions targeted exclusively at small businesses.

ERP Platforms Continue to Move Quickly to the Cloud

Service-centric organizations continue to move ERP platforms to the cloud, embracing it faster than product-centric organizations. The consistently higher growth of service-centric as opposed to product-centric (or operational) ERP is due in part to the higher prominence of cloud revenue within HCM and FMS, versus on-premises-based software revenue, which is a significant revenue contributor to core manufacturing and operations.

The pressure of digital transformation and replacement cycles is driving service organizations to modernize and improve their back-office processes. ERP leaders continue to focus on finding approaches to modernize their ERP strategies via cloud migration and SaaS adoption. At the same time, ERP vendors are accelerating their pace of innovation, leading to the broader consideration of GenAI and germinating agentic AI. As organizations prioritize agility and efficiency, Gartner continues to see increased interest in cloud ERP solutions that facilitate collaboration, automate processes and provide real-time insights for informed decisions. Continuous investments from ERP vendors to enable AI-embedded features, alongside increasing interest from clients to take advantage of such capabilities, are among the principal drivers behind the uptick in on-premises-to-cloud ERP migrations.

AI Represents Transformational Opportunity

As organizations migrate their administrative processes to the cloud, support functions increasingly drive the business’s digital transformation. As AI technology evolves, its integration with ERP systems will play a pivotal role in shaping the future of service-centric industries. Emerging technologies like AI are further enhancing digital processes and improving user experiences through features such as content recommendations, automated accessibility and intelligent resource management. In exploring the transformative potential of AI in ERP systems, service-centric companies are poised to unlock unprecedented insights for strategic decision-making while substantially automating many end-to-end processes.

Gartner predicts that by 2031, ERP with agentic AI and GenAI will surpass that of non-AI offerings (see Emerging Tech: Market Risk Projection of Generative AI on ERP Software). Through 2030, AI has the potential to significantly elevate and transform productivity, usability and business outcomes for ERP software, especially when augmented with agentic AI capabilities that are becoming available. While still in the early stages of development, agentic AI has the potential to greatly automate workflow tasks within ERP processes, enabling users to devote more time to value-added activities. Service-centric organizations will use AI to automate repetitive tasks and reduce human error in processes such as data entry, invoice processing and recruitment, seeking to enable employees to focus on more value-added activities that enhance operational efficiency and accuracy. These organizations will likewise leverage AI to improve decision-making and planning capabilities — including demand forecasting, resource allocation, profit optimization and capacity planning — to improve margins and deliver better service, predict periods of high service demand, and optimize staffing levels.

Robust, Complete Functionality Improves Implementations

Service-centric ERP implementations have advanced significantly thanks to more robust and comprehensive functionality. Improvements are evident in areas such as service configure, price and quote (CPQ); recurring billing management and revenue recognition; supplier and contract life cycle management; extended planning and analysis (xP&A); and integrated PSA. These enhancements are emerging within the context of a composable application architecture, prompting organizations to consider ERP solutions for a broader range of needs due to the availability of these new components.

Many organizations seek to improve their order-to-cash (O2C) strategies by adopting a consolidated solutions approach, where feasible, while still prioritizing applications that best fit their functional requirements. Given the close integration of O2C with FMS’ and procurement, organizations increasingly recognize the benefits of a more unified ERP approach, rather than purchasing core financials and extensions separately. By 2027, Gartner predicts that more than 50% of service-centric enterprises will look for an ERP-suite approach to meet their need for system-of-record capabilities.

Many of the ERP solutions focused on service-centric industries are becoming more robust in their depth of coverage, with many rivaling the capabilities of the best-of-breed products. Vendors are offering more industry-specific features that address the unique operational, regulatory and customer requirements of service-centric organizations. This trend will continue as more functionality makes its way into the suite, increasing the compelling rationale to seek a more integrated, service-centric ERP approach and easing the degree of integration required in implementations.

Acronym Key and Glossary Terms

| ERP | Enterprise resource planning |

| FMS | Financial management suite |

| HCM | Human capital management |

| O2C | Order-to-cash |

| xP&A | Extended planning and analysis |

1 2024 Gartner Enterprise Application Leaders Signature Survey. This study was conducted to understand how enterprise application leaders are pursuing and implementing innovative technologies.

The research was conducted online from January through March 2024 among 272 respondents from organizations across all industries in North America (n = 143), Europe (n = 70) and Asia/Pacific (n = 50) with annual revenue of $500 million or more. Soft quotas were established for company size, type of industry, applications portfolio (CRM, digital workplace and ERP), and respondent’s function type and job level to ensure a good representation across the sample.

Organizations were required to have deployed or plan to deploy within two years at least one of the following technologies: generative AI, augmented analytics, digital experience monitoring, hyperautomation or intelligent applications.

Respondents were midlevel managers or above, directly involved in the applications portfolio and were required to have certain responsibilities when related to its innovative technologies. In addition, respondents were required to have knowledge of technology innovation funding, technology innovation deployment models and technology innovation priorities.

Disclaimer: The results of this survey do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.

Additional Notes:

Gartner used several sources of input for the inclusion criteria, market definition and vendor evaluations in this research. The primary sources of data include:

- Author interactions with more than 1,000 end-user clients on their ERP application strategies since 2021

- Peer Insights survey data through 31 January 2023, blended with demo, special survey and inquiry insights

The evaluation of vendor products for many of the categories was developed using a multianalyst approach, in which finance, O2C, HCM, procurement and operations were evaluated separately, then consolidated to create a weighted-score. The weights were based on the main drivers of purchasing a service-centric ERP, based on years of inquiry from Gartner clients, as well as the combined experience of the authors.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.