Magic Quadrant for Higher Education SaaS Student Information Systems

31 March 2026 - ID G00833213 - 44 min read

By Robert Yanckello, Grace Farrell

Cloud/SaaS student information systems adoption has reached a tipping point. Vendor solutions are advancing while institutions struggle to modernize due to budget limits, legacy models and poor cross-unit collaboration. Higher education CIOs can use this research to assess and navigate the market.

Strategic Planning Assumption

By 2031, more than 50% of higher education institutions will have fully migrated to SaaS student information systems (SISs).

Market Definition/Description

Gartner defines student information system (SIS) software as a service (SaaS) as a core system of record for higher education institutions that serves as the central hub for storing, organizing and processing student academic and administrative activities. The SIS supports student, faculty and staff-facing functionality, including management of information assets, while also supporting back-end administrative functionality. SIS SaaS is delivered under a pay-for-use basis or as a subscription license model (with regular updates), where application support and infrastructure provisioning and management are the responsibility of the vendor.

Serving the students, faculty and administrative staff, the SIS provides a chronology of business transactions, academic activity, advising interactions and educational outcomes. Additionally, it manages vital information assets, including course offerings, course catalogs, course registration, student accounts, financial aid, grades and transcripts throughout the student life cycle. The SIS may be part of a larger administrative ERP application suite and a critical component of an education institution’s larger digital technology platform.

Mandatory Features

The must-have capabilities for this market include:

- Course catalog

- Course registration/scheduling

- Degree audit

- Enrollment and matriculation management

- Grades and transcripts (that is, an academic record)

- Student accounts (that is, bill presentment and payment)

Common Features

The optional capabilities for this market include:

- Academic advising

- Admission processing

- Attendance tracking

- Curriculum management

- Delivered integration services

- Financial aid

- Operational and regulatory dashboarding/reporting

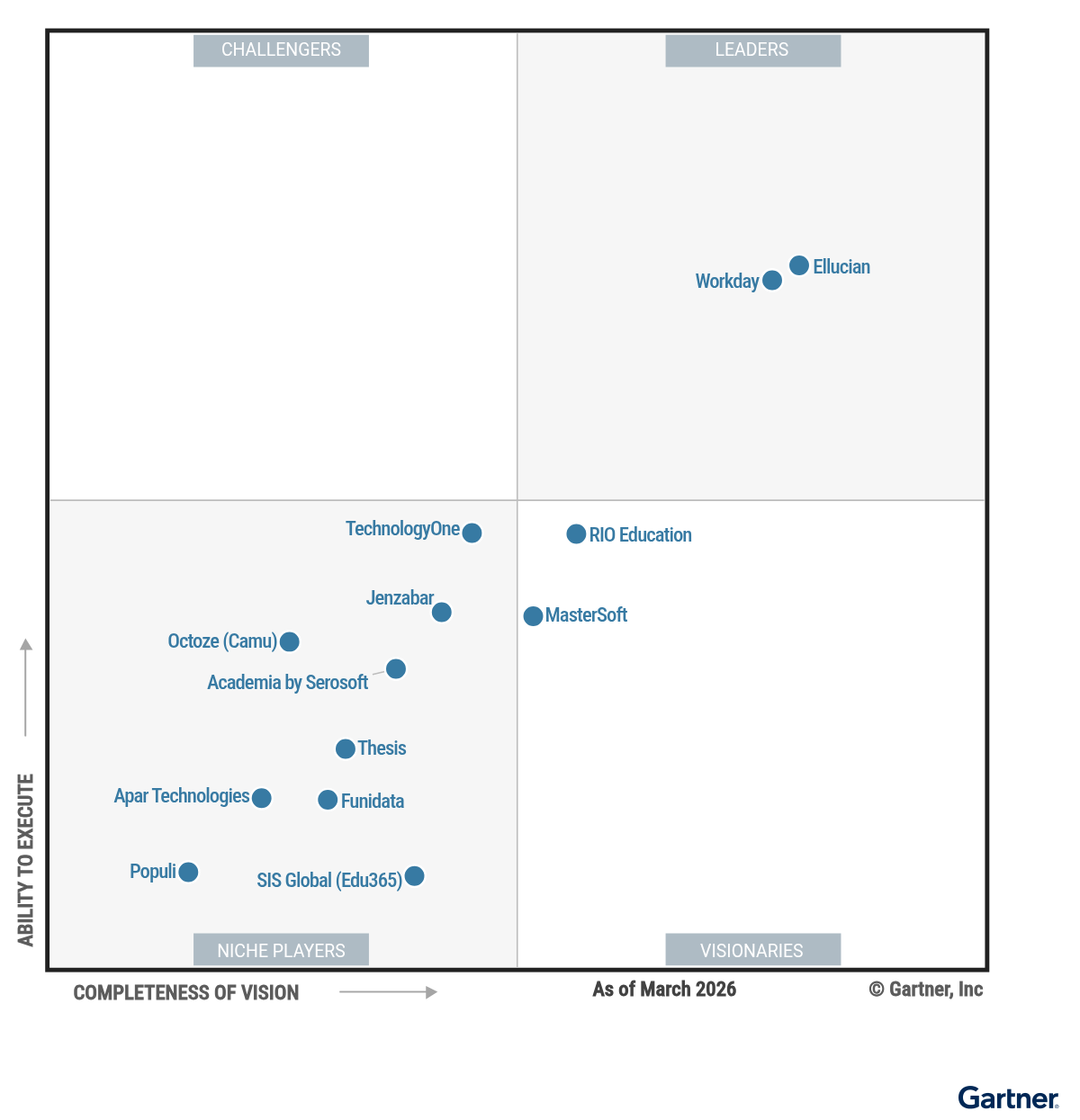

Magic Quadrant

Vendor Strengths and Cautions

Academia by Serosoft

Academia by Serosoft is a Niche Player in this Magic Quadrant. It is a privately owned company headquartered in Indore, India. The vendor offers Academia SIS, an all-in-one SIS, enterprise resource planning (ERP) and CRM solution serving midsize-to-large institutions globally. It has a large footprint in EMEA and Asia/Pacific. The platform is designed for interoperability and rapid implementation.

