Virtualized Security – The end of Big Irons

Virtualized, scalable and carrier grade performance/functionalities, a true game changer for CSP's.

Research from Gartner

Market Insight: Key Strategic Implications for CSPs' CTO, CIO and CMO to Consider When Planning SDN and NFV

The telecom industry is facing a huge technology transition. Software-defined network/network function virtualization will be very disruptive for CSPs' network-centric operations. CSPs' C-level decision-makers must ensure strategic service-centric, bimodal operations to exploit new related revenues.

Key Findings

- Communications service providers' (CSPs') C-level and business unit leaders have to work toward an intertwined technology and business strategy. This requires CTO, CIO and chief marketing officer (CMO) to collaboratively execute upon a common software-defined network (SDN) and network function virtualization (NFV) corporate vision, by synchronizing operational processes, business models and corresponding skillsets across the organization.

- The role of the CIO will become more influential or may be merged with the CTO into a combined role – the chief technology and information officer (CTIO). The CMO will take a more technology-proficient role to define business requirements and build business cases to impel SDN and NFV technology investments.

- SDN/NFV will reach an inflection point once CSPs have transformed traditional network-centric to services-driven and software-orchestrated, multidomain operational infrastructures. CSPs will need to incubate, deliver and monetize revenue streams from SDN/NFV technology-enabled services and business models.

Recommendations

For CSPs' C-level decision makers:

- Make SDN/NFV a board-level priority involving all business unit (BU) leaders executing a shared technology and business strategy.

- Consider SDN and NFV as a major source of competitive differentiation allowing you to directly compete with over-the-top (OTT) players. Establish adequate operational capabilities to enable on-demand, usage-based business models and enhance customer experience and revenue streams. A first-mover CSP will be able to expand within the SDN and NFV arena quickly.

- Use a mix of short-term evolutionary benefits and long-term business and technology changes for your SDN/NFV evolutionary journey using the bimodal approach. An incremental SDN/NFV operational transformation in discrete areas will allow you to take a first-mover advantage.

Analysis

Introduction

We consider virtualized networks and software-driven networks as an approach that will incrementally evolve over the next 10 to 15 years for traditional CSPs. SDN and NFV will revolutionize these CSPs' operations, which will include the way they create, deploy and deliver services. To be competitive in the future, CSP systems' functionality will need more interoperability to work across products, services and lines of business to deliver improved customer experience, new business models and innovative offerings. Instead of delivering services in technology-centric vertical silo stacks, CSPs will shift their focus to operate horizontal, agile, fully automated, software-driven operations. This shift is necessary in order to be able to compete with other CSPs, like Amazon and Google, who already have a virtualized architecture.

CSPs deploy SDN and NFV congruently as they are the two key pillars of CSPs' evolution toward software-driven operations and virtualized network. Network function virtualization (NFV) allows classes of network node functions to be used as distinct pieces, which may be connected or chained, to create communication services. Software-defined networks (SDNs) are an architectural principle that provides decoupling of control and data plan to increase operational efficiency and to dynamically adapt to changing business needs. In simple terms, NFV brings the cloud to the network, while SDN brings the network to the cloud.

During the past 12 months, the discussion has focused on the network-technology-related aspects of SDN and NFV. Now focus is shifting from a technology-driven discussion toward a revenue-driven discussion. Early mover CSPs, like AT&T, Orange and Vodafone, are shifting their focus on the operational aspects to deliver service mashups and virtualized services, leveraging both technologies congruently to take an early mover advantage in the market. We anticipate that eventually, by 2030, services will become predominantly virtual. However, in the interim, we will see hybrid physical network and virtual data center environments. During this period, most CSPs will invest in virtualization of existing network technologies incrementally, and test SDN in discrete areas, such as virtualized enterprise customer premises equipment (CPE). The key legacy network systems will remain network-element-based rather than virtualized. Initially, SDN is being added as a separate architectural component before it is deployed on a wider scale – in order to test performance and scalability. As a result of this increasing complexity, CSPs will heavily invest in a new, horizontal orchestration layer that allows abstraction of complexity and simplification across heterogeneous SDN, NFV and legacy environments, in order to fulfill the promise of operating expenditure (opex)/capital expenditure (capex) reduction associated with this new technology.

