Magic Quadrant for Cloud ERP Services

6 May 2026 - ID G00827853 - 58 min read

By Danny Kreidy, Shubham Rathore, and 2 more

Enterprises engage external services for cloud ERP applications to modernize their ERPs and drive better business outcomes. IT leaders should use this Magic Quadrant to evaluate providers of cloud ERP services as part of their composable ERP strategy.

Market Definition/Description

Gartner defines cloud ERP services as those delivered by third-party system integrators that drive enterprisewide business transformation through the modernization of back-office systems. These services go beyond technical implementation, acting as strategic enablers that fundamentally reshape how organizations operate, innovate and compete. By leveraging cloud-based ERP platforms, businesses are transforming core processes across finance, human capital, supply chain, procurement and manufacturing to achieve greater agility, resilience and digital maturity.

Clients engage third-party ERP service providers to lead holistic business transformations anchored in cloud ERP solutions. This includes:

- End-to-end process transformation for financial management (FM) functionality, human capital management (HCM) and supply chain management (SCM)

- Implementation strategy innovation and operation of the cloud ERP solution

- Continuous enhancement and innovation of the surrounding ERP ecosystem to support business adaptability, growth and evolving industry demands

Mandatory Features

The mandatory service provider competencies for this market include:

- Ability to provide services on the cloud ERP solutions (SaaS and associated PaaS) and to support clients across all phases of assessment, implementation and ongoing managed services of cloud ERP platforms. Note: This excludes IaaS based solutions where noncloud ERP products are hosted on a cloud platform.

- Deep business consulting expertise to design transformative operating models and workflows aligned with ERP capabilities.

- Tools and capabilities for data transformation, integration and change management to ensure adoption and sustainable value realization.

- Functional and domain knowledge of ERP modules and components, with an understanding of industry-specific nuances and regional regulatory contexts.

- Ongoing support for ERP updates, alignment with roadmap enhancements and a proactive role in helping clients innovate continuously.

- Expertise in at least two of the following technologies:

- Microsoft Dynamics 365

- Oracle Fusion Cloud ERP

- SAP Cloud ERP

- Workday

Optional Features

The optional features for this market include:

- Outcome-based engagement models, with providers taking accountability for achieving defined business benefits

- Scalable, modern support models that ensure agility and responsiveness postimplementation

- Ability to support enterprises through the quarterly or biannual updates from the software provider

- Ability to provide expertise and vision related to the future capabilities needed and added to the cloud ERP product over time, plus work with the SaaS provider to get the client priorities addressed

- Ability to support enterprises of varying sizes and across multiple geographies

- Capabilities to embed AI/ML within cloud ERP platforms to enable predictive analytics

- Intelligent automation to enhance decision making and operational efficiency across ERP processes

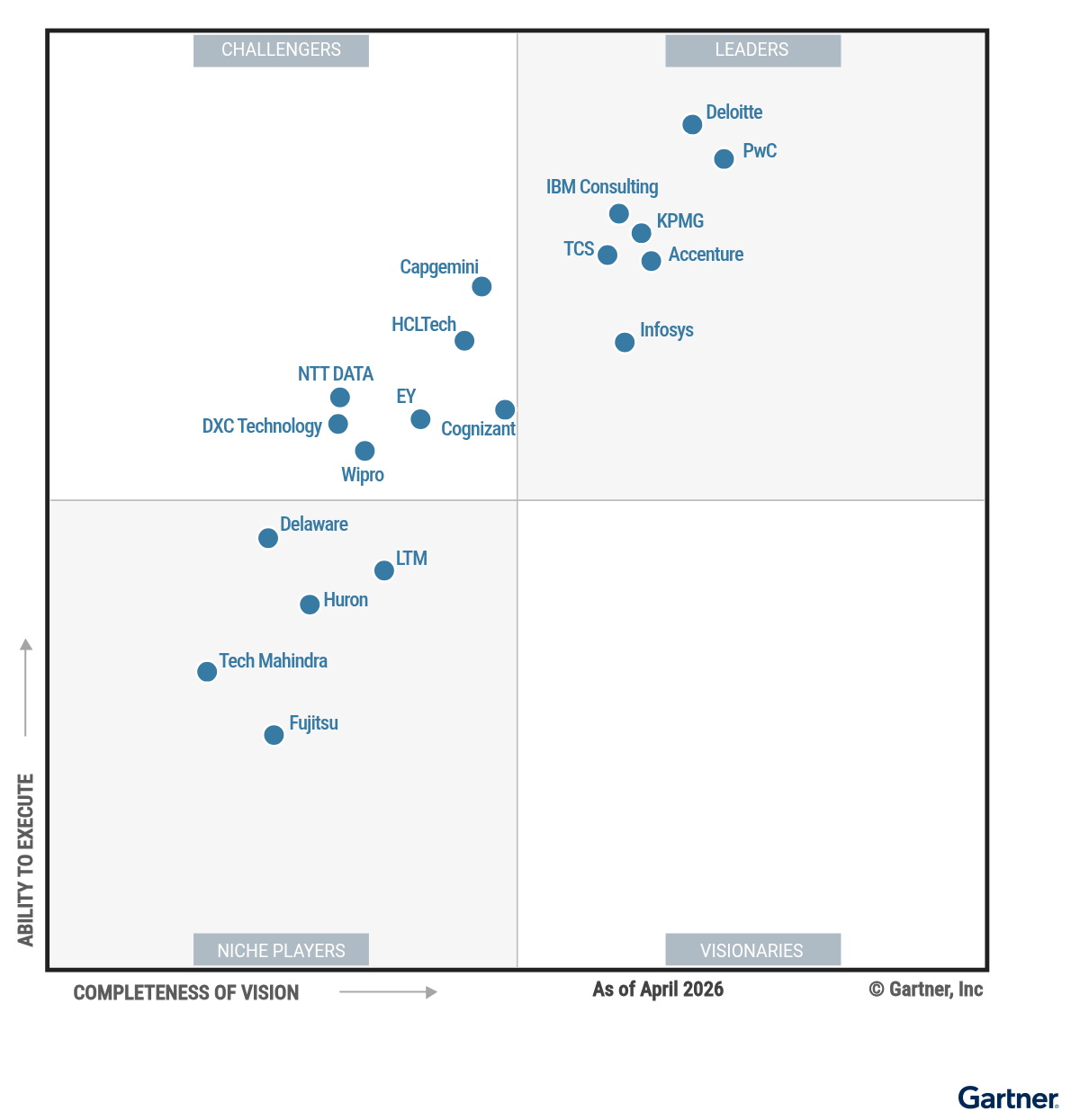

Magic Quadrant

Vendor Strengths and Cautions

Accenture

Accenture is a Leader in this Magic Quadrant. Headquartered in Ireland, its cloud ERP services are broadly focused on “Total Enterprise Reinvention,” integrating cloud infrastructure, AI and autonomous business processes. Operations are geographically diversified across 120 countries, serving large global enterprises across 13 major industries.

Its cloud ERP practice represents roughly 7% to 10% of its total global employees. Furthermore, Accenture maintains strong solution coverage across the four major cloud ERP platforms, operating as a leading, strategic partner for SAP, Oracle, Microsoft, and Workday.

Accenture declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- Execution excellence and automation: Accenture leverages its “platform-first” approach using proprietary assets like myWizard and GenWizard to automate the software delivery life cycle. By infusing the use of AI and industry templates, clients have reported up to a 30% reduction in total cost of ownership (TCO) and a 40% reduction in incident resolution time.

- Pervasive AI and industry innovation: Accenture uses agentic AI hierarchies and preconfigured vertical solutions (like NAVAI for the public sector) and Industry X digital twins/robotics. However,the AI-platform-led approach often conflicts with the specific needs and agility required for specialized ERP migrations.

- Flexible outcome-based models: Accenture is aggressively shifting from input-based pricing to outcome-driven partnerships. By utilizing intelligent pricing that mixes multiple models within a single agreement, clients benefit from a partnership where payments are aligned with business outcomes.

