Car manufacturers embrace new challenges with Digital Empowerment

Research from Gartner

2022 CIO and Technology Executive Agenda: An Automotive Perspective

Automotive companies clearly lag behind the leaders in composability practices. The 2022 Gartner CIO and Technology Executive Survey, focused on the concept of business composability, reveals several gaps automotive CIOs must address to increase the digital competitiveness of their organizations.

Overview

Key Findings

- Companies displaying high business composability deliver superior business performance, especially in times of volatility. Automotive companies trail top performers.

- The gap between high business composability companies and the average automotive organizations is wide in terms of the percentage of digital-enabled processes, both internally and externally. Few industries overall do well in the ratings compared to individual companies that are very composable.

- IT budgets are rising in automotive but much more slowly than for the cohort of highly composable businesses, with new automotive spending focusing on cybersecurity and cloud platforms.

Recommendations

CIOs advancing IT optimization and modernization in manufacturing and automotive must:

- Make your IT organization more capable of adapting to change by creating new targets around flexibility and agility. Then determine what technology investments would help the overall enterprise become more adaptable to change. It is important to determine just how composable you would like it to be or is practical.

- Invest in technologies that help to share information inside of the organization and outside. Create a hub of information that can be used by employees and consumers, and serve as the basis of new business capabilities.

- Get the most out of technology investments by arranging the appropriate data governance, processes and talent so that the main areas of investment can be successful.

Survey Objective

The 2022 Gartner CIO and Technology Executive Survey was conducted to inform CIOs and other technology executives on how composability can improve business performance during times of volatility.

Data Insights

Automotive companies are not highly composable businesses, which means they are not set up to adapt to fast-changing business environments. However, there are signs that the companies are making efforts to change.

For the past five years, automotive industry CIOs have reported in this Gartner CIO Survey (now Gartner CIO and Technology Executive Survey) a steady maturation of digital investments, but they have historically and continue to significantly lag the leaders as Gartner has identified them. Leadership in these surveys has been captured in different ways, whether by adoption of digital technologies or, for 2022, with composability. There are many rationales for this lack of forward progress. By nature, manufacturing is a business based on hard physical assets and optimization efforts to increase gross margins. This legacy is part of the reason why these companies struggle to keep pace with high-tech or finance companies, which can more easily make changes in their products with software. However, nearly every automotive company executive has expressed a desire to become more like the technology leaders. And to do that, they need to make their businesses more composable. For a look at how Gartner defines manufacturing and composability, see Innovation Insight for Composable Business for Manufacturers.