The vendor’s roadmap includes agentic AI for student services, AI-driven reporting and compliance frameworks for the Middle East and North America to aid market expansion. The vendor plans to grow by targeting corporate education organizations with 1,000 to 10,000 students. The platform supports multiple languages, including English, Spanish, French and Arabic.

- AI innovation: The vendor has rapidly integrated AI-driven analytics and visual reporting tools into the Academia SIS platform. The AI-first vision provides a forward-looking roadmap that enables institutions to leverage predictive analytics for student retention and automate routine administrative tasks without needing third-party business intelligence tools.

- Configurable architecture: A key differentiator is the platform’s rule-driven configuration engine, which separates business logic from the application code. This “low-code” architecture allows institutions with complex multicampus or multicountry organizations to independently configure academic rules, grading schemas and fee structures via the UI, significantly reducing reliance on the vendor for hard-coded customizations.

- Fee-based trial: The vendor provides a fee-based demo environment that enables clients to focus on essential operational areas while evaluating key features and integrations of the solution. This model allows prospective clients to validate critical functionalities in a proof-of-concept environment, minimizing risk and ensuring the solution aligns with their needs prior to a long-term commitment.

- Smaller scale: Academia by Serosoft operates at a smaller scale than the Leaders in this Magic Quadrant, even though the company is profitable and debt-free. This lack of scale could limit the long-term capacity to fund and support the global development and infrastructure required to compete globally.

- Limited competitiveness: The vendor’s limited marketing budget and underdeveloped growth and partner strategies put it at a disadvantage when entering competitive regions like North America and Europe, compared to established legacy providers. Customers in these markets may experience slower innovation, support gaps or limited local resources.

- Conflicting market priorities: The vendor’s attempt to serve both cost-conscious emerging markets and complex large-scale institutions leads to conflicting product priorities, such as affordability and simplicity versus compliance and complexity. This can result in unfocused product development that fails to meet the needs of either market.

Apar Technologies

Apar Technologies is a Niche Player in this Magic Quadrant. It is a privately held company headquartered in Singapore. It offers eLite SIS HD, an all-in-one solution built on Microsoft Dynamics 365, targeting midsize institutions (fewer than 10,000 students). The vendor operates primarily in the Asia/Pacific and Middle East regions. The platform encompasses SIS, CRM and analytics capabilities.

The vendor’s roadmap focuses on AI-driven analytics, Microsoft Copilot chatbots, omnichannel communication tools, enhanced integration capabilities and advanced security features. Currently available in English, the vendor plans to add multilingual support to facilitate growth into North American and European markets.

- Customizable platform: Apar’s eLite SIS HD is driven by a flexible platform built on Microsoft Dynamics 365 that lets users adjust workflows to match unique operational requirements.

- Modular product: The product modularity enables institutions to adapt and scale at their own pace across a broader composable platform. The solution is offered unbundled, giving customers the option to purchase only the modules they find valuable instead of the full suite.

- Targeted sales strategy: Apar’s sales strategy displays a clear approach to targeting midsize institutions in the Asia/Pacific and Middle East regions. It offers an attractive pricing model that demonstrates a detailed understanding of the Asia/Pacific region’s needs and how to successfully navigate it.

- Capability gaps: While eLite SIS HD has addressed several functionality gaps, it still lacks key standard capabilities in some areas, including student accounts and billing, degree auditing, enrollment/matriculation management and region‑specific regulatory reporting.

- Inadequate marketing strategy: Apar lacks significant brand awareness in major expansion targets like North America and Europe. Apar needs more effective campaigns and brand differentiation to compete against established global players.

- Misaligned growth strategy: Apar’s growth aspirations do not align well with committed resources or metrics regarding expansion. Its small footprint outside of Asia/Pacific, lack of global partner programs and narrow regional regulatory capabilities point to limited success in global expansion.

Ellucian

Ellucian is a Leader in this Magic Quadrant. It is a privately held company based in Reston, Virginia, U.S. Ellucian now offers a single unified product — Ellucian Student. This product unifies its previous products Banner SaaS and Colleague SaaS and serves a diverse global client base with a dominant presence in North America. As a comprehensive ERP/SIS provider, Ellucian targets institutions of all sizes, from community colleges to large research universities.

Ellucian’s roadmap focuses on advanced development of the SaaS platform, agentic AI for workflows and improving global regulatory compliance. Recent strategic moves include the acquisition of Anthology’s SIS and ERP assets to consolidate market leadership. The platform supports multiple languages, including English, French, Spanish and Arabic.

Ellucian closed its acquisition of Anthology’s SIS and ERP assets on 31 December 2025. Ellucian states Anthology customers will continue operating as they have preacquisition. Anthology systems, support channels and day-to-day workflows remain unchanged. However, Ellucian has shared its intent not to sell the Anthology platform to new clients; therefore, Anthology was dropped from this research.

- Comprehensive capabilities: Given its longstanding market life and product acquisition history, robust product capabilities remain a significant strength. Its comprehensive SaaS platform architecture covers the end-to-end student life cycle, including common features like financial aid and degree planning.

- Deep market knowledge: Ellucian’s deep expertise in the higher education domain and long experience serving a variety of different market segments point to its broad understanding of the market and ability to distinguish and address client expectations. The vendor combines this with extensive client feedback to gain thorough market knowledge and plan relevant roadmaps.

- Strong market responsiveness: Ellucian’s sensitivity to evolving market dynamics is evident in its “student-first” deployment strategy instead of the traditional “ERP/HCM-first” approach. Additionally, it has introduced deployment services that leverage business capabilities using its Customer Architecture Reference Model (CARM), as well as platform tools for regulatory reporting to make it easier for clients to adapt to evolving market dynamics and expectations.

- Unclear customer deployments: The number of institutions fully “live” on Ellucian SIS is unclear, even though it reports growth in customer base. Its pipeline includes both new and upgrading (modernization) clients. Without a clear, objective definition of “live” or “in production” customers, prospective customers lack visibility into real adoption levels.

- Postacquisition uncertainties: Customers could face uncertainties during the transition phase following the vendor’s recent acquisition of Anthology’s SIS and ERP assets. Additionally, it is yet to be seen if Ellucian’s increased scale and market share will drive favorable outcomes and translate into competitive pricing and fee models for customers.

