Market Guide for Outsourced Managed Security Services

5 January 2026 - ID G00837548 - 28 min read

By Christopher Wiles, Joe Trejo

Outsourced managed security services providers deliver cybersecurity services to meet regulatory demands and talent shortages. Sourcing and vendor management leaders should use this research to identify OMSS partners and enhance security operations.

Overview

This document was revised on 5 January 2026. The document you are viewing is the corrected version. For more information, see the Corrections page on gartner.com.

Today’s cybersecurity landscape is relentless, marked by advanced, persistent threats, complex hybrid multicloud environments, and stringent global regulations. With ongoing talent shortages and prohibitive costs of sustaining in-house 24/7 security functions, organizations are having to turn to outsourced managed security services (OMSS) providers for the comprehensive end-to-end specialized expertise and operational resilience essential to defend against modern cyber risks.

Today’s cybersecurity landscape is relentless, marked by advanced, persistent threats, complex hybrid multicloud environments, and stringent global regulations. With ongoing talent shortages and prohibitive costs of sustaining in-house 24/7 security functions, organizations are having to turn to outsourced managed security services (OMSS) providers for the comprehensive end-to-end specialized expertise and operational resilience essential to defend against modern cyber risks.

OMSS providers are transforming cybersecurity approaches by shifting from reactive tactics to proactive, outcome-focused solutions. Harnessing AI and machine learning, they deliver superior real-time threat detection, rapid incident response, and maximized operational efficiency. OMSS also empowers organizations to master complex compliance demands with continuous monitoring and expert guidance, reinforcing strong governance. While OMSS excels at managing tactical security operations, organizations must maintain clear processes and robust collaboration, as ultimate responsibility for security remains firmly in their hands.

Key Findings

- Organizations face relentless cyberattacks and complex hybrid cloud challenges, making in-house security a riskier option. As a result, resilient, outcome-focused security operations are driving demand for expert external providers.

- Many organizations continue to rely on reactive security approaches, which are proving insufficient against today’s rapidly evolving threats. This has led to a growing demand for outsourced security services, as organizations seek proactive solutions powered by advanced AI and machine learning to achieve better threat detection, faster response times, and optimized operations.

- Expanding global compliance requirements make external expertise crucial for risk mitigation. Organizations increasingly depend on outside specialists for robust compliance management, ongoing monitoring, and tailored guidance to avoid breaches and penalties.

- While most security service providers now offer similar core capabilities, evaluating the wider vendor ecosystem reveals that different provider types can deliver unique strategic advantages.

Recommendations

- Seek providers that integrate AI and machine learning (ML) across their offerings to enhance real-time analytics, automate critical security tasks, and accelerate incident response, in reaction to an evolving attack sophistication.

- Prioritize providers that offer specialized expertise and experienced security professionals who leverage proactive methodologies to counter sophisticated adversaries and defend complex environments.

- Select providers who can help maintain adherence to increasing global regulatory demands through continuous monitoring, reporting, and expert guidance, significantly reducing the risk of breaches and associated penalties.

- Choose providers with modular, customizable solutions and flexible pricing to deliver adaptive, outcome-driven protection and cost efficiency.

Strategic Planning Assumption(s)

Market Definition

Outsourced managed security services (OMSS) provide enterprises with comprehensive expertise and operational support across a broad spectrum of cybersecurity functions. These services and predetermined cybersecurity outcomes deliver the management and operation of complex security technologies. OMSS are delivered against a structured services scope, governance and reporting frameworks, service levels, pricing models and clear contractual obligations. OMSS allow the optimization of internal resources, accelerate security maturity and focus on strategic business objectives.

Outsourced managed security services provide organizations with specialized external expertise and operational support for critical cybersecurity functions. OMSS allow enterprises to maximize the value of security investments, overcome internal cybersecurity resource limitations and enable internal IT teams to reduce risk while maintaining focus on strategic outcomes.

Mandatory Features

The mandatory features for this market include:

- Remotely or locally delivered expertise to deploy, configure, update, maintain and operate a variety of security technologies including, but not limited to, endpoint detection and response (EDR) tools, security information and event management (SIEM) platforms, and cloud security posture management (CSPM) tools.

- 24/7 availability of comprehensive expertise to support the triage, investigation and resolution of cybersecurity incidents.