- Target market focus on massive-scale enterprises: Since Accenture prioritizes large-scale, complex transformations and “Total Enterprise Reinvention,” midsize organizations or those seeking traditional ERP upgrades may find Accenture’s comprehensive orchestration models over-engineered or misaligned with their scope and budget.

- Value realization timelines in AI services: As Accenture prioritizes large-scale, AI-driven transformations and autonomous enterprise operations, the initial value realization for clients may be delayed or difficult to assess. This requires a reliance on “pay only for results” structures to mitigate upfront financial risk, which may not be suitable for organizations seeking immediate transactional deployments.

- Pace of compressed transformations: Accenture’s “Method One” delivery methodology relies heavily on tech composability and rapid microservices to accelerate multiyear modernization journeys into mere months. Organizations with legacy technical debt or those unprepared for rapid change management may struggle to keep pace with the continuous real-time evaluation and stringent tollgate reviews required by Accenture’s approach.

Capgemini

Capgemini is a Challenger in this Magic Quadrant. Headquartered in France, it is a global leader in partnering with companies to transform and manage their businesses by harnessing the power of technology. The cloud ERP practice represents approximately 6% of the total company workforce.

The geographic distribution of Capgemini’s cloud ERP resources is split across regions in the following ranking: Asia/Pacific, where most resources are based in India, serving clients through its Global Delivery Center, then Western Europe, North America, Eastern Europe, Latin America, and the Middle East and Africa.

Capgemini’s portfolio is led by SAP, followed by Oracle, Microsoft, and Workday. Discovery and design, as well as application managed services (AMS), also represent significant portions of its revenue.

- Data-first transformation: Capgemini differentiates itself through its data-first approach, supported by the Syniti Knowledge Platform, which integrates data quality, migration, and governance as the foundation for transformation. The platform derisks complex ERP moves and enables business-ready data for a foundation that supports AI adoption, downstream analytics, ongoing change, reduced risk, and data reliability.

- AI-driven delivery and innovation: The vendor aggressively integrates AI into its “Enterprise Core” offering through its RAISE platform and over 50 GenAI accelerators. Capgemini utilizes agentic AI for tasks ranging from code modernization to automated support.

- Strategic partnerships and scale: Capgemini maintains deep, top-tier alliances; it is an SAP Pinnacle Award winner for business AI and a Microsoft partner dedicating a multimillion-dollar investment to growing its Dynamics footprint. Its large-scale global delivery network and industrial assets, such as the Digital Acceleration Navigator (DAN), allow it to execute massive, complex transformations for large enterprises.

- Geographic resource imbalance: While Capgemini has a strong presence in Western Europe and North America, its Cloud ERP headcount is heavily concentrated in Asia/Pacific. Clients in the Americas requiring extensive onshore or nearshore presence for cultural alignment or time zone collaboration should validate the specific delivery model proposed.

- Limited workday capabilities: Capgemini’s solutions coverage and execution capacity for Workday are limited, compared to its SAP and Oracle powerhouses. While it focuses on consultant expertise and specific industry tenants, its market footprint and depth of proprietary tooling are still being developed. With limited coverage, Capgemini may not be a viable primary partner for large-scale Workday transformations.

- Midmarket focus and alignment: While Capgemini is increasing its focus on midsize clients, its cloud ERP practice remains heavily skewed toward large, global enterprises, which currently make up the majority of its client base. Midmarket organizations should carefully evaluate whether Capgemini’s enterprise-centric delivery models and pricing align with their specific scale, needs, and budget constraints.

Cognizant

Cognizant is a Challenger in this Magic Quadrant. Headquartered in the U.S., it is a global system integrator focused on engineering modern businesses through its AI-first strategy.

Cognizant’s cloud ERP business is evenly balanced, with Oracle accounting for 45% and SAP for 40% of revenue, and SAP representing 48% of the vendor’s FTEs against Oracle’s 43%, reflecting a closely matched and well-rounded practice. It offers capabilities across the life cycle, utilizing frameworks like Oracle Cloud Map Advisory for discovery and design, and AppLens for application managed services.

Across all cloud ERP practices, Cognizant operates a rightshored global delivery model, with onshore certified resources typically representing 25%, complemented by scaled offshore and nearshore capabilities across its Oracle, SAP, Workday, and Microsoft practices.

- “AI Builder” strategy and IP: Cognizant has aggressively pivoted to an AI-first delivery model, deploying proprietary assets like Ora0 (for Oracle) and Brownfield Conversion Express (for SAP). The latter reduces S/4HANA migration timelines by 30% through GenAI-driven code remediation and automation. Cognizant leverages its Bluebolt grassroots innovation program to accelerate delivery and enhance “human-agent orchestration.”

- Oracle practice scale and depth: Cognizant maintains a top-tier Oracle practice with over 16,500 certifications, significantly outpacing its other ERP capabilities. It is a top 5 Global Strategic Service Partner for Oracle and has invested deeply in industry-specific solutions, such as the Cognizant Telco Solution and Healthcare in a Box to drive vertical-specific outcomes.

- Growth in midmarket segment: Addressing the needs of midsize enterprises, Cognizant utilizes preconfigured delivery models, such as the Rapid Implementation fixed-fee offering for Oracle, and GROW with SAP. These frameworks enable predictable timelines and transparent pricing.

- Proprietary offering complexity: Cognizant’s extensive array of proprietary AI platforms and branded service offerings can create navigation challenges for clients. Overlapping nomenclature and specialized solution sets may require guidance to ensure buyers select the most suitable tools without incurring architectural complexity.

- Outcome-based contract risks: As Cognizant shifts toward outcome-based commercial models, there is a risk of misaligned incentives if KPIs are not strictly instrumented from day one. Clients should ensure rigorous governance and clear reporting frameworks are established while partnering with Cognizant to support their transformation journey.

- Geographic and industry concentration: Cognizant needs to increase penetration in Southern Europe and the Asia/Pacific and Japan markets, as well as improve coverage in the oil and gas and public sector verticals. Clients in these regions or industries should carefully verify the availability of localized resources and industry-specific assets, as the current talent pool for major platforms like Oracle and SAP is heavily concentrated in India.

Delaware

Delaware is a Niche Player in this Magic Quadrant. Headquartered in Belgium, its cloud ERP services are focused on SAP and Microsoft transformations for midmarket to large enterprises. Its operations are geographically diversified but heavily anchored in Western Europe, and its clients are in the manufacturing, retail, utilities and professional services sectors.

The geographic distribution of Delaware’s cloud ERP resources is heavily weighted toward Western Europe and Asia/Pacific, with 57% in Western Europe, 21% in Asia/Pacific (excluding Japan), 10% in North America, 9% in Latin America, 2% in the Middle East and Africa, and 1% in Eastern Europe.

Delaware’s portfolio is composed of SAP at 69%, followed by Microsoft at 12%, with Oracle and Workday both at 0%. Discovery and design represents 8%, and AMS 11%.

- Deep industry-specific IP and accelerators: Delaware sets itself apart with mature, proprietary assets like DM4Mill and over 31 cross-industry accelerators. This strategy allows compressed project timelines, minimized customizations, and reduced delivery risks for complex verticals such as manufacturing, print and packaging, and utilities.

- Cross-environment integration: Delaware effectively capitalizes on its cross-environment expertise to compound value for clients. By developing proprietary connectors, such as linking Microsoft Copilot with SAP S/4HANA for natural language financial and procurement queries, it bridges the gap between core systems of record and advanced workplace productivity tools.

- Talent retention and Phase 0 discovery: Delaware maintains a low employee attrition rate of under 7%, fostering high continuity and deep expertise within its project teams, coupled with a rigorous Phase 0 discovery methodology that actively challenges clients to eliminate legacy processes.

- Limited platform breadth: Delaware’s Cloud ERP strategy is strictly confined to the SAP and Microsoft ecosystems. Organizations seeking a vendor-agnostic advisor or those requiring implementations for Oracle Fusion or Workday will find Delaware unsuitable, as it offers no implementation services for these specific platforms.

