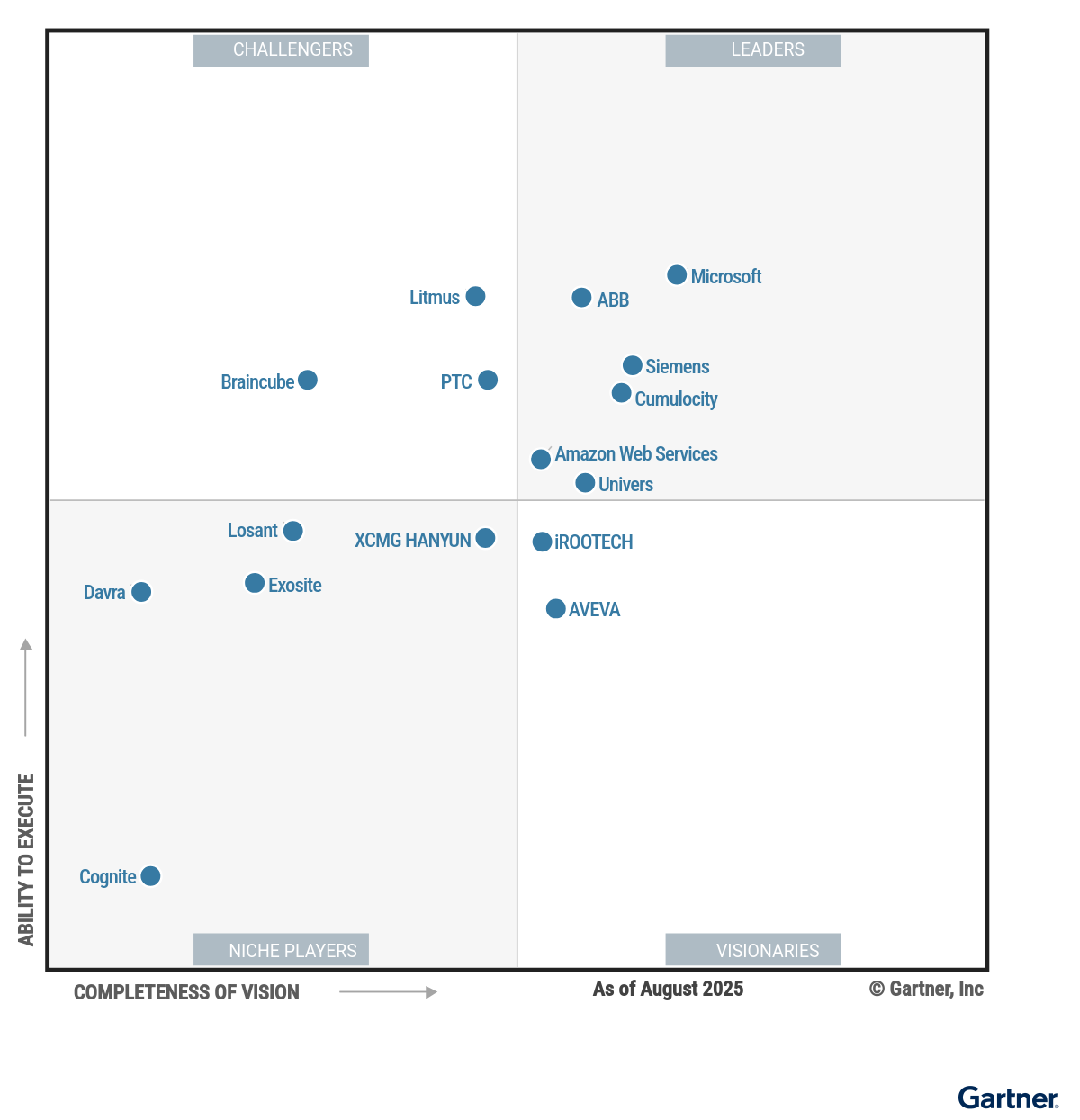

Magic Quadrant for Global Industrial IoT Platforms

8 September 2025 - ID G00816612 - 67 min read

By Scot Kim, Sudip Pattanayak, and 4 more

Global IIoT platforms have expanded their capabilities to enable industrial automation, industrial data management, smart operations and sustainability use cases. These platforms have matured to deliver value-added capabilities to CIOs from integrated IT/OT systems.

Market Definition/Description

This document was revised on 10 September 2025. The document you are viewing is the corrected version. For more information, see the Corrections page on gartner.com.

The global industrial IoT platform delivers multiple integrations to industrial OT assets and other asset-intensive enterprises’ industrial data sources to aggregate, curate and deliver contextualized insights that enable intelligent applications and dashboards through an edge-to-cloud architecture.

The global industrial Internet of Things (IIoT) platform market exists because of the core capabilities of integrated middleware software that support a multivendor marketplace of intelligent applications to facilitate and automate asset management decision making. IIoT platforms also provide operational visibility and control for plants, infrastructure and equipment. Common use cases are augmentation of industrial automation, remote operations, sustainability and energy management, global scalability, IT/operational technology (OT) convergence, and product servitization of industrial products.

The IIoT platform monitors IoT endpoints and event streams, supports and/or translates a variety of manufacturer and industry proprietary protocols, analyzes data in the platform, at the edge and in the cloud, integrates and engages IT and OT systems in data sharing and consumption, enables application development and deployment and can enrich and supplement OT functions for improved asset management life cycle strategies and processes. In some emerging use cases, the IIoT platform may obviate some OT functions.

The IIoT platform, in concert with the IoT edge and through enterprise IT-OT integration, prepares asset-intensive industries to become digital businesses by enhancing and connecting their core business with external business partners.

The IIoT platform may be consumed as software or cloud services, as a technology suite, or as an open and general purpose application platform, or in combination with analytics, application enablement, data management, device management, integration, and security functional capabilities. It is engineered to include the requirements of safety and mission criticality associated with industrial assets and their operating environments.

Must-Have Capabilities

The global IIoT platform must have the following capabilities:

- Device management — This function that enables manual and automated tasks to create, provision, configure, troubleshoot and securely manage fleets of IoT devices and gateways remotely, in bulk or individually.

- Integration — This function includes tools and technologies, such as communications protocols, APIs and application adapters, which address the data, process, enterprise application and IIoT ecosystem integration requirements across cloud and on-premises implementations for end-to-end IIoT solutions. IIoT platforms integrate into IIoT devices (for example, communications modules and controllers), IIoT gateways, historians OT systems (hardware, software and industrial apps) and enterprise applications (for example, ERP, materials requirements planning [MRP], supply chain management and CRM).

- Data management — This function includes capabilities that support:

- Ingesting IoT endpoint and edge device data

- Storing data from multiple industrial data sources like historians, data control systems and edge gateways

- Providing data accessibility (by devices, IT, OT, engineering technology systems and external parties, when required)

- Tracking lineage and flow of data

- Enforcing data and analytics governance policies to ensure the quality, security, privacy and currency of data

- Analytics — This function includes the processing of data streams, such as device, enterprise and contextual data, to provide insights into asset states by monitoring use, providing indicators, tracking patterns and optimizing asset use. A variety of techniques, such as rule engines, event stream processing, data visualization and machine learning, may be applied.

Standard Capabilities

The global IIoT platform should have the following capabilities:

- Application enablement and management — This function enables business applications in any deployment model to analyze data and accomplish IoT-related business functions. Core software components manage the OS, standard input and output, or file systems to enable other software components of the platform. The application capabilities, such as application platform as a service, include application-enabling infrastructure components, application development, runtime management, and digital twin and digital thread templates and instances. The platform allows users to achieve “cloud scale” scalability and reliability, and to deploy and deliver IoT solutions quickly and seamlessly.

- Security — This function includes the software, tools and practices facilitated to audit and ensure compliance. It also establishes preventive, detective and corrective controls and actions to ensure privacy and the security of data across the IIoT solution.

