Top Technology Trends in Digital Assets and Blockchain for Financial Services CIOs

16 February 2026 - ID G00843466 - 31 min read

By Christophe Uzureau, David Furlonger

Global regulatory frameworks now support the issuance and trade of stablecoins, cryptocurrencies and tokenized RWA. To remain competitive, FSI CIOs must develop IT strategies integrating the new digital asset classes that enable on-chain finance opportunities while minimizing lock-in and security risks.

Insights at a Glance

The financial services industry is undergoing a profound transformation driven by digital assets, programmable money, and blockchain-based infrastructures. By 2030, programmable monies — such as stablecoins, deposit tokens, and CBDCs — will be integral to payment orchestration, enabling more dynamic, programmable, and efficient value exchanges. Regulatory developments and technological advances are accelerating adoption, but also raising concerns around sovereignty, compliance, and operational risk. Digital asset natives are evolving into neo-banks, leveraging on-chain finance to compete with traditional FSIs and offering integrated custody, trading, and payment solutions. As a result, traditional FSIs must modernize, expand digital asset custody, and develop orchestration capabilities to retain client relationships and revenue. Tokenization and fractionalization of assets are democratizing access to capital markets, increasing liquidity, and enabling new customer engagement models. On-chain finance infrastructures are emerging, supported by regulatory clarity and collaborative industry initiatives, creating new opportunities for product innovation and market integration. AI agents are set to automate and accelerate digital asset trading and distribution, further reshaping advisory, compliance, and investment services. To remain competitive, FSIs must develop robust digital asset strategies, invest in technology, and build partnerships, while carefully managing risks and governance in this rapidly evolving landscape.

