Survey Analysis: Digitalizing Corporate Banking

The state of corporate banking IT in the digital business world is precarious. Survey data indicates CIOs are underestimating the importance of digital technology, lack adequate staff and resources, and are largely ignoring nonbank disrupters. This situation will be unsustainable in the long term.

Key Findings

- Banks have documented digital strategies and have started implementations, but execution risk is high due to a lack of defined digital leadership and vision.

- Improvements in operational efficiencies and reducing transaction costs are the key motivating factors for corporate banking digital technology adoption.

- A slight majority of bank executives and CIOs do not believe digital servicing models in corporate banking will dominate customer interactions in three years.

Recommendations

- CIOs and business leaders must raise digital corporate banking strategy creation from the lines of business (LOBs) and channels to the CIO level. Doing so will propel digital technologies beyond the automation of specific projects, processes and services to enterprise-level initiatives.

- CIOs should perform a coordination role, closely integrating IT road maps with the institution's digital vision. This will enable the IT organization to acquire skills for digital technologies through training and new hires that are directly related to the institution's broader business direction. They should also monitor digital disrupters and create strategy to build similar services, and partner with or acquire the disrupter.

Survey Objective

This survey assesses the current state of digital corporate banking. Gartner designed the survey to provide insights into the following questions:

- What is the current business and IT maturity and readiness of banks to address the evolution of digital business?

- Are banks using digital technologies to change the interaction paradigm with their customers?

Data Insights

Digital Transformation in Corporate Banking

The corporate banking environment has consistently lagged behind the technological evolution in retail banking. Historically, corporate banking has been heavily dependent on personal human interaction and noncommoditized, brand-related services and relationships. However, as business is increasingly being transformed by the development of digital capabilities, long-standing preconceptions about the corporate banking business are being questioned.

Technology – particularly software – is becoming a critical differentiator, not just in the context of transactional activities, such as electronic funds transfer or foreign exchange execution. Banks are now being associated with their technology innovations and the way they use those innovations to maintain brand presence and reinforce customer loyalty. Unlike in retail banking, CIOs cannot merely reorient their technology strategy to offer commoditized apps, mobile banking and mobile payment services. For corporate banking, technology, and especially digital technology, should be seen more as an augmenter of human interactions in the banking relationship, as opposed to a replacement.

One critical fallout from the global financial crisis has been the emphasis on working capital flows in terms of absolute levels of bank-provided liquidity, as well as the cost of borrowing and classifications of operational deposits. This means that the role of the corporate treasurer and the ability of a bank to better support that role have never been more important. This is especially true in relation to the access to, capture of and analysis of information, as well as the requirement to reduce friction in business processes – for example, in payments and the management of money.1

The consumerization of technology is working in three ways to impact the digitalization of corporate banking:

- In the context of bank employees needing more agility and insight to better manage their corporate relationships

- In the context of the corporate employees who now expect the same levels of functionality and service in a corporate context that they receive in their own personal lives

- In relation to corporate entities have been digitalizing their own processes and expect partners to provide products and services that align with their new digital systems, applications and infrastructures

Digital Challenges to the Status Quo

Consequently, CIOs have to look through three lenses when designing and deploying digital solutions for the corporate bank: how a corporate employee as a consumer will adopt and use the digital capability, how the use of technology by the corporate banker will change the nature of the customer relationship and as a "solution," where a number of products and services are bundled together, changing the way specific components are delivered, priced, serviced and so on.

Clearly, the opportunity for self-service by corporates, greater information transparency, nonintermediated transaction execution and availability of analytical tools will impact the corporate banking business model; for example, via the consumption of an integrated service, as opposed to independent data and product streams – in effect, the digitalization of the supply chain. As with retail banking, CIOs and business leaders will need to prepare for a detrimental shift in margins and revenue, and fundamental decisions will need to be made about where they focus core resources and, thence, technology enablement – that is, in terms of transactional activity or in terms of services. For example, Standard Treasury is starting to leverage digital technology to transform customer experience and relationships.