- An edge-to-cloud architecture — This a centrally managed cloud environment has established cloud service capabilities that are extended to edge environments. In a cloud-to-edge architecture, the cloud control plane — including security, value-added automation principles, governance, operations, programming models and interfaces, and other control elements — originates in the cloud and is then instantiated at the edge. There are some instances where AI is at the edge, and some control plane functions reside at the edge.

- Data acquisition layer — IT (including IoT) and OT endpoints for analytics and data sharing across various enterprise business applications and middleware that aggregate, analyze, contextualize and visualize data.

Magic Quadrant

Vendor Strengths and Cautions

ABB

ABB is a Leader in this Magic Quadrant. It provides IIoT platform software and digitalization solutions connecting its electrification, robotics, automation and motion portfolio. ABB Genix Industrial IoT and AI Suite integrates and contextualizes IT, OT and ET systems and data, and it provides advanced analytics and AI to drive industry-specific business outcomes. ABB Genix APM is built on its ABB Genix Industrial IoT and AI Suite providing integrated applications tailored for asset performance management and predictive maintenance.

ABB operates globally in North America, South America, Asia/Pacific, Europe and the Middle East. The North American region is predominantly served through direct sales channels. Customers in the Middle East and Africa mostly belong to the oil and gas and utilities industries.

ABB is making investments to advance its ABB Genix Industrial IoT and AI Suite and related digital solutions, focusing on areas like AI, autonomous operations and hybrid edge-cloud deployments.

- AI-driven assets: ABB Genix Industrial IoT and AI Suite provides a closed feedback loop automation of its own ABB industrial assets. This integrates real-time operational data and AI-driven insights with heterogeneous control systems to enable automated decision making. It empowers customers to respond rapidly to changing conditions, minimize manual intervention and optimize asset performance.

- Strong partner ecosystem and market reach: ABB heavily leverages go-to-market and technology partnerships with key players like Microsoft, IBM, Red Hat and Amazon Web Services to enhance its ability to execute and expand its reach for IT/OT integration services. The products are easily accessible through marketplaces, such as Microsoft Azure, and the partnerships offer specialized expertise to customers.

- Industrial data management: ABB offers integrated products and services to its ABB Genix Industrial IoT and AI Suite that enable customers to undertake smart manufacturing initiatives by transitioning their industries to intelligent operations. These operations involve advanced data management, contextualization and seamless IT/OT/ET integration across hybrid edge/cloud environments.

- No native L1 and L2 security function: Genix Platform’s integrated security does not natively extend to the foundational L1 and L2 network layers for non-ABB systems and devices; instead, this capability is delivered through its integrated partner solutions. While ABB Genix provides embedded upper-level security, customers requiring integrated security down to these lowest network layers need to assess ABB’s partner solutions and may need to implement additional third-party solutions.

- Limited exposure of ABB Genix among non-ABB industrial customers: Though ABB Genix has been deployed to both existing ABB customers and nonexisting customers, ABB Genix is still gaining the mind share of non-ABB industrial customers who seek more immediate, out-of-the-box solutions.

- Limited photorealistic digital twin capabilities: ABB Ability Genix currently lacks photorealistic digital twin capabilities, which are increasingly sought after for advanced visualization and immersive operational scenarios. ABB Genix supports AI models and simulation-based digital twins, but it is still advancing its agentic-AI-driven self-optimization features. Organizations seeking photorealistic visualization and an autonomous optimization twin should assess ABB’s roadmap and current feature set.

Amazon Web Services

Amazon Web Services (AWS) is a Leader in this Magic Quadrant, offering an IIoT suite for edge, cloud and hybrid environments. It leverages AWS IoT SiteWise for industrial data management, Amazon SageMaker for machine learning (ML), AWS IoT TwinMaker for digital twins and Amazon Bedrock for generative AI (GenAI). Edge solutions like AWS IoT Greengrass and AWS Outposts enable local processing and on-premises deployments, while AWS IoT ExpressLink and FreeRTOS provide secure microcontroller connectivity.

AWS serves a global customer base across the automotive, energy, heavy industry, life sciences and utilities industries, using direct sales, localized industry teams and partners worldwide.

The roadmap focuses on advancing AI-driven autonomous operations; democratizing data access; enhancing IT/OT integration, device management and zero-trust security; and accelerating industrial application enablement.

- Industrial data management: AWS offers an industrial data management solution that spans the edge and cloud environments, supporting a wide range of industrial protocols such as OPC UA and Modbus and organizing data using an ISA-95 hierarchical reference in their IIoT platform. The platform’s integration with AI services — including Amazon SageMaker and Amazon Bedrock — and its integration of Element Unify supports contextualization of IT and OT data.

- Openness and interoperability: AWS’s IoT platform business model continues to be open and extensible. This enables customers to leverage advanced analytics, ML and a wide array of industrial applications. AWS’s business model supports a large ecosystem of partners, including system integrators, ISVs and OEMs and can deliver specialized industrial solutions.

- Good scalability: AWS demonstrates IIoT platform viability through its scalable global cloud infrastructure for industrial assets. It offers AI capabilities, like AWS IoT SiteWise Assistant for industrial data insights and decision making, alongside a robust security posture supporting IEC 62443 and NERC CIP.

- Limited industry-specific analytics: AWS’s solutions typically require specialized IT or data science resources to tailor general-purpose tools for specific OT use cases. AWS offers native anomaly detection but is limited in providing deeper, proprietary and highly specialized industrial AI/ML models for anomaly detection as compared to other providers in the marketplace. The vendor may not be able to meet the rising demand for prepackaged, vertical- and solution-specific analytics and templates.

- Implementation complexity: AWS’s extensive portfolio of modular IoT services often necessitates significant configuration and integration efforts to deliver end-to-end IIoT solutions. Large-scale enterprise deployments may require collaboration with AWS Professional Services or certified partners, resulting in lengthy implementation cycles for complex IT/OT integration. Some industrial enterprises have claimed that AWS is a “horizontal toolbox” that needs extensive customization and may require third-party applications to address AI/ML gaps, increasing project complexity and delaying time to value.

- Unpredictable pricing: AWS’s granular, usage-based pricing model provides flexibility but can result in cost unpredictability, particularly as deployments scale or data volumes fluctuate. This means customers must closely monitor and manage consumption to avoid unexpected expenses. Hence, compared with other vendors who offer more predictable, scope-based or fixed-fee licensing models, AWS pricing may be less customer friendly.

AVEVA

AVEVA is a Visionary in this Magic Quadrant. CONNECT, the vendor’s platform, offers a software portfolio for on-premises, cloud and hybrid environments. Core platform services include data storage, contextualization, data shaping, data access, data sharing, visualization and analytics, with additional cloud solutions such as AVEVA Asset Information Management and AVEVA Advanced Analytics available to customers through CONNECT. It also includes hybrid offerings like AVEVA PI Data Infrastructure (including AVEVA Edge Management, AVEVA Data Pipeline, AVEVA Edge Data Store and AVEVA Adapters) and AVEVA Operations Control.

By delivering an end-to-end technology stack approach, the vendor ensures a consistent user experience within the AVEVA ecosystem of technologies that supports IT/OT integration. CONNECT is available across North America, South America, Europe, the Middle East, Africa and Asia/Pacific. It does not operate in China and Saudi Arabia due to public cloud restrictions.

AVEVA’s roadmap focuses on evolving CONNECT into an AI-driven industrial intelligence platform, enhancing GenAI, digital twin and open ecosystem capabilities.

- Native integration: CONNECT provides native integration to its own industrial products like AVEVA PI System (Historian), AVEVA Manufacturing Execution System (MES), AVEVA Edge Data Store and AVEVA Operations Control. Enterprise companies that are standardized with AVEVA software may find an advantage with CONNECT’s native integration.

- Wide partner ecosystem: The vendor has partnerships with key cloud, database and application providers like Databricks, Snowflake, Microsoft, Schneider Electric and Seeq. Through partnerships, AVEVA can provide database integration and application capabilities for extending industrial data management.

- Use cases in diverse industries: The vendor focuses on power generation; oil and gas; mining and metals; chemicals; and CPG. It has also forayed into adjacent markets like life sciences, water/wastewater and marine. Customers who are looking for industrial providers with deployments in multiple industries will find AVEVA to be well experienced.

