2021 Global AI+IoT Developers Ecosystem

Tuya Smart, the leading global AI+IoT platform #interconnectivity

Preface by Schneider Electric

The world is becoming more digital, leading to disruptions in every sector of our economy. The global pandemic has profoundly shaken society and will continue to be a catalyst for change as we build the new normal. Digitization of everything has rapidly increased as companies look for solutions to ensure business continuity. Rapid acceleration of digitization brings new opportunities for growth for some, and challenges for those not able to pivot and adapt.

As industries digitize, the Internet of things (IoT), real-time information, and digital tools are breaking traditional silos, enabling remote operation of facilities and creating innovative and sustainable economic models. Artificial Intelligence technologies are enabling new solutions that can increase efficiency and sustainability as decisions are made in real-time.

At Schneider Electric, we believe 'Life is On' and have a customer-first approach and obsession with innovation and sustainability. We are leveraging IoT to connect energy, automation, software, and analytics to fuel revolutionary innovations in efficiency, sustainability, reliability, and safety for our customers.

We also know we can’t create all the solutions needed for a more sustainable and resilient future on our own. This is why we believe in building an eco-system of partners to co-innovate and scale bold ideas to meet customer needs. We also empower our over 650,000-strong partner ecosystem to expand our coverage.

It's clear that AI and IoT industry's development cannot be separated from a diverse developer ecosystem and a neutral and open development platform. Industries working together to build an interconnected development ecosystem strengthens the innovation generated. Strategic partnerships and alliances are essential to create and shape the future of IoT technology and smart living to ensure our buildings are efficient, sustainable and adaptable to new technologies. By working together and leveraging technology, we can develop the innovations needed to tackle the biggest problem we face collectively- fighting climate change, reducing inequality and creating a more sustainable world.

- Emmanuel Lagarrigue, Chief Innovation Officer, Schneider Electric

Preface by Philips

Today, a world based on Internet of Things is at the horizon. From single smart device functionality to multi-categories devices interactions, from remote control in mobile to user value generation in data, users extract more from AIoT applications. Meanwhile, AIoT ecosystems turn more diversified. New collaboration models appear continuously across the spectrum as “closed” in one end and “open” in the other. Under various scenarios, richer vertical applications will be seen.At Philips, a 130-year history health-tech company, we believe that care should be organized seamlessly around people's health journey, across consumers' healthy living at home, out-of-hospital and in healthcare settings – connecting people, data and technology. We believe that IoT is really about people not things.

The true added value of the AIoT lies not in any single device, but in integrated solutions: combinations of many systems, devices, software and services, configured and delivered in a way that address needs of our customers and consumers. IoT enables real-time data capturing and integration from various consumer and medical devices, translating those data into useful insights through AI. Our engagement and care can be very personalized, proactive, and preventative, across an entire journey.

The Global AIoT Developers Ecosystem White Paper analyzes the current situation and future direction of the AIoT industry from a macro perspective, and reveals the current challenges and the key to the development of the industry. In order to realize the interconnection of all things, rich and diverse developers, and an open and neutral platform are indispensable. We look forward to the publication of the White Paper to inject new vitality to the AIoT industry, and enrich vertical applications in different scenarios.

- Andy Ho, President of Philips Greater China, Member of the Royal Philips Executive Committee

Preface by Calex

The surge of digitalization, which took place in the past decades, changed the global business landscape. The new environment pushes the traditional business model's transformation to feed the consumer experience's new requirements. Staying "smart" and "connected" have become the new rules of survival.Lighting is an essential need in daily life. As an innovator of the lighting industry, Calex has been fortunate to follow the progress of the smart home market as a developer since its early days and has offered various products. With the introduction of the Tuya Platform, we found the ideal combination between the ease of use from a consumer point of view and the right price entry point, making smart products available for the mass market.

Technology develops itself as quickly as consumers can adapt. Most good corporations have now come to a stage where they have embraced an ecosystem and welcome its broad compatibility and functionality. No longer does a consumer have to worry about choosing the wrong platform or system as long as there is the cloud to cloud communication between the primary standards. One should think of Google and Amazon, where all the diverse platforms can come together, and the different protocols included in the platform like Wi-Fi, Bluetooth, Bluetooth Mesh, and Zigbee. Each protocol serves a different purpose with its unique features though it is no longer the basis of a consumer choice for a specific smart platform.