The decisions on business model will also have implications for IT architecture. Perhaps more than retail banking, corporate systems are heavily siloed and often extremely niche, attuned to particular functionalities/processes, where the processes themselves are very rigid and opaque. The evolution of more open architectures and apps will allow CIOs to offer corporate clients more flexibility in accessing bank services. However, this openness carries risk. It affords corporates a better opportunity to "shop around," because one of the building blocks is more standardization in terms of process.

While corporate bankers have relied on the frictional constraints of regulation and security, data protection, and so on as a means of "locking in" corporate relationships, some of those constraints are starting to loosen. Central bankers already meet regularly for advanced discussions on how to enable greater use in the industry of public cloud. And corporates, like consumers, will make trade-offs between getting the job done – more efficiently or for a better price – and assuming a slightly higher risk quotient.

Even if open architectures and nonproprietary Web APIs are problematic for some corporate bankers and their CIOs to adopt in relation to external customer interactions, those same architectural principles can be used internally to allow employees greater agility in addressing customer requirements.

Unlike the 20th century, when corporate bankers were the face of the brand, and banks poached teams to better create and deliver their offerings, the 21st century will see digital capabilities as the face of the brand. This will require a significant mindset shift by business leaders. Digital capabilities will be the key differentiator, requiring significant investment, resource realignment, training, product, process and service redesign. The question is, will deeply entrenched 20th century corporate banking business practices and cultures give way in favor of the newer 21st century models we have seen established in the consumer markets? Digital laggards will find out to their cost soon enough.

This survey reveals how CIOs and digital leaders measure their digital corporate banking business, the focus and state of their digital maturity, technology intent, customer adoption of digital technology, and views on competitors. This data sheds light on what bank executives must plan to improve if they want to become digital leaders or sustain a leadership position in the digital marketplace.

Finding No. 1: Banks have documented digital strategies and have started implementations, but execution risk is high due to lack of defined digital leadership and vision.

Several survey questions showed us that banks are actively engaged in digitalization, and 94% of firms have an IT strategy that is aligned and integrated with an attendant technology road map for implementing a digital business. Sixty-two percent of institutions reported that they have already started deploying a digital banking road map, but 53% of respondents have not appointed an executive to define and lead implementation. This suggests several significant road bumps are likely to appear during the digital transformation journey:

- Current strategies may include a large, unprioritized list of every project or idea that has even a passing resemblance to digital, creating a rather chaotic road map with limited sense on prioritization and the important linkage to performance/outcome, resourcing and so on.

- The strategy could, therefore, contain just a collection of IT-related projects without any real sense of how digital plays a role in the business and, importantly, how a particular project will transform the institution – with the risk that inadvisable investments could be committed. This problem is compounded by nearly half of respondents reacting to change by buying technology after significant process or operational requirements have already been acted on.

- Digital transformation requires a leader to ask some hard questions, such as what business(es) do we want to be in; how do digital capabilities add value to the business; who are our customers, and what is the digital value proposition; and what capabilities do we need to differentiate in a digital corporate banking environment? If a strategy has been able to address these questions, the lack of a leader who can execute decisions stemming from the answers will, at best, delay vision realization and, at worst, create potentially substantial performance lags.

Another aspect of the lack of defined leadership and the CEO's propensity to consider digital a "team sport" is that institutions are usually not short on ideas to address market conditions or opportunities. A 2014 survey by the Economist Intelligence Unit (EIU)2 revealed that 54% of corporate bankers admitted having a plethora of ideas for a change agenda; however, they simultaneously admit to lacking the capability to execute any of them successfully. The EIU believes the execution problem is 11% worse than in other industries, which does not bode well for a financial services industry already challenged by competition from companies outside their traditional domain.

