Five Key Essentials for the New Generation of Intelligent Video Cloud

Research from Gartner

Forecast Overview: Consumer Video Media Services, Worldwide, 2017 Update

Stand-alone internet-delivered linear television offerings will challenge traditional pay-TV services in the long term. Technology strategic planners at video service providers need to develop a service portfolio roadmap that includes internet-delivered services to increase and retain subscribers.

Overview

This annually updated document contains the forecast market model or methodology and explains the market dynamics and foundational assumptions that underpin our understanding and analysis of the market.

Key Findings

- Internet-delivered linear pay TV will initially target niche audiences. However, the market is growing fast with the potential to be a major threat to traditional pay-TV services in the long term.

- The S-VOD market will become more competitive in all regions as the international popularity of Netflix continues enticing more players to launch these services. By 2021, the household adoption rate of S-VOD is expected to reach up to 66% in mature regions and 17% in emerging regions, from as low as 17% and 2%, respectively, in 2016.

- Worldwide adoption of traditional pay-TV services will remain flat through 2021. While year-over-year adoption in emerging regions will grow by up to 11%, mature regions will experience negative growth as consumers switch to IDLTV/S-VOD alternatives.

Recommendations

Technology strategic planners at video service providers looking to exploit the personal technologies market dynamics should:

- Increase their subscriber base by developing and launching internet-delivered packages and content. Find a balance between price, content and features for new services and target market.

- Evaluate regional expansion by partnering with new S-VOD platforms and adding them onto their provider's platform.

- Develop a differentiated user experience by integrating their existing managed channels with internet-delivered content, enabling users to navigate between the two sources without leaving the platform.

Market Description

The video media service market is an aggregate market composed of multiple and diverse submarkets with the common characteristic of delivering video content entertainment services (films, TV programs and video) to a screen. These services can be delivered for free, for a fee, or supported by advertisements (or any combination of these three models).

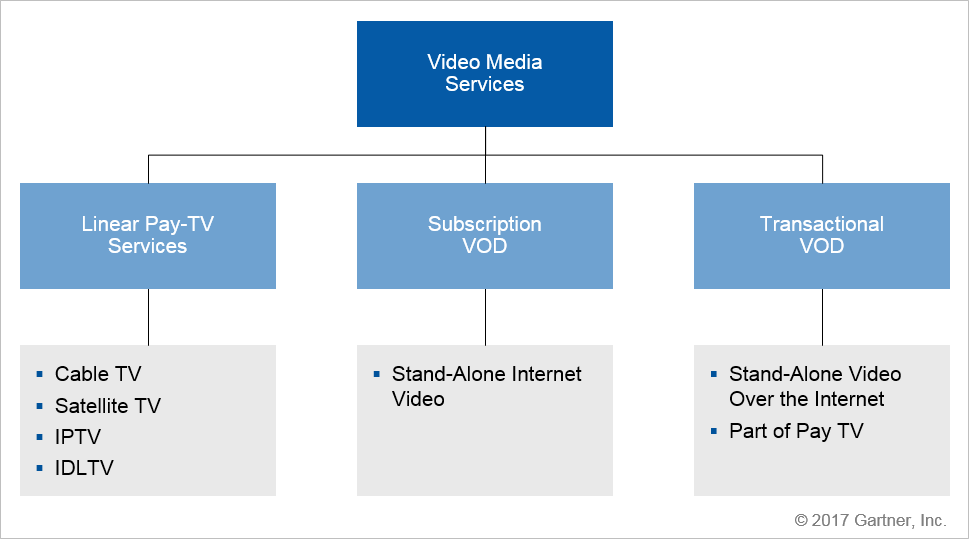

They can be delivered over a managed network or over a broadband connection as a best effort. We refer to traditional services as those delivered over a managed network. In the case of the latter, we refer to these services as internet video. Gartner's forecast of this market focuses only on those services for which consumers pay a fee to access this video content (directly to the service provider) on a subscription or a pay-per-view basis. (For more information, see Note 1.) Figure 1 shows Gartner's video media service forecast taxonomy.

Video Media Taxonomy

Figure 1. Gartner's Video Media Service Forecast Taxonomy Identifies Three Main Categories

IDLTV = internet-delivered linear TV; VOD = video on demand

Source: Gartner (August 2017)

Cable TV, satellite TV and managed IPTV services are grouped under pay-TV services, because they represent traditional TV services that require a dedicated closed infrastructure to deliver a managed service, mainly to a TV screen, with assured quality of service (QoS). We also included live TV streaming, also known as internet-delivered linear TV (IDLTV), in this category. These are internet-based services delivered at best effort. Many pay-TV providers offer both services in their portfolio – managed and best-effort delivery.