- Geographic and scale limitations: While Delaware is actively expanding into North America and other regions via targeted M&A, its delivery footprint and brand visibility remain heavily concentrated in Western Europe. Clients executing global rollouts across highly distributed geographies may find Delaware lacks the sheer scale of global system integrators.

- Selective capacity pressures: Due to rapid growth and a strategic avoidance of ultra-low-cost, pure offshore delivery models, Delaware has selective capacity pressures in high-demand niche skills, such as SAP S/4HANA Cloud Public Edition and AI-adjacent technologies. Clients should lock in talent early and establish strong governance to avoid potential resource constraints.

Deloitte

Deloitte is a Leader in this Magic Quadrant. Headquartered in the U.K., it is a global professional services organization that delivers end-to-end cloud ERP transformations through its Advise-Implement-Operate life cycle framework. Gartner estimates that Deloitte’s cloud ERP practice represents 20% to 25% of the total company workforce.

Gartner estimates that the geographic distribution of Deloitte’s cloud ERP resources is weighted toward offshore delivery. Cloud ERP resources are located in the following regions in rank order: Asia/Pacific (excluding Japan), North America, Western Europe, Latin America, Eastern Europe, Middle East and Africa, and Japan.

Deloitte can cover all featured cloud ERP technologies, with the revenue split in the following ranking: discovery and design, SAP, AMS, Oracle (Fusion Cloud ERP), Workday and Microsoft (Dynamics 365).

- AI-enabled delivery and innovation: Deloitte’s delivery strategy relies heavily on platform-enabled execution. It uses its proprietary Deloitte Ascend delivery platform and Zora AI agents to automate approximately one-third of its configuration, data migration, coding, and testing. Backed by a multimillion-dollar investment in shared core and technology-specific assets, Deloitte accelerates time to value while improving release readiness and sustaining continuous improvement post-go-live.

- Value-driven approach: Through its Vision to Value governance framework, Deloitte manages scope trade-offs against measurable business outcomes. To align incentives with client success, Deloitte champions flexible commercial structures; 30% of its contract revenue is tied to fixed-price models featuring revenue-at-risk or business-outcome-based milestones.

- Ecosystem synergy: Deloitte utilizes its IndustryAdvantage model to offer hundreds of preconfigured, sector-specific accelerators, including unique IPs for government and healthcare clients. Its execution is reinforced by serving as SAP’s No. 1 global revenue influencer, winning Workday’s 2025 Global Partner of the Year and Oracle’s 2025 Global AI Innovation Partner of the Year award.

- Independence restrictions: Due to its multidisciplinary expertise, including its global audit practice, Deloitte faces some independence restrictions that may limit the scope of cloud ERP services it can offer to existing attest/audit clients.

- Prerequisite for transformation: Deloitte’s cloud ERP services execution model depends on a “clean core” philosophy and a client’s willingness to adopt leading practices rather than heavily customizing their software. Some clients may not prefer Deloitte’s rigorous governance and transformation-heavy approach .

- Solution footprint: SAP and Oracle represent the largest shares of Deloitte’s Cloud ERP revenue, while Workday and Microsoft account for smaller portions of the portfolio. Clients evaluating Workday- or Microsoft-based programs should validate the scale and experience of the proposed team for their specific requirements.

DXC Technology

DXC Technology is a Challenger in this Magic Quadrant. Headquartered in the U.S., it is an enterprise technology and innovation partner that supports customers by modernizing their IT estates and driving digital transformation through cloud ERP and AI-driven solutions.

The geographic distribution of DXC Technology’s cloud ERP resources is heavily weighted toward offshore delivery (60%), with 62% in Asia/Pacific (excluding Japan), 13% in Western Europe, 9% in North America, 6% in Eastern Europe, 5% in Latin America, 5% in the Middle East and Africa, and 1% in Japan.

DXC Technology’s portfolio is led by SAP at 65%, followed by Oracle at 24%, Microsoft Dynamics at 9%, and Workday at 2%. Its top three market verticals are manufacturing and natural resources, government, and healthcare and life sciences.

- Agentic AI and service automation: DXC has successfully moved beyond theoretical AI by embedding tangible agentic AI into both implementation and AMS. Its Service Automation 2.0 framework utilizes proactive monitoring (DXC autoDetect) and self-healing runbooks (DXC autoResolve) to autonomously fix issues before users log tickets.

- Clean core and complex manufacturing modernization: DXC demonstrates strong execution in modernizing highly customized legacy environments, particularly manufacturing execution systems (MES). By strictly enforcing “clean core” principles, DXC uses platforms like SAP BTP and standard API connectors to move custom logic into side-by-side extensions.

- Public sector data sovereignty: DXC is highly capable of architecting cloud ERP solutions for strictly regulated industries. Its data management and control extensions, combined with bring-your-own-key encryption on localized sovereign clouds, guarantee that ERP data life cycles are handled in full alignment with EU public-sector digital-sovereignty expectations.

- Vision articulation and marketing execution: DXC still operates primarily as an engineering-focused company; clients seeking a highly consultative, digitally visionary partner to drive business model transformation may need to do further research into DXC’s capabilities.

- Limited native Workday scale: DXC’s Workday practice is remarkably small for a global system integrator. While DXC mitigates this by partnering with certified third parties for Workday Financial Management implementations and leveraging its broader HCM talent pool, clients seeking a single, globally scaled provider for massive Workday-led transformations may find DXC’s internal capacity lacking.

- Lagging business-outcome-based commercial models: Despite industry trends leaning toward shared-risk and business-outcome-based pricing, DXC’s adoption remains low. Only 5% of its 2025 cloud ERP deals utilized a business-outcome-based model. The vast majority of DXC’s engagements remain anchored to traditional IT performance SLAs; clients desiring true value-based pricing will have to heavily negotiate those structures.

EY

EY is a Challenger in this Magic Quadrant. Headquartered in the U.K., but operating globally across more than 150 countries, it is a global leader in partnering with companies to transform their businesses by shifting them from legacy systems of record to autonomous systems of action.

EY provides implementation and advisory services across the major cloud ERP platforms. EY has long standing and strategic alliances with SAP and Microsoft and serves as an independent external auditor to several large enterprise software providers, which precludes it from joint partnership agreements with those entities.

The geographic distribution of EY’s cloud ERP resources relies on a hub-and-spoke model heavily supported by its Global Delivery Services (GDS) network, utilizing strategic centers of excellence located in India, Poland, the Philippines, Mexico, and Spain.

Given that EY is the auditor of many of the largest technology vendors and providers, EY has restrictions that limit how they can publicly promote their work with the products of these vendors.

EY declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- Human-centric approach and change management: EY strongly differentiates itself by placing the “human side” of adoption at the core of its cloud ERP transformations, primarily delivered through its Transformation EQ (emotional intelligence) discipline.

- Pervasive AI investments and automation: Backed by a $1.4 billion investment in its EY.ai program, EY has embedded AI across its technology platforms, ecosystems and services. Built on the EY.ai Agentic Platform through a partnership with Microsoft and NVIDIA, EY uses AI agents to execute complex multistep workflows across core enterprise functions, including tax, risk, finance, audit, and supply chain.

- Outcome-based pricing and rapid delivery: EY is actively shifting away from traditional seat-based or time-and-materials (T&M) subscriptions toward outcome-based commercial models. By linking variable success fees to tangible metrics, EY directly aligns its financial incentives with client ROI.

- Customization limitations in supply chain: While EY excels in standardized “clean core” architectures, some clients have identified specific limitations when attempting deep customization for complex supply chain workflows.

- Scope volatility from resource mix: EY’s execution phases can occasionally rely on junior resources. Client feedback indicates that if initial project planning lacks rigorous discipline, this resource mix can lead to execution challenges and variance from scope during complex cloud ERP transitions.

- Premium pricing: While EY provides high-value multidisciplinary expertise, its services are often premium-priced. With its focus on a holistic, 360-degree value-based approach, many transformation projects expand in scope and size during implementations. Clients engaging with EY should ensure they have strong project governance and controls in place to avoid overruns.

