Predicts 2019: Increasing Reliance on Cloud Computing Transforms IT and Business Practices

Most technology innovation today is cloud-native or cloud-inspired. “Cloud computing” is morphing into just “computing,” and so application leaders must seek cloud-style quality of service across their hybrid information and technology environments.

Key Findings

- “Cloud computing” is shifting from an isolated delivery option to an all-encompassing computing strategy, including public and private cloud, on-premises enterprise systems, Internet of Things (IoT) edge and a variety of user experience outlets.

- Organizations are moving beyond, now common, “cloud-first” strategies. Even typically slower-changing government agencies are accelerating their cloud-only initiatives.

- Business innovation increasingly depends, in part or in whole, on the capabilities and performance delivered by public cloud’s advanced quality of service (QoS), including elastic scalability, agility, productivity and continuous global reach.

- Organizations are making strategic plans for consuming cloud services and are pursuing long-term relationships with cloud megavendors. They are looking for continuous access to cloud and hybrid innovation, and maximized efficiency, but, at the same time, wish to control vendor lock-in by adopting open standards and integration technologies.

Recommendations

Application leaders guiding their organizations’ cloud computing strategies should:

- Embrace cloud-native computing to stay abreast with information, technology and business innovation by investing in modern technologies and practices.

- Avoid exclusive commitments to any one provider; instead, embrace multiplatform operations and a hybrid integration strategy to retain greater flexibility of choice and innovation.

- Advance close relationships with business leaders to assist them in recognizing strategic cloud-centric business opportunities by creating IT-business liaison teams and practices.

- Promote organizational and cultural changes in support of cloud-native operations to ensure consistent transition outcomes by investing in continuous cross-organization education and process innovation.

Strategic Planning Assumptions

By 2021, over 75% of midsize and large organizations will have adopted a multicloud and/or hybrid IT strategy.

By 2022, public cloud services will be essential for 90% of business innovation.

By 2021, less than 10% of multicloud deployments will take advantage of the anticipated portability.

Analysis

What You Need to Know

Cloud quality of service (CQoS) is now viewed as state of the art for enterprise computing and replaces enterprise quality of service (EQoS), which dominated computing for decades. Cloud quality of service is where business organizations demand access to information and technology services with self-service features, agility, effortless scaling, resilience, productivity, efficiency and data integrity, paired with continuous innovation. Meanwhile, most organizations discover that adopting cloud using a simple lift-and-shift migration does not deliver any of the cloud benefits, but does incur costs and risks. In this context, computing is becoming a hybrid effort of cloud innovation, on-premises application modernization and strategic integration – all of which are increasingly cloud-based or cloud-inspired.

The ubiquitous presence of cloud-inspired, cloud-based and cloud-native design in most cloud, on-premises and on-edge technology initiatives amounts to morphing “cloud computing” into just “computing.”