In this context, the Gartner bimodal approach explains this transition of managing legacy stacks at a slow pace in the traditional mode, while gradually growing the footprint in parallel for new, more agile IT. SDN services like bandwidth on-demand are linearly deployed, with interop-based testing performed according to bimodal Mode 1. NFV services of DevOps-based applications are service-chained nonlinearly, which falls into bimodal Mode 2.

The new software abstraction/orchestration layer will be a critical capability of managing both virtual network functions and network elements, as well as bridging the gap to SDN in real time. The result will be at a higher level with more dynamic operational intelligence, such as closed-loop service fulfillment and assurance, self-healing and constant performance optimization. That means CSPs will ultimately run their networks according to IT services design principles.

As a result of this evolution, the role of the CIO will become more influential or could even be merged with the CTO to form a combined role – the chief technology and information officer (CTIO). Simultaneously, the CMO needs to become more technology-proficient to be able to transform those technology assets into new, revenue-generating products and services, helping define and advance the business case.

Operationalizing SDN and NFV Will Require a Paradigm Shift to IT-Centric Networking

CSPs invested in multiple heterogeneous network, operational and business support legacy stacks as new technologies were introduced. They created unique technological capabilities for each generation of fixed and wireless networks to fulfill evolving requirements regarding more flexible site and capacity management, service creation, fulfillment and assurance of new services. This evolution has led to the static systems' functionality and silo operations of CSPs' current network and operations support system (OSS)/business support system (BSS) environment. This functional separation is also mirrored in the organizational separation of network and IT.

With all this complexity and a plethora of legacy systems from 2G, 3G, Internet Protocol (IP) and Long Term Evolution (LTE) eras for example, CSPs recognize that the fifth-generation (5G) network technology needs to be simpler. CSPs endeavor to enable that transformation to 5G through the utilization of NFV and software-defined networking to take advantage of virtualization and software-driven design principles.

CSPs' prevailing network, operations and support system environments have remained static, requiring disparate, partly manual processes (for example, static provisioning rules for legacy technologies, separate configuration of network elements). In the current environment, they will not be able to handle this shift from the physical network to virtual network infrastructures, along with the necessary agile and streamlined processes that follow, which will severely hamper CSPs' efforts to launch virtualized services. This inflexibility has led to the realization that CSPs' investments in more automated operations intelligence will be crucial for CSPs to take a more proactive approach to network and customer requirements in the future. Primarily, CSPs will adopt SDN and NFV – leveraging benefits of cloud-centric, software-driven orchestration. This will help them exploit more intelligent, automated operational support processes to accelerate time to market, improve customer experience, along with enabling new virtualized services.

As a result, CSPs are looking to embrace new dynamic, unified, multidomain network, service and customer orchestration architecture with streamlined, horizontal core functionality and processes, which provide the "holy grail" between the two worlds – physical and virtual. This ultimately entails:

- A holistic view of the entire network

- Modeling of new types of services— hybrid physical/logical services

- Integrated analytics – automated real-time customer experience management (CXM)

- Aggregation and disaggregation of components and resources

- Automated optimization and remediation of resources based on end-to-end OSS

- Hyperscale architecture – scalable clustering technology

- Resource elasticity – dynamically scaling in and out/adding resources

- Service durability – automated service recovery and troubleshooting

Early mover CSPs will support this hybrid environment transition using a pace-layered, bimodal operations approach. In essence, CSPs run their legacy infrastructure in parallel to the new virtualized environments. Gradually, the horizontal orchestration architecture will encompass more operational functionality while legacy functionality will be phased out over time.

