Magic Quadrant for 4G and 5G Private Mobile Network Services

5 March 2026 - ID G00828050 - 69 min read

By Sylvain Fabre, Frank Marsala, and 5 more

The emerging 4G and 5G private network services market includes vendors with varying capabilities in geographic reach, multivendor support, orchestration and industry-vertical focus. This research helps CIOs evaluate providers against their global 4G and 5G private mobile network service needs.

Market Definition/Description

This document was revised on 9 March 2026. The document you are viewing is the corrected version. For more information, see the Corrections page on gartner.com.

4G and 5G private mobile network services encompass the complete life cycle of private wireless networks — from design and deployment to operation and management. They are for the exclusive use of a given organization and provide dedicated connectivity for the people and assets of an enterprise setting. 4G and 5G PMN services are delivered as an end-to-end service, with either fully dedicated or a mix of shared assets, such as spectrum or core network.

Enterprises deploy private mobile networks (PMNs) for wireless connectivity in enterprise locations such as factories, warehouses, ports, airports and mines to provide:

- Improved coverage

- Better reliability than other wireless options

- Simplified wireless network architecture

- Better network control compared to public networks

- Enhanced data privacy protection from better surface attack management

- Isolation from public cellular networks

- Stronger authentication mechanisms than in Wi-Fi networks

- Operational efficiencies by simplifying overall network management and consolidating multiple pre-existing connectivity technologies into one PMN

- Data collection and analysis that enable real-time insights into various operations, allowing enterprises to optimize processes, improve efficiency and make data-driven decisions.

- Better scalability compared to Wi-Fi (such as the number of endpoints and use cases)

- Assets’ connections across private and public mobile networks

- High-performance networking for demanding use cases, such as computer vision

Mandatory Features

These capabilities must be supported by the PMN service providers:

- Network end-to-end sourcing — Sourcing the full scope of network elements for the PMN. This includes hardware or software elements such as radios, packet core and transport that are either vendor-owned or sourced from a third party, possibly from multiple providers. Vendors should be able to act as an agent on behalf of a customer with these third-party providers. These providers could be third-party equipment vendors, network operators, independent software vendors (ISVs), Internet of Things (IoT) device manufacturers and resellers.

- Network design — Includes all the activities necessary to plan and design a solution for the specific enterprise locations for which the vendor is responsible. Network design comprises:

- Creating project requirements and site surveys

- Selecting for most suitable technology (such as 4G and 5G)

- Creating the network architecture design

- Performing radio and capacity planning to support the desired number of endpoints, users and applications

- Designing network security

- Determining all costs

- Identifying all required approvals, permits and regulatory approvals

- Implementation and integration — Includes commissioning of individual network elements, installation, integration testing between network elements and final acceptance test of the end-to-end network. It can include several deployment options (for example, scalable proof of concept [POC], dedicated on-site, hybrid, hyperscaler partner and sliced network).

- Service management and support — This feature comprises all of the following:

- The systems and services to track and manage private 4G/5G contracts, network usage patterns, related assets and service elements.

- End-to-end operations, maintenance and optimization of enterprise private mobile networks. This capability provides remote and on-site management, including proactive monitoring, fault detection and resolution, with tiered support (Levels 1, 2 and 3) and escalation procedures to ensure rapid incident response and service continuity.

- Project management to orchestrate transition and transformation activities — overseeing technology migrations, site rollouts and process realignment to ensure timely delivery and alignment with business objectives.

- Service management to act as an agent for the enterprise, coordinating with third-party vendors, network operators and device manufacturers to support multivendor environments under a single pane of glass and ensure seamless integration. Life cycle management covers network upgrades (such as 4G to 5G), technology migrations and ongoing maintenance, including warranty and device management.

- Comprehensive performance and availability management through auditing, logging and analytics, enabling alignment with negotiated SLAs and continuous service optimization. Transparent governance models define clear roles and responsibilities between the provider and client, supported by integrated service desks, security operations centers (SOCs) and network operations centers (NOCs).

- Robust asset and usage management, delivering actionable insights for operational efficiency and billing management.

- SIM and subscription management — This capability covers any asset or device that connects (directly) to the PMN and includes the systems and services that make connectivity information visible. It also covers over-the-air (OTA) SIM management capabilities to manage single SIM, multi-IMSI SIMs, eSIM (eUiCC) and iSIM (“soft” SIM or virtual eUiCC). This capability also covers the vendor’s ability to integrate clients’ public connectivity agreements and leverage preintegrated agreements with local mobile network providers.

Optional Features

Enterprise clients increasingly expect the following additional capabilities to be included as part of end-to-end PMN service vendors’ scope, supported by vendors to varying degrees to add differentiation:

- Connectivity management portal — This capability includes the systems to administer and manage operational functions for device acquisition; provisioning and activation; ordering and provisioning capabilities across multiple vendors under a single pane of glass; inventory management; change, incident and problem management; and network performance. These portals monitor real-time utilization and asset status, generating alerts that trigger automatic actions against SIM cards or other connectivity assets in real time (for example, changing SIM status). These portals can expose APIs that are integrated with third-party systems. It also includes private 4G/5G and public network life cycle management under a single pane of glass.

- Device logistics and management — This capability includes the systems and services that make connected endpoints and managed asset information visible. It also applies health diagnostics to measure connectivity and edge device performance and manages connection options. This capability also includes processing activities and management tasks that are performed at the edge, aggregating several edge devices and filtering the information that needs to be sent to the device management platforms. It also offers analytics and reporting related to the edge device and software parameters. This device management capability may be transversal or focused on specific industry use cases, such as automotive, global asset tracking or manufacturing.

- Security management — This capability includes the systems and services to administer and enforce policies relating to identity and data access, data transmission and encryption, and the secure consumption of business services linked to PMN and PMN-connected assets. Included in this capability are private 4G/5G networks and the mechanisms that seamlessly support the transition from private networks to public cellular networks and integration with OT security policies and systems.

- Spectrum acquisition and support — This includes provision of spectrum assets for the PMN project if the supplier is already a licensed spectrum holder (typically, this would be a communications service provider [CSP]) or assistance in the application process for unlicensed/industrial spectrum as required by the enterprise client.

- 5G network slicing — Network capabilities may include 5G network slicing. This capability may be offered under a single management interface, which is preferred, or implemented via different systems.

- Edge computing services — Edge computing deployment and operation, management and orchestration, as part of the PMN infrastructure. This edge can be part of the initial project or be a later addition.

- Multisite management — Delivers a purpose-built management and orchestration framework for environments spanning multiple PMN sites, enabling centralized oversight and coordination of deployments involving different vendors and technologies under a unified systems and management model.

- PMN site connection — Provides for the interconnection of PMN site(s) where applicable.

