Accelerating Digital Transformation in Insurance

Transformational Challenges

Digitalization is enabling new products, services, business models and new value propositions across the value-chain. For any insurance company hoping to realize these tremendous opportunities, digital transformation must be at the forefront of their strategy. But those taking these important steps are often faced with several challenges:

- Legacy systems. Replacing existing infrastructure and processes that are embedded deep in the organization can be a burden on resources and a timely process. Furthermore, any transition must have little to no disruption to day-to-day business.

- Complexities. Adopting the right partners and the right solutions that are scalable in design and future-proof at conception. Handling of more and more data being generated by the connected economy, while conducting more complex analytics.

- Realizing return on investment. Generating returns within a short space of time and mitigating risk from new digital centric entrants looking to disrupt the market. Meeting and exceeding ever increasing customer expectations, while increasing the value pool.

To help overcome these challenges, insurers need to:

- Prioritize IT transformation and support with a strong economic business case

- Invest in new areas including mobile, digital marketing, analytics, cloud and security

- Support customer-centricity through new business models such as usage-based insurance, affinity-based marketing and new customer interaction options

- Include off-premises hosting and cloud-based models

Accelerating Digital Transformation with Octo

Octo's solution, the Next Generation Platform (NGP), uniquely links the characteristics of a horizontal IoT framework with rapidity and revenue to pre-built vertical use cases, helping insurance companies accelerate their digital evolution.

