Hype Cycle for Digital Commerce, 2026

2 June 2026 - ID G00846349 - 105 min read

By Sandy Shen

AI and AI agents are transforming digital commerce, impacting customer behavior, technology capabilities and architecture. This Hype Cycle helps digital commerce leaders tune into the latest technology trends to future-proof their investment decisions.

Analysis

What You Need to Know

As AI and agentic commerce take center stage in the evolution of commerce technologies and customers’ buying behavior, they are no longer optional but essential to organizations’ growth and competitiveness. The 2026 Gartner CEO and Senior Business Executive Survey shows that growth remains the top strategic business priority for CEOs, who expect a “high” to “medium” degree of change in their organization’s capabilities due to AI.1

This year, many technologies have moved past the trigger stage and into later stages of the Hype Cycle. This indicates a rapid pace of change in the AI era where new technologies keep emerging but can quickly mature or become obsolete. This makes it ever more important for technology leaders to be well-informed of the changing market trends and directions. This Hype Cycle features more AI-powered commerce technologies than any previous year, and will help digital commerce leaders make informed technology decisions related to AI and commerce.

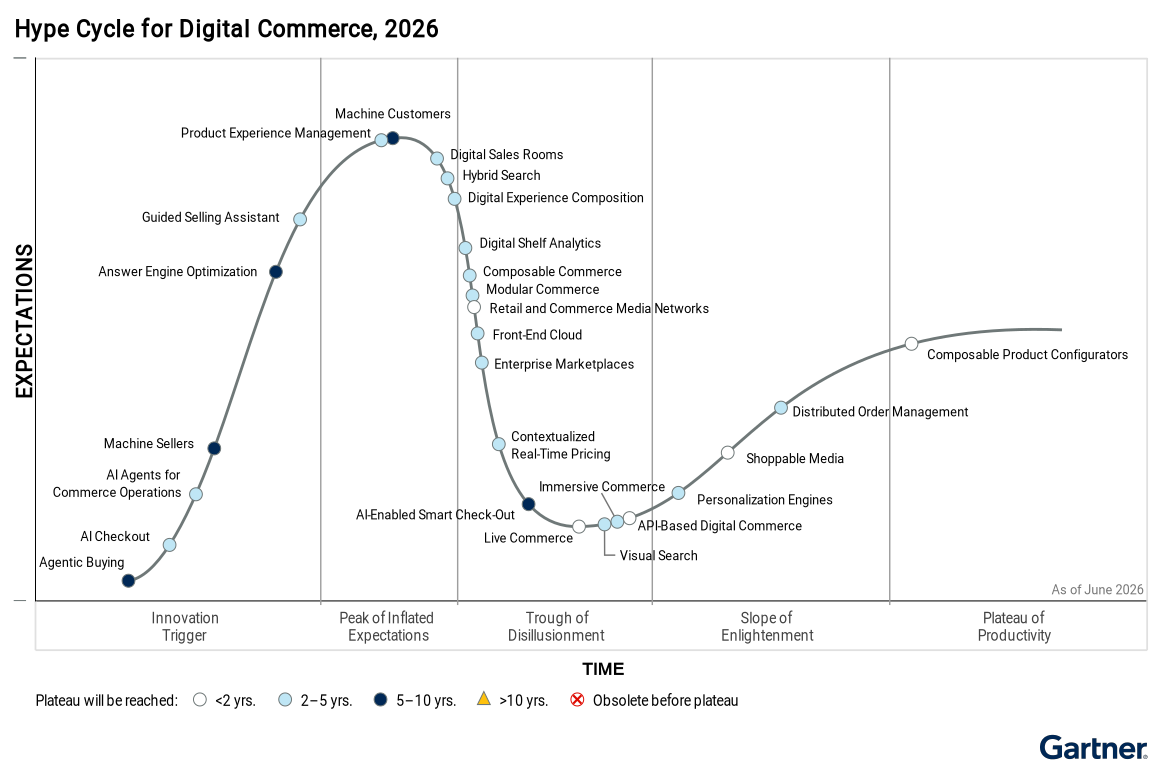

The Hype Cycle

As organizations focus on growth, agentic commerce is a key opportunity to unlock new revenue. Three new entrants related to agentic commerce are featured on this year’s Hype Cycle:

- AI checkout enables customers to buy directly on AI platforms (e.g., ChatGPT, Google Gemini and Perplexity) without going to the merchant’s website.

- Agentic buying sees AI agents act as customers that make end-to-end transactions with little or no human involvement. It is a future state of agentic commerce.

- Answer engine optimization (AEO) helps organizations improve product visibility on AI platforms, increasing referrals to commerce sites.

Other technologies have advanced significantly on the Hype Cycle due to an increase in their maturity, or a lack of market interest:

- Composable product configurators moved onto the Plateau of Productivity due to the maturing of visual configurators and virtual photography, and the wide availability of the product.

- Immersive commerce moved into the Trough of Disillusionment because, though the benefits are well understood, the value is limited to products requiring visual or spatial support.

- Product experience management moved to the Peak of Inflated Expectations, with vendors extending solutions to cover more components in the framework, while organizations still struggle to measure the ROI.

- Digital experience composition is descending into the Trough of Disillusionment due to relatively low awareness among developers and front-end deliveries remaining code-heavy.

- Hybrid search moved to the late stage of the Peak of Inflated Expectations due to it becoming a common capability for leading search and product discovery solutions despite the technology being relatively new.

- Visual search moved into the Trough of Disillusionment because, though the technology has matured quickly with better accuracy, organizations have yet to integrate it into multimodal use cases to see more value.

The Priority Matrix

Agentic buying will have transformational impacts on how customers buy and how organizations sell in five to 10 years. AI agents will act as customers, make purchase decisions and transact with little or no human involvement. When technology obstacles are overcome, AI agents will bypass the storefront and connect directly to commerce systems using APIs and protocols to transact. Organizations need to prepare to serve this type of new customer to stay relevant, or miss the revenue opportunities and lose customer relationships.

AEO will have transformational impacts on agentic commerce in five to 10 years. This not only impacts product visibility in AI checkouts but also referrals from “AI answers” to commerce sites. Organizations need to develop content best practices and use visibility tools to ensure a good presence on AI platforms, to offset the decline in referrals from traditional search engines.

AI agents for commerce operations are expected to have a transformational impact in the next two to five years, due to its quickly becoming a common capability in commerce solutions. Typical use cases include merchandising configurations, setup of rules and campaigns, event-based actions, and insight analytics. The primary benefit is productivity enhancement.

While modular commerce and composable commerce have transformational impacts, the complexity and costs associated with implementing these technologies are now better understood by the market. Organizations are taking a more pragmatic approach by balancing agility and flexibility with total cost of ownership (TCO), and selectively using extensions when needed.

Priority Matrix for Digital Commerce, 2026

| Benefit | Years to Mainstream Adoption | |||

|---|---|---|---|---|

| Less Than 2 Years | 2 to 5 Years | 5 to 10 Years | More Than 10 Years | |

Transformational | ||||

High | ||||

Moderate | ||||

Low | ||||

Source: Gartner (July 2026)

Off the Hype Cycle

Technologies that have been dropped from the Hype Cycle include:

- Customer data platform supports a wide range of use cases beyond commerce and is not a commerce-specific technology anymore.

- Customer journey maps support various purposes and are not a commerce-specific technology anymore.

- Payment as a packaged service has entered the mainstream and is now off the Hype Cycle.

- Retail media supply-side technologies serve retailers instead of brand organizations, which are the focus of retail media on this Hype Cycle.