- Lack of security differentiators: The vendor does not specifically focus on technical security differentiators, instead leveraging third-party identity providers using Open ID Connect (OIDC). This can make it unsuitable for customers who require specific security capabilities that require native embedded security features, rather than third-party security solutions.

- Lack of a full self-service IIoT software marketplace: Customers who require a marketplace of third-party industrial applications that are non-AVEVA will need to utilize what is currently available, or wait for the availability of a full self-service marketplace within CONNECT.

- Limited agentic AI capabilities: The vendor’s AI agent capabilities are in the early stages, and it lacks agentic AI capabilities today. Therefore, it may be unsuitable for customers who are investing in AI agent capabilities.

Braincube

Braincube is a Challenger in this Magic Quadrant. Braincube offers an industrial IoT (IIoT) platform for process manufacturing productivity, with deployment flexibility across cloud, edge, hybrid and on-premises environments. It ensures consistent functionality and user experience in all modes.

While the vendor serves a broad spectrum of industrial sectors, its core customer base is in process manufacturing, including pulp and paper; food and beverage; mining; and metals industries. Braincube serves customers across North America, South America, Europe, the Middle East, Africa, China and Japan.

Braincube’s future roadmap is centered on elevating its autonomous factory capabilities by incorporating AI agents capable of simulating outcomes and making proactive, data-driven decisions across multiple production lines. These agents will leverage real-time, closed-loop analytics to dynamically influence and optimize production control systems.

- Use cases in process manufacturing: Braincube is purpose built for process manufacturing, providing industry expertise focused on use cases related to waste, energy, material, efficiency and quality. Its off-the-shelf analytics tools help manufacturers optimize processes, reduce costs and maximize productivity.

- Purpose-built analytics: Braincube drives productivity gains through advanced analytics, using its proprietary CrossRank AI engine for multivariate analysis across thousands of variables. This identifies the most influential performance factors and delivers actionable, process-specific recommendations for industrial operations.

- Digital twin maturity: Their digital twin capability, powered by its “Product Clone,” links every data point from raw material to finished product to create a comprehensive composite digital twin. Capturing real-world process variability allows engineers to trace productivity outcomes and quality issues back to their actual source.

- Limited focus on other industrial markets: Braincube’s strong focus on process and discrete manufacturing may limit its suitability for other industrial sectors, where some features could be underutilized or require significant customization, increasing complexity and time to value.

- Limited autonomy in AI agents: Braincube’s current digital assistants are described as guided copilots that enhance decision making and operational awareness, but they are not yet fully autonomous AI agents. Braincube’s roadmap includes advancing toward “AI agents that simulate outcomes and make proactive decisions.”

- Limited direct sales outside of North America, Brazil and Europe: Braincube depends on partners for delivery and support outside Brazil, Europe and North America. Therefore, customers with operations outside these regions should be prepared to evaluate and collaborate closely with partners or develop in-house expertise.

Cognite

Cognite is a Niche Player in this Magic Quadrant. The primary function of Cognite Data Fusion is industrial Dataops, focusing on mapping, contextualizing and governing complex IT, OT and ET data, including unstructured sources. Cognite provides applications, such as Cognite InField, Cognite Maintain and Cognite InRobot.

Cognite is publicly available from major cloud providers, including Google Cloud, Microsoft Azure and Amazon Web Services (as of June 2023). Cognite has customers and stores its data in regions such as North America, Asia and Europe. Additionally, Cognite has established a joint venture, CNTXT, with Saudi Aramco and Google Cloud.

Cognite’s future roadmap is focused on advancing AI, including agentic AI, to enable autonomous industrial operations and provide intelligent assistance through natural language interaction.

- Comprehensive data management: Cognite offers industrial data management, contextualization and governance software solutions based on its knowledge graph technology. The knowledge graph technology enables the staging of industrial data to be utilized by the digital twin and advanced analytics, and it orchestrates industrial assets and intelligent dashboards.

- Layered data architecture: Cognite Data Fusion (CDF) supports layered data architectures, enabling the reuse of data without any proprietary formats and includes a built-in data catalog for discoverability and governance.

- 3D modeling in DataOps: The vendor’s solution enables industrial enterprises to ingest and automatically contextualize raw 3D models with diverse industrial data (e.g., time series, documents) into a unified knowledge graph. This facilitates visual exploration and AI-powered insights for comprehensive digital twins for applications such as anomaly detection.

- Third-party capabilities: CDF consists of third-party capabilities from partners such as Agora, Litmus Automation, Microsoft, Rockwell Automation and Siemens. Therefore, enterprises considering Cognite as their end-to-end IIoT platform provider would be confined to a limited set of implementation partners who have knowledge of and skills to manage both Cognite and third-party technology capabilities.

- Diversity in cross-industry use cases: The vendor’s industrial deployments are in oil and gas as well as power generation, renewables and chemicals. Cognite Data Fusion has a small percentage of their install-based manufacturing. Large manufacturers seeking connected products for servitization and/or custom integration to proprietary industrial machines (SECS/GEM) may need to develop such an API through third-party partners or in-house.

- Limited geographical reach: Most CDF deployments are in Europe, North America and the Middle East.

Cognite declined requests for supplemental information or to review the draft contents of this document. Gartner’s analysis is therefore based on other credible sources.

Cumulocity

Cumulocity is a Leader in this Magic Quadrant. Cumulocity IoT has capabilities such as Cumulocity’s device management functionality to manage device fleets throughout their life cycle as well as thin-edge.io to manage resource-constrained IoT devices connected to the platform.

Cumulocity supports over 1,000 active customers and operates in North America, South America, Europe, the Middle East, Australia, China and Japan. It focuses on connected products and operations for industrial clients mainly in discrete manufacturing and transportation.

Cumulocity’s roadmap consists of a strategic partnership with SAP around asset performance management and investments in an artificial intelligence of things (AIoT) platform strategy to address AI-powered applications, and it plans to expand capabilities in industrial operations. This emphasizes a continued focus on improving IIoT.

- Device management and edge: Cumulocity has partnered with Takebishi and thin-edge.io to extend its OT protocol drivers and add a new historian driver. Also, the vendor’s public key infrastructure offers device management certificates without third-party solutions.

- Sales strategy: Cumulocity has invested in building up a broader set of go-to-market partners, including industrial devices, technology and implementation partners and resellers and distributors. Customers will benefit from such developments through supported solution plays in all major regions.

- Comprehensive security: Cumulocity provides a layered security approach across aspects such as enterprise-grade authentication and authorization, secure communications and deployment and life cycle security management. It further enhances customer security through advancements in certificate authentication and identity management.

- Limited AI and analytics: Though the vendor has a strong vision for AIoT and its applications, it is too early to measure Cumulocity’s broad deployments and implementations in agentic AI, GenAI and other AI technologies.

- Market responsiveness: The vendor’s solutions, especially in industries such as utilities, that have specific intelligent assets and operations requirements may need partnership-driven analytics and functions rather than readily available tried-and-tested dashboard templates.

- Limited transportation and logistics capabilities: Currently, the vendor offers limited platform solution capabilities for transportation and logistics companies and their operations.

Davra

Davra is a Niche Player in this Magic Quadrant. It offers a portable IIoT platform that is tailored to industrial assets, transportation and mining. Key offerings include Davra Rail for fleet management, Edge SDK for telematics and AI safety; Davra Sentinel for mining compliance; and asset health for enabling predictive maintenance.

Davra operates via direct sales in North America, Europe and the Middle East. Davra primarily targets industrial equipment manufacturers and OEMs that are looking to embed sensors and connectivity into their products to offer value-added digital services.

Davra’s future roadmap includes introducing agentic AI features for process automation and expanding computer vision models for enhanced safety and security. Key advancements include deepening Earth observation capabilities for environmental and geospatial contextualization and integrating LIDAR data for precision 3D modeling to evolve digital twins.