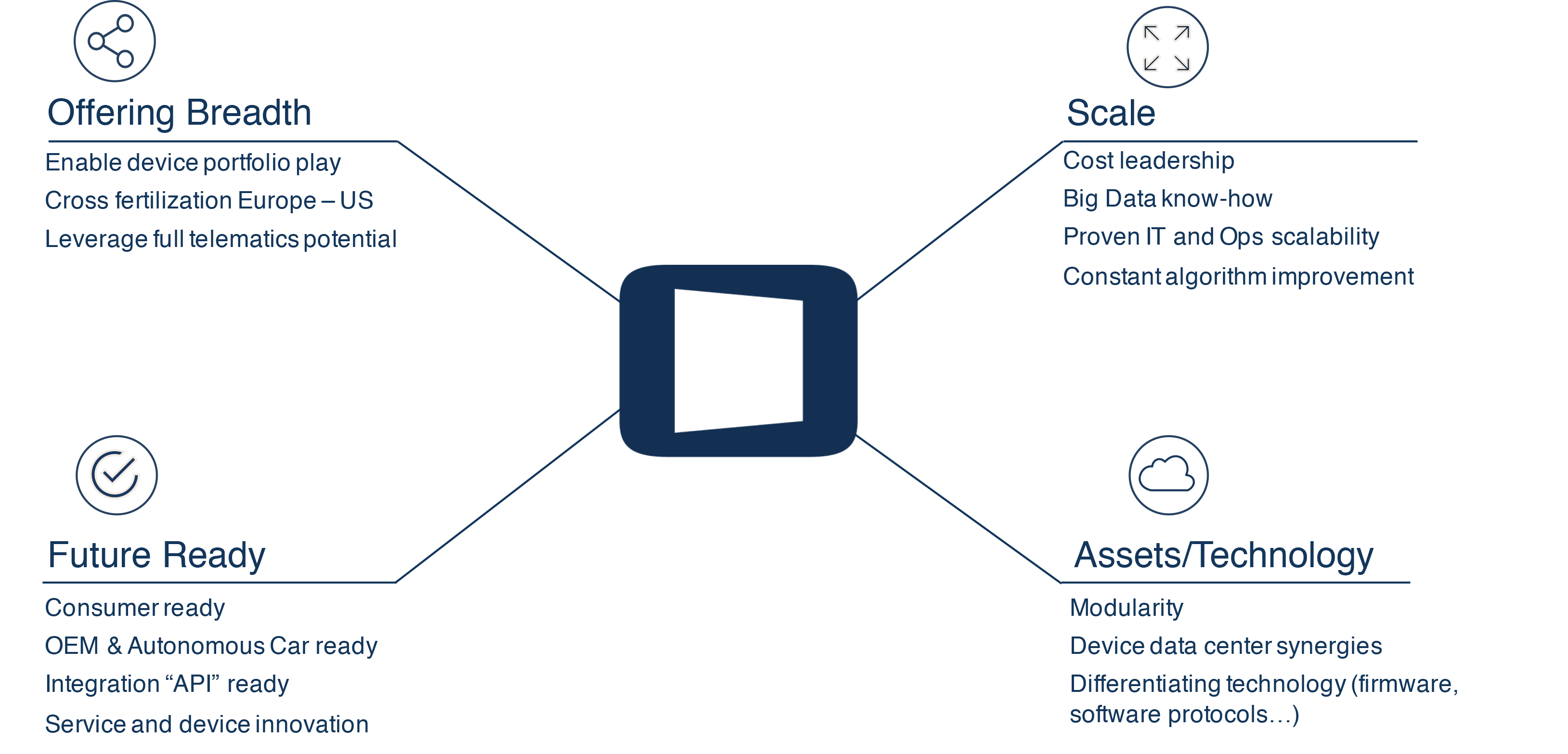

The platform has been built with four underlining principles. Breadth of offering to cater for all market needs, scale of capability that today already includes the world's largest insurance telematics database, assets/technology compatibility in its widest form and be fully future ready (see Figure 1).

Figure 1. Core Principles of Innovation and Competitive Differentiation

Source: Octo Telematics

Centered around Octo's NGP are five unique components:

- From a Traditional Approach to Real Data-Driven Big Data Analytics and Scoring

- Breadth of Services and Breadth Sensors

- Driver Genome

- AI for Crash Validation and Reconstruction

- CRM Service Cloud and Digital

1: From a Traditional Approach to Real Data-Driven Big Data Analytics and Scoring

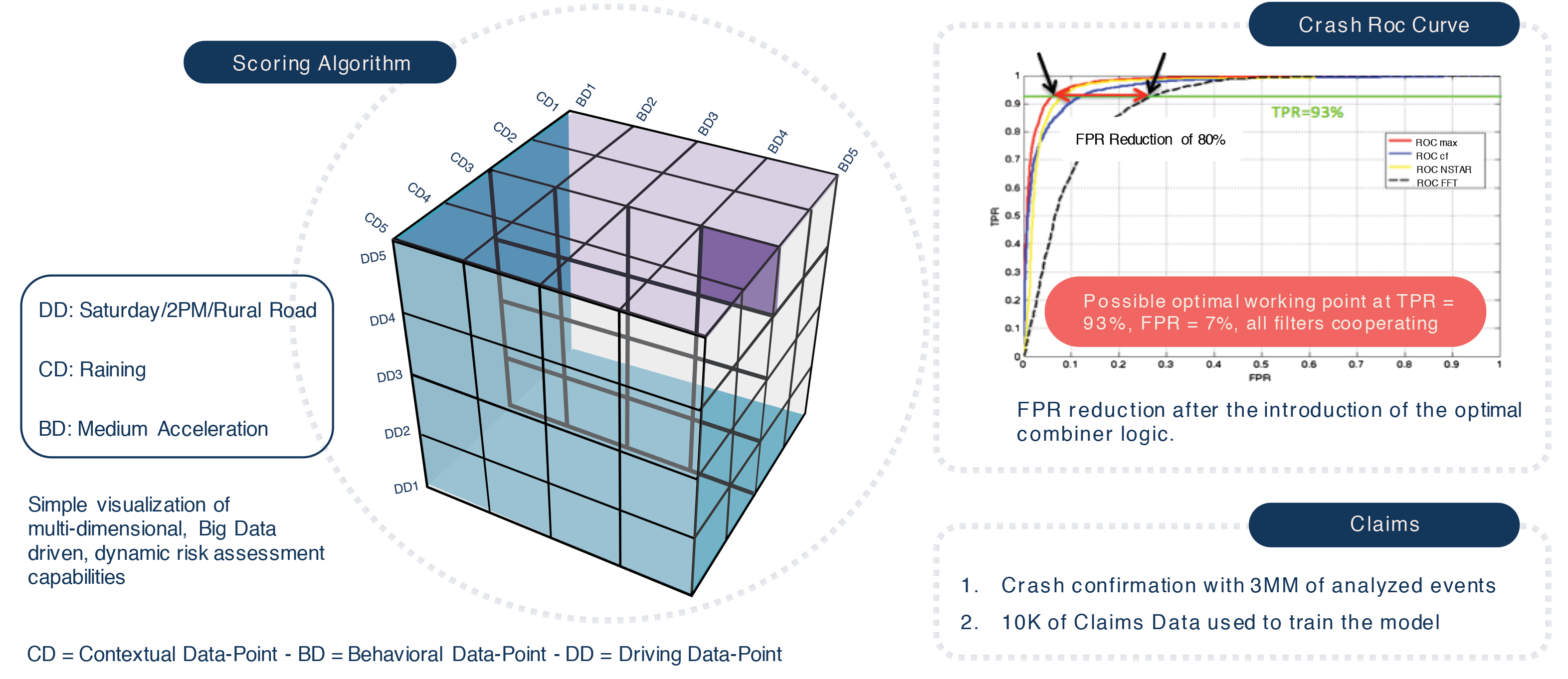

Supporting the insurer through digital transformation with market-ready analytics based on the performance generated from the world's largest insurance telematics database. Simplifying the complexities from multiple dimensions of driving data and shortening the time-to-market with ready to use scoring algorithms that replace legacy actuarial practices.