In the lighting industry, the discussion on the dimmability of bulbs when changing from incandescent to compact fluorescent to LED took almost five decades. We genuinely believe that the discussion about smart lighting will take less than one decade to come to the conclusion: smart will be the standard for a light source.

It is my privilege to be the preface writer of the 2021 Global AIoT Developers Ecosystem White Paper. The articles inside this white paper indicate the industry's potential trends and elucidate the possibilities of consumer habits variation in the future. I strongly recommend you to read.

- Will Smits, Managing Director from Electro Cirkel B.V. (Calex)

1. Current

1.1 The Definition of AIoT or AI+IoT

AIoT stands for artificial intelligence and internet of things. Broadly speaking, it refers to the integration and application of artificial intelligence and internet of things.

AI (Artificial Intelligence) refers to a technical science about the theories, methods, technologies and application systems to simulate, extend and expand human intelligence through research and development. As a branch of computer science, AI seeks to understand the essence of intelligence to produce a new, intelligent machine that reacts in a similar way to human intelligence.

IoT (Internet of Things): Built upon the internet, IoT is one step beyond connecting devices: it establishes connection between physical objects as well as between physical objects and people.

When AI and IoT are combined, massive amounts of data generated and collected by the IoT are stored on terminals, edges or clouds. These data are then analyzed intelligently through machine learning, thus allowing us to digitize and intelligently connect everything. On the technical level, AI enables IoT to acquire perception and recognition capabilities, while IoT provides data that trains AI algorithms. On the commercial level, the two work in synergy to enhance the real economy through promoting industrial upgrades and experience optimization.

1.2 The Origin, Background and Development of AIoT

AI (Artificial Intelligence) was first formally coined at the Dartmouth Conference, by pioneers in the discipline such as John McCarthy, who was the first to conduct in-depth academic research on AI.

The concept of the Internet of Things was proposed in 1991 by Professor Kevin Ashton of the Massachusetts Institute of Technology. In 1999, a research on Radio Frequency Identification (RFID) first clarified the definition of the Internet of Things: all things are connected to the internet through information sensors, such as RFID and bar codes, to achieve smart recognition and management.

In 2017, at the "All Things Smart · New Era AIoT Future Conference", China officially proposed the concept of AIoT.