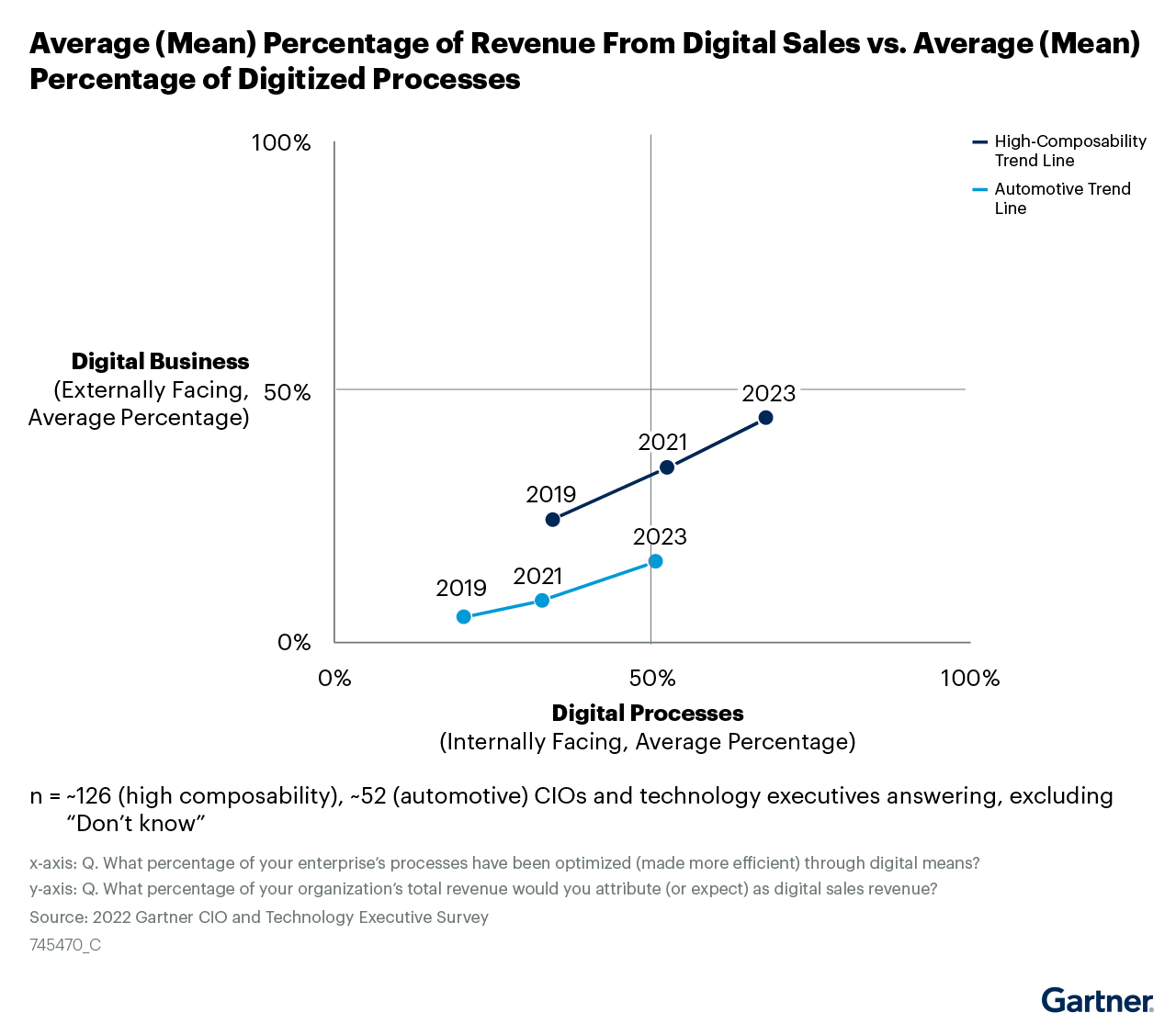

The Automotive Industry Makes Progress on Digital Initiatives

Auto companies are projecting a big jump in the number of digital processes and digital revenue in the next two years; however, they are well behind the companies that Gartner has identified as having high composability.

In automotive, digital processes are easier to tackle than digital sales, which is recognized on the y-axis in Figure 1.

Figure 1. Digital Progress: Automotive vs. High-Composability Enterprises

For a large number of suppliers that make parts for cars, digital revenue is challenging to generate. Some suppliers, such as ZF, are building data-based businesses, but the vast majority of business still is related to building a physical product that is integrated into a vehicle. Growing digital as a percentage of that business will be difficult. For automakers, however, the plan is to deliver much higher digital revenue through services, including:

- Downloading digital content and upgrades to vehicles

- Extending other services to vehicle owners

However, this pace of evolution is still slow in comparison to the most composable companies. On average, CIOs and technology executives in those companies expect online sales to be over 40% of their total revenue by 2023. Similarly, they expect the percentage of digitally enhanced internal processes to be above 65% by 2023, while their automotive peers only see those inching slightly above 50% by the same year.

Recommendation:

- Advance digital initiatives inside the company by creating new KPIs designed to advance those projects. These KPIs should be tied to overall business metrics, like operating profit, and have a logical connection to them.