Gartner's survey analysis indicates that digital corporate banking strategy not only lacks leadership, but also that leadership is confined to LOBs at worst and heads of "e-channels" at best. The bank's head of strategic planning is often not involved or responsible for digital banking strategy. Only 67% of respondents reported that digital banking strategy was the responsibility of the head of strategic planning versus 100% of the heads of e-channels reporting that they were responsible for digital banking strategy. Implications

Bank strategy officers who have roles inside the LOBs, as well as related CIOs/CTOs whose roles are positioned entirely within that LOB, may not understand the big picture value of digital banking strategy to the rest of the business. Consequently, it will be difficult for such banks to leverage digital banking capabilities to transform the commercial bank beyond discrete, project-specific initiatives. This may well appeal to LOB heads who are seeking localized digital project returns. However, corporate CIOs and CEOs should note that there is a trade-off at the group level due to the potential increase in costs created from the duplication of resources and lack of simple integrability of processes, data, applications and customer servicing.

Execution will already be hampered by regulatory and compliance pressures, as well as the concern that disruptive change will undermine customer value propositions, increase expenses and generate more/different types of risk. Something an industry segment already suffering from low margins, reduced lending capacity and business flow consolidation will find hard to bear.

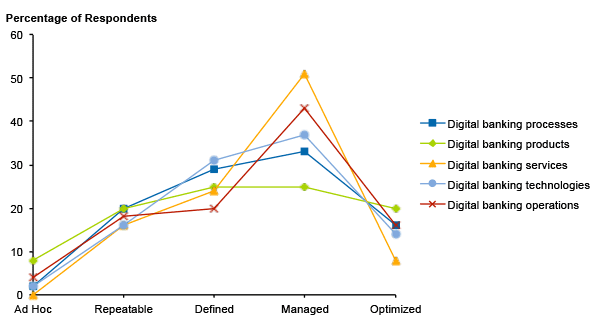

Lack of an execution capability can only be made worse from overconfidence within the bank. According to Gartner client enquiries and an analysis of comparable retail banking digital maturity, a major concern is that corporate bankers and CIOs overestimate the extent of their institution's digital maturity (see Figure 1). Gartner research usually indicates that a well-articulated and documented digital strategy correlates with a higher capability maturity. However, there is ample evidence from areas such as manual customer onboarding, reconciliation management, risk management and compliance to suggest a problem with causation. Moreover:

- Fifty-four percent of institutions have less than 45% of their corporate banking products digitally enabled.

- Fifty-eight percent of institutions have less than 45% of their corporate banking processes digitally enabled.

Figure 1. Digital Focus

n = 51

Source: Gartner (March 2015)

One reason for this dichotomy is that digital maturity is often mistaken for IT maturity, as evidenced by the amount of technology prevalent within the business. However, aspects relating to IT maturity haven't necessarily been converted into digital operating models – for example, in the context of new risk frameworks, changes in investment profiles and strategy, and changes in value metrics and performance criteria, as well as governance practices, resourcing, delivery and technology design.

As CEOs focus on the need for greater collaboration and ecosystem involvement, a lack of organizational integration (or at least cohesion) and sustainable executive sponsorship and leadership will significantly inhibit digital execution – at least in a competitively differentiated manner.

Consistent Gartner client interactions also highlight that operating models and governance structures remain unchanged or do not map to changing levels of digital maturity and business scope. This is not a "once and done" enablement. Technology and now business models are dynamically changing. CIOs and business leaders will need to regularly evaluate their digital capabilities to ensure a constantly mature status, as well as reinforcing those capabilities as strategic assets that can enhance ongoing profitability.

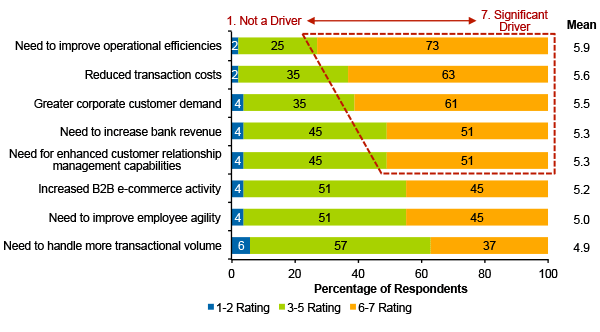

Finding No. 2: Improvements in operational efficiencies and reducing transaction costs are the key motivating factors for digital technology adoption.