- Platform openness and interoperability: Davra’s IIoT platform delivers consistent functionality across cloud, edge and on-premises environments, including VMware ESXi and bare metal. The platform’s architecture is independent of external PaaS components and minimizes the risk of vendor lock-in.

- Comprehensive security framework for connected products: The platform holds ISO 27001:2022, SOC 2 Type 2 and Department of Defense (DoD) IL5 certifications. Security is further enhanced by FIPS 140-3 compliant encryption, a robust AAA layer, fine-grained RBAC and multitenant SSO, supporting use in highly regulated and mission-critical environments.

- Analytics prepackaged functionalities: The vendor’s analytics package includes predictive modeling, remaining useful life (RUL) estimation and anomaly detection. These are supported by a unified data platform that integrates leading databases, such as Apache Cassandra and MongoDB, reducing integration complexity and reliance on third-party data services.

- Lack of proprietary marketplace and customer insights: Davra does not offer a proprietary IIoT platform marketplace, relying instead on partner marketplaces for solution distribution. This approach restricts the development of a centralized hub for direct customer engagement, public customer insights and community-driven innovation.

- Nontransparent partnerships: Davra’s key go-to-market partnerships are not publicly disclosed. This makes it difficult for industrial enterprises to assess the breadth and depth of Davra’s partners and the different types of solutions they provide.

- Maturity of agentic AI features for automation: Davra currently provides “GenAI-powered IoT assistants” for insights and recommendations but states its plan to begin “development of agentic AI features in 2026” for automating processes like scheduling repairs or ordering parts. There are early adopters of agentic AI proofs of concept projects deployed among industrial customers.

Exosite

Exosite is a Niche Player in this Magic Quadrant. Exosite’s product portfolio is built around its Murano IIoT platform, which is offered in both multitenant and dedicated cloud deployments. The company also offers hybrid edge/cloud and on-premises solutions through products like ExoEdge and IoT Connector, enabling industrial protocol support, real-time data ingestion and comprehensive device life cycle management. Exosite’s offerings also include data management and analytics with embedded AI/ML, strong security features and an IoT Marketplace Exchange for deploying off-the-shelf solutions.

Exosite provides a direct sales approach for North America, South America and Europe, and it has an indirect sales model via partners in the Middle East, Africa, China and Japan. Exosite has over 100 unique customers spanning 19 countries.

Exosite’s future roadmap focuses on making analytics easy by providing a unified platform for leveraging large historical datasets, digital twin information and application data. This includes continued investment in edge AI with ExoEdge, enhancing the platform’s query engine for large historical and fleet analytic queries, incorporating additional IoT device analytics for connectivity and security, as well as improving digital twin interoperability.

- Device and edge management: Exosite provides a device and edge management capability for IT/OT integration as well as device connectors for ease of installation. Their low-/no-code platform enables a quick development of industrial assets. Also, edge management provides diagnoses of industrial assets to trigger a maintenance query to a service management system.

- Auto scalability: Exosite supports auto-scaling cloud infrastructure for handling a high volume of connected devices.

- Rapid deployments: Exosite has direct and indirect sales channels and targets industrial OEM providers, focusing on rapid deployments and faster time to market.

- Limited vertical-specific solutions: Exosite is more focused on general-purpose tools and applications and lacks vertical-focused, specialized solutions. It also lacks market penetration in sectors such as automotive, utilities and heavy industries.

- Limited off-the-shelf integration: Multitenant cloud deployments offer the widest range of integrations, but the Exchange IoT marketplace is unavailable for edge or on-premises deployments. Customers using edge or on-premises models have limited access to third-party services and integrations, which may restrict their ability to expand functionality and leverage a broader ecosystem.

- Less focus on a code-centric developer program: Exosite’s ExoSense application framework offers a no-/low-code environment for ease of use. The developer program mainly provides online documentation, onboarding and training. While beneficial for nontechnical users, this may be a drawback for organizations with strong in-house development teams needing more advanced tools, SDKs and support for complex, code-heavy custom development or integration projects.

Litmus

Litmus is a Challenger in this Magic Quadrant. Litmus Edge delivers an IIoT platform built on an edge-first architecture, featuring two core products: Litmus Edge for edge data connectivity and Litmus Edge Manager for centralized management. These solutions work in tandem to provide a unified industrial data infrastructure, with consistent functionality across edge, cloud, hybrid and on-premises deployments.

While it serves a broad spectrum of industrial sectors, its core customer base is in discrete manufacturing, food and beverage, consumer packaging goods and automotive. It also has a presence in the transportation; utilities; and oil and gas industries. Litmus serves North America, Europe and Asia/Pacific (excluding China).

The vendor’s roadmap includes an AI-driven centralized management and orchestration feature that will allow users to deploy and manage Litmus Edge across hundreds of sites using natural language and GitOps based approaches.

- Comprehensive data integration: Litmus supports over 250 prebuilt OT device drivers, enabling zero-code, minimal-configuration connections across diverse industrial protocols. The platform contextualizes industrial data by cleansing, normalizing and enriching raw data with metadata, primarily at the edge.

- AI agent integration: The platform features an MCP server that uses AI models like OpenAI’s GPT to enable customers to configure and query Litmus Edge devices with natural language prompts. Running as a container on Litmus Edge or securely interfacing with external LLMs, this simplifies device management by allowing users to add device drivers. This leads to accelerated deployment.

- Extensive partner ecosystem: Litmus has an OEM and distribution network across hyperscalers, such as Google and Microsoft, hardware vendors (Dell and Belden), SIs and OEMs that license its products. Customers looking for an IIoT platform solution with “best-of-breed” technologies can procure Litmus’ software alongside other joint solutions or from service providers.

- Lack of domain-specific AI solutions: While Litmus enables the orchestration and local hosting of GenAI models, it does not build or train these models itself. The vendor depends on specialized partners or third-party platforms to provide domain-specific solutions for specific industrial requirements such as predictive maintenance. The vendor may not be a suitable option for customers seeking domain-specific or highly accurate models.

- Lack of direct cloud infrastructure coverage: Litmus states that it has “No cloud infrastructure coverage” in any listed global region. This indicates that Litmus relies entirely on third-party hyperscalers (e.g., Microsoft Azure, AWS) for its cloud and hybrid deployments through managed service agreements. It can also be deployed on a customer’s own data center or cloud environment.

- Limited industry reach: Over half of customers are from manufacturing, with a minimal presence in natural resources, utilities and transportation. This indicates limited experience outside of the manufacturing sector.

Losant

Losant is a Niche Player in this Magic Quadrant. It provides a full-stack IIoT platform with deployment options across cloud, edge, hybrid and on-premises environments. Losant Enterprise IoT Platform is self-managed and does not require external PaaS components. The product suite includes the Losant’s Enterprise IoT Platform, Gateway Edge Agent (GEA) and Embedded Edge Agent (EEA), supporting data collection, visualization and automation.

Losant’s cloud infrastructure is available in North America, South America, Europe, the Middle East, Africa and Asia/Pacific (excluding China and Japan). The vendor operates in China through third parties. The platform’s primary users are industrial OEMs, enterprise facility managers and telecommunications providers. In 2024, Losant reported more than 712,000 connected industrial assets and over 72,000 IoT gateways.

The development roadmap includes streaming analytics, data orchestration with tagging and conversational AI for digital twin querying.

- Deployment portability: Losant maintains consistent platform functionality across cloud, edge, hybrid and on-premises environments and does not rely on external PaaS services. This architecture provides customers with a unified experience and simplifies deployment and management due to consistent processes. This offers scalability and availability across diverse operational environments without feature compromise.

- Application enablement for OEMs: The platform includes “Experiences,” a low-/no-code application builder for external-facing applications. This supports OEMs in building customer-facing solutions easily and at scale.

- Digital twin aggregation: The “Device Systems” feature supports hierarchical digital twin modeling and automated data aggregation for different levels of physical environments. This feature benefits customers by enabling them to define hierarchical digital twin representations of their physical environments and automatically perform data aggregations.

