How AI Workhubs Will Disrupt Microsoft’s Productivity Suite

24 February 2026 - ID G00846368 - 11 min read

By Joe Mariano, Nikos Drakos, and 2 more

GenAI and AI agents will create the first true challenge to mainstream personal and team productivity suites in over 30 years. To prepare, IT leaders must move beyond a generic one-size-fits-all strategy to a strategic portfolio approach that profiles users and matches them with appropriate AI capability tiers. This shift is critical to combatting vendor licensing structures that prioritize universal overlicensing over rightsized value.

Insights at a Glance

The Reality: Microsoft 365 is the dominant digital workplace tool, with a market share majority as modern enterprises’ standardized infrastructure. However, this enables vendors to design licensing structures that discourage rightsizing, making overlicensing an entire workforce easier than profiling individual needs. Relying solely on a monolithic ecosystem risks prioritizing vendor-driven continuity over innovation, creating a document-centric workflow trap that fails to deliver value commensurate with rising prices.

The Challenge: While Microsoft 365 remains a technology foundation, multitiered AI benefits are burgeoning (e.g., Microsoft Copilot Chat vs. Microsoft 365 Copilot). To avoid overlicensing, EA leaders must aggressively defend budgets by mapping AI tiers to specific user roles rather than accepting a “premium” default for all.

The Solution: A hybrid portfolio is the true strategic opportunity. Integrate best-of-breed specialized tools alongside core suites to:

- Avoid stagnation: Break traditional suites’ document-centric rut.

- Leverage specialized agents: Use tools where AI is built for specific workflows (like project management or design) rather than generic assistance.

- Maintain leverage: A modular stack prevents total vendor lock-in, providing flexibility to swap out AI layers as the market matures.

Strategic Action: Rightsizing the intelligence-tier success requires moving beyond a binary choice between major vendors. Organizations must architect a tiered ecosystem for a core data and identity foundation, and allow more specialized agent layers to flourish in high-impact departments. Future value will be measured by the ability to profile users and rightsize AI purchases based on utility rather than vendor-mandated bundles.

Strategic Planning Assumptions

Through 2027, GenAI and agent use will create the first true challenge to mainstream productivity tools in 30 years, prompting a $58 billion market shake-up.

Through 2029, a majority of Microsoft-centric organizers will spend 30% to 50% more on Microsoft software and SaaS every three years without having a budget for such a significant increase.

Issue Context

The Shift in Paradigm

AI workhubs are the use of artificial intelligence to enhance content creation and automate workplace tasks, decision making and collaboration, increasing efficiency and effectiveness for employees. It encompasses a set of evolving services that may converge markets such as collaborative work management, visual collaboration, workstream collaboration, intranets and other leading productivity tools. AI workhubs extend beyond basic AI chat services by delivering industry-specific context and role-based support, tailored to employees’ job functions and collaboration needs within their organizations.

The productivity market is experiencing structural changes. The industry is moving from a general editor-focused model, which involves manual user interaction with static files, to an agent-focused model, where users assign tasks to an AI orchestration layer. This change is expected to facilitate the integration of orchestration and modeling layers with existing office tools, making orchestration more accessible to employees as part of the productivity toolkit. This transition results in a distinction within the enterprise technology stack:

- The Data Layer (The Anchor): Incumbent services (e.g., Amazon, Google, Microsoft) retain massive “data gravity” due to established identity, security and compliance frameworks. Legal records and foundational data repositories will likely remain within these ecosystems.

- The Orchestration Layer (The New Interface): User workflows are increasingly decoupling from the traditional productivity suites’ native interfaces. Instead, organizations are adopting specialized orchestration platforms (e.g., Asana, DeepL, Miro, monday.com, Superhuman) or horizontal agents to intake, triage and route work efficiently. With workflow handled via Agent2Agent (A2A), model context protocol (MCP) and API integrations (e.g., using tools like Zapier to connect disparate applications), teams can streamline processes across various systems.