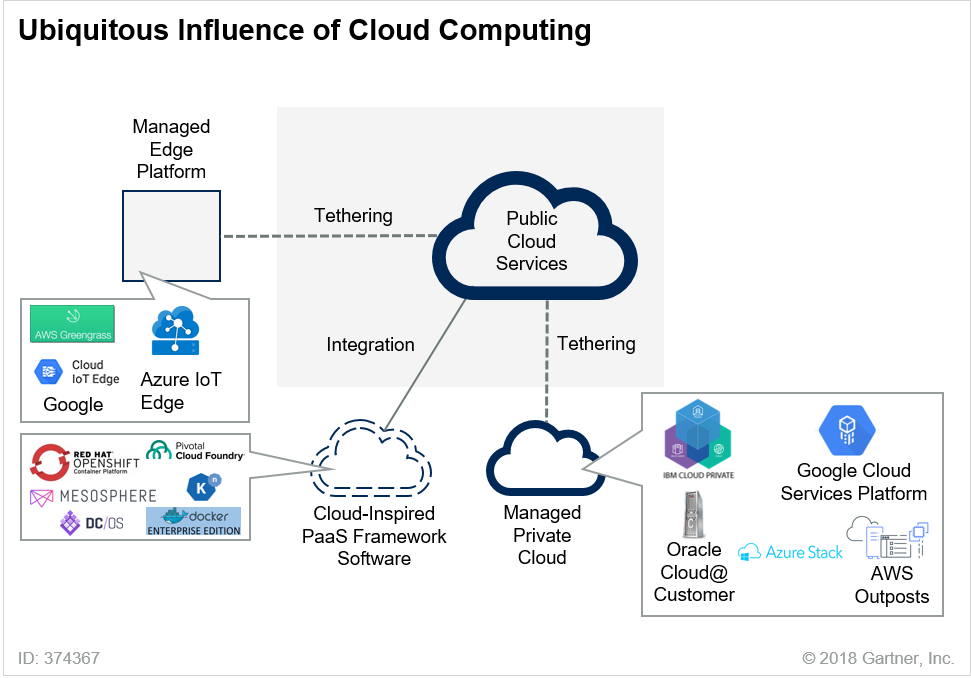

Figure 1. Ubiquitous Influence of Cloud Computing

Source: Gartner (December 2018)

Gartner’s 2018 CIO Survey indicates that IT leaders perceive improvement to core systems and adoption of cloud services as equally high priorities. Early hype centered on cloud fully replacing all on-premises computing, but this has given way to the reality of multicloud being combined with the some on-premises and other off-cloud computing (also referred to as “hybrid computing”). Most organizations have realized by now that not only will the current situation be hybrid, but so will their long-term information and technology environments:

- Cloud providers compete through innovation. Organizations that wish to lead through business innovation want to have access to new technology as it emerges from various cloud service providers. Thus, organizations plan to consume the services of multiple cloud providers.

- Customers discover that most cloud services are at least partially proprietary. The prospect of lock-in in the cloud has become one of the widespread concerns among customer organizations. Most are determined to adopt a multicloud strategy to minimize lock-in.

- Few midsize and large organizations plan to fully eliminate their on-premises systems in the foreseeable future. And while traditional on-premises computing is gradually declining, other off-cloud deployments, such as IoT edge, emerge. Thus, hybrid IT is recognized by most organizations as a long-term strategic prospect.

- Most organization are planning, or are already engaged in, a digital transformation. One of the fundamentals of digital business is the interdependence of organizations and ecosystems of partners and providers. Cooperation and coordination between independent business organizations within an ecosystem inevitably creates a heterogeneous multicloud, multiplatform computing environment.

Issues of reconciling the dependence on multiple cloud service providers and continuing reliance on the on-premises core applications, has created new challenges. They lead organizations to redesign their cloud adoption strategies, shifting the focus from specific capabilities in isolation to integration and coordination of multiplatform business operations. While the challenges of hybrid computing may seem complex, expensive and even dangerous early in the process, as the new integration-centric strategy begins to martialize, organizations discover the liberation that it provides for their technology and business decision making. Once ready for heterogeneity, the organization is ready to embrace a vastly broader sources of innovation and permit more of their systems to be redesigned for cloud-native and cloud-only deployment.

This year, Gartner’s SPAs highlight the increasing reliance of organizations on nearly ubiquitous cloud services, and the increasing maturity of cloud adoption in mainstream organizations.

Strategic Planning Assumptions

Strategic Planning Assumption: By 2021, over 75% of midsize and large organizations will have adopted a multicloud and/or hybrid IT strategy.

Analysis by: Sid Nag, Rene Buest

Key Findings:

- Cloud is the foundation for digital business, and hybrid cloud and multicloud models are increasingly being adopted by organizations. The market size for public cloud is growing exponentially and is projected to reach $360.3 billion by 2022 (Note 1).

- The number of cloud managed service providers (MSPs) addressing this space will likely triple to peak in 2020, then face massive consolidation by 2023. While many service providers are racing to enter this space, fast movers will commence acquisition sprees as the rush turns into more of a flow.