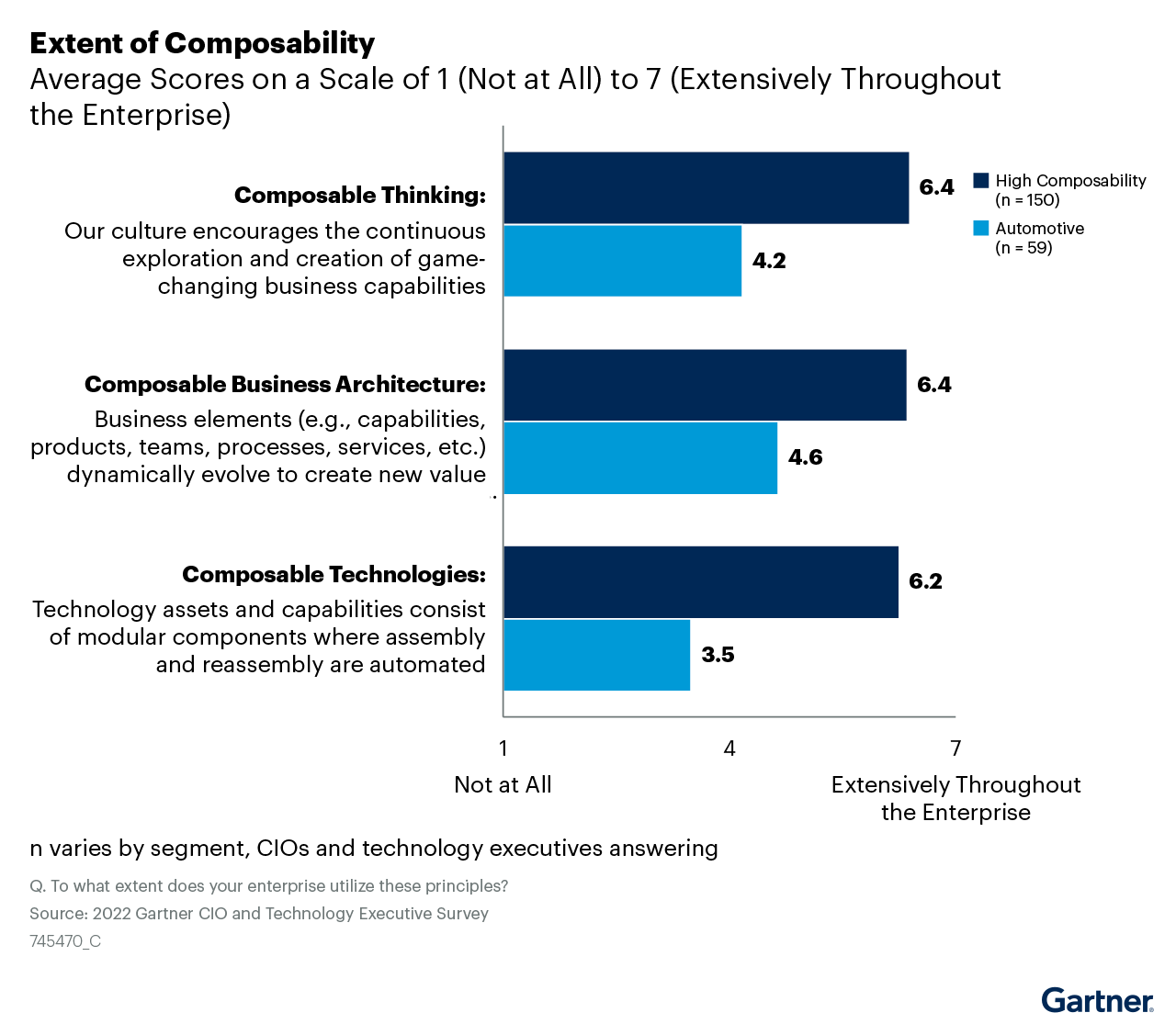

Business Composability Practices Lag Badly

Business composability practices consist of three different categories: composable thinking, composable business architecture and composable technologies.

The responses of the 2022 Gartner CIO and Technology Executive Survey reveal automotive CIOs and technology executives are less likely to use the key composable business principles compared to the highly composable companies (see Figure 2).

Just 5% of automotive respondents answered questions that indicated their company was “highly composable,” compared with 19% for high-tech and 11% for communications service providers.

Figure 2. Composable Business Practices

Auto companies fared poorly in composable technologies, where CIOs ranked their companies the lowest of the three categories. For automakers to make progress toward their goals of selling more aftermarket services, delivering content via software and through digital connections, CIOs must make improvements to composable technology.