- Complex delivery model: Migrations or deployments of Ellucian SIS require considerable assessment, planning and change management. The overhauled partner programs entail more involvement from third-party integrators during negotiations. It is critical to clarify details between professional services and partners to ensure timely and optimized project delivery.

Funidata

Funidata is a Niche Player in this Magic Quadrant. It is a private limited liability company owned by nine Finnish universities; its headquarters are in Helsinki, Finland. Funidata provides Sisu, a SaaS SIS designed for Finnish universities and cross-institutional consortiums. The solution prioritizes interoperability, visual degree planning and seamless cross-study capabilities.

The vendor’s roadmap features AI-powered analytics (using LLMs), automated scheduling optimization and a mobile app with near-field communication (NFC) capabilities. Sisu is designed to support the specific needs of the Finnish and European higher education frameworks. The platform supports Finnish, Swedish and English, with plans to add more languages as it expands to Africa and other parts of Europe.

- Regional support: Funidata is committed to delivering regional value to customers via continuous updates and scalable software. The offering is a solution purpose-built for the regulatory and operational needs of the Finnish and European higher education sectors.

- Strong client understanding: Funidata’s product capabilities and roadmap demonstrate a thorough understanding of its current client needs. Its focused strategy reflects effective efforts to position Sisu within its target Nordic, African and broader European markets.

- Strong viability: The solution is financially supported by a stable group of nine Finnish universities. With positive cash flow, no debt and a modest pipeline, it is well-positioned as a viable solution in this market. Since the owners are also customers of the product, this solution stands a good chance of remaining relevant in the long term, because real users are involved in its development and evolution.

- Limited global capabilities: In the broader global context, Sisu is narrowly focused. It lacks common capabilities in some areas, including student accounts and billing, as well as region-specific regulatory reporting required by international markets.

- Narrow market focus: Funidata has a more narrow view of the market, reflecting its niche focus, rather than a broad view of the global higher education landscape outside its home region. This may make its growth plans to expand into other regions, such as Africa and other European places, less competitive.

- Limited roadmap: Funidata’s product roadmap is not fully developed and focuses on administrative use cases and common functionalities, which largely serve the needs of Finnish universities. Therefore, the vendor needs a broader functional roadmap to appeal to institutions outside Finland.

Jenzabar

Jenzabar is a Niche Player in this Magic Quadrant. It is a privately held company based in Boston, Massachusetts, U.S. Jenzabar offers Jenzabar One and Jenzabar SONIS, primarily targeting U.S. private and public institutions with under 10,000 full-time equivalent students (FTEs; see Note 1). Jenzabar One provides a complete ERP/SIS suite, while Jenzabar SONIS does not and serves smaller, specialized schools.

The vendor’s roadmap priorities include a fully web-based interface for Jenzabar One, generative AI for predictive analytics and communications, and a new workflow automation module. Jenzabar has combined resources and strategies to optimize sales and services, but maintains distinctions in product development and capabilities for its two SaaS SIS offerings. The solutions are currently available in English.

- Customer-centric solutions: Jenzabar demonstrates deep knowledge of the needs of small-to-midsize U.S. institutions and delivers tailored solutions for the industry segment. This focus ensures that its products align with their clients’ specific needs and can easily adapt to an institution’s business requirements.

- Good viability: Jenzabar has positive cash with no debt, reflecting a stable financial position and a consistent track record in the small-to-midsize institution market. The two Jenzabar solutions are well-positioned to capture new opportunities from higher education institutions that are running SIS products from other providers that are no longer available on the market.

- Proactive customer support: Jenzabar provides robust education resources for customers. It fosters an active user community for engaging with the unique challenges and requirements of its clients. The vendor’s monthly office hours activity is unique and provides opportunities for customers to engage with development teams, provide feedback and leverage live training.

- Geographic and language limitations: Jenzabar remains primarily focused on the North American market with limited international expansion or localized support. Additionally, its geographic expansion plans are focused on English-speaking schools and regions.

- Near-term roadmap: Jenzabar’s near-term roadmap is focused on platform- and web-based enhancements. Therefore, it may not be able to keep pace with the rapid AI advancements required to meet client and prospect expectations.

- Lack of continuous delivery: Although SaaS-based, Jenzabar does not support continuous delivery of new functionalities. Product enhancements are delivered using traditional installation packages for each part of the Jenzabar platform, then deployed to test and production environments.

MasterSoft

MasterSoft is a Visionary in this Magic Quadrant. It is a privately held company headquartered in Nagpur, India. It offers a SIS that serves multicampus and midsize-to-large institutions in India, the Middle East and southeast Asia. The all-in-one platform is built to manage the entire student life cycle. MasterSoft’s SIS solution includes admission, ERP, LMS and alumni modules. It can be deployed in a multitenant or private-tenant environment.

The vendor’s roadmap investments focus on an AI “intelligence layer,” microcredentialing and region-specific compliance packs for planned expansion into the U.S. and EMEA. Near-term growth plans target multicampus groups and non-profits (300 to 5,000 students) in the U.S. and EMEA. The solution supports multiple languages, including English and Arabic.

- Customer support and flexibility: MasterSoft allows customers to choose their cloud, AI and data geography. It also offers an “online-offline” capability with apps that autosync when connected. The vendor’s structured support includes a Hypercare support service during go-live and peak academic periods, which ensures that any issues are triaged daily.

- Strong AI features: Mastersoft is adapting its compliance-first platform to new regulatory frameworks and AI-native requirements. Its “agentic campus OS” vision is ambitious and demonstrates proactive engagement with evolving AI technologies. The vendor also offers “bring your own AI model” capabilities that allow institutions to plug in preferred LLMs.

- Local partner support: Mastersoft’s strong partner network and co-sell model let local partners manage sales and implementation, while Mastersoft oversees governance and architecture. Customers benefit from local expertise and support, with the assurance of consistent quality and oversight.

- Geographic limitations: MasterSoft is yet to develop mature geographic strategies in Western markets. Its expansion into North America is currently focused on specific market segments (nonprofits with 300 to 5,000 students), limiting the solution’s immediate suitability for large or midsize institutions in that region.