On the Rise

AI Checkout

Analysis By: Sandy Shen

Benefit Rating: Moderate

Market Penetration: Less than 1% of target audience

Maturity: Emerging

Definition:

AI checkout is a form of agentic commerce where AI platforms recommend products relevant to a user’s query, based on factors such as product data, shipping and quality signals. Buyers can select products and complete checkout on the platform using either the platform’s native checkout experience or an embedded merchant experience. AI checkout differs from agentic buying, another form of agentic commerce, because humans retain full control over purchase decisions and use AI solely as tools.

Why This Is Important

AI checkout is relatively small due to limited availability and buying options. However, it can become an important channel to reach large audiences and increase commerce revenues, given the large user base of AI platforms. If participating, organizations must actively manage technical integration and channel mix strategy to ensure overall revenue growth. Even organizations that choose not to participate can get referrals as AI platforms include links to products not yet available in checkout.

Business Impact

Organizations can increase commerce revenue and acquire new customers through AI checkout, but platform-specific integrations add technical complexity. They must carefully manage their channel mix to prevent cannibalization of existing sales channels. As AI platforms increasingly control product discovery and purchase decisions, organizations need to protect brand visibility and influence. To maintain customer mind share, they should strengthen D2C experiences to match or exceed AI checkout convenience.

Drivers

- More AI platforms are rolling out checkout, and their large user base offers potential to drive sales for organizations.

- Organizations struggling with visibility on answer engines can participate in AI checkout as a “fast track” to win customers and grow sales.

- Technology vendors are integrating with AI platforms to facilitate product listing, including channel integration providers, such as Feedonomics, and commerce platforms, such as Shopify and Shopware. These integrations ease the technical complexity of preparing product data and connecting to multiple platforms.

Obstacles

- AI checkout is currently available on a limited number of AI platforms, primarily in the U.S. Most platforms require merchants to go through a curation and approval process, which means many relevant products may not yet be available for purchase through AI checkout.

- Product discovery remains central to AI checkout. Even when participating, organizations still compete with other merchants for visibility on the “digital shelf.”

- AI checkout today supports B2C transactions only and does not enable B2B purchasing. Even within B2C, support for capabilities such as multiitem purchases, bundles, subscriptions and service add-ons remains limited or unavailable.

- Checkout experiences vary by platform, resulting in inconsistent purchase journeys for the same product. Some platforms use standardized, platform-native checkout flows (e.g., Google and Perplexity), while others rely on embedded merchant checkout experiences (e.g., OpenAI and Google).

- AI checkout programs also differ in product feed mechanisms and protocols (e.g., OpenAI’s ACP vs. Google’s UCP), often requiring organizations to create and maintain platform-specific merchant accounts to ensure product discoverability, adding technical complexity.

- AI platforms use opaque product recommendation algorithms. Organizations can influence limited factors, such as product data, availability and shipping, but not model evolution or personalization depth.

- As AI platforms increasingly control both product discovery and checkout, they build direct customer relationships, shifting the starting point of the buying journey away from individual merchants.

User Recommendations

- Assess whether AI checkout aligns with product fit and go-to-market strategy. If participating, start with a limited product set to evaluate technical requirements and the impact on sales volume and customer acquisition before expanding participation.

- Monitor changes in AI platform policies, ranking mechanisms, buying options and checkout experiences, and adjust technical configurations, product listings and channel mix accordingly. Reassess participation decisions on an ongoing basis as these platforms evolve.

- While participating in AI checkout, retain influence over product discovery by delivering agentic commerce experiences across channels and customer touchpoints. Agentic commerce CX enables personalized, transparent interactions throughout the buying journey, helping build stronger customer relationships and long-term loyalty.

- Implement technologies that support efficient product feed integration with AI platforms, and apply SEO and AEO best practices to improve product visibility and discoverability.

Sample Vendors

Feedonomics, Google, Microsoft, OpenAI, Perplexity, Shopify

Gartner Recommended Reading

AI Agents for Commerce Operations

Analysis By: Sandy Shen

Benefit Rating: Transformational

Market Penetration: 1% to 5% of target audience

Maturity: Emerging

Definition:

AI agents for commerce operations assist business users in automating digital commerce operational tasks, leading to better productivity and business outcomes. These agents have multiple skills to support business roles and can interact with humans using natural language. They can also collaborate among themselves for complex tasks. AI agents are typically powered by LLMs but can also use other technologies such as rule engines and machine learning.

Why This Is Important

AI agents can improve productivity in digital commerce operations by automating tasks such as content generation, customer segmentation and campaign setups. These agents can also enhance business outcomes by suggesting optimization strategies that may not be obvious to business users. Organizations can apply rules and guardrails to constrain the actions taken by agents. AI agents are currently emerging in digital commerce but are expected to become a standard capability in vendor solutions within the next two years.

Business Impact

AI agents make business users more productive and improve digital commerce outcomes by automating tasks and suggesting optimization strategies. AI agents, when not properly implemented, can negatively impact the business and CX by delivering misleading answers, exposing sensitive data to unintended users or taking wrong actions.

Drivers

- AI features embedded in commerce platforms, such as product description generation, search optimization, review summaries and data insight analysis, are underlying capabilities that can be invoked by AI agents.

- Business users are more likely to adopt AI agents for daily tasks due to their ability to interact using natural language.

- AI agents become the gateway to business systems, supporting various tasks and reducing the number of tools business users need to learn and interact with. These tasks include arranging campaigns, developing webpages, segmenting customers, suggesting personalization strategies, generating data insights and customizing reporting.

- Organizations have a high awareness and willingness to invest in AI agents to improve commerce productivity and performance.

- Digital commerce vendors are deploying AI agents in their solutions, leveraging the extensive data residing in the platform. This drives customer adoption.

- Low-code agent builder and integration platform as a service (iPaaS) tools within commerce platforms allow business users to customize agent skills and workflows to execute tasks across systems and even those (e.g., ERP) beyond the commerce platform.

Obstacles

- There is a lack of transparency of vendor’s AI capabilities and a common understanding by organizations about AI agents, AI assistants, chatbots and robotic process automation, leading to organizations investing in suboptimal solutions for their needs.

- Organizations don’t always have sufficient or accurate data (e.g., customer preferences, inventory availability), nor robust data management, to achieve the expected outcomes of AI agents.

- An Insufficient amount or lack of security controls and guardrails can lead to security breaches or misconduct by AI agents, or unintended use of AI agents.

- Besides Model Context Protocol (MCP), multiple agentic protocols are competing to become the standard to enable agents to connect with organizations’ internal data and systems. Although MCP is the most adopted by the installed base, organizations may need to invest in other protocols for various purposes, such as connecting with an AI discovery channel.

User Recommendations

- Use Gartner research to understand the scope and capabilities of AI agents and what they can reasonably achieve.

- Ensure that accurate and sufficient data is present for key commerce entities, such as product, pricing, inventory, order and customers. Take stock, organize, and enrich the data for agents to easily access and retrieve.

- Experiment with agentic capabilities embedded in digital commerce applications to assess their impact on productivity and business outcomes. When available, use low-code agent builders and iPaaS tools to construct your custom agents and workflows.

- Set up security mechanisms and guardrails to regulate the input and output of AI agents to ensure compliance and accuracy. Put employees in the loop when needed to verify the behavior and output of AI agents.

- Communicate the deployment of AI agents to employees and equip them with skills to work with agents in data preparation, prompt formulation, monitoring and feedback. Encourage them to focus on higher-value tasks such as goal setting, use cases and CX designs that cannot yet be undertaken by AI agents.

Sample Vendors

KIBO; Salesforce; SAP; Shopify; Shopware; VTEX

Gartner Recommended Reading

Machine Sellers

Analysis By: Luke Tipping, Daniel Hawkyard

Benefit Rating: High

Market Penetration: 1% to 5% of target audience

Maturity: Emerging

Definition:

Machine sellers (or sellerbots) are persona-based AI agents that automate end-to-end sales workflows for simple transactions or complete specific deal activities on behalf of human sellers during more complex sales processes. Currently, they predominantly facilitate routine, predictable transactions. This includes selling to and serving human customers, or interacting directly with AI agents acting on behalf of human customers to purchase goods and services (machine customers or custobots).