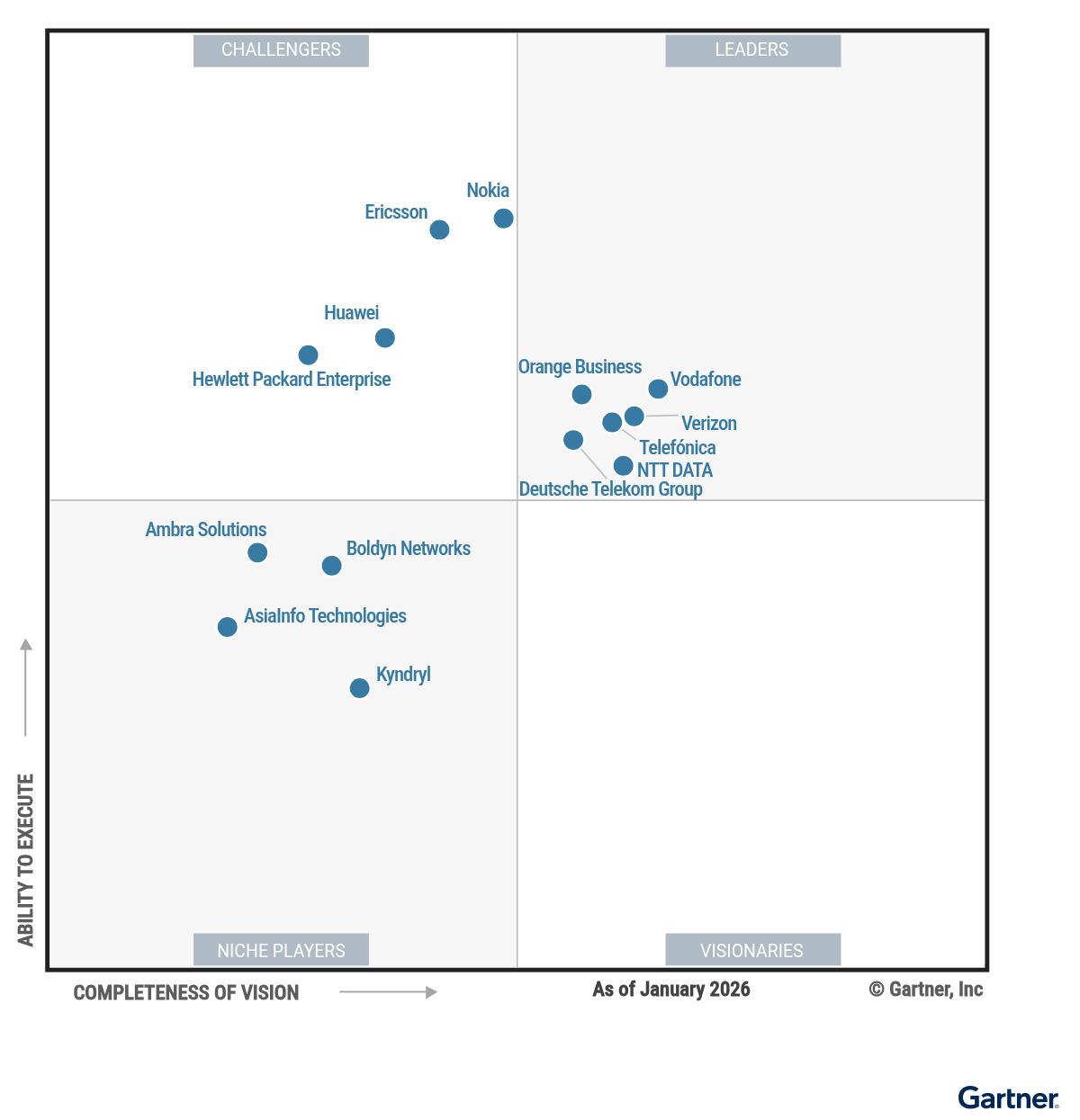

Magic Quadrant

Vendor Strengths and Cautions

Ambra Solutions

Ambra Solutions is a Niche Player in this Magic Quadrant. The privately held wireless engineering specialist and equipment manufacturer is headquartered in Canada. It provides turnkey, OT-focused private 4G and 5G services for mission-critical environments, primarily in mining, and is expanding into utilities, rail, heavy industry, and large construction sites. Its services include high-reliability voice and video communications, as well as real-time asset tracking.

As a vendor-agnostic contractor, Ambra performs all design and commissioning in-house. The company owns Canadian spectrum and manufactures proprietary rugged devices, including patented positioning systems. Recent additions include iBwave for in-building RF design, a new warehouse in Canada to optimize logistics and AI-driven network configuration to reduce PMN configuration time to just a few hours.

As of June 2025, Ambra reported 126 active sites across 14 countries spanning five global regions.

- Deep customization and technical engineering: Ambra Solutions delivers vendor-agnostic private 4G/5G services with advanced wireless engineering, including dedicated, hybrid, multisite and neutral-host PMN deployment models. Ruggedized IP67 5G devices and antennas are tailored for harsh industrial settings, while AI-driven telemetry from proprietary hardware and software enables predictive maintenance and real-time asset tracking, and minimizes downtime.

- Proven resilience in hazardous settings: With over 1,000 kilometers of underground infrastructure, Ambra deploys systems engineered for extreme vibration, metal interference and high temperatures. High availability is ensured through redundant core architectures (EPCs and switches) and 12- to 24-hour backup batteries, keeping safety-critical OT functions, such as remote machinery control and real-time gas detection, operational during power outages.

- End-to-end services and operations: Ambra offers a full project life cycle portfolio, including spectrum access, radio planning, site surveys, industrial device manufacturing, monitoring and network management. The company supports both proprietary and third-party systems (mainly Ericsson, Nokia and Cisco) and now manages brownfield PMN deployments. Support capabilities have expanded to include AI-driven configuration and proactive governance via multiple global network operations centers (NOCs), enabling 24/7 support.

- Stagnant site growth and high geographic concentration: Ambra added just 11 new sites over the past year, with nearly 70% of its overall sites concentrated in North America. Its reliance on a direct sales model rather than a broad channel ecosystem may limit scalability in regions where it lacks significant presence.

- Limited scope and lack of standardized private 4G and 5G services: Ambra focuses on custom solutions for industrial OT deployments, resulting in a limited portfolio of standardized offerings. Consequently, Ambra is not focused on sectors like healthcare, education, retail, media, and financial services, where demand for standardized, integrated solutions is increasing. It does not provide edge computing or support campus IT use cases or standard WLAN/Wi-Fi integration, making it less attractive for organizations seeking unified IT/OT connectivity or a single vendor for both WLAN and PMN environments.

- Lack of standardized productization and edge capabilities: Ambra primarily delivers its networks as tailored professional services projects rather than standardized offerings. The portfolio does not include integrated industry edge solutions that span technologies beyond communications, such as compute, storage or application enablement, though the company can take on discrete projects with its partners.

AsiaInfo Technologies

AsiaInfo Technologies is a Niche Player in this Magic Quadrant. The company offers AISWare AgileNet, an all-in-one private 5G service for vertical industries. Key components include 5G RAN with multiband base stations, a 5G core network (certified AMF/SMF/UPF) and an operations platform with edge computing. Deployments span dedicated, hybrid, campus and neutral-host models, with flexible capital expenditure and operating expenditure commercial options.

AsiaInfo focuses primarily on the China market, with limited presence in other regions, including Asia/Pacific, Europe, North America and the Middle East and Africa. Its clients include enterprises and operators in asset-intensive sectors such as energy, natural resources, mining, manufacturing, ports and education, targeting high-risk operations and high-value facilities.

Since 2024, AsiaInfo has launched solutions that include AI-integrated 5G base stations with edge intelligence. As of June 2025, the company reported 79 live sites globally across 18 deals, with 67 sites in Asia/Pacific and leveraging regional service partners outside its core market.

- Full-stack portfolio: Unlike many system integrators (SIs) that must orchestrate multiple third-party OEMs, AsiaInfo provides a fully independent end-to-end 5G stack. This vertical integration allows AsiaInfo to bypass multivendor interoperability hurdles.

- AI innovation: AsiaInfo has pioneered integrated AI, communication and computing base stations with, for example, its embedded Qwen LLM and ISAC architecture (see Note 2) for edge intelligence and wireless sensing. This enables an AI-first approach where AI is a core component of the physical network infrastructure.

- Industrial sector experience: AsiaInfo delivers full-stack solutions for safety-critical sectors with radiation-hardened base stations, nuclear facility coverage and intrinsically safe equipment for explosive environments.

- Limited regional presence: Eighty-five percent of AsiaInfo deployments are in Asia/Pacific, with 67 of its 79 operational sites located there, mostly in China. As a newer vendor without established global brand recognition or proven global commercial scale, it has the lowest number of deals in this research.

- Global servicing limitations: International service delivery relies entirely on third-party partners, which can complicate support. The company’s centralized global network operations center in China (GMT+8) also creates time-zone challenges for real-time support outside Asia.

- Missing features: Capabilities such as data-in-transit encryption, private-public handover security, over-the-air management and multivendor ordering are not available. These gaps limit the vendor’s applicability compared to some competitors.

Boldyn Networks

Boldyn Networks is a Niche Player in this Magic Quadrant. Headquartered in the U.K., Boldyn is a neutral host provider with PMN operations focused mostly in Europe, the U.K. and North America.