Subscription video on demand (S-VOD) services, as well as transactional video on demand (T-VOD) services, can be advertising-funded and free for the consumer, paid services, or a combination of both. Stand-alone, internet-based S-VOD services are characterized by being a best-effort offering. T-VOD can be delivered over the managed network of a pay-TV operator or internet-based and best effort. Gartner forecasts subscription and transactional VOD only where the consumer directly pays for the content accessed.

Market Characteristics

Pay-TV Market Expands to Internet Delivery

Traditional Pay-TV Market Is Mature in Most Geographies

Traditional pay-TV services have been around for decades with a well-developed market and consumer awareness of services offered in most geographies. Three main delivery technologies compete in this space: cable, satellite (direct broadcast satellite [DBS]) and IPTV. However, the technology over which pay-TV services are delivered is not usually an influencer in the decision-making process of the consumer, while features, convenience, pricing and content available are.

Markets in North America, most of Western Europe and Latin America, as well as Mature Asia/Pacific and Japan, are saturated or close to saturation. The launch of satellite and IPTV services and cable TV network upgrades and expansions are generating an ebullient market in Eastern European and Eurasian countries. The service concept of pay TV is well-understood, even in regions with no services, so that as services are rolled out, adoption can be quite strong, especially where free-to-air content does not meet expectations.

Internet-Delivered Linear TV Pulls "Cord Nevers" Into the Pay-TV Market

Generally, millennial heads of households are less likely to subscribe to traditional pay-TV services, in particular where these services do not get bundled with fixed broadband services. However, with the advent of IDLTV, these "cord-never" households are now joining the pay-TV marketplace with subscriptions to this new, generally more affordable service. These packages look and feel like a traditional pay-TV service, but are delivered over the internet instead of a managed network. Examples include DIRECTV Now, Sling TV and KPN Play, among others. Content can be accessed on a variety of connected TVs, mobile, computer and gaming console devices without specialty hardware or a managed network connection. IDLTV packages typically offer fewer channels than a traditional pay-TV service at a greatly reduced price, with basic packages being as low as $20 a month in the U.S. In addition to a greater perceived value, IDLTV services offer other features and benefits that are attractive to millennials and the early adopter segments, including app-based streaming across multiple devices and more customizable user interfaces and channel layouts.

Stand-Alone S-VOD Is Changing the Video Media Service Market Dynamics

Increases in broadband throughput and pure-play video streaming services, such as Netflix, Amazon's Prime Video and Hulu Plus, have created very favorable conditions not only for internet video, but also for all the video media streaming service market. Consumers can choose and pick what type of content they access, when they view it, and on what screen they view it. The emergence of S-VOD services has challenged the traditional pay-TV service providers' and content owners' business models so that they have to quickly adapt to consumers' changing behaviors and new competition that targets specific consumer preferences. However, S-VOD services are mainly being adopted as complementary to a pay-TV subscription.

Direct-to-Consumer Services Are a Viable Option Today

In addition to pure-play S-VOD services, channel networks have launched direct-to-consumer streaming services that are independent of a pay-TV subscription. Viacom, HBO and CBS, among others, have launched Nickelodeon, HBO Now and CBS All Access, respectively. The list of these type of services is on the increase. Premium channel networks with international distribution through pay-TV service providers are making their direct-to-consumer over-the-top (OTT) services globally available. Free-to-air broadcasters have adopted this approach as well, in most cases freely within their regions, where consumers can access the broadcaster's video on demand (VOD) and linear content online. Direct-to-consumer offerings, both free and paid-for, have the potential of a higher negative impact on traditional pay-TV subscription services, in particular among millennial demographics.

T-VOD Is Well-Established

The convenience of renting movies and video a click away using a remote control and streaming the movie almost instantaneously continues to win over consumers, particularly in developed markets. Rental video stores have disappeared with only Redbox kiosks remaining. Originally mail-in DVD rental services, such as Netflix in the U.S. and Amazon Video in Europe (formerly LOVEFiLM), have changed their business models to incorporate S-VOD and/or T-VOD services and are slowly winding down their physical rental businesses. At the same time, pay-TV service providers have bumped up their T-VOD services, with many of them offering such services over the top, as in the case of Sky, Orange and TalkTalk TV.

There Is a Ceiling to Pay-TV Spending

Household spending on pay-TV services has an upper limit that is defined not necessarily by disposable income, but by the opportunity to spend. In any given country, this ceiling for household spend is provided by the available premium channels and packages locally offered. Once the household has subscribed to all the premium packages, it cannot spend any more on traditional pay-TV services.