Fujitsu

Fujitsu is a Niche Player in this Magic Quadrant. Headquartered in Japan, its cloud ERP strategy is shifting from traditional back-office optimization toward an emphasis on sustainability transformation, driven by its Fujitsu Uvance brand.

The geographic distribution of Fujitsu’s cloud ERP resources relies on a robust global delivery model. Its execution is heavily supported by Global Delivery Centers located in China, India, Poland, Portugal, and the Philippines.

Its portfolio features notable certifications, including status as Japan’s first premium supplier for RISE with SAP.

Fujitsu declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- Purpose-driven sustainability focus: Fujitsu links cloud ERP implementations directly to societal and environmental sustainability goals, rather than purely functional IT metrics. Its Uvance portfolio, which saw a 31% revenue growth in fiscal 2024, targets positive outcomes for enterprises.

- AI and data integration: The Fujitsu Kozuchi AI platform and Data Intelligence PaaS embed proprietary generative AI and quantum-inspired optimization (Digital Annealer) into enterprise workflows. This allows clients to automate complex decisions in areas like production planning and healthcare resource allocation.

- Deep manufacturing expertise: Fujitsu leverages over 40 years of manufacturing experience, using solutions like SAP PLM to digitally connect engineering chains with supply chains.

- Risks from shift to cloud advisory partner: Fujitsu is actively navigating a massive cultural and operational transition from a traditional hardware-heavy IT firm to an agile, software-led consulting partner. Clients seeking pure-play, cloud-native advisory services must evaluate whether Fujitsu’s evolving methodologies have fully matured beyond its legacy system construction roots.

- Talent reskilling dependencies: To support its new Uvance business model, Fujitsu is reskilling 28,000 employees in cloud and AI technologies, which creates a risk of employee turnover. Customers engaging with Fujitsu should ensure they explicitly contract for and lock in the vendor’s top-tier transformation resources.

- Niche market positioning: Outside of Japan, Fujitsu’s brand salience as an end-to-end ERP transformation orchestrator may lag behind other vendors.

HCLTech

HCLTech is a Challenger in this Magic Quadrant. Headquartered in India, it partners with enterprises by leveraging outcome-linked commercial models and embedding agentic AI workflows to automate their digital modernization.

HCLTech’s Cloud ERP delivery resources are geographically diversified, though heavily weighted toward Asia/Pacific and North America. The vendor has 53% of its resources in Asia/Pacific (excluding Japan), 30% in North America, 11% in Europe (which consolidates both Western and Eastern Europe resources), 3% in Latin America, 2% in the Middle East and Africa, and 1% in Japan.

HCLTech’s portfolio is led by SAP at 29%, followed by Oracle Fusion at 18%, Microsoft Dynamics at 14%, and Workday at 5%. AMS represents 22%, and discovery and design represents 12%.

- AI-native delivery and agentic workflows: HCLTech integrates agentic workflows throughout the ERP life cycle, using its AI Force platform for Oracle and SAP. This targeted approach automates finance, supply chain, and HR tasks, reducing build effort by up to 30% and accelerating data conversions by 60%, delivering measurable implementation efficiencies.

- Outcome-linked commercial models: HCLTech is shifting clients away from traditional, effort-based contracting toward value realization and shared risk. Currently, 13% of HCLTech’s cloud ERP revenue is tied directly to business-outcome-based models, and 18% utilizes fixed-price models with revenue at risk, ensuring vendor accountability is aligned with client KPIs.

- Deep industry-specific IP: HCLTech’s portfolio of microvertical solutions and accelerators reduces customization needs. Notable examples include the SAP iMRO solution for aerospace and defense, and the Power Manufacturing template for Microsoft Dynamics 365, which digitizes shop floor operations and asset maintenance.

- Limited Workday scale: HCLTech’s scale and market share in the Workday ecosystem are comparatively limited. Workday-based implementation accounts for only 5% of its cloud ERP revenue and utilizes under 3,000 FTEs, making it a smaller player for clients seeking purely Workday-led transformations.

- Dependence on installed base for growth: HCLTech relies heavily on its existing client relationships to drive its cloud ERP business expansion. In 2025, 69% of the vendor’s cloud ERP services revenue growth was generated from existing customers, with 31% coming from net-new logos, which may indicate challenges in capturing broader market share against competitors.

- Limited penetration in the SMB market: HCLTech’s client portfolio is mainly focused on very large organizations. Only 3% of its cloud ERP revenue comes from clients with fewer than 500 employees, and just 7% comes from organizations with 500 to 999 employees. Small and midsize businesses may struggle to negotiate competitive outcomes or find rightsized packaged offerings.

Huron

Huron is a Niche Player in this Magic Quadrant. Headquartered in the U.S., it is a global professional services firm and technology-enabled transformation partner with growing digital and managed services capabilities, particularly across the healthcare, higher education, energy, and commercial sectors.

The geographic distribution of Huron’s Cloud ERP resources is currently heavily weighted toward North America, with 75% in North America, complemented by 22% in Asia/Pacific (excluding Japan), and 2% in Western Europe. Huron has expanded its international footprint through strategic client engagements and regional expansion initiatives.

Huron’s portfolio is led by Oracle at 55%, followed by Workday at 35%, and expanding capabilities in Microsoft at 3%. Discovery and design represents 2% and AMS represents 5% across these supported platforms.

- Deep industry specialization: Huron delivers tailored ERP capabilities for highly regulated and complex industries. It has over 20 proprietary, industry-specific accelerators across the healthcare, higher education, utilities, financial services, and manufacturing verticals, with repeatable deployment across global clients and measurable reductions in implementation timelines and risk.

- AI-embedded delivery operations: Huron embeds AI directly into its standard delivery operations, backed by a recent $44 million investment in delivery innovation, including AI-enabled accelerators, automation frameworks, and embedded intelligence across the ERP implementation life cycle.

- Advisory-led “future of function” methodology: Huron anchors cloud implementations in business process redesign rather than technology selection. Its “future of function” methodology reframes ERP implementations into function-level transformation roadmaps, aligning system deployments to enterprise operating model transformation, organizational design, and data-driven decision-making capabilities.

- Platform ecosystem limitations: Huron does not position itself as a large-scale S/4HANA system integrator, supporting the SAP ecosystem only selectively through Concur implementations and advisory projects. Additionally, while the firm recently expanded into Microsoft Dynamics 365, this practice remains a smaller portion of its business — accounting for 3% of the ERP portfolio and approximately 50 specialists — compared to its more-established Oracle and Workday practices.

- Commercial pricing model mix: Although Huron is expanding its use of fixed-fee and milestone-based models, more than 50% of its 2025 cloud ERP revenue continues to be derived from T&M contracts. The firm intentionally avoids broad, fully outcome-based pricing tied to enterprise financial metrics, such as revenue uplift or cost savings, which may not align with clients seeking to shift significant financial risk to their service provider.

- Heavy North American concentration: Huron’s delivery and revenue footprints are heavily centered in North America, which serves as its primary innovation and delivery hub. While the vendor is scaling global hubs; 70% of its ERP workforce is located onshore, and its permanent footprint in regions like the Middle East or Japan remains limited or partner-led, compared to larger global system integrators.

IBM Consulting

IBM Consulting is a Leader in this Magic Quadrant. Headquartered in the U.S., it is a full-service technology and transformation company. It focuses on serving midsize-to-large enterprises and public-sector and government organizations with complex, multigeography operations. Its cloud ERP practice represents approximately 18% of the total company workforce.

The distribution of IBM’s cloud ERP resources is heavily weighted toward offshore delivery, with 60% offshore, 23% onshore on-site, 10% onshore remote, and 7% nearshore.

IBM’s portfolio is led by SAP at 61%, followed by Oracle at 23%, Workday at 2%, and Microsoft at 1%. AMS represents 13% of the portfolio.