The company offers turnkey, dedicated, end-to-end PMN solutions encompassing design, build, operation and management, collaborating with technology partners such as Nokia and Hewlett Packard Enterprise (HPE), alongside recent additions such as Druid Software and Airspan Networks. Its top PMN verticals include mining, energy, transport hubs (including ports and airports), manufacturing, venues, and healthcare.

Boldyn’s PMN solutions include advanced capabilities like 5G slicing, traffic separation and flexible security, and quality-of-service management. The company offers managed services as well as four-tiered private 5G-as-a-service solutions, leverages SmartSIM technology for seamless roaming and provides an in-house built Edge Video Orchestrator platform for real-time video stream orchestration. Boldyn is also working to add more interactive features to its connectivity management portal.

As of June 2025, Boldyn Networks reported over 130 4G/5G PMN sites deployed across 97 deals, mostly in Europe and the U.K.

- European expansion: Boldyn expanded its presence in Germany with its acquisition of Smart Mobile Labs, reinforcing its ability to deliver and manage PMNs for European customers. This builds on previous acquisitions, strengthening the company’s overall portfolio breadth and expertise.

- Networking engineering and delivery: Boldyn offers integrated PMN and NHN solutions using a single infrastructure to streamline deployment and reduce its physical footprint. The company maintains a vendor-agnostic approach across core and RAN components, recently adding partners like Druid and Airspan, and works with specialized platform partners to bolster supply chain resilience.

- Specialist in challenging environments: Boldyn has extensive experience delivering and managing complex PMNs in mission-critical settings such as nuclear power plants, underground mines and operating hospitals. Its architectures are designed to support stringent service-level agreements up to 99.99% for critical operational environments.

- Limited geographic diversity: Ninety-seven percent of Boldyn’s current PMN deployed sites are in Western Europe, and in the U.K., with only a few in the U.S. The number of regions the vendor currently supports for PMN deployments is in the lower range among vendors in this Magic Quadrant. Eighty percent of its dedicated PMN sales force is based in Western Europe and in the U.K., with the remaining 20% in North America.

- Limited market awareness: Boldyn is among the vendors less frequently mentioned by end users in the context of private mobile network services.

- Evolving service model and integration maturity: Boldyn has expanded beyond custom-made engineering to offer standardized private-5G-as-a-service tiers and IT-focused campus solutions with Wi-Fi integration. However, the company’s transition toward these modular blueprints, with fully integrated PMN and NHN architectures, remains in development. Organizations prioritizing seamless IT/OT convergence should verify the maturity and regional availability of these services, compared to Boldyn’s proven capabilities in complex, high-availability industrial deployments.

Deutsche Telekom Group

Deutsche Telekom is a Leader in this Magic Quadrant. Headquartered in Germany, its 5G campus networks service offers various deployment models, including Campus Network S, Campus Network M, and Campus Network L, along with Campus Network Private for dedicated local networks supporting secure, high-performance connectivity in industrial IoT, automation and smart manufacturing. Its 5G Advanced Network Solutions (ANS) service, offered through T-Mobile for Business in the U.S., provides similar tiered solutions (public, hybrid, and private) across broader areas.

Deutsche Telekom is actively deploying 5G mmWave (26 GHz) and leveraging Edge Control (Local Breakout) to deliver ultra-low latency and prioritized data transmission for applications like industrial automation. This solution routes traffic to on-premises edge servers for local data processing, boosting security and supporting real-time analytics. Services span design, implementation, managed operations and tiered customer care.

Its operations are focused in Western and Eastern Europe, as well as North America, and its customers tend to be midsize and large global enterprises in manufacturing, transportation/logistics, energy/utilities, healthcare and government sectors.

Deutsche Telekom reported 377 4G/5G PMN sites deployed over 168 deals at the end of June 2025, mainly in Europe.

- Hybrid and campus networks: Deutsche Telekom has demonstrated a strong focus on hybrid and campus private 4G and 5G services, using public 5G networks in countries where it has local communications service provider (CSP) operations, including T-Mobile for Business in the U.S. This approach could be attractive for enterprises seeking more cost-effective deployments.

- Curated regional portfolio for industries: Deutsche Telekom’s European portfolio is homogeneous, featuring three products using its public 5G network that address the needs of enterprises looking for cost-effective solutions that are easy to implement, and one product with private spectrum for complex industrial environments. In the U.S., the portfolio includes three solutions for public, hybrid and dedicated.

- Flexible pricing: Deutsche Telekom offers flexible pricing models, including options for operating expenditure, capital expenditure and customized pricing structures. This allows customers to choose a financial model that best suits their operational and budgetary requirements.

- Limited geographic diversity and roadmap: Most of Deutsche Telekom’s current PMN deployments are in Europe and the U.S. The number of regions the vendor currently supports for PMN deployments is in the lower range among vendors in this Magic Quadrant. Deutsche Telekom lacks a detailed, group-level strategy for expanding its services geographically or providing unified portfolio updates across its various operating regions.

- Regional service fragmentation: Enterprise clients with projects in different regions may find that differences in the vendor’s local PMN service offering and capabilities, particularly across the U.S. and Europe, may make it more difficult to harmonize their enterprise PMN services in different countries.

- Lack of combined edge computing offer: Deutsche Telekom currently offers Edge Control/Local Breakout and does not directly commercialize a fully integrated edge compute service as part of its private mobile network portfolio, which may be a requirement for certain OT and government clients.

Ericsson

Ericsson is a Challenger in this Magic Quadrant. It is a multinational networking and telecommunications company headquartered in Sweden. Its division, Ericsson Enterprise Wireless Solutions, delivers solutions including private 5G, NHN and wireless WAN. Ericsson’s private 4G and 5G services are optimized for industrial verticals such as manufacturing, mining, ports and transport, and support mission-critical features including mission-critical push-to-talk (MC-PTT) and IMS-compliant voice.

In 2025, Ericsson started unifying its private 5G stack within Ericsson NetCloud Manager, delivering partner-serviceable architecture and single-pane-of-glass management across RAN, core and security domains. The platform now incorporates advanced AI-powered analytics, including its generative AI-Based NetCloud Assistant (ANA) and service health analytics for proactive anomaly detection. Multisite enhancements such as Ericsson Session Continuity, geographic redundancy and a centralized core architecture streamline operations and reduce TCO. The Ericsson Radio Dot System enables support for up to three public carriers and a private segment on shared infrastructure.

The number of deployed sites reported by Ericsson is among the highest for the vendors included in this research.

Ericsson did not respond to requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- End-to-end private 5G integration and management: Ericsson’s carrier-grade private 5G solution features integrated management of RAN, core, and security through NetCloud Manager, which serves as the ongoing operational interface. The architecture incorporates AI-enabled capabilities — including service health analytics, user equipment anomaly detection, and the ANA generative AI assistant for natural language troubleshooting — to support continuous monitoring and streamlined operations.

- Global vertical reach and multisite architecture: Ericsson distinguishes itself with extensive geographic coverage and focus on large-scale mission-critical and industrial networks. Ericsson is focusing on multisite capabilities such as session continuity and geographic redundancy, which are designed to reduce TCO and enhance service resilience for distributed enterprises in sectors such as logistic and manufacturing, which require seamless device mobility across multiple locations.

- Buyer awareness: Ericsson remains a prominent choice for enterprises that frequently consider Ericsson during their RFP processes for PMN services.

- Indirect sales and transactional model: Ericsson sells mainly through channel partners — CSPs, SIs, MSPs, VARs, and technology partners — who manage delivery and contracts. Vertical teams provide presales expertise for large enterprises, but transactions and ongoing management remain with partners. End-user experience depends heavily on the selected partner’s technical capabilities.

- Limited support and partner serviceability: Tier 1 support is mainly delivered by partners, while Ericsson reserves Tier 2 and Tier 3 support for escalations and fixes. The partner-serviceable architecture equips partners with CLI access and maintenance tools for Day 1/Day 2 operations. Enterprises lacking capable partners may have limited direct access to Ericsson for basic troubleshooting at scale.