- Regional focus: MasterSoft’s focus on growth markets may limit its ability to deliver solutions that meet the broader needs of global enterprises. Customers in the global enterprise sector could face gaps in MasterSoft’s features, scalability or international compliance, compared to offerings from global providers.

- Limited capabilities: To compete globally, Mastersoft will need to deepen the product’s functionality. It lacks key standard capabilities in some areas, including student accounts and billing, degree auditing, Web Content Accessibility Guidelines (WCAG) compliance and region‑specific regulatory reporting in target markets.

Octoze (Camu)

Octoze is a Niche Player in this Magic Quadrant. It is a privately held company based in Singapore. The vendor’s solution, Camu, is an all-in-one mobile-first SIS and LMS solution targeting education institutions in Australia, India, southeast Asia and the Middle East. It is suitable for midsize-to-large higher education institutions seeking a comprehensive, mobile-native platform. The platform’s end-to-end student life cycle model supports various academic models, including outcome-based education (OBE).

The vendor’s roadmap includes AI-assisted content creation, grading automation and conversational bots on WhatsApp. The solution supports multiple languages, including English, Arabic, Spanish and French.

- Geographic expansion: Octoze’s Camu has successfully expanded across India, Southeast Asia and the Middle East, demonstrating adaptability to diverse markets. It has a growing list of partners in North America and has already secured an opportunity in Texas, U.S. via a Texas Department of Information Resources (DIR) education IT contract.

- Student-centric innovation: Octoze’s roadmap is focused on optimizing student functionality and engagement. It is reflective of the vendor’s ability to quickly adapt its flexible platform capabilities to projections, workflow approvals and conversational bots on WhatsApp.

- Strong viability: Camu’s financial stability — evidenced by no external debt, positive cash flow and consistent revenue growth — reduces risk for customers. Also, Octoze’s business model demonstrates strong growth potential.

- Product strategy challenges: Octoze lacks capabilities in specific functional areas, such as student accounts, regulatory reporting and advising, which are required by large complex institutions. Additionally, the roadmap relies on partner-led localizations for new markets, which carries more risk compared to vendors with established regulatory capabilities.

- Limited competitiveness: Camu’s sales strategy relies heavily on displacing established legacy vendors in small-to-midsize institutions, making it harder to win deals in markets where larger incumbents are seen as the “safe choice.” Customers should consider potential challenges with long sales cycles and resource allocation, as Camu scales direct sales globally and manages disparities in deal sizes.

- Limited resources: Camu has smaller scale and limited R&D and marketing budgets, compared to leaders in this research. Its size and resources impose structural limits on its ability to outinvest competitors in R&D, marketing and global support. The company operates with a small core team while attempting to support a complex product across multiple time zones and regulatory environments. Customers should be aware of potential limitations in product innovation, service and support.

Populi

Populi is a Niche Player in this Magic Quadrant. It is a privately held company based in Moscow, Idaho, U.S., and offers Populi, an all-in-one cloud SIS that includes LMS, financials and admissions. The solution specifically serves and targets small colleges (fewer than 1,000 FTEs [see Note 1]) and seminaries in North America. Populi offers a straightforward monthly pricing model.

Populi does not release a formal roadmap; however, recent updates include AI-generated video subtitles and features to maintain ease of use for small administrative teams. Populi is available in English.

- Strong customer experience: Populi manages all implementations and customer support in-house, ensuring consistent quality of service and accountability. Also, the solution’s design allows for rapid deployment, where clients can often log in and begin configuring their environment immediately. It significantly shortens the time to value compared to traditional SIS deployments.

- Transparent monthly pricing: The vendor’s standard pricing is publicly available on its website and is very transparent. This eliminates the complexity of typical enterprise software negotiations. Populi offers month-to-month contracts, rather than locking institutions into multiyear agreements. This lowers the barrier to entry and aligns the vendor’s incentives with ongoing customer satisfaction and retention.

- Strong viability: Populi demonstrates a highly stable and sustainable financial profile for its business model targeting small colleges. The vendor operates with no debt and relies on a recurring revenue model driven by monthly subscriptions, which allows for rapid, subscriber‑driven investment in product development and support.

- No published roadmap: Populi does not publish a formal product roadmap and relies on a feature-driven development model based on immediate customer feedback. Also, its conservative approach to emerging tech, including a limited AI vision, makes it unsuitable for customers who expect the latest AI capabilities.

- Community insights: Populi’s reliance on word of mouth and limited marketing means its brand visibility is low compared to competitors. Customers will find fewer user communities, resources or peer references available to support the platform’s use.

- Limited product flexibility: Populi lacks the depth of configurability, hierarchy management and advanced features required by complex institutions and multicampus organizations. The solution is explicitly designed for a niche segment consisting of small colleges and seminaries.

RIO Education

RIO Education, a subsidiary of WDCi, is a Visionary in this Magic Quadrant. It is a privately held company headquartered in Queensland, Australia. Its product, also named RIO Education, is a Salesforce-native SIS. It is available on the Salesforce AppExchange, as part of the Salesforce ecosystem. The solution targets diverse institution sizes and types that use Salesforce and serves clients in North America, the U.K., Australia/New Zealand and Europe.

RIO Education’s roadmap focus includes external AI interfaces, enhanced curriculum management and an “any cloud” deployment option to run independently of Salesforce Education Cloud Data Architecture or Education Data Architecture. The platform supports multiple languages, including English, Spanish, French and Mandarin.

- Platform independence: RIO Education leverages its “any cloud” architecture to run natively on the Salesforce platform while maintaining independence from Salesforce’s EDA and Education Cloud data models. This allows institutions to utilize the robust security, workflow automation and accessibility features of Salesforce without being locked into Salesforce’s shifting higher education product roadmap.

- Regulatory compliance across regions: The solution demonstrates strong agility to meet diverse regional regulatory requirements, supporting a global client base across the U.K., Australia, Spain, Canada and the U.S.

- Multilingual translation: The vendor has developed a unique “long-text translation” module, which enables dynamic translation of data (e.g., course descriptions) rather than just field labels, differentiating it for multilingual global institutions.