- Operational security expertise in threat detection, investigation, active mitigation, rapid escalation and incident response.

- Continuous evaluation and validation of digital asset exposures, including visibility, accessibility and exploitability.

- Availability of accredited staff to support configuration issues and change requests on cybersecurity technologies in scope of the service agreement.

- Service management and third-party coordination including, but not limited to, the delivery of service offerings to a pre-agreed set of service-level agreements (SLAs), regular service reviews, customized reporting and a dedicated service manager.

Common Features

The common features for this market include:

- The ability to provide 24/7 security operations center (SOC) triage functions for the purposes of investigating configured alerting and alarms generated by commercial cybersecurity technologies and via any deployed SIEM platform.

- Digital forensics and incident response consultancy, offering call-off access to identified lessons and remedial guidance for discovered security incidents.

- Expert tool configuration and associated consultancy to support exposure management capabilities such as vulnerability management (VM), external attack surface management (EASM) and adversarial exposure validation (AEV) capabilities, including breach and attack simulation (BAS)

- Threat intelligence interpretation, reporting and implementation of mitigation actions across a variety of security technologies including the development of new threat detection capabilities on SIEM platforms. Such reports should encompass technical, operational and strategic insights.

- Adjacent security technology management in specialized areas such as identity and access management (IAM), data loss prevention (DLP) and application security through configuration of web application firewall (WAF) appliances.

- Turnkey delivery models with predefined processes, regularly evolving detection content and standard playbooks for rapid deployment, which offer predefined and optimized processes and regularly evolving detection content, including a standard playbook of workflows, procedures, and analytics validated and updated.

- Automated orchestration and workflow functions to streamline security operations and incident response tasks.

Market Description

Driven by the escalating frequency and sophistication of cyberattacks, the persistent global shortage of cybersecurity talent, and increasing regulatory pressures, the OMSS market has evolved beyond the traditional reactive models of compliance checklists and technology deployment. The OMSS market is shifting toward integrated, proactive, and measurable security offerings that deliver tangible business value. Organizations are increasingly turning to these services to address internal expertise limitations.

The services consolidate various capabilities, ranging from advisory and consulting to end-to-end detection and response services, threat hunting, and the full life cycle management of security technologies. This holistic approach is crucial as organizations seek to optimize their security posture, reduce operational overhead, and accelerate incident response times. Most providers are leveraging advanced technologies like AI and ML to enhance threat detection and reduce response times, integrating them across security information and event management (SIEM), extended detection and response (XDR), endpoint detection and response (EDR), and security orchestration, automation and response (SOAR) and cloud-native services to provide comprehensive coverage.

While both OMSS and traditional managed security services (MSS) aim to strengthen organizational security, they differ notably in their scope and approach. MSS generally centers around technology-driven monitoring, alerting, and basic incident response, often operating as a reactive service focused on maintaining operational continuity. In contrast, OMSS extends beyond these foundational capabilities by offering integrated, proactive, and outcome-oriented services that align closely with business objectives and risk management strategies. OMSS providers typically deliver a broader range of expertise — including advisory, consulting, and life cycle management — and are more likely to embed governance and accountability frameworks into their offerings. Within the managed security ecosystem, there are also distinct markets such as managed detection and response (MDR), which specializes in advanced threat detection and rapid incident response, and digital forensics and incident response (DFIR), which focuses on investigating, containing, and remediating security breaches. These specialized services may be delivered independently or as part of a comprehensive OMSS solution, enabling organizations to address specific needs and regulatory requirements with greater flexibility.