The Strategic Consequence: To mitigate vendor lock-in and capture emerging value, application leaders must adopt a portfolio approach. This involves securing the foundational data layer with established suites while layering specialized agentic tools on top to drive domain and role-specific workflow automation.

Impact Brief

AI Workhubs’ Impact on the Digital Workplace

Microsoft 365 will continue to provide a significant technology foundation in the digital workplace for the foreseeable future. Even Google Workplace deployments tend to run alongside Microsoft 365 in most large organizations. Microsoft Excel and SharePoint are key products that many organizations find indispensable. And although Microsoft Teams has been unbundled from Microsoft 365 due to regulatory pressures, most clients find the product to be an important technology for communications and collaboration.

The questions Gartner clients often ask are:

- Can we move away from Microsoft 365 in favor of a best-of-breed approach or move to alternatives like Google Workspace?

- How can we choose the right mix of investments to make in Microsoft 365 to balance cost and value?

Increasingly, AI workhubs are the key factor in deciding whether to go deeper with Microsoft and what is familiar, or to find alternatives that break the habits of employees to aim for transformation of work. While Microsoft 365 Copilot is steadily evolving, the window of opportunity is still open for organizations looking to broaden their AI workhubs tools strategy and lessen dependencies on Microsoft (see Use the Coming GenAI Workhubs Revolution to Rethink Your Microsoft Relationship).

As enterprise application leaders look toward the future, the conversation is shifting. The focus is increasingly on delivering a modern, engaging and AI-first employee experience — one that balances cost, flexibility and innovation. This requires reevaluating long-held assumptions about all-in-one productivity suites, exploring best-in-class alternatives and refining vendor management strategies that encourage innovation over contract consolidation.

Over the long term, best-in-class services from areas such as Asana, Canva, ClickUp, DeepL, Miro, monday.com, Notion and Superhuman are poised to fuel market competition, catalyzing the development of a new generation of AI-first productivity platforms. At the same time, established organizations like Anthropic, Google, Microsoft, and OpenAI are pursuing AI-first productivity strategies. However, they may face agility challenges due to the constraints of their existing ecosystems. Some organizations may also struggle because they lack such ecosystems altogether.