Why This Is Important

Sales organizations can achieve scale using machine sellers to automate deal workflows that would require significant human resources to complete. These AI agents unburden human sellers from low-value activities, enabling a focus on high-value tasks. Furthermore, machine sellers provide the vast datasets, interfaces, and instant response times that machine customers (custobots) expect, ensuring an optimal, frictionless buying experience that drives faster deal conversions.

Business Impact

Sales organizations deploying machine sellers will gain a competitive advantage, locking in recurring revenue by satisfying buyer preferences for seamless purchases. Machine sellers enable organizations to meet the expectations of machine customers at scale and unlock seller productivity by unburdening them from involvement in nonstrategic purchases and low-value activities. Organizations that do not adopt machine sellers risk wasting resources, decreasing efficiency, and missing revenue goals.

Drivers

- Machine sellers present an opportunity for sales organizations to drive recurring revenue and shorten sales cycle times by automating repurchases. They provide revenue and margin enhancement opportunities by surfacing buyer needs that may not be immediately obvious to sellers or buyers, and product recommendations optimized for conversion rate or improved profit margins.

- Buyers increasingly expect suppliers to deliver an effortless and frictionless customer experience. According to the 2025 Gartner B2B Buyer Survey, 67% of B2B buyers state that they prefer rep-free sales experiences. Machines are better equipped than humans to make instant, data-driven decisions that meet buyer demands for streamlined purchasing processes, cost-efficiencies, and productivity gains.

- Deployment of machine sellers will be critical for delivering CEO strategies for engaging with machine customers and AI agents. According to the 2026 Gartner CEO and Senior Business Executive Survey, CEOs anticipate 20% of their revenue to be generated by AI agents or machines acting as customers by 2030. With the increasing level of sophistication and autonomy of agentic AI, machine sellers and machine customers will interact with each other to make complex purchase decisions and transact among themselves.

- Continued advancement of agentic technology will expand and improve the capabilities of machine sellers for supporting increasingly sophisticated tasks. This trend will also see buying groups increasingly adopt machine customers, forcing sales organizations to deploy machine sellers in response.

- Machine sellers offer productivity gains to sales organizations by unburdening sellers from overseeing routine, nonstrategic transactions, and automating more complex deal activities, enabling sellers to focus on high-value tasks.

Obstacles

- Machine sellers are an emerging technology and do not represent a single market. Instead, sales organizations leverage automation and agentic capabilities within existing software, or technology embedded within connected products to support specific tasks or outcomes for customers, such as automated reordering or subscriptions.

- AI agents must be connected to a central, integrated data platform to successfully execute their assigned tasks, consolidating data from disparate sales systems.

- Organizations must establish trust in machine sellers across internal and external stakeholders. Sales leaders must build confidence that tasks executed by the technology are understandable and deliver optimal outcomes.

- Impact of machine sellers will vary by industry, geography, business model and use case. Complex industries are less likely to adopt machine sellers in the short term as buyers prefer to receive guidance from humans. In these cases, machine sellers will autonomously execute specific deal activities such as call scheduling, automated follow-ups, and contract negotiations.

User Recommendations

- Incorporate machine sellers into your go-to-market strategy roadmap within the next one to two years, particularly if you’re in a market that predominantly consists of highly routine, predictable transactions. However, regardless of your industry or solutions, buying organizations will increasingly expect suppliers to offer efficient, frictionless purchase experiences.

- Establish a cross-functional team to explore the business potential of launching your own machine sellers to drive revenue and customer retention. Evaluate your offerings and customer segments to identify those most suited to routine, predictable transactions that can be serviced by a machine seller through autonomous replenishment.

- Conduct an assessment of complex deal processes, identifying the most burdensome activities for sellers and buyers, to surface opportunities to automate these tasks via machine sellers.

- Pilot machine sellers to facilitate tasks, such as solution building, quote creation, and contract writing, to determine productivity and effectiveness gains compared to human-seller-led processes.

Gartner Recommended Reading

Answer Engine Optimization

Analysis By: Noam Dorros

Benefit Rating: Transformational

Market Penetration: 20% to 50% of target audience

Maturity: Emerging

Definition:

Answer engine optimization (AEO) refers to optimizing content to appear in direct answers provided by public search and large language model (LLM) answer engines. AEO tactics and technology promise to help marketers measure and manage the disruptive impact of GenAI on search.

Why This Is Important

Answer engines and LLM algorithms continue to profoundly disrupt human behavior and communications patterns. As information discovery and retrieval habits are upended, marketing must adapt. CMOs must rethink how to build brands, drive traffic, generate leads and acquire customers. The balance of paid, earned and owned media investments must be reevaluated. AEO refers to the nascent but essential process of maximizing marketing outcomes in this new world.

Business Impact

AEO aims to help marketers harness answer engine disruption by creating and measuring content that is readily discovered and featured by answer engines and AI chatbots. AEO focuses on providing clear, concise answers to specific user queries. It aims to structure content for readability and extraction by LLMs, thereby boosting visibility and increasing brand trust. By using AEO to quickly meet user intent, businesses may gain an edge, despite reductions in site traffic due to answer engine zero-click search dynamics. AEO can be reasonably viewed as an incremental update to search engine optimization (SEO), but its continued evolution is likely to be convoluted as competition for Google heats up and users establish new behavior patterns.

Drivers

The adoption of AEO is driven by several key factors that reflect changes in technology, user behavior and the digital landscape:

- Growth of AI and conversational search: Advanced AI models and chatbots (such as ChatGPT) can interpret and respond to complex queries. Users now expect immediate, accurate answers rather than sifting through multiple webpages, pushing businesses to optimize for these answer engines.

- Rise of voice search and virtual assistants: The increasing use of voice-activated devices, such as smartphones, smart speakers and virtual assistants, has shifted how users search for information. Voice queries are more conversational and specific, making concise, direct answers more valuable.

- Increased competition for visibility: As organic search becomes more competitive, securing placement as a featured answer or snippet can significantly boost visibility and traffic. AEO provides a strategic advantage by positioning content where users are most likely to see it.

- Enhanced search engine capabilities: Search engines are increasingly capable of parsing structured data, understanding context and extracting answers from well-optimized content. Businesses must adapt their content to these evolving algorithms.

- Motivational targeting: In contrast with traditional keyword-based search queries, which marketers interpret as signals of basic intent, conversations with extended context are more likely to reveal the “why” behind a request. This ability offers marketers opportunities to produce content aligned to more specific user concerns, collapsing purchase cycles and enabling more tailored solutions.

- Extended content strategy: Traditional website content is constrained by information architecture design and site-search limitations. Websites designed with AEO in mind have few limitations on the breadth and depth of content exposed to indexers.

Obstacles

AEO presents several obstacles and challenges:

- Lack of algorithm transparency: Search engines and AI assistants do not disclose how they select and rank content.

- Content strategy inertia: The rise of conversational AI means queries are more nuanced, requiring a more agile content strategy that goes beyond keyword focus to deeper search intent and consumer preferences.

- Limited data and measurement tools: It’s difficult to track and measure the impact of AEO compared to traditional SEO.

- Zero-click searches: When direct answers are provided, users may not click through to your site, limiting traffic, conversion and measurement opportunities.

- Frequent algorithm updates: Answer engines frequently update how they craft answers.

- Localization challenges: Optimizing for multiple languages or regions adds complexity.

- Intense competition: Many brands are targeting the same questions, making it difficult to win and retain answer-box positions.