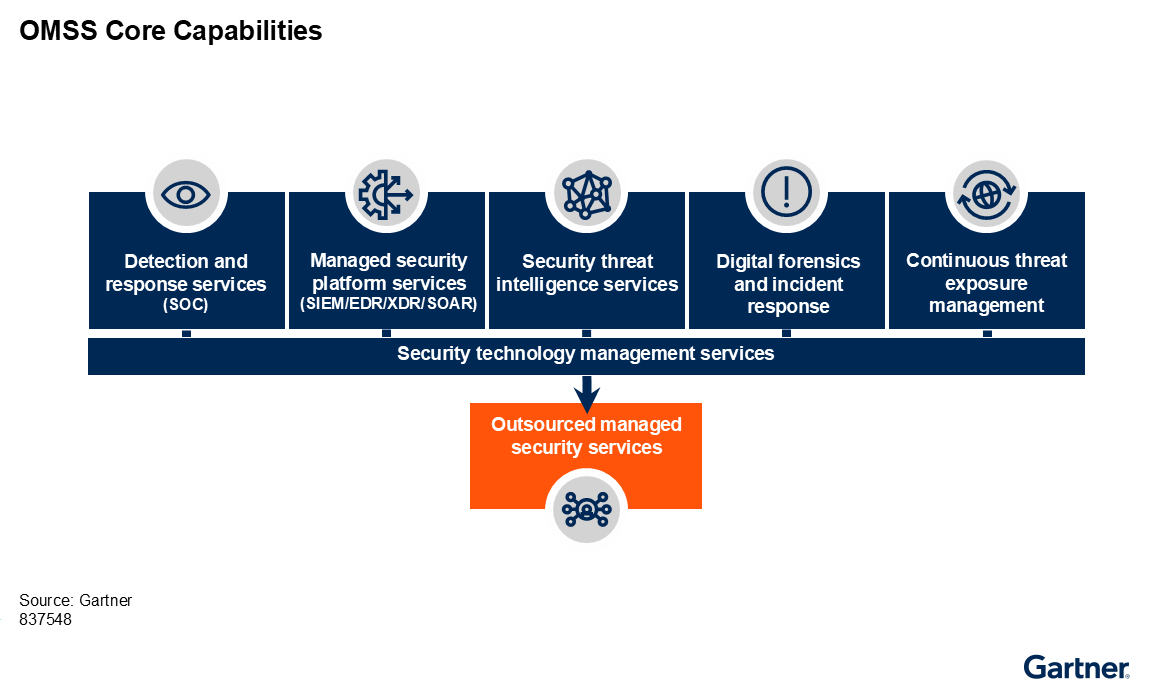

An effective OMSS delivery model will depend on strong coordination and governance across multidisciplinary teams. While service providers deliver critical capabilities like threat detection and response, ultimate accountability for security risks remains with the client organization. Clear governance structures — aligned with standards such as NIST and ISO/IEC 27001 — are essential to define roles, ensure accountability, and drive measurable outcomes. Seamless coordination between security, IT, and business units enables rapid, effective responses to threats. Objective, business-focused metrics empower leadership to make informed decisions and demonstrate the value of security investments. In short, robust governance and cross-functional collaboration are crucial to achieving defensible, business-aligned cybersecurity outcomes (see Figure 1).

Figure 1 depicts the core capabilities delivered by OMSS providers. These core capabilities include:

Detection and response services — Provides the customers with remotely delivered, human-led modern security operations center (SOC) functions, enabling rapid detection, analysis, investigation, and active response through threat disruption and containment. OMSS providers offer a turnkey experience, utilizing a predefined technology stack covering areas such as endpoint, network, logs, and cloud, with expert analysts performing threat hunting and incident management to deliver actionable outcomes. These services are critical for organizations that lack the resources, budget, or appetite to build and run their own 24/7 SOC functions. MDR services are designed to reduce the time between detecting and responding to threats and provide an assessment of current exposures. Further detail can be found in the Market Guide for Managed Detection and Response.

Managed security platform services — Encompasses SIEM, XDR, EDR, and SOAR, and considers the management of client-owned or provider-hosted security technologies, including initial provisioning, configuration, ongoing maintenance, updates, patch management, and integration across diverse security toolsets. Such services ensure security technologies are aligned with organizational policies, supporting functions like continuous monitoring, event analysis, and data source connection for log collection.

- SIEM acts as a configurable security system of record that aggregates and analyzes security event data from on-premises and cloud environments to assist with response actions and satisfy compliance and reporting requirements.

- EDR monitors endpoints for malicious activity and unusual behavior. It uses advanced analytics, machine learning, and threat intelligence to detect attacks, automate cleanup, and streamline incident response by providing continuous visibility and deep analysis of system, process, and user behavior.

- XDR delivers unified security incident detection and response capabilities by integrating threat intelligence, security events, and telemetry data from multiple sources with security analytics to contextualize and correlate alerts.

- SOAR platforms combine incident response, orchestration and automation, and threat intelligence management capabilities to streamline operations, automate routine tasks, and enhance the consistency and timeliness of security work.