Issue Context

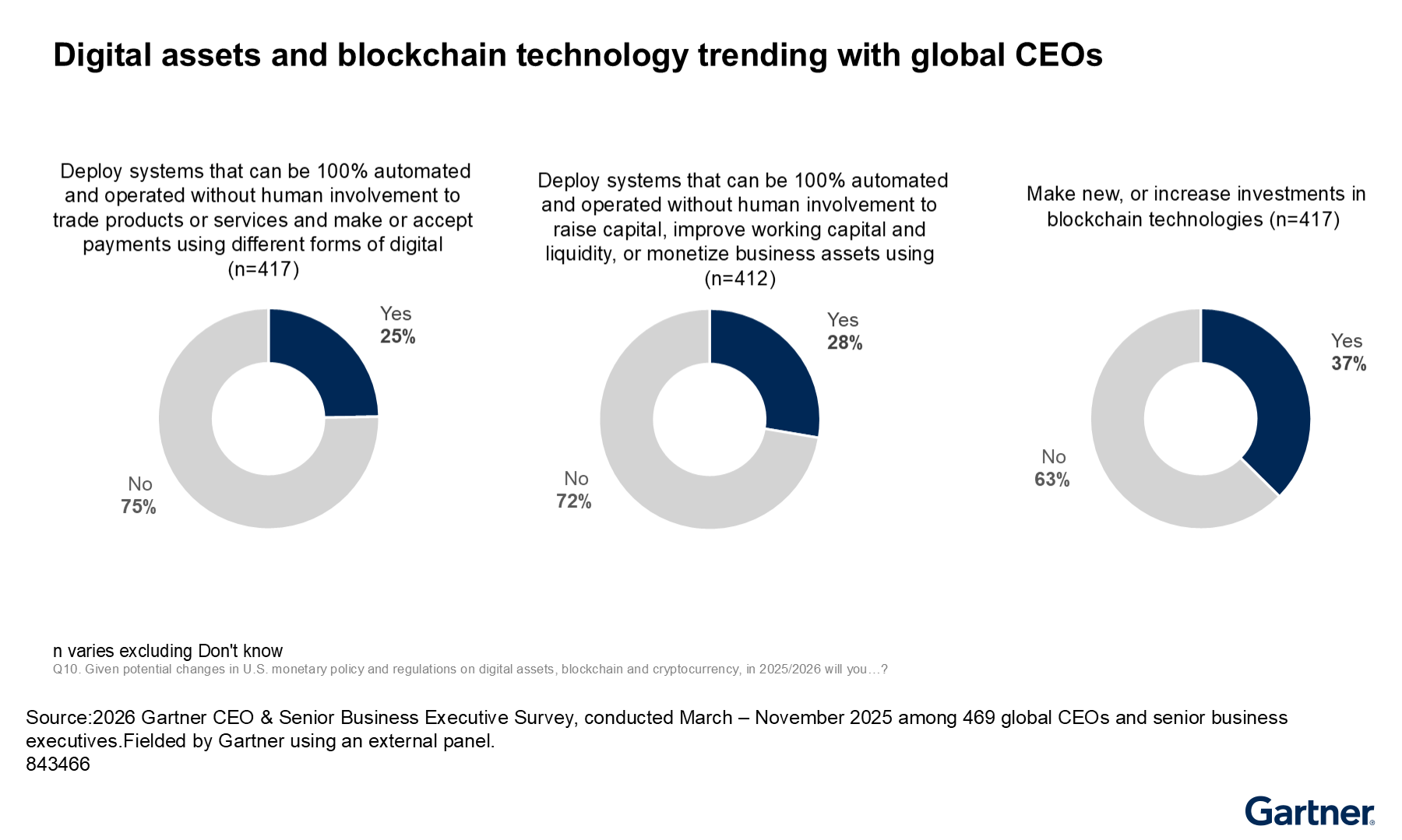

Interest in digital assets is driven by changes in regulations but also an interest in delivering efficiency gains and accessing new sources of funding and capital. Digital assets and blockchain are therefore finding their ways into the boardroom. 2026 Gartner CEO & Senior Business Executive Survey illustrates the current perception by senior executives of the business value of digital assets and blockchain technology. And this translates into investing in blockchain technology to monetize programmable money and tokenized financial and real-world assets (RWAs) combined with the adoption of AI (see AI and Programmable Money Cause CEOs to Reassess Corporate Assets).

For financial services companies, this is not a simple yes or no decision to participate in the digital asset market. With growing enterprise interest in digital assets, this is not about deciding between participating in centralized finance (CeFi) versus decentralized finance (DeFi). The delimitations of these two markets have never been well-defined and new asset classes, services and partnerships enabled by regulatory frameworks are further blurring the lines. What’s really at stake here for FSIs is to anticipate the emergence of a programmable economy compounded by AI agents’ commercial activities (see Act Now to Prepare for the Autonomous Business of Banking).

Impact Brief

To plan for their digital asset journey, financial services institutions need to reason in terms of on-chain finance — the financial activities, instruments, and workflows that are issued, executed, settled, and recorded directly on a blockchain, where the ledger itself is the system of record with business logic enabled by smart contracts. They need to anticipate how the development of on-chain finance will transform their industry. This includes preparing for the specific roles their organizations need to embrace in order to influence the design of the financial ecosystems transformed by on-chain finance.