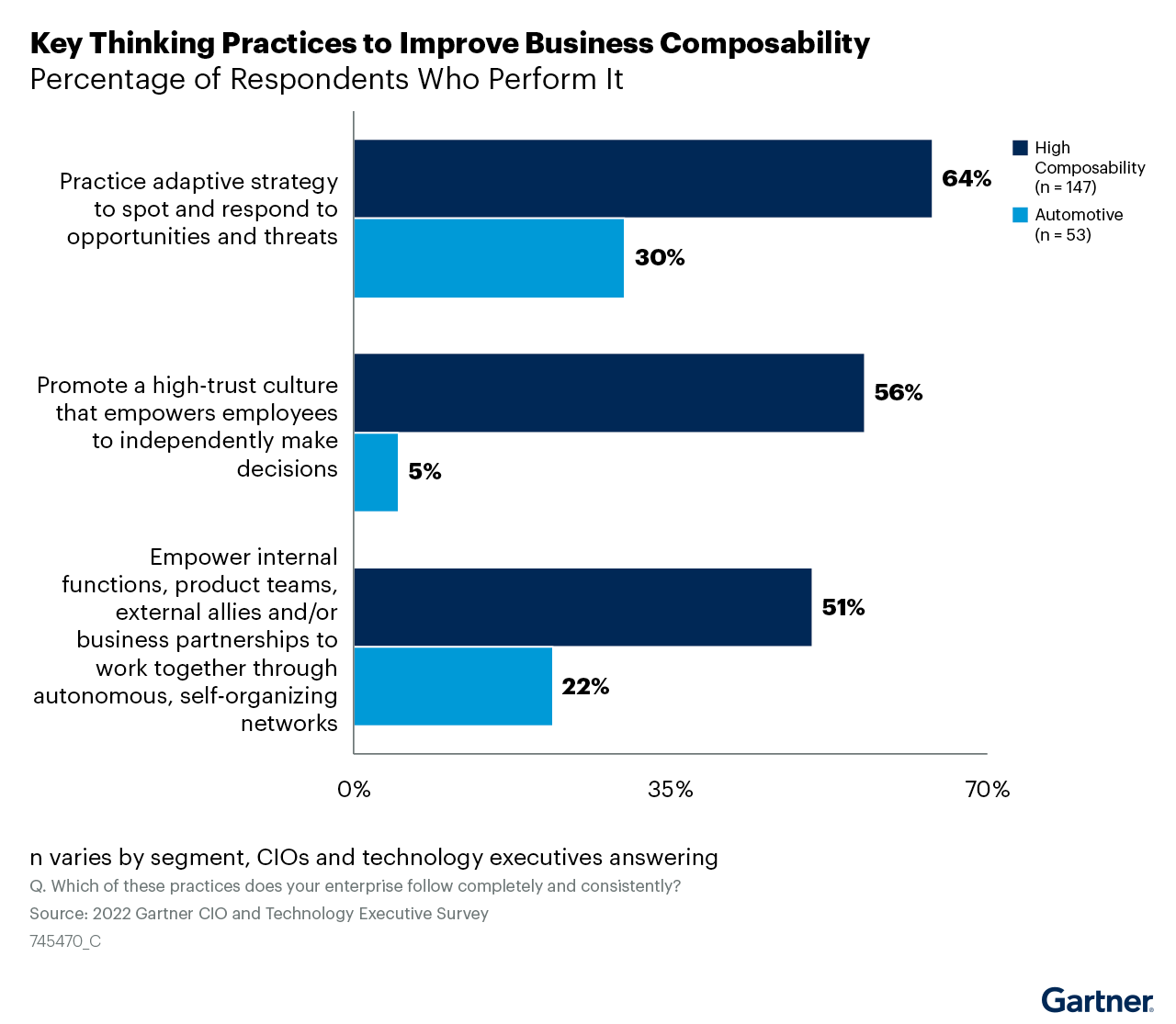

But perhaps the most striking result came from the lack of trust in employees to make decisions, which is a key practice to improve composable thinking (see Figure 3). For instance, 56% of respondents from highly composable companies claim their companies promote a high-trust culture that empowers employees to independently make decisions, but only 5% of their automotive peers are of the same opinion.

This lack of trust in employees to make their own decisions independently is likely the result of decades of reliance on a system engineering approach to everything. Each process in the organization is designed around strict efficiency improvement efforts to deliver lower costs and defects in the products. Even IT where there rarely is a physical product, there is more pressure on CIOs to deliver operational efficiency gains than enable new business.