- Absence of a public marketplace: Losant does not have a full IIoT platform software marketplace, offering only an app template marketplace. This reduces access to community-driven or third-party solutions compared with vendors with broader marketplaces. It also limits online customer insights.

- Limited AI innovations and prompt-based analysis: The platform does not include a prompt-based data analysis tool, restricting natural language data interaction. Also, the vendor has not released any new edge AI or edge analytics features in the past 12 months.

- Limited dedicated CMDB functionality and adoption: Losant does not offer an exclusive configuration management database (CMDB) functionality. While the platform provides device management features such as device databases, metadata storage, configuration tracking and over-the-air (OTA) updates that overlap with some CMDB capabilities, Losant reports low adoption for this use case. As a result, the platform is not widely utilized or perceived as a comprehensive CMDB solution.

Microsoft

Microsoft is a Leader in this Magic Quadrant. Azure IoT Operations, enabled by Azure Arc, supports cloud, hybrid/edge cloud and on-premises environments. Other key products include Azure IoT Hub, Azure Device Registry, Azure IoT Hub Device Provisioning Service, Azure Device Update for IoT, Azure IoT Central, Arc-enabled Kubernetes, Azure Event Grid, Microsoft Fabric, Power Apps, Azure Digital Twins, Microsoft Copilot, Microsoft Defender for IoT and Microsoft Sentinel.

Microsoft maintains a global footprint in North America, South America, Europe, the Middle East, Africa and Asia/Pacific (excluding China). China cloud infrastructure coverage is facilitated through third-party partnerships, ensuring adherence to local cybersecurity laws and data residency requirements.

Microsoft’s future roadmap is heavily centered on integrating and expanding AI capabilities, including generative and agentic AI, across its entire stack to drive insights.

- Wide partner ecosystem: Microsoft has over 300,000 global and local partners in different regions of the world. Their go-to-market industrial partners include Avanade, Capgemini, Celebal Technologies, Cognizant, DXC Technology, Innominds, MaibornWolff, Mesh Systems, Softweb Solutions and TCS, among others.

- In-built security features: The Azure IoT portfolio allows the integration of security into the design and operate phase, enabling automatic protections to reduce user burden. The company emphasizes a fully integrated suite through Microsoft Defender, Sentinel and Entra.

- Integration of Azure Copilot: Microsoft Copilot and broader GenAI capabilities are integrated into its IIoT platform, especially with Azure IoT Operations and real-time intelligence in Microsoft Fabric. The integration of Copilot can provide recommendations for operations management, including reasoning, validation and supervisory tasks.

- Cloud-dependent strategy: Microsoft’s cloud-dependent edge strategy may be less suitable or robust for customers operating in industrial scenarios that have severe connectivity constraints or strict data sovereignty requirements. Microsoft’s edge AI is less optimized for highly disconnected or constrained edge environments.

- Azure service costs: Customer architectures that are not native Azure IoT Operations will need to send data to Azure services to get analytical results can incur higher transfer and/or service costs. Therefore, this solution may be more expensive for customers who have data architectures that are not natively built within the Azure IoT operations suite.

- Partner-first time-to-market: Microsoft has offered a core IoT platform for partners to build applications and solutions. Taking a partner-first approach has required more time to launch its IoT operations solutions as compared to other participating IIoT platform providers due to longer product release lead times between Microsoft and its partners.

PTC

PTC is a Challenger in this Magic Quadrant. The vendor offers the ThingWorx IIoT platform for core IIoT capabilities, such as connectivity, analytics and data management, across cloud, edge and on-premises environments. Applications like Digital Performance Management, Real-Time Production Performance Monitoring, Connected Work Cell, Asset Monitoring and Capacity Utilization help to address OEE, asset monitoring, manufacturing execution and remote services. Within the IIoT tech stack, Kepware supports industrial connectivity.

PTC serves global discrete and process manufacturing segments, managing over 13 million connected assets (not all industrial related). It has good adoption rates among large-scale discrete manufacturing clients. PTC operates globally, with direct sales in North America and Japan, and partner-led strategies in other regions.

The vendor’s roadmap emphasizes ThingWorx as a core platform, GenAI capabilities, distributed data architectures, edge AI and enhanced security.

- Seamless IT/OT integration: PTC delivers OT data integration using Kepware for standardized industrial connectivity and the ThingWorx platform for advanced data aggregation and analytics. This enables seamless integration with a wide range of OT systems, letting customers adopt IIoT applications incrementally without replacing existing infrastructure.

- Localized support: PTC’s global sales and support network for its IIoT platform combines direct teams and system integrators across North America, Europe and Asia/Pacific. Customers benefit from localized implementation and support, including a direct presence in key markets like Japan and solutions tailored to regional regulatory needs.

- Assets performance optimization: PTC’s IIoT platform is designed for the industrial sector, helping manufacturers enable a shift from reactive to predictive maintenance through real-time monitoring, predictive diagnostics and prescriptive insights that anticipate equipment failures and recommend optimal actions.

- Limited AI features: PTC’s IIoT platform offers native analytics and AI integration; however, it did not show any customer proofs of concept when it comes to out-of-the-box support for prompt-based data analysis and agentic AI features, such as conversational (advisory) interfaces or context-aware agents. As a result, customers may face limitations in leveraging intuitive, AI-driven insights and automation. PTC has added AI capabilities in its roadmap.

- Lack of a centralized marketplace: PTC’s IIoT solution strategy and marketing do not seem to be keeping pace with industry trends, especially in developing marketplace-driven ecosystems and rapid go-to-market approaches. The lack of a centralized marketplace limits customers’ access to specialized analytics solutions. As a result, customers may experience fewer options, slower innovation and reduced value. PTC employs a partner ecosystem approach to providing applications.

- Complex pricing: While PTC has improved its pricing competitiveness and simplicity, its model, depending on operational sites, user counts and connected assets, can be complex. This complexity, combined with challenges in tracking diverse asset types and their operating sites, may hinder cost predictability for organizations with dynamic or evolving asset inventories.

iROOTECH

iROOTECH (previously ROOTCLOUD) is a Visionary in this Magic Quadrant. The vendor’s capabilities include a set of AI Foundation Model Integrators and Insight Agents. It also includes a self-developed, fine-tuned LLM-based retrieval-augmented generation (RAG) architecture to support operational decision making.

iROOTECH has over 1,300 customers worldwide, supported by 14 global certificated partners. iROOTECH delivers on use cases that include Smart Operations and Smart Works for Asia/Pacific and European manufacturing sectors.

iROOTECH’s product roadmap for the next three years focuses on integrating AI and GenAI, expanding edge computing capabilities (including new Edge Pilot and Edge Vision solutions) and digital twin applications to enable autonomous industrial operations and intelligent full-life-cycle device management.

- Comprehensive IT/OT data management with industrial data fabric: iROOTECH’s Industrial Data Fabric (IDF) integrates IT and OT domains, optimizing data warehousing and data lake concepts to ensure consistent data standardization and calibration. This approach simplifies complex industrial data landscapes, providing a foundational source for flexible IT/OT data calculations.

- AI-powered analytics and natural language interaction: The GenAI Data Insight Agent processes complex data workflows into natural language dialogues, enabling more efficient and actionable insights. This capability supports prompt-based data analysis and root cause analysis, empowering business users with a zero-code metric toolkit for formula customization and automated aggregation.

- Extensive industrial connectivity and digital twin visualization: The platform offers extensive connectivity, supporting over 1,100 industrial protocols to integrate with over 98% of industrial devices across dozens of industries. This is combined with a no-code digital twin platform that allows users to create and visualize digital twins by enabling real-time monitoring and predictive maintenance of physical assets through solutions like iROOTECH Data Viz and ROOTPILOT 3D Machine Control System.

- Geopolitical challenges: iROOTECH’s presence and responsiveness outside its core markets such as China and the Asia/Pacific need to be stronger, as global markets have become more cautious about foreign providers.

- Lack of use cases in diverse industries: iROOTECH’s expertise is primarily in the manufacturing, natural resources and transportation and logistics industries, despite some experience in equipment monitoring for irrigation channel construction. Customers in other sectors may find its solutions less tailored to their specific needs.