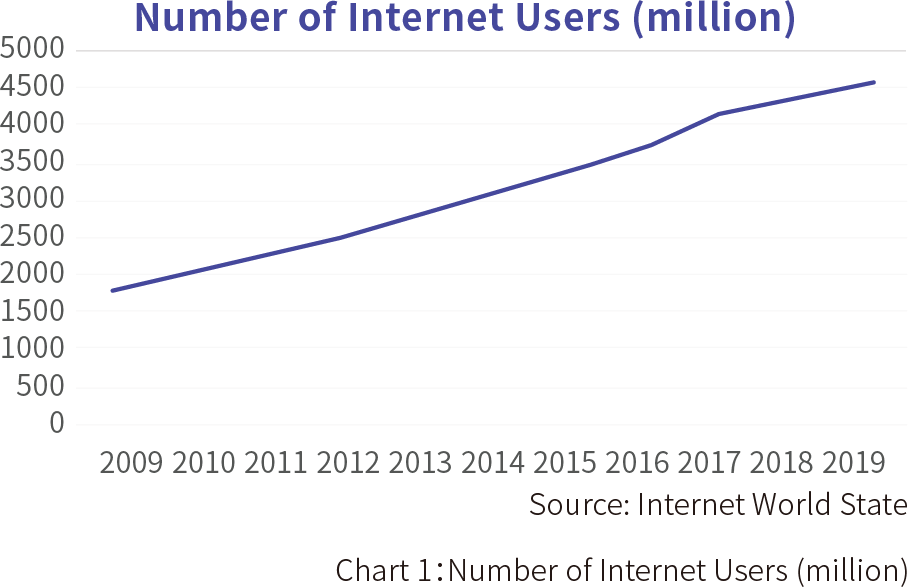

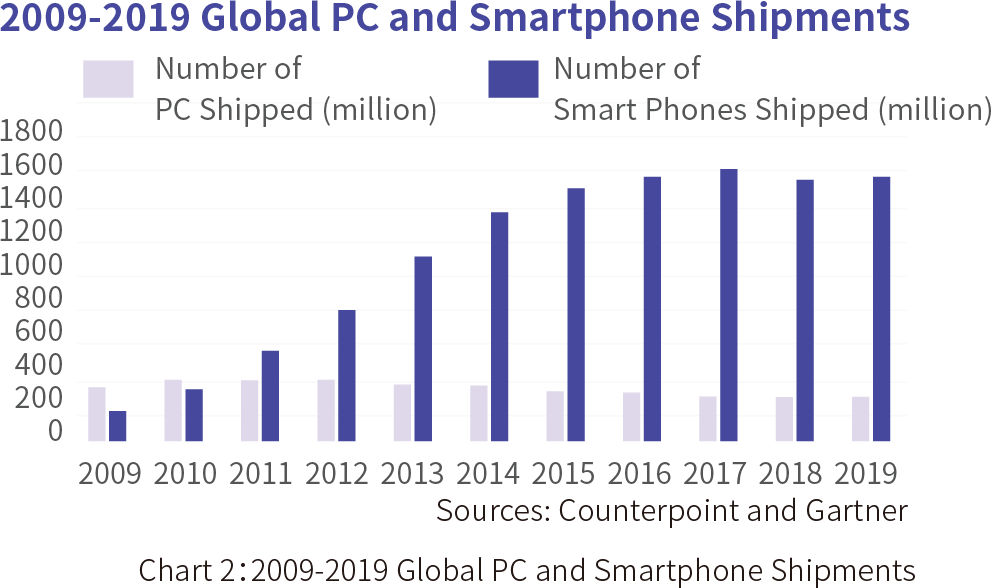

From the perspective of industrial development, the first-generation Internet (PC Internet) is essentially a network of computers. Users gain access to information on the internet through machines, and the main media for connection are signal lines/network lines; the second-generation Internet (mobile Internet), by its very nature, is a network of people, and it’s the reason behind a booming mobile devices sector which churns out smartphones and laptops. In addition, signal transmission of the network has evolved from fixed lines to radiowaves.

With the popularization of the Internet, the number of netizens is gradually increasing, but the demographic dividend is gradually being exhausted, and the shipments of PC devices and smartphones, representatives of the two eras, have peaked. As network communication technologies are continuously innovated (the upgrade from the fixed network to the 5G network brings forth a comprehensive upgrade of bandwidth, capacity, and transmission rate) and device connection technologies see further development (the cost of networking is further reduced), the new generation of the Internet will grant connection to various devices, bringing us one step closer to the phase of "All Things Connected".