- Limited brand visibility: RIO Education’s brand recognition is limited outside of the Salesforce ecosystem. Due to limited resources, its marketing strategy is mostly dependent on leads from the Salesforce AppExchange and consultant referrals, reducing its recognition.

- Limited human resources: The vendor’s staffing model is lean, with only around 30 full-time staff members dedicated to product development and support. This is a significantly smaller resource pool than many of its competitors. It can impact the vendor’s long-term capacity to support a rapidly expanding global client base across multiple time zones and regulatory environments.

- Inconsistent sales: RIO Education’s indirect sales model is still developing and its direct sales team is resource-constrained. Additionally, its partner channel is yet to mature and it faces sales challenges due to the dependency on the Salesforce ecosystem. All these lead to difficulties in consistently closing deals.

SIS Global (Edu365)

SIS Global is a Niche Player in this Magic Quadrant. It is a privately held company located in Ebene, Mauritius. SIS Global offers Edu365, built on Microsoft Dynamics 365, and it primarily serves universities and business schools in EMEA. The solution covers the full student life cycle and leverages the Microsoft ecosystem for ERP capabilities.

The vendor’s product roadmap includes an AI autonomous employee framework, enhanced alumni outreach and research management modules. SIS Global is focused on higher education digital transformation based on the Microsoft technology stack. The platform supports multiple languages, including English, French, Spanish and Dutch.

- Access to Microsoft stack: Edu365 is built directly on Dynamics 365 and Dataverse. This enables clients to leverage the full Microsoft stack, including Power BI, Power Automate and Copilot, without complex middleware. The offering facilitates a low-code/no-code environment that can extend the system, configure reports and modify workflows using standard Microsoft tools.

- Data and regulatory compliance: SIS Global offers a unique single-tenant option within the institution’s own Azure environment, alongside standard multitenant deployments. This is appealing for organizations with strict data sovereignty and security requirements that generic multitenant SaaS cannot meet. Additionally, the solution offers prebuilt regulatory packs for markets like South Africa and the U.K.

- Responsive to market needs: The vendor serves the needs of organizations committed to the Microsoft ecosystem by focusing on smooth Microsoft integration, data sovereignty, the future trajectory of agentic AI and global compliance requirements. It addresses budget constraints across the sector by offering flexible licensing that enables clients to leverage the Microsoft ecosystem, where it makes sense, to lower entry barriers.

- Third-party partnership: While the vendor utilizes a hybrid sales model, its indirect channel is limited. SIS Global does not certify its partners, and their formal ecosystem for third-party delivery is not as robust or standardized as their competitors. It relies on its own resources for quality assurance, which could create bottlenecks as the vendor scales globally.

- Limited brand visibility: SIS Global’s marketing execution lacks a broad view, which limits its recognition outside of its established regions such as Africa, Europe, Latin America and North America. The vendor’s marketing strategy is heavily dependent on the Microsoft partnership and co-sell opportunities, rather than independent brand recognition. Therefore, institutions not deeply invested in the Microsoft ecosystem may overlook Edu365 entirely.

- Risky global expansion: SIS Global is ambitiously targeting simultaneous expansions into multiple markets, such as eastern Europe, the U.K., the U.S., Canada and Latin America. This raises concerns about scaling resources, partner capabilities and partner network maturity. Without a rigorous certification mechanism, partners may not be able to successfully navigate the intricacies of the Edu365 platform and local regulatory requirements.

TechnologyOne

TechnologyOne is a Niche Player in this Magic Quadrant. It is a public company headquartered in Brisbane, Australia. The vendor offers Student Management as part of its Connected Intelligence Anywhere (CiA) cloud/SaaS platform and the OneEducation solutions suite. It serves institutions across a broad range of sizes and types, but primarily focuses on large technical and further education (TAFE) and higher education institutions in Australia/New Zealand and the U.K.

The vendor’s innovation focuses on contextual and conversational AI and the deep integration of recent acquisitions like CourseLoop (curriculum management) and Scientia (timetabling/scheduling). Its growth plans are focused on the United Kingdom. The platform is available in English.

- Serves dual-sector needs: The solution supports the unique dual-sector needs of the U.K. and Australian markets, handling both higher education and TAFE requirements within a single platform. The platform achieves this via OOTB functionalities enhanced by its recent acquisition and integration of tools like Scientia and CourseLoop, and strong configuration capabilities.

- Australia- and New Zealand-specific support: TechnologyOne’s strong focus on the Australian education model makes it highly specialized for Australia/New Zealand institutions. Its native compliance supports complex local standards, such as TCSI in Australia and Data Futures compliance in the U.K., which positions it as an alternative to U.S.-centric vendors that often require heavy localization.

- Strong viability: TechnologyOne is a publicly listed company with a strong financial profile. It has a strong market position in Australia/New Zealand and a disciplined expansion strategy. The vendor reports no external debt, positive cash flow and consistent revenue growth, which is projected to rise next fiscal year.

- Narrow geographic reach: The vendor focuses only on the U.K. and Australia/New Zealand markets, with no current SIS sales operations in North America. Its core SIS is not marketed globally, even though it may explore the U.S. market via acquisitions or point solutions like CourseLoop.

- Limited revenue potential: The vendor’s growth is restricted by a focus on just two regions. This limited market reach caps revenue potential, compared to competitors that cover North America, Europe and Asia simultaneously. Customers should be aware this may affect future investment, innovation and long-term support.

- Scaling challenges: The vendor operates with no implementation partners, choosing to perform all deployments in-house to control quality and manage the “SaaS+” delivery model. While this ensures accountability, it creates a potential bottleneck for scaling support and service delivery and achieving rapid growth when SIS demand spikes in markets like the U.K.

Thesis

Thesis is a Niche Player in the Magic Quadrant. It is a privately held company and a completely virtual organization. Thesis provides Elements, a cloud-native SaaS SIS for small-to-midsize (500 to 5,000 FTEs [see Note 1]) institutions in the U.S. and Canada. The solution is delivered via Microsoft Azure in a multitenant SaaS environment and includes an integration platform.