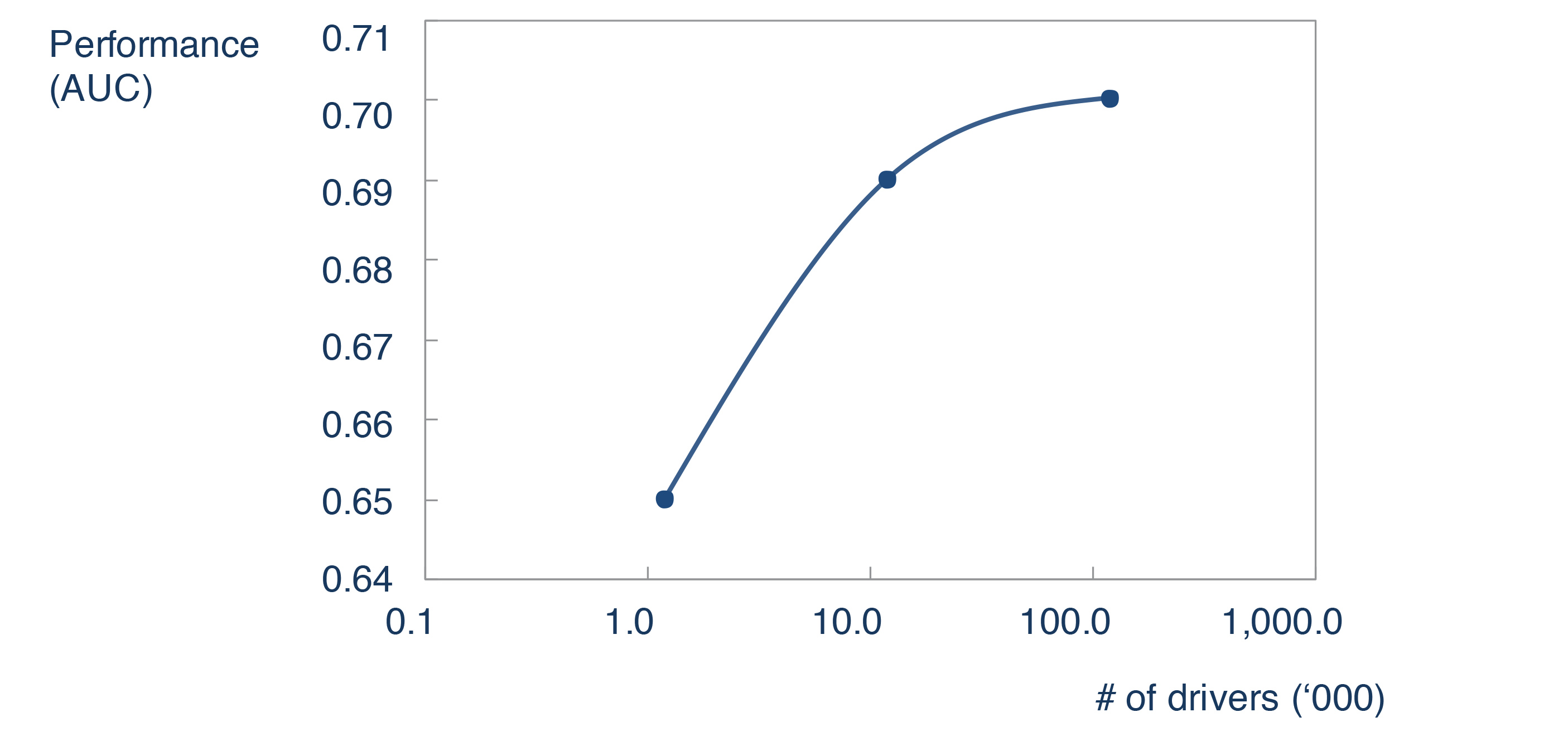

As the market leader in connected auto insurance, Octo have over 100 B2B partners and more than 5.3 million connected users. With the largest number of connected users, Octo is the only telematics provider who can access new levels of performance from big data analytics. As the volumetric size of the dataset from drivers increases, performance increases at an exponential rate (see figure 2).

Figure 2. Exponential performance versus driver data sets

Source: Octo Telematics

Octo scoring algorithms leverage on three main dimensions, Driving Habits, Driving Behavior and Driving Context.

Driving Habits: Consider where and when the customer drives at different times of the day, days of the week and various road types (highways, urban and extra-urban roads). This information is collected from the GPS sensors and can be analyzed with different levels of granularity. The Octo standard is based on a 2 km frame.