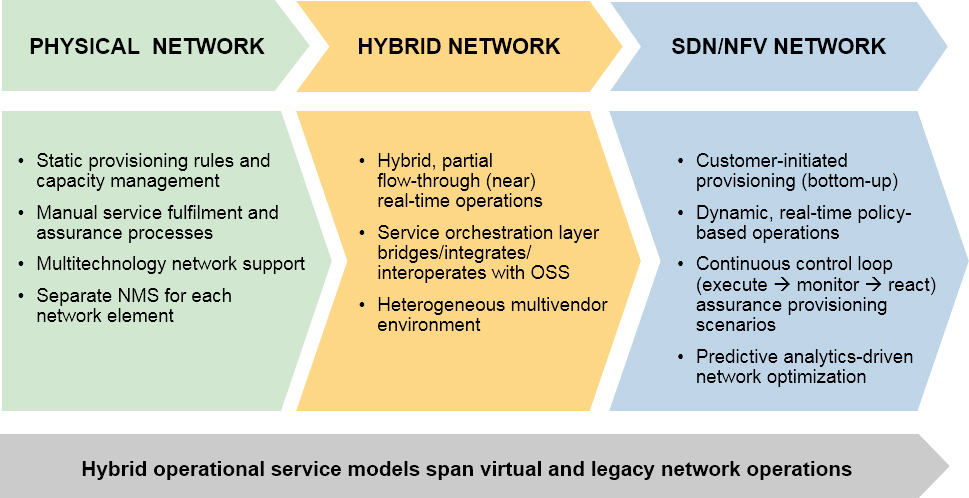

Figure 1 illustrates future hybrid operational models, visualizing the operational impact of physical, virtual and hybrid, as well as IT-driven network operations.

Figure 1. Evolution Toward Hybrid Networks and Impact on OSS

NFV = network function virtualization; NMS = network management system; OSS = operations support system; SDN = software-defined network

Source: Gartner (March 2016)

Anticipated Benefits of SDN/NFV

The new SDN/NFV approach will require a paradigm shift in the entire service creation, management and delivery value chain to exploit the anticipated benefits of the new technology.

- Significant improvements in operational efficiency (up to 60% through continuous closed loop self-healing, optimization of performance, mediation, scaling resources). This will ensure constant optimization of service fulfillment processes as well as assuring quality of the service as closed-loop operations. Features include self-healing, mediating between technologies and scaling up/down of capacity in direct response to business demands.

- Capability to embrace external innovation through digital partner ecosystems. Personalized services will be delivered in more self-service-oriented service-delivery environments. Customers can configure the service or modify network parameters of the existing service, accompanied by automatic service provisioning and delivery.

- Operational agility to bring new services to the market much faster. Centralized DevOps service design and delivery environments, with end-to-end service life cycle orchestration will be vital (specifically, to reduce time-to-market from months/weeks to days/hours).

- Operating expenditure (opex)/capex reductions will be achieved since the network will be run in the data center through general-purpose hardware (commodity servers) applying software and IT design principles. However, this transition to data-center-driven networking will not happen immediately. In the interim, CSPs will have to invest in operational infrastructures to facilitate hybrid physical and virtual resources as well as business models, which will increase opex/capex in the medium-term before cost savings eventually materialize.

- Customer experience SDN/NFV architectures have the potential to improve customer experience and drive new customer revenue streams, based on underlying principles of automated analytics, policy management, API exposure and highly dynamic service delivery. The new layered orchestration approach will change how data is collected, with different levels of information being derived from millions of virtual machines (VMs). Coupled with cloud analytics, this new way of data collection will help drive a positive customer experience and exploit the enormous promise of big data. It allows scaling to manage huge amounts of data from millions of VMs in real time to collect and model different service views, in order to enable new business models, drive new marketing initiatives (upsell, churn reduction) and venture into new markets (such as enterprise B2B storage, backup and security). Coupled with a unified data-driven data model, the new real-time orchestration architecture enables the rapid onboarding of new devices in the virtual world. Key characteristics are:

- Dynamically shaped behavior of network functions.

- Applications driving processes, not the network/technical planning taking place in isolation.

- Major impact on customer experience.

- Customers configuring the network themselves.

- Open APIs for partners to create application-defined networks.

- Dynamic service chaining (SDN- and NFV-enabled software-driven service chain provisioning, helping to accelerate timely and more cost-efficient service delivery).