- Single-vendor preference and restricted multivendor orchestration: Ericsson prioritizes its full-stack PMN infrastructure. Advanced management and analytics are optimized for Ericsson hardware, limiting multivendor RAN integration outside supported environments.

Hewlett Packard Enterprise

Hewlett Packard Enterprise (HPE) is a Challenger in this Magic Quadrant. HPE is a U.S.-based multinational information technology and service provider that offers HPE Aruba Networking Private 5G, utilizing 4G and 5G, over both licensed and shared spectrum. Wi-Fi is a separate offering also available through HPE Networking for both HPE Aruba and HPE Juniper Networking customers.

HPE Networking Private 5G is an end-to-end HPE solution with a full-stack, preintegrated solution with HPE radios. It allows integration between its 5G core, edge functionality, and HPE’s own and third-party 3GPP-compliant radios. It also has a reseller agreement with Nokia to facilitate global radio adoption. HPE offers on-premises and cloud options.

HPE offers vertical-specific solutions, including for manufacturing, mining, oil and gas, transportation, education, tactical/defense, and public safety organizations.

Full integration of the private 4G and 5G service with Mist AI remains a roadmap item.

As of June 2025, HPE reported 601 4G/5G PMN sites deployed in multiple regions, mostly Western Europe and North America.

- Unified IT-centric management: HPE’s PMN model is suited for IT teams familiar with the company’s existing Wi-Fi solutions and provides a single-vendor sourcing model. Capabilities such as HPE Aruba ClearPass Policy Manager support unified policy management across IT domains.

- Automated IT-native deployment: HPE utilizes a seven-step wizard and zero-touch automation within a cloud-native dashboard to simplify 5G deployment, reducing 3GPP complexities and allowing standard IT teams to activate production-ready networks in less than 30 minutes without specialized cellular expertise.

- Integrated mission-critical voice and radio flexibility: HPE supports voice services, including emergency calls, utilizing a 3GPP-compliant IP Multimedia Subsystem (IMS) application. This functionality allows legacy telephony integration with private branch exchange (PBX) systems for MC-PTT.

- Delayed Wi-Fi convergence: HPE markets its PMN service as a way for customers to augment their Wi-Fi. However, the foundational elements of this synergy, such as integrated interface for PMN and Wi-Fi, shared user identity, and neutral host offering, are still roadmap items, which limits seamless connectivity between PMN and Wi-Fi networks.

- Inconsistent global deployment: HPE’s portfolio is bifurcated, offering a seamless cloud-managed deployment model primarily for the U.S. (Citizens Broadband Radio Service [CBRS]), while forcing global sites to use an on-premises approach built on HPE’s private 5G core that requires significant in-house expertise for separate radio integration. This fragmentation creates operational inconsistency and deployment challenges for multinational enterprises that may find it difficult to achieve a consistent deployment and management experience across their global sites.

- Third-party Wi-Fi friction: While HPE supports open APIs and standard interfaces for cross-domain provisioning and authentication, integrating non-HPE Wi-Fi networks currently requires custom professional services to establish protocols and design rules. This creates a synergy gap for enterprises with heterogeneous environments, compared to the native, unified policy and management experience HPE is developing for its own Aruba and Juniper portfolios.

Huawei

Huawei is a Challenger in this Magic Quadrant. The company delivers end-to-end private 4G and 5G services, from initial site survey planning, commissioning and engineering implementation to ongoing assurance services and software-driven operation optimization. Huawei’s product strategy involves developing solutions for industrial scenarios, such as its Intelligent Twins products. It is embedding service capabilities directly into hardware. The company’s operations are primarily in the Asia/Pacific, Middle East and Africa, and Latin America regions; it targets verticals that include mining, manufacturing, power and transportation.

The number of deals reported by Huawei is among the highest for the vendors included in this research, with over 10,000 deployed sites as of June 2025, mainly in China, with most projects sold via operators (China Mobile, China Telecom and China Unicom) and delivered by Huawei.

- Full-stack product portfolio and network integration: Huawei offers end-to-end capabilities from RAN to core, supported by a global ecosystem. Its private 5G services can integrate 5G, wired and Wi-Fi networks into unified deployments, enabling complex scenarios such as macro-micro coordinated coverage and high-density small cell deployments in challenging industrial environments.

- Standards leadership: Huawei is a leading contributor of technical proposals in areas like network automation and deterministic networking.

- Unified management: The platform provides unified life cycle management for both private and public networks within its private 4G and 5G service features.

- Geographic concentration: Huawei’s PMN deployments are heavily focused in Asia/Pacific, primarily the Chinese mainland, with other deployments in Latin America, the Middle East and Africa, and Europe. Ninety percent of its installed base for PMN services is in China.

- Geopolitical and regulatory exposure: The company is subject to ongoing geopolitical tensions between the U.S. and China. Alongside a limited strategy outside China, this environment creates regulatory uncertainty that can directly limit its market access.

- Geographic variance: Huawei leverages its full-stack capabilities to mostly offer a broad, horizontal 5GtoB platform internationally with selective customization, with its most specialized private 5G solutions concentrated in China.

Kyndryl

Kyndryl is a Niche Player in this Magic Quadrant. Kyndryl is a multinational IT infrastructure services provider headquartered in the U.S. The company offers PMN-managed services that span across Nokia Digital Automation Cloud (DAC), Nokia Modular Private Wireless (MPW), and HPE Athonet Mobile Core capabilities coupled with Airspan Radio Access Network. This multivendor PMN solution enables greater autonomy over application integration. Kyndryl adds its overlay service layer and additional capabilities such as the integrated Kyndryl Bridge platform for network operations and management.

Kyndryl offers private 4G and 5G network sourcing and design services across all major regions. Its customers are mainly in the manufacturing, chemical, oil and gas, and mining sectors.

The company delivers PMN design and planning, sourcing, implementation and integration services. Kyndryl has added neutral host network capability as part of its hybrid PMN offering, as well as unified SIM support, with plans to add AI-based enhancements and increased life cycle management capabilities.

As of June 2025, Kyndryl reported approximately 48 sites (and over 50 managed sites), mostly in the U.S.

- Diversifying industrial expertise: Kyndryl maintains a strong focus on the industrial vertical and has developed deep expertise in dedicated PMN use cases. The addition of NHNs and SIM support positions Kyndryl to expand into new verticals and address broader use cases.

- Flexible architecture options: The expanded portfolio gives customers the option of selecting either an end-to-end PMN based on Nokia solutions or a multivendor offering that supports RAN from different vendors with the HPE Athonet core.

- Automated operations: Kyndryl Bridge supports automated operations and client onboarding through integration with IT service management ticketing systems. The software’s AI capabilities provide observability and orchestration across the PMN.

- Limited nonindustrial scale: While Kyndryl offers robust edge computing capabilities through the Nokia MX Industrial Edge (MXIE) platform — hosting mission-critical applications like High Accuracy Indoor Positioning (HAIP) and connected worker solutions — its current lack of network slicing support may restrict its suitability for complex campus IT environments that require dynamic traffic segmentation. Furthermore, its deployment footprint remains heavily concentrated in industrial OT sectors, potentially limiting its proven experience in broader commercial or general enterprise settings.

- Geographic concentration: The company continues to lack deployment scale across multiple geographies, with deployed sites concentrated in the U.S., Canada and the Netherlands — a global scale that is among the lowest in the vendors in this report. Furthermore, its hybrid private 4G and 5G services are currently specific to the U.S. market (and further constrained by the fact that it only supports T-Mobile and AT&T), which restricts its ability to serve multinational enterprises requiring consistent global implementations.

- Low client footprint: Kyndryl’s reported number of PMN services deals is among the lowest in the group of vendors in this Magic Quadrant.

Nokia

Nokia is a Challenger in this Magic Quadrant. The company offers private 4G and 5G services, including Nokia Digital Automation Cloud and Modular Private Wireless . Key components include 4.9G/5G radios, Nokia MX Industrial Edge and an extensive application catalog. Deployments span fully customizable, cloud-based as-a-service and hybrid PMN models.