Unlike Gartner's CEO survey, which showed senior executives switching their attention in 2014 to growing revenue, improving customer experience and so on, corporate banking executives and CIOs clearly believe that digital focus should be more concentrated on improving operational efficiency and reducing costs (see Figure 2). The findings in Figure 2 are similar to the recent Gartner digital surveys conducted during the fourth quarter of 2014 in Latin America, which also highlighted that the CIOs' digital intent is cost-to-income ratio improvement.

This is hardly surprising. Expectations of loan growth have existed for several years, but continued uncertainty about interest rates, a revival of the sovereign crisis in Europe, regulatory uncertainty and other geopolitical volatility are encouraging corporate banking executives to exercise caution.

From an IT standpoint, corroborating evidence can also be seen in the Gartner 2015 CIO survey, which revealed CIOs are spending more time than previously on running traditional core IT, rather than focusing on new, differentiated customer experience enhancements and digital transformation.

Figure 2. Digital Demand Focus

n = 51

Source: Gartner (March 2015)

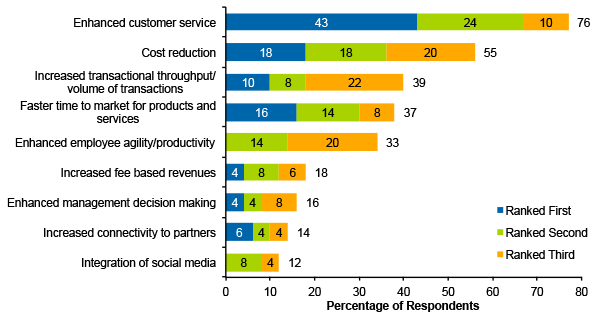

More detailed analysis of the data reveals another dichotomy. Although the need for cost reduction and improvements in operational efficiency are the top demand factors influencing digital evolution, 76% of respondents indicate that the biggest competitive advantage from digital technology use will be obtained via enhanced customer service (see Figure 3). However, enhanced customer service may mean additional costs are incurred to add and train staff to support digital services, and add digital technology to enable capabilities like secure video, new risk processes and digital payment authentication. Better customer service could also mean redesigning websites and portals for internal and external use.

Figure 3. Digital Competitive Advantage

n = 51

Source: Gartner (March 2015)

Secondary advantages from cost reductions and increases in transactional throughput, coupled with the perception that digital maturity is the same as IT maturity, suggest that respondents are seeking to leverage automation as a means of obtaining scale and potentially driving down variable costs. Customer service in this context is solely about increased commoditization of transactional activity, promotion of self-service (similar to consumer-based interactions) and automation, such as for hedging, liquidity management and high-value payments. This thinking implies that corporate banks are in Stage 1 of the three-stage digital model Gartner outlined in 2014.

For this to be successful, CIOs will need to substantially overhaul their legacy process and technology environments. Even more than in retail banking, the corporate bank is supported by an eclectic mix of complicated and largely unintegrated systems, architectures and processes – from customer onboarding to relationship management, hedging, cash management, payments and risk management. In many cases, these processes and systems span business functions beyond the corporate bank (for example, into investment banking), resulting in complicated remediation work to implement change.

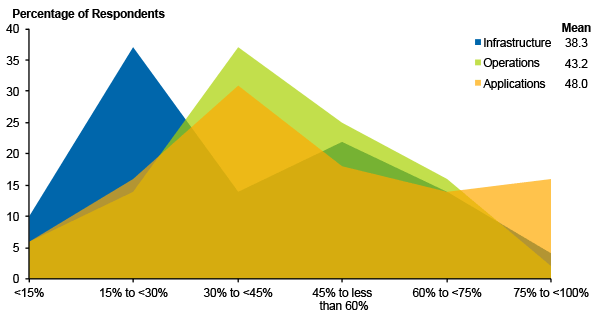

Therefore, Gartner believes that respondents are underestimating the extent to which such remediation is required (see Figure 4). On average, respondents believe they will need to re-engineer 38% of their infrastructures, 43% of their operational environments and 48% of their application portfolios.