Technology Investments Should be Closely Linked to Revenue

The arrival of software defined networks (SDNs) and network function virtualization (NFV) promises to reduce operational expenditure (opex)/capital expenditure (capex) through decoupling of software from hardware, as well as using highly automated cloud-centric, software-driven operations. CSPs will move from proprietary, dedicated network solutions with embedded network-element management to industrial-standard hardware, running in the data center. Capex reduction is achieved via elimination of stranded capacity and efficient use of resources; whereas opex reductions are made through an elevated level of operational intelligence and new orchestration infrastructures.

One early mover CSP anticipates opex reduction of 60% and capex reduction of 40%, providing virtualized Internet Protocol Multimedia Subsystem (IMS) for voice over LTE (VoLTE) services. However, this requires investments in new software orchestration with modernization of existing OSS/BSS, which only increases opex/capex. As a result of this increasing complexity, CSPs refrain from the opex and capex discussion and shift focus to the SDN/NFV technology-enabled business case with associated revenue potential.

CSPs' primary inhibitor for the enterprisewide adoption of SDN/NFV is of an organizational and strategic nature. Foremost, network architects are driving the adoption of SDN/NFV at large incumbent CSPs such as Deutsche Telekom (DT), Orange (formerly France Télécom), Telefónica and Telstra. However, implementations will only succeed if the organization's CTO closely collaborates with its CIO and CMO counterparts to move toward a more IT-like service factory design and service operations. Early movers like AT&T synchronize C-level decisions across all constituents of the enterprise to make sure the company is moving in one direction. Customer-facing lines of business, operations, security and governance departments all need to align toward one objective – shifting from network-centric toward service-driven operations and IT-factory design and service delivery.

SDN/NFV will allow CSPs to tap into the digital value chain, enabling them to create new service models in partnership with third-party vendors, as well as over-the-top (OTT) players and content providers. We will observe the evolution of hybrid service mashups, whereby CSPs will play the role of consumers as well as providers. Moreover, virtual functions will come from a variety of technology providers, including many offerings that will involve several functions working in tandem in a service-chain scenario. CSPs will only be able to monetize these new partnership ecosystems through adequate investments in open and agile, process-driven orchestration environments, which foster external collaboration and innovation. This encompasses streamlining every aspect of internal, customer and partnership processes. Moreover, real-time customer-facing service orchestration capability will be key to fully monetize SDN/NFV.

SDN/NFV Revenue Opportunities

Business stakeholders need to become adequately technology-proficient to define pragmatic business requirements in order to drive the evolution of service and technology requirements from a business perspective. BU leaders will also have to transform the way they sell new services to customers.

We perceive that early mover CSPs have successfully involved commercial constituents, such as the CMO, lines of business, to instigate the investment process by defining the business case that tie revenue opportunities to particular SDN/NFV investment decisions.

CSPs build the SDN/NFV business case by linking technology investments, such as service orchestration and self-service customer portals, to specific anticipated revenue streams (for example, on demand and virtual VPN connections for enterprise customers).

The low-hanging fruits – in terms of return on SDN/NFV investments – are investments that tap into existing OSS/BSS and network infrastructures, by adding an end-to-end orchestration overlay. This orchestration overlay will drive customer experience and reduce churn reduction through more advanced, real-time, closed-loop analytics and policy-driven operations. This new horizontal architecture will allow more automated cross-sell and upsell processes, based on better customer and market insights. It will also result in increased service delivery processes, which will accelerate time to market and drive new revenue streams.

Thus, the task of operationalizing SDN/NFV to protect existing investments and simultaneous proliferation of new revenue streams – derived from evolving hybrid physical and virtual business environments – will take center stage. Hybrid infrastructures will allow incubation of manifold composite services, many of which comprise external product components and content, for example, quality of service for OTT content.

A U.S. incumbent estimates the revenue potential of $1.5 billion from upsell of SDN-infrastructure and NFV-based services, such as firewall, cloud VPN, Internet Protocol virtual private network (IP VPN) on-demand services, as well as capabilities to scale resources up and down. Virtual CPE (vCPE) – for both enterprise and consumer customers – is low-hanging fruit for building the business case. This U.S. CSP anticipates up to 45% of cost-savings per site, per year, for reusable vCPE, as well as a potential ROI of 153% over three to three-and-a-half years – directly linked to OSS efficiency improvements (based on investments in service orchestration and self-service technologies).