Video Media Service Availability Is Not Uniform Across Geographies

Adoption, whether of traditional and IDLTV pay-TV or the two main forms of VOD services, is constrained by availability of services, as well as cost. In some geographies, especially in markets such as sub-Saharan Africa and Emerging Asia/Pacific, pay-TV services are not well-developed, and there is little service availability. A good broadband service is a prerequisite for the satisfactory delivery of IDLTV and OTT S-VOD and T-VOD.

Foundational Assumptions

Gartner's primary source for projected number of households, as well as household income, is IHS Markit. We set our assumptions about household numbers and income at the beginning of each forecast cycle, once a year, based on the latest available IHS Markit forecasts.

Demographics

Total Households and Household Income

The total number of households worldwide will grow by approximately 1.7% per year on average through 2021.

We regard video media services as services that households rather than individuals subscribe to, so an increase in households increases the addressable market. IHS Markit data shows household growth of 9% on average between 2016 and 2021 across developed regions (North America, Western Europe, Japan and Mature Asia/Pacific). Growth in emerging regions (Emerging Asia/Pacific, Eastern Europe, Eurasia, Greater China, Latin America, the Middle East and North Africa, and sub-Saharan Africa) is greater, with an average annual growth of 1.9%. Given low rates of household formation in emerging markets, population growth does not translate directly into household growth.

Gartner segments households in four income bands. As households move up into higher income bands within any given year and over time, they will have more disposable income available to subscribe and consume video media services through the forecast.

Household Segments

.Household segments, defined by their attitude toward technology, will have similar behavior independently of geography across the forecast period.

Based on Gartner's household segmentation analysis, households are grouped in four segments, determined by their self-reported attitude toward technology consumption:

- Early adopters

- Early mainstreams

- Late mainstreams

- Stragglers

Each of these attitudinal segments was further segmented into four income band groups to better understand and project household segment behavior based on their income capabilities. Each of these subsegments will consume and adopt video media services at different stages throughout the forecast period, based on its attitude toward consumption of technology combined with their ability to pay for video media services. For example:

- In North America, a saturated market, traditional pay-TV subscription growth is expected to start declining by 2017 as new modes of consumption (IDLTV) take off among early adopters and early mainstreams.

- In sub-Saharan Africa, a region with low availability of pay-TV services, we expect early adopters to acquire pay-TV services as they become available in the region, more so than other modes of consumption, which will not be that readily available in the region.

Macroeconomics

Global GDP per capita will grow by an average of 3% per year through 2021. This will lead to increasing affordability for consumers in various domains, including video media services.

Whether at a household or individual level, increasing GDP per capita links to higher disposable income. This helps to increase people's propensity to spend on video media services. Depending on a particular country's maturity, higher income together with faster technology availability and increased availability of content and services will contribute to rise in spending on all types of video media services, especially in emerging markets.

At any given household income level, the share of the consumer wallet destined to video services will remain stable through 2021.

- Monthly spend on pay-TV services in developed markets will represent approximately 2% of household income through 2021.

- Small temporary fluctuations in disposable income have no impact on spending on pay TV.

Gartner's research shows the percentage of the consumer technology and service wallet allocated to services and media will remain constant during the next five years at around 14%. Based on this research, we assume the amount of money that households will spend on video media services will also remain relatively constant over time. Events that could temporarily cause small fluctuations in disposable income will not significantly impact pay-TV and other media service spending. The time-contractual characteristics of these services versus the temporary nature of the income fluctuation will discourage consumers from engaging in higher spending, but not decrease it.

Pay-TV service monthly spend will represent roughly 2% of household income, at any given income level, in developed economies. This percentage will be slightly more in less-developed economies.

Regions with well-developed video media service spending on additional features or additional T-VOD purchases will drive a small average monthly spend growth of about 2.35% per year through 2021.

Increased availability of video media services in emerging regions will trigger an average monthly spend growth of up to 10% through 2021.

In developed regions where video media services are already available, the limited increases in average monthly spend will be driven by additional features or additional T-VOD purchases. Total spending on T-VOD services will grow on average by 13.3% year over year during the forecast period, compared with pay-TV services that will grow by just 0.6%. In emerging markets, average spending on these types of services will be triggered by increasing availability of video media services and premium services, as well as an expected household shift to higher income bands. Consequently, total spending on pay TV will experience an average annual growth of 8.2% in emerging regions for the forecast period, while total spending on S-VOD will increase by 22.5% and T-VOD by 10.5%.

Demand-Side Factors

Consumer Purchase Preferences and Usage Behavior

Households' Willingness to Pay

As the total budget for video media services remains stable through 2021, traditional pay-TV subscribers in mature markets, on average, will reduce spending on pay-TV services by as much as 37%, diverting part of their budgets to S-VOD and lower-priced services.