- Limited partnerships: The majority of iROOTECH’s partnerships are focused on issues around carbon management, smart operations and smart works. It lacks a deeper set of industry partners for underserved industrial sectors such as energy and utilities.

Siemens

Siemens is a Leader in this Magic Quadrant. It delivers a broad IIoT solutions portfolio via its cloud-based Insights Hub (SaaS, Virtual/Local Private Cloud) and on-premises Industrial Edge solutions. The vendor’s key offerings include Insights Hub Monitor, Intelligent Energy Management, Quality Prediction and Production Copilot. They address asset uptime, predictive quality and throughput optimization.

Siemens serves global customers across the manufacturing, transportation and utilities industries, connecting over 200,000 plus industrial assets and gateways. Siemen’s Insight Hub has cloud infrastructure coverage through third-party providers in North America, South America, Europe, the Middle East, Africa, China and Japan.

The strategic roadmap focuses on AI and analytics, expanding Production Copilot, advanced data management, flexible connectivity and integrated digital twin capabilities.

- Wide range of edge functionalities: The Industrial Edge platform offers centralized management for fleets of edge devices and containerized applications, supporting both on-premises and private cloud deployments. The Industrial Edge Management handles updates, configurations and security across devices and is designed to support high-frequency data processing.

- AI and analytics: Siemens has improved its edge analytics and AI capabilities. The platform’s AI copilot feature that leverages a large language model, retrieval-augmented generation (RAG) chains and AI agents to enable users to ask ad hoc questions. Production Copilot supports root cause analysis and decision making based on diverse data sources, including Industrial Edge.

- Expansion into adjacent industrial markets: Siemens is expanding its IIoT platform beyond manufacturing into transportation, logistics and utilities. Integration with Siemens’ broader digital portfolio and support for open standards enable the vendor to expand into multiple industrial markets.

- Data modeling limitations: Siemens’ current IoT data model within Insights Hub has limitations to accommodate complex industrial use cases that require relationship mapping across multiple product and/or asset data hierarchies. When modeling complex production processes, Insight Hub may require manual mapping of these hierarchies to establish comprehensive relationships across diverse data domains. Customers with highly customized data modeling requirements may encounter constraints until these enhancements are fully realized.

- Specific platform customization limitations: Gartner Peer Insights feedback indicates that customers have experienced additional steps in customizing and integrating the platform to fit specific operational or integration needs. This may impact customers with unique equipment requirements such as DNP3 (Distributed Network Protocol), IEC 61850, NMEA 2000, SEC/GEM or CANopen that may require custom-built API connectors via Insight Hub SDK.

- Lack of visibility into customer onboarding: The customer onboarding and partner enablement processes are not always transparent, making it difficult for customers and partners to track progress or understand how effectively the vendor supports new users. This lack of visibility can lead to uncertainty about the quality of certain engagements.

Univers

Univers is a Leader in this Magic Quadrant. The vendor’s EnOS includes capabilities such as Ark AI Energy and Resource Management (RM), Wind AI Analytics and Renewable Power Forecast for supporting industrial customers transitioning from automation to autonomous intelligence at scale.

Univers supports over 800 customers and operates in more than 45 countries. Univers’ cloud infrastructure serves North America, South America, Europe, the Middle East, Africa, Southeast Asia, China and Japan. The vendor has partnerships with Microsoft as a hyperscaler and with IBM and Accenture as global system integrators. Univers’ roadmap focuses on integrating AI and GenAI across its unified cloud-edge IIoT platform, EnOS, to enable autonomous industrial operations and intelligent full-life-cycle device management.

- Comprehensive energy asset management: EnOS is designed to consolidate and manage energy assets, enabling customers to monitor operations, optimize processes and achieve sustainability goals.

- Advanced data management: EnOS offers enhanced prebuilt data quality checks for completeness, validity and timeliness, along with automated corrections during operations. It also offers domain-based, built-on semantic relationships, industrial data management and multitype data hierarchies.

- Strategic partnerships: Univers enhances its AI-first energy management solutions by partnering with industry leaders like Microsoft, Mott MacDonald, Dassault Systèmes and Primustech. These collaborations bring together deep domain expertise and advanced technology.

- Energy operations focus: EnOS is primarily focused on monitoring, orchestrating and control of energy system use cases for the optimization of energy transition and sustainability objectives. Customers seeking an IIoT platform for broader asset management, OEE, quality control, automation or nonenergy-related transportation and logistics use cases may need to inquire Univers for their nonenergy use cases to meet the broader optimization use cases.

- Limited protocols of low-/no-code integration capabilities: EnOS includes a featured development toolkit for app creation and AI-powered common building blocks with over 200 protocols for application integration. Customers with specific and proprietary integration requirements may need customization from the Univers (composable building blocks) CBB for broader application development.

- Lack of tiered pricing and streamlined evaluation processes: Initial customer feedback on Gartner Peer Insights indicates potential concerns about limited tiered pricing options and challenges during the evaluation and contract process. This may result in customers paying for features they do not need or experiencing a less streamlined onboarding experience.

XCMG HANYUN

XCMG HANYUN is a Niche Player in this Magic Quadrant. The vendor’s IIoT platform supports cloud, hybrid edge/cloud and on-premises deployment. It has a robust data management layer with automated data detection and contextualization, enabling key use cases in life cycle management, predictive maintenance and intelligent manufacturing.

XCMG HANYUN supports nearly 200 unique customers, with China being the main focus, but the company has expanded in Europe, particularly Germany. The vendor has key partnerships with Alibaba, AWS, Orange and Huawei. It has a strong focus on industries like manufacturing, natural resources and transportation and logistics.

Their strategic roadmap focuses on AI/ML and GenAI capabilities, such as autonomous agents for device management and security as well as multimodal data and knowledge graph management.

- Device and edge management: XCMG HANYUN IIoT platform supports over 1,657 terminal device protocols with zero-code access. The platform uses an AI agent for device life cycle management. They combine containerized application orchestration and OTA updates for edge computing tasks.

- Application enablement and management: The platform provides a low-code development environment and built-in CI/CD pipelines, making it easier and faster for customers to build, deploy and update applications. Integrated AI agents automate code generation and optimization, while industry-specific AI supports intelligent decision making.

- Improved applied AI functionalities: The vendor has improved its AI and analytics capabilities. XCMG HANYUN deeply integrates AI/ML and GenAI using a transformer-based industrial foundation model. It features a multiagent system enabling “conversational analytics” for nontechnical users and multiple agents for predictive maintenance, process optimization and smart scheduling.

- Lack of global presence: XCMG HANYUN is based in China and has operations expanding in Europe. Customers outside these regions may find it difficult to implement its software.

- Limited global use cases: The vendor’s strongest partnerships and most proven use cases are concentrated in China and Europe, with some presence in the Middle East and South Africa. There is limited experience and exposure in the American markets. Customers in these regions should carefully assess local support, references and the platform’s ability to meet regional requirements before adoption.

- Integration and pricing challenges: During Gartner client inquiries and in the Gartner Peer Insights forum, customers report the lack of integration capability and high pricing as one of main drawbacks of the vendor’s platform.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

Cumulocity: as of January 2025, the majority stake of Cumulocity was purchased by its management team from Software AG, thus creating a private independent company.

Dropped

Eurotech has defocused their global outreach by divesting its presence in the Asia market. Thus, it cannot make the minimum global unique customers to maintain its global status. Furthermore, Eurotech no longer focuses on the end-to-end industrial applications.

Rockwell Automation’s FactoryTalk DataMosaix Private Cloud has demonstrated inadequate market penetration or global adoption due to the divestiture of the platform resources and innovation roadmap. Rockwell Automation’s FactoryTalk DataMosaix Private Cloud is no longer available as a stand-alone platform but rather as a service directed solution through Rockwell Digital Solutions with Kalypso.