Driving Behavior: Driving behavior indicators are mainly based on cinematic measures collected from the accelerometer and gyroscope, and generated from car movements. Events measured include:

- Speeding

- Hard braking

- Harsh acceleration

- Cornering (fast driving through corners)

- Sprinting (quick changes of direction)

- Lateral movement

Each event brings distinctive information and when pieced together provides a thorough picture of the manner of driving, focusing on driver behaviors. Driving behavior events are measured and analyzed considering both the number of events and also a comparison of the best combination of key metrics. A sample of these metrics could be reported as follows:

- Duration of events (milliseconds)

- Average severity (milliG)

- Maximum peak severity (milliG)

- Speeds (Km/hour at the beginning and end of the event)

Driving Context: all external information like metrological environment, traffic and demographic communities coming from different sources.

With regards to contextual habits information, depending on the country, the Octo algorithm takes into consideration the risk component of driving in a certain geographical area. To support this Octo has developed a new proprietary solution for the definition of risk areas (communities) working at a map level. The process relies on the following assets:

- Big data availability to geo-reference millions of events

- Analytics based on methodology working at a spatial level

- External data fusion

The outcome is a new area definition which is different from common zip code classifications traditionally used by insurers. The new area definition used with road type classification allows the insurer to define a more granular classification of the risk context. This includes vehicle, driver behavior, location, context, environment, crash and other complex data that we analyze across more than 2,000 combinations of parameters to provide actionable intelligence and insurance grade algorithms.

2: Breadth of Services and Breadth Sensors

While remaining device agnostic, Octo supports the insurer through digital transformation with the widest breadth of services and sensors, catering for all target markets. As well as significantly reducing the time-to-market, the breadth of services helps insurers increase their value pool.

Octo continues to define the connected auto insurance market with:

- A breadth of class leading services such as risk scoring the trend analytics, fraud prevention and crash and claims

- A breadth of sensors such as GNSS, accelerometers, gyroscopes and cameras; with a wide variety of form factors, including AAAS (App as a Service on the smartphone), AAAS + Smart Tag Sensor, Black-Boxes, ODB-II, 12v Adaptor and OEM line-fit