- AI-driven execution and “Client Zero” credibility: IBM uses its own global organization as “Client Zero” to validate cloud ERP and AI capabilities before taking them to market. It embeds its IBM Consulting Advantage platform and agentic AI into its delivery framework, with the goal of 30% to 50% productivity gains and faster time to value for clients.

- Comprehensive industry accelerators: IBM has an expansive library of prebuilt, industry-specific assets designed to accelerate the discovery and design phases of transformation. Tools such as the Oracle Cloud Augmented Resilient Enterprise (CARE) platform and the AI-driven Business Maturity Index (BMI) Assessment standardize complex implementations across highly regulated verticals like government, manufacturing, and healthcare.

- Value-aligned commercial models: IBM provides flexibility in its commercial structures by offering options for hybrid and business-outcome-based pricing models. Particularly in its AMS operations, IBM can tie subscription-based fees directly to measurable operational improvements, automated ticket resolution, and telemetry-driven adoption KPIs.

- Global delivery model: IBM relies on a globalized delivery model, with an average of 70% of its work performed off-site or offshore. Prospective clients should carefully construct governance structures and contractually lock in key onshore roles during multiyear programs, to mitigate potential risks related to offshore resources.

- Portfolio navigation: While IBM has simplified its core offering portfolio, it maintains a vast array of branded platforms and specialized AI agents, such as IBM Consulting Advantage (ICA), Intelligent Delivery Suite (IDS), BMI, and CARE. The sheer number of industry-specific solutions may make it challenging for clients to navigate the portfolio and select the most appropriate tools without significant consultant guidance

- Not suited for small organizations: IBM’s delivery model is optimized for high-value, enterprise-scale transformation and is not a suitable fit for small organizations or engagements that are narrowly tactical in nature. Clients may find IBM’s global delivery scale and governance requirements to be disproportionate to their specific needs.

Infosys

Infosys is a Leader in this Magic Quadrant. Headquartered in India, its cloud ERP operations are broadly focused on complex, large-scale, AI-led business transformations for midsize to large enterprises across global markets. Its target industries heavily emphasize manufacturing, energy, retail, and communications. In 2025, Infosys generated approximately 27% of its total overall revenue from cloud ERP services.

The geographic distribution of Infosys’ cloud ERP resources is heavily weighted toward offshore delivery (69%), with 61% in Asia/Pacific (excluding Japan) and 17% in North America,.

Infosys’s portfolio is led by Oracle at 35%, followed by SAP at 27%, Microsoft at 3%, and Workday at 1%. Discovery and design represents 19% and AMS represents 15%.

- AI-native operations and agentic AI: Utilizing its Topaz Fabric and Enterprise AI Workbench, Infosys deploys over 80 prebuilt “true agents” that resolve conflicting data and automate complex processes like period end closing and incident remediation.

- Scale of certified talent: Infosys maintains a delivery engine that includes more than 19,000 SAP and 12,000 Oracle FTEs. This scale ensures the operational capacity to handle simultaneous, large-scale global rollouts and complex consolidations.

- Outcome-aligned commercial models: Infosys demonstrates a mature understanding of buyer financial constraints by championing value-driven commercial constructs. Approximately 40% of its cloud ERP revenue is generated through business outcome-based models and fixed-price models with revenue at risk.

- Limited suitability for small enterprises: Infosys’ highly structured delivery frameworks and transformation-heavy consulting approach are optimally designed for large enterprises. Small organizations seeking highly commoditized, out-of-the-box deployments may find it misaligned with their budget constraints.

- Delivery footprint mix: While Infosys’ resourcing model is weighted toward offshore locations, clients in highly regulated industries with strict data sovereignty, national cloud mandates, or a strong preference for localized, in-person collaboration must carefully define specific resourcing requirements to ensure compliance.

- Scale of the Workday practice: Infosys’ Workday practice accounts for just 1% of its portfolio. Customers looking to execute massive, globally scaled Workday transformations should verify that the vendor has sufficient dedicated capacity to meet aggressive timelines.

KPMG

KPMG is a Leader in this Magic Quadrant. Headquartered in the U.K., its cloud ERP services are broadly focused on enterprisewide, AI-first business transformations. The geographic distribution of KPMG’s cloud ERP resources is heavily weighted toward North American and offshore delivery, with 53% in North America, 23% in Asia/Pacific (excluding Japan), 21% in Western Europe, and 3% in Latin America. The cloud ERP practice represents approximately 20.2% of the total company workforce. Customers tend to be large global organizations primarily operating in regulated and complex industries, such as government, healthcare, and financial services.

KPMG’s portfolio is led by Oracle at 17%, followed by SAP at 13%, Microsoft at 13%, and Workday at 6%. Discovery and design represents 49% and AMS represents 2%. Customers using KPMG for their accounting, tax and audit purposes must evaluate any possible conflict of interest before contracting them for their cloud ERP transformation programs.

- AI-driven delivery and innovation: KPMG deploys over 50 purpose-built delivery agents that automate complex implementation tasks, such as testing, data conversion, and code decomposition. Its proprietary Velocity platform embeds agentic AI and preconfigured Target Operating Models (TOMs) directly into the delivery life cycle.

- Continuous modernization: KPMG differentiates its post-go-live support through its KPMG Velocity platform. This AI-first continuous service utilizes AI-driven process mining to monitor business user performance and ensures the ERP platform continuously evolves in lockstep with the client’s business goals.

- Deep industry verticalization: KPMG possesses an extensive, highly specialized library of proprietary industry accelerators, spanning 24 industry sectors, including over 2,700 for healthcare on Oracle and over 3,200 for government on SAP. This allows KPMG to tailor cloud ERP implementations to customers’ unique regulatory, compliance, and operational demands across all major platforms.

- Market focus: KPMG explicitly targets large, complex enterprise transformations. Small to midsize businesses prioritizing highly tactical lift-and-shift projects will need to take a closer look at KPMG’s premium strategic offerings.

- Independence restrictions: Due to its heritage as a global audit and tax practice, KPMG faces strict independence restrictions that structurally limit the scope of cloud ERP services it can offer to its existing attest and audit clients.

- Limited AMS footprint: With AMS representing only 2% of its total cloud ERP revenue, KPMG’s practice leans heavily toward upfront design and implementation. Customers looking for a provider with a massively established traditional IT maintenance and support footprint may find KPMG’s offerings less dominant in this area.

LTM

LTM is a Niche Player in this Magic Quadrant. Headquartered in India, it is a global technology consulting and digital solutions company. Its cloud ERP services practice is focused on a “Timeless Enterprise” strategy, emphasizing composable architectures and agentic AI. LTM serves a globally diverse client base in large and midsize enterprises within the manufacturing, natural resources, banking, and retail sectors.

The geographic distribution of LTM’s cloud ERP resources is heavily weighted toward offshore delivery (63%), with 73.4% in Asia/Pacific (excluding Japan), 14.5% in North America, 6.4% in Western Europe, 2.9% in the Middle East and Africa, 1.4% in Latin America, 0.9% in Eastern Europe, and 0.5% in Japan.

LTM’s portfolio is led by SAP at 31.6%, followed by Oracle at 26.6%, Microsoft Dynamics at 4.8%, and Workday at 1.9%. AMS represents 30.7%, and discovery and design represents 4.4%.

- AI-led innovation and platforms: LTM leverages its proprietary BlueVerse ecosystem to integrate GenAI and agentic AI across the ERP life cycle, empowering clients to accelerate time to value and scale AI adoption responsibly. To achieve these outcomes, LTM deploys a suite of assets. LTM Enclose streamlines core transformation with a simplified, “fit-to-standard” approach, delivering faster results and supporting more than country localizations. Its RELY.AI framework mitigates implementation risks by expediting resource-intensive testing and assurance cycles. The Reimagination Studio Platform provides executives with a “See-Believe-Accept” ROI analysis tool and access to over 300 prebuilt process maps, enabling rapid validation of business cases without starting from scratch.