Further detail can be found in the Market Guide for Extended Detection and Response and Magic Quadrant for Security Information and Event Management.

Security threat intelligence services (TI) — Provides organizations with relevant context and insight about the cyberthreat landscape by documenting tactics, techniques, and procedures (TTPs), and by profiling attack campaigns, threats, and threat actors. TI products also deliver tools to assist organizations in aggregating, collecting, curating, and operationalizing their own TI. This intelligence empowers cybersecurity teams to preemptively adjust defensive measures, correlate emerging threats with internal event data, and inform overall risk management and security technology capabilities to reduce exposure and compromise. These services are applicable across all industries and security functions. Further detail can be found in the Market Guide for Security Threat Intelligence Products and Services.

Digital forensics and incident response (DFIR) — Incorporates advisory and professional services that help organizations assess and manage the impact of security incidents. They assist with forensic response, aid in forensic information gathering, advise on proactive best practices for avoiding a breach, and help with breach investigation, triage, and impact classification. These services are typically offered on a retainer-based model, providing specialized skills for investigating, negotiating, and responding to advanced attacks like ransomware. Further detail can be found in the Market Guide for Digital Forensics and Incident Response Retainer Services.

Continuous threat exposure management (CTEM) — Allows enterprises to continually assess the visibility and validate the accessibility and exploitability of their digital assets. CTEM governs and prioritizes risk reduction for the modern enterprise, factoring in business importance, likelihood of attack, visibility of vulnerability, and validation of attack paths to enable responses to genuine, impactful risks. It represents a shift from traditional technology vulnerability management to a broader, more dynamic continuous threat and exposure management practice. A CTEM program should be the first step in identifying and planning for resolution, requiring cross-team collaboration and federation of responsibilities. Further detail can be found in the Strategic Roadmap for Continuous Threat Exposure Management.

Security technology management services — Considers the management and operational services specific to security technologies and business outcomes for security. This includes the full life cycle management of security technologies, whether deployed on-premises, in a customer-owned cloud, or as provider-hosted solutions, covering initial provisioning, configuration, ongoing management, updates, patch management, and performance optimization. These services aim to maintain security technologies and address security technology changes, including modernization, migration, and design/management of security configurations and integrations.

Market Direction

The OMSS market represents a subset of the $25.5 billion managed security services market which has seen 11.5% annual growth in recent years.1 This growth in externally sourced comprehensive services is driven by organizations struggling to internally address the changes required due to rapidly evolving cybersecurity threat landscapes, technological advancements, shifting business needs and the growing complexity of IT environments. These changes require OMSS providers to evolve their offerings, adopting new technologies, and focusing on proactive, cloud-centric, and compliance-driven services to address the ever changing cybersecurity landscape.

Traditionally, OMSS providers focused on core services such as firewall management, intrusion detection, and basic monitoring. However, as cyberattacks have become more sophisticated and frequent, organizations now demand advanced threat intelligence, rapid incident response, and proactive security measures. This shift has prompted OMSS providers to expand their offerings to include services like threat hunting, vulnerability management, and security orchestration, automation, and response (SOAR).

Increased hybrid multicloud adoption — Cloud adoption has been a major catalyst for change in the OMSS market. As businesses migrate to cloud platforms, OMSS providers have had to adapt their solutions to secure hybrid and multicloud environments. This includes integrating cloud-native security tools, supporting compliance across different jurisdictions, and providing visibility into cloud workloads. Additionally, the rise of remote work has increased the attack surface, requiring OMSS providers to deliver endpoint protection and secure remote access at scale.

Leveraging AI and machine learning — Another notable trend is the growing use of AI and ML in managed security services. These technologies enable OMSS providers to analyze vast amounts of data, detect anomalies, and automate responses to threats more efficiently. The integration of AI and ML has improved the speed of threat detection, allowing organizations to mitigate risks before they escalate. Furthermore, OMSS providers are increasingly leveraging automation to reduce manual tasks and address the cybersecurity skills gap faced by many organizations.