As content available on S-VOD and T-VOD services becomes richer, services themselves become more available, and broadband connections become even faster and more reliable, households subscribing to traditional pay-TV services will discontinue certain premium add-on services to their subscription packages and redirect this spending to S-VOD services delivered over the internet. For all effects, S-VOD is a complementary service to pay-TV services, providing accessibility for the additional type of content consumers want.

Spending diverted to complementary services such as S-VOD offerings will vary by region and household, depending on whether the household discontinues the totality of the premium traditional pay-TV services or just part of it. North America is where this potential is maximized, where households can divert as much as 37% of their spending in traditional pay-TV services to other forms of video subscriptions.

This behavior already became noticeable in the early adopters' segment in 2014 in developed economies with a mature pay-TV market and the availability of satisfactory S-VOD offerings. Early mainstreams lagged with this behavior by two years, while late mainstream households are now emulating this behavior.

Stragglers' households will continue subscribing to full pay-TV packages and premium add-ons as their household budgets permit them.

Because of cost, the availability of online stand-alone premium channel offerings will have little or no impact on adoption rates of traditional pay-TV service beyond the millennial demographic segment.

The advent of online a-la-carte channels from broadcasters in the U.S., such as CBS and Viacom's Nickelodeon, and premium channels such as HBO and Showtime, has created expectations that these types of offerings, as they increase, will negatively impact pay-TV subscriptions and lead to an increase in cord-cutting behavior. Gartner believes that such a negative impact on pay-TV subscriptions will be observed in not more than 2% of households beyond the millennials' household segment. For these stand-alone channels to be economically viable, they will require prices that are the same as or even higher than the prices charged for them when they are part of pay-TV bundles. Hence, consumers that go the a-la-carte way will find they could end up paying more than through a traditional pay-TV bundle and revert to a pay-TV type of subscription.

Household Behavior

Mature Regions

Adoption of pay-TV services reached saturation levels in 2016, ranging between 60% and 90% of households, depending on the region and country.

- In North America and some parts of Western Europe, early adopter households will be more likely to drop their traditional pay-TV subscription and adopt internet video, becoming the segment with the largest proportion of households without a pay-TV subscription by 2018.

All Regions

Starting in 2016 and continuing through 2021, the number of households that acquire a secondary S-VOD subscription will increase by up to 13% for high-income, early adopter households and 5% for higher-income straggler households in all regions.

The proliferation of S-VOD providers, each with a unique offering such as original or exclusive content, and consumer familiarity with this type of service, will drive consumers to increasingly subscribe to more than one S-VOD service. New offerings in sporting S-VOD packages, as well as other types of specialized content, will further incentivize consumers to subscribe to multiple S-VOD services.

Consumers, especially middle-income and high-income early adopter and early mainstream households, are unlikely to be satisfied with the content offerings of a single S-VOD provider, and they are likely to take advantage of multiple S-VOD services to maximize the value and diversity of the streaming content they can access. The assumption impacts only consumers in middle-income to high-income brackets. Early adopter segments will have the highest utilization of secondary S-VOD services during the forecast period, ranging from 17% of subscribers in 2016 to more than 50% in 2021. Meanwhile, stragglers will be slower to subscribe to a secondary service, ranging from 0% in 2016 to about 10% by 2021.

Between 50% and 60% of the newly formed households worldwide will not subscribe to a traditional pay-TV service and will choose only among IDLTV, S-VOD, T-VOD and free online video services by 2019.

- Early mainstream households will lag early adopters' behavior by two to three years.

Households' adoption of traditional pay-TV subscriptions started to taper off in mature markets in 2015 and will continue onward. However, there are exceptions in southwestern Europe, Emerging Asia/Pacific, the Middle East and North Africa, and some Latin American countries that will continue on a growth path. Alternative services, such as S-VOD and other forms of internet video services, will become a solid complement or even an alternative to traditional pay-TV services.

Cord-cutting behavior, specifically dropping the traditional pay-TV subscription, will be driven by early adopter households, especially in the highly penetrated pay-TV markets. For example, in North America, traditional pay-TV subscriptions will have dropped by 2.7% between 2016 and 2021, while in some Northern European countries, we expect the drop to exceed 4%.

Toward the end of the forecast, many of the newly formed households within this segment will never subscribe to traditional pay-TV services, because they will be composed of younger demographics, usually referred to as millennials, who grew up accustomed to viewing video from streaming services or internet video services. In emerging markets, the percentage of newly formed households that will choose only internet video services will reach around 60% by 2019. Millennials in these markets will not have been conditioned by a "pay-TV culture" prior to them forming their own households.