- Brand and content ownership: When answer engines use your content, there is a risk of losing brand visibility.

User Recommendations

Achieving success with AEO requires ongoing adaptation, investment in structured content development and distribution, and acceptance that not all benefits will be directly measurable or controllable. Given this, Gartner recommends that marketing leaders:

- Continue building domain authority through traditional SEO practices, such as ensuring mobile-friendliness and adding appropriate alt text.

- Monitor your brand’s presence on answer engines, either manually or with third-party tools.

- Create concise, authoritative answers to common user questions, and distribute them multimodally across the web and social media — in text, visual, and video formats.

- Use structured data (schema markup) to help engines extract answers.

- Develop use-case-specific landing pages that target key queries.

Gartner Recommended Reading

Guided Selling Assistant

Analysis By: Sandy Shen

Benefit Rating: High

Market Penetration: 5% to 20% of target audience

Maturity: Adolescent

Definition:

A guided selling assistant is a customer-facing solution that enables self-service product discovery with a goal to convert buyers into customers. It uses search engines, leveraging AI, vectors and domain knowledge to power intent detection and responses that are delivered through an experience combining conversations, facets and quizzes to recommend products per customer requirements.

Why This Is Important

Guided selling assistants improve buyer confidence in product choice and, as a result, can increase conversion and average order value (AOV). AI has elevated the buying experience through conversational capabilities and its ability to understand user intent and handle complex questions. Blending conversations with existing guided-selling techniques is an area of innovation for product discovery solutions that used to be designed primarily for search and browse experiences.

Business Impact

Guided selling assistants reduce buyer friction in finding the right products, thus improving conversion and revenue. They can handle complex questions and support solution cross-selling, further increasing revenue. They can support digital and physical channels, helping both customers and store employees find the right product quickly.

Drivers

- Guided selling assistants reduce buyer friction in the purchase journey by leveraging multiple types of content, self-service tools and calls to actions. For example, interactions can include images, videos, instructions and reviews, self-service tools such as size guide, product comparison and virtual try on, and calls to action like talk to an agent, add to favorites and add to cart. They increase customer engagement and conversions.

- The technology often layers over search and product discovery solutions, and can be used for multiple channels, including commerce sites, apps, emails, social media, messaging platforms, ads and retail stores. This broad applicability expands the technology’s reach and generates high-quality leads.

- AI improves the conversational capabilities to understand vague or open-ended requests and handle complex questions via a dialog — an advancement over the previous technologies that were often scripted and too rigid to adapt to user intent. The technology also helps business users set up questionnaires more efficiently without managing complex rules.

- Guided selling assistants will merge with traditional search and browse experiences to drive a new, hybrid UI that better suits user preferences. Product discovery vendors are experimenting with optimal UX to offer a more intuitive experience with hybrid conversational and browsing experience.

Obstacles

- While more customers are asking full questions on answer engines, they are still unaccustomed to such behavior on websites and default to searching with a few keywords. Evolving the “search box” towards a conversational UI needs careful consideration and iteration to encourage richer interactions.

- AI hallucination is a key challenge, leading to customer frustrations and loss of trust in the recommendations. Gartner surveys show that 75% of U.S. consumers feel that GenAI has made it harder to distinguish what is real vs. not, and a similar portion of people feel it more stressful to let AI make purchase decisions on their behalf.

- Organizations do not use guided selling for channels such as social media, messaging apps or stores, failing to reach a wider audience and generate a higher ROI for the investment.

- Guided selling assistants are better positioned for simple or moderately complex products and have limitations for highly complex products such as those requiring design or engineering efforts, where a visual configuration tool is more appropriate.

User Recommendations

- Assess whether guided selling assistants are a good fit for your offerings. Typically, products that require high consideration, are performance-driven or have many similar options are good candidates.

- Select the solution based on its ability to leverage multiple techniques, including filters, quizzes and conversations, and how it blends conversations with the browsing experiences. Avoid positioning and presenting it as a traditional chatbot or education tool, as customers may have gained reservations about the usefulness of these.

- Use A/B testing to find the right UX for blending various techniques and for different channels.

- Address the usefulness and trustworthiness of the assistant by including self-service tools, connecting to humans, and explanation of recommendations and tool limitations.

Sample Vendors

Constructor; Fractal; Google; Jio Platforms (Haptik); Salesfloor; Zoovu

Gartner Recommended Reading

At the Peak

Machine Customers

Analysis By: Don Scheibenreif

Benefit Rating: High

Market Penetration: 1% to 5% of target audience

Maturity: Emerging

Definition:

Machine customers are nonhuman economic actors that obtain goods or services in exchange for payment. Examples of machine customers include AI agents, generative AI chatbots, smart appliances, connected cars and Internet of Things (IoT)-enabled factory equipment. Machine customers act on behalf of a human customer or an organization.

Why This Is Important

Gartner estimates 5 billion B2B and B2C internet-connected machines can act as customers today, growing to 12 billion by 2030. These machine customers will have varying degrees of autonomy. AI assistants (or chatbots) will also reach into the billions. Machines are increasingly capable of buying, selling and requesting services. Moreover, machine customers are evolving from simple informers to advisors and decision-makers.

Business Impact

Over time, trillions of dollars are expected to be in control of nonhuman customers. This will result in new opportunities for revenue, efficiencies and managing customer relationships. Leaders seeking new growth must reimagine their operating and business models to take advantage of this emerging market of tens of billions of machine customers. Organizations that miss this opportunity will be marginalized, just like those retailers who missed the digital commerce wave.

Drivers

- In the coming years, machine customers are set to become major players in industrial, retail, and consumer sectors. Billions of connected products, powered by advanced technologies, will soon act as autonomous customers, shopping for services and supplies for themselves and their owners. According to Gartner’s CEO and Senior Business Executive Surveys, 29% of CEOs are developing strategies to engage with machine customers and AI agents, with half expected to have a strategy by the end of 2026. By 2030, 19.5% of revenue is projected to come from machine customers.

- Currently, machines inform, recommend, and perform routine tasks but are evolving into sophisticated customers. Examples include Amazon’s Dash Replenishment Service, HP Instant Ink, Tesla’s self-ordering of spare parts, and Fastenal’s auto-replenishing vending machines. More advanced tasks are handled by Waymo’s autonomous taxis and Agility Robotics’ Digit.

- AI platforms and agents are accelerating this trend. Services like Amazon Alexa+, Google Gemini, and OpenAI’s Instant Checkout enable 24/7 inquiries, product recommendations, streamlined check-out, and support for human agents. In B2B, AI-based contract negotiation systems like Pactum AI, used by Walmart and Maersk, generate fair contracts, while supplier discovery and data platforms are shaping machine customer interactions.

- Payment solutions — such as Mastercard’s Agent Pay and Google’s Universal Commerce Protocol — will further empower AI agents to execute digital transactions. Overall, machine customers represent new revenue streams, increased productivity, enhanced health and security, and benefits for both sellers and buyers.

Obstacles

- Operating model changes: Serving machine customers will disrupt existing models. Companies must create separate experiences for machines and humans, scaling operations to meet real-time machine demands or risk losing them.

- Lack of trust: Humans may distrust machine customer technology over privacy and accuracy, while machines may distrust suppliers.

- Fear of machines: Some fear delegating purchasing to machines and AI. Customers and organizations must assess governance for ethical, legal, fraud, and risk standards.

- Security and governance: Increased AI use may lack security, leading to misinformation and reputational damage.

- Cost: Implementing and maintaining these systems is complex and costly. Adapting to changing needs requires significant investment in technology, software, and support.

User Recommendations

- Identify use cases where your products and services can be extended to machine customers. Collaborate with digital, data, strategy, sales, and customer officers to explore the potential.