Figure 3. Key Composable Business Thinking Practices

Automakers and suppliers lag the leaders when looking at the findings from survey questions that try to encapsulate composable principles. Auto businesses do best with the actual design of processes to be flexible and capable of creating value, but are fairly limited in the technologies that they are creating. This makes logical sense. Ultimately, manufacturers make a physical product, and it isn’t practical or even needed for the product and technology to be modular or flexible. However, as vehicles become more software-defined, the composability of technology in the auto industry will increase. This Hype Cycle details how the landscape is changing: Hype Cycle for Connected, Electric and Autonomous Vehicles, 2021.

Automotive organizations are subject to onerous safety legislation, which limits their flexibility in terms of composability. The high complexity of automotive manufacturing also hinders the ability of these companies to adopt composability in relation to other sectors.

However, respondents to our survey place sectors like oil and gas and asset-intensive manufacturing ahead of automotive in terms of composability. Companies in these industries also face similar constraints.

Recommendations:

- Look for ways to digitalize processes so that information can be easily shared across different parts of the business and externally, possibly through data marketplaces or exchanges such as Catena-X. Go beyond a master data management tool and instead create a hub through which the customer and employees can access and utilize information throughout the organization.

- Create a way for employees to experiment with new ideas without risking safety. Prove to employees that independent thinking and strong decision making is supported.

- Invest in platforms that communicate with vehicles and enable over-the-air software updates to drive potential new digital upgrades, understanding that the customer can now be engaged with the manufacturer for years after the purchase.

- Invest in improving online customer experience to encourage customers to buy vehicles online and to have an improved digital customer experience.