Early mainstream households will follow suit and begin to replace traditional pay-TV services with internet video services beginning in 2017 and 2018, as internet video and S-VOD offerings become more stable and the alternatives more similar to the services they replace. Late mainstream and stragglers will not replace pay-TV services with alternative modes during the forecast period.

By 2018, driven by live events and news, cord-cutting behavior will reach a floor below which households will not discontinue their pay-TV services.

Despite early adopter and early mainstream households' cord-cutting behavior in the most mature regions, there will be a floor below which households in any segment will not discontinue pay-TV basic services. This floor will be determined by the convenience provided by the availability of free-to-air television channels in areas where these channels do not have good reception, live and sports events, and certain premium content that is and will be available only through pay-TV services, as well as the way the services are bundled with other communications services that the household purchases. Hence, this theoretical floor will vary by region and by country within the region depending on pricing, quality of service, and availability of alternative services. These minimum levels of subscription to basic pay-TV services will continue beyond 2021.

Average spending per transaction on T-VOD will drop by 2.4% between 2016 and 2021, as consumers purchase a wider variety of content at different price points rather than just premium content.

Overall household average monthly spending on T-VOD will increase as households consume more transactions per month. However, from purchasing almost exclusively blockbuster films at a premium price, the mix of the VOD viewed and paid for will include on-demand TV series episodes and long-tail movies at lower prices per view, pushing down the average spend per transaction. This trend is not even across all regions. Some additional features on T-VOD content, such as 4K and virtual reality (VR) streaming, will command a premium, impacting favorably in North America where average spending per transaction will increase by 2.9%.

Supply-Side Factors

Technology Roadmap

Analog television switch-off will drive adoption of pay-TV services in emerging markets through 2021.

The conversion of analog television broadcasting to digital television renders television sets with no digital tuner obsolete. By 2018, a large number of countries around the world will have completed the switch-over to digital television, with Brazil being one of the last countries to switch off analog transmission. China, Iran and North Korea are exceptions, as no deadlines have been set, although migration to digital transmission has already begun in these countries. Households in sub-Saharan Africa, Emerging Asia/Pacific and Latin America will extend the use of their analog TV sets by subscribing to pay-TV services that have external digital-to-analog convertors as part of the service.

Digitization of TV signals and deployment of new transponders will make traditional pay-TV services available to nearly 100% of households by 2021.

This is particularly true in sub-Saharan Africa, the Middle East and North Africa, and Emerging Asia/Pacific, where pay-TV service provider networks cover mostly densely populated urban areas. Availability of pay-TV services, mostly over satellite platforms, will meet unfulfilled needs as service providers increase their reach.

Required investments in technology will delay wide availability of ultrahigh definition (UHD) content and services other than via streaming after 2019.

Currently, most of UHD (or 4K) content available is through streaming services, and it is very limited. Streaming services are best-positioned to deliver UHD content, followed by satellite services, and broadcast TV lagging well behind. Even with UHD service available, experiencing it on the big screen requires a UHD-ready television set (or any access screen) in the home, a device that has a replacement cycle of eight years on average.

Managing bandwidth for UHD resolution is still challenging. Implementation of High-Efficiency Video Coding (HVEC), the advance video codecs that allow for better compression and makes delivery of this ultrahigh definition delivery possible, is still struggling with licensing fee issues. This slows down implementation since it is not clear how costly adopting this technology will be down the road. Also, one hour of 4K broadcast can require between 400 and 500 gigabytes, which exponentially increases bandwidth transport requirements.

Furthermore, broadband access speed requirements for UHD video streaming are high (between 20 Mbps and 25 Mbps minimum), which will have an impact on the consumer experience as well as adoption.

The current fragmentation on UHD delivery technologies and that of the complementary technology high dynamic range (HDR) has added confusion to consumers when it comes to acquiring UHD- and HDR-ready TV sets. We expect that the new International Telecommunication Union (ITU)-approved HDR standards in June 2016 have not yet brought clarity and uniformity to TV technology deployments on TV sets.

A positive move that will not be fruitful for a while is the U.S. Federal Communications Commission (FCC) giving its approval to broadcasters to voluntarily start rolling out ATSC 3.0, a broadcasting standard used in North America, some Latin American countries and South Korea. This standard will support UHD video, HDR, high frame rate, wide color gamut and 3D. However, it is still unclear how the implementation will take place. In South Korea, the standard will start to be rolled out this year, and LG has started to ship TV sets with ATSC 3.0 tuners. However, this is still moving very slowly.

However, the slow move to make content available on UHD for television consumption as well as the slow adoption by traditional pay-TV service providers will result in a not significant level of consumer adoption before 2019.