Figure 1: 2009-2019 Global Internet Users

Figure 2: 2009-2019 Global PC and Smartphone Shipments

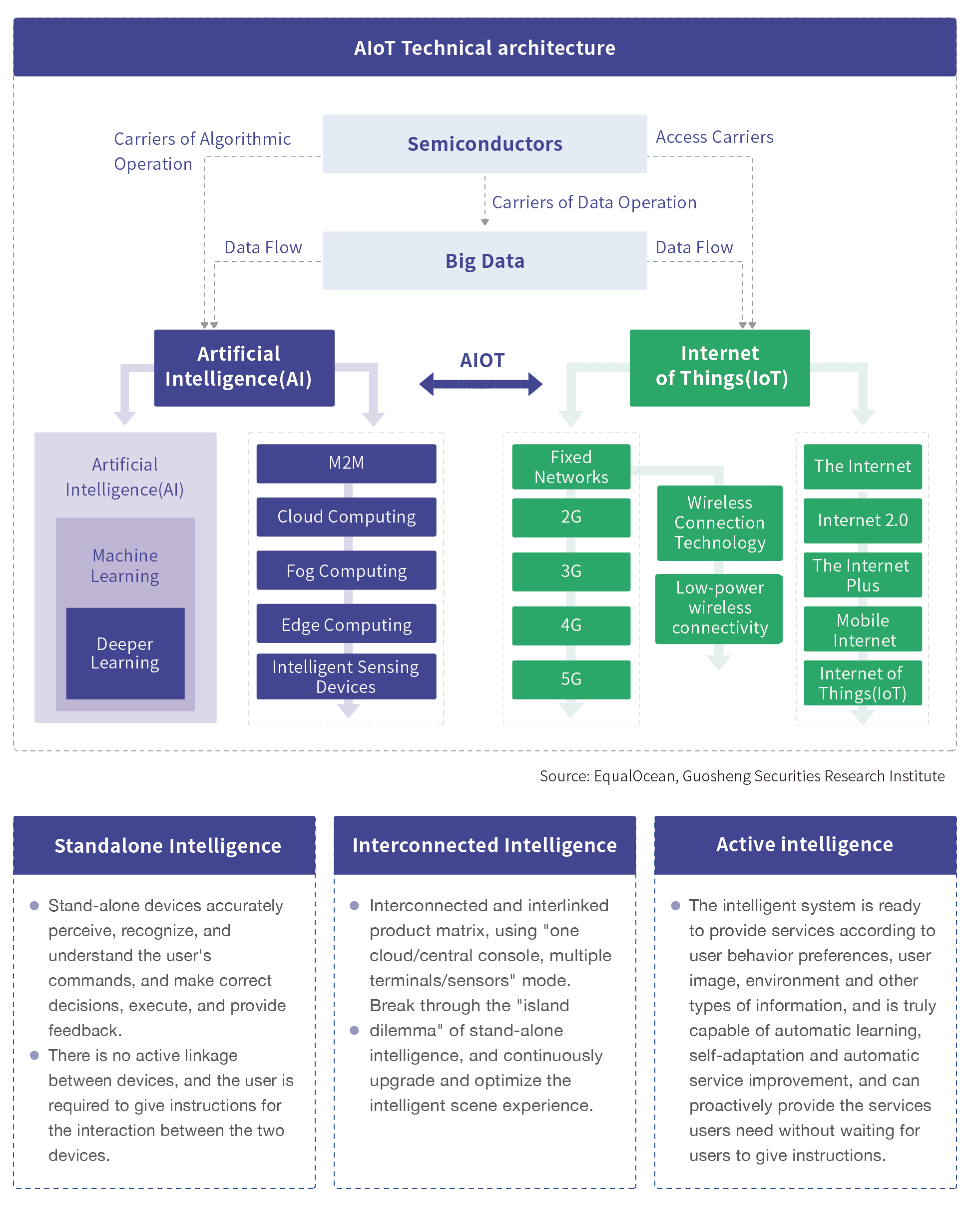

With the iterations of technologies such as AI, big data, and cloud computing, the ultimate development objective of IoT is "All Things Connected." AI technologies are used to analyze and process data collected by smart terminals to improve user experience and product intelligence, which ultimately leads to a shift in our lifestyle.

Figure 3: AIoT Technology Architecture

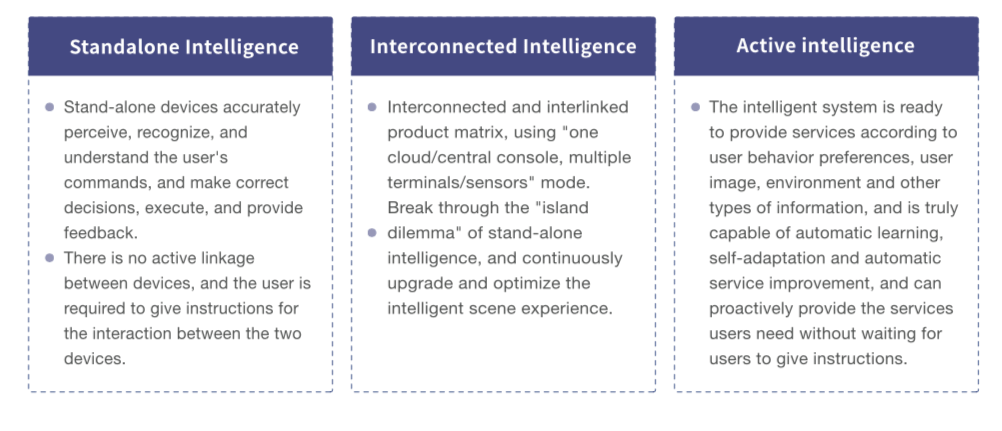

Wu Hequan, an Academician of the Chinese Academy of Engineering, predicted that for AIoT to become truly intelligent, it will go through three developmental stages: single-device intelligence, interconnected intelligence, and active intelligence. AIoT is evolving from single-device intelligence to interconnected intelligence, while the development of smart terminals is reaching maturity.