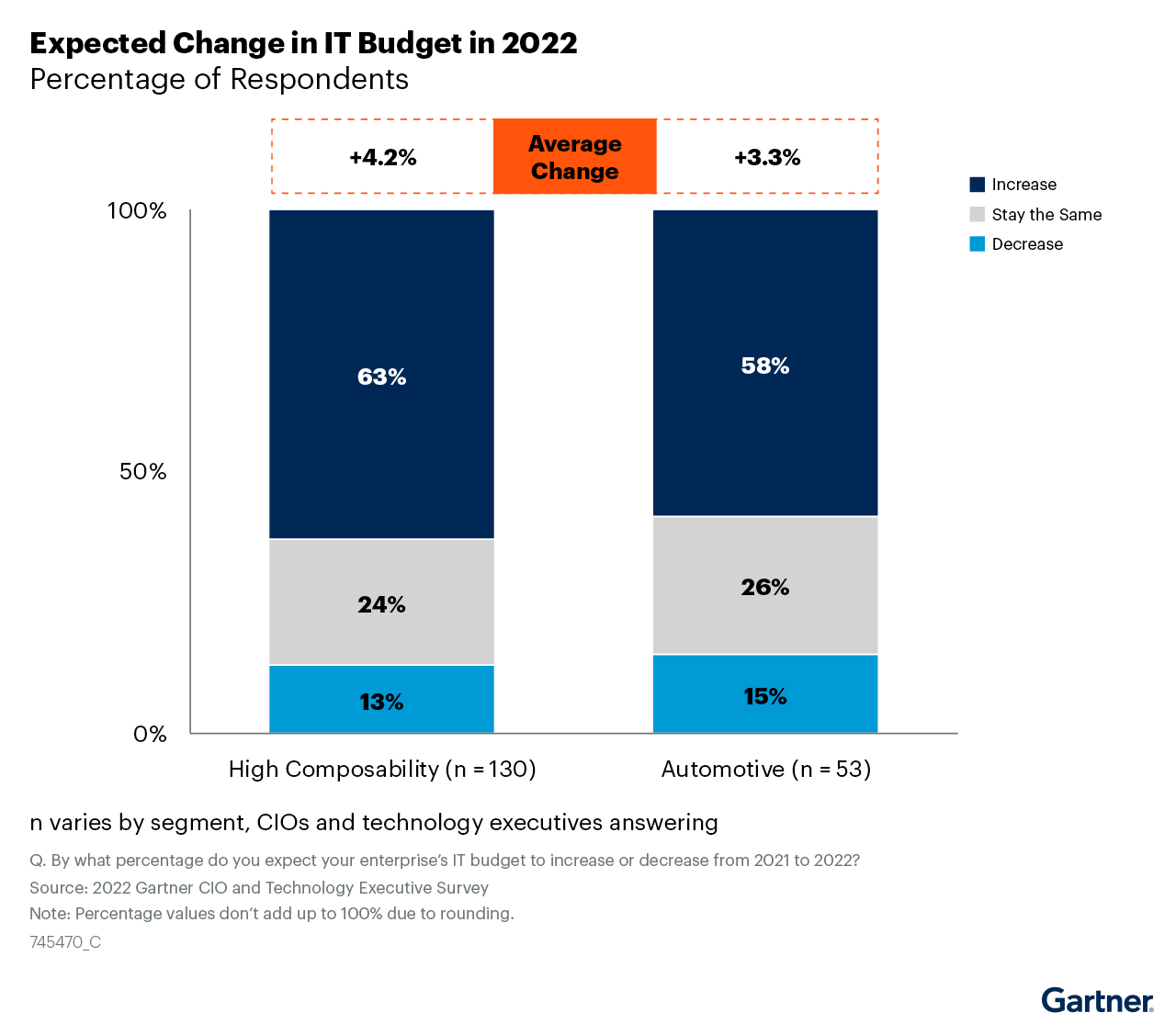

IT Budgets Rise More Slowly Than in High-Composability Companies

The survey of all companies shows that companies with high composability have higher increases in IT spending (see Figure 4). While this may not indicate that higher IT spending equals higher revenue, our survey results over time have shown that companies that have invested more in IT tend to have better business results.