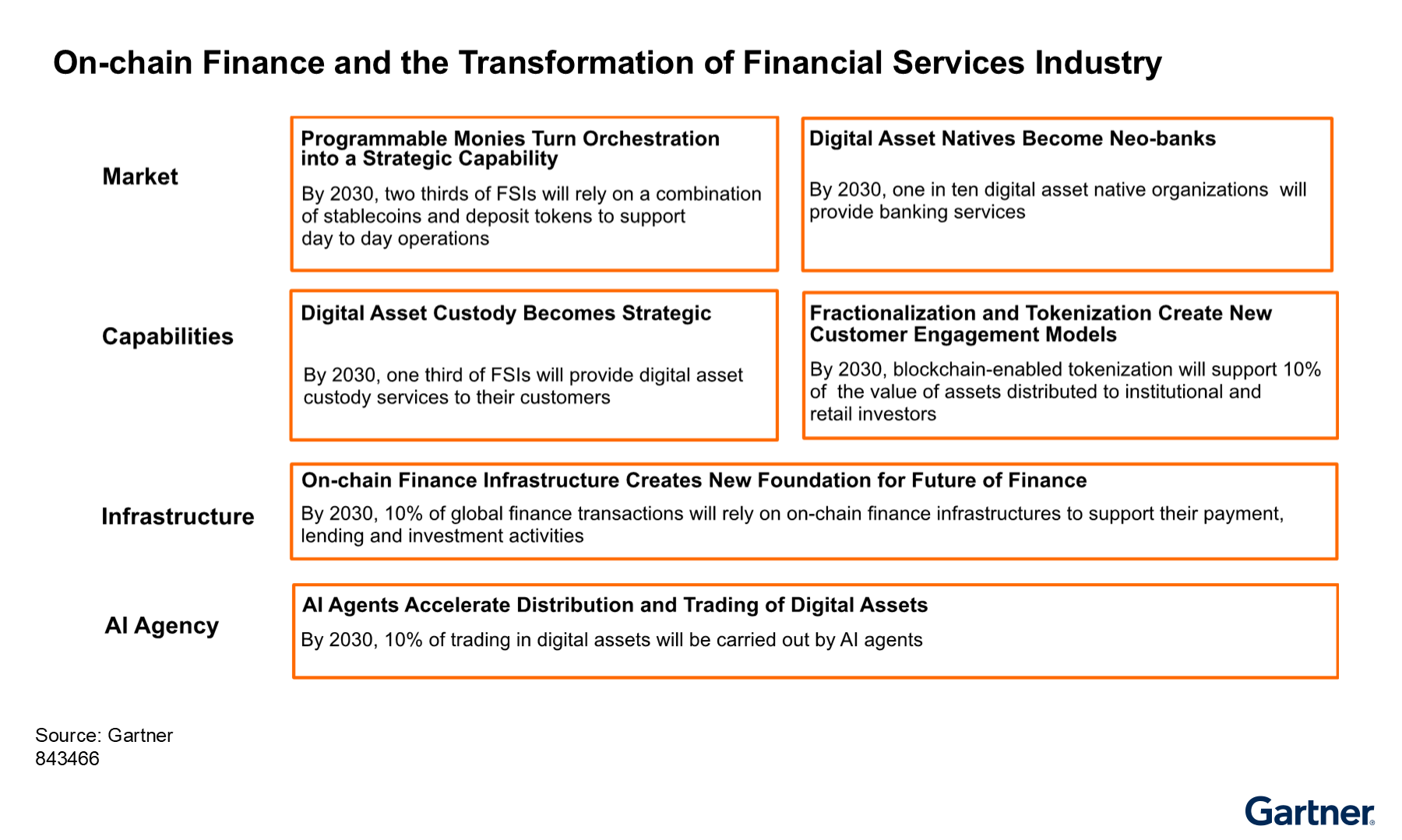

In order to support this objective, this report explores the key trends that characterize the development of on-chain finance and the strategic planning assumptions (SPAs) they need to consider to prepare their organizations for the resulting digital transformation as introduced in Figure 2.

These technology trends highlight a series of impacts within the span of control of financial services CIOs. We will explore these trends starting from the market and competitive dynamic infrastructure layer, then moving to the trends in capabilities before considering how the new on-chain finance infrastructure will accelerate FSIs’ overall digital transformation. And finally, we will explore the role of AI agents in accelerating the development of digital asset markets.

More Detail

Programmable Monies Turn Orchestration Into a Strategic Capability

Analysis by Christophe Uzureau and David Furlonger

Strategic Planning Assumption:

By 2030, two-thirds of financial services institutions will rely on a combination of stablecoins and deposit tokens to support day-to-day operations.

Description:

Programmable money is any form of digital money that can be programmed using software that determines its operation based on algorithmic criteria. Programmable money relies on blockchain-enabled tokenization and smart contracts to increase the participation of economic actors and program value exchanges. Stablecoins, deposit tokens, retail and wholesale CBDCs are all forms of programmable money. The battle for influence between stablecoins and deposit tokens is at the core of the future of programmable money and global payment systems, with wholesale CBDCs playing a supporting role and retail CBDCs a defensive one.

Why Trending:

The degree of programmability of money is improving thanks to the adoption of public blockchains such as Ethereum, and Layer 2 and EVM-compatible infrastructures. Thanks to a large community of developers and an ecosystem of startups, combined with the open source testing of smart contracts, Ethereum (and to a certain extent EVM-based blockchains) provides an environment to experiment with, test and deploy programmable money as well as embedded compliance.

The first wave of smart contracts impacting the programmability of money: payment vs. payment (PvP) and delivery vs. payment (DvP) are now well-understood. New smart contracts are emerging, for example improving programmability of treasury operations based on real-time data, embedding compliance into value exchanges (and as part of ERCs such as ERC3643), enhancing supply chain finance as well as supporting the needs of AI agents.

The battle for who will program money is intensifying. The emergence of new regulatory frameworks, such as in the U.S. with the GENIUS Act, contributes to an acceleration of stablecoin issuance and their distribution. Global transactional banks such as JPM and Citi recognize the threat to their payment operations. And commercial banks have also identified deposit flight as a potential risk which would lead to an increase in cost of funding, and reduce net interest margins and liquidity coverage ratios (LCRs). They are therefore developing or issuing deposit tokens (as well as tokenized deposits). However, banks also recognize the potential for stablecoins to extend the reach of their network thanks to public blockchains and exploring the issuing of stablecoins in parallel to deposit tokens:

- Qivalis, a MiCAR-compliant stablecoin issuer supervised by the Dutch central bank (DNB). The consortium aims to issue a regulated euro stablecoin and involves DZ BANK, BNP Paribas, CaixaBank, Danske Bank, DekaBank, ING, xKBC, Raiffeisen Bank International, SEB, and UniCredit.

- Citi, Bank of America, Goldman Sachs, Deutsche Bank, and UBS are jointly exploring issuing a stablecoin pegged to G7 currencies.

- Zelle by Early Warning Services (owned by Bank of America, Capital One, JPMorgan Chase, PNC Bank, Truist, U.S. Bank, and Wells Fargo) in the U.S. is planning to allow users to start making international payments using stablecoins — which will be available to customers of any bank that is part of the Zelle network.

In terms of market capitalization, most of the current stablecoins are USD-denominated and backed by liquid U.S. asset reserves (mostly in Treasury bills). Countries outside the U.S. increasingly recognize the sovereignty risks of relying on stablecoins for their payment infrastructure — due to the risk of dependency on U.S. monetary policy and impact of possible sanctions. There is therefore renewed interest in issuing retail and wholesale CBDCs for defensive rationales, notably in the Eurozone and China. But this is also making regulators pay more attention to deposit tokens as an acceptable alternative to stablecoins, since they have more control over the regulation of commercial bank deposits.

Implications:

Delivering business value from programmable money will demand new orchestration capabilities. The objective is to enable retail, SMB and corporate clients to accept programmable forms of money but most importantly to be able to program money according to their personal and commercial objectives.