Household fixed broadband penetration in mature markets will grow from about 74% in 2016 to more than 76% in 2021.

Household fixed broadband penetration in emerging markets will grow from about 26% in 2016 to more than 28% in 2021.

Fixed household broadband penetration is the foundational technology for most behavior around VOD services, but it is not the only gating factor. Advancements on 3G and 4G mobile data deployments and speeds are enabling consumers to access VOD services without a fixed connection. This is more prevalent in emerging markets, although not exclusive, especially in rural and more remote areas. It is expected that toward the end of the forecast period, 5G technologies will start to provide bandwidth capacity in rural and remote areas capable of streaming very high video resolution such as 4K content, effectively replacing fixed broadband connections.

Households in mature markets choosing greater than 100 Mbps services will grow from 10% of those that choose to have broadband in 2016 to 25% of broadband subscribers in 2021.

Demand for accessing video streams simultaneously, either on-demand or live, on multiple devices in the home will continue to increase, creating a bottleneck in the broadband access. Encoding techniques and streaming technology improvements implemented by service providers will contribute to enhance the experience, but not enough to catch up with general usage and adoption of 4K services. To improve the experience and as technology becomes deployed and available, consumers will be motivated to try higher bandwidth throughput services by service providers' promotional marketing, and will continue subscribing to such services after the promotions run out.

Competitive Landscape

Where free-to-air television content offering is strong and its geographic reach is good, households will have a lower adoption of paid-for video media services than in regions with low quality free-to-air TV content or poor geographic coverage.

Lack of compelling content on free-to-air television and extensive country territories, where free-to-air television coverage tends to be poor, are strong influencers on household decisions to subscribe to pay-TV services. North America and Latin America are characterized by the vastness of territories, poor reach of free-to-air television and high household penetration of pay-TV services. Conversely, in some Western European countries where content is compelling and coverage is good, pay-TV service penetration has lagged behind other regions.

Sixty percent to 70% of broadcasters worldwide will have launched online access to catch up content and live broadcasts by 2017, making their content accessible from any connected screen.

At least half of the pay-TV service providers will have launched stand-alone, internet-based S-VOD and T-VOD services to monetize their content catalogs by 2021.

Most large film studios, distributors and independent studios will have launched T-VOD services, while premium channel networks will have launched direct-to-consumer S-VOD services to monetize their content beyond pay-TV services by 2017.

The number of video service providers will be multiplied several times during the forecast period. Pay-TV service providers will be competing among themselves and against new alternative services, such as HBO Now, Showtime Anytime, CBS All Access and Now TV, for the household monthly spend on video media services.

Through 2021, sports events, premium movies and TV series increasingly will be available only on paid services, such as pay-TV, S-VOD or T-VOD, driving growth in these segments.

Content owners will strive to protect and increase the perceived value of their productions by ensuring that they can be available only through platforms and services that derive additional revenue from them. We expect business models around content release and rights to somewhat change over the forecast period; for example, premium TV series and films being available first on S-VOD services but always extracting additional value, driving households to subscribe to video media services in order to access this content. Additionally, pure-play VOD services specializing in sports will compete with traditional service providers to acquire exclusive premium sports content distribution rights.

360-degree content and immersive reality will be limited to complementary online content through 2021.

The delivery of content in 360 degrees and virtual reality requires high bandwidth and the use of head-mounted devices (HMDs) for a high quality experience. The minimum bandwidth requirements for these types of immersive experiences are similar to that of UHD requirements. Yet in the last 12 months, providers are experimenting with immersive reality content delivered to mobile devices as a way to assess interest in 360-degree video and to differentiate from the competition.

Sky in the U.K., Orange in France, Movistar in Chile, Portugal Telecom in Portugal, and MTG for its Nordics Viasat service, among others, have launched VR apps to allow users to watch 360-degree videos with a HMD. All of these offerings are just videos to promote content, such as sports events, or are extensions to main content that has high viewership. Similarly, Hulu and Netflix also have a VR app to promote some of its original TV series with complementary 360-degree content. We expect 360-degree content to be limited to streaming to mobile devices and to promotional or complementary content for the main content delivered to the screen beyond 2021 because of the cost of production, the requirement of a HMD to experience the content, and the technical difficulties and investment to deliver such content to TV screens.

Pricing Strategies

Video media service pricing will experience small increases through 2021.

Pricing of S-VOD services will be similar across most geographies and represent roughly 10% of the monthly spend on pay-TV services through 2021.