Figure 4. IT Budgets Rise More Slowly Than Those in Highly Composable Companies

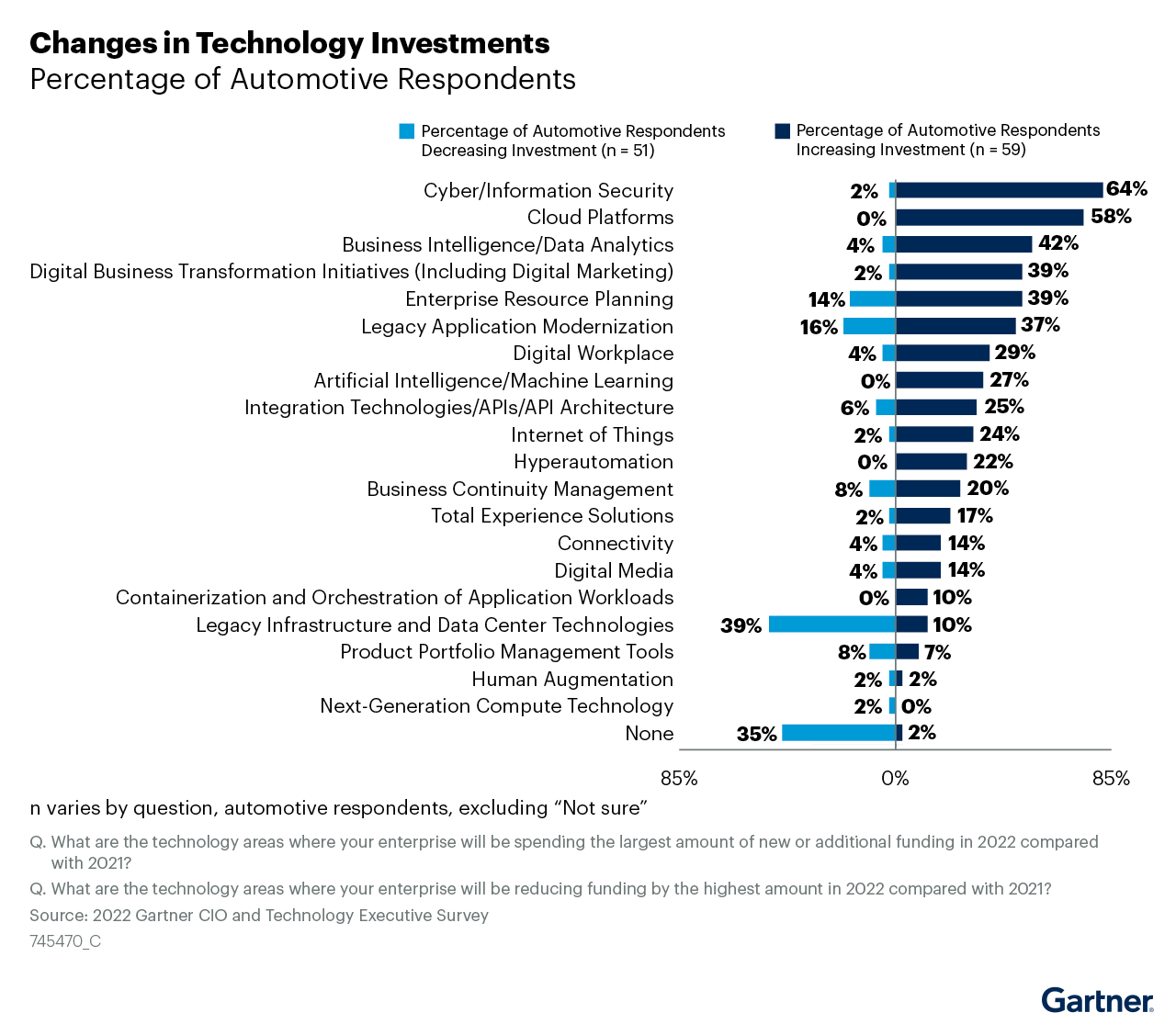

Cybersecurity and Cloud Platforms Lead Investments

Automotive CIOs who responded to the CIO and Technology Executive Survey are most likely to increase investments in cyber and information security as well as cloud platforms (see Figure 5). For several years, business information and data and analytics investments have been near the top of investments, and they remain so for 2022, but cloud platform investments surged in this year’s survey. Automakers like VW and Ford have both announced very significant deals with Amazon Web Services (AWS) and Google, respectively, to develop cloud initiatives. Digital transformation initiatives, including digital marketing also increased almost uniformly across the sample.

AI investments remain an important area for CIOs, and none in this sample reported a reduction of spending there. Three areas that saw the most respondents decreasing investments were around ERP, legacy application modernization, and legacy infrastructure and data center technology. Indeed, many of these lowering investments may be directly related to the surge of investments in cloud. Most cloud applications that manufacturers use replace on-premises applications, and there is a direct relationship between investment in cloud and reduction in spending on legacy applications.

Figure 5. Automotive CIO Investments

Recommendations:

- Get the most out of technology investments by arranging the appropriate governance, processes and talent so that the main areas of investment can be successful.

- Consider where top performers are investing and determine whether you need to rebalance investments in the correct areas.

Presentation Deck

Full results for automotive CIOs for the 2022 CIO and Technology Executive Agenda

Additional research contribution and review

Melissa Rossi Wood

Evidence

Research Methodology

The 2022 Gartner CIO and Technology Executive Survey was conducted online from 3 May 2021 through 19 July 2021 among Gartner Executive Programs members and other technology executives. The total sample is 2,387, with representation from all geographies and industry sectors (public and private), including 59 from the automotive industry. The survey was developed collaboratively by a team of Gartner analysts, and was reviewed, tested and administered by Gartner’s Research Data and Analytics team.

Disclaimer: Results do not represent global findings or the market as a whole but reflect sentiment of the respondents and companies surveyed.

The 2022 CIO and Technology Executive Agenda report segments respondents based on self-reported extent of utilization of principles of composability. This segmentation allows a group of “high composability” enterprises to be identified as a best practices group to contrast the performance of others.

We define high-composability enterprises (n = 150) as those that utilize the principles of composable thinking, business architecture and technologies “widely” or “extensively throughout the enterprise.”

Low-composability enterprises (n = 316) utilize the principles of composable thinking, business architecture and technologies “not at all,” “rarely” or “somewhat.”

Moderate-composability enterprises (n = 1,921) encompass the rest of the sample.

Source: Gartner Research Note G00745470, Mike Ramsey, Pedro Pacheco, 5 November 2021