Figure 4: Three development stages of AIoT development

1.3 An Analysis on the Macro Environment of the AIoT industry

1.3.1 An Analysis on Policies for the AIoT Industry

Many countries across the world are attaching great importance to the development of the AIoT industry, and continue to introduce relevant policies and establish strategies to gain an upper hand in the international competition of future technologies, especially in developed countries and regions such as the United States, the European Union, Japan and South Korea.

1. China

National strategies: On November 3rd, 2009, Premier Wen Jiabao delivered a speech entitled "Let Science and Technology Lead China's Sustainable Development", in which he stated clearly that the Internet of Things is one of China's strategic emerging industries; in 2010, the Internet of Things was first included in the "Report on the Work of the Government".

Top-level design: During the "12th Five-Year Plan", the government strengthened its efforts in promoting the industry; in early 2013, the "Guidelines of the State Council on Promoting the Orderly and Healthy Development of the Internet of Things" was formally released, which laid out the overall strategy of the Internet of Things and clarified developmental objectives.

Organizational structure: The Inter-ministerial Joint Meeting and Expert Advisory Committee for the Development of the Internet of Things was established to coordinate all relevant departments;

Development plan: "Special Action Plan for the Internet of Things Development (2013-2015)"; "the Development Plan for the Internet of Things (2016-2020)" (to clarify the development goals of our main performance indicators, in the IoT industry by 2020).

Financial support: The central government has arranged dedicated funds for the development of the Internet of Things for 4 consecutive years, and has included the Internet of Things in the list of high-tech industries to be determined and supported. Strategic upgrade: During the "13th Five-Year Plan", the Chinese government emphasized the implementation of the "Cyberpower" strategy, acceleration of the building of “digital China", and promotion of a full integration of technologies such as the IoT, cloud computing and AI into various industries. In 2017, the State Council issued "The New-generation Artificial Intelligence Development Plan", elevated the development of AI into a national strategy. The "2019 State Council Report on the Work of the Government" proposed to "build an industrial Internet platform and expand 'smart+' ", an initiative regarded as the government’s first foray into a new era of all things connected intelligently; In 2020, the country emphasized the development of "new infrastructure", namely, cloud computing and artificial intelligence, blockchain, 5G, Internet of Things, industrial Internet and other technologies, as well as the integration of these technologies, empowering traditional industries to make smart upgrades.

2. United States

National Strategies: In 2009, the Obama administration proposed their key strategy to revitalize the economy and establish the US's global competitive advantage, namely the US Internet of Things strategy. And the American Recovery and Reinvestment Act (787 billion USD in total) proposed to focus on industries including energy, technology, education and health in terms of developing and applying IoT technologies through increased government investment.

Organizational structure/financial support: In 2015, the US government announced that it would invest $160 million to promote the Smart City Initiative; the US Department of Energy established the "Smart Manufacturing Innovation" organization and invested $70 million to promote the R&D of advanced sensors, controllers, platforms and manufacturing modeling technologies.

Strategic upgrade: In February 2019, US President Trump signed Executive Order No. 13859 to launch the new US artificial intelligence plan, as a national strategy to enhance the US AI leadership; at the end of February 2020, the White House Office of Science and Technology Policy released the "American Artificial Intelligence Initiative: Year One Annual Report", which outlined the progress of AI development in the United States and emphasized six key policies and practices.

3. The European Union

Strategies: In June 2009, the European Commission submitted the world’s first IoT development strategic plan, titled "Internet of Things - an Action Plan for Europe", in which the Commission proposed 14 IoT action plans.

Organizational structure/financial support: In 2015, the Alliance for the Internet of Things Innovation (AIoTI), an organization that bridges the EU and the industry circle, was established with an investment of 50 million euros; in 2016, the Internet of Things - European Platform Initiative (IoT-EPI) was established with the purpose of building a sustainable European IoT ecosystem; through the "Horizon 2020" R&D program, nearly 200 million euros will be invested in the IoT to build an IoT platform that connects smart devices, which promotes IoT integration and platform research and innovation. The R&D program focuses on five smart applications that will be carried out on a large scale: connected cars, smart cities, smart wearable devices, smart agriculture and food safety, and smart elderly care.

Strategic upgrade: In April 2018, the European Commission issued a policy document "Artificial Intelligence for Europe", which proposed the EU way of artificial intelligence; in February 2020, the European Commission issued the "White Paper on Artificial Intelligence", emphasizing that the European AI strategy aims to improve innovation capabilities in the field, while simultaneously promoting the application of ethical and trustworthy AI technologies in the European economy.