S-VOD services, particularly those delivered by global service providers, will be between $8 and $14 per month across most geographic regions and will have slight increases over the forecast period to account for increased cost in securing additional content rights and additional value-added features. For some regional S-VOD providers that are in regions where such price levels are not sustainable, such as in Emerging Asia/Pacific and Greater China, services are offered at lower prices, but will remain constant over time. In these regions, the more expensive S-VOD services' pricing will represent 25% or more of average monthly spend of pay-TV services.

Pay-TV services will experience small increases in subscription fees over the forecast period to account for higher content costs and newly launched value-added services, such as 4K content.

Regulation

Through 2021, pay-TV services will remain heavily regulated and subject to intervention by governments.

Through 2021, S-VOD services will remain largely free from direct regulation in most geographies.

Government rulings, regulation and direct intervention in the market through public broadcasters will have an impact in specific regions and countries. For example, government regulation forcing pay-TV service providers to offer content for which they have exclusive rights on a wholesale basis to the competition, or the outright acquisition of rights to broadcast live sports events by public broadcasters, will have a direct effect on subscription and spending on video media services.

Additionally, regulation or lack of it will influence the availability of services in different countries and regions. Traditional pay-TV services are heavily regulated in most countries, while IDLTV and S-VOD services are seldom directly regulated and consequently have a faster go-to-market approach. However, regulatory agencies are increasingly focusing on the latter, although there are no indications of intentions to regulate the industry in the near term.

There are, however, attempts to tax S-VOD services. Since January 2015, a 2% tax on the monthly subscription applies to VOD providers that operate in France that do not have their headquarters in the country. Legislation to reach S-VOD service providers with the same taxes that are applied to pay-TV operators or other forms of taxation to help fund local content is being considered in several countries, including the EU, Brazil, Paraguay and Argentina. We expect different types of taxation to increasingly reach S-VOD and T-VOD in an attempt to exert fiscal control and to fund local content production.