Nokia’s operations are geographically diversified, serving enterprises and government entities across manufacturing, mining, ports, energy and public safety. Nokia One Platform for Industrial Digitization now integrates MX Workmate, an OT-compliant GenAI for workers, and MX Grid, which enables industrial far-edge distributed AI compute.

As of June 2025, Nokia reported over 920 private 4G/5G network customers and over 1,500 sites across seven regions, with the majority in North America and Europe, and most deployments delivered through service partners.

In November 2025, Nokia announced it is reviewing the future direction of its PMN business. Nokia declined requests for supplemental information. Gartner’s analysis is therefore based on other credible sources.

- Global coverage: Nokia’s private 4G and 5G services are available worldwide across the Americas, Western Europe, the Middle East, Africa, advanced APAC markets and Antarctica.

- Market recognition: Nokia is frequently considered by enterprises in RFP processes, as reflected in Gartner inquiries. Nokia is also the top infrastructure partner selected for PMN RAN and core deployments, especially in manufacturing and mining.

- Integrated end-to-end PMN services: Nokia’s DAC is optimized for large-scale enterprise and government PMN deployments that require minimal customization and can scale down for smaller sites with DAC PW Compact.

- Channel partner dependency: Over two-thirds of Nokia private 4G and 5G services sales are through indirect channel partners, rather than Nokia acting as prime contractor to the enterprise. This indirect focus is expected to increase following the company’s latest strategy update.

- No multivendor support: Nokia does not support multivendor private network deployments in its management and orchestration tools, and only provides a single-vendor solution. This limits its ability to deliver diverse configurations or best-of-breed private 4G and 5G services.

- Narrow vertical focus: While Nokia addresses multiple verticals, it relies exclusively on partners for non-OT segments. Clients in verticals outside manufacturing and OT industries should confirm support and experience with their requirements.

NTT DATA

NTT DATA is a Leader in this Magic Quadrant. Part of the NTT Group and headquartered in Japan, NTT DATA provides IT solutions and international communications services.

The company provides professional and managed end-to-end private 4G and 5G services, with core and RAN options from partners including Celona, Cisco, Ericsson, Nokia and GXC. 4G and 5G PMN services are available in Latin America, Asia/Pacific, the Middle East, Africa and Canada. Its customers span the manufacturing, transportation and logistics, automotive, energy and utilities, healthcare, mining, airports and ports, oil and gas, and smart cities sectors. Additional partnerships support edge computing, 5G devices, and industrial edge AI applications.

NTT DATA’s native offerings include client-facing PMN management portals and dashboards such as NTT DATA Network Orchestrator, NOC and SOC systems for PMN management and support, and NTT DATA Edge Compute (including GPUaaS). It also offers Edge AI and Transatel mobile virtual network operator (MVNO) physical and embedded subscriber identity modules (pSIMS and eSIMs) for private to public roaming, as well as PMN use case development and testing, PMN interoperability testing for 5G devices, and device as a service (DaaS; see Note 1).

The company has expanded regional availability, spectrum partnerships and added neutral host capability with the PMN service.

As of June 2025, NTT DATA had 148 deals and 152 sites, with most deployments in North America and Europe.

- Global reach and full-stack services: NTT DATA delivers PMN deployments across North America, Europe, Africa and Asia/Pacific, backed by strong local sales teams and global managed services and support. Its portfolio spans full-stack services that include IoT connectivity, managed network and security, application development and system integration, enhanced by edge computing and AI, with preintegrated solutions for smart factory, connected workforce, machine vision and digital twins.

- AI-driven operations and centralized management: NTT DATA uses agentic AI and machine learning for anomaly detection, capacity forecasting and autonomous monitoring, reducing resolution times for proactive management of network incidents. The proprietary NTT DATA customer portal platform provides centralized management of private 5G and multivendor network services, with advanced API integrations for Celona, Cisco and other environments.

- Strategic spectrum and hybrid network services: NTT DATA helps clients navigate spectrum regulatory processes through direct acquisition or partnerships with mobile network operators for spectrum licensing. The company supports flexible PMN architectures, including NHNs using CBRS in the U.S., and offers multioperator core network gateways for continuous public/private network coverage.

- Stand-alone deployment focus: Although seamless public-private integration is available through the core private 5G portfolio and Transatel MVNO services, the primary focus of NTT’s private 4G and 5G services’ remains on stand-alone, LAN-integrated private networks. This may require careful validation by enterprises prioritizing the native public network slicing and ubiquity typically associated with CSP-led hybrid models.

- Organizational complexity: The ongoing integration of NTT Ltd and NTT DATA combines multiple IT service offerings across different legal entities. This can increase complexity for clients when projects require coordination across several NTT teams or involve services beyond PMNs.

- Advanced feature maturity lag: While granular QoS, performance visibility, and network/RF observability are available, NTT DATA leverages partner solutions to deliver these capabilities. This approach implies that achieving deep, slice-level monitoring in complex industrial scenarios depends on the seamless integration of third-party tools, rather than a proprietary, single-stack operational console.

Orange Business

Orange Business is a Leader in this Magic Quadrant. The company offers managed PMN services encompassing consultation, design, build and run phases. Its solutions leverage capabilities such as 5G stand-alone and core network slicing; the solutions integrate with edge computing, IoT, data analytics and security. Orange provides options for stand-alone, hybrid and virtual PMN models.

Orange’s operations are primarily focused in Europe, while maintaining a strong presence in the Middle East and Africa. The company’s strategy centers on OT digitization in core verticals, including manufacturing, transport and logistics. In 2025, Orange launched a public-private dual-slice hybrid mobile private network offering. The company is also investing in industrializing operating models for hybrid and virtual PMNs over 5G stand-alone.

As of June 2025, Orange Business reported 62 deals and 143 sites deployed, mostly in Europe.

- Vertical/industry focus: Orange tailors private 4G and 5G services to verticals requiring deep integration of IT and OT capabilities, focusing on delivering tangible business outcomes in critical environments.

- Managed security: The company integrates managed OT industrial security services into its solutions via subsidiary Orange Cyberdefense, supported by more than 150 in-house IT/OT experts.

- Global operations: Orange provides global coverage supported by its Global Delivery & Operations organization, which operates a 24/7 follow-the-sun model with six service operation centers located across Africa, America, Asia and Europe.

- Geographic concentration: While Orange is actively scaling its global reach, with early traction in North America and the Middle East and Africa, more than 90% of Orange’s commercial PMN deployments and active POCs are concentrated in Western Europe. International customers seeking consistent global deployments must verify Orange’s field capabilities and local support outside this core region.

- Wi-Fi integration: Orange does not see a market demand for a native link between its private 4G and 5G services and traditional Wi-Fi networks in campus environments. For seamless roaming between cellular and Wi-Fi networks, customers must undertake complex custom integration, potentially increasing project risk and operational burden.

- NHN solutions: Orange does not currently offer integrated PMN and NHN solutions, although they are testing combined operator and private frequency solutions for future sourcing. Nowadays, Orange only sees potential interest in co-financed deployments for this capability in the U.S. market.

Telefónica

Telefónica is a Leader in this Magic Quadrant. Telefónica is a global CSP and next-generation solution provider headquartered in Spain. Telefónica PMN offerings leverage mainly Ericsson, Nokia DAC and Nokia MPW as key RAN and packet core partners. The company has expanded its core portfolio to include solutions from HPE, Cisco and others. PMN services are delivered through Telefónica Tech, which acts as a global integrator utilizing its proprietary orchestration platform, and Telefónica local operating companies. Telefónica offers dedicated PMNs (on-premises) across Europe, Latin America and hybrid PMNs primarily in Spain and Brazil, with availability expanding to Germany and the U.K.

Telefónica’s primary industry focus continues to center on energy (mining, oil and gas) and manufacturing, while significantly increasing presence in universities and innovation centers, security and defense, and airports.

Telefonica’s planned additions emphasize seamless deployments, achieving general availability for network slicing and Open RAN solutions, and major platform improvements. This includes refining its unified orchestration platform, NearbyOne, by introducing new troubleshooting capabilities, deeper portal integration, and increased AI/ML features for predictive maintenance and network configuration.