Figure 4. Legacy Remediation

n = 50

Source: Gartner (March 2015)

Further, the ability to scale and differentiate will likely rely on new. That CIOs/CTOs see "low or no competitive value for increased connectivity to partners" means that scale and differentiation will be difficult to achieve.

This underestimation also leaves the bank vulnerable to disrupters that will place high value on the digital competitive advantages and focus on all the capabilities required to achieve them. Banks will then struggle to find resources, talent, services and partnerships to compete in time, much less differentiate.

Significant challenges exist in relation to any re-engineering efforts. In many cases (especially in the larger firms), bureaucratic decision-making processes elongate the time to market and business agility. Platform integration is problematic due to the heavily customized and proprietary nature of information, process and applications. Poor governance – especially in relation to change management – and the lack of alignment between IT and business departments continues to be emphasized in client enquiry.

Beyond many of these "run the bank" challenges, we asked respondents to rank the largest barrier within their institution inhibiting digital technology usage in corporate banking. The top three, in order of priority across all respondents, were:

- Lack of talented staff

- Lack of IT resources

- Executive opinion that corporate banking is a traditional business, not enhanced via the use of digital technologies

We also analyzed this data by respondent asset size (see Table 1).

Table 1. Barriers to Digital Technology Usage

| Asset Size ($B) | Largest Barrier |

| 5-99 | Lack of talented staff |

| 100-499 | Lack of talented staff |

| 500-999 | Lack of appropriate off-the-shelf technologies to purchase |

| ≥1,000 | Executive opinion that corporate banking is a traditional business, not enhanced via the use of digital technologies |

Source: Gartner (March 2015)

However, when analyzing responses by role, a slightly different picture is revealed:

- The majority of senior vice presidents in the business felt that the lack of IT talent was a moderate barrier. Twenty-five percent responded that the lack of talented staff was a significant barrier to using digital technology.

- Sixty percent of CIOs felt it was a moderate barrier, and 15% a significant barrier, whereas 67% of CTOs felt it was a moderate barrier. None of the CTOs felt it was a significant barrier.

A lack of talented staff has ramifications beyond mere technology use. It also impacts how resources are used within the institution. This is especially true from a legacy cultural standpoint. Business leaders give the impression that digital technology is "IT's problem." However, as customers became more digitally adept and demanding, IT's problem will quickly become the business unit's nightmare.

That said, more often than not, executives spend too much time trying to address internal operational friction points and not enough time with customers. Ironically, digital technology can help in this context with things like customer onboarding, information analysis, scheduling, performance management and measurement. The concern here is that, if the digital focus mentioned earlier is on automation, and (as with retail banking) there is a move to customer self-service, then corporate bankers may miss the larger relationship opportunity. Moreover, digital technologies are an essential way of uncovering greater customer context, which will be a critical enabler of enhancing customer service (see Figure 5).

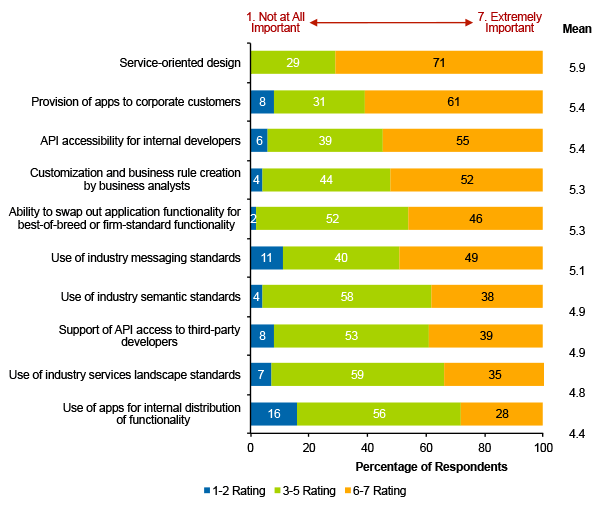

Figure 5. Technology Design and Selection Criteria

n = 50

Source: Gartner (March 2015)