- Assess B2B customers’ tech purchase intent data to spot machine customer capabilities and use cases.

- Pilot ideas to understand required technologies, processes, and skills. Build digital commerce and AI capabilities — starting with generative and agentic AI.

- Use APIs and bots for low-complexity transactions, then expand to complex purchases.

- Monitor competitor adoption of AI agents as machine customers. Follow examples from Amazon, Google, HP, iProd, NEC, OpenAI, and Tesla for evidence of capabilities and business-model impact.

Sample Vendors

Amazon; Anthropic; Google; HP Inc.; iProd; NEC; OpenAI; Pactum; Perplexity; Tesla

Gartner Recommended Reading

Product Experience Management

Analysis By: Jason Daigler

Benefit Rating: High

Market Penetration: 20% to 50% of target audience

Maturity: Early mainstream

Definition:

Product experience management (PXM) is a framework of applications and capabilities that optimize the creation, delivery, activation and analysis of product content across various channels. PXM enhances digital commerce by ensuring consistent and accurate product information. It does not replace product information management (PIM) solutions or digital asset management (DAM) platforms. Rather, PIM solutions and DAMs are fundamental components of PXM.

Why This Is Important

PXM is crucial in digital commerce, where accurate, consistent and enhanced product information is vital for customer engagement and sales conversion across a variety of channels. PXM leverages and consolidates product content from existing systems, addressing the challenges of siloed data and enhancing brand representation across channels. Its relevance is amplified by the growing demand for seamless shopping experiences and an ever-increasing number of channels, including AI platforms and AI assistants on retail sites and marketplaces.

Business Impact

Industries such as consumer packaged goods will benefit most from PXM by improving product data accuracy. PXM enables streamlined product content management, aligning with channel requirements and driving revenue growth. It increases operational efficiency by managing frequently changing integration requirements and reducing manual efforts involved in integration, compliance, governance and product listing optimization. Companies focused on digital commerce, especially in indirect channels, should prioritize PXM implementation.

Drivers

- Growing consumer demand for personalized and seamless shopping experiences across digital channels, including AI platforms and retailer sites and marketplaces that use AI assistants.

- The increasing complexity and volume of product data requires streamlined management solutions.

- Marketplaces are increasingly augmenting their product listing offerings by integrating with video services, chat features, brand stores, etc. These advancements require more capabilities from PXM applications to optimize listings.

- Advancements in AI to enhance PXM capabilities.

- Pressure on brands to provide best-in-class content and maintain consistent and accurate product information across multiple platforms to optimize listings and grow sales.

- The increasing number of channels that companies need to sell on requires robust management of product experiences.

- Regulatory requirements for accurate product information and data compliance.

Obstacles

- Integration with existing systems is complex, particularly in harmonizing product information across diverse platforms.

- Managing PXM across many geographies is complex, especially for large organizations with separate business units using different tools while selling in geographically specific channels.

- Organizations might not see value if they don’t develop closed-loop processes whereby they draw insights from digital shelf analytics applications, make changes in a PIM and resyndicate to downstream channels.

- Organizations may struggle to identify a clear ROI from PXM investments due to the disconnected nature of the channels where products are sold.

- Potential confusion between the roles of PIM, DAM, MDM, ERP and product catalogs within digital commerce platforms can hinder effective implementation and utilization of PXM. Most PIM vendors are evolving their offerings to include applications and capabilities within the PXM framework. Additionally, many channel integration applications offer product catalog capabilities that could be confused with PIM solutions.

User Recommendations

- Prioritize the integration of source data from existing systems of record to a PIM to get started with PXM.

- Develop a list of channels where products are currently sold and a list of potential future sales channels. Ensure that syndication and channel integration applications, along with digital shelf analytics applications, are aligned with your organization’s required channel coverage.

- Avoid relying on product catalogs within digital commerce platforms as substitutes for PXM capabilities, as they are insufficient for channel integration/syndication and other capabilities within the PXM framework.

- Explore PXM capabilities and partnerships offered by PIM vendors first, as most PIM solutions are evolving their native capabilities and partner ecosystem to solve PXM use cases.

- Develop closed-loop processes whereby insights from digital shelf analytics applications are used to enhance product information. Explore the emerging agentic capabilities of PIM and DSA vendors for this purpose.

- Enable marketers and product experts to collaboratively enhance content and data, optimize product information for different channels, and distribute product information to common and emerging channels.

- Use PXM to expand product sales across a variety of new channels. Consider whether existing order management systems (OMS), which are often purpose-built for orders from direct channels, are sufficient for managing orders from indirect channels. If they are not fit for the purpose, consider vendors who can offer both syndication and order management capabilities. PIM solutions and DSA applications rarely have OMS capabilities.

Sample Vendors

Akeneo; Baozun; Centric Software; ChannelEngine; Inriver; Rithum; Salsify; Syndigo

Gartner Recommended Reading

Digital Sales Rooms

Analysis By: Melissa Hilbert

Benefit Rating: Transformational

Market Penetration: 5% to 20% of target audience

Maturity: Adolescent

Definition:

Digital sales rooms (DSRs) are a channel designed to increase buyer and seller engagement throughout the customer journey via a privately formed persistent microsite. DSRs use a combination of digital assets, e-commerce and workstream planning capabilities. Customers or prospects can interact asynchronously or live anytime and especially at critical decision points. Revenue teams can provide personalized and relevant insights at various touchpoints to facilitate the customer’s journey.

Why This Is Important

Digital interactions in combination with seller-led interactions is a permanent shift heavily affecting complex B2B buying and selling processes. DSRs support new business, growth and customer retention by providing a platform where suppliers and buying groups engage in ongoing collaboration across the buying journey and customer life cycle. This primary interface for live and asynchronous digital interactions with buying teams can strongly improve customer experience (CX) and lifetime value.

Business Impact

DSRs provide the following advantages:

- Improved win rates with tailored and focused buyer-centric collaboration.

- Accelerated pipeline conversion rates and improved buyer confidence and consensus at key stages in a buying process.

- Hyper-personalized content for buyers, leading to faster sales cycles.

- Improved seller visibility into the buyer stakeholders’ engagement with content, process and tools, resulting in faster action.

- Improved forecast accuracy with improved insight into buyer engagement.

Drivers

- Buyers prefer to engage digitally and want to control how and when they interact with suppliers and sellers.

- DSRs offer a streamlined platform for digital interaction and collaboration with buyers located globally, thereby ensuring sustained value throughout the customer relationship — from presale activity to postsales relationship-building, growth and renewal.

- DSRs enhance the customer lifetime value by improving the buyer’s experience and consolidating digital channels, simplifying the interaction process with the supplier.

Obstacles

- Incomplete DSR capabilities and inadequate integration with existing systems — such as CRM sales platforms, digital content management, configure, price and quote (CPQ), interactive demo applications, digital commerce platforms, and AI assistants — can lead to a fragmented subpar buyer experience.

- Limiting DSRs to a single use case reduces their comprehensive value and utility across the customer life cycle.

- Tighter budgets require DSRs to prove commercial impact, including revenue growth and sales cycle time, which may be difficult if the DSR does not have full capabilities — including key capabilities such as bidirectional content sharing, mutual action plans or digital commerce.

- DSRs not integrated with CRM platforms limit insights that can be surfaced to sellers.

User Recommendations

- Evaluate DSR capabilities offered by best-of-breed solutions and those offered by revenue enablement platforms, digital commerce and CRM sales platform vendors.

- Prioritize the following capabilities, depending on your organization’s needs:

- Configurable templates for a personalized persistent microsite for the entire life cycle of the customer

- Bidirectional content sharing for all forms of media types

- Integrations with CRM platforms, videoconferencing tools and collaboration tools

- Call scheduling for buyers

- Buyer engagement analytics for interactions within the DSR

- Collaborative mutual action plans for sellers and buyers or customers

- Integrations with e-signature, digital commerce and CPQ applications

- Complex deal negotiation support for sellers and buyers

- AI assistants in the DSR answering buyer questions.