4. Japan and South Korea

In August 2016, the South Korean government identified nine national strategic projects (AI, autonomous driving, smart cities, virtual reality, etc.) as new engines for new economic growth and improving the quality of their citizens' lives. The Ministry of Science, ICT and Future Planning of South Korea will invest over 2 trillion won to promote these nine projects, while South Korean carriers are actively deploying dedicated networks for the Internet of Things. In January 2019, the Ministry of Science and ICT of South Korea formulated and released the "Economic Activation Plan Based on Data and Artificial Intelligence" to promote the integration of data and artificial intelligence.

In 2004, the Ministry of Internal Affairs and Communications (MIC), the authority of Japan's information and communications industry, proposed the "U-Japan" strategy. Subsequently, Japan began to promote the application of the Internet of Things in power grids, remote monitoring, smart homes, and Internet of Vehicles; In July 2009, the Japanese IT Strategy Headquarters proposed "I-Japan Strategy 2015", setting the goals to achieve a citizen-centered digital security and a society of vitality, and to strengthen the application of the IoT in the fields of transportation, medical care, education, and environmental monitoring. In January 2016, the Japanese Cabinet proposed “Super Intelligent Society 5.0”, aiming to make lives more convenient through technologies such as the IoT, robotics, AI, and big data. In June 2018, the Japanese government proposed a new artificial intelligence strategy, "Integrated Innovation Strategy", and established the Promotion Committee of Integrated Innovation Strategy.

1.3.2 An Analysis of the Economic Environment of the AIoT Industry

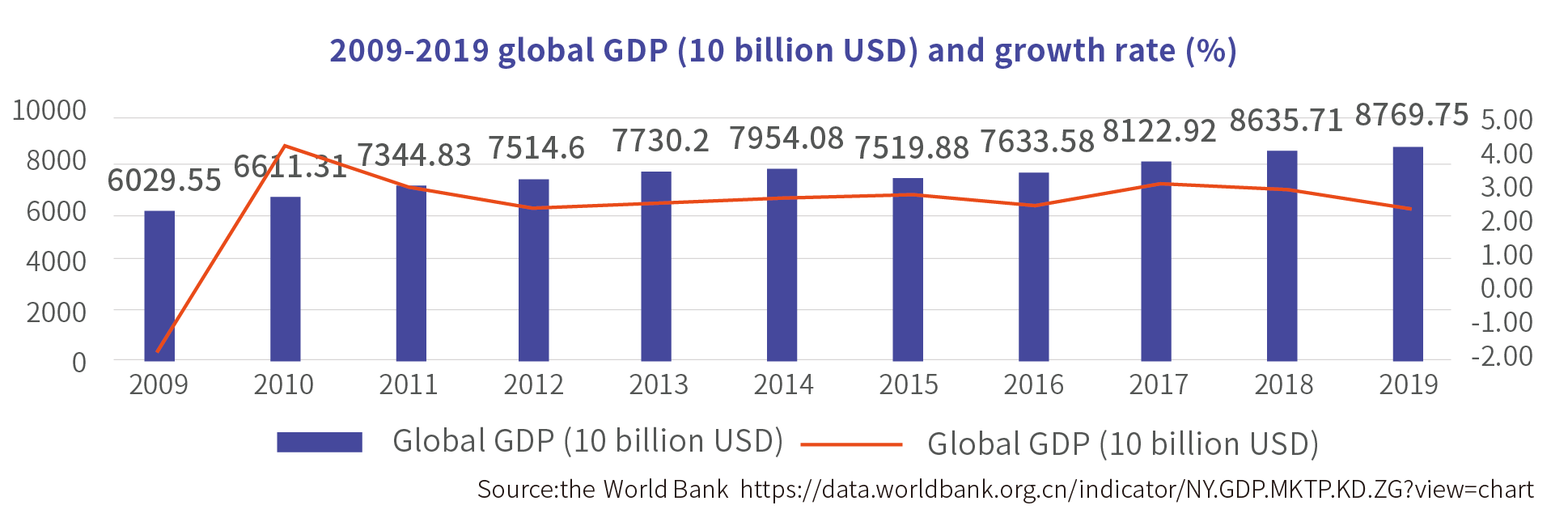

The global economy has slowed down (the growth rate of global GDP has decreased), and it is expected that 2020 will see a slower economic growth due to the impact of global trade disputes and the Covid-19 pandemic. Meanwhile, international competition has intensified, and countries are increasingly vying to become a technological power. Therefore, they have paid more attention to the development of emerging technologies such as artificial intelligence, cloud computing, communications, and the Internet of Things. Due to the overall macroeconomic environment, the investment environment for AI and IoT has gradually become more rational, and the commercialization of AIoT-related fields has become the key to future strategies.