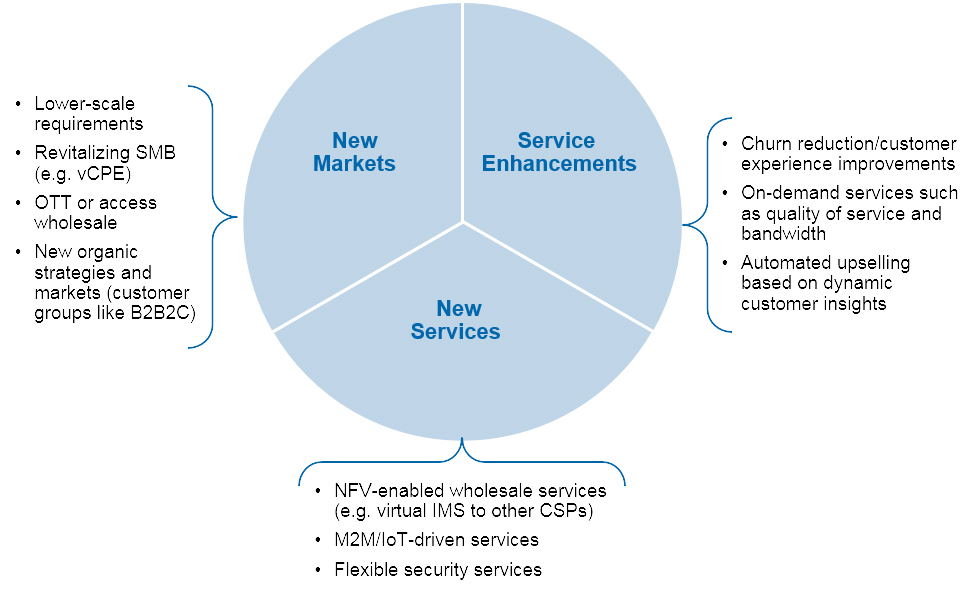

As an example, PCCW Global leverages infrastructure as a service (IaaS) to provide on-demand vCPE to enterprise customers via the cloud. CSPs discover that the utility-like usage model inherits a strong revenue potential, especially for connectivity-based services to be provided in a pay-as-you-go or pay-as-you-grow model. Figure 2 shows the available potential revenue of SDN/NFV.

Figure 2. Revenue Potential Related to SDN/NFV Architecture Investments

B2B2C = business-to-business-to-consumer; CSP = communications service provider; IMS = Internet Protocol Multimedia Subsystem; IoT = Internet of Things; M2M = machine-to-machine; NFV = network function virtualization; OSS = operations support system; OTT = over-the-top; SDN = software-defined network; SMB = small or midsize business; vCPE = virtual customer premises equipment

Source: Gartner (March 2016)

Service Enhancements

- On-Demand Services – The most immediate revenue opportunity is associated with enhancements of existing products or services, such as on-demand connectivity services, quality of service (QoS), capacity and bandwidth, which are delivered through self-service portals.

- Customer Experience Improvements – Initiatives to reduce churn using more advanced correlation, aggregation, analytics and policy capabilities. This is to help anticipate events that might otherwise have had a negative impact on customer experience; instead, it will trigger a resolution before the customer actually notices.

- Automated Upselling – Increasing operational intelligence will allow cross-selling and upselling opportunities, providing more tailored customer offerings based on better customer insights.

New Markets

- Virtualized CPE – Through virtualization of physical CPE offerings. The majority of early-mover CSPs engage in vCPE business cases due to the strong ROI potential. Today, Telefónica leverages vCPE to reduce costs and deliver services to its residential customers at half the time it would have taken previously.

- New Business Services – Business market opportunities through offerings like on-demand, VPN services across CSP groups (DT, Telefónica, Vodafone). Virtualized services for specific customer groups which can be deployed initially on a smaller scale and then leveraged to expand the footprint, for example, cross-selling of Web-security services in a business-to-business-to-business (B2B2B) model (for example DT).

- New Organic Strategy – This implies entering new markets and venturing into new vertical industries.