Expanding regulatory and compliance expectations — Increasing compliance and regulatory mandates has had a profound impact on the OMSS market. Organizations across industries are now required to adhere to an expanding array of standards — such as General Data Protection Regulation (GDPR), (Health Insurance Portability and Accountability Act (HIPAA), Payment Card Industry Data Security Standard (PCI DSS), and California Consumer Privacy Act (CCPA) — as well as region-specific cybersecurity laws. This has driven demand for OMSS providers that can offer not only robust security but also comprehensive compliance management and reporting capabilities. OMSS vendors have responded by developing specialized services to help clients continuously monitor compliance status, generate audit-ready reports, and quickly address gaps in their security posture. As regulations continue to evolve and become more complex, OMSS providers are positioning themselves as strategic partners, guiding organizations through the intricacies of compliance and reducing the risk of costly penalties or reputational damage associated with noncompliance.

Customizable service offerings — A growing emphasis on customer-centric, customizable services has also reshaped the OMSS market, as organizations increasingly seek solutions tailored to their unique needs and risk profiles. OMSS providers are responding by offering modular service packages, flexible pricing models, and highly configurable dashboards that deliver actionable insights specific to each client’s environment. This shift enables organizations to select only the services most relevant to their operations, optimizing costs while enhancing security outcomes. Customizable dashboards and reporting tools empower clients with real-time visibility into their security posture, incident trends, and compliance status. This fosters greater collaboration and transparency between OMSS providers and their clients. As a result, the OMSS market is moving away from one-size-fits-all offerings toward more agile, personalized solutions that align closely with business objectives and regulatory requirements.

Significant market consolidation — The OMSS market has seen significant consolidation, with larger providers acquiring specialized firms to broaden their capabilities and global reach. This has been driven by a more competitive landscape, where differentiation is achieved through advanced analytics, tailored solutions, and industry-specific expertise. As regulatory requirements become stricter, OMSS providers are offering compliance management as part of their services, helping clients navigate complex legal and industry standards. Overall, the OMSS market has evolved from basic monitoring to comprehensive, proactive, and adaptive security solutions that address the dynamic needs of modern enterprises.

Market Analysis

The OMSS market is composed of a diverse array of service providers that have expanded their offerings to generate increased penetration in this rapidly evolving market. The different types of service providers can be generalized into the following types:

- Consulting and professional services providers

- Global technology managed services providers

- Global telecommunications providers

- Security product vendors

- Boutique managed security service providers (MSSPs)

Although many of these providers may have started from different core offerings, they often provide a similar set of OMSS capabilities. However, the different service provider types may offer wider benefits to an organization when considered in their wider service provider landscape.

Consulting and Professional Services Providers

Consulting and professional services firms come from a history of helping organizations develop comprehensive security strategies aligned with business objectives and regulatory requirements. Their approach tends to be highly consultative, often starting with in-depth risk assessments, maturity evaluations, and the design of tailored security roadmaps. They assist clients in implementing governance frameworks, selecting appropriate technologies, and integrating security into broader business processes. Additionally, they provide support for incident response planning, crisis management, and post-breach remediation, leveraging their multidisciplinary teams and global resources.

Many consulting and professional services firms have used their position as strategic cybersecurity advisors and technical implementation specialists, to build out into delivering end-to-end security solutions for clients. Their deep understanding of industry-specific regulations and business challenges makes them valuable partners for organizations facing complex compliance landscapes or undergoing digital transformation. They help organizations navigate the complexities of modern security challenges by delivering holistic, business-aligned solutions that go beyond technical defense, focusing on governance, risk management, and long-term resilience. Their involvement is particularly beneficial for large enterprises and regulated industries seeking to elevate their cybersecurity posture while aligning with broader organizational goals.

While consulting and professional services firms offer access to broad security expertise, it is important to understand the scale and structure of their global managed services delivery model and how consistent this is across various regions. This includes considering the role of global delivery centers, local expertise and resources. Additionally, consulting and professional services firms can come with a pricing premium and can typically charge higher fees, sometimes with hidden costs for customizations, add-ons, or out-of-scope work.

Global Technology Managed Services Providers

Global technology managed services providers (MSPs) are global technology firms that specialize in delivering end-to-end IT and security solutions to organizations of all sizes. These companies combine deep technical expertise with broad industry knowledge to help clients design, implement, and manage complex technology environments, including cybersecurity infrastructures. Their role in the OMSS market is multifaceted, encompassing everything from consulting and integration to ongoing management and optimization of security operations.