- Multicloud or hybrid cloud models require add-on capabilities around aggregation, integration, customization and governance to manage these disparate cloud assets and properties. This presents a follow-on opportunity for providers.

Market Implications:

Cloud computing has become the epitome of modern IT environments, and cloud-first strategies are the common approach for new IT investment. Gartner expects cloud adoption rates among organizations to jump from 68% in 2017 to 85% in 2019. Through 2020, cloud will be used for use cases that impact most organizations’ core business operations.

While cloud computing has become the new normal for modern IT environments, hybrid and multicloud are the reality when driving business transformation initiatives. Gartner research shows that, by 2020, about half of infrastructure as a service (IaaS) is expected to be deployed via public cloud and one-third will be deployed on-premises. Colocation, however, will be scarcely used.

Digital business requires organizations to leverage cloud solutions from more than one cloud provider. In doing so, they are able to take advantage of a variety of best-in-class services from every provider. Hybrid cloud and multicloud usage also lets them reutilize their systems of records and combine them with systems of innovation.

Leveraging hybrid cloud and multicloud environments, however, promotes complexity for the necessary cloud integration, as well as operation and management. That’s why we expect that, by 2021, 75% of enterprise customers seeking cloud-managed IaaS and PaaS solutions will require multicloud capabilities from a cloud MSP, up from 30% in 2018.

Recommendations:

To fully leverage multicloud and hybrid cloud models, application leaders must:

- Adopt multicloud and hybrid offerings with the desired digital business outcomes and broader IT initiatives in mind by leveraging metrics-based service offerings, such as operating productivity, cost savings and business efficiency.

- Take advantage of the agility, innovation, scalability and synchronization capabilities of services and solutions for hybrid and multicloud environments.

- Engage and contract with strong ecosystem partners that focus on industry verticals, specific geographies, adjacent markets and customer size. Leverage intellectual property (IP) and advanced techniques from service providers for relevance to, and focus on, your desired business results.

- Adopt cloud integration capabilities that bring together multiple cloud services and make them work together to deliver seamless distributed business process execution. These capabilities are typically delivered via an enterprise integration PaaS (eiPaaS) or cloud service brokerage functions, which include integration of cloud endpoints at scale, and community management and migration skills.

Strategic Planning Assumption: By 2022, public cloud services will be essential for 90% of business innovation.

Analysis by: Ed Anderson and Yefim Natis

Key Findings:

Modern business depends on technology for its competitive operations and customer experiences; and most technology innovation has firmly shifted to the cloud. Few, if any, organizations will be able to implement new business models or ecosystem relationships without relying on cloud services.

- Integration technologies are ubiquitous, and have developed to the levels of maturity that enable organizations to safely combine the slowly modernizing traditional business systems with the fast-changing systems of innovation. This reduces the risk of the innovative use of cloud services and its agile operational models.

- Organizations that have achieved cloud adoption maturity use cloud to create a dynamic, agile and innovative platform for their new operating processes. Innovations flow from public cloud services into the organization, spawning new ways of thinking about the role of technology in driving business outcomes.

- The ease of consumption and proportional pricing models of many cloud services make innovation technologies accessible to every organization. These democratized IT capabilities include AI, API marketplaces, event-driven continuous intelligence, next-generation user interfaces, real-time situation awareness, decision automation, digital twins and a large market of modern application systems (SaaS).

Market Implications:

- Innovation consumed from public cloud services democratizes IT innovation. It delivers new business outcomes that were previously out of reach for all but the most advanced IT organizations, to a broad spectrum of business users.

- Cloud-inspired business innovation is shifting organizations to new ways of thinking and operating. The new self-service access and productivity, delivered to lines of business by cloud services, forces IT organizations to redefine their mission and build a new relationship with business leaders.

- The requirement for cohesive business operations is challenged by the conflict between the entrenched dependence on traditional business systems and the emerging need to compete through cloud-based innovation. In this context, competence in hybrid multicloud integration becomes a strategic imperative for most organizations.