For enterprises, programmable money provides an opportunity to influence how payment value chains adapt to their own supply chains and treasury operations. Utilizing programmable money reduces operational costs but also creates a financial infrastructure where collateral and liquidity are managed more dynamically and transparently.

Programmability enables a rule-based asset to be created and directed at the programmers’ requirements. They can, for example, set the terms and conditions of the value exchanges directly within the money construct. One of the key strategic considerations for FSIs is therefore who is doing the programming and how to build influence over programmability of financial exchanges.

There is therefore an opportunity for financial organizations to orchestrate multiple payment rails, including multiple stablecoins and deposit tokens (their own and via partnerships), to enhance their customers’ payment and treasury operations as well as improve the settlement of and liquidity for digital assets. This also has implications in terms of building orchestration APIs and updated security policies such as, for example, handling smart-contract-related risks.

It is also imperative for FSIs to appraise partnerships both in terms of immediate business value and risk of dependency from a programmability perspective. For example, relying on an organization that issues a stablecoin while also managing the underlying blockchain as Circle is attempting to do via the deployment of its Arc blockchain.

Actions:

- Build your programmable money strategy by considering all forms of programmable monies, not just stablecoins. Deposit tokens and wholesale CBDCs provide FSIs, notably banks, with an opportunity to dilute the influence of stablecoin issuers.

- Build orchestration capabilities for programmable monies to deliver the next generation of financial services. An FSI may not need to issue programmable money, but its customers (notably corporate customers and SMBs) expect them to orchestrate stablecoins, deposit tokens and CBDCs to fit with their commercial value chains.

- Conduct due diligence on the forms of digital money you are using. There is a risk of stablecoin issuers not fully backing their stablecoin or going bankrupt.

- Establish an internal programmability of money governance model covering key parameters such as who defines smart-contract logic, how compliance is embedded and how upgrades and kill-switches are controlled.

- Provide clients with programmable money templates built on client-configurable rules (limits, timing, conditions) that are supported by sandbox environments such as for testing treasury automation.

- Create a smart contract center of excellence for programmable money, taking into account standardized contract constructs (for PvPs, DvPs, treasury operations, compliance-enabled ERCs (like ERC-3643), formal verification and audit processes.

Further Reading:

Digital Asset Natives Becoming Neo-Banks

Analysis by Christophe Uzureau and David Furlonger

Strategic Planning Assumption:

By 2030, one in 10 digital asset native organizations will provide banking services.

Description:

Digital asset natives — organizations that build their core business model, infrastructure, and operations around blockchain technology and digital assets — are entering the banking and investment industries. They are applying for banking licenses or charters in at least one jurisdiction in order to access payment and banking systems. Beyond building access to established financial infrastructures, some are using on-chain finance to build a new generation of banking services. They are becoming the new neo-banks. Today’s partners are therefore becoming tomorrow’s competitors, forcing FSIs to adopt a careful approach to strategic alliances and partnerships.

Why Trending:

Traditional FSIs benefit from increasing regulatory clarity as well as less restrictions in issuing, taking custody of and trading digital assets. However, the new regulatory environments also strengthen the competitive position of digital asset natives. Digital asset custody and wallet infrastructure providers such as Coinbase and Gemini offer hot/cold storage of digital assets as well as asset life cycle management, payments, technology development and engines for integration. These developments have led to several digital asset natives to apply for banking licenses. For example, Ripple, Circle and Paxos received conditional approval for a national trust bank charter (see Breaking: OCC Grants Ripple Conditional Approval For Banking License) while Coinbase made an application (see Coinbase applies for federal trust banking license, says ‘we have no ambitions to be a bank). This will allow them to custody customer assets (including stablecoin reserves), act on customers’ behalf to settle related transactions and make payments. Beyond accessing payment systems, custodial services provide them with a foundation to seek a larger share of the banking market and encroach on existing banking business.

Furthermore, the Federal Reserve in the U.S. is exploring the option of “skinny” master accounts that would allow eligible stablecoin issuers and fintechs direct but limited access to the Federal Reserve’s payment infrastructure’s payment rails (e.g., Fedwire and FedNow). These accounts are expected to deliver operational benefits to stablecoin issuers that previously had to rely on intermediary banks. Moreover, incorporation into the U.S. payment system affords stablecoin issuers increased legitimacy in the eyes of market participants, notably by operating under rules tailored to limit risk (e.g., balance caps and restrictions on interest payments).

Adoption of stablecoins will further encourage the development of on-chain finance as a foundation for new financial products and services. Bridge’s Orchestration APIs enable enterprises and SMBs to adopt new payment rails by handling regulatory, compliance, and technical complexities. And combined with Bridge’s stablecoin financial accounts, this provides an SMB with a USD account, cross-border, payroll, FX, and cash management capabilities.

Beyond these digital asset natives, FSIs also need to face the emergence of one-stop-shop apps for investment services that have rapidly added digital asset classes to their offering, including from existing neo-banks. For example, Revolut provides a crypto trading service integrated into its “all-in-one” app. Revolut claimed at the end of October 2025 that at least 14 million of its 65 million customers — 21.5% — are crypto users, which the company defined as users who have passed know-your-customer checks and been fully onboarded for crypto services. To achieve that objective of becoming a one-stop-shop app, companies such as Robinhood are introducing new capabilities such as Robinhood Social to increase engagement among users and drive trading in new asset classes.

Implications:

Circle, Ripple and Coinbase support FSIs’ digital asset capabilities. This provides them insights to capture the intent and maturity of FSIs, and will facilitate the development of their financial services, especially banking services.

Digital asset natives rely on banking relationships to access payment systems. They are now getting better access to the financial services infrastructure and the financial licenses needed to support new products and customer relationships. Traditional financial services institutions such as banks will lose payment revenue as well as their influence on the global payment infrastructure.

Overall, not getting involved exposes FSIs to primary client’s relationships moving to digital asset natives and one-stop-shop app for retail investors. However, FSIs will struggle to match the pricing models adopted by one-stop-shop apps. For example, Revolut provides free conversion services for US$ into USDC and USDT. As a result, FSIs will have to expand products and services, notably regarding custodial and tokenization services, and demonstrate how their established industry position translates into superior levels of security and accountability for customers’ assets.

Actions:

- Consider digital asset custody to support new business value and to alleviate the challenge from new entrants to the financial services industry.

- Augment your investment services with digital asset trading services, considering cryptocurrencies and tokenized financials and real-world assets.

- Develop or partner to be able to orchestrate programmable money (stablecoins, deposit tokens, tokenized funds) across various blockchains and use cases.

- Vet partnerships with digital asset natives (e.g., Coinbase, Circle, Ripple and others) for both opportunity and long-term competitive risk by enhancing partner due diligence.

- Modernize your open financial services capabilities by adopting APIs to integrate with programmable money and digital asset services.

- Ensure your IT infrastructure can support increased transaction volumes and new asset classes.

Further Reading:

Digital Asset Custody Becomes Strategic

Analysis by Christophe Uzureau and David Furlonger

Strategic Planning Assumption:

By 2030, one-third of financial services institutions (FSIs) will provide digital asset custody services to their customers.

Description:

Custody of digital assets is becoming more strategic. New digital asset classes are transforming payment, lending and capital markets. Offering safekeeping for digital assets of their institutional and retail investors is a natural step for more traditional FSIs to enter the digital asset market, build trust at scale and engage new customers. Whether they provide such services directly or by relying on a third party, digital asset custody is a foundation to build a more extensive digital asset service proposition, notably by capturing demand signals.

Why Trending:

Growth in cryptocurrencies adoption and new digital asset classes creates new opportunities for FSIs to reinforce trusted entity status with their clients. The growing interest by institutional and retail clients in owning digital assets further drives cybercriminal activity and the potential for fraud and operational breaches. This demands stronger access controls, and governance around digital asset private keys, as well as forensic analysis creating demand for institutional-grade solutions and segregation of duties. There is therefore a natural evolution of banks’ operations and their brand into digital asset custody, providing they have the security capabilities to support it.

Traditional FSIs also benefit from increasing regulatory clarity as well as less restrictions in developing digital asset custody solutions. For example, SAB 122 in the U.S., removed the requirement for custodians to book customer digital assets as liabilities on its balance sheets and the Monetary Authority of Singapore (MAS) clarifies the rules to safeguard customers’ assets (see MAS finalises crypto segregation and custody regulations).

Beyond regulatory clarity, FSIs are also more confident in adopting the best practices and experiences of their peers notably with regard to cold wallets and how they fit into their overall governance and security frameworks:

- From a governance and ecosystem perspective, DBS adopted the industry best practice of custodying its clients’ digital assets within the bank using institutional-grade cold wallets but separated from the exchange. Their digital exchange (DDex) does not hold any customer funds. DBS Digital Custody is an approved custodian of the DBS Digital Exchange, and DBS Digital Custody is embedded within the bank system and leveraging its existing custodial infrastructure for regulatory compliance and security.

- From a security perspective, FSIs understand this is an arms race with cybercriminality that will require ongoing investments. As a result, the industry is continuously improving its digital asset cybersecurity measures. For example, Fidelity is now providing cold storage with 24/7 on-site security, hardened room structure, as well as multiperson and multiorganization access controls. Another illustration is Amina with its “off-grid” storage with hardware and software isolated from the internet with an ‘air gap’ with radio signals in and out of the facility blocked.

The ecosystem is therefore maturing with traditional custody providers launching digital custody platforms to support institutional clients, such as CACEIS, and BNY. More specifically, BNY’s approach implies a willingness to create a full-stack offering encompassing wallets, segregated assets, policy and security controls, investment services/fund management integration — while being in compliance with capital, accounting and taxation regimes. The goal is to increase client/product stickiness and therefore revenue synergy across ETFs, funds and digital assets.

Implications:

First, FSIs need to recognize that building the business case for digital asset custody solutions demands the creation of a digital asset strategy first. This is because the main business benefits will derive from indirect revenue such as from trading, staking and other yield services, collateral management solutions, cash management and treasury services, as well as providing advisory services. As a result, while custodial services will generate recurring fees; this will also demand new criteria to appraise the benefits of digital asset custody solutions, such as for example revenue generated from collateral management.

Developing a digital asset custody foundation also paves the way for product development:

- BNY launched Digital Asset Data Insights. This solution is feeding data about the assets BNY is administrating — both on-chain and off-chain data — to public blockchains via smart contracts in order to improve the consumption of these data assets (see BNY Expands Digital Asset Platform with Launch of Innovative On-Chain Offering).

- Digital asset custody solutions also provide strong foundations to detect new demand patterns and therefore assist the organization in prioritizing which digital asset class to support.

This requires important technology, product strategy, and sourcing choices such as managing the digital assets via direct custody or by relying on a subcustodian. Relying on a subcustodian may simplify go-to-market by avoiding adoption of new and specialized technologies and the complex updates to risk management processes. However, this approach limits the development of product functionalities, and potentially creates reputation and fiduciary risks.

For traditional FSIs, not getting involved exposes them to the risk of primary investor relationships moving to digital asset exchanges and fintech providers. If they get involved too late, they also risk having to negotiate with large solution providers due to consolidation. There is also the risk of digital asset custodians entering the banking market and obtaining banking licenses to monetize their digital asset client relationships.

Actions:

- Craft a dedicated-custody strategy that takes into account legal frameworks in your jurisdictions, type of wallets offered, type of custody offered and integration with other noncustodial digital asset products and services.

- Define the implications in terms of cost of integration but also security risks of relying on a direct custody model or a subcustodian.

- Track the rapid evolution of the technologies supporting digital asset custody solutions, notably multiparty computation (MPC) that provides a higher level of security but is more complex to implement.

Further Reading:

Fractionalization and Tokenization Create New Customer Engagement Models

Analysis by Christophe Uzureau and David Furlonger

Strategic Planning Assumption:

By 2030, blockchain-enabled tokenization will support 10% of the value of assets distributed to institutional and retail investors.

Description:

Fractionalization and tokenization enable the digitization of a financial or real-world asset in which the value (or partial value) of its digital form is converted into digital tokens. The ownership and right to use are recorded via a blockchain. The rules that define the creation, representation and exchange of assets are executed via a smart contract, such as enabling new trading and collateral management opportunities, and who can own this type of asset.

Why Trending:

The business value of tokenizing financials or real-world assets is now more visible hence strengthening interest by the industry in developing or participating into the digital asset ecosystem. For example:

- Blackrock BUIDL (BlackRock USD Institutional Digital Liquidity Fund) launched in March 2024 which has around $2.5 billion in assets under management (AUM). BUIDL tokens represent investments in cash, U.S. Treasury bills, and repurchase agreements, providing investors an opportunity to earn U.S. dollar yield while holding tokens on-chain.

- DBS which organized its DBS digital exchange ecosystem into three entities — Digital custody, digital exchange (DDex) and Security Token Offerings. Their CEO stressed that their “objective is to operate a full-stack ecosystem: we originate, issue, list, handle payments and settlements, and manage collateral and reserves. We cover the entire suite, and so far, it has proven to be a good profitable business” (Source: Edited transcript of DBS second-quarter 2025 conference call for buy and sell sides, 7 August 2025).

Regulators are authorizing security infrastructure providers to experiment with tokenization. One important pilot is the DTCC plan to tokenize U.S. stocks, exchange-traded funds (ETFs) and U.S. treasury securities, hence creating digital twins of these assets (see DTCC Authorized to Offer New Tokenization Service, Paving the Way to Tokenized DTC-Custodied Assets). The participants opting into the pilot can elect to have their security entitlements converted from book-entry form into digital tokens. When issued, the tokens are then delivered to participant-registered wallet addresses on preapproved blockchains. These tokens will represent the same rights as the underlying securities.

The demand for such assets already exists. For example, Kraken provides access to 55 U.S. Stocks and five ETFs via its xStocks. Value of the token is derived from the value of the underlying share, but the token doesn’t confer the stocks’ ownership and voting rights. As a result, the DTCC approach is providing an important foundation for the development of the digital asset market in the U.S. and influencing investment infrastructure providers globally.

Token standards are maturing to accommodate regulatory requirements, such as the permissioned ERC3643, initially developed by Tokeny and now being adopted by more traditional market participants. For example, the U.S. Depository Trust and Clearing Corporation (DTCC) joined the ERC3643 Association to promote the new standard.

Implications:

Fractionalization and tokenization impact a wide range of financial services by:

- Increasing the velocity of exchanges and the number of investors who can acquire and trade high value and/or illiquid assets, such as private equity funds.

- Creating new capital markets that are more accessible and aligned with the needs of new investor constituencies such as younger demographics looking to support local providers, for example, paying attention to their environmental concerns.

- Enhancing global collateral management. Smart contracts enable on-chain assets to be used as collateral for trading other digital assets as well as traditional assets. This limits intermediation, manual processes and reduces counterparty risk.

- Generating cost efficiencies by automating processes in record keeping and increasing liquidity. The use of smart contracts reduces the reliance on intermediaries, further reducing manual processes and errors.

- Enhancing transparency since every transaction is recorded on an immutable ledger, creating a common and more reliable systems of record, but also implying more transparency on positions taken by market participants.

- Improving settlement finality, efficiency, and programmability by facilitating the use of programmable money, such as deposit tokens or stablecoins, to settle the assets via smart contracts (DvP).

- Providing an asset that can be utilized by AI agents for payment, trading and investing.

For banks, there is an opportunity to create new sources of funding or capital for SMBs by tokenizing their assets and distributing such assets to their retail clients. Fractionalization and tokenization can therefore enable the monetization of customer relationships, increasing the number of products per customer across customer segments.

Actions:

- Treat tokenized RWAs as catalysts for customer engagement, notably bridging the financing needs of SMBs with retail investors seeking to connect with local investment opportunities.

- Consider tokenization as an opportunity to improve liquidity thanks to tokenization of RWAs and enabling new collateral management opportunities.

- Define and refine the impact of tokenization for key financial functions such as issuance, custody, trading and insurance, and, therefore, reprioritize your R&D investments.

- Review your current IT capabilities to determine whether you can support the tokenization of RWAs or are in a position to use the services from a third-party tokenization platform.

- Collaborate with established or emerging tokenization platforms, blockchain infrastructure providers, and other banks to share pilot experiences and drive interoperability protocols.

- Prepare the corporate, legal, and trading teams for next-gen securities — token issuance, including microfractionalization and 24/7 settlement by offering guidance on blockchain and tokenization mechanisms.

Further Reading:

On-Chain Finance Infrastructure Creates New Foundation for Future of Finance

Analysis by Christophe Uzureau and David Furlonger

Strategic Planning Assumption:

By 2030, 10% of global finance transaction value will rely on on-chain finance infrastructures to support their payment, lending and investment activities.

Description:

On-chain finance relies on the use of blockchain technology and smart contracts to issue digital assets, track their ownership and change of ownership thus enabling new sources of financing, funding and investment opportunities for individuals and businesses. The new on-chain finance infrastructure is not limited by traditional LOB and product silos, and much less constrained by traditional customer segmentation across retail, SMB, corporate and wholesale banking.

Why Trending:

Regulatory frameworks such the GENIUS and CLARITY Acts in the U.S., MiCA in Europe, Stablecoin Ordinance in Hong Kong enable the issuance and adoption of digital assets classes by established FSIs. Regulators are also supporting the traditional market infrastructure providers in developing new services and adopting new roles in digital asset markets such as for example:

- On 11 December 2025, the SEC’s Division of Trading and Markets issued a No-Action Letter in response to the Depository Trust Company DTC’s request to operate a pilot version of its tokenization service. By converting conventional securities into digital tokens that maintain identical legal rights and investor protections, this creates an opportunity to formalize the use of digital assets in capital markets (see DTCC Authorized to Offer New Tokenization Service, Paving the Way to Tokenized DTC-Custodied Assets).

- Project Borderless, Liquid, Open, Online, Multi-currency (BLOOM) in Singapore aims at using settlement assets such as tokenized forms of commercial bank money and stablecoins for domestic and cross-border payments, corporate treasury management, trade finance and agentic payments.

Public blockchains have demonstrated their ability to sustain new digital asset classes and business models while being constantly tested by cybercriminality. Established FSIs are adopting them. Societe Generale FORGE has issued its USDCV and EURCV stablecoins on Ethereum (ERC20) and Solana, XRPL and Stellar. And JP Morgan Chase is testing a deposit token, JPMD, for institutional clients on Coinbase’s public blockchain Base.

While infrastructure silos exist and will persist, new collaborative models are contributing to the emergence of a more integrated on-chain finance infrastructure:

- Financial services institutions such as Standard Chartered, Banco Santander, Societe Generale and Deutsche Bank, are advising and participating in the Circle Payment Network (CPN)

- In turn, seeing this as a challenge to its model, Swift has announced a new blockchain-based infrastructure (see Swift to add blockchain-based ledger).

- JPM and DBS are also collaborating for token settlement for cross-bank transactions by connecting JPM’s Kinexys Digital Payments and DBS Token Services.

- Blackrock is now positioning its tokenized money market funds as a safe haven for institutional investors in between trades involving stablecoins:

- Securitize allows qualified institutions to convert their USDC (stablecoin) to USD for acquiring BUIDL.

- Via Securitize, holders of BUIDL can exchange tokens for Ripple USD (RLUSD).

In emerging markets, the adoption of stablecoin for remittances has equipped retail and SMBs with digital asset wallets. This results in new data flows and a foundation for bancarization independently of the existing financial infrastructure. The new data flows enable alternative credit records, and the programmability of money enables it to deliver at a lower cost microloans, deposits and investment products. Fintechs are now using this foundation to create proxy-current account, deposit, lending and investment products, all relying on the programmability of smart contracts to reduce costs, and create localized products while reducing risks and embedding compliance into processes.

Implications:

This shift toward on-chain finance is redefining market dynamics. Financial services institutions that do not integrate with this new infrastructure risk falling behind and experiencing higher client churns.

In spite of the early stage of the approach, the on-chain finance foundation for bancarization already exists. Nonbanks are therefore rolling out new banking products and services. It’s also worth stressing that superapp providers such as GCash, the Philippines’ largest digital wallet provider, has integrated its services with Circle to access USDC, which will further contribute to the development of on-chain finance for banking services in the region.

On-chain finance is also enabling new entrants to use new digital asset classes not only to acquire FSIs’ existing retail and corporate customers but increasingly to serve their more traditional financial services needs. Digital asset natives such as Coinbase, Ripple and Bitgo are all applying for banking licenses or charters. While they may not initially provide traditional banking products and services, their infrastructure will provide new entrants with a foundation to do so, improving the integration between the off-chain and on-chain finance infrastructures.

Actions:

- Challenge your CxO peers on the state of your digital asset strategy with a focus on their understanding of how on-chain finance could enable new products and services — demonstrating that on-chain finance is not limited to trading cryptocurrencies.

- Create a multiyear on-chain finance infrastructure roadmap aligned with payments, securities and data platforms.

- Explore now which partnerships could give you access to some on-chain finance capabilities, including from potential competitors. For example Standard Chartered is strengthening its partnership with Coinbase to support its institutional clients (see Standard Chartered and Coinbase deepen partnership to expand institutional digital asset collaboration).

Further Reading:

AI Agents Accelerate Distribution and Trading of Digital Assets

Analysis by Christophe Uzureau and Alistair Newton

Strategic Planning Assumption:

By 2030, 10% of trading in digital assets will be carried out by AI agents.

Description:

With finance on-chain, via the programmability of smart contracts, AI agents are better equipped to onboard themselves or clients, trade and settle digital assets as well as access new sources of liquidity or capital such as via the tokenization of financials and RWAs. Smart contracts also enable embedding compliance into value exchanges, progressively providing more autonomy to AI agents — as well as equipping AI agents to carry out some of the compliance requirements. AI agents have therefore an ability to support the issuance, discovery and trading of new digital asset classes.

Why Trending:

The increase in the diversity of digital asset classes as well as the novelty of these assets (and of their issuers) create challenges in advisory services, sales and service, portfolio allocation, due diligence and compliance and regulatory arbitrage. AI agents can support and augment such tasks, notably thanks to the access to on-chain data pertaining to the new digital asset classes.

The one-stop investment app approach relies on robo-advisors that can transition to AI agents. For example:

- Robinhood launched Robinhood Strategies to provide robo-advisory services to some of its members. Combined with their crypto-asset services, this provides the right combination for developing AI agents delivering clients with digital asset recommendations as well as investing on their behalf.

- Similarly, SoFi Invest provides robo-advisory services, while continuing to expand it crypto-asset trading services.

Stablecoins, deposit tokens and CBDCs combined with smart contracts enable value exchanges to be programmable, including the ability to embed compliance requirements. The development of a new programmable money infrastructure therefore provides a foundation to enable AI agents to increase their autonomy when trading digital assets, increasing their ability to contribute to the development of digital asset markets.

Implications:

The reliance on AI agents to research, investigate, trade and utilize digital assets will evolve across investment operations. AI agents will gain more autonomy and a better understanding of digital asset classes leading them to:

- Provide expanded investor education to educate clients on both the opportunities and risks of investing in digital assets, while explicitly addressing the immaturity and fragmentation of current regulatory frameworks.

- Identify excess liquidity across individuals, enterprises, and other AI agents, and signal where portions of that liquidity could be allocated to digital assets.

- Deliver digital-asset advisory services, guiding customers on relevant digital-asset classes in line with their risk tolerance, investment horizon and preferences.

- Diversify portfolios, taking into account multiple digital asset classes by benchmarking performance across retail, institutional and other AI agent-managed portfolios.

- Participate in the due diligence process of digital asset classes (notably on behalf of institutional investors) by collecting data and performing data analytics.

- Take on new capital-formation and funding-enablement roles by building and advertising the case for investing in a given company or infrastructure project on behalf of company shareholders and management such as via security tokens.

The development of AI agents risks accelerating the concentration of market power, creating inefficiencies, and favoring investments into digital assets favoring companies programming, or influencing the programming of, the AI agents. KPIs aligned to the performance of the assets combined with the use of on-chain data showing performance vs. other classes of digital assets would assist in mitigating such risks.

Actions:

- Identify specific use cases where AI agents can make an autonomous investment decision and review workflows across custody, trading and settlement capabilities.

- Build a dedicated roadmap for AI agents as investors, such as enabling them to advise, promote and support digital asset trading.

- Coordinate your own agents to work in tandem with the AI agents utilized by your customers.