Inclusion and Exclusion Criteria

To qualify for inclusion in this Magic Quadrant, each vendor had to meet the following criteria:

- The vendor must be an IoT platform supplier to asset-intensive industries. The IoT software platform tendered for consideration must be generally available (GA) and in production deployments in at least three defined industrial sectors. For this evaluation, Gartner has identified the following sectors (and allowed subsectors) as representing asset-intensive industries:

- Manufacturing and natural resources: Subsectors are automotive, consumer nondurable products, energy resources and processing, A&D industry, IT hardware, life sciences and healthcare products, mining, oil and gas and construction.

- Transportation: Subsectors are air transport, motor freight, pipelines, rail and water, warehousing, couriers and support services.

- Power and utilities: Subsectors are electrical, gas, thermal and water.

- The IIoT platform must be able to deliver and support the following capabilities in a single bundled offering, across a distributed architecture:

- AI and analytics

- Device management/edge

- Integration

- Data acquisition and management

- Application enablement and management

- Security and monitoring

- The provider may include, via a formal ongoing partnership or partnerships with other software vendors, portions of the IIoT platform capabilities. The vendor must demonstrate purpose-built integration and support for scalability and interoperability relating to partnered IIoT platform capabilities. Partnered solution capabilities can include IaaS and PaaS elements from third-party cloud service providers. If the predominance of the intellectual property that comprises the IIoT platform is derived from third parties, then the partnered software functionality or capabilities must only be accessible by the evaluated vendor’s own APIs. Evaluated vendors cannot consider third-party software sold under a separate contract as an IIoT platform functionality or capability.

- The GA date for the IIoT platform must be by 31 March 2025 or earlier. For enhanced guidance relating to product releases, product releases must be GA by 31 March 2025 in order to be assessed in the reference for information questionnaire.

- The IIoT platform must be saleable as an independent purchase without requirements for companion hardware or software purchases. Similarly, the purchase of the IIoT platform should not be contingent on an existing asset base of vertical applications, software or hardware (e.g., including product life cycle management, asset performance management, manufacturing execution systems, industrial control systems, historians). However, the IIoT platform can take advantage of existing legacy installed bases, provided it also connects to other third-party applications.

Note: Stand-alone IoT-enabled applications and SaaS are not considered part of this market and do not meet the Inclusion Criteria. Stand-alone IoT-enabled applications and SaaS will be considered an element of Vision, but not considered within “execution” (e.g., product/service evaluation criteria). Manufacturers considered for inclusion within this Magic Quadrant must offer value to the equipment of other manufacturers. At least 50% of assets connected to and interacting with the manufacturer’s IIoT platform must be outside of their own product lines.

- The vendor has 100 customers who have deployed GA versions of the IIoT platform in production. These customers must demonstrate data acquisition, ingestion and analysis from industrial assets, from a diverse set of OEMs, in industrial environments for industrial companies. Among the 100 customers, the vendor must show both product services (product servitization enablement) and owner-operator intelligent operations (outcome-based capabilities such as asset utilization, energy efficiency, process health, remote operations, global scalability, IT/OT integration, app enablement/production and/or robotics automation) to show diversity of the capability enablement of the IIoT platform deployment. Other types of innovative enablement are welcome in lieu of the suggestions highlighted.

- The IIoT platform has to be “in production,” enabling product services and/or owner-operated intelligent operations (outcome-based solutions such as asset utilization, energy efficiency and process health). In lieu of the suggestions highlighted, other types of innovative outcomes are welcome.

- The vendor must have a minimum of 12 unique customers operating the GA platform in production in at least each of the three major geographies (such as North America, South America, Europe, Asia/Pacific, the Middle East or Africa) for a minimum total of 36 unique customers. Within the three major geographies, there must be a minimum of five certified implementation/migration partners per geography:

- Number and name of third-party certified developers

- Company name

- Type of certifications

- Number of trained engineers/developers on the platform (by region)

- The vendor must have, at a minimum, 450,000 industrial IoT endpoints, which can span industrial IoT endpoints connected to their platforms across the installed base of customers. At least 30,000 of these must be industrial gateways. Note: An IoT endpoint enables equipment, assets or other objects to participate in one or more IoT solutions. There are three characteristics of an IoT endpoint when it is enabling an asset or object: (1) sense or activation capabilities; (2) compute (at a minimum, data acquisition and control functions); and (3) communication. Gateways may have sense/actuation capabilities but must provide some computation (even if this is fundamental message filtering and formatting) and communication.

- The product must be available in at least these designated deployment models: cloud-only, hybrid edgecloud, on-premises with microcontroller cloud/edge capabilities. For on-premises deployments, Gartner will accept containerized solutions where all solution elements are available, and the system is able to operate in a disconnected scenario for extended periods of time.

- Offer, directly or through partnerships, professional services (installation, implementation and integration) and support services (help desk, product support, sustaining engineering) in at least three major geographies and in at least three major languages (such as English, French, German, Mandarin, Arabic, Spanish, Japanese, Hindi-Urdu).

- The vendor solutions must support and or enable most and/or all of the use cases that will be referenced in the critical capabilities, such as:

- Predictive maintenance

- Industrial automation

- Sustainability (operations and assets)

- Digital twins

- Industrial data management

Honorable Mentions

The evaluation process identified more than 50 vendors that were excluded from this Magic Quadrant, but each has forward-looking or specialized value for industrial enterprises. CIOs and IT leaders have myriad choices for their IIoT platforms beyond the cohort of vendors evaluated herein.

It is important to note that the exclusion of any vendor from this market evaluation is not a de facto assessment that the excluded vendor cannot provide value to industrial enterprises. Exclusion is a function of nonconformance with the inclusion criteria established, which are based on Gartner’s view of the evaluated market. Upon determining the criteria, Gartner seeks to evaluate vendors that are relevant and extensible to as many Gartner customers as possible. This evaluation of IIoT platforms focuses on a small number of providers that meet Gartner’s inclusion criteria for this Magic Quadrant cycle. Other vendors merit consideration in any due diligence for IIoT solutions.

The following vendors are presented based on platform capabilities, experience with industrial enterprises and the ability to create related value.

Covacsis Technologies

Intelligent Plant Framework (IPF) offers implementation services of advanced analytics, AI/ML models and IoT, with a strong presence in Asia and India markets. Covacsis Technologies partners with system integrators to extend its market reach outside of its core geographic footprint. IPF is predominantly a manufacturing IoT platform that supports such use cases as quality improvement, yield production efficiency and production throughput resiliency. The company did not meet the Magic Quadrant criterion because it did not provide any customers in other subindustries such as transportation and utilities.

Eurotech

Eurotech’s IIoT offering consists of Everyware Software Framework (ESF), which is Eurotech’s IoT device/gateway middleware, available as a perpetual license or subscription on its hardware and Everyware Cloud (EC) for data, device life cycle, security and remote management. The core functionality is developed in the Eclipse IoT Working Group, specifically in the projects Eclipse Kura (for edge environments) and Kapua (for data and device management). Eurotech’s global IIoT offering is to simplify edge complexity through both modular hardware and open-source-based, commercially supported software solutions. The company was dropped from this year’s Magic Quadrant because it did not provide a unique set of new customers in regions beyond Europe and North America. Furthermore, Eurotech is focused on IoT and AI edge infrastructure building blocks, rather than on end-to-end applications.

Inductive Automation

Inductive Automation’s IIoT offering spans a range of required IIoT platform components for industrial enterprises, with a strong North America presence, plus partners for the rest of the world. It works with customers in manufacturing, both process and discrete, as well as water and power utilities. Typical projects involve integrating plant data to drive cost optimization or automation efforts. The company did not meet the Magic Quadrant criterion for offering the platform as a stand-alone solution without the need for acquiring third-party software sold under a separate contract.

IoT.nxt

IoT.nxt is an IIoT platform that enables real-time data orchestration across industrial environments. It leverages edge computing, digital twins and ML to help organizations optimize operations, reduce costs and improve decision making. IoT.nxt operates in North America, Europe and Africa. Their IIoT platform is predominantly in the telecommunication subsector but recently expanded out to other vertical markets like manufacturing and energy markets. The company did not meet the Magic Quadrant criterion because it did not meet the necessary minimum of customers in each of the subindustries, such as transportation and utilities.