- Establish a business methodology with DSRs to support your B2B customers at customer life cycle inflection points where DSRs are effective, valued or helpful to deliver strategic outcomes.

Sample Vendors

Aligned; Allego; ClientPoint; Dock; Flowla; Highspot; Mindtickle; SalesHood; Shopware; trumpet

Gartner Recommended Reading

Hybrid Search

Analysis By: Mike Lowndes

Benefit Rating: High

Market Penetration: 5% to 20% of target audience

Maturity: Adolescent

Definition:

Hybrid search is the integration of keyword (or term-based) search, natural language processing (NLP)-based semantic search and vector search to provide an improved search and product discovery solution. A hybrid approach connects the speed and accuracy (precision) of keyword search and the intent detection and inference capabilities (recall) of vector search, within the same search experience.

Why This Is Important

Keyword-based search has dominated discovery by matching queries to keywords indexed from documents and assigning relevance based on position, frequency and other rules. NLP extended this via linguistic understanding of queries and mapping them to knowledge graphs for inference, giving rise to semantic search. Vector search takes a fundamentally different approach via mathematical representation, enabling results to be identified for a much broader range of queries than previously.

Business Impact

- Responding to both keyword and natural language or multiword queries with relevant results improves customer experience.

- Vendors that can dynamically select the right results to show based on intent provide customers a more seamless experience.

- Customers are beginning to expect discovery experiences delivered through more conversational, agentic UIs. Hybrid search is a step toward future discovery UIs and conversational modes of discovery, and will underpin such UIs.

Drivers

- Discovery is transitioning toward natural language, often with a question-based approach. As users increasingly use natural language queries when searching the internet and social media, they will expect the same from websites, portals, intranets and apps.

- Hybrid search solves “zero results” by invoking vector search for lower-precision queries. Zero results remain a significant challenge to businesses, acting as a blocker to conversion when there may be a product or service that is relevant but uses different terms to those in the query.

- Keyword search, especially for single terms such as product SKU codes, remains an accurate and efficient method of retrieval and so is preferred over vectors. The use of named entity recognition (NER) for NLP is an effective extension of this for intent detection, especially when using context data; (for example, where the search is done from within a taxonomy, previous search terms or using knowledge graphs providing inference). Blending together keyword, NLP/NER and vector approaches provides a mechanism to return results based on all these methods as appropriate.

- Vector databases also support visual search by vectorizing image features, and AI-based semantic feature tagging can blend this into hybrid search.

- While training LLMs remains rare and training domain-specific language models (DSLM) remains expensive, retrieval-augmented generation (RAG) is used to ground models in the appropriate dataset. However, as with human searches, RAG can use hybrid search to improve the efficiency of GenAI pipelines and new UIs to discovery.

Obstacles

- The World Wide Web has focused on keyword search use for over 25 years, and many desktop applications are still limited to this function. Although expectations are changing, especially generationally, there are many who still use keyword search and don’t expect hybrid search when visiting websites or in native apps.

- Many users are not yet comfortable conducting long or full-sentence searches on brand/digital commerce websites, especially when using the search bar, and tend to enter fewer words, which requires more accurate intent detection to deliver high relevancy.

- Some vendors are already moving to multidimensional unified search indexes requiring only one query, rendering the hybrid approach obsolete. It is too early to tell how successful this new paradigm will be, but it could replace hybrid search if generally accepted.

User Recommendations

- Use analytics on the kinds of search terms used by customers to detect the proportion of natural language and complex queries. Also, look into the proportion of zero or low-quality results with low conversion. The queries against these pages may be better served via hybrid search.

- Look for a long tail of low-quality results that may indicate a large volume of poorly performing search that may be due to keyword search limitations.

- Be aware that search analytics may be skewed by the limitations of the current solution and customer expectations.

- Run proofs of concept (POCs) to test the effectiveness of this new approach. Use messaging to alert the customer that the search accepts natural language, or provide it as an option. Many search and product discovery vendors support POCs as part of their sales cycle.

Sample Vendors

Algolia; Constructor; Coveo Solutions; Lucidworks; Netcore Unbxd

Gartner Recommended Reading

Digital Experience Composition

Analysis By: Mike Lowndes

Benefit Rating: High

Market Penetration: 5% to 20% of target audience

Maturity: Adolescent

Definition:

DXC is the “head for headless,” composing digital experiences backed by API-first content and applications. It can include front-end cloud, visual page builders and templating tools with design system integration. DXC enables developers to manage digital experience UIs at scale and assign them to business users for day-to-day, no-code management. DXC employs API connectivity to headless services such as content management systems (CMSs), search, personalization and digital commerce.

Why This Is Important

Monolithic head-on applications with integrated UIs deliver wide functionality, but are often slow to update, release and scale. Headless architecture brought agility to front-end development, but forgot about the business user. Digital experience composition (DXC) brings experience orchestration and what you see is what you get (WYSIWYG) to the headless world, providing a modular capability for business users and developers to rapidly compose and iterate digital experiences.

Business Impact

Rapid innovation is essential to achieve digital business goals. By orchestrating experiences through DXC, business and technical users can drive innovation while preserving the integrity of decoupled back-end applications. This decoupling enables faster release of front-end innovations. While DXC platforms are not digital experience platforms (DXPs), they serve as a foundational element of DXP, providing a composition layer in no-code/low-code environments. DXC is increasingly merging with the DXP market.

Drivers

- A headless or composable approach to DXP often requires significant development and architectural expertise. Early adoption often resulted in business users being unable to manage the digital experience directly in a way they were used to via a head-on solution.

- Front-end cloud (e.g., Netlify, Vercel) has commoditized the runtimes for presentation layers. Its focus is on the front-end developer and DevOps but usually lacks the business tooling for no-code management for the resulting front ends.

- Experience builders (page builders, visual builders) enable business users to control the layout and composition of web content and functionality from multiple underlying systems via a drag-and-drop or WYSIWYG UI, with the ability to configure component behaviors and presentation and integrate widgets and third-party components.

- As front-end delivery remains code-heavy, low-code and no-code platforms need to package these capabilities and make them easier to consume. DXC contains a templating engine and integration to design systems, providing an integrated development environment for developers to create and orchestrate experiences at scale.

- An API integration and orchestration layer between multiple technologies powers the digital experience. This enables the integration of assets (such as content, products and images) or interactions (such as forms, search, access control and cart/basket) from their source system into a unified digital experience.

- API integration can also be used to orchestrate between components. Some vendors differentiate by focusing on this, maintaining productized, prebuilt connectors to leading vendors in core digital experience segments.

Obstacles

- DXC is not necessary for simple, mainstream “brochureware” needs where packaged, head-on solutions such as web content management (WCM) with lower agility offer a good fit.

- DXC can be misused. Avoid considering it from a purely technical or architectural perspective. DXC enables businesses to manage headless, API-first experiences with full consideration for business users, but this is not always required.

- B2B penetration of API-first approaches and DXC has been slower due to the requirement for deeper integration with multiple internal systems and more complex UIs and workflows.

User Recommendations

- Ensure the expertise and resources are available to implement and manage the new architecture. A high level of digital maturity is still required to manage UI decoupling and integration. Tools, design and implementation skills can vary greatly from a monolithic/head-on approach.

- DXC has mostly converged with and has become part of composable digital experience platforms. Via evolution and M&A, most “headless CMS” and DXPs have brought DXC into their suites. This is only an obstacle to DXC as a stand-alone capability — it is likely to be reduced to a feature but broadly accepted.