The vendor’s roadmap emphasizes agentic AI workflows using natural language, borrower-based aid processing and a new data query tool. Its production deployments have doubled over the past year. The solution is available in English, Spanish and French.

- Optimized sales strategy: Thesis uses a disciplined sales strategy, focusing on small-to-midsize institutions (500 to 5,000 FTEs [see Note 1]) with primarily modernization needs, especially those moving from its CAMS product or from Ellucian PowerCampus. By targeting a sharply defined customer segment and specific services, it avoids overextending resources and delivers solutions that are rightsized and aligned with client expectations.

- Strong customer outreach: Thesis has built strong brand awareness and community engagement through focused campaigns and an annual conference for users. Its personalized webinars make it easier for clients migrating from rival platforms to modernize. Customers also benefit from direct access to experts who understand the unique needs of small colleges.

- Faster integration and flexibility: Elements is a multitenant, cloud-native SaaS platform on Microsoft Azure, enabling fast implementations in about 10 months. Its built-in integration layer offers prebuilt connectors for common higher education tools like LMS and CRM. Therefore, customers can get “best-of-breed” features, reducing customization needs and lowering professional services costs.

- Automation and workflow: Elements lacks a native workflow orchestration engine and a business rule engine within the core product. While the system is configurable, this architectural limitation forces institutions to rely on the integration platform or third-party tools for complex process automation, rather than handling it natively within the SIS.

- Limited financial growth potential: The vendor has a relatively small SaaS installed base and a target market of small colleges that face significant budget constraints and risk of closure. Therefore, the vendor’s long-term financial growth potential is more constrained than some of the broader market providers.

- Limited global presence: Thesis has no plans to expand into Europe, Asia/Pacific or the Middle East. While it is exploring opportunities in the Caribbean and Latin America via partners, it lacks the global localization capabilities, language support and partner networks required to compete internationally.

Workday

Workday is a Leader in this Magic Quadrant. It is a publicly traded company headquartered in Pleasanton, California, U.S. The company offers Workday Student, a unified cloud platform combining HCM, ERP/finance and student applications. It serves institutions of all sizes in North America, with expansion plans for Australia/New Zealand, the U.K. and Ireland. Workday targets the full spectrum of higher education, from community colleges to research-intensive (doctoral) universities.

The vendor’s roadmap priorities include agentic AI for administrative efficiency, globalization capabilities (localization for new regions) and an optimized registration experience. The solution is currently available in English.

- AI innovation: Workday is advancing from basic automation to agentic AI through its Workday AI engine. Leveraging companywide R&D, the SIS now delivers faster AI-driven solutions for some administrative tasks. It also has plans to use AI for tasks like transfer credit evaluations and advising, and to introduce specialized agents, such as the Student Administration Agent, in the next 12 months.

- Strong market understanding: Based on its market vision, Workday offers a unified, cloud-native platform that connects HR, finance and student data across campus, reducing product silos. Additionally, its roadmap is shaped by ongoing input from student user groups and design partners to ensure alignment with dynamic user needs.

- Strong brand presence: Workday has a powerful brand presence and industry alliances that position it as a transformation partner. Workday’s marketing strategy leverages third-party market research to validate messaging and understand client purchasing habits. This enables it to adjust its messaging and resonate effectively with higher education IT leaders.

- Bundled sales: Workday’s bundled platform requirements act as a high barrier to entry. To use Workday Student, institutions must commit to the full platform (HCM and finance), creating a large initial cost and implementation scope that can deter institutions looking for a stand-alone SIS or organizations with lower budgets.

- Geographic strategy: Workday Student mainly focuses on North America and currently supports only English, with French Canadian and Spanish translations coming in late 2026. It has been slow to expand into Australia/New Zealand; entry into the U.K./Ireland markets is not planned until 2027. This cautious rollout leaves Workday behind competitors with established local clients.

- Compliance complexities: Workday relies on partners and the “Built on Workday” apps for regulatory compliance reporting and regional localizations. This approach can add complexity, especially for international clients. Customers may face more challenges compared to vendors with built-in, region-specific compliance capabilities.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

- Funidata

- MasterSoft

- Octoze (Camu)

- Populi

- SISGlobal (Edu365)

- TechnologyOne

Dropped

- No vendors were dropped from this year’s Magic Quadrant.

Inclusion and Exclusion Criteria

Gartner’s Magic Quadrant report identifies and analyzes the most relevant providers and products in the higher education SaaS SIS market. The inclusion criteria represent the specific attributes that Gartner analysts believe are necessary for inclusion in this research.

To qualify for inclusion, providers needed to demonstrate they met the following criteria:

Business criteria:

- Revenue: Each vendor’s SaaS SIS offering must have generated revenue of at least $2 million, be generally available, and the vendor must have at least five SaaS SIS customers in production in the 12 months leading up to 31 August 2025.

- Sales: Each vendor had to have been selling and branding a SaaS SIS to a tertiary, degree-seeking institution since at least December 2024.

- Go-to-market approach: Each vendor’s go-to-market approach must explicitly mention its SaaS SIS in its go-to-market activities, such as positioning, marketing, messaging, pricing and packaging for its SaaS SIS. Vendors must be able to present aspects such as thought leadership, product marketing and management, public presentations, events, customer experience, partner channel, word of mouth and sales strategy.

- Licensing: Licensing for the SaaS SIS product must be on a subscription basis or pay for metered use arrangement. SaaS subscription includes contract value (CV) for a calendar year, but excludes any services included in an annual contract. For multiyear contracts, only the CV for the first 12 months is considered.

Product Criteria:

- The vendor must have a separate and distinct SKU (stock keeping unit) that clearly identifies a SaaS SIS product.

- The SaaS SIS must be able to deliver on all capabilities:

- Manage enrollments: Student records, status changes, registration, degree audit, graduation processing, transfers, grades, academic history.

- Student accounts: Tuition and fees, billing, payments and refunds.

- Composability: Modular architecture that can be deployed and integrated alongside other applications or platforms outside the primary SaaS SIS application suite to fulfill a composable business strategy. This includes, but is not limited to, the extension of the data model and/or functionality and the ability to consume, provide and exchange data/metadata.