- Deep industry expertise in manufacturing: As a co-innovation partner with SAP, LTM offers industry-specific accelerators, particularly for complex manufacturing and engineer-to-order, and complements them with advanced robotics, digital logistics, and specialized IP for oil and gas and energy.

- Flexible and outcome-based commercial models: LTM uses four innovative, outcome-based commercial models, where its approach aligns fees to measurable business results, lowers upfront risk through usage-based and as-a-service models, accelerates value realization, and enables shared innovation through co-investment and IP creation, going well beyond traditional fixed-price contracting.

- Imbalanced technology scale: LTM’s Workday practice is comparatively small, accompanied by partnerships with certified niche and boutique players. Prospective clients seeking large-scale, global transformations may find LTM lacks the sheer delivery volume of its larger peers in its early-stage ERP practices.

- Geographic staffing imbalance: While LTM maintains a robust global delivery model, its resources are heavily concentrated in the Asia/Pacific region, which accounts for over 80% of its SAP and Oracle Fusion FTEs. Regions such as Eastern Europe and Japan have significantly smaller footprints. Clients need to discuss with LTM when requiring deep local presence in specific markets.

- Emerging business consultancy services: LTM is currently establishing a dedicated transformation advisory and consulting services, which is a relatively new addition to its technical delivery model. Clients seeking a provider with a mature, business-led advisory legacy should note that these capabilities are still in an early scaling phase.

NTT DATA

NTT DATA is a Challenger in this Magic Quadrant. Headquartered in Japan, it is a global innovator operating in over 70 countries. Gartner estimates that the vendor’s cloud ERP practice represents approximately 12% of its total workforce.

Its cloud ERP client base is geographically diversified. For example, approximately 45% of its clients are in Western Europe, 14% are in Japan, and 11% are in North America.

Their ERP vendor’s coverage is heavily weighted toward SAP (approximately 90%), followed by Oracle (7%), Microsoft (3%), and Workday (<1%). NTT DATA’s clients tend to be international midsize and large enterprises, particularly in the manufacturing, automotive, and life sciences sectors. NTT DATA continues to invest in its agentic AI strategy, industry-specific solutions, and expanding its “360-degree partner” model with hyperscalers.

- SAP and data migration expertise: NTT DATA demonstrates massive scale in the SAP ecosystem, supported by its acquisition of Natuvion. This combination allows for complex bluefield migrations and “carve-outs,” enabling the vendor to offer aggressive commercial models like the Zero Cost Move program for S/4HANA Cloud.

- Vertical industry focus: The vendor leverages deep roots in manufacturing and automotive to deliver specialized solutions such as the Unified Namespace for IT/OT convergence. Clients in regulated industries like life sciences benefit from prevalidated packages that reduce compliance risk and accelerate time to value.

- Agentic AI strategy: NTT DATA has pivoted heavily toward agentic AI, deploying over 50 autonomous agents and its open aXet platform to automate delivery tasks. This AI-first approach aims to reduce project timelines and operational costs by automating code generation, testing, and document intelligence.

- Platform capability imbalance: NTT DATA’s organic resources for Oracle and Microsoft are smaller than for SAP, and its Workday practice relies heavily on partners. Clients seeking large-scale transformations on non-SAP platforms should verify local resource availability and depth of expertise compared to the SAP practice.

- Resource allocation and talent acquisition: Customers undertaking complex cloud ERP transformations should secure commitments for named, experienced resources upfront and ensure staffing plans and capacity models are explicitly detailed in the statement of work, to mitigate potential resource or skills gaps.

- Integration of acquisitions: NTT DATA has expanded its capabilities through acquisitions. With the rapid inorganic growth, clients with complex cloud ERP programs should pay attention to how service delivery, culture and tooling are aligned, as these capabilities are integrated into the global operating model.

PwC

PwC is a Leader in this Magic Quadrant. A global network of firms headquartered in the U.K. and U.S., the vendor allocates 10% of its workforce to the cloud ERP market, which Gartner estimates generates 19% of PwC’s revenue. Its top targeted enterprise market verticals include healthcare and life sciences, as well as manufacturing and natural resources, and banking and investment services.

The geographic distribution of PwC’s cloud ERP resources is globally balanced, with approximately 36% in Asia/Pacific (excluding Japan), 32% in North America, 14% in Western Europe, 5% in Eastern Europe, 5% in Latin America, 4% in the Middle East and Africa, and 3% in Japan.

- Outcome-led agentic AI: PwC has moved agentic AI out of the pilot phase and into live production environments using its Agent Powered Performance engine. By deploying “Sense, Think, Act” AI agents, PwC helps clients establish a hybrid workforce where humans and agents co-orchestrate workflows across the ERP and boundary systems to achieve targeted KPIs.

- Industry model systems: PwC heavily leverages its preconfigured, microvertical ERP model systems. It maintains a massive library of these blueprints, including 21 for SAP, 18 for Oracle, seven for Microsoft, and five for Workday, allowing the usage of a “design by exception” approach.

- Continuous modernization: PwC addresses the market shift away from static post-go-live support by offering Application Evolution Services (AES). This “run-optimize-innovate” framework ensures that clients continuously adopt new features, deploy AI enhancements, and realize value long after the initial implementation is complete.

- Complexity for rapid upgrade or lift and shift: PwC’s vision of “complex global transformations,” “ecosystem orchestration,” and “model systems” may be overengineered for customers that need simple, rapid deployments without extensive transformation services.

- Structured, fit-to-standard principles: Because PwC’s delivery scale and speed rely heavily on its proprietary model systems, clients may face friction if they demand heavy customizations that erode the clean core. Organizations that are unable to adopt standard processes should assess their data readiness with PwC during the buying process.

- Limited U.S. public sector focus: PwC’s capabilities are relatively limited in the public sector. U.S. state and local government, as well as higher education, are lower strategic priorities compared to its core commercial microverticals.

TCS

Tata Consultancy Services (TCS) is a Leader in this Magic Quadrant. Headquartered in India, it is one of the largest IT services companies. The cloud ERP practice represents approximately 13.8% of the total company workforce.

The geographic distribution of TCS’ cloud ERP resources is heavily weighted toward offshore delivery, with 49% in Asia/Pacific (excluding Japan), 26% in North America, 17% in Western Europe, 3% in the Middle East and Africa, 2% in Latin America, 2% in Eastern Europe, and 1% in Japan.

It typically serves global enterprises across complex, multigeography programs, specializing in verticals like manufacturing, retail, life sciences, and financial services.

- AI-first delivery and innovation: TCS is transitioning its delivery model from traditional automation to an “agentic workforce.” By leveraging proprietary IP like TCS WisdomNext and TCS Crystallus, with an estimated 86% of its cloud ERP associates now AI-enabled, the TCS Human + AI Autonomy model embeds AI and GenAI deeply into ERP landscapes.

- Next-gen AMS: TCS’ Application Management Services has shifted to “Autonomous Global Business Services.” By embedding agentic AI, GenAI assistants, and proprietary tools like Digitate ignio, TCS enables self-healing operations, proactive anomaly detection, and automated ticket resolution.

- AI-enhanced organizational change management (OCM): TCS employs a strong, consulting-led approach via its TCS Enterprise Navigator framework. It embeds GenAI directly into its change management stack, using AI to accelerate stakeholder impact analysis, generate persona-based training content, and deliver just-in-time learning and targeted communications.

- Optimized for large-scale environments: TCS’ deep methodology and extensive IP library (featuring over 8,000 assets and 650+ AI apps) are purposefully built for massive scale. Consequently, small to midsize organizations may find it difficult to negotiate cost-effective, rightsized engagements.

- Uneven platform coverage: TCS’ dedicated footprint for Workday and Microsoft Dynamics 365 is comparatively small when compared to those for SAP and Oracle. Clients seeking highly specialized, large-scale transformations strictly on Microsoft or Workday may require additional evaluation to ensure the right depth and scalability for their specific needs.

- Offshore-led delivery mix: With approximately 49% of its dedicated resources located in the Asia/Pacific region (excluding Japan), clients in North America or Western Europe that require a highly localized, time-zone-aligned, high-touch, on-site presence will need to carefully negotiate their contract’s resource mix to ensure adequate local staffing.