Sample Vendors

Amplience; Builder.io; Conscia; Contentful; Contentstack; Netlify; Sanity; Uniform

Gartner Recommended Reading

Sliding into the Trough

Digital Shelf Analytics

Analysis By: Jason Daigler

Benefit Rating: High

Market Penetration: 20% to 50% of target audience

Maturity: Early mainstream

Definition:

Digital shelf analytics (DSA) applications provide brands and manufacturers with data from third-party digital channels where their products are sold, such as online marketplaces and retailers’ digital commerce sites. These applications scrape websites or consume data from APIs to improve the governance of product listings and monitor the performance metrics used to optimize product discovery and conversion.

Why This Is Important

Companies need to sell through an optimal mix of channels to reach their ideal customers. This channel mix constantly evolves as consumer behaviors change and companies learn which channels yield the best results. DSA applications improve the quality of online product listings, enabling sellers to make better decisions about their channel mix, protect their brand image, monitor inventories, improve retail media advertising, and optimize listings for maximum discoverability and conversion rates.

Business Impact

DSA applications enable brands and manufacturers to:

- Gain visibility into their product content on the digital shelf

- Improve positioning in search results

- Improve responsiveness to ratings and reviews

- Highlight inventory issues, even at the local store level

- Automate actions to update product listings and purchase advertising on retail media networks (RMNs)

- Integrate with other applications, such as product information management (PIM) solutions, and move toward product experience management (PXM)

Drivers

- Online sellers continue to leverage an increasing number of channels to reach their customers, and customers continue to demonstrate a preference for online buying.

- Brands and manufacturers often lack comprehensive oversight of their products’ performance on the digital shelf, making decisions about their chosen channel and product mix more difficult.

- DSA is a valuable technology for consumer goods companies that leverage digital channels they don’t own, such as marketplaces, retailers’ digital commerce sites, and comparison engines.

- For retailers that don’t sell on other retail sites — and sell less frequently on marketplaces — data and insight from DSA applications will originate primarily from social channels or other locations where retailers syndicate their products. Retailers can benefit from competitive pricing insights and promotional information. They can also track new product additions from competitors and identify internal assortment gaps, as well as competitors’ assortment gaps.

- Some DSA applications also provide competitive pricing information. As digital commerce grows and more marketplaces emerge, brands will experience increased pricing pressures. Leveraging DSA applications will help ensure that they’re pricing their products correctly.

- Preventing items from going out of stock and understanding inventory challenges have become critical priorities for many companies. Some DSA applications can gather insights about inventory at the local store level.

- Native AI capabilities within applications such as PIM solutions have increased companies’ ability to generate new product content at scale, thereby creating more content variations on third-party channels that need to be governed and optimized.

- The emergence of agentic commerce and the growing ability of AI platforms to ingest product content have increased the need for visibility on third-party channels. However, it remains to be seen how DSA applications will adapt to provide insight to AI platforms.

Obstacles

- Brands need to ensure that their DSA vendors can monitor their required channels and continue to add new, relevant channels.

- DSA applications are not beneficial without strong processes, technologies, and integration with other systems. Brands should develop processes for gaining insights using DSA applications, identifying changes to make, implementing those changes in a PIM or other system, and then resyndicating or publishing content to channels. They can then “close the loop” using the DSA application to ensure the changes are visible. Agentic capabilities with the DSA application and the existing tech stack could provide the needed technology and insight to facilitate the closed-loop concept.

- Even with strong closed-loop processes, the number of required optimizations can be daunting as product portfolios and channels expand. Automation is needed for simple changes, yet many vendors lack strong automation functionality, or the integrations may be inadequate to achieve automation.

- For retailers with physical stores, there is one digital shelf per store, especially for inventory. This increases the data sources and the amount of data returned, making analysis cumbersome.

User Recommendations

- Identify all channels through which products are being sold and the data available to define product performance in those channels.

- Use DSA applications to monitor the performance of the company’s products on digital shelves and gain insights about competitive products.

- Manage the end-to-end product content life cycle by developing a closed-loop process in which the DSA applications uncover insight and product teams make changes in other systems, such as digital commerce, marketing, and merchandising, to optimize performance. This may require offline processes for making changes to multiple systems; tight integration between the DSA application and other systems (e.g., PIM, PXM, and digital asset management [DAM]), plus integration with different RMNs; or selecting a vendor that offers a closed-loop system.

- Invest in automation once a closed-loop system is in place, allowing changes to be made in internal systems and pushed to external commerce sites without human intervention. Leverage AI and agentic capabilities from DSA vendors to automate product data changes.

Sample Vendors

CommerceIQ; Inriver; NIQ; Profitero+; Salsify; Shalion; Stackline; Syndigo; Wayvia; XPLN

Gartner Recommended Reading

Composable Commerce

Analysis By: Jason Daigler, Mike Lowndes, Sandy Shen

Benefit Rating: Transformational

Market Penetration: 1% to 5% of target audience

Maturity: Adolescent

Definition:

Composable commerce is an architectural approach to digital commerce whereby applications are constructed in a modular fashion. It requires loosely coupled back-end application capabilities, which are used to compose new commerce functionality and custom experiences. This approach contrasts with a platform-centric approach, in which monolithic commerce platforms are deployed to manage most aspects of the commerce customer experience.

Why This Is Important

Digital commerce solutions must be flexible to react to changing customer expectations, products, processes, delivery methods and customer experiences. Composable commerce enables solution changes, deployment to production environments and flexibility in scaling, whereas a monolithic platform includes many tightly coupled components that are not changed in every release. Composable commerce solutions are ideal for evolving AI and agentic commerce applications, allowing easier integration and automation than monolithic platforms.

Business Impact

Composable commerce:

- Provides benefits to digital commerce teams that want a more flexible architecture

- Provides greater ability to move quickly in response to customer demand

- Reduces reliance on large version upgrades

- Provides a means to replace capabilities when new vendors emerge

- Enables integration with AI and agentic commerce solutions, supporting advanced automation and data sharing

Drivers

- The foundational concept of composable commerce, whereby companies use best-of-breed, individual applications to construct commerce experiences, is not new. Many of the individual components of full digital commerce solutions — such as personalization engines, product search and discovery, and content management applications — have been around for several years, and have been sold and integrated independently.

- Modular commerce takes commerce experience a step further by offering granular functional components within the core commerce offering. Composable commerce is a further evolution, in which business users may construct commerce experiences using low-code tools.

- More complex requirements and increased investment in digital commerce often leads to the need for external “best-of-breed” point solutions from third parties — easy integration of those modules is enabled by composable approaches.

Moves toward composable commerce are often driven by:

- The desire to move away from inflexible, slow-to-update and monolithic digital commerce platforms.

- The need to adopt a modular approach that provides more flexibility to a digital commerce technology stack by allowing companies to replace nonoptimal functionalities with best-of-breed modules from a different vendor or with a solution that they develop themselves.

- The need for individual business units or geographically dispersed teams to customize capabilities to meet their needs without duplicating investments or needing to collaborate on a shared set of development priorities.

- The opportunity to consolidate software investments through reuse by reducing redundancy of functionality across applications and departments.

Obstacles

- Confusion abounds in the digital commerce market, as vendors use terms like “headless,” “microservices” and “API first,” resulting in confusion for buyers.

- Companies with smaller development teams or fewer solution integration resources may be more comfortable with a larger commerce suite with a single business user administration console. Achieving composable commerce takes time; business value may not appear instantly.

- In a challenging macroeconomic climate, organizations focus more on cost optimization and time to market. A shift toward composability, which can take longer and cost more to implement, may be more challenging due to smaller budgets and fewer resources. Some businesses that began a composable journey have reverted to selecting packaged or suite solutions featuring lower composability.