This Magic Quadrant does not cover the following type of offerings:

- LMS applications and/or functionality

- HCM and finance (aka ERP solutions) applications and/or functionality

- CRM applications and/or functionality

- Continuing education and workforce development (CE/WFD) solutions and/or functionality

- Student degree-planning applications and/or functionality

Evaluation Criteria

The evaluation criteria are composed of the Ability to Execute and Completeness of Vision. The criteria and weights describe the specific characteristics and their relative importance that support Gartner’s view of the market. These criteria are used to comparatively evaluate SIS SaaS providers in this research.

Ability to Execute

Gartner evaluates vendors on their Ability to Execute by examining how effectively they deliver and support a SaaS SIS solution that enables institutions to meet both their current operational requirements and their future modernization objectives. This includes an assessment of the functional depth and maturity across the vendor’s product portfolio, with particular focus on capabilities required to administer and manage student enrollment records.

Gartner also considers the methods and resources vendors provide to help institutions deploy, maintain and evolve their SIS; the level of staff education and training programs; and the extent to which vendors promote best practices across the end‑to‑end student life cycle.

Vendors are further evaluated on how well their market presence and communication efforts reflect the strength and significance of their product vision. This is demonstrated through the scale and engagement of the active customer base, customer and market recognition and the likelihood that institutions will extend their use of the solution through expanded functionality or broader institutional growth.

The following criteria are the most influential factors within the Ability to Execute dimension: product or service, overall viability, market responsiveness and track record, customer experience and operations receive high weightings. Institutions place a strong emphasis on the richness of product functionality, the vendor’s consistency in delivering on its roadmap, the satisfaction and outcomes reported by customers and the vendor’s capacity to operate effectively and efficiently during implementation and overtime in production.

Sales execution/pricing and marketing execution are important in signaling the vendor’s organizational health, its ability to offer solutions aligned to institutional value propositions at sustainable and competitive price points, and its overall positioning and visibility in the market.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | High |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | High |

Marketing Execution | Low |

Customer Experience | High |

Operations | High |

Source: Gartner (March 2026)

Completeness of Vision

Gartner evaluates a vendor’s Completeness of Vision by examining how well the vendor understands current market trends and how effectively it articulates a forward-looking vision for the SIS market. This includes the vendor’s perspective on emerging technologies, its ability to enhance the effectiveness of the SIS, its approach to driving software adoption and how it responds to customer needs and competitive dynamics as Gartner views them.

Vendors must clearly communicate to Gartner and to the market a three-to-five-year strategic direction that aligns with Gartner’s expectations for the evolution of SaaS-based SIS solutions. This vision should demonstrate a strong grasp of the major technological and architectural shifts affecting the market and present a credible, actionable roadmap for leveraging these shifts to deliver relevant solutions.

The criteria for market understanding, offering (product) strategy and innovation assess how well a vendor envisions the SIS supporting institutional modernization, as planning and operations increasingly converge across the student life cycle and extend into a composable enterprise ecosystem. These areas often highlight key differentiators among vendors.

Criteria for sales strategy and geographic strategy are important in evaluating a vendor’s investment priorities and growth plans, including the ability to support a diverse customer base across education providers and regions.

Finally, business model and marketing strategy tend to have less influence on clients’ purchasing decisions in this market.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Low |

Sales Strategy | Medium |

Offering (Product) Strategy | High |

Business Model | Low |

Vertical/Industry Strategy | NotRated |

Innovation | High |

Geographic Strategy | Medium |

Source: Gartner (March 2026)

Quadrant Descriptions

Leaders

Providers in the Leaders quadrant have the highest combined measures of Ability to Execute and Completeness of Vision. They are performing well, are prepared for the near term and the future and have a robust and evolving understanding of the market. They are positioned to be responsive to dynamic market needs; offer products and services that enable clients to realize the value of their investment; and introduce and deliver new ways of bringing innovation to SaaS SIS. These new ways can include AI, embedded analytics, automation and user experience.

Challengers

Challengers offer functionalities across all the evaluated product capabilities, but they may lack the depth of Leaders in certain places like student-facing functionality, regional requirements or security. A Challenger’s product roadmap doesn’t expansively address the dynamic, emerging issues that the market requires. They tend to have a viable and proven solution, but focus on a specific size of institution or industry segment.

Visionaries

Visionaries have an ambitious and strong vision for the future and are making pointed investments to develop unique options in this market. They understand where the market is going or have a vision for changing market rules, but they have yet to take action that delivers on that understanding. Their solution is still emerging, and they have a handful of capabilities in development. Visionaries may have a developing customer base, but they might not yet serve a broad range of use cases.

Niche Players

Niche Players focus on a narrow view of the market, which makes their offering appropriate for a very specific market sector. They usually offer limited functional capabilities and a more simplified product experience in comparison to Leaders. They satisfy the product requirements through a basic set of functions, rarely demonstrate a target mid- or long-term vision and generally address a narrower scope of clients in certain geographic regions or more commonly, small to midsize institutions.

Context

The higher education SaaS SIS market is experiencing a pivotal moment of transformation. A convergence of digital imperatives like accelerated migration to cloud-based solutions, as well as vendor consolidation, enhanced integration capabilities and rapid innovation in AI, is reshaping the way institutions manage their SISs. In contrast to the traditional legacy systems, modern, composable platforms offer the promise of enhanced operational efficiency, improved student engagement and a more agile alignment with business capabilities and institutional strategic goals.

The current SIS transformation can be a digital enabler of institutional mission-critical functions and is driving the market momentum. This notable evolution in product strategy by vendors to flexible, composable platforms allows institutions to mix and match functionalities. This will enable higher education buyers to focus on integrating SIS with broader ERP systems, other campus technology and foster an ecosystem that supports end-to-end student life cycle management. This modular approach not only enables greater agility for an institution’s unique needs, but also facilitates continuous improvement and integration of new technologies, and it accommodates real-time analytics, robust security measures and continuous updates.

The future of the higher education SaaS SIS market appears promising, driven by several emerging trends. higher education CIOs and SIS leaders looking to invest wisely in SIS technology should consider:

- AI-driven student success initiatives: The integration of predictive analytics and AI-powered tools holds the potential to significantly improve student retention and academic performance. By leveraging data to identify at-risk students and personalize learning pathways, institutions can make more informed, proactive decisions.