Recommendations:

Application leaders must plan for the use of public cloud services for future business innovations. To do so, they must:

- Establish cloud competencies for consuming public cloud services and operating in a cloud-like fashion dynamically, adaptively and innovatively.

- Use public cloud services for both tactical (short-term) and strategic (long-term) outcomes.

- Tie cloud initiatives to business outcomes, in addition to any technology outcomes you seek.

- Build strategic integration competency to facilitate business innovation across the new cloud investments, and the established enterprise processes and information systems.

- Manage the transformation of the IT organization in terms of how it adapts to the new modes of business operation and innovation, including self-service, agility and productivity of lines of business, and the fast-growing catalog of available SaaS solutions.

- To help enable rapid business innovation, begin consuming new technology capabilities delivered through public cloud services as they emerge, such as artificial intelligence, analytics, edge computing, event-driven design and IoT.

Strategic Planning Assumption: By 2021, less than 10% of multicloud deployments will take advantage of the anticipated portability.

Analysis by: David Smith and Yefim Natis

Key Findings:

- Multicloud can refer to many different scenarios. For vendors, it primarily refers to the availability of their offerings on multiple major cloud platforms and ecosystems. For users, it typically refers to the use of multiple major cloud data center networks (like AWS, Microsoft Azure or Salesforce, and their ecosystems) to meet all of the business’s cloud computing requirements.

- Customers’ cloud strategies often turn to multicloud to control costs and complexity, and to avoid excessive lock-in. To manage the lock-in, portability and dynamism are often prioritized in the decision framework for multicloud strategies.

- In practice, the ability to relocate applications (and their data) between the major cloud platforms (the dynamism enabled by portability) is rarely engaged because of business, technology and cost reasons:

- Migration, even if with maximum portability, is bound to affect and inconvenience business users, which IT leadership would rather avoid in straight migration cases, when business does not get new capabilities.

- Portability can never be complete, and technology changes during and after the crossing of the environments represent an unwanted unknown.

- The cost of migration is usually hard to justify, given that it is hard to estimate and also represents potential challenges and minimal benefit for business users.

- Cloud computing strategies today increasingly include multicloud as a primary objective. Although multicloud computing is seen as offering the potential to increase customer resilience and to lower the risk of cloud provider lock-in, most organizations will not solve the problem of lock-in through multicloud, nor will they achieve greater resiliency.

Market Implications:

As with many cloud-related concepts, there are many variations in multicloud’s real-world use and scope. While multicloud (much like cloud itself 10 years ago) is a hyped term that remains somewhat unclear to many, we have outlined three categories of multicloud computing competencies:

- Multicloud strategy. Most organizations will have a multicloud strategy focused on sourcing issues. This typically requires little to no technical or architectural decisions. It requires a strategy for vendor management, a framework for workload placement, and a strategy for developing and maintaining employees’ skills.

- Multicloud management. This refers to a coordinated approach toward managing and governing environments making use of multiple cloud providers. This includes enabling standardization of some policies, procedures and processes, and tools, especially tools that allow cost governance and optimization across multiple cloud providers. This includes, but goes beyond “single pane of glass” approaches to monitoring

- Multicloud architecture. The focus here is on architectures that enable applications to span multiple cloud providers. Indeed, some applications may be a composite of multiple different types of services and providers. Portability and migratability are usual goals. Some applications may also be deployed on different cloud providers’ platforms at different times and decided at runtime. For example, a batch-job application might be deployed to the least expensive cloud provider at a given time.

Most multicloud situations today are centered around the strategy or procurement approach. This is followed by multicloud management, and then multicloud architectures. Even within the focus on multicloud, we expect that multicloud architectures enabling true portability (not just ease of migration), and dynamism will account for, at most, 10% of multicloud situations through 2021.

Recommendations:

Application leaders should:

- Avoid hype-driven multicloud strategies.