These providers are distinguished by their ability to integrate diverse security technologies and platforms into cohesive, enterprisewide solutions. Their global reach and large-scale delivery capabilities make them ideal partners for multinational organizations with complex, distributed IT environments. Technology MSPs possess the ability to deliver both strategic guidance and hands-on management, bridging the gap between high-level consulting and day-to-day security operations. Their comprehensive approach enables clients to achieve robust, scalable, and resilient security postures while navigating digital transformation and regulatory challenges. As trusted partners, they play a critical role in helping organizations stay ahead of emerging threats and maintain business continuity in an increasingly complex cybersecurity landscape.

While global technology managed services providers offer scale, reach, and robust infrastructure, organizations must be cognizant that they often deliver highly standardized solutions for efficiency and scalability, which may not fit unique or complex client requirements. It is also important to understand how they maintain separation of responsibilities between security and other managed services provided to the organization by the provider.

Global Telecommunications Providers

Global telecommunications providers occupy a unique position in the OMSS market, leveraging their vast network infrastructure and deep expertise in connectivity to deliver robust security solutions. These companies have traditionally focused on providing core telecommunications services — such as voice, data, and internet connectivity — but have expanded their portfolios to include comprehensive managed security offerings in response to the growing demand for integrated cyber protection.

Telecommunications providers are particularly valuable for organizations seeking to protect complex, distributed environments and ensure the security of their network infrastructure. This is thanks to their global reach and ability to deliver consistent security services across multiple countries and continents. They frequently serve large enterprises, multinational corporations, and critical infrastructure sectors that require reliable, scalable, and compliant security solutions. Additionally, global telecommunications providers often bundle security services with connectivity solutions, simplifying vendor management and streamlining service delivery for their clients.

Although global telecommunications providers can offer robust network-based security services and global reach, organizations need to be aware that telecommunications provider OMSS solutions are often highly standardized. They also have limited options for customization to unique business requirements. Additionally, as they are primarily network providers, their security services may be heavily focused on network security (enterprisewide firewalls, DDoS protection, etc.), potentially lacking depth in endpoint, cloud, or application security.

Security Product Vendors

Many security product vendors have extended their offerings by combining cutting-edge security technologies with managed service offerings. These vendors are primarily known for their innovative cybersecurity products, which serve as the foundation for their OMSS portfolios. Their expertise in developing and deploying specialized security technologies enables them to deliver highly effective and targeted managed services to organizations seeking robust protection against modern cyberthreats.

Security product vendors can leverage their ability to deliver rapid innovation and adapt to emerging threat vectors, ensuring that clients benefit from the latest advancements in cybersecurity. These product-centric MSS providers typically serve organizations that require specialized, technology-driven security solutions. Their managed services are often tightly integrated with their proprietary platforms, enabling seamless deployment, centralized management, and real-time visibility into security events. By offering both advanced security products and managed services, these vendors empower clients to strengthen their cybersecurity posture while alleviating the burden of day-to-day security management.

Even though security product vendors excel at managing and optimizing their own technologies, organizations must be aware that services are focused on their own products. This potentially neglects other security layers or technologies that could provide an improved security posture. Additionally, resources tend to be product specialists, not generalists, lack broader security operations or multidomain experience, and may not provide the same level of strategic security advisory or holistic risk management capabilities.

Boutique Managed Security Service Providers (MSSPs)

Boutique managed security service providers (MSSPs) focus on delivering highly tailored cybersecurity solutions and expert advisory services. Unlike large, global MSSPs or product-centric vendors, these firms typically emphasize agility, personalized customer engagement, and deep domain expertise. They cater to organizations seeking customized security strategies, hands-on support, and advanced threat protection that address specific business needs or industry challenges.

These boutique providers often serve sectors with specialized requirements — such as finance, healthcare, or critical infrastructure — where tailored solutions and deep technical knowledge are essential. They provide a high-touch, consultative approach that combines advanced technology with expert guidance, making them ideal partners for organizations that require more than generic, one-size-fits-all security services. Their focus on customization, responsiveness, and industry-specific expertise allows clients to address complex security challenges while maintaining flexibility and control over their cybersecurity strategy.

Boutique MSSPs can deliver highly personalized, specialized, and agile security services. However, but organizations must consider potential challenges related to scale, breadth, stability, and global reach as they typically have smaller teams, which can lead to resource limitations during high-demand periods or major incidents. Also, they often don’t have the same financial clout which can impact their operational and process maturity and mean they may not have access to the latest or most sophisticated security technologies, threat intelligence feeds, or automation platforms.