Remediating legacy environments is only one aspect of digital transformation. Buying and building technologies that are fit for purpose in a digital world is also essential. Various criteria will influence CIOs' decision making in this regard (see Figure 5). Generally, respondents from institutions of any size indicated that SOA was an essential condition for digital business. However, for institutions over $1 trillion in assets, the use of messaging and data standards, such as Interactive Financial eXchange (IFX) and International Organization for Standardization (ISO) 20022, are considered essential. Midtier (in terms of size) institutions and all those from EMEA viewed such focus as the least important of any criteria. This will create interoperability problems for those firms going forward.

Respondents were asked about open banking – specifically how mature their institutions were in strategically developing and implementing open development banking platforms:

- Less than 6% of respondents consider their institutions mature, and virtually all were based in North America. Smaller firms are as likely to be developing and implementing as larger firms.

In terms of whether corporate banking IT used app stores to distribute internally developed smartphone and tablet applications, respondents were a little more mature:

- Fourteen percent have engaged in app development and implementation through app stores – the majority from EMEA. Again, smaller firms are more likely to be developing and implementing apps compared with larger firms.

App store usage for distributing externally developed smartphone and tablet applications shows greater maturity:

- Twenty percent of respondents consider their institutions mature, with the majority from EMEA and Asia/Pacific. Institutions with larger asset size were more likely to use such apps than smaller firms, likely due to the existence of more robust security, compliance and governance controls.

Clearly, corporate banking takeup of open banking and apps lags the retail banking environment. Some examples exist, but the entrenched traditional and manual process environment, lack of sufficient use cases and analog business practices are inhibiting adoption.

Finding No. 3: A slight majority of bank executives and CIOs do not believe digital servicing models will dominate customer interactions in three years.

The finding from this section of the research is disconcerting, because CIOs and corporate banking executives are challenged by the lack of holistic customer relationship analytical insight and transparency – relationships being tied up in individual relationship manager interactions. There is also the constant challenge in wrestling with manual processes, inexact performance measurement (for products, customers and employees) and requirements for substantial customization, such as for onboarding, pricing and reporting.

With continued pressure on margins and a low interest regime impacting credit businesses, reliance on traditional servicing models will not suffice, especially as corporate customers are becoming more demanding. The consumerization of technology over the last decade now affords corporate banking customers a chance to compare products, servicing and pricing, and embark on a more self-service interaction model. Market share among providers continues to consolidate across many asset classes and products. Speed and flexibility (of offering and servicing), as well as liquidity and price, are defining factors of an evolving digital corporate relationship.

In this context, we asked respondents to assess their customers' use of different technologies in relationship interactions with their banks (see Table 2):

Table 2. Corporate Customer Use of Technologies to Interact With Their Bank

| Mean Percent of Customers | Interaction Method/Technology |

| 56 | Online banking |

| 51 | Landline phone |

| 49 | Internet-based desktop portal |

| 40 | Smartphone |

| 39 | SMS/text |

| 31 | Tablet |

| 25 | Facsimile |

| 23 | Internet chat |

| 21 | Social media |

| 19 | Video |

Source: Gartner (March 2015)

The large spread of interaction paradigms suggests the need to evolve multichannel architectures that have been in use for some time in retail banking. CIOs and business leaders need to fix the gap between employee use of mobile technologies and the bank's institutional maturity in using those same technologies:

- Only 18% of institutions feel mature in using mobile technology directly for corporate/wholesale banking.