As of June 2025, Telefónica reported 104 4G/5G PMN sites deployed globally across 53 deals in Europe and Latin America.

- Broad multivendor portfolio: Telefónica has dedicated PMNs in Western Europe, Latin America and the U.S., including Wi-Fi integration, proprietary and AWS edge stacks, security, and cloud and edge orchestration and management, with different support levels and additional packet core vendor integration (Nokia, Ericsson, HPE and Cisco). Telefónica also offers hybrid PMNs with dedicated packet core and RAN sharing and roaming to public networks in Spain, Germany and Brazil, integrated with its Kite Platform for IoT.

- Advanced end-to-end industrial private 4G and 5G services: This capability was significantly enhanced by the acquisition of Geprom, strengthening specialized consulting and SI services for manufacturing enterprise software solutions from vendors like Siemens and ABB. It further expands its PMN offering with edge computing, security, AI/ML, blockchain, IT/OT integration, mobile robotics and connected assets. All deployed technologies undergo mandatory prevalidation and certification for interoperability in Telefónica Tech’s TheThinX laboratory.

- Latin American market leadership: Telefónica reports 57 active sites deployed across dedicated PMN (21 sites), hybrid PMN (one site) and multisite scenarios (35 sites) in Latin America as of June 2025, with deployments spanning Brazil, Chile, Ecuador, Mexico and Peru, supporting mission-critical use cases such as autonomous trucks, real-time monitoring and anticollision detection in open pit mines.

- Limited geographic diversity: Most of Telefónica’s current PMN deployments are in Western Europe and Latin America, with a small sales force in the U.S. and no presence in other regions. Enterprises should verify with Telefónica its capabilities in other regions, as the number of countries it supports for PMN deployments is among the lowest in this Magic Quadrant.

- Limited integrated portal: Telefónica lacks a unified customer portal for its multivendor portfolio. While its internal NOC uses proprietary orchestration for integration, customers are restricted to a ServiceNow incident system. Deep administrative control requires vendor-specific portals or managed services

- Limited solution customization: Telefónica relies heavily on external vendors for Level 3 technical support and core product components, risking slower bug fixes. This multivendor approach imposes limited deep customization on the end solution and impedes the implementation of key advanced features.

Verizon

Verizon is a Leader in this Magic Quadrant. Headquartered in the U.S., Verizon offers its Private 5G Network service, marketed as a robust, secure and scalable wireless network tailored to business-critical applications. The network can leverage Verizon’s licensed 4G/5G and CBRS spectra (in the U.S.), and its industrial spectrum internationally. The portfolio includes multivendor configurations (such as Celona, Ericsson and Nokia) depending on enterprise size, customer use case, deployment complexity, and RAN and packet core combinations.

Verizon has relationships with various industry-specific partners — for example, with NVIDIA to create AI-powered solutions that run on Verizon 5G Edge with Private MEC. Verizon sells private 4G and 5G services in industries that include manufacturing; transportation and logistics; healthcare, life sciences and pharmaceuticals; energy, oil and gas, mining and utilities; and sport, media and entertainment.

Private 4G and 5G services are currently available for network end-to-end sourcing in regions across the Americas (United States, Canada, Mexico, Brazil, Chile), Europe (including the U.K., Germany, Finland, France, Spain, Ireland and a dozen other countries), and Asia/Pacific (Australia, Japan). Additionally, Verizon can support implementations outside these regions as a custom engagement.

As of June 2025, Gartner estimates that Verizon has 115 4G/5G PMN sites deployed, mostly in North America, across 70 deals.

- Well-curated portfolio: Verizon covers enterprise segments by leveraging RAN and packet core technology solutions from Celona, Ericsson and Nokia. It addresses midsize to global enterprises as well as the public sector, leveraging all major OEMs: Ericsson, Nokia and Celona.

- End-to-end private 4G and 5G services: Verizon delivers comprehensive solutions by integrating its PMN offering with adjacent technologies, including NHNs, managed IoT connectivity, security, edge computing, voice/data and video analytics. The company is actively expanding its ecosystem of solution integrators, device OEMs and application developers to enable the co-creation of specialized, repeatable solutions for critical business outcomes. Verizon also enhances security using Subscriber Concealed Identifier (SUCI) support for 5G stand-alone connections, aligning with a zero-trust security model.

- Unified management and orchestration: Verizon’s unified platform, On Site Network Dashboard (OSND), provides a centralized, vendor-neutral, single-pane-of-glass experience, and is fully integrated with Ericsson and Nokia. OSND integrates with the ThingSpace IoT connectivity management platform and monitors private edge compute solutions, including AWS Outposts. Back-end efficiency relies on the proprietary Flow360 tool, automating solution design, quoting, ordering and contracting. This streamlines the customer journey and drastically reduces contract creation and deployment time.

- Narrow geographic scope: Most of Verizon’s current PMN deployments are in the U.S. (Gartner estimates over 90 percent), with a few in Western Europe and Latin America. Over 90% of its sales force is based in the U.S., with the remaining 8% primarily in Western Europe, and a small presence in Asia/Pacific (specifically Australia and Japan).

- Limited capabilities outside the US: Enterprises should assess Verizon’s offering outside the U.S. for their specific scenario. While Verizon leverages its U.S. expertise in RF design for international customers, it collaborates with partners for delivery and deployment and does not offer access to CSP public networks.

- Advanced features support: Advanced features, including PMN slicing configuration and slice affinity for edge computing, are currently offered as custom solutions, but are not yet part of the standard portfolio.

Vodafone

Vodafone is a Leader in this Magic Quadrant. It offers managed private 4G and 5G services, including design, build, operation and managed services. It employs a multivendor strategy, primarily leveraging HPE Athonet, Nokia and Huawei for core network functions and integrating RAN components from Ericsson, Huawei and Nokia. It offers dedicated, hybrid, campus and segregated PMN deployment models.

Vodafone’s operations span 19 countries and 46 partner markets, with Europe as its primary market. Its clients tend to be large enterprises and multinational companies in manufacturing, energy, logistics, ports, sport venues, universities, and research institutions. Since 2024, Vodafone has commercially launched a fully embedded eSIM solution and it is expanding its dedicated MEC, built on Azure Stack HCI, to support ultra-low-latency applications.

As of June 2025, Vodafone reported 169 sites across 53 deals in all regions, mostly Europe (90 percent).

- Unified multivendor orchestration: Vodafone’s proprietary management plane console provides a single dashboard for multivendor orchestration and visibility across the PMN environment. This platform integrates with Nokia and HPE packet cores, as well as Ericsson, Nokia and Huawei radios, simplifying monitoring, asset management and SIM life cycle control.

- Seamless public-private mobility: Vodafone offers hybrid private 4G and 5G services, using technologies like multioperator core network to enable seamless device mobility between dedicated private networks and public networks.

- Flexible financial models: The portfolio supports flexible financial structures, including full OPEX/subscription models like PMN as a service, hybrid CAPEX/OPEX and traditional CAPEX deployment. Vodafone is developing outcome-based pricing and tiered service-level agreements to align costs directly with application requirements.

- Geographic concentration: Vodafone’s deployment history and sales and service staff remain heavily concentrated in Western Europe. Customers operating outside this core region should expect reliance on centralized resources and local third-party partners whose standards may vary.

- Service portfolio: Vodafone has not yet deployed an integrated solution connecting cellular PMN and on-campus Wi-Fi networks within a single environment. Enterprises seeking seamless mobility and unified connectivity management between cellular and Wi-Fi devices must budget for custom integration work.

- Pricing: Vodafone uses a “cost-plus” model for customizations and nonstandard network components, such as RAN sourcing. Enterprises should scrutinize costs for necessary integrations outside of Vodafone’s standard product bundles.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor's appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

- AsiaInfo Technologies

- Huawei

Dropped

- Fujitsu: Offers end-to-end managed private 4G and 5G services, combining proprietary Fujitsu technology (PW300) with Ericsson’s EP5G as a strategic partner. The vendor did not meet the Magic Quadrant criterion of having deployed private 4G and 5G services as a prime contractor in at least three new commercial contracts won or new contract(s), resulting in at least three new facilities from 1 April 2024 to 30 June 2025.