Overall, the OMSS market is characterized by a rich variety of providers, each bringing distinct strengths and capabilities to the table. Enterprises must carefully assess their security needs, risk profiles, and operational requirements to select the provider type that best aligns with their business objectives. Whether seeking broad coverage from a global player, specialized expertise from a pure-play provider, bundled IT and security services from an MSP, or tailored solutions from a boutique firm, organizations have a wide range of options to address the increasingly complex cybersecurity landscape.

Representative Vendors

The vendors listed in this Market Guide do not imply an exhaustive list. This section is intended to provide more understanding of the market and its offerings.

Vendor Selection

Representative OMSS vendors, the regions in which they operate, their service names and their types are listed in Table 1.

OMSS Vendors

| Vendor | Regions | Service name(s) | Vendor type |

|---|---|---|---|

Accenture |

|

|

|

Ackcent |

|

|

|

Arctic Wolf Networks |

|

|

|

Atos |

|

|

|

BT Security |

|

|

|

Bullet Solutions |

|

|

|

Capgemini |

|

|

|

Coalfire |

|

|

|

Deloitte |

|

|

|

DXC Technology |

|

|

|

eSentire |

|

|

|

EY |

|

|

|

Fujitsu |

|

|

|

HCLTech |

|

|

|

Heartland Business Systems |

|

|

|

Help AG |

|

|

|

IBM Security |

|

|

|

Integrity360 |

|

|

|

Kyndryl |

|

|

|

LevelBlue (formerly AT&T Cybersecurity) |

|

|

|

Lumen |

|

|

|

NCC Group |

|

|

|

NTT Security |

|

|

|

Optiv |

|

|

|

Orange Cyberdefense |

|

|

|

Port 53 |

|

|

|

PwC |

|

|

|

RedLegg |

|

|

|

Sophos (formerly Secureworks) |

|

|

|

Tata Consultancy Services (TCS) |

|

|

|

Telstra |

|

|

|

T-Systems |

|

|

|

Verizon |

|

|

|

Wipro |

|

|

|

Source: Gartner

Market Recommendations

Over 40% of organizations, including two-thirds of midsize enterprises, are projected to rely on consolidated platforms or managed service providers for cybersecurity validation assessments by 2026, driven by talent shortages and the high cost of internal security operations.2 When looking to engage an OMSS, it is critical to:

- Define clear outcomes and requirements: Document desired outcomes and specific security needs, including threat landscape priorities and business risks, before engaging with any service provider to ensure alignment and effective service consumption.

- Assess provider capabilities for active response: Evaluate how MSSPs approach containment and incident reporting as they integrate with internal processes, and determine if they can perform remote disruption and containment actions on your behalf, aligned with business and regulatory policies.

- Plan for long-term partnership and exit: View managed security service contracts as long-term partnerships that emphasize adaptability, regular technology updates, and continuous improvement processes. Additionally, establish clear exit criteria, including data portability and destruction, for service continuity.

- Embrace hybrid models and integration: Consider hybrid outsourcing models that combine internal teams with external service providers for accelerated maturity and cost-effectiveness, and prioritize providers who demonstrate strong integration capabilities with existing and future IT infrastructure, including multicloud environments.

Acronym Key and Glossary Terms

| Acronym | Description |

| CCPA | California Consumer Privacy Act |

| CTEM | Continuous Threat Exposure Management |

| DFIR | Digital Forensics and Incident Response |

| EDR | Endpoint Detection and Response |

| GDPR | General Data Protection Regulation |

| HIPAA | Health Insurance Portability and Accountability Act |

| MDR | Managed Detection and Response |

| MSP | Managed Services Provider |

| MSSP | Managed Security Service Provider |

| NIST | National Institute of Standards and Technology |

| OMSS | Outsourced Managed Security Services |

| PCI DSS | Payment Card Industry Data Security Standard. |

| SIEM | Security Information and Event Management |

| SOC | Security Operations Center |

| SOAR | Security Orchestration, Automation and Response |

| TI | Threat Intelligence |

| TTPs | Tactics, Techniques, and Procedures |

| XDR | Extended Detection and Response |

Note 1 Gartner’s Initial Market Coverage

This Market Guide provides Gartner’s initial coverage of the market and focuses on the market definition, rationale and market dynamics.