- Mobile-first and personalized user experience: With a growing percentage of students and faculty relying heavily on mobile devices for day-to-day activities, SaaS vendors are increasingly focusing on designing intuitive, mobile-friendly interfaces that enhance user engagement.

- Business capabilities and composable platforms: The move toward modular, composable architectures built on business capabilities enables institutions to adopt best practices incrementally. This approach mitigates the risk of a massive, disruptive initiative while providing flexibility to reconfigure systems as needs evolve.

- Regulatory and security innovations: The inclusion of built-in compliance features and advanced cybersecurity measures is not only a market prerequisite, but also an opportunity for vendors to differentiate their offerings. Platforms are expected to offer enhanced, automated compliance reporting and real-time monitoring to counter emerging threats.

- Digital transformation and operational efficiency: Institutions are not merely looking for software to manage administrative tasks; solutions need to drive efficiency, enhance student engagement and ultimately generate improved academic and financial outcomes. A robust rule engine combined with strong configurability, interoperability and integration will enable business process functionality and ensure that the chosen platform can grow with the institution’s evolving needs.

Market Overview

The landscape of SISs for higher education is undergoing a profound transformation as institutions move toward modern, cloud-based offerings delivered through SaaS models. According to the Hype Cycle for Higher Education, 2025, the SaaS SIS market is emerging from the Trough of Disillusionment and approaching the Slope of Enlightenment, implying that SaaS SIS technologies are gaining more traction.

Institutions Are Spending More on SIS Modernization and Demanding More Capabilities

Globally, institutions are becoming more adept at deploying and leveraging these cloud offerings. Higher education CIOs are prioritizing investment in SIS/ERP modernization. This is evident in the increase in education software spending. (See Forecast: Enterprise IT Spending for the Government and Education Markets, Worldwide, 2023-2029, 4Q25.) Although some institutions continue to maintain their legacy on-premises solutions, virtually no one is looking to purchase that type of offering any longer.

In turn, vendors are making meaningful advances by designing solutions that capitalize on the operational efficiencies of SaaS. Since institutions are demanding more feature parity and new capabilities, vendors are continuing to develop new products and services to meet client needs.

Competition Is Reshaping Market Dynamics

In the past year, significant consolidation events have reshaped the competitive landscape. A notable example is Ellucian’s acquisition of Anthology’s SIS and ERP business (see Closed Corporate Transaction Notification: Anthology, Higher Education Student Information System SaaS). This transaction serves as a clear indicator of the pressure on vendors to consolidate resources, increase revenue and expand their product portfolios to offer more comprehensive solutions capable of addressing the evolving needs of higher education institutions.

SaaS SIS Markets Are Emerging

While the current SaaS SIS vendor landscape remains concentrated in North America and Europe, it is gradually expanding around the globe. A growing number of competitive offerings deliver robust capabilities to education providers that don’t require complex business functionality. In such cases, the institutions are satisfied with standard capabilities that introduce automation and expand digital experiences that were not part of their routine operations earlier.

Vendors Are Modernizing Services

As this evolution progresses, legacy vendors are very focused on the development and promotion of their SaaS/cloud offerings, while newer players highlight the native capabilities of their modern portfolio of products. Whether building on established platforms such as Salesforce or Microsoft Dynamics 365, blending older systems into new SaaS solutions, enhancing partner programs, supporting institutions with better migration planning, or iPaaS and BPM tools, the majority of vendors are moving toward enabling a composable business architecture.

As legacy vendors continue to retrofit older systems, newer cloud-native providers with modern architectures and rapid product adoption have opportunities to capture an increasing share of the market.

Challenges in Market Transformation

Despite the tremendous progress made by vendors in evolving the SIS market, many challenges continue to hinder the market’s transformation:

- Legacy system inertia: Many institutions have long relied on heavily customized, legacy systems that are deeply rooted in their operational workflows. The transition to a new, cloud-based platform requires significant process reengineering, which can be both costly and disruptive. Institutions often face internal resistance from stakeholders accustomed to the legacy environment, as well as practical challenges in migrating complex historical data.

- Resource constraints: Financial limitations and human resource shortages are common obstacles. Smaller institutions, while more agile in decision making, often struggle with limited IT budgets and insufficient technical expertise to manage large-scale digital transformations. Even larger institutions with greater resources may experience delays due to bureaucratic apathy and distributed decision making processes.

- Change management and stakeholder buy-in: The success of a transformation initiative is heavily dependent on effective change management and cross-unit collaboration. Institutions must invest in comprehensive training programs, robust communication strategies and stakeholder engagement initiatives to ensure that the benefits of a new cloud-based SIS are fully realized. Without clear accountability and measurable outcomes, resistance to change will undermine the overall transformation effort.

- Integration complexities: As SIS systems increasingly require integration with many other applications, each with their own data standards and protocols, the technical challenges associated with seamless integration become more pronounced. Institutions must not only ensure that the new platform can interface with existing systems, but also manage the risks associated with data consistency and security across a connected ecosystem.

Research for this Magic Quadrant was informed by:

- Client interactions between user organization clients and education analysts from November 2024 through January 2026

- Analysis of survey responses completed by the included vendors

- A vendor briefing and product demonstration from each featured service provider addressing capability proof points for the Magic Quadrant evaluation criteria

Note 1: Definition of Full-Time Equivalent Student

For this research, a full-time equivalent (FTE) student is a unit of measurement intended to represent one student enrolled full-time for one academic year. FTE student enrollment at the undergraduate and graduate levels is estimated using instructional activity data.

Ability to Execute

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships as defined in the market definition and detailed in the subcriteria.

Overall Viability: Viability includes an assessment of the overall organization's financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization's portfolio of products.

Sales Execution/Pricing: The vendor's capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor's history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization's message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification with the product/brand and organization in the minds of buyers. This "mind share" can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of Vision

Market Understanding: Ability of the vendor to understand buyers' wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers' wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service, and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor's approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor's underlying business proposition.

Vertical/Industry Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor's strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the "home" or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.