- Tech Mahindra: Offers a suite of private 4G and 5G services through a provider-agnostic, end-to-end approach. Its 5G4E portfolio includes consulting, planning, design, build, deployment and management, targeting large deployments. The vendor did not meet the Magic Quadrant criterion of having at least 25% of commercial contracts (excluding POCs) for 4G and 5G PMN services managed by the vendor, where it is the prime contractor with the enterprise (i.e., sourcing directly) or having at least 50 direct contracts (excluding POCs) as of June 2025.

Inclusion and Exclusion Criteria

To be included in this Magic Quadrant assessment, vendors had to meet all of the following criteria by 30 June 2025 (the cut-off date):

- At least 25 direct, deployed commercial contracts or 25 direct, deployed commercial sites (excluding POCs) for 4G and 5G private mobile network services are managed by the vendor, where it is the prime contractor with the enterprise (end user) — in other words, sourcing directly (not through a third party).

- At least 25% of commercial contracts (excluding POCs) for 4G and 5G private mobile network services are managed by the vendor, where it is the prime contractor with the enterprise (end user) — in other words, sourcing directly (not through a third party).

- If the vendor has less than 25% direct contracts, it must have at least 50 direct contracts (excluding POCs).

- Commercial contracts in two or more regions where the vendor is the prime contractor, (excluding POCs) for 4G and 5G private mobile network services provided by the vendor. Regions are defined as follows:

- North America

- Latin America

- Europe

- Asia/Pacific

- Middle East and Africa

- New business won where the vendor is the prime contractor (excluding POCs), for 4G and 5G private mobile network services managed by the vendor in the last 15 months (1 April 2024 to 30 June 2025).

- Either: at least three new commercial contracts won

- Or: new contract(s) resulting in at least three new facilities

- Provide the following capabilities defined in this Magic Quadrant, as the prime contractor (first-party or through a third party):

- Network end-to-end sourcing

- Network design

- Implementation and integration

- Service management and support

- SIM and subscription management

Honorable Mentions

Celona is a specialist PMN network equipment vendor headquartered in the U.S. Its end-to-end Celona 5G LAN solution includes radios, core, edge, and management and orchestration functionality, as well as neutral host options. In addition, Celona offers RF design, network deployment and operations support. The solution can be deployed either as self-managed network infrastructure as a service, or as a managed service sold and delivered almost entirely through partnerships with resellers, CSPs (e.g., Verizon in the U.S., stc in the Middle East, and Vodafone worldwide) and global system integrators (e.g., NTT DATA, HCLTech and Tech Mahindra).

Over 80% of Celona’s current footprint is in the U.S. Celona’s PMN infrastructure is relevant to include in PMN service projects.

The vendor’s business model is to sell through partners and CSPs, and so did not meet the PMN services Magic Quadrant criteria of having at least 25 direct, deployed commercial contracts or 20 direct, deployed commercial sites (excluding POCs) and at least 25% direct contracts.

Fujitsu offers end-to-end managed private 4G and 5G services positioned as an innovation platform for digital transformation. These solutions leverage flexible architectures that combine proprietary Fujitsu technology (PW300) with Ericsson’s EP5G as a strategic partner.

Its customers are typically large enterprises in manufacturing, transport (airports and ports) and utilities.

As of July 2025, a stand-alone network communications subsidiary named 1FINITY, consolidates Fujitsu’s global network-related organizations under one brand. Fujitsu’s 4G and 5G PMN service operations are mainly concentrated in Asia/Pacific, primarily in Japan.

The vendor did not meet the Magic Quadrant criterion of having deployed PMN services as prime contractor in at three new sites or regions from 1 April 2024 to 30 June 2025.

Highway 9 Networks is a solution provider headquartered in the U.S., and delivers a PMN that tightly integrates with enterprise IT networks and security tools/policies, as well as mobile network operators. Delivered via partners, the solution is aimed at enterprises (e.g., dedicated PMNs, indoor/outdoor coverage and neutral host), and can be deployed on premise, via the cloud or virtual machine.

The solution leverages the availability of freely licensed spectrum and the multi-eSIM capability included in modern devices, along with a software-defined 5G full stack, delivered as a SaaS service via the Highway 9 Mobile Cloud.

Highway 9 is relevant for enterprises located in the U.S.

The vendor did not meet the Magic Quadrant criterion of having deployed PMN services as a prime contractor in two or more regions as of 30 June 2025.

ZTE is an IT technology solution provider headquartered in China. It offers a comprehensive private 4G and 5G services portfolio spanning RAN, core, transport, design, build, system integration, operation and maintenance services. Most of its delivery is through CSPs. ZTE’s operations are primarily based in China, with key customers in manufacturing, transportation, mining, steel and power utilities.

ZTE’s private 4G and 5G services are particularly relevant for enterprises based in China, either directly or through CSP partners.

The vendor did not meet the Magic Quadrant criterion of having deployed PMN services as prime contractor in at least two regions as of 30 June 2025.

ZTE did not respond to requests to review the draft contents of this document. Gartner’s analysis is therefore based on other credible sources.

Evaluation Criteria

Ability to Execute

Gartner evaluates vendors on the quality of their multiregion, end-to-end PMN services offering that enables enterprises to improve their operational performance and efficiency, and to positively impact revenue, retention and reputation within Gartner’s view of the market. Ability to Execute is judged by seven main criteria:

Product or Service: Core goods and services that compete in and or serve the defined market. This includes current product and service capabilities, quality, feature sets, skills, and more. This can be offered natively or through OEM agreements/partnerships, as defined in the Market Definition.

The emphasis is on comprehensive and advanced offerings, strong interoperability and interworking across all elements of the offer, whether offered as first party or via partners. It also emphasizes robust security offerings and flexible support for diverse usage as well as deployment scenarios, including in cloud environments.

We evaluated the vendors based on the offering’s capabilities that are covered in this Magic Quadrant as of 30 June 2025. We also considered specific offerings per segment, preintegrated functions with ecosystem partners, productized versus project-based offering for each segment, and geographic availability of each of the offerings (global/regional/local).

The following capabilities were considered: dedicated/stand-alone capabilities, hybrid PMN, PMN with core network slicing, and campus and level of integration with WLAN solutions. We also considered PMN for industrial sites, including OT security capabilities and compliance, as well as multisite capabilities, including capabilities to provide a centralized life cycle management experience for all included sites.

Other factors considered were radio planning and site survey capabilities; the modularity of the offer; public network integration capabilities (private/public handover features); service management options (self-service, co-managed, fully managed); API capabilities; and integrated capabilities with other related, prepackaged technologies and services, such as IoT, MEC, managed mobility, cloud, security, and industry edge applications.

Overall Viability: Viability includes an assessment of the organization’s overall financial health, as well as the financial and practical success of the business unit. It also includes our assessment of the organization’s likelihood to continue to offer and invest in the solution, as well as the solution’s position in the current portfolio.

Sales Execution/Pricing: The organization’s capabilities in all presales activities and the structure that supports them. This includes quantifying overall PMN deployments across segments, industry verticals, geographies and technologies, and the balance of direct versus indirect sales (with a focus on analyzing direct sales). It also includes negotiation, presales support and the overall effectiveness of the sales channel, as well as the vendor’s price competitiveness and account management experience.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization’s message in order to influence the market, promote the brand, increase awareness of products and establish a positive identification in the minds of customers. This mind share can be driven by a combination of publicity, promotional activity, thought leadership, social media, referrals and sales activities.

Customer Experience: Products and services and/or programs that enable customers to achieve anticipated results with the products evaluated. Specifically, this includes quality supplier/buyer interactions, technical support or account support. This also may include ancillary tools, customer support programs, availability of user groups, service-level agreements, and more.

Operations: The ability of the organization to meet goals and commitments. Factors include the quality of the organizational structure, skills, experiences and programs. It also includes roles like project and service managers, help desk support structure, systems and other vehicles that enable the organization to operate effectively and efficiently. We also evaluated SLAs and credits offered by the vendors and NOC and SOC organizations.