Figure 5: 2009-2019 global GDP (10 billion USD) and growth rate (%)

1.3.3 An Analysis of the Social Environment of the AIoT industry

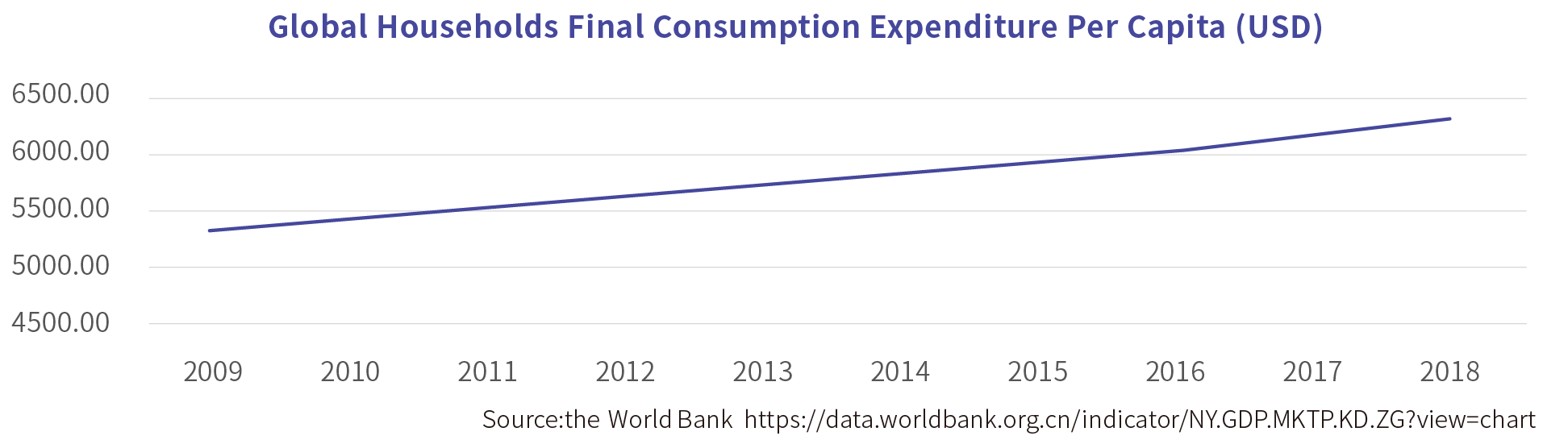

Mass consumers: Globally, the per capita consumption continues to rise. Consumption upgrades have brought about changes in consumption mindsets. In addition, smart terminal products, the most representatives of which are smart speakers and smart watches, continue to enjoy more and more variety, while their fast iterations also offer new functions. As a result, people are more willing to purchase smart products that could improve their lives.

Figure 6: 2010-2018 Global Households Final Consumption Expenditure Per Capita (USD)

Business environment: Digitalization has penetrated industries. Traditional industries, most notable representatives of which are manufacturing, medical care, and energy, are facing digital transformation. The application of the intelligent IoT is one important way to complete digital transformation. Driven by industrial applications, the business models surrounding the AIoT industry are constantly being innovated, developed and optimized. Services such as shared bicycles and telemedicine are all innovative business models based on the development of the Internet of Things.

1.3.4 An Analysis of the Technologies in the AIoT Industry

(1) Sensing technologies: In the AIoT industry, sensing technologies are the entry to data collection, and sensors are the underlying components that perceive various information and data related to the objects, their status, and the environment. Sensors are gradually moving away from their traditional forms and becoming smart. They are now able to detect the external information, perform self-diagnose, process data and adapt to different situations. Currently, MEMS1 (Microelectro Mechanical Systems) sensors have become a new development trend. Due to integrated communications, CPU, batteries