- Adopters of composable commerce need digital maturity — strong architectural, process, product management, integration and API orchestration skills and governance to be successful.

- User-friendly integration tools, such as low-code application platforms, will need to emerge before composable commerce can become mainstream.

- Smaller, less-complex companies may not see the same benefits from composable commerce as those with more complex businesses that have diverse systems, business units and processes that require customization of a common set of underlying functionalities.

- Commerce platform vendors that have attempted to decompose their legacy monolithic offerings to evolve toward composable architectures have had varied results and such initiatives generally remain incomplete. Prospects must look beyond composable marketing claims and evaluate platform architectures in order to gain confidence in new platforms.

User Recommendations

- Assess your digital maturity. Succeeding with composable commerce requires a digitally mature perspective that embraces processes, such as digital product management, fusion teams and DevOps.

- Work with the individual product teams responsible for functional areas of digital commerce to build the business case for composable commerce.

- Evaluate your commerce technology stack to identify inflexible and tightly coupled or redundant components that could benefit from composable commerce.

- Advance toward composable commerce in small increments, ensuring the presence of governance at each step before proceeding further.

- Plan for integration complexity. Low-code or no-code integration tools are nascent between digital commerce capabilities, especially if they come from different vendors. Resources to build and maintain integrations over time will be required. Give preference to application vendors that deliver well-articulated business-modular applications.

Sample Vendors

BigCommerce; Broadleaf Commerce; commercetools; Elastic Path; Emporix; Infosys Equinox; KIBO; Spryker; Virto Commerce; VTEX

Gartner Recommended Reading

Modular Commerce

Analysis By: Aditya Vasudevan

Benefit Rating: Transformational

Market Penetration: 5% to 20% of target audience

Maturity: Early mainstream

Definition:

Modular commerce extends API-based (headless) commerce by decomposing core platform functions into independently deployable, API-driven business modules. This approach enhances flexibility, agility and scalability by enabling organizations to integrate AI faster, deliver personalized experiences and optimize commerce operations using composable, best-of-breed capabilities.

Why This Is Important

Modular commerce is critical as it shifts digital commerce from monolithic to componentized, API-driven architectures. This modular approach drives faster innovation, increases agility and simplifies AI integration, while reducing deployment risk and complexity and enabling businesses to adapt quickly to changing market demands.

Business Impact

- Delivers maximum flexibility across customer journey touchpoints.

- Supports product-led, personalized experiences.

- Increases business agility and drives innovation.

- Empowers business units to deliver differentiated experiences.

- Accelerates speed to market for new features.

- Reduces development costs by enabling rapid feature delivery.

- Aligns business and IT around shared objectives.

Drivers

- Modular commerce represents the next step beyond API-based (headless) commerce on the path to composability, enabling organizations to replace or upgrade individual components without replatforming.

- Organizations that have adopted, or are adopting, an API-based digital commerce approach should consider a product-led solution rather than a platform-led one. This approach enables them to innovate and scale critical capabilities independently without affecting others.

- Modularity improves organizational agility by “productizing” capabilities, allowing organizations focused on innovation and growth to avoid constraints imposed by monolithic platforms. Faster innovation cycles, for example, help business users enhance targeted experiences and capabilities more effectively.

- Modular commerce also reduces platform dependencies by enabling each capability to be delivered, maintained, upgraded, or replaced independently.

- In parallel, more digital commerce platforms now offer modular pricing models, giving organizations the flexibility to implement only the capabilities they use.

- Gartner research shows that organizations adopting modular commerce are better positioned to leverage AI, automation, and advanced analytics, resulting in stronger customer experiences and improved operational efficiency.

Obstacles

- Data dependencies across modules can create integration challenges, especially in single-vendor, “walled-garden” environments, limiting flexibility to adopt third-party alternatives.

- Modular architectures introduce additional complexity, requiring higher levels of digital maturity and often leading to longer initial implementation timelines than traditional platforms.

- Skills gaps can hinder adoption, including insufficient availability of technical skills, such as API integration and DevOps as well as business skills, such as digital product management.

- Maintaining multiple applications that support modular components demands robust DevOps processes and ongoing resource investment to maintain agility and reliability.

User Recommendations

- Develop and stabilize a headless storefront roadmap as a foundational step toward modular commerce.

- Select tools and platforms that empower business users to control the UI and customer journey, even within a modular architecture.

- Evaluate commerce platforms for modular capabilities and assess vendor roadmaps to ensure timely module decomposition and integration.

- Invest in DevOps and agile practices to manage complexity, enable rapid deployment and support ongoing module maintenance.

- Build internal capabilities in API integration, DevOps and digital product management to maximize the success of modular commerce initiatives.

Sample Vendors

BigCommerce; commercetools; Elastic Path; KIBO Commerce; SCAYLE; Spryker; VTEX

Gartner Recommended Reading

Retail and Commerce Media Networks

Analysis By: Greg Carlucci

Benefit Rating: High

Market Penetration: 20% to 50% of target audience

Maturity: Early mainstream

Definition:

Retail and commerce media networks aggregate audiences across commerce-owned sites, apps and digital assets to create advertising opportunities on search, display, video and off-site channels. They use first-party behavioral and transaction data to package audience segments for advertisers through direct or programmatic buying models, enabling targeted activation and commerce-linked performance measurement.

Why This Is Important

Retail and commerce media networks allow advertisers to activate first-party shopper and customer data across both on-site and off-site channels, at a time when signal loss and rising performance media costs are increasing pressure on digital advertising efficiency. As more networks launch across industries, fragmentation and rising CPMs increase the need for standardized measurement, incrementality insights and data collaboration capabilities.

Business Impact

Retail and commerce media networks offer advertisers the ability to reach users via first-party data, providing more direct links between media exposure and commerce outcomes than most digital advertising channels. As budgets shift toward performance-accountable media, identity resolution technologies and programmatic access enable deeper audience insights, advanced incrementality analysis and unified activation across channels.

Drivers

Several factors are accelerating the evolution of commerce media, driven by changes in technology, measurement needs and media buying behavior:

- Expansion beyond retail: Commerce networks are moving into industries such as banking, travel and delivery services, increasing advertiser options and competition among networks.

- AI-driven planning access: Generative AI planning capabilities are democratizing access to commerce media networks, enabling more advertisers to activate and optimize campaigns.

- Measurement beyond ROAS: Rising media costs and cross-network orchestration are driving demand for improved measurement frameworks focused on new customers, retention and long-term category growth.

- Performance-led investment: Brands that sell through retailers are investing heavily in performance marketing tactics like retail media to drive online and in-store sales.

- Signal loss pressures: Cookieless environments and consumer-driven signal loss are pushing indirect-to-consumer brands toward new targeting and measurement data sources closer to the point of sale across digital and physical touchpoints.

- Programmatic enablement: Ad technology platforms are building supply relationships with commerce networks and their SSPs, allowing advertisers to access select networks programmatically through third-party DSPs.

- Off-site media expansion: Retail and commerce media networks are extending into streaming, social and walled-garden environments such as Meta and Google, creating new off-site advertising opportunities.

Obstacles

- Lack of standardization and cost pressures: Proliferation of networks has created inconsistent attribution measurement standards, and rising CPMs make it difficult for advertisers to manage frequency, compare performance and scale investment efficiently.

- Network effects concentration: Advertisers must select from larger networks with scale at a higher price point, or diversify in multiple networks that may be less costly but lack efficiency and scale.

- Scale and profitability challenges: While digital marketing leaders value the targeting accuracy of commerce media, reaching audiences at scale and driving profitable growth remain difficult outside of the largest network partners.

- Budget and data constraints: The rapid growth of retail and commerce media is straining brand media budgets, while evolving privacy regulations and cookieless environments limit data availability for targeting and measurement.

User Recommendations