New Services

- NFV-Enabled Wholesale Services – For instance, offers virtual IMS to other CSPs providing SLAs and corresponding charging and monetization services.

- Machine-to-Machine (M2M)/Internet of Things (IoT)-Driven Services – This type of technology investment will depend on the business model as an enabler or IoT service provider. SDN/NFV will play an important role to provide the underlying infrastructure to prove a real-time or near-real-time view of the multifaceted IoT infrastructures spanning external partners. In particular, IoT requires investments in multidomain orchestration capabilities, embracing closed-loop fulfillment, assurance, policy and analytics.

- New IT-Centric Services – For example, flexible security services, firewall.

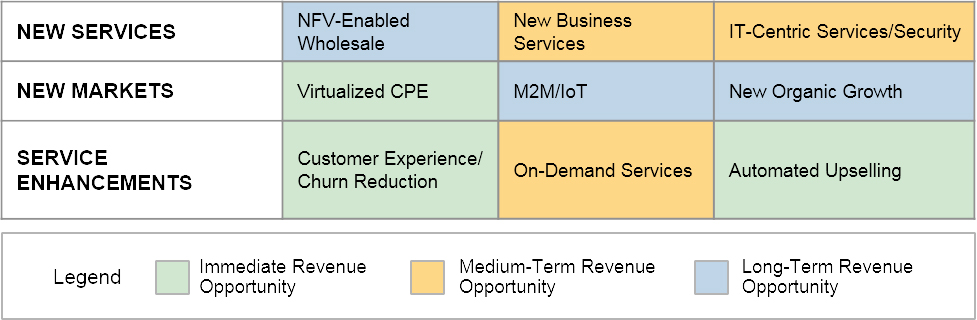

The heat map in Figure 3 represents the revenue potential related to SDN/NFV-enabled services. SDN/NFV revenue opportunities are categorized as new markets, new services or service enhancements. The legend below shows short term, medium term or long-term revenue opportunities depending on the scope and scale of technology investments required to operationalize SDN/NFV in the respective revenue areas.

Figure 3. Revenue Potential Immediacy: Heat Map for New Services, New Markets and Service Enhancements

CPE = customer premises equipment; IoT = Internet of Things; M2M = machine-to-machine; NFV = network function virtualization

Source: Gartner (March 2016)

Modeling the SDN/NFV Business Case

The questions of modeling a complex multifaceted business case – taking into account financial, operational, technical and business use case parameters to justify SDN/NFV related investments – become fundamental for CSPs. Currently, the cost side of the equation remains premature, especially in the beginning of the investment period. A solid prediction of cost reduction/savings is merely impossible or not practical due to increasing complexity related to modernization and redesign of operational OSS/BSS infrastructures in order to orchestrate SDN/NFV services across hybrid resource infrastructures. Running legacy infrastructure in tandem with the new architecture prevents CSPs from early cost savings (major cost savings will be anticipated toward the end of the investment period). Alternatively, if service providers do not virtualize or invest in software-driven infrastructures, they will not be able to change their operational model and drive service innovation, which will likely result in costs owed to a missed opportunity.