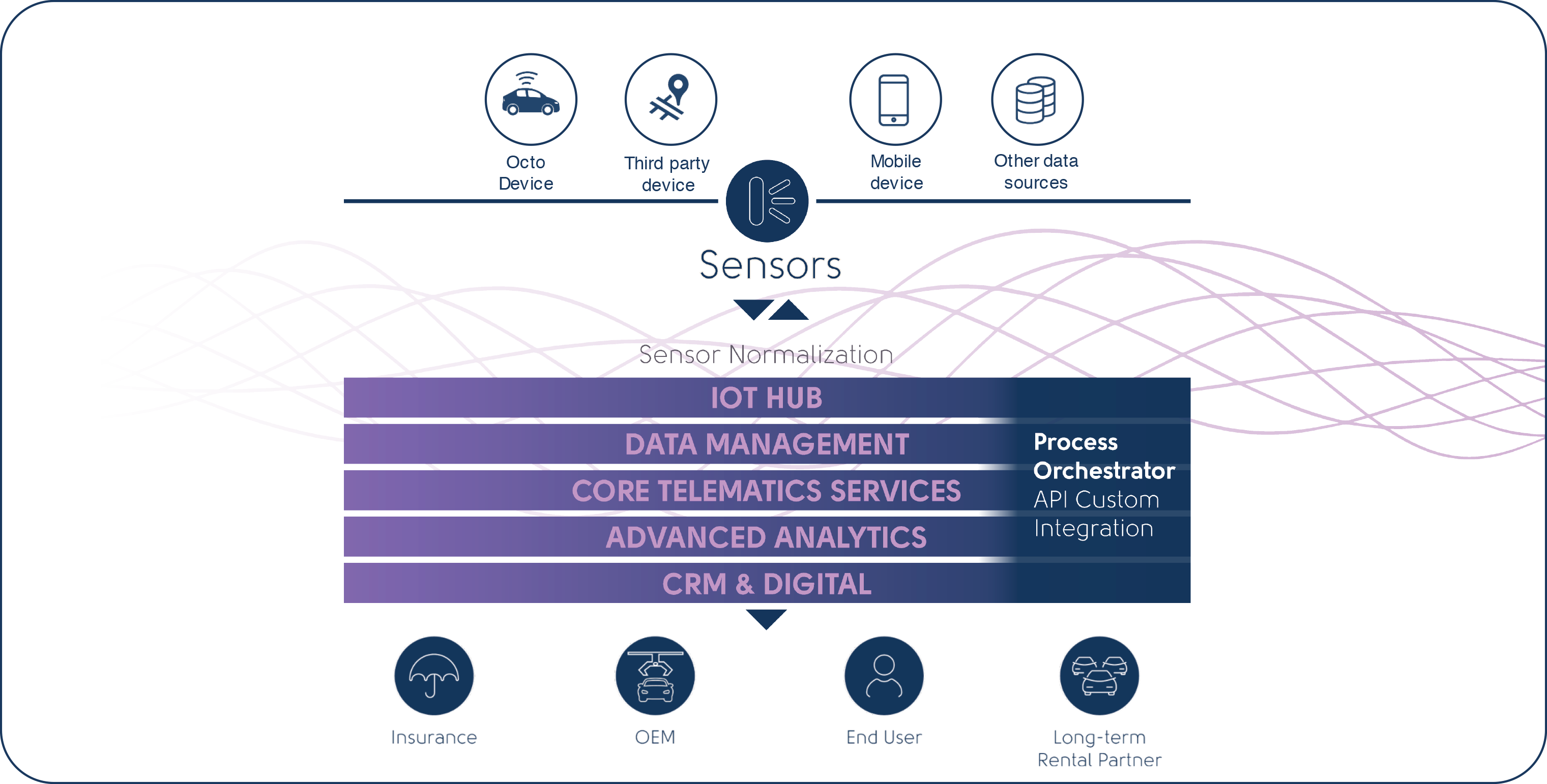

Furthermore, the NGP is designed to be truly device agnostic, not only supporting Octo devices, but third-party and mobile devices, as well as multiple data sources. Complexities and compatibility is fully maintained by the platform through sensor normalization, before value propositions such as data management and advanced analytics service multiple vertical business lines (see Figure 3).

Figure 3. Device Agnostic, Servicing Multiple Verticals

Source: Octo Telematics

3: Driver Genome

Supporting the insurer through digital transformation through detailed 'gene' analytics that provides better driver profiling and proactive risk management. Better understanding drivers on such a granular level also provides visibility when there are data gaps, therefore maintaining a robust service.

The Insurance market is seeking disruptive, technology-driven innovation. Customers are expecting more from their connected insurance policies and insurers can exceed this expectation with capabilities such as machine learning and artificial intelligence (AI), that can potentially prevent an accident before it happens.

Driver Genome is Octo's system for a holistic and granular map of characteristics that influence the risk exposure. It consists of identifying, measuring and tracking changes across a number of features known as "genes". The more complex the Genes are, the more data is required to build them and as a result, the higher the predictivity of the model.

The Driver Genome aims to:

- Address risks that are not well captured by classic insurance pricing parameters

- Allow meaningful inferences from changes to its components

- Contain information about the future evolution of components so the risk evolution is visible

Furthermore, as it is designed to carry a metric, it can also be used for relative assessment by detecting clusters in its genes. This is particularly useful in aiding inferences when there are limited observations available.