The opportunity here is that employees and the employees of corporate customers are also consumers, so they expect/want the same kind of mobile experience as in the retail banking environment – that is, view balances, approve transactions, create functions and check positions. In this context, CIOs need to focus mobile initiatives on:

- Mobile capabilities becoming an augmenter for traditional channels and servicing paradigms, such as via data presentation and analysis

- Encouraging greater standardization of mobility to promote adoption otherwise inhibited by variance in policies, security mandates, business requirements, internal capabilities (technologies and processes), data usage and access rights

- Increasing the culture of consumerization to promote cash management, risk and transactional visibility, together with approval controls

- Social and data-driven investments, such as for enabling industry-specific ecosystems and assessing specific industry initiatives, as a means of improving product and service alignment and for employees to share knowledge and best practices

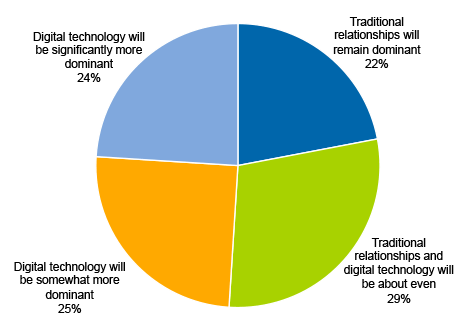

Unlike in retail banking, where mobile interactions are becoming de rigueur, there is a considerable uncertainty about how digital technologies will be used in customers' interactions over the next three years (see Figure 6).

Figure 6. Digital Technology's Role in Customer Interactions

n = 51

Source: Gartner (March 2015)

The data indicates that CIOs will continue to support a blend of traditional and digital technology interaction paradigms. There is concern that brand conveyance into nonhuman interactions will be challenging, and in noncommoditized offerings, this is a significant risk. CIOs must work with marketing executives and product/relationship managers to identify how to maintain brand presence in a more virtual context. This will require a change of mindset away from the relationship manager solely being the face of the brand to something that highlights how technological capabilities (such as analysis, information flow, networking and real time) are conveyed by less personal faces, such as logos, apps and websites.

CIOs also need to use digital technologies to simplify the lives of their corporate customers. Corporate customers can get answers to most things via a simple phone call to their relationship manager. Can those same answers be found with one click or one swipe? If not, adoption of digital technologies will be lower, and relationships will suffer. Simplifying interfaces and user experiences will also promote self-service, which could lower transaction costs. However, in a 2014 report from EY, 63% of corporates reported product and service innovation to be a critical part of their relationship with banks.3 However, those respondents also suggested that only 40% of banks have satisfactory performance levels.

Respondents to Gartner's survey seem sanguine about the impact of nonbank competition filling this innovation gap. Only 25% of all survey respondents believe that nonbank digital enterprises will be extremely disruptive to traditional financial services providers, and 12% of firms believe they will suffer zero disruption. However, the risks should not be underestimated. While it has been easier for consumer-oriented disruption to occur, every business is at risk:

- Financing: In 2014, Chilango launched the Burrito Bond. U.K. investors could purchase bonds issued by the fast food chain with bonds, with investments tied to a loyalty scheme and where payments were crowdsourced via CrowdCube, Zopa and LendingClub offer business loans. Kickstarter and Indiegogo platforms have raised funds for new services.

- Investing: Patagonia launched $20 Million and Change in 2013, a venture fund targeted at startups, with partnerships reflecting equity investments, majority ownership and joint ventures.

- Financing: MarketInvoice from the U.K. created an online exchange, allowing companies to selectively and confidentially sell outstanding invoices to fund working capital.

- Trading: Loyal3 created a platform for trading stock and investing in initial public offerings (IPOs). Companies can sell shares directly to their fans on Facebook and install a trading app directly onto their Facebook pages, which gives visitors the option to buy a stake in the business through a three-click process.

- Reconciliations: Duco created a hosted self-service trade-reconciliation platform that enables banks to quickly match trades using break management workflow. Duco also supports audit and change management. Customers include China Merchants Securities (U.K.), two North American-based global banks and a Japanese financial institution.

- Payments: Sage offers payment services integrated with small or midsize businesses' (SMBs') financial supply chains. Taulia also provides tools to digitalize business payments, invoicing and discount services. Customers include PayPal, Coca-Cola and Pitney Bowes.