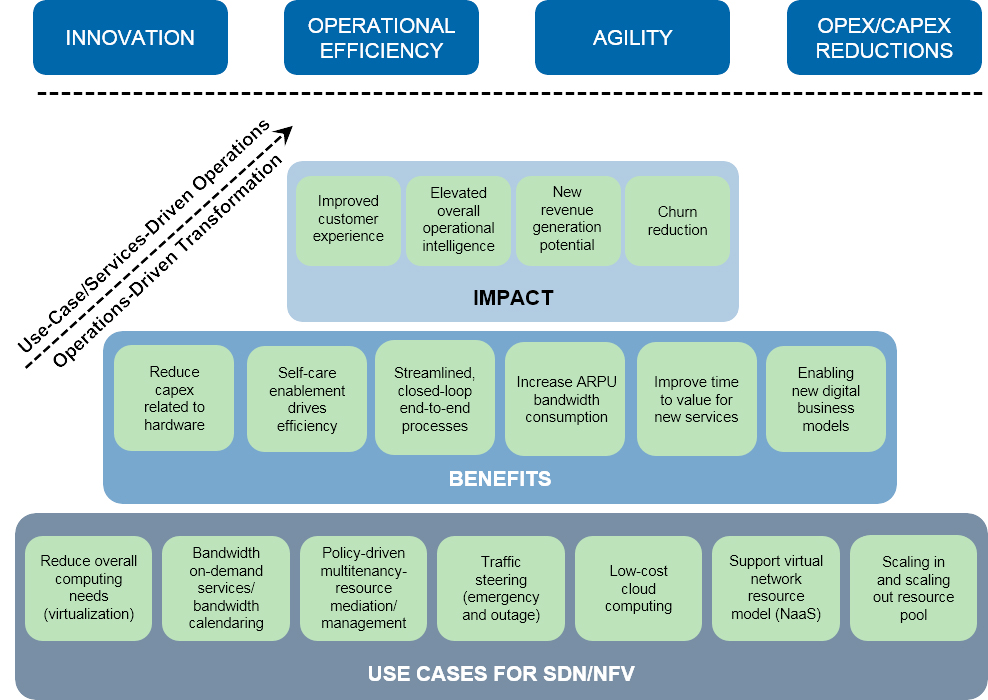

More advanced and early mover CSPs in the market, such as AT&T, Bell Canada and Vodafone, endeavor to grasp the overall benefits of SDN/NFV via the development of a multifaceted market model (see Figure 4). Such a model captures key building blocks for the SDN/NFV business case. The approach that early mover CSPs are taking is to build a holistic case for change by using financial models founded on a few strategic use cases. Typically, CSPs start by determining the most critical use cases for their company. This may include specific services (storage, security, vCPE) that CSPs provide to enterprise or consumer customers, venturing into new organic markets, operational use cases or service enhancements (on-demand connectivity services of bandwidth). Increasingly, operational use cases – closely tied to services-driven operations – are factored into the equation, such as:

- Policy-driven multitenancy, hybrid network resource remediation.

Benefit: Elevated operational automation and efficiency, significant time-to-market improvements (days versus weeks). - Closed-loop service quality optimization.

Benefit: Significant improvement in customer experience through analytics-driven automation. - Policy-driven autoscaling.

Benefit: Impact on opex and customer experience due to "just-in-time" capacity. - NFV virtualized network function (VNF) degradation-service optimization.

Benefit: Opex reduction due to automatic optimized service fulfillment and improved service assurance/customer experience.

Direct and indirect benefits are modeled taking into account capital cost and risk/transformation associated with those use cases. The outcome of such models may be displayed as a combination of financial metrics, operational parameters, and functional measures and capabilities.

Figure 4. Building the Business Case for SDN/NFV

ARPU = average revenue per unit; capex = capital expenditure; NaaS = network as a service; NFV = network function virtualization; opex = operating expenditure; SDN = software-defined network

Source: Gartner (March 2016)

Background and Context

CSPs can realize operating expenditure (opex) and capital expenditure (capex) reductions through the sharing of resources, which include common data centers, shared infrastructure, capacity management and hardware. However, CSPs can only realize opex and capex savings if they simultaneously simplify and reduce the complexity of the network and the support system layer. Moving away from traditional silo operations requires new software-driven architectures to support hybrid operational models for simultaneous support of traditional network, IT and virtual resources.

Large CSPs such as Telefónica, expect significant opex reductions – up from 40% to 60% over 10 years. Simultaneously, CSPs' transitioning from the legacy to the new SDN/NFV architectures will add to the complexity and increase opex drastically, especially at the beginning of the deployment period. The maintenance of legacy network and operational environments will also result in opex increases, especially during the first two to five years of the investment period.

This requires CSPs to carefully plan the modernization and/or phasing out of their legacy network and IT effectively. Similarly, the move away from network-centric toward service-driven operations requires a clear definition of business requirements and alignment regarding use cases and services.