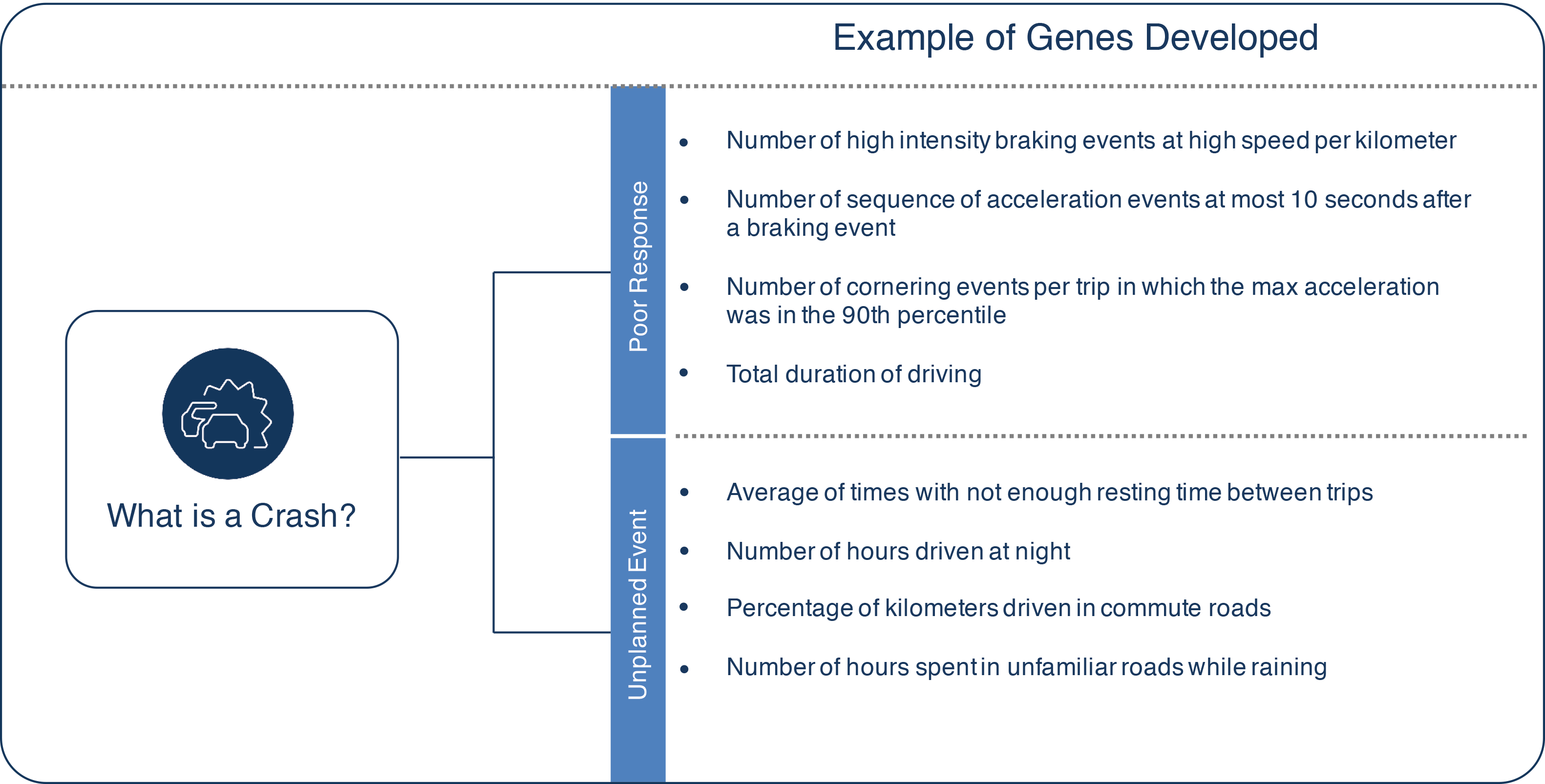

For example, a crash event takes place when a driver provides a poor response to an unplanned event. To better understand the circumstances of a crash event, several genes are developed around possible poor responses and situations in which an unplanned event could take place (see Figure 4).

Figure 4. Example Crash Related Genes

Source: Octo Telematics

This generates additional value for Octo's insurance partners, as it allows them to enhance their technical pricing, positively influence the insured's behavior and enable new innovative pay-per-use services and products.

4: AI for Crash Validation and Reconstruction

Supporting the insurer through digital transformation with services that supersede legacy systems, in terms of risk assessment, crash notifications and claims processing. Value is realized across the value-chain, with customers benefiting from more accurate insurance quotes, emergency/breakdown support when needed and in the case of an accident, a faster settlement.

Consistent with the quality of Octo's scoring algorithm in which risk is modeled against three dimensions, contextual, behavioral and driving data-points to provide actionable insights for insurance partners (see Figure 8). Octo's state of art technology for crash detection is combined with different algorithms such as space state corridors, neural networks, genetic algorithms, as well as frequency and time analysis.

The accuracy of this approach is measured by the best compromise between the False Positive Rate (FPR) and True Positive Rate (TPR) represented by the ROC (Receiver Operating Characteristic) curve. Based on millions of analyzed events and thousands of confirmed claims, Octo has reduced the FPR by 80%, while maximizing TPR detection to 93% (see Figure 5).

Figure 5. Analytics Models: 3D Risk Model with Embedded Crash Data

Source: Octo Telematics

The engine behind the complete crash and claims service is a combination of a powerful mathematical model and a proprietary statistic engine. Currently, with any new crash recorded, the system searches for similar events in the claims database based on acceleration values, similar values are then expected to have similar levels of damage. Pictures relating to the stored claim are then displayed for comparison proposes.

Furthermore, by combining the telematics data recorded from the sensors (acceleration, brakes, oscillations, impacts, etc.) with 3D and 2D animations, Octo's Multimedia Claim Service allows you to objectively reconstruct a claim, visualizing a crash as if it were real. In this way, the insurance company can lead a reliable process of accountability and claims settlement, limiting potential fraud. Starting from the analysis of a video reconstruction, it will be possible to verify the compatibility and the suitability of the documentation of each claim received.

The next step of evolution is the damage estimation based on image recognition technology. To achieve this goal, it is necessary to develop an engine capable of recognizing different types of vehicles, types of damage and the magnitude of damage, solely from vehicle photographs (see Figure 6).