Tech Mahindra

Tech Mahindra is a Niche Player in this Magic Quadrant. Its cloud ERP services are broadly focused on phased, fit-to-standard modernizations for large and midmarket enterprises. Headquartered in India, its operations are geographically diversified with a strong footprint in Asia/Pacific, North America, and EMEA, and its clients tend to be concentrated in the manufacturing, retail, transportation, and telecommunications sectors.

The geographic distribution of Tech Mahindra’s cloud ERP resources is heavily weighted toward offshore delivery, with approximately 61% of FTEs in Asia/Pacific (excluding Japan) and 24% in North America.

The vendor’s portfolio is led by SAP at 26%, followed by Oracle at 25%, Microsoft at 2%, and Workday at 0%, with AMS representing 45%, and discovery and design representing 2%.

- AI-augmented delivery and operations: Tech Mahindra integrates GenAI and agentic AI into its delivery life cycle through its proprietary TechM Orion platform. This capability automates complex workflows, such as blueprinting, testing, data migration mapping, and L1/L1.5 support ticket resolution.

- Industry-specific accelerators: Packaged assets, such as AutoSHIFT for automotive manufacturing, Telecom xPress for communications, and PharmaChain for life sciences, enable clients to achieve faster fit-to-standard cloud deployments.

- Flexible, value-driven commercial models: Tech Mahindra actively utilizes progressive contracting structures, with over 25% of its cloud ERP revenue generated through business-outcome-based models and fixed-price models with revenue at risk. This approach aligns its commercial success directly with the client’s strategic objectives.

- Evolving Workday capabilities: Tech Mahindra is pursuing formal implementation partner status for Workday and currently, it is still building scale. Customers seeking a multivendor best-of-breed strategy that pairs a core financial cloud ERP with Workday Human Capital Management will need to look to alternative integrators to fulfill those architectural requirements.

- Heavy reliance on existing client base: With 78% of its cloud ERP revenue growth generated from its existing customer pool, the vendor demonstrates lower momentum in acquiring net-new logos. This heavy account-mining focus may suggest challenges within its sales execution engine when competing for new enterprise market share.

- Aversion to highly customized ERP environments: Tech Mahindra’s delivery methodologies prioritize “fit-to-standard” cloud deployments. Clients with highly specialized, unique business models that absolutely require heavy ERP customization will need to assess vendor capabilities beyond standard SaaS processes.

Wipro

Wipro is a Challenger in this Magic Quadrant. Headquartered in India, Wipro’s cloud ERP practice revenue accounts for roughly 25% of its total enterprise revenue.

Wipro demonstrates deep market penetration and tailored accelerators for the manufacturing and natural resources, power and utilities, retail, and banking, financial services and insurance verticals.

The geographic distribution of Wipro’s Cloud ERP resources is heavily weighted toward offshore delivery (70% offshore), with 60% in Asia/Pacific (excluding Japan), 17% in North America, 12% in Western Europe, 4% in Latin America, 4% in the Middle East and Africa, 2% in Eastern Europe, and 1% in Japan.

Wipro’s portfolio is led by SAP at 33%, followed by Oracle at 18%, Microsoft at 5%, and Workday at 1%. Discovery and design represents 13% and AMS represents 30%.

- AI-centric innovation: Wipro has invested heavily in Wipro Intelligence, deploying proprietary platforms like Agentic OS and WINGS (for autonomous operations) to drive measurable automation, predictive observability, and productivity gains across the ERP life cycle.

- Consulting-led transformation: Utilizing its “Vision to Value” life cycle, Wipro elevates engagements from technical migrations to business transformations. By leveraging its eSymphony and Digital Navigator Advisory (DNA) frameworks, Wipro excels at early-stage discovery, process mining, and alignment of technology directly with CxO business priorities.

- Outcome-based commercial models: Aligning with evolving buyer behavior, Wipro offers flexible, outcome-based pricing structures. The firm links contract payments to measurable business improvements, such as cost reduction, incident reduction, and productivity gains, sharing accountability and risk with its clients.

- Limited Workday capabilities: Wipro’s solutions coverage and execution capacity for Workday are limited, compared to its SAP and Oracle powerhouses. With limited coverage, Wipro may not be a viable primary partner for large-scale Workday transformations.

- Regional delivery disparities: Wipro’s Centers of Excellence (COEs) and resource pools are heavily skewed toward Asia/Pacific and North America. Clients requiring heavy, localized nearshore delivery in regions like Latin America or Eastern Europe may face resource constraints and a heavier reliance on remote delivery.

- Strategic advisory gaps: Although Wipro is highly effective in technical execution and system support, its depth in high-level transformational consulting is considered limited compared to leading peers, despite strategic investments in specialized firms like Capco and Rizing. Clients seeking exhaustive strategic guidance or complex, human-centric change leadership may find Wipro’s advisory portfolio modest.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

The following vendors were added to this Magic Quadrant:

- Delaware

- EY

Inclusion and Exclusion Criteria

The criteria for inclusion of service providers in this Magic Quadrant are based on a combination of quantitative and qualitative measures.

Quantitative Criteria:

Service vendors included in this Magic Quadrant must satisfy ALL four of the following quantitative criteria:

- Is able to provide cloud ERP services for at least two relevant ERP technology products for the following software vendors: Microsoft, Oracle, SAP, and Workday.

- Delivers cloud ERP services to current active clients in a minimum of two of five geographies (North America, EMEA, Asia/Pacific, Japan, and Latin America), not exceeding 85% of the vendor’s headquartered region.

- Is able to provide AMS for cloud ERP services for at least two relevant ERP technology products for the following software vendors: Microsoft, Oracle, SAP, and Workday.

- Has a minimum of $500 million annual worldwide revenue (USD) in total implementation and AMS (across all cloud ERP software products covered) during the period of September 2024 through September 2025 for cloud ERP services.

Qualitative Criteria:

- Overall market interest in and visibility of the service vendor, as determined by serious consideration for selection from enterprise clients and Gartner analysis of internal and external search patterns.

- Gartner analysts’ interactions with enterprise buyers, which reveal interest in specific cloud ERP services vendors.

- Demonstrated capability to consistently invest in tools, automation, methodology, frameworks, and processes, as well as to invest in resource development to deliver services in this market.

Evaluation Criteria

Ability to Execute

Gartner analysts evaluate providers on the quality and efficacy of the processes, systems, methods, or procedures that enable IT provider performance to be competitive, efficient and effective, and to positively impact revenue, retention, and reputation within Gartner’s view of the market.

Product/Service: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include performance on critical capabilities, methodologies and processes, and tools used to simplify and speed up implementations and evolution.

Overall Viability: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include year-over-year growth, market-specific revenue growth and retention, and strategic alignment of these services within the overall organization.

Sales Execution/Pricing: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include pricing models and contract flexibility, analyst perception of value provided, and focus on business outcomes of contracts and client success.

Market Responsiveness and Track Record: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include mechanisms for monitoring and responding to customer needs, examples of delivery against business outcomes, and analyst perception of roadmap promises being met.

Marketing Execution: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include brand/name recognition and/or customers’ familiarity with the vendor, tailoring of the vendor’s marketing message by industry/enterprise/geography, and leadership and vision demonstrated in publicity for the vendor.

Customer Experience: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include overall satisfaction with the provider’s capabilities and delivery, customer and employee retention, and reference feedback.

Operations: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include global and regional delivery capabilities, effective resource management that provides high-quality skills when needed, ethics and transparency mandates and standards, and continuity of staff/attrition/certification rates.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | Medium |

Marketing Execution | Low |

Customer Experience | High |

Operations | High |

Source: Gartner (May 2026)

Completeness of Vision

Gartner analysts evaluate providers on their ability to convincingly articulate logical statements. This includes current and future market direction, innovation, customer needs, and competitive forces and how well they map to Gartner’s view of the market.