Implications

The AI Workhub Will Evolve With AI Productivity

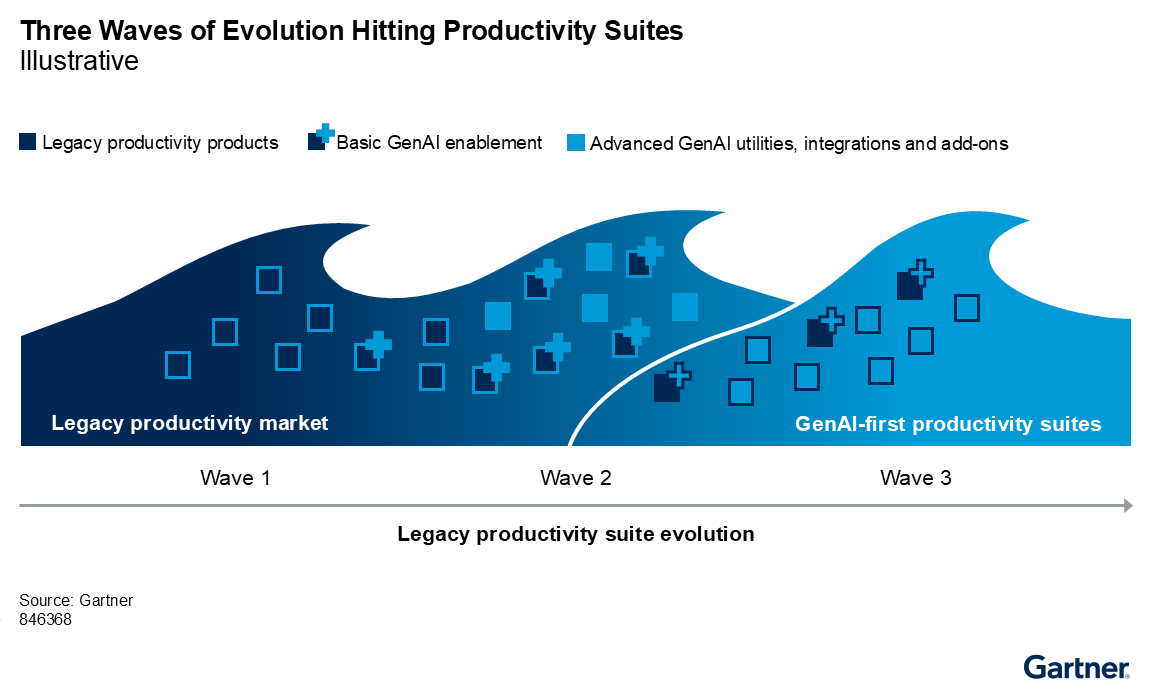

This change will not be instantaneous; products will evolve through three distinct waves of capability. To disrupt the entrenched dynamics of the productivity market, vendors and buyers must look beyond simple editing tools toward true agentic behavior (see Figure 1).

Wave 1: GenAI Integration and Economic Realignment (2023 to 2027)

- Focus: GenAI functions are integrated directly into existing productivity tools (e.g., Copilot for Microsoft 365, Gemini for Google Workspace).

- Capability: Users adapt these “side-panel” features into existing manual workflows.

- Strategic Shift: GenAI begins changing the economics of switching. For organizations wanting GenAI for all users, the perceived cost of migrating from Microsoft to Google Workspace (or vice versa) decreases as AI becomes the primary value driver over legacy file compatibility.

Wave 2: Process Optimization and Vertical Components (2025 to 2029)

- Focus: Transition from generic assistants to specialized, modular components.

- Capability: Multiple vendors release GenAI components specifically designed to replace, accelerate and optimize core business work processes (e.g., automated project intake, autonomous triage and context-aware synthesis).

- Strategic Shift: The workforce begins to delegate operational tasks to these specialized layers rather than just using AI for drafting text.

Wave 3: The AI-First Suite and the Innovator’s Dilemma (2028 and Beyond)

- Focus: Market maturity and radical architectural redesign.

- Capability: Early components and vendors either mature, get acquired or fail, eventually resurfacing as part of a new generation of AI-first suites. These suites feature a massive redesign with entirely new user interfaces, content types and document formats.

- Strategic Shift: This represents a classic innovator’s dilemma for incumbents like Microsoft. They must choose between responding to competitive products that offer radically improved functions or maintaining the legacy compatibility and familiarity that their massive enterprise base expects.

How to Prepare for AI Workhubs

Develop and prioritize high-impact AI workhubs use cases that specifically drive increased employee adoption, rather than focusing on general all-purpose applications.

- Research shows that only 18% of employees feel their organization provides support to integrate GenAI tools into their daily work.1 To help alleviate this issue, utilize Tool: Digital Employee Experience Journey Map to identify specific business processes, such as legal discovery, R&D summarization or complex data extraction, where GenAI can deliver measurable time savings.

- Implement GenAI tools in these areas and track “minutes saved per day” with AI application telemetry and analytics guidance from Gartner.

- Leverage Toolkit: Business Case Templates for Enterprise Applications to quantify productivity improvements and build a compelling case for further investment, especially in environments with overlapping tools like Google Workspace and Microsoft 365.

Ensure AI workhubs have access to the right information by prioritizing integration and interoperability across workplace tools.

- Data from the Magic Quadrant for AI Application Development Platforms provides insights into a rapidly growing market where over 41% leaders have said embedding advanced AI capabilities into their enterprise systems is a top priority.2

- Leverage Gartner’s strategies in How Generative AI Is Impacting Integration Teams to help modernize integration strategies and move beyond traditional iPaaS to composable and event-driven architectures.

- Ensure seamless interoperability between suites like Google Workspace or Microsoft 365 and core systems such as CRM, ERP and communication hubs through APIs and context-aware protocols.

- Strengthen identity governance to support secure, agentic workflows, enabling AI agents to access and interact with enterprise tools and databases. This approach eliminates information silos, ensures accurate version control and empowers AI to deliver context-aware productivity enhancements.