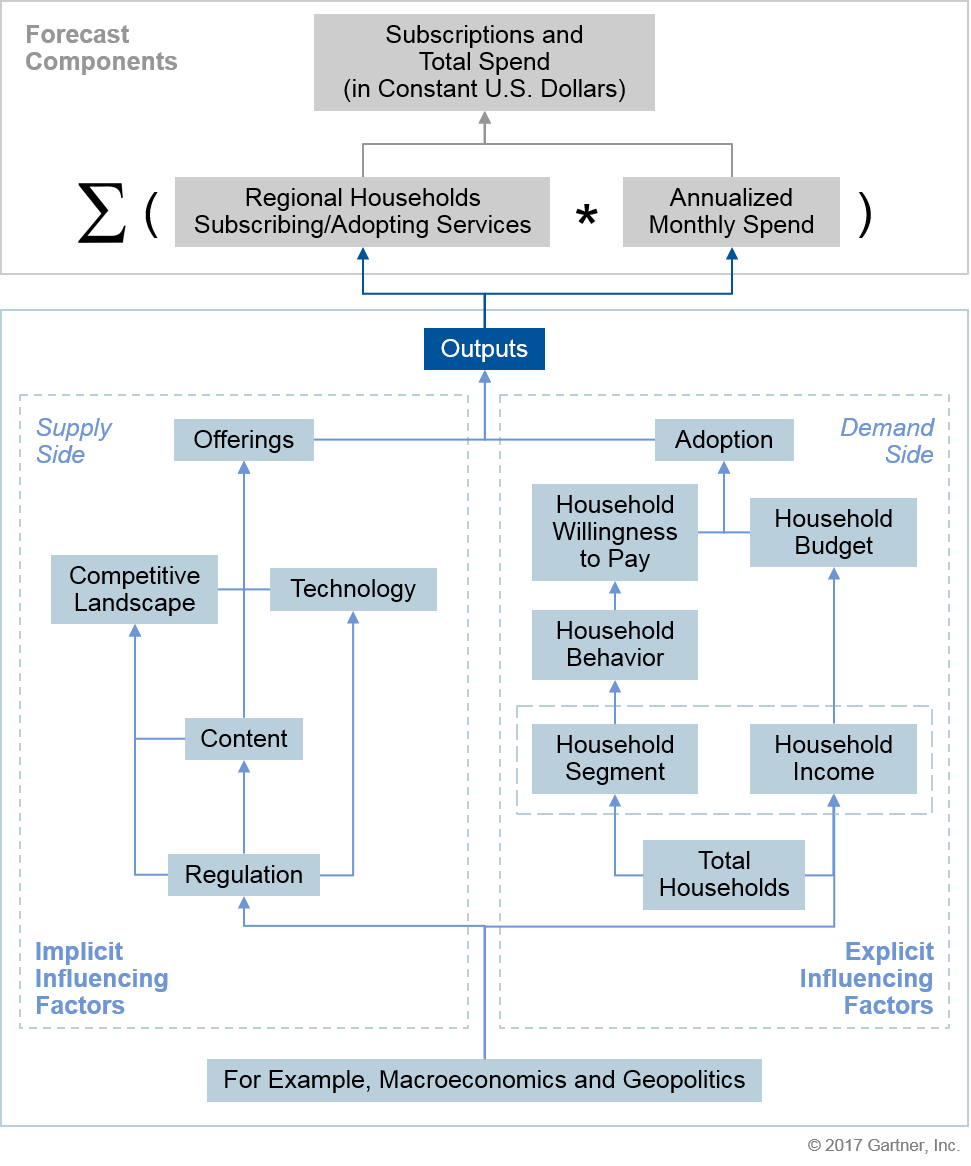

Market Model or Methodology

The video media service market model consists of two fundamental components – subscription/adoption of video media services and average monthly spend.

- Households subscribing/adopting services. This component estimates the projected number of households subscribing to pay-TV (traditional and IDLTV) and S-VOD services and spending on T-VOD.

- Annualized monthly spend. This component estimates the projected household monthly spend, annualized, on pay-TV (traditional and IDLTV), S-VOD and T-VOD services.

The two components are aggregated at the regional level to provide total pay-TV (traditional and IDLTV), S-VOD and T-VOD service revenue worldwide and total pay-TV subscriptions worldwide.

Figure 2 provides a graphical representation of the video media service forecast.

Figure 2. Video Media Service Forecast Market Model

Source: Gartner (August 2017)

Influencing Factors

We have grouped the influencing factors in the demand-side and supply-side categories. Demand-side factors are deemed explicit because they directly impact household decisions to consume these services. Supply-side factors are implicit influencers in this model because they don't have a direct impact on the households, which also have no control over them.

Explicit Influencing Factors

Total Households

The number of households will impact the overall forecast both directly and indirectly. A direct impact means that an increase in the forecast for households will cause an increase in the forecast for spending on video media services. An indirect impact means that any changes in the forecast for the distribution of the households across income bands or consumer psychographic segments will cause a change in the forecast for spending due to the differences in average spend or due to the differences in propensity to consume.

Household Income

Household income will directly influence the households' ability to spend on video media services. Increases in household income will impact the forecast for spending on video media services as more disposable income is available for these types of services.

Household Budget

Each household allocates a certain amount of its income for video media services, and this is directly influenced by its overall income. Households in higher income bands will have bigger budgets to spend on these types of services. For any given household in any given income band, this budget is relatively fixed but will be spent differently depending on the household preferences.

Household Segment

Applying Gartner's psychographics segmentation study, we defined four distinct household segments, based on their attitude to technology consumption. Each household segment will have a different behavior toward adoption of video media services and the different alternative services available to them. Each segment has and will have different preferences when it comes to consumption of the different types of video media services.

Willingness to Pay

Households have and will have different dispositions as to how they spend their budgets for video media services. They can spend it all on one type of service, for example, a traditional pay-TV or IDLTV subscription, or allocate to two or more types of services, such as pay-TV, S-VOD and T-VOD services. Their willingness to pay for these types of services is defined by the psychographic segment where they belong, their preferences and what's available to them.

Implicit Influencing Factors

Regulation

Regulatory policies determine the provider's deployment of technology and infrastructure needed to access video media services. They also determine what the services are and how they can or will be offered.

Competitive Landscape

The competitive landscape provides a variety of alternative services that compete within the same category of service and across categories. The competitive landscape influences the options available to consumers in a particular geography, which in turn influence the choices that consumers make, as well as the spending.

Technology Roadmap

Infrastructure makes available the various technological connectivity options to the consumer's home. Once the technology is available, consumers have the option whether to choose a subscription to a particular communications service.

Note 1. Pay-TV Services, Subscription-Based VOD Services and Transaction-Based VOD Services

Pay-TV Services: Linear television services, typically delivered over a dedicated, closed infrastructure – be it cable, satellite or IPTV – where the quality of service is assured. This category also includes internet-delivered linear TV (IDLTV) services or what the industry markets as live streaming TV services – where the service is delivered over-the-top, on a best effort, to any screen.

Subscription-Based VOD Services: Paid subscription services where a monthly fee provides access to an unlimited video-on-demand service, delivered over-the-top, on a best effort, to any screen.

Transaction-Based VOD Services: Transactional-based video-on-demand (pay-per-view) access to video content delivered via the pay-TV service provider's managed network or over-the-top service providers as best effort.

Source: Gartner Research Note G00328433, Fernando Elizalde, Amanda Sabia, Derek O'Donnell, 14 August 2017