Market Understanding: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include vision and strategic focus, competitive differentiators, IP investments, and knowledge of Cloud ERP trends.

Marketing Strategy: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include go-to-market approach, market visibility, and reference responses.

Sales Strategy: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include customer acquisition strategy effectiveness, incentive plans for existing clients, and reference response information.

Offering (Product) Strategy: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include product portfolio breadth and depth, investment levels in critical capabilities, new delivery models, and proprietary IP that delivers value in this market.

Business Model: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include significance and alignment of the Magic Quadrant market to overall business, establishment and support of long-term customer relationships, sustainability, and willingness to implement different commercial models.

Vertical/Industry Strategy: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include clear and consistent vertical focus, vertical/industry-specific investment, and industry knowledge.

Innovation: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include proprietary innovation platforms, commitment to innovation, use of automation, and innovation use cases.

Geographic Strategy: In addition to the criteria outlined in the Evaluation Criteria Definitions section, the subcriteria for this Magic Quadrant include clear and consistent region focus, region-specific partnerships/ecosystem, widespread availability of in-country resources for functional work, and proprietary IP that delivers value in this market.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Low |

Sales Strategy | Low |

Offering (Product) Strategy | High |

Business Model | Medium |

Vertical/Industry Strategy | High |

Innovation | High |

Geographic Strategy | Medium |

Source: Gartner (May 2026)

Quadrant Descriptions

Leaders

Leaders are performing well today, gaining traction and mind share in the market. They have a clear vision of market direction and are actively building competencies to sustain their leadership position in the market.

Challengers

Challengers execute well today for the portfolio of work selected, but they have a less-well-defined view of the market’s direction than Leaders do. Consequently, they may be tomorrow’s Leaders, or they may not be aggressive and proactive enough in preparing for the future.

Visionaries

Visionaries articulate important market trends and directions. However, they may not be in a position to fully deliver and consistently execute on that vision. They may need to improve their service delivery.

Niche Players

Niche Players focus on a particular segment of the market, such as a particular industry, size of client, functional area (for example, human capital management or supply chain) or geography. Their Ability to Execute is limited to those areas of focus. Their ability to innovate may be affected by their narrow focus. Many of the providers in this segment received positive client feedback, and many can be considered to be leading players within their niche market focus.

Context

This Magic Quadrant addresses the cloud ERP services capabilities of providers, for both service-centric and product-centric enterprises, that meet Gartner’s criteria for inclusion.

This Magic Quadrant evaluates 19 providers. It is a point-in-time analysis, with the status of all provider profiles reflected as of March 2026. Quantitative data collected was for a 12-month period ending September 2025. As part of the research, the analyst team generated more than 1,000 data points that collectively determined the placement of the dots on the Magic Quadrant.

In this evaluation, all vendors were assessed lower on Completeness of Vision than in prior cycles. This reflects a market shift rather than diminished capability. Previously differentiating innovations, such as AI-driven predictive analytics, intelligent automation, and outcome-based engagement models, are now broadly adopted and expected across the industry. On the other hand, reimagining enterprise business workflows, eliminating tasks and making them autonomous (less human) is considered more visionary.

Additionally, greater weight has been placed on Geographic Strategy, which was elevated from medium to high. This change underscores the increasing importance of geopolitical risk, regulatory fragmentation, and national sovereignty requirements. Vendors are increasingly differentiated by their ability to operate effectively across jurisdictions, manage data residency and sovereign cloud mandates, and align delivery models with regional political and regulatory realities. As a result, geographic and sovereign alignment has become a critical indicator of long-term vision and resilience.

When considering cloud ERP services, clients are advised not to simply select service providers in the Leaders quadrant. A provider may appear in a particular quadrant based on Gartner’s extensive analysis across the full-service life cycle in many industries and other criteria. However, for any given deal, a client company’s selection criteria will be narrower and more specific. Consequently, providers in the Challengers, Visionaries or Niche Players quadrants may prove to be more appropriate for the engagement. A more detailed analysis of the service providers’ capabilities, with scoring based on use cases, is available in Critical Capabilities for Cloud ERP Services.

Additionally, because the inclusion criteria in the Magic Quadrant result in the analysis of a subset of providers in the cloud ERP services market, clients should not disqualify any potential competitors simply because they do not appear in this research. Other IT service providers not evaluated in this Magic Quadrant may present better alternatives for your business requirements. Consider using an analysis to ensure you have an optimum basis and evaluation criteria for narrowing down the most suitable providers. A Gartner analyst can help with a shortlist of the most suitable candidates based on client requirements.

Market Overview

This Magic Quadrant is focused on transformation and targets both service-centric and product-centric enterprises.

Gartner estimates that the application services market overall will be approximately $428 billion in 2025, of which approximately $306 billion will be devoted to implementing and supporting software products. The remaining $122 billion covers custom application software development. The $306 billion covers services on all packaged products (including noncloud and non-ERP), and we estimate that the total services devoted to the specific cloud ERP market will be around $80 billion. Across the board, cloud ERP services represent approximately 13% of the total enterprise revenue declared by the evaluated system integrators.

This Magic Quadrant evaluates 19 service providers, reflecting the recent additions of Delaware and EY to the market analysis. The market relies heavily on providers exhibiting several common features: outcome-based engagement models tied to defined business benefits, scalable modern support models, capabilities to embed AI/ML within cloud ERP platforms to enable predictive analytics, and intelligent automation to enhance operational efficiency.

Most of the featured providers focus on delivering cloud ERP services using highly globalized, offshore-centric delivery models. Providers such as Capgemini, Deloitte, DXC, HCLTech, IBM, Infosys, LTM, TCS, Tech Mahindra, and Wipro report that 59% to 73% of their cloud ERP resources are located in the Asia/Pacific region (excluding Japan) or other offshore centers. Conversely, firms like Huron (75% in North America) and KPMG (53% in North America) maintain a significantly heavier onshore presence. To accelerate delivery and continuous operations, providers are heavily investing in AI and automation. Integrators like Accenture, EY, and IBM are deploying proprietary agentic AI platforms, GenAI accelerators, and multiagent workflows, supported by individual corporate AI investments ranging from $1 billion to $3 billion.

The cloud ERP services market is actively shifting from traditional time-and-materials (T&M) or effort-based contracting toward value realization and shared risk. Providers such as Deloitte, HCLTech, Infosys, and Tech Mahindra report that up to 24% to 35% of their cloud ERP revenue is now tied directly to business-outcome-based models or fixed-price contracts with revenue at risk. Conversely, a few providers like Huron still derive the majority (54%) of their cloud ERP revenue from traditional T&M contracts.

The primary technologies driving these transformational engagements are centered around four core software ecosystems:

- Microsoft Dynamics 365

- Oracle Fusion Cloud ERP

- SAP Cloud ERP

- Workday

This Magic Quadrant assesses the relative positioning of the providers in delivering cloud ERP services. In the companion Critical Capabilities research, specific use cases have been identified so that the performance in each area can be judged.

Evaluation in this Magic Quadrant is informed by:

- Gartner client interactions: Gartner inquiries between user organization clients and sourcing, procurement and vendor management analysts on service providers relating to cloud ERP services over 12 months (January 2025 through December 2025).

- Primary research: A detailed collection of data points via the Gartner vendor portal from the 19 participating service providers.

- Primary research: A 90-minute vendor briefing from each participating service provider addressing capability proof points of each evaluation criterion in the Magic Quadrant.

- Primary research: Feedback from over 200 reference responses across the 19 participants in this Magic Quadrant.

- Secondary research: Press releases and publicly available information, including company websites and financial reports.

- Other Gartner analysts: Peer review by Gartner analysts. Their views and comments were considered. In addition, this research was reviewed at internal research community sessions.

Note 1: Market Practice Sizing

Size definitions for this market are based on the number of FTEs used to provide cloud ERP services:

- Small: 2,000 or fewer

- Medium: 2,001 to 10,000

- Large: 10,001 to 20,000

- Very Large: 20,001 to 60,000

- Extra-Large: More than 60,000

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.