- When establishing multicloud strategies, do it to achieve provable benefits to the organization and respond to the reality of public cloud adoption practices.

- Examine the multitude of multicloud business and technology scenarios – it is not just one thing.

Replay Prediction

The replay prediction is a prediction from a previously published report that is so significant that it is being republished here.

Strategic Planning Assumption: By 2020, more than 30% of government agencies with “cloud-first” strategies will adopt “public-cloud-only” strategies for all new initiatives.

Analysis by: Neville Cannon

Key Findings:

The first country to adopt a “cloud-first” policy was the U.S. back in 2011. Since then, many countries have followed suit, although it is fair to say that adoption and migration remained low for many years. The usual constraints of security and sovereignty played out for government IT departments. The focus of “cloud-first” policies during these early days was on revenue saving, with many white papers being produced extolling significant budget savings (75% to 85% was a commonly quoted figures). However the experience has been somewhat more limited and Gartner now reports cloud-based savings of around 16%.

In the intervening seven years since 2011, the hyperscalers have not stood still waiting for the bonanza. They have significantly developed their offerings, both in terms of the security and range of services offered, and the regions served by in-country data centers. This development has taken place as the understanding of cloud potential has matured. While savings are still paramount, governments and individual agencies are prioritizing different cloud capabilities and benefits to suit their requirements for flexibility and agility when it comes to policy introduction. Introducing more innovation is vital to many departments or ministries, and we now have examples at local, regional and national levels of agencies that are 100% operating in the cloud for just that purpose.

The U.K. government continues to recognize the wider value of cloud adoption in supporting agility. It encourages departments to break away from monolithic, complex contracts to consumption-based models that are flexible and agile. The U.K. now operates a “cloud-native” policy and Gartner has seen increased pressure being placed on governments in other countries, such as the U.S. and Australia. Data classified as “official” or “protected” is now routinely being placed in public cloud environments and, in the U.S., dedicated cloud facilities are able to host data that is classified as “secret” and “top secret.” Such facilities share their infrastructure with public sector and approved clients, such as defense contractors.

The drive to use a public-cloud-first strategy is not solely being driven by policy, however. With the advent of SaaS, Gartner has seen consistent growth in the adoption of shadow IT – mission departments, hungry for innovation, are increasingly embracing their own directly sourced solutions. Across government departments, it is not uncommon to see 30% to 36% of organizational technology expenditure taking place outside of the view of the central IT department. Continued adoption of SaaS solutions is expected to contribute to making this prediction accurate, as departments take control of their own transformational initiatives.

Government agencies believe that supporting an on-premises policy is likely to create a number of challenges going forward:

- Improved security will mainly be developed for cloud architectures and solutions, given that cloud is increasingly becoming the mainstream method for computing.

- Talent will gravitate toward more modern solutions and architectures to improve their employability and overall career prospects.

- Software providers will seek to migrate users onto consumption- or subscription-based models by effectively ceasing development for on-premises solutions.

The implication of these issues will effectively support and accelerate the adoption of public cloud across governments.

Market Implications:

CSPs are continuing to address the sovereignty issue by creating more IaaS regions, but the cost of implementing these local regions is too high for vendors to cover all countries where they have (or wish to have) customers. These limitations are already being identified, and price increases are being applied in smaller (in hyperscaler terms) regions. As SaaS continues to become the dominant model for government applications, vendors are likely to continue the migration of existing applications to subscription-based models. This will put pressure on those government CFOs who are reluctant to address the need to update their accounting practices to support the cloud-native subscription model.

As the move to public cloud continues, governments will increasingly seek further security assurances and tools to not only protect data sovereignty, but also privacy. Vendors operating in this space should expect the market to grow.

Justification:

Gartner has noticed a shift in client inquiries regarding cloud services for the government sector. The conversation has moved away from security- and strategy-based inquiries to a migration planning focus – essentially moving from a “should I” mindset to a “how do I” approach. Even those operating at the most secure end of the government sensitivity spectrum (defense, intelligence and health) are now asking how they can better take advantage of the capabilities and services offered by the public cloud.