Ability to Execute Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | High |

Market Responsiveness/Record | Medium |

Marketing Execution | Low |

Customer Experience | High |

Operations | High |

Source: Gartner (March 2026)

Completeness of Vision

Gartner evaluates service providers on their ability to articulate logical statements convincingly about the market’s current and future direction, innovations, customer needs, and competitive forces, and on how well these correspond to Gartner’s position. Ultimately, we rate providers on their understanding of how they can exploit market forces to create opportunities for their organizations. Completeness of Vision is judged by seven main criteria:

Market Understanding: Ability to understand customer needs and translate them into products and services. Vendors that show a clear vision of their market — listen, understand customer demands, and can shape or enhance market changes with their added vision. We also evaluated the vendor’s ability to see the PMN in the wider context of enterprises’ overall transformation was of particular importance in our evaluation, provided this insight is reflected directly by the vendor, or service provider, in the solution roadmap and design. We also evaluated the vendor’s ability to understand and address the evolving sourcing and contracting requirements of the segments it serves, including the evolving competitive and partner landscapes.

The vendor was evaluated based on its global reach when acting as a prime contractor, and its ecosystem play, particularly across Wi-Fi vendors, edge computing/MEC, segments and industries. We also considered the vendor’s ability to differentiate based on market understanding and its multiple-facility deployment strategy for a single client.

Marketing Strategy: Clear, differentiated messaging consistently communicated internally, and externalized through social media, advertising, customer programs, events and positioning statements. We evaluated the alignment of the vendor’s private mobile network solution core marketing strategy with its current market position and its overall 5G private mobile network solution portfolio strategy, including a market segment focus.

We also evaluated the structure of the vendor’s marketing function and the role PMN marketing plays in the sales process. We also considered projected and ongoing PMN-related investments in the marketing function.

Sales Strategy: A sound strategy for selling PMN solutions that uses the appropriate channels, including direct and indirect sales, marketing, services and communication. This includes partners that extend the scope and depth of market reach, expertise, technologies, and services, as well as each vendor’s customer base.

We also evaluated the vendors’ pricing strategy and distribution channels for different scenarios. The vendors were assessed on their homogeneous and global sales strategy across the entire service portfolio with focus on the direct channel. Indirect sales channels were evaluated as an add-on, but are not the focus of this Magic Quadrant. We also evaluated the structure of the sales function, and projected and ongoing investments in terms of governance and end-to-end sales processes relating to global, regional and local sales efforts. The homogeneity of the partner ecosystem strategy across segments, technologies and industries was also considered.

This evaluation also considered projected and ongoing investments in the channel partner strategy, the vendor’s pricing strategy, and whether the vendor was moving into a solution-oriented approach for each industry, where PMNs are one component of the solution together with IoT, MEC, managed mobility, cloud, security, industry-edge applications, or other technologies and services.

Offering (Product) Strategy: An approach to product development and delivery that emphasizes market differentiation, functionality, methodology, and features as they map to current and future requirements. This encompasses innovation, level of conformance/adherence to 3GPP standards or initiatives, differentiation, and considerations such as solution performance, architecture, scalability, and portfolio comprehensiveness. Vendors were assessed on the scope of their offering, and planned or ongoing investments in capabilities covered in this Magic Quadrant, as well as specific offerings per segment and productized versus project-based offerings for each segment.

Capabilities covered by this Magic Quadrant included dedicated/stand-alone, hybrid PMN, PMN with core network slicing, campus and level of integration with WLAN solutions. Capabilities considered also included PMN for industrial sites, including OT security capabilities and compliance; multisite, including management capabilities to provide a centralized life cycle management experience for all included sites; and PMN offerings for small and midsize businesses.

This evaluation category also considered PMN-related acquisitions or strategic partnerships to add capabilities to the PMN offering, radio planning and site survey capabilities, and the modularity of the offer. We further considered the vendor’s flexibility to offer an open partner ecosystem for core PMN elements (radio, core network, monitoring and life cycle management, edge/cloud computing infrastructure stack, SIM management).

Public network integration (private/public handover features) and service management options (self-service, co-managed, fully managed service) were also part of the evaluation. Finally, we considered API capabilities and bundling capabilities with other related prepackaged technologies and services such as IoT, MEC, managed mobility, cloud, security. and industry-edge applications.

The vendor’s business model was also considered. This included the design, logic and execution of the vendor’s business proposition to achieve continued success, as well as its value proposition, revenue models, customer segmentation, distribution channels, and so on. We considered whether the vendor appropriately used build/buy/partner options to maximize profitability, and its management of customization costs. Finally, we considered its use of automation to improve cost-efficiency.

Additionally, the vendors were assessed based on the scope of the spectrum offered, for both regulated and industrial spectra (CBRS type). They were assessed on POC models, their flexibility in offering capex and opex models, and the flexibility to have clients bring their own partners.

Vertical/Industry Strategy: The strategy to direct resources (sales, solution, development) and skills to meet the specific needs of individual market segments, including verticals. We evaluated the vendor’s ability to organize sales and marketing in support of vertical-specific target markets, showing evidence of knowledge of how to deploy specific go-to-market strategies across industries. We also assessed their ability to develop vertical-specific propositions, with evidence of solution adoption within each industry, including number of deployments, use cases deployed and geographic scope. Finally, we considered the vendor’s ongoing or planned investments for the purpose of developing additional vertical sectors to target.

Innovation: Direct, related, complementary, and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or preemptive purposes. This encompasses the vendor’s ongoing demonstration of technological expertise and leadership, allocation of adequate R&D budget, involvement in and contribution to the evolution of the private mobile network solutions sector, and facilitation of ecosystem partner support, as well as fostering co-innovation through collaborative initiatives with partners, customers, industry forums, and other stakeholders. This also includes innovating in commercial models and practices.

Geographic Strategy: The provider’s strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels and subsidiaries, as appropriate for that geography and market. This includes evidence of deployments across different regions at scale and planned or ongoing investments to increase geographical scope.

Completeness of Vision Evaluation Criteria

| Evaluation Criteria | Weighting |

|---|---|

Market Understanding | High |

Marketing Strategy | Low |

Sales Strategy | Low |

Offering (Product) Strategy | High |

Business Model | Medium |

Vertical/Industry Strategy | Medium |

Innovation | High |

Geographic Strategy | High |

Source: Gartner (March 2026)

Quadrant Descriptions

Leaders

Leaders primarily sell and deliver PMN services directly, investing in a PMN services future that includes a continuum of value from infrastructure to services; orchestration and management platforms; and related analytics. They perform skillfully and often exceed expectations. Leaders have a clear vision of the market’s direction and develop competencies to maintain their leadership. Leaders engage customers and provide value across several geographies. They shape the market, rather than follow it, and they often set the benchmark for market growth.

Leaders have the size and scale (for example, operations, sales and marketing, and formal bid and product management) to pursue panregional and multinational opportunities for PMN service across a number of industry verticals. They have established a robust and diverse ecosystem of technology alliances and service delivery partnerships, spanning PMN and services for network, IT, OT and IoT to meet broad market requirements.

Leaders typically have a significant number of commercial references for the PMN services market. They also have momentum in this area, as exemplified by new contract wins. They have a broad portfolio and, even where they need partners, they are often enterprises’ preferred primary vendors. They appear frequently in enterprise PMN service procurement and trials. These are high-viability technology providers. They are well-positioned with their current service portfolios and are likely to continue delivering leading services. Leaders do not necessarily offer the best solution for every customer requirement, nor do they necessarily address all geographies, and their products may not be “best-of-breed” in every area. Overall, Leaders provide solutions that offer relatively low risk and can achieve and sustain high-quality PMN service deployments.

Challengers

Challengers execute well today, have a strong PMN offering with reliable service delivery capabilities, and maintain a sizable installed base. Most of the PMN solutions deployments they participate in are through their indirect channels. Their offerings may be more specialized and focused on a specific domain, such as network infrastructure, and a few target industries. They tend to rely more heavily on channel partners and resellers. They also favor a single-vendor approach, based on their own first-party infrastructure offerings.