Figure 6. Example Image Recognition Technology

Source: Octo Telematics

5: CRM Service Cloud and Digital

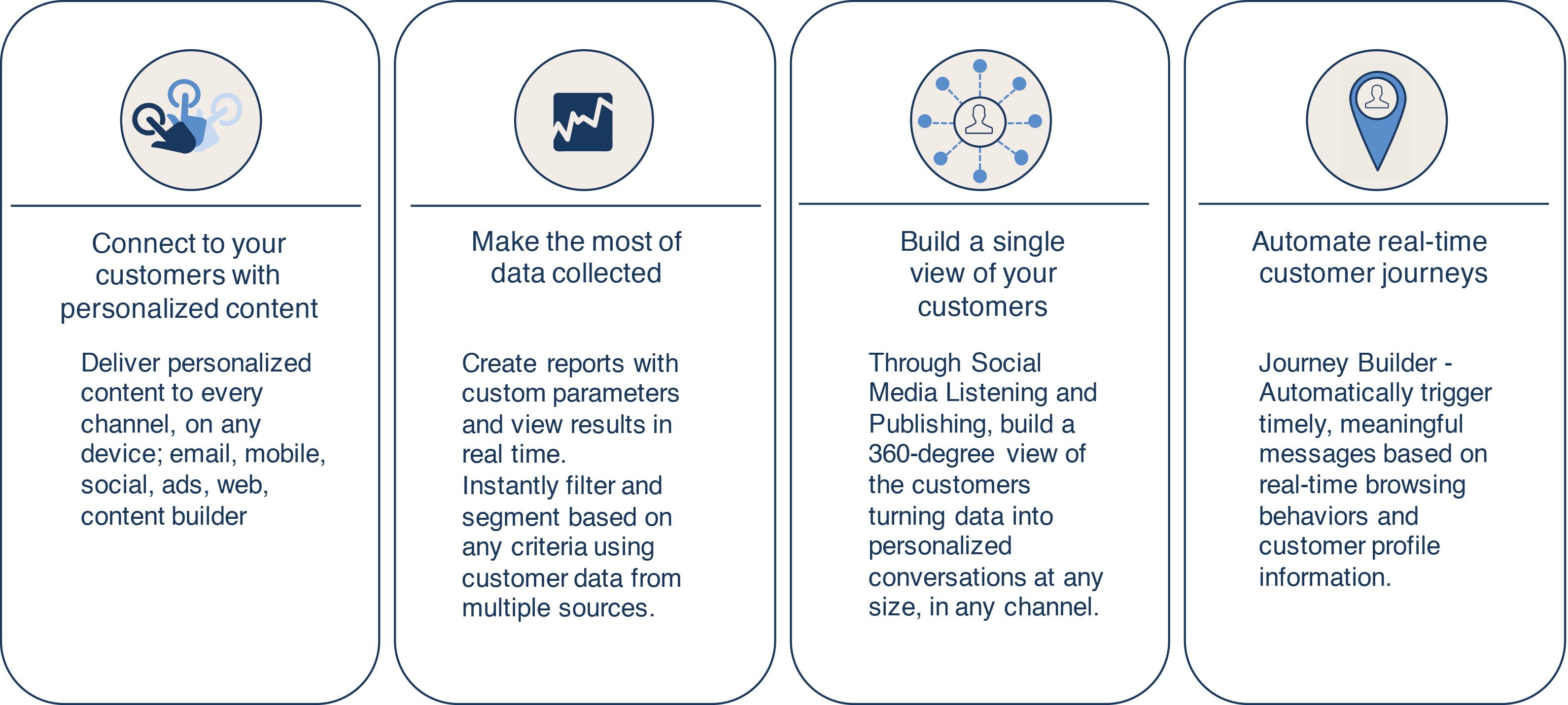

Supporting the insurer through digital transformation with an integrated Customer Relationship Management (CRM) solution to increase customer retention, as well as increase up-sell and cross-sell potential. Enhancing the opportunities for more targeted, tailored marketing and pricing strategies.

The NGP is designed to be highly configurable, modular with product and service building blocks, with an architecture that reduces time-to-market. Compatible with B2B, B2B2C and B2C working environments, it supports personalized customer content which can be automatically triggered, provide custom reporting and helps build a 360-degree view of individual customers (see Figure 7).