Recommendations:

Government application leaders must:

- Continue to develop the relevant skills within their teams – leaving this too late will only exacerbate the pressures on recruitment and retention.

- If not already started, begin experimenting with public cloud to appreciate the operational practices that need to be considered and mastered.

- Gain visibility into how the government is already making use of SaaS applications. Utilize tools such as CMPs or services from cloud access security brokers (CASBs) to obtain an overview of the shadow IT activities currently being carried out in the organization in use in order to build a stronger case for a full cloud strategy.

A Look Back

In response to your requests, we are taking a look back at some key predictions from previous years. We have intentionally selected predictions from opposite ends of the scale – one where we were wholly or largely on target, as well as one we missed.

On Target: 2015 Prediction – Through 2017, the value delivered by Docker will be centered on a new ecosystem for container-oriented management, rather than vendor-hyped portability benefits.

We have seen vendor hype around portability – including hybrid cloud and multicloud portability – continue. That hype remains as feverish as ever, although it is increasingly focused on Kubernetes (container orchestration software) rather than Docker or containers in general. These technologies offer a more agile and consistent application development and deployment process. However, they do not significantly increase portability between on-premises and cloud environments, or between cloud environments, including different IaaS providers and PaaS frameworks.

As we anticipated, a large ecosystem has emerged around container-oriented management. That ecosystem is still evolving rapidly. The benefits of containers have primarily accrued to developers, especially those that use continuous integration/continuous delivery (CI/CD), DevOps automation tools, and immutable infrastructure. Infrastructure and operations (I&O) teams often struggle to adapt their processes to manage and secure containers, and to orchestrate containers at scale. Public cloud providers have responded to these operational challenges by offering container services, such as Amazon Elastic Container Service, Azure Kubernetes Service and Google Kubernetes Engine.

Missed: 2015 Prediction – By 2020, over 50% of all new applications developed on PaaS will be IoT-centric, disrupting conventional architecture practices.

The base expectation in this prediction was that adoption of IoT solutions would accelerate at a much faster rate than it in fact occurred. Part of the reason for the slower pace of growth is the complexity of multistaged IoT solutions, which deterred many organizations from developing custom IoT solutions. And, meanwhile, cloud service providers’ IoT platform offerings are maturing slower than expected, making it more difficult for organizations to rely on IoT platform service providers either.

Another important change of direction that affected the prediction has to do with the shifting focus of IoT innovation to IoT edge computing. A larger than expected share of IoT solutions and investment is implemented directly at the edge, leaving the cloud IoT platforms with a smaller role in the overall design of IoT solutions.

It is important to note the second part of the prediction, however (“…disrupting conventional architecture practices…”). In those scenarios where IoT PaaS is engaged in the design of IoT solutions, that approach does indeed alter many conventional architecture practices:

- The pipelined assembly of platform capabilities

- The cascading application of analytics with increasing scope of context

- The adoption of a digital twin architecture

- The reliance on event processing and event stream analytics

For most organizations, these practices and patterns represent new design and architectural models.

As IoT solutions overall, and IoT platform services in particular, reach greater maturity and organizations develop best practices for adopting IoT-required architectural principles, the essential finding of this prediction will be justified. IoT architecture and use cases will become a common experience of mainstream organizations.

Additional research by Lydia Leong

Note 1

Multicloud and Hybrid Cloud Defined

According to Gartner’s Hype Cycle for Cloud Computing, the definitions for multicloud and hybrid cloud are as follows:

- Multicloud computing refers to the use of cloud services from multiple public cloud providers for the same purpose. It is a special case of “hybrid cloud computing,” which is a broader term.

- Hybrid cloud refers to multiple cloud services from multiple providers. It does not specify the origin of those services, but in most cases a public source and a private source are involved. “Hybrid cloud,” as a broad term, is subject to more hype and confusion, and is more common.