The interest surrounding digital currency evolution was more pronounced. Respondents in North America and Asia/Pacific in particular believe that digital currencies are becoming a major enabler of corporate banking transactions, including e-commerce, payments, trade finance, capital markets activity and lending, within the next three years. Using a seven-point scale, with seven being extremely likely, respondents scored the result at 4.5. This is a little surprising, considering that the hype surrounding bitcoin has been predominantly consumer-centric. However, the transition to the programmable economy will open new windows of opportunity for corporate banks to access untapped revenue streams for hedging, insuring, trading and financing risk.

An important element of this shift to the programmable economy will be the evolution of the Internet of Things (IoT). Things (such as cars and refrigerators) already have connectivity and commercial capacity for ordering goods and services. Accessing stores of value, negotiating and trading are merely a matter of protocols and coding. It is unclear whether CIOs have significant insight into these trends based on client enquiries. (Future research will highlight financial services CIO thinking in this regard, later in the first half of 2015.) However, 33% of all respondents felt IoT would be extremely important in their organization's ability to service customers in the next three years, with 47% of North American IT leaders believing this to be the case – far more than the rest of the countries surveyed. There is also a modest positive correlation between the expected importance of the IoT on the ability to service customers in three years and the maturity of using mobile technology directly for corporate banking activities.

Conclusion

This Gartner survey of financial services organizations that provide commercial banking services shows results that are consistent with other survey data and client enquiry regarding the preparedness of commercial banking for digital technology and its ability to develop digital banking services for commercial banking customers.

Digital banking strategies tend to remain in the LOB control, with strategy heads outside of channels or LOBs out of the loop. This inability is compounded by the lack of internal IT talent and resources, which are key barriers to the banks' use of digital technologies.

Commercial bank IT leaders view the corporate banking world as more traditional and less vulnerable to the increasing presence and disruption of digital technologies with which their counterparts in other parts of the bank, especially retail banking, but also wealth management, contend. Executives do not perceive any threat from nonbank digital disrupters. This position leaves commercial banks vulnerable to disruption for both new and existing services.

Corporate bank executives underestimate the importance of digital technologies for their customers and for developing new services. They focus, instead, on traditional goals of improving operational efficiencies and reducing costs.

Methodology

From September to November 2014, Gartner surveyed 51 financial services organizations, using executive interviews in a research study to understand how corporate/wholesale banks use digital technologies to interact with their corporate, business and SMB customers, and the banks' level of maturity with respect to digital business evolution.

Definitions

A digital bank uses a broad range of technology-centric capabilities that enable new methods of interaction and service delivery to augment the customer experience and potentially transform the business. These capabilities are supported by a robust, dynamic and accessible digital infrastructure and open banking system that transform the analog environment. Critically, digital banking is the creation of new business designs by blurring the boundaries between the digital and physical worlds due to the convergence of three core elements: people who execute business activities, business activities and things – smart, Internet-enabled objects.

A total of 51 interviews were conducted:

- North America, n = 15

- EMEA, n = 19

- Asia/Pacific, n = 12

- Latin America, n = 5

Respondents were screened for direct responsibility or knowledge of the company's corporate banking strategies, or a functional piece within it, as well as knowledge or involvement in digital strategy.

Companies engaged in corporate (business or wholesale) banking, investment banking or institutional asset management were required to have at least $5 billion or more in FY13 total assets to qualify for the study.

The survey was developed collaboratively by a team of Gartner analysts who follow the banking and investment market, and was reviewed, tested and administered by Gartner's Research Data Analytics (RDA) team.

Evidence

For details about the survey methodology and its respondent base, see the Methodology section above.

1 S. Sposito, "Deutsche Bank Adds Financial Supply Chain Services to Autobahn App," American Banker, 5 August 2013.

2 "The Challenge of Speed: Driving Slow in the Fast Lane," The Economist, 25 February 2014.

3 "Successful Corporate Banking: Focus on Fundamentals," EY, 2013.