The Impact

CSPs Will Streamline Efforts Over the Next Five Years to Tap Into SDN/NFV

As networks will be operated according to software principles, SDN and NFV technology implementations will only succeed if the CTOs in organizations closely collaborate with their CIO counterparts. This implies adoption of IT and software-based service design and delivery principles (such as cloud-based delivery of traditional physical network elements or service-chain principles for software-defined networks). The CMO needs to become adequately technology-proficient to define pragmatic business requirements (in close collaboration with sales and product development), and hence drive the evolution of service and technology requirements from a business perspective. This has implications on sales and marketing operations. In order to tap into new digital ecosystems, CSPs need to train existing sales channels and/or find new partner channels.

The current organizational silo operation and separation – in terms of mindset, operational development and commercial approaches – will be the biggest obstacle in the adoption of this new technology within the industry. CSPs are heavily expanding their teams of software professionals or acquiring software shops with network proficiency to shrink their development cycle. CSPs such as AT&T have more than 2,000 software engineers working on their domain 2.0 projects. Moreover, CSPs are looking to introduce DevOps-style development environments to expedite the service development and testing cycle, and accelerate time to market through unified development and operations processes. The idea is to provide automatic development and testing tools to allow constant staging of new product and deployment processes.

Some CSPs focus on merging internal resources and processes within development and architecture, in order to foster innovation and creativity of internal developers, for example, by providing open sandbox tools. DevOps processes are also vital for the congruent deployment and evolution of SDN and NFV services. SDN services like bandwidth-on-demand are linearly deployed, where interop-based testing occurs; and NFV services of DevOps-based applications are service chained nonlinearly.

Conclusion

- SDN/NFV will become a board-level priority involving all BU leaders executing a common defined strategy and shared goals.

- Technology investment decisions should be linked to revenue generation potential and the overall commercial and business strategy.

- Successful CSP SDN/NFV technology investments should be linked to revenue strategies, backed up by well-defined use case justifications.

- The transformation approach depends on the architectural vision for SDN and NFV, and the operational impact to drive new revenue streams, in line with business and commercial planning. Ultimately, the commercial and technology organization must be able to deliver on the vision collaboratively.

- CMO and commercial lines of business should be involved by initiating the process to build the business case, which links tangible revenue opportunities and specific technology investment decisions (closed-loop orchestration, self-service, performance and service quality management). Substantial ROI can be achieved within a period of six to 24 months.

- The journey from legacy network and IT infrastructures to virtual and software-defined network operations should start with the definition of a single unified target architecture (starting with layer K+1) embracing multidomain, multiservice management and resource orchestration infrastructures across physical and virtual resources.

- This will be best achieved through an operations and service-delivery, process-driven, end-to-end transformation approach. The operational aspects such as root-cause analysis, analytics, QoS and fault management for multidomain architectures will be crucial for the success of SDN/NFV.

- Consider the merging of architecture and development, or development and operations to boost efficiency of service-delivery innovation, fostered by more agile, bimodal internal development approaches. Apply lessons learnt from the enterprise market.

Source: Gartner Research Note G00293312, Martina Kurth, 17 March 2016

Acronym Key and Glossary Terms

2G - second generation3G - third generation

5G - fifth generation

API - application programming interface

ARPU - average revenue per unit

B2B - business-to-business

B2B2B - business-to-business-to-business

B2B2C - to-business-to-consumer

BSS - business support system

BU - business unit

capex - capital expenditure

CIO - chief information officer

CMO - chief marketing officer

CPE - customer premises equipment

CSP - communications service provider

CTIO - chief technology and information officer

CTO - chief technology officer

CXM - customer experience management

DT - Deutsche Telekom

IaaS - infrastructure as a service

IMS - Internet Protocol Multimedia Subsystem

IoT - Internet of Things

IP - Internet Protocol

IP VPN - Internet Protocol virtual private network

LTE - Long Term Evolution

M2M - machine-to-machine

NaaS - network as a service

NFV - network function virtualization

NMS - network management system

opex - operating expenditure

OSS - operations support system

OTT - over-the-top

QoS - quality of service

ROI - return on investment

SDN - software-defined network

SLA - service-level agreement

SMB - small or midsize business

vCPE - virtual customer premises equipment

VM - virtual machine

VNF - virtualized network function

VoLTE - voice over LTE