Figure 7. Data Derived CRM Value

Source: Octo Telematics

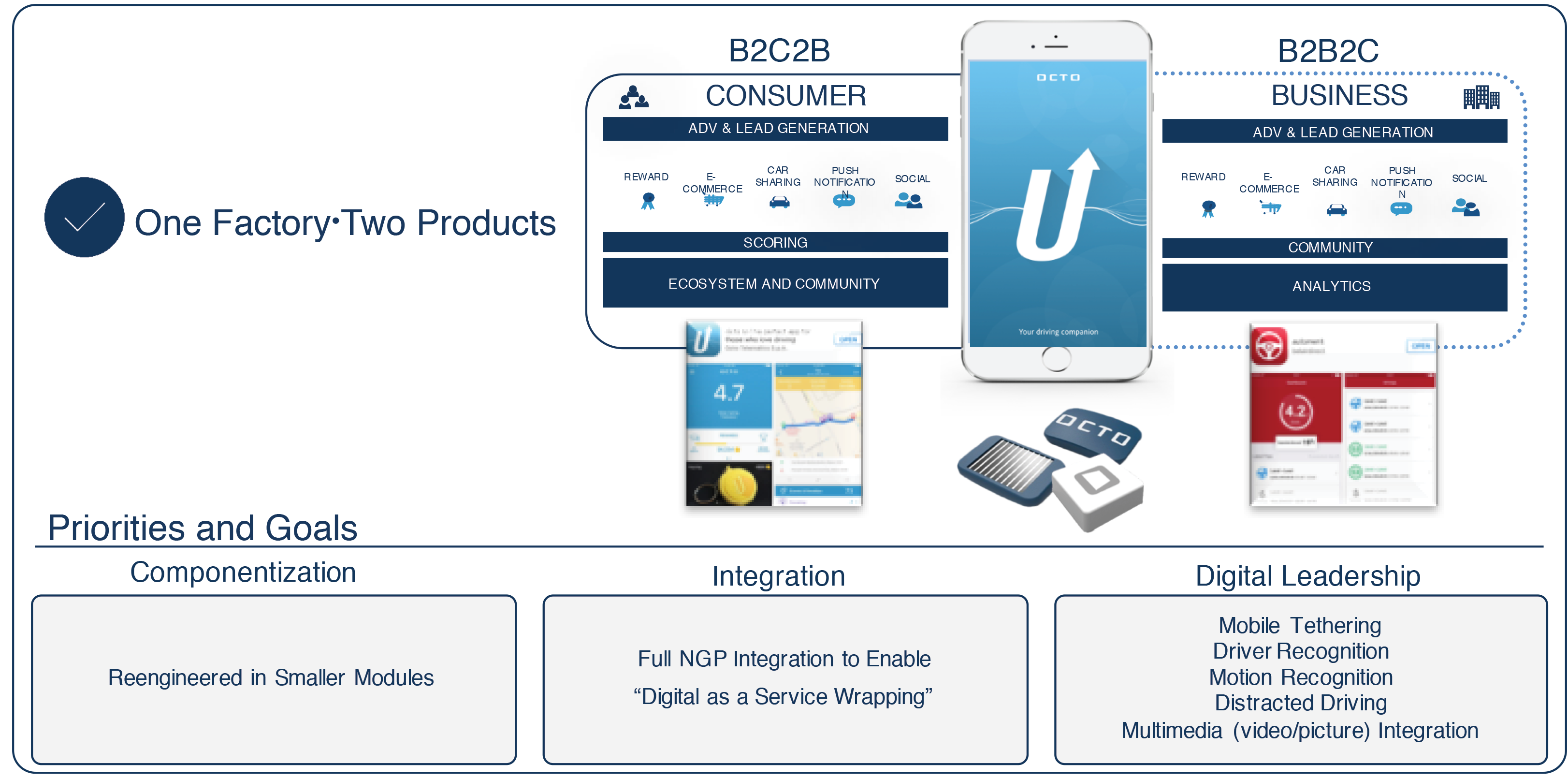

Directly complimenting Octo's CRM services, is Octo's enhanced digital offering. Designed around the smartphone, the app supports both B2C2B and B2B2C business requirements. For example, building a community of consumers for gamification or analytics that support business activities (See Figure 8).

Figure 8. Digital Value Proposition

Source: Octo Telematics

While the Octo smartphone app utilizes the latest built-in sensors from a smartphone, additional value can be further leveraged from being fully integrated with other sensors on the NGP. For example:

- Bidirectional flow of experiences between the Octo smartphone app and any additional sensors

- Octo smartphone app crash detection and reconstruction can be implemented with ease with Smart Tag integration

- Driver identification schemes can be implemented by exploiting user interaction with the app

- Distracted driving schemes can be better implemented by exploiting the integration of additional sensors

Digital leadership across Octo solutions is focused on supporting partners in achieving their priorities and goals across componentization, integration and leadership.

CRM Service Cloud and Digital, like the other unique components of Octo's NGP, is another step towards achieving digital business excellence.

Source: Octo Telematics