SAS Analytics for IoT

SAS Analytics for IoT is an IIoT platform that analyzes data, builds models and provides real-time analytics, data management, data reduction and visualization. The platform focuses on connecting and analyzing data from industrial equipment and operations. Some notable use cases are predictive maintenance, manufacturing quality, supply chain optimization and workplace safety. The company did not meet the Magic Quadrant criterion because it did not meet the necessary minimum number of customers in each of the subindustries, such as transportation and utilities.

Servitly

Is an IIoT platform that focuses on connecting products for remote monitoring and enabling equipment-as-a-service capabilities to device companies that deliver advanced device capabilities. The core of Servity’s platform is to support the smart connected products where remote operations are mandatory for end customers. The company did not meet the Magic Quadrant criterion due to not meeting the minimum requirements for industrial connected devices, unique customers and deployments.

Evaluation Criteria

Ability to Execute

Gartner evaluates vendors on the quality and efficacy of the processes, systems, methods or procedures that enable IT provider performance to be competitive, efficient and effective. Vendors are also evaluated on the ability to positively impact revenue, retention and reputation within Gartner’s view of the market.

Providers are judged on their ability and success in translating market requirements — and their vision for the market — into products that match market needs and enable clients to achieve a successful outcome with minimal risk.

Product or Service

The capabilities, features and overall quality of the core goods and services that compete in and or serve the defined market.

Core goods and services that compete in and/or serve the defined market include current product and service capabilities, quality, feature sets, skills, etc. This can be offered natively or through some OEM agreements/partnerships as defined in the Market Definition and detailed in the subcriteria.

The subcriteria for this Evaluation Criteria are:

- AI and analytics: Processing of data streams such as device, enterprise and contextual data to provide insights into asset state by monitoring use, providing indicators, tracking patterns and optimizing asset use. A variety of techniques, such as rule engines, AI, GenAI, event stream processing, data visualization and ML, may be applied.

- Device management/edge: This feature enables manual and automated tasks to create, provision, configure, troubleshoot and manage fleets of IoT devices and gateways remotely, in bulk or individually and securely as required by industry standards and regulatory mandates.

- Integration: Tools and technologies, including communications protocols, APIs and application adaptors, that minimally address the data, process, enterprise application and IIoT ecosystem integration requirements across cloud and on-premises implementations for end-to-end IIoT solutions, including IIoT devices, IIoT gateways, IIoT edge and IIoT platforms.

- IoT data management: Capabilities that support ingesting IoT endpoint and edge device data, storing data from edge to enterprise platforms, providing data accessibility (by devices, IT and OT systems and external parties when required), tracking lineage and the flow of data and enforcing governance policies to ensure the quality, security, privacy and currency of data.

- Application enablement and management: This component enables business applications in any deployment model to analyze data and accomplish IoT-related business functions. Core components manage the OS and standard input, output or file systems to enable other software or cloud service components of the platform. The application platform (e.g., aPaaS) includes application-enabling infrastructure components, application development, runtime management, a low-code application platform and digital twins.

- Security: The tools and practices facilitated to audit and ensure compliance as well as to establish and execute preventive, detective and corrective controls and actions to ensure privacy and the security of the data across the IIoT solution.

- Edge AI: AI techniques embedded within Internet of Things (IoT) endpoints, gateways and other edge devices. Use cases range from autonomous vehicles to streaming analytics. While predominantly focused on AI inference, many systems also use statistical techniques to adapt to — and accommodate — local conditions. Edge AI is a platform for value implemented on resource-constrained “edges” and environments. The gating factors for edge AI are the design constraints of the hardware and software deployed, such as power sources, processing and connectivity.

- Digital twin: A digital representation of a real-world entity or system. The implementation of a digital twin is an encapsulated software object or model that mirrors a unique physical object, process, organization, person or other abstraction. Data from multiple digital twins can be aggregated for a composite view across a number of real-world entities, such as a power plant or a city and their related processes.

- Viability includes an assessment of the organization’s overall financial health as well as the financial and practical success of the business unit. Views the likelihood of the organization to continue to offer and invest in the product, as well as the product’s position in the current portfolio.

Overall Viability (Business Unit, Financial, Strategy and Organization)

The organization’s overall financial health, as well as the financial and practical success of the relevant business unit. This includes the likelihood that the organization can continue to offer and invest in the product, as well as the product’s position in the organization’s portfolio.

To ascertain overall viability, areas of focus are year-over-yeargrowth rate in terms of new logos and project implementations, overall financial growth and continued investments in the IIoT platform.

Sales Execution/Pricing

The organization’s capabilities in all presales activities and the structures that support these activities. This includes deal management, pricing and negotiation, presales support and the overall effectiveness of the sales channel.

How pricing is set for all different groups and subindustries, how the sales organization is structured (through partnerships, integrators or direct) and how quickly sales close from the start of the sales cycle to the end.

Market Responsiveness/Record

The ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This includes the provider’s history of responsiveness to changing market demands.

We will specifically examine how the platform addresses the current socioeconomic climate (e.g., tariffs), customer dynamics and competitive pressures.

Marketing Execution

The ability to deliver clear, high-quality, creative and effective messaging via publicity, promotional activity, thought leadership, social media, referrals and sales activities. This includes the organization’s ability to influence the market, promote the brand, increase product awareness and establish a positive reputation among customers.

Customer Experience

The degree to which a vendor’s products, services and programs enable customers to achieve their desired results. This includes the quality of supplier/buyer interactions, technical support or account support, as well as ancillary tools, customer support programs, availability of user groups and service-level agreements.

How to improve the customer experience through GenAI, customer service and training of customer cultures to be more digitally dexterous.

Operations

The ability of the organization to meet its goals and commitments. This includes the quality of its organizational structure, skills, experiences, programs and systems that enable the organization to operate effectively and efficiently.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | High |

Sales Execution/Pricing | High |

Market Responsiveness/Record | High |

Marketing Execution | Medium |

Customer Experience | High |

Operations | Medium |

Source: Gartner (September 2025)

Completeness of Vision

Market Understanding

The ability to understand customer needs and translate that understanding into products and services. Vendors with a clear vision of the market listen to and understand customer demands, and they can shape or enhance market changes with their vision.

The ability to understand customer needs and trailblaze new IT/OT integration use cases (examples in industrial data management, remote and intelligent operations and industrial edge) in asset-intensive industries and translate them into products, services and market awareness and trust. Vendors that show a clear vision of the evolution of the IIoT platform market into further transformation of connected products and owner-operator assets show market understanding.

Marketing Strategy

The ability to clearly communicate differentiated messaging, both internally and externally, through social media, advertising, customer programs and positioning statements.

Offers clear, differentiated messaging consistently communicated internally, externalized through social media, advertising, customer-facing programs, partner programs and positioning statements to generate platform recognition and positive brand regard.

The ability to identify opportunities to expand adoption through geographic expansion or the identification of underserved or poorly served market subsectors and unique business requirements through microsegmentation analysis and outreach.

Sales Strategy

The ability to create a sound strategy for selling that uses the appropriate networks, including direct and indirect sales, marketing, service and communication. This includes partnerships that extend the scope and depth of a provider’s market reach, expertise, technologies, services and their customer base.

A focused and structured strategy for selling that identifies the appropriate channel mix, including: direct and indirect sales, marketing and business development, direct and partnered service delivery (partner-led, co-delivery and private label) and supportive communication. What are the new investments being made to develop sales and value-added services, partners and market alliances that extend the scope and depth of global market reach, expertise, technologies, services and their customer base are key considerations.

Offering (Product) Strategy

The ability to approach product development and delivery in a way that meets current and future requirements, with an emphasis on market differentiation, functionality, methodology and features.

An approach to platform development and delivery that emphasizes market differentiation, functionality, methodology and features as they map to current and future requirements for asset-intensive businesses.

Business Model

The design, logic and execution of the organization’s business proposition.