Maximize AI workhubs by curating content access that is meaningful to employees.

- Only 14% of IT leaders report high confidence that their content and data can provide value for AI and human interactions.3 Utilize Gartner’s Structure Content (Unstructured Data) for AI and Knowledge Management Initiatives to ensure your AI tools interact only with high-quality, curated data, reducing the risk of “garbage in, garbage out.”

- Maintain incumbent productivity suites as a foundational data layer, and strategically integrate specialized agent layers (such as Asana or Miro) to automate domain-specific workflows.

- Apply Tool: Employee Personal Template to assess user roles and rightsize AI capability tiers, helping you mitigate digital friction, avoid vendor lock-in, and control licensing costs.

- Leverage Gartner’s security and risk management frameworks such as TRiSM (see Govern AI Using TRisM: The Technical Framework for Trust, Risk and Security) to enforce agent-level security and customized policies. This will help ensure sensitive information is compartmentalized and risk is dynamically managed as your portfolio evolves.

Ensure effective AI adoption and employee enablement by applying a human-centric learning strategy.

- Only 20% of IT leaders report their organizations provide personal and/or role-based guidance to drive GenAI user adoption.3 IT leaders will need to tailor the AI workhubs experience to the employees role. To do so, leverage The AI-Era Learning Manifesto: Outcome-Driven Agile Learning to design rigorous training and enablement programs that go beyond basic prompt engineering, helping employees fully utilize nuanced AI features within the workhubs services employees utilize.

- Use the manifesto’s guiding principles to identify strategic use cases, support collaboration, flexibility and engagement, and foster a digital workplace where AI augments human capability.

- Apply the manifesto’s framework to establish collaborative governance, prioritize transparency and accountability in AI decision making and commit to continuous learning so employees can adapt to evolving risks and avoid the creation of information silos from stand-alone tools without robust integration.

1 The 2024 Gartner Employee Perspectives on the Future of Work Survey. This survey was conducted to understand employee perspectives regarding various emerging technologies, and how it impacts their daily work. The research was conducted online from 20 August through 27 September 2024 and contains responses from 3,496 employees with representation from various geographies, industries and functions. Disclaimer: The results of this survey do not represent global findings or the market as a whole but reflect the sentiments of the respondents and companies surveyed.

2 Gartner Software Engineering Survey for 2025. The survey was conducted to provide a comprehensive understanding of the current landscape in software engineering. It aims to identify the demand for various roles, essential skills and upskilling strategies within the software engineering organization. It explores the integration of AI in software engineering workflows, their leadership experiences and prior roles of the current leaders. It also assesses their budget expectations, team structures, organizational outcomes and priorities. The survey was conducted online from October through December 2024 among 400 respondents from the U.S. (n = 320) and U.K. (n = 80). Qualifying organizations operated in multiple industries (excluding the IT software industry involved in the development of commercial software and the education sector) and reported enterprisewide revenue for fiscal year 2023 of at least $250 million or equivalent. Qualified participants were highly involved in managing software engineering/application development teams and the activities they perform. Disclaimer: The results of this study do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.

3 2025 Gartner Generative and Agentic AI in Enterprise Applications Survey. This study was conducted to understand the key challenges and opportunities when deploying generative AI (GenAI) tools, and where organizations should focus their AI investments. This research also aims to understand what stage organizations are at on their AI agent journey and their thoughts on AI agents. The research was conducted online from May through June 2025 among 360 respondents from organizations with at least 250 full-time employees across all industries (except IT software) in North America (n = 149), Europe (n = 140) and Asia/Pacific (n = 71). Soft quotas were established for country, company size, and respondent’s function type and job level to ensure a good representation across the sample. Organizations were required to have deployed or plan to deploy in less than one year at least one generative AI tool in at least one core enterprise application domain: digital workplace applications, customer relationship management applications, or enterprise resource planning applications. Respondents were team leaders or above, excluding C level, and involved in the rollout of generative AI tools; they were required to have certain responsibilities regarding these generative AI tools. Disclaimer: The results of this survey do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.