2026 Emerging Tech Impact Radar: Internet of Things for Manufacturing

4 March 2026 - ID G00811802 - 51 min read

By Scot Kim, Evan Brown, and 5 more

IoT is not optional; it's foundational. Product leaders must engineer IoT for both edge and industrial AI applications. Sustained competitive advantage in the manufacturing market requires relentless focus on AIoT-enabled platform capabilities for both automation and autonomous factories.

Overview

Key Findings

- The strategic adoption of the Internet of Things (IoT) and industrial data platforms is essential to unlock significant operational efficiency and drive competitive advantage. Industrial data management is the foundational capability that ensures the high data quality necessary to transition from basic analytics to scalable, high-impact AI capabilities.

- Generative AI (GenAI), integrated with IoT, is a powerful combined capability for market share growth. By leveraging domain-specific language models (DSLMs), product leaders can fundamentally redefine intelligent automation, enable new levels of operational excellence, and embed AI into critical business decisions across the manufacturing value chain.

- Manufacturing companies are shifting their IoT strategy from underlying platforms to outcome-specific, packaged applications. Application-centric solutions are the fastest path to realizing and scaling tangible business value.

Recommendations

- Near-term focus: Capitalize immediately on operational technology opportunities. This requires integrating IoT and edge computing technologies into your product roadmaps and explicitly targeting and solving high-value manufacturer business problems to secure short-to-medium-term market leadership.

- Long-term vision: Simultaneously, establish a clear path for sustained advantage by continuously integrating emerging innovations in AI, machine learning, and advanced process automation to shape and future-proof your long-term product development strategy.

- Build a composable IoT architecture: This is essential agility to adapt to the varying maturities and unique business requirements of different customers and use cases. This adaptive foundation is the only way to ensure both rapid deployment and sustained competitive differentiation.

- Elevate platform offerings through partnerships to extend into the applications: Deliver highly specialized, use-case-specific business capabilities and applications. This must be executed by strategically cultivating and leveraging robust partner ecosystems and dedicated marketplaces. This is not an optional add-on; it is the nonnegotiable strategy to lock in maximum customer value, accelerate time to market, and establish your platform as the indispensable standard in the industry.

Analysis

IoT gives manufacturers the real‑time data foundation that powers AI, enabling smarter automation, faster decisions, and accelerated innovation.

Overview of the Emerging Tech Impact Radar

The Emerging Tech Impact Radar is an analysis of the maturity, market momentum and influence of emerging technologies and trends. In this Impact Radar, Gartner includes 10 emerging technologies and trends (ETTs) that are specific to the industrial manufacturing market. These ETTs also have a horizontal impact on IoT technology and service providers, as related to the product leader’s ability to pivot forward and accelerate business opportunities. These 10 technology profiles cover both the “what” and the “how” — areas for product investment, foundational technologies and related nontechnology trends (see Figure 1).

In analyzing the 10 profiles, Gartner has identified three overarching themes:

- Industrial data management is the linchpin for AI/ML and AI agents to stop hallucinating.

- GenAI-enabled IoT is the beginning of creating domain-specific language models.

- IoT platform, industrial data platform, and IoT data analytics are enabling smart factory applications.

Industrial Data Management Is the Linchpin for AI/ML and AI Agents to Stop Hallucinating

Industrial data management is emerging as critical in the evolution of IoT platforms. This trend is driven by the escalating need to transform vast, disparate operational technology (OT), information technology (IT) and IoT data into actionable, trustworthy insights. This trend signifies a shift from basic data collection to comprehensive, intelligent management systems that can handle high-velocity, high-volume data while ensuring its quality, lineage and contextual relevance.

Key innovations include the adoption of industrial data management principles (see Innovation Insight: Industrial Data Management Framework for Smart Manufacturing) to streamline data pipelines and enable automated collection, cleansing, transformation, and delivery. Platforms are increasingly leveraging industrial data fabric concepts to create unified, interoperable data architectures that break down traditional silos and provide a "single source of truth" across the enterprise.

Furthermore, there's a strong focus on contextualization of IT/OT data and creating curated data objects, including semantic models, knowledge graphs, and digital twins. These are essential for powering advanced analytics and generative AI applications reliably, without the risk of hallucinations.

GenAI-Enabled IoT Is the Beginning of Creating Domain-Specific Language Models

GenAI-enabled IoT is the fundamental building block for manufacturers to create DSLMs. To create value from manufacturers’ industrial data and industry-specific insights, DSLMs need to be developed by using a combination of retrieval-augmented generation (RAG) techniques, tool-augmented models, GenAI-enabled IoT, and industrial data. Domain models provide greater reliance and accuracy while meeting increased enterprise needs for data security, cost-efficiency, and flexibility.

Gartner expects IT spending growth for GenAI-enabled IoT to outpace that of general-purpose foundation models (LLMs) from 2025, with specialized models expected to account for at least 12% of all IT spending on GenAI models by 2028 (see Forecast Analysis: Generative AI Models, Worldwide, 2025). Many of these models will be based on open-source GenAI models like Gemma, Llama3, Mistral, and others that are narrowing the performance gaps when compared with closed-source models like ChatGPT.

IoT Platform, Industrial Data Platform, and IoT Data Analytics Are Enabling Smart Factory Applications

Smart factories are the future of production. They offer an opportunity to leverage different technologies — cloud computing, AI and edge — to simultaneously minimize risk, increase competitiveness, innovate production processes and improve human interactions. Ultimately, smart factories will play a role in enabling new ecosystem models, such as direct-to-consumer (DTC), or different capacity orientations, such as mobile factories, asset-light or lights-out factories. They will also play a role in accelerating sustainability initiatives by using digital twins and flexible automation to improve resource efficiencies or lower carbon emissions.

According to the 2025 Gartner Business Outcomes of Technology Survey, 69% of manufacturers rated industrial IoT as an extremely important technology investment to support smart manufacturing.1 Additionally, 84% of manufacturers plan to increase their investments in industrial IoT over the next two years, including 18% who expect to boost spending by more than 10%.

Product leaders have a unique opportunity to deliver composable architectures that drive smart factory use cases like:

- Improving asset reliability

- Managing in-process quality

- Adding accuracy to finished goods inspection

- Automating replenishment and materials handling

- Maximizing production rates

- Enhancing worker safety

- Improving labor productivity

- Enabling frontline worker collaboration

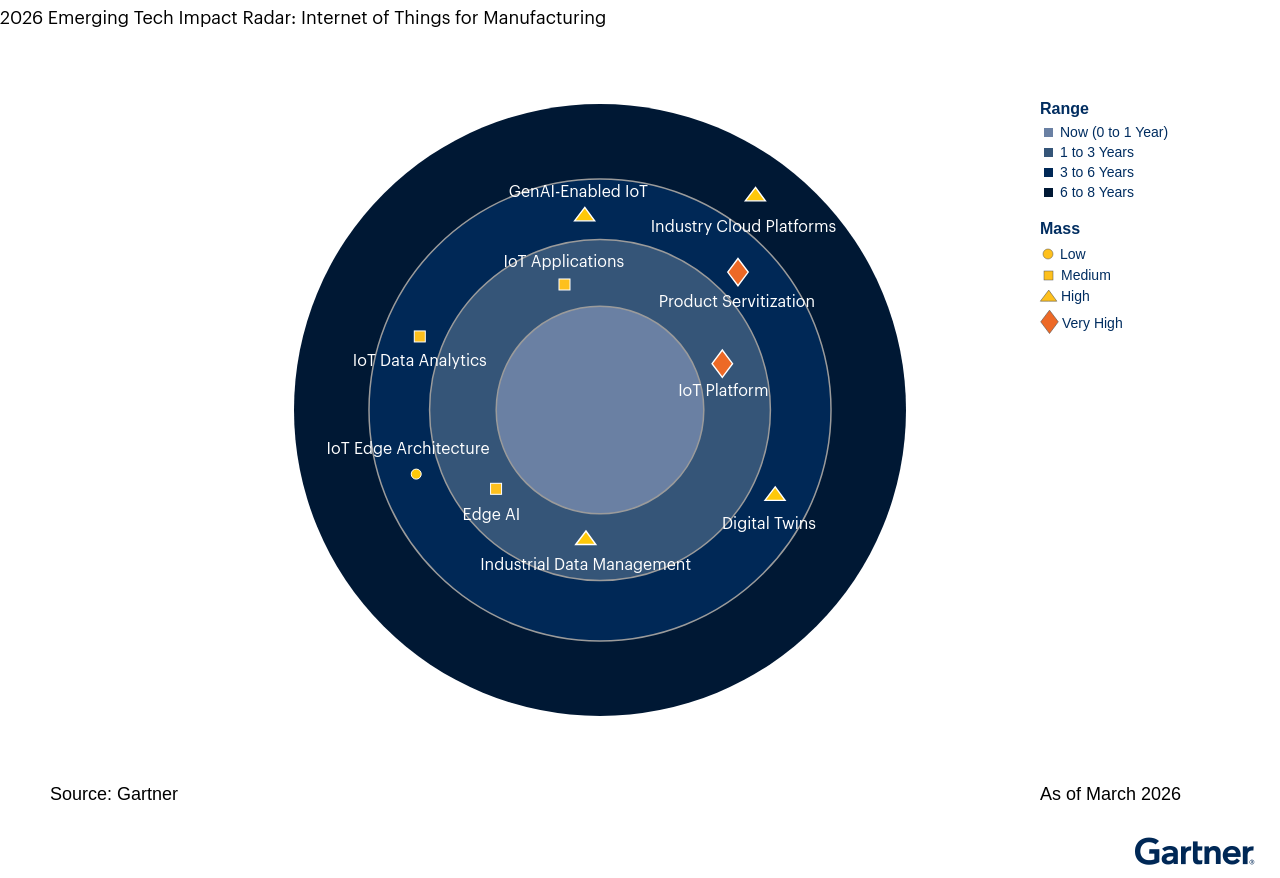

The Impact Radar

Product leaders should use the Radar Profile range to plan investment timing in the related emerging technology or trend. “Range” represents Gartner’s estimate of time to reach early majority (more than 15% target market adoption), not when product leaders should act on investment. Considering time to plan, develop and launch, a starter guide to product leader investment timing, based on product strategy, is as follows:

- First movers should be acting now on items in the six-to-eight-years ring (or beyond).

- Fast followers should be acting now on ETTs in the three-to-six-years ring.

- Majority followers should be acting on ETTs in the Now and one-to-three-years rings.

- Laggard followers can wait until the ETT has passed through to early, or even late, majority.

Refer to the About the Impact Radar section for more information.

Emerging Technologies or Trend Profiles

The Priority Matrix lists emerging technologies and trends identified in the impact radar in [technology area] according to their range (see the About the Impact Radar section for our methodology). Click on a technology name in the table to jump to a profile of the Emerging technology or trend.

Priority Matrix for Internet of Things for Manufacturing

| Mass | Range | |||

|---|---|---|---|---|

| Now (0 to 1 Year) | 1 to 3 Years | 3 to 6 Years | 6 to 8 Years | |

Very High | ||||

High | ||||

Medium | ||||

Low | ||||

Source: Gartner

1 to 3 Years

Edge AI

Analysis By: Arindam Das

Definition:

Edge AI refers to the use of AI techniques embedded within IoT endpoints, gateways and other edge devices. The asset-heavy manufacturing industry is adopting use cases ranging from autonomous vehicles and connected production assets to streaming analytics. While predominantly focused on AI inference, many systems also use statistical techniques to adapt to and accommodate local conditions.

Sample Vendors

Amazon Web Services; IFS (Falkonry); Intel; Johnson Controls; NVIDIA; Pratexo; Qualcomm; Qualcomm (Edge Impulse); Synadia; Syntiant

Range

The range for edge AI opportunities in the manufacturing industry is one to three years out. According to the 2025 Gartner CIO and Technology Executive Survey, 27% of manufacturing enterprises have already deployed edge computing, and 64% plan to have it deployed by the end of 2027. Having an appropriate edge AI strategy aligned with fast-changing business dynamics is inevitable.

The manufacturing industry will invest in edge AI to accelerate its business growth. With the evolution of edge computing, traditional IoT devices need not send data to the cloud or centralized data center for processing anymore. By adopting AI capabilities, the edge endpoints are becoming smarter at analyzing data, interpreting it and acting locally close to where it’s generated. Thus, it leads to faster and more accurate decision-making processes.

Large manufacturers, including automotive, aerospace, electronics and heavy machinery, are accelerating the adoption of edge AI for maintenance, predictive controls and defect detection. Midsize manufacturers are also expected to invest in edge AI as hardware becomes cheaper in the near future.

By 2029, at least 60% of edge computing deployments will use composite AI (both predictive and generative AI [GenAI]), compared to less than 5% in 2023. With edge AI enabling decentralized intelligence across the edge endpoints, the demand for real-time decision making at the edge, reduced downtime and data security within the firewall will continue to drive growth for edge AI adoption in the manufacturing industry.

Given the latency issues with cloud, edge AI emerges as a reliable and resilient alternative for the manufacturing industry. By leveraging edge AI, the manufacturing industry can have lower transmission costs and operate even while connectivity is limited for remote operations.

Another important accelerator for edge AI in the manufacturing industry is data privacy and compliance. IoT devices often contain sensitive data (video feeds, health data, industrial statistics, etc.), and by processing the data locally on the edge, it minimizes the risk during data transmission, thus preserving data privacy and complying with regulations like GDPR and HIPAA.

Mass

The mass for the edge AI opportunity in the manufacturing industry is high as it is becoming the default architecture for the next generation of intelligence.

As the edge AI market matures, Gartner is seeing the emergence of high-impact, edge-centric architectures and capabilities that will transform or replace existing product capabilities. Thus, edge AI will be revolutionary in nature, reflecting the features and capabilities enabled by advanced solutions and use cases.

Manufacturing industry leaders should evaluate the appropriate fit-for-purpose use cases, including augmented reality (AR)/virtual reality (VR), device control and real-time analytics, robotics, sensor data analytics, privacy-by-design algorithms for data security and workers’ safety compliance monitoring, smart asset tracking and logistics, energy usage optimization, and GenAI in disconnected scenarios. These enable their OT architecture landscape to accelerate digital transformation initiatives.

The potential embedded edge for GenAI comprises a large Internet of Things asset installed base, including smartphones, PCs, smart wearables, healthcare assets, cars, robotics, construction equipment, sensors and cameras. The emergence of generative AI models will lead to demand for deployment at the edge of CPUs, GPUs or custom AI chips. As these GenAI models are optimized to run on low-powered hardware, more use cases will take advantage of the technology.

Vendors are increasingly offering pretrained, optimized models specifically designed for deployment within the limited computational capacity of edge devices such as single-board computers (SBCs) and industrial PCs. These solutions often feature low-code or no-code interfaces with drag-and-drop functionality, enabling modular and easy deployment for predictive maintenance and other use cases. Additionally, the ability to retrofit these models to existing edge infrastructure, along with the availability of affordable yet innovative new hardware, is accelerating edge AI adoption among manufacturing leaders.

Additionally, Gartner has observed many uses of generative AI models beyond SLMs being used on the edge to provide real-time value from data generated locally. These include variational autoencoders, recurrent neural networks, long short-term memory networks and various forms of reinforcement-learning-based models.

Recommended Actions

- Articulate ROI to manufacturers who need on-premises automation by validating the compatibility of edge AI use cases with OT control network architectures.

- Deliver prebuilt edge AI design patterns by innovating on containerized, modular, low-code and no-code solutions that can operate within the limitations of network, power, compute and storage at the edge.

- Reinforce the value of a data security strategy and embrace privacy by delivering AI models that analyze data learned locally at the edge, ensure that raw data remains at the edge, and pass on the learning to core modeling in the cloud or regional data center, thus preserving privacy.

Gartner Recommended Reading

Industrial Data Management

Analysis By: Emil Berthelsen, Scot Kim

Definition:

Industrial data management involves the collection, integration, and normalization of diverse data from operational technology (OT), information technology (IT), and Internet of Things (IoT) devices. A core function is contextualizing the raw data into semantic models, resulting in normalization and common data objects to create a unified and meaningful view of industrial-scale operations. This process includes capabilities for data cleansing of event, process and operational data streams, translation, quality assurance, scalable storage in time-series databases and data lakes, and security and governance throughout the data life cycle. The ultimate goal is to transform raw data into actionable insights and outcomes, providing a reliable foundation for advanced analytics, AI applications, and optimized decision making across the enterprise.

Sample Vendors

Cybus; Highbyte; HiveMQ; Litmus Automation; MachineMetrics; SightMachine; SymphonyAI

Range

The range for industrial data management is 1 to 3 years from early majority adoption. This range is determined by industrial sector organizations continuing to scale their industrial IoT solutions through connected equipment and assets into enterprisewide solutions with a greater requirement and attention to having ready-to-use and contextualized data for further use in applications, analytical tools and various AI techniques.

Industrial organizations are driving production, asset, and process optimization by harnessing real-time operational data and embracing data-driven operations. Yet, the task of acquiring, harmonizing, and contextualizing this data remains complex and demanding. Addressing these challenges requires a comprehensive strategy: investing in industrial IoT platforms to efficiently collect and manage data; capturing and embedding deep process knowledge and key performance metrics unique to each environment; and leveraging skilled industrial data operations engineers to prepare and curate data for maximum value. Ultimately, this process prepares the operational data for nontechnical engineers as well and builds a structure for federated governance and consistent metadata management.

Each of these steps involves distinct investments and presents cultural and resource challenges, especially as organizations strive for IT-OT convergence to unlock improved business performance.

Advanced analytics and rapidly emerging AI technologies — particularly generative AI — have significantly heightened the strategic importance of industrial data management. Set against the background where data has had an important role in industry and the quantity of that acquired data has experienced an accelerated growth rate, improved tools and processes to store this data have added to the transformation and silo-breaking approaches.

By harmonizing and contextualizing data from diverse industrial assets and enterprise systems, organizations can bridge longstanding silos and unlock transformative insights. As digital transformations accelerate and as companies seek to monetize data through improved decision making and AI-driven automation, investments in industrial data readiness have become a priority. Seamless integration with enterprise data sources is essential for informed decision making and maximizing business value.

Worth noting that despite the promise of generative AI, the general enterprise landscape is characterized by a proliferation of pilot projects with less than 50% conversion to production rates. This underscores the vast potential and the substantial challenges that remain with the latest technologies, including industrial data management (see Providers Must Build Enterprise Scale Adoption of Generative AI).

Mass

The mass is high as IDM becomes a critical and necessary data management process within industry, enhancing the quality and readiness of industrial data by advancing the capabilities of the data to be interoperable and manageable for analytic, AI and application purposes.

The adoption of industrial data management is set to span multiple industries, such as manufacturing, energy and automotive, and functional areas, fundamentally transforming how organizations leverage their information assets. By unifying previously separated IT and OT data environments, companies can create a single, normalized and enterprise-ready set of data objects. This harmonized data foundation enables organizations to break down silos, streamline operations and extract maximum value from their data across the enterprise. Industrial data management will significantly amplify the impact of a wide range of applications and AI-driven use cases. For example, in predictive maintenance, integrated data streams from equipment sensors and historical records will enable more accurate failure predictions and optimized maintenance schedules. Asset performance management will benefit from richer, cross-functional data, supporting better asset utilization and extended equipment lifespans. Additionally, energy management initiatives will be strengthened through improved monitoring and analysis of consumption patterns, helping organizations achieve sustainability goals. Process optimization will become more effective as organizations gain a holistic view of production variables, leading to continuous improvement and greater operational agility. Furthermore, digital twin implementations will rely on high-quality, contextualized data to create accurate virtual models of physical assets and processes.

Current approaches to preparing OT data for IT-OT data management solutions lack a scalable, well-defined and industry-aligned common data object modeling framework at this point in time. This shortfall, as well as an overlap with other data management platforms, makes it difficult to capture the unique characteristics and requirements of specific industries and their processes. By implementing industrial data management solutions that systematically collect, integrate, and normalize diverse data from OT, IT, and IoT sources, organizations can achieve a unified and actionable view of their operations. This comprehensive data foundation enables seamless access for upstream applications, advanced analytics and AI-driven decision making — transforming traditionally slow, costly, and manual data management practices into efficient, automated, and value-generating processes.

Recommended Actions

Product leaders developing industrial data management solutions should focus on highly scalable, industry-specific data collection, integration, and normalization management solutions, tailored to support advanced analytical tools and AI-enabled applications. To achieve this, product leaders should:

- Direct development efforts for industrial data management solutions toward common manufacturing data frameworks, such as Unified Namespaces or a unified data fabric, allowing federated governance and consistent metadata management.

- Partner and collaborate with system integrators who specialize in smart manufacturing to effectively integrate the IDM platform with existing technologies and deliver business value through the implementation of technologies, such as AI-enabled applications, digital twins and simulations.

- Develop specific design patterns for vertical industry use cases with quicker value delivery. These use cases should be scalable and cost-effective, allowing for quicker implementation and reducing technical debt associated with legacy systems.

Gartner Recommended Reading

IoT Applications

Analysis By: Scot Kim

Definition:

An IoT application is software that is natively designed or architecturally enhanced to directly support or integrate with IoT platforms or software. Application integration with IoT edge devices and platforms can be achieved through IoT middleware. It ingests, processes, and analyzes IoT data, along with IT data and other contextual information and events, to improve situational awareness and produce business-relevant outcomes. It can support automation and optimization across enterprise processes. Some enterprise applications, such as APM, CRM, and FSM, use IoT application capabilities today.

Sample Vendors

ABB; Aveva; GE Vernova; Hitachi; IBM; Infor; Oracle; SAP; Siemens; SAS

Range

The majority of IoT applications are expected to be adopted within one to three years, driven by the growing demand for industrial IoT capabilities, particularly the integration of embedded sensors within industrial devices. Examples of IoT applications are predictive maintenance, asset tracking, and quality control. IoT applications’ growth will continue to follow the IT/OT integration adoption trend.

IT/OT integration and AI agents are accelerating IoT application development, which will make this a plausible technology in one to three years by bridging the gap between operational technologies like sensors and machinery, and IT systems that manage data and analytics. According to the 2025 Gartner IT/OT Alignment & Integration Survey, this IT/OT integration with IoT application will deliver cost optimization, workplace and workforce enhancement, product/customer experience, and industrial/equipment operations benefits. As a result, manufacturers, utilities, and other asset operators are deploying more intelligent, connected solutions that enhance efficiency, safety, and decision making.

IoT applications are gaining traction in the industrial sector, driven by market demands such as IT/OT integration, which enables the collection and contextualization of industrial data. According to the 2025 Gartner IT/OT Alignment & Integration Survey, 47% of respondents are extending and 36% are augmenting operational technology (OT) monitoring capabilities through these applications. The common use cases are to enable real-time monitoring, predictive maintenance, and cost optimization. Additionally, the integration of IoT with AI and cloud technologies in multiple industrial markets, such as manufacturing, utilities, oil and gas, and transportation, is contributing to the growth of IoT applications.

Mass

IoT applications have a medium impact on manufacturing among products, people, the environment, equipment, and business processes. However, some manufacturing applications, like predictive maintenance and asset utilization dashboards, are accelerating to a larger scale.

IoT applications have become integrated across all industrial markets, including manufacturing, energy, oil and gas, logistics, and pharmaceuticals, enabling smarter, more connected operations. Their widespread adoption is fueled by the universal demand for real-time data, automation, and advanced analytics to drive hyperautomation and reduce costs. As industries continue to digitize, IoT applications serve as a differentiating technology that allows enterprises to be efficient, agile, and effective in their digital transformation.

The IoT application landscape will continue to evolve, driven by the increasing integration of agentic AI (model context protocol) and agent-to-agent (A2A) within the IoT platform to enable machine learning, computer vision, and edge AI into industrial systems. This integration of different data sources and AI models will deliver real-time analytics and predictive maintenance. As industries continue to digitize, IoT applications will become a foundational technology for operational efficiency, scalability, and innovation.

Recommended Actions

- Partner with IoT platform vendors that offer development tools, integration capabilities, and software-defined kits to support standardized and composable IoT application development.

- Start with IoT applications that offer access to and visibility of key IT and OT data before tackling more complex use cases (e.g., predictive maintenance, real-time asset tracking, energy usage monitoring, quality control automation, and remote equipment management).

- Accelerate innovation and gain a competitive edge by integrating GenAI into your IoT application strategy — empowering teams to rapidly build smarter, more adaptive applications.

Gartner Recommended Reading

IoT Platform

Analysis By: Scot Kim

Definition:

An IoT platform is a composable architecture of assorted software components that enables the development, deployment and management of solutions that connect to and capture data from IoT endpoints to drive improved business decisions. Functional capabilities include IoT edge device management, integration tools and management, data management, analytics, application enablement and management, and security. IoT platforms may be deployed on-premises, as a cloud-based IoT platform as a service (PaaS) or as a hybrid consisting of edge software as IoT PaaS.

Sample Vendors

ABB; Amazon Web Services (AWS); AVEVA; Braincube; Cumulocity; Microsoft; PTC; ROOTCLOUD; Siemens; XCMG Hanyun

Range

The range for IoT platforms is one to three years due to the widely adopted capabilities of industrial data management and advanced analytics, and the enablement of industrial use cases. The IoT platform market is the industry standard for hyperautomated solutions.

IoT platforms are mainstream in manufacturing due to their proven ability to deliver tangible operational excellence, driving significant cost-efficiencies, waste reduction, and improvements in asset reliability. This is further fueled by the pervasive integration of AI and machine learning, including generative AI, into IoT platforms, transforming complex operational data into actionable insights for predictive maintenance, process optimization, and AI-enhanced decision making. These platforms meet evolving market demands for IT/OT convergence, real-time visibility, autonomous operations, and scalable solutions across diverse industrial environments, including legacy systems.

IoT platform adoption in manufacturing is experiencing rapid and accelerating growth, with several vendors reporting substantial year-over-year revenue increases, some reaching up to 180%. This swift uptake is further demonstrated by platform growth rates frequently surpassing the industrial IoT platform market’s average of 21.4%, reflecting these solutions’ broadly acknowledged tangible top- and bottom-line impact. The pervasive integration of AI and machine learning, including generative AI, alongside the critical need for IT/OT convergence, transforms operational data into actionable insights, driving autonomous operations and scalable digital transformation initiatives across industries.

Mass

The mass of the IoT platform is very high because the capabilities of agentic AI and AI agents have been added to the overall platform solutions.

IoT has broad appeal within the manufacturing sector (discrete and process) in terms of the value derived from connecting and analyzing assets and processes. Industrial enterprise IoT deployments have proven to be the larger market. This is because global manufacturers use IoT for optimizing costs, improving processes, and augmenting and replacing the functions of OT systems.

What has distinguished the IoT platform market over the past few years is the impact of non-IT, nontraditional buying centers that drive increasing demand for IoT solutions. This trend will increase as IoT becomes more entwined with digital business. By combining cloud and traditional analytics with innovative AI/ML techniques, the investments required to be competitive are rising.

IIoT platform adoption is rapidly disrupting traditional operational technology (OT) by acting as the central enabler for IT/OT convergence, dissolving long-standing data silos across the manufacturing enterprise. This is achieved by securely integrating real-time data from legacy and modern industrial control systems, contextualizing it through digital twins, and embedding advanced AI/ML and generative AI capabilities directly into operational workflows at both the edge and the cloud. This paradigm shift moves manufacturing from reactive to proactive and autonomous operations, democratizing data-driven insights and leading to substantial improvements in efficiency, quality, and cost that reshape traditional production and asset management.

Recommended Actions

- Accelerate AI-native and generative AI capabilities across the data life cycle: Product leaders should prioritize integrating cutting-edge AI and generative AI to move beyond basic monitoring toward intelligent automation, enabling faster operational decisions, automated reporting and guided diagnostics. This includes leveraging AI for insights, generating synthetic data and even building AI-assisted applications to enhance the entire industrial data life cycle.

- Deepen IT/OT convergence through unified industrial data management and knowledge graphs: Investment is crucial in platforms that can securely integrate and contextualize disparate data from various IT, OT and engineering technology (ET) sources, creating a comprehensive digital twin and a unifying data layer. This approach transforms siloed data into actionable intelligence, enabling cross-domain analytics and a “closed loop” between insights and operational improvements.

- Prioritize edge-native capabilities for real-time autonomy and enhanced security: Focus on robust edge solutions that support local data processing, AI execution and real-time control, thereby minimizing latency and reducing reliance on cloud connectivity for critical operations. This also enhances security by creating a protective barrier between sensitive OT systems and the internet, addressing growing concerns about cyberthreats like ransomware.

Gartner Recommended Reading

3 to 6 Years

Digital Twins

Analysis By: Evan Brown, Scot Kim

Definition:

A digital twin is a technology-enabled proxy that mirrors the state of a thing. A “thing” may be a physical or a virtual asset, process, person or organization, or collections thereof. A digital twin corresponds one-on-one to the thing it mirrors, with at least some stateful data about the thing (such as IoT telemetry or application state changes) sourced via monitoring. An external application can be used to query this information (e.g., via APIs), and in some cases, send control signals to the digital twin that change the state of the “real” asset or process.

Sample Vendors

Aerogility; AVEVA; AWS; Braincube; Cognite; Cosmo Tech; Cumulocity; DataMesh; Hexagon; Microsoft

Range

Digital twins are one to three years out from early majority adoption in manufacturing due to increasing interest among prospective adopters, a growing number of high-value deployments, and ongoing tech advancements among providers enabling new use cases and increasing product functionality.

Digital twin adoption has grown over the last five years and continues to expand when it comes to early majority adoption of manufacturing-related solutions. As current trends continue, digital twins in manufacturing will become a standard technology, especially as more midsize manufacturers follow the lead of early adopters, and as issues surrounding standards and integration are addressed, making IoT platforms more plug-and-play.

According to the 2025 Gartner CIO and Technology Executive Survey, 23% of respondents have already invested in digital twins for manufacturing, with another 56% planning to invest within the next three years. This indicates growing interest in the technology; however, the form of these solutions varies.

While some comprehensive digital twins cover entire facilities, most current deployments are limited in scope due to challenges such as high costs, lack of standards, employee resistance, and the need for significant retrofitting. In some cases, companies are opting to build new facilities specifically designed for digital twin integration. As a result, most digital twins in manufacturing today focus on specific use cases or sets of assets.

Despite these challenges, digital twins are delivering substantial value, encouraging further investment and broader adoption. As organizations gain confidence in the ROI of digital twins, larger-scale projects are expected to increase, expanding the technology’s impact across the manufacturing sector.

Mass

The mass for digital twins is high as they are an evolution of existing ET, OT and IoT infrastructure that provides strong value across multiple segments of manufacturing.

Digital twins are a unification of existing systems. This enables them to address many use cases, most of which provide cost savings and/or efficiency gains. Today, common use cases for digital twins in manufacturing include:

Equipment monitoring and predictive maintenance: Digital twins provide a deeper look at the historical and current status of an asset. This is enabling the identification of discrepancies in everyday operations and thus potential problems that would have gone unnoticed by more traditional methods.

Production optimization: Digital twins are optimizing production via simulation and analysis of manufacturing assets and processes to identify bottlenecks and other inefficiencies, including factory layout and planning.

Supply chain planning: By increasing end-to-end visibility in the supply chain, digital twins can simulate potential disruptions and better optimize logistics.

Warehouse monitoring: Digital twins in warehousing are being used to optimize layouts and manage inventory, as well as support early deployments of robotics and automation.

Digital twins show substantial potential, and product leaders are actively working to address the challenges associated with current adoption. This includes templates and libraries to more seamlessly integrate with a wider range of IoT devices and sensors, as well as adopting standards and APIs to better ensure their solutions can work across different platforms and ecosystems.

Additionally, providers are rapidly increasing the value provided by digital twin solutions via the incorporation of advanced simulation capabilities. While the most common outcomes of this advancement are often further enhancements to overall efficiency, simulation is also enabling entirely new use cases for digital twins, such as digital product and production testing, as well as AI assessment and guidance of processes.

Recommended Actions

- Enable more comprehensive and higher-performing implementations by preemptively seeking out manufacturing prospects in the earliest stages of IoT adoption in operations, as the combination of IoT and digital twin enhances the overall value proposition of the implementation.

- Develop modular, templatized digital twin solutions tailored to high-value manufacturing verticals (e.g., automotive, aerospace, electronics) and common use cases to accelerate deployment, lower customization costs and increase success rates.

- Pursue partnerships with providers of associated technologies and services, such as manufacturing equipment, logistics and eventually simulation solutions, to better address more advanced use cases and expand existing implementations.

Gartner Recommended Reading

GenAI-Enabled IoT

Analysis By: Milly Xiang

Definition:

Generative AI (GenAI)-enabled Internet of Things (IoT) solutions represent a transformative convergence of GenAI and IoT. These solutions leverage GenAI techniques across multiple tiers of the IoT technology stack — including edge, on-premises, and cloud environments — to extract actionable insights from diverse data sources, such as sensors, machine vision (video and still images), acoustic signals and network traffic. The primary objective is to unlock new operational efficiencies, accelerate innovation in product and process design, and enable real-time, context-aware decision making.

Sample Vendors

Amazon Web Services (AWS); GE Vernova; IBM; Microsoft; PTC; Rockwell Automation; Siemens

Range: 3 to 6 Years

The GenAI-enabled IoT is a growing technology that will enrich the IoT manufacturing market. Due to the early stages of GenAI-enabled IoT, the adoption of the technology will accelerate when manufacturers begin to enable factory automation.

Gartner considers GenAI-enabled IoT to be three to six years from early majority adoption, with industrial-specific use cases still in the nascent stage. The current focus of most GenAI models is on unstructured data (text, images and audio), with limited application to time-series and sensor data prevalent in manufacturing environments. The sector’s stringent requirements for accuracy, reliability and low-latency responses — especially in safety-critical or process-intensive operations — pose additional challenges for large-scale deployment.

Major developments have been witnessed around product launches and upgrades catering to a plethora of use cases. For example, Wiliot announced the launch of WiliBot, a GenAI chatbot that enables natural language conversations with any ambient IoT-connected product. Climate LLC, the digital farming subsidiary of Bayer, has developed Climate FieldView — an AI agent that allows farmers to design and monitor their fields for greater yields and efficient fertilization. Other developments included partnerships and collaborations among companies to co-develop solutions with GenAI capabilities to better serve customers through improved data collection and remediations, enabling significant gains in efficiency and productivity. Over the next three years, we expect to see increased vendor activity applying GenAI to the IoT context to bring GenAI-enabled IoT innovations to broader use cases.

Mass: High

The opportunity to grow into multiple sectors is highly likely due to the overall buying trends of manufacturers to proliferate smart manufacturing.

The very high mass rating for GenAI-enabled IoT is due to its applicability across:

- Smart factory design: GenAI can generate digital twins and virtual prototypes, allowing manufacturers to simulate, test and optimize production lines before physical implementation, thus reducing time to market and prototyping costs.

- Predictive maintenance: By synthesizing new data and learning from historical machine logs, GenAI can improve anomaly detection, predict equipment failures and recommend optimal maintenance schedules, minimizing unplanned downtime.

- Process optimization: GenAI can analyze sensor and machine data in real time to dynamically adjust process parameters, maximizing yield, reducing scrap and improving energy efficiency.

- Quality assurance: Advanced machine vision models can be generated and fine-tuned to identify defects, classify products and ensure compliance with quality standards.

- Supply chain resilience: GenAI can simulate supply chain disruptions and optimize inventory and logistics in response to real-time IoT data.

In addition, GenAI enables further advancements in IoT and has the potential to create new use cases, capabilities and business models across the manufacturing value chain. Not only IoT device and smart-connected product manufacturers, and IoT asset operators will be impacted, but also broader software and service product leaders that can leverage GenAI to develop industry-specific solutions that offer differentiated value, thus creating a competitive edge.

Recommended Actions

- Integrate GenAI capabilities into your IoT solution roadmap now. Identify high-impact use cases — such as predictive maintenance, process optimization or digital twin simulations — where GenAI can deliver measurable improvements in efficiency, quality or cost.

- Utilize established IoT platforms and GenAI toolkits to accelerate model development and deployment. Focus on modular, use-case-oriented solutions that can be iteratively refined based on real-world feedback and fine-tune models using domain-specific data to ensure high accuracy and reliability in manufacturing contexts.

- Engage with different stakeholders in customers such as data scientists, process engineers and IT/operational technology (OT) teams to ensure that GenAI-enabled IoT solutions are aligned with operational realities and regulatory requirements.

Gartner Recommended Reading

IoT Data Analytics

Analysis By: Kevin Quinn, Scot Kim

Definition:

Internet of Things (IoT) data analytics is insights (including predictions and recommendations) derived from the data emanating from IoT devices. Data may be structured, semi-structured or unstructured and may come from sensors, actuators and cameras in equipment. The data is often fragmented and delivered at different intervals, requiring significant integration efforts. Data from cameras — like images, video and audio — may require computer vision AI to process and leverage its potential insights. The data may also be integrated via industrial IoT (IIoT) platforms and originate from core business applications such as ERP, manufacturing execution systems (MES), product life cycle management (PLM) and CRM.

IoT data analytics may require real-time visualizations that represent the data as it arrives (e.g., stock tickers showing price fluctuations). Additionally, it might need to apply adaptive learning to data as it continuously arrives to make predictions about future conditions and issues. Recent advancements in IoT data analytics have introduced generative AI (GenAI) to process data from equipment documentation and ticketing systems to automatically recommend the next best action for issue mitigation (a.k.a. prescriptive analytics).

Sample Vendors

Altair; AVEVA; Bentley Systems; Cognite; Databricks; MathWorks; SAS; Seeq; Siemens; Sight Machine

Range

IoT data analytics is three to six years from early majority adoption because multiple data analytics solutions have already been deployed across IoT applications in industries and building automation. Organizations quickly move through four stages of maturity that include: connect, monitor, predict and prescribe, and optimize. Most will experience these IoT data analytics as part of an IoT application that contextualizes IoT insights to enhance decision making.

IoT data analytics is close to majority adoption, as it is already manifested in widely adopted applications for predictive maintenance, product quality, energy management, asset monitoring and tracking, and employee safety. Each of these use cases drives significant savings and risk mitigation.

Companies have been slow to take steps toward maturity in IoT data analytics, often hitting roadblocks after connecting and monitoring equipment. Lack of knowledgeable resources and insufficient or poorly prepared data inhibit the positive effects of AI and machine learning, slowing progress toward the next stages. Further, companies often opt for prebuilt applications that require a vetting process.

Mass

IoT data analytics has a high impact because reducing equipment downtime and energy consumption while improving product quality and employee safety all have evident, quantifiable results, resulting in clear ROI.

We rate the mass of IoT data analytics as medium because it builds on existing datasets, extends the value of data and applies to almost all non-service-based industries across geographies. Generating insights from large amounts of unstructured operational technology (OT) data, and structured but fragmented data from legacy systems like ERP, product life cycle management (PLM) and manufacturing execution system (MES), is already perceived as valuable. Those capabilities will improve as large investments continue to be made in IoT data analytics to meet customers’ business needs.

IoT analytics is secondary to AI as a technology, but AI is driving renewed interest in the insights and business outcomes that can be achieved by combining AI and IoT data. According to State of IoT Spring 2024: 10 Emerging IoT Trends Driving Market Growth, the IoT market will grow at a compound annual growth rate (CAGR) of 17% through 2030, reaching a market value of $236 billion. The massive investments in AI will act as a tailwind driving the significant growth and impact of IoT data analytics.

Recommended Actions

- Develop a robust data fabric that aggregates data from heterogeneous manufacturing devices and applications using tools and techniques that facilitate data sharing across physical data sources and applications, thereby improving data-driven decision making.

- Build or partner to offer solutions that can contextualize data from business applications by developing generic data models and optimizing them for vertical submarkets, in order to enhance interoperability and reliability of output.

- Provide a set of data standards by auditing data origins, establishing policy around data ownership and providing access across the business process.

- Provide templates for common IoT solutions like predictive maintenance, energy management, product quality and employee safety to accelerate customer business outcomes.

- Leverage unstructured data from IT ticketing systems and documentation via large language models to provide conversational solutions that recommend the next best action.

Gartner Recommended Reading

IoT Edge Architecture

Analysis By: Mohini Dukes

Definition:

IoT edge architecture represents hardware, software and communication elements that optimize capabilities — such as computing, storage, networking and analytics — to be deployed closer to where the IoT data and events are produced or consumed. Edge architecture defines how information generated by sensors and endpoints is aggregated, managed and handled at the edge of a network or location. Under an IoT edge architecture, intelligence within a connected system is distributed according to where the business case requires it most. IoT edge architecture is part of a broader distributed data and computing topology to meet IoT-enabled business outcomes.

Sample Vendors

Amazon Web Services (AWS); Cisco; Edge Impulse; Ericsson; Litmus; Microsoft; Siemens; StorMagic; Supermicro; ZEDEDA

Range

The range is one to three years because 34% of manufacturing organizations have deployed edge computing (as per the 2023 Gartner Smart Manufacturing Strategy and Implementation Trends Survey), but they need to shift toward a platform approach that combines these components and evolves with data. Skill sets, processes and partnerships must develop in conjunction with technologies and architecture.

Infrastructure components such as compute, storage and networking are foundational for distributed IoT data processing. The trend toward multimodal data and AI drives the gradual sophistication of processing capabilities and higher data gravity at the edge. This, in turn, results in the creation of a platform that combines IoT and edge architecture components.

Organizations are beginning to include edge capabilities in their product and technology evaluations. The broad scope of IoT and edge reflects a range of business and technical requirements and use cases that the market needs to address.

Technology vendors focused on IoT are trying to develop varying levels of edge processing capabilities into their solutions and services. The implementations are still nascent due to the level of complexity, need for partner ecosystem, existing friction between IT and OT requirements, emergent AI capabilities, limited solution integration and complexity.

IoT edge architecture involves diverse physical environments, remote locations and a heterogeneous equipment mix. Accordingly, there can be a need for ruggedized hardware appliances, edge-native software adapted to resource constraints, remote zero-touch deployment and maintenance.

Mass

The mass is high because an IoT edge architecture based on a well-defined technology roadmap is the cornerstone of many digital transformation initiatives, particularly in industrial verticals such as manufacturing, oil and gas, utilities, heavy transportation, and mining. For example, saving the cost of data transmitted or high latency drives initial focus. This can evolve toward including digital twins to predict supply fluctuations or dynamic process optimization and execution with agentic AI or applying physical AI to execute tasks in hazardous environments.

IoT edge architecture consists of several technologies or solutions and service components. Moreover, some of these components may be associated entirely with the IT or OT environments, thereby increasing the complexity of planning and preparing for this stack. By addressing the complexity of IT/OT integration, the number of industrial IoT platforms and edge providers has increased over the last three years due to manufacturers who are increasing investments to achieve higher levels of automation and autonomy.

The availability of interoperable or compatible services and solutions, or products within an ecosystem will directly impact edge architectural choices. This is because edge architecture is part of a broader data and computing topology discussion for an organization. Thus, edge architecture either drives or influences the IoT project’s upfront costs (particularly software and integration), as well as operational costs (especially communications).

Technology providers have the opportunity to provide integrated solutions that reduce complexity and provide manufacturing organizations the flexibility to adapt to changing business needs, including implementing AI initiatives based on IoT data.

Recommended Actions

- Create industry-specific edge architectural solutions that can support an organization’s living IoT edge architectural platform strategy, aligning with its changing business and operational outcomes. The solution architecture has to be flexible to accommodate multiple concurrent states of data evolution.

- Establish an IoT edge design pattern to align against the manufacturer’s IoT strategy with an edge-to-cloud strategy by determining which elements of the edge the product will enable to achieve key manufacturing outcomes like closed feedback loop automation, data security at the edge and industrial data management capabilities.

- Make sure to profile and track IoT and edge deployment among top manufacturers. This allows you to track their lessons learned on data patterns and the convergence between edge platform and IoT capabilities that need to be developed.

Gartner Recommended Reading

Product Servitization

Analysis By: Scot Kim

Definition:

Product servitization is a business model that delivers a product (typically non-IT or software-defined Internet of Things [IoT] assets) with life cycle services as either a recurring-revenue service or a metered usage-based service. This is a digital product that is tightly coupling with the physical product to deliver value-add outcomes. These outcomes range from real-time reporting on the state and health of the products, to advanced anomaly detection, to a machine’s increased capabilities for remote operations or even autonomous operation. Product servitization agreements are differentiated from legacy asset ownership, outsourcing and leasing models by offering guaranteed outcomes associated with the product’s functionality and reliability with qualitative benchmarks for asset availability, performance and the quality of business outcomes. These guaranteed outcomes can be delivered to the customer as an equipment-as-a-service agreement or a digital product experience. Essential among the required technologies for product servitization is edge AI to ensure product servitization achieves cost-effectiveness, in terms of shifting the business model from capital expenditure (capex) offerings to an operating expenditure (opex) offering. This increases profitability for both the user organization and the service provider. Edge AI also provides essential capabilities for autonomy, improved service levels, and avoidance and remediation of service-impacting events.

Sample Vendors

Aria Systems; Augury; Caterpillar; Cumulocity; KCF Technologies; Michelin Group; Microsoft; NTT Data; Servitly; Xylem; ZIPIT; Zuora

Range: 3 to 6 Years

The range is three to six years as product servitization for heavy assets and equipment is still being reconciled in terms of an opex-based transaction. Some products are extended at cost, or free of charge, based on a multiyear engagement to include full life cycle services and other ad hoc transactions enabled by the new digital foundation (machines as customers).

There are technical inhibitors to product servitization adoption. For example, the complexity of end-to-end IoT and AI business solutions. Also included are technical challenges with device management and security, and the integration and information management of asset data with enterprise business planning and logistics applications. Product servitization faces key commercial inhibitors, such as:

- Immature and ever-changing product servitization business models and fears of cannibalizing existing revenue of OEMs and service providers offering traditional, reactive services in support of products

- Manufacturers’ reluctance to open access, sensitive product data to partners and competitors that seek to manage heterogeneous environments. For example, third-party service providers or the service units of competitive OEMs seeking to servitize the refrigeration infrastructure and freezer cases from multiple manufacturers within a grocery store and chain)

- Lack of digital skills, investments and digital dexterity by the legacy IT and OT providers

In addition to a technical challenge for enablement, product servitization is largely driven by supply- and demand-side requirements. Despite these obstacles, product servitization is well-positioned to experience accelerated adoption in the next three to six years. Most manufacturers of discrete products seek servitization that creates unique customer experiences and new forms of monetization. Enterprises look to servitized products as a way to change how they invest in personal property for the business.

Gartner believes that over the next few years, there will be many examples of success where OEMs — or their various go-to-market partners — work to servitize mobility products. For example, trucks, construction equipment, farming equipment, home appliances and automobiles, to usage-based acquisition.

Additionally, Gartner has observed commercial real estate and construction companies pursuing relationships with OEMs to create intelligent work environments. In these environments, such as manufacturing, office space, and construction sites, they engage OEMs or their distributors and resellers to create usage-based agreements for equipment built into the physical plant, such as repatriated manufacturing. The future success of product servitization lies in the use of the Internet of Things (IoT), edge computing, AI and software applications to improve product performance and facilitate remote intervention and control when needed.

The most common impediment to product servitization is any approach to risk mitigation by manufacturers and service providers. If the asset is large or integrated into the physical plant, removing the risk inherent in at-will contracts associated with as-a-service structures is nearly impossible.

Mass: Very High

The mass is very high because it will enable providers to sell new services and will impact virtually every industry.

Product servitization enables capital assets offered by OEMs or OEM partners to be extended as outcomes, priced as recurring operating charges. When products are servitized, the user acquires asset-based services (outputs), scoped within the desired results relating to performance, availability and output quality.

Moreover, servitized products are integrated with the asset owner’s back-end business and operational applications and field service management systems, automating the procurement of spare parts and repair scheduling without intermediaries. Product servitization creates a more streamlined approach to asset management. Growing demand for improved visibility and control of IoT devices in asset-dense and distributed environments creates an opportunity for product leaders to servitize their offerings.

The key to this emerging business model’s success is using embedded technologies, advanced analytics and AI techniques for optimized functionality, and providing users and service providers with asset insight and control. Edge AI enables remote product monitoring, control and optimization, and feature expansion through software releases (over-the-air software upgrades, updates and patches). These use cases are most commonly found in industrial environments, because manufacturers are asset-intensive enterprises. The barriers to entry for product servitization is not the technology adoption but the change in behavior when it comes to a lucrative business model. There are several obstacles for both provider and end-user when it comes to adoption. Those obstacles can be but not limited to pricing, reliability of servitization, data sharing among the ecosystem of partners and ownership of services and assets.

Recommended Actions

- Target manufacturers of smaller, mobile and semimobile products by creating use-case templates that span technical and financial engineering to enable product servitization that offers undeniable value.

- Work to create a service delivery platform that extends beyond connectivity and basic asset state and health data by focusing on service delivery elements that extend to customer experience. For example, subscription software for rating-metering-billing, or working with industrial customers to transform their human-machine interface (HMI) systems for more advanced and dynamic data presentation.

- Create loyalty with OEMs that servitize products by identifying and creating service catalogs for users and reseller-distribution partners, to benefit from data and services from servitized products.

Gartner Recommended Reading

6 to 8 Years

Industry Cloud Platforms

Analysis By: Kentaro Shikanai

Definition:

Industry cloud platforms (ICPs) are orchestration capabilities that address industry-specific business outcomes by combining underlying SaaS, PaaS and IaaS services into composable offerings. They coordinate and deliver modular packaged business capabilities (PBCs), such as predictive maintenance, quality control, and batch optimization, typically including industry data fabric, marketplace ecosystems, and business orchestration and automation tools (BOATs). Many ICPs incorporate AI-based capabilities to enhance decision making and automation. Effective ICPs require alignment with industrial Internet of Things (IIoT) platforms for foundational device connectivity, data ingestion and protocol translation, enabling efficient PBC deployment across complex industrial environments while addressing regulatory compliance and macroeconomic VUCA challenges.

Sample Vendors

Amazon Web Services; Google; IBM; Microsoft; Oracle; SAP; Siemens

Range

The range is six to eight years, as ICP adoption is accelerated by the growth of the ICP ecosystem offering industry-specific PBCs, strong demand for modular solutions addressing targeted manufacturing pain points, and widespread IIoT platform deployment enabling seamless device connectivity and data ingestion. Additionally, regulatory requirements for traceability and compliance, digital transformation imperatives, and competitive pressures are supporting adoption, as PBCs provide auditable, modular tools that meet industry standards efficiently.

Integration with legacy applications and diverse operational technology (OT) and engineering technology (ET) systems is complex and costly, while a lack of unified IIoT platforms leads to persistent data silos and limited actionable insights. Interoperability issues, inconsistent APIs, digital thread absence and vendor lock-in slow deployment. Security vulnerabilities and regulatory hurdles increase compliance risk. High initial costs, skills shortages and workforce resistance further delay adoption. Fragmented vendor ecosystems and the absence of modular standards hinder scalability and time to maturity.

ICPs are gradually transforming industries by enabling agile, data-driven operations. New regulations like the Digital Markets Act are pushing compliant cloud architectures. With IIoT platforms, ICPs enable cross-functional data integration across IT/OT/ET systems with industry-standard protocols and cloud-native scalability capabilities that exceed traditional data mart approaches, which are typically limited to departmental scope and face scalability constraints as data volumes grow. However, legacy integration challenges and regulatory tensions prompt some to reassess cloud strategies, though data mesh and hybrid approaches help mitigate these issues.

Mass

The mass is high because the ICP ecosystem, serving customers across various industries, enhances enterprise solutions by advancing their product capabilities with interoperable, rapidly deployable features.

The ICP ecosystem spans multiple industries, business functions, and markets because its modular PBCs address common and sector-specific needs, such as predictive maintenance, compliance and process optimization. These capabilities can be tailored for manufacturing, healthcare, energy, and more, supporting diverse workflows from supply chain to R&D. Collaboration among hyperscalers, enterprise software, OT/ET vendors, and system integrators ensures interoperability and regulatory compliance, enabling ICPs to adapt globally and regionally.

ICPs with modular, industry-specific PBCs aligned to IIoT platforms advance enterprise software, OT, ET vendors and system integrators by enabling verticalized, interoperable and rapidly deployable solutions. Product capabilities typically enhanced include real-time process optimization, digital twin integration, compliance automation, and cross-life-cycle data sharing. Challenges include interoperability fragmentation, skills gaps and legacy integration. Overcoming these requires adopting open standards, building PBC libraries, leveraging low-code tools, and fostering vendor collaboration for seamless integration and deployment.

Recommended Actions

Product leaders developing ICPs must focus on building vertical-specific, interoperable and rapidly deployable PBCs tailored to industry-specific workflows.

- Enterprise software vendors must design PBCs that leverage IIoT data via open standards (OPC UA, MQTT) and APIs, ensuring seamless integration with enterprise application systems and compliance automation.

- OT vendors should standardize device connectivity and security, offering edge-to-cloud solutions for real-time data processing.

- ET vendors need to enable digital twin integration and low-code customization, connecting CAD/PLM tools to IIoT data streams for real-time process optimization and sustainability analytics.

- System integrators should bridge legacy systems with IIoT platforms, curate industry-specific PBC libraries and provide training for IIoT-PBC orchestration.

This approach ensures ICPs deliver actionable, industry-specific outcomes while remaining flexible and scalable. It addresses key challenges like legacy integration and compliance.

Gartner Recommended Reading

About the Impact Radar

This Emerging Tech Impact Radar content analyzes and illustrates two significant aspects of impact — when we expect it to have a significant impact on the market (namely, the range); and how big of an impact it has on relevant markets (specifically, mass). Each emerging technology or trend profile analysis is composed of these two aspects. See Note 1 for a complete description of our approach to this research.

In this document, profiles are organized by range and mass. Impact Radar range starts with the center and moves to the outer rings of the radar.The emerging technology’s position on the impact radar represents when it will cross the chasm from early adopter to early majority. The rings represent one to three years, three to six years and six to eight years from crossing the chasm.

Mass is rated from very high to very low. The higher the mass score, the more broadly the emerging technology or trend is predicted to be adopted, and the more revolutionary the innovation is expected to be.

The objective of this research is to guide product leaders on how emerging technologies and trends are evolving and impacting areas of interest. Providers can leverage this knowledge to determine which technologies or trends are most important to the success of their business and when it makes sense to advance their products and services by investing in them.

Technology vendors should use this Emerging Tech Impact Radar to:

- Identify emerging technologies and trends that are important to the success of their business

- Determine when to act on those trends and technologies based on business strategy

- Begin formulating a response to the technology’s or trend’s evolution

1 2025 Gartner Business Outcomes of Technology Survey. This survey was conducted to understand how industries leverage technologies for various use cases. It assessed investment, deployment and implementation strategies for industry technologies. It also examined key areas intended to be impacted by technology investments, including challenges to realizing business outcomes and industry key performance indicators. The survey was conducted online from June through August 2025. The 648 respondents were from midsize, large and global enterprises from North America, EMEA and Asia/Pacific. The respondents were screened for senior IT and some business leadership roles with technology decision-making responsibilities. Disclaimer: The results of this survey do not represent global findings or the market as a whole, but reflect the sentiments of the respondents and companies surveyed.

Note 1: Research and Methodology for the Emerging Tech Impact Radar

The Emerging Tech Impact Radar content analyzes and illustrates two significant aspects of impact:

- When we expect it to have a significant impact on the market (specifically, range)

- How big an impact it will have on relevant markets (namely, mass)

Analysts evaluate range and mass independently and score them each on a 1-to-5 Likert-type scale:

- For range, this scoring determines in which radar ring the emerging technologies and trends will appear.

- For mass, the score determines the size of the radar point.

In the Emerging Tech Impact Radar, the range estimates the distance (in years) that the technology, technique or trend is from crossing over from early adopter status to early majority adoption. This indicates that the technology is prepared for and progressing toward mass adoption. So at its core, range is an estimation of the rate at which successful customer implementations will accelerate. That acceleration is scored on a 5-point scale, with 1 being very distant (beyond eight years) and 5 being very near (within a year). Each of the five scoring points corresponds to a ring of the Emerging Tech Impact Radar graphic (see Figure 1). Those emerging technologies and trends with a score of 1 (beyond eight years) do not qualify for inclusion on the radar. When formulating scores for range, Gartner analysts consider many factors, including:

- The volume of current successful implementations

- The rate of new successful implementations

- The number of implementations required to move from early adopter to early majority

- The growth of the vendor community

- The growth in venture investment

Mass in the Emerging Tech Impact Radar estimates how substantial an impact the technology or trend will have on existing products and markets. Mass is also scored on a 5-point scale — with 1 being very low impact and 5 being very high impact. Emerging technologies and trends with a score of 1 are not included in the radar. When evaluating mass, Gartner analysts examine the breadth of impact across existing products (specifically, sectors affected) and the extent of the disruption to existing product capabilities. It should be noted that an emerging technology or trend may be expressed in different positions on different Emerging Tech Impact Radars. This occurs when the maturity of emerging technologies and trends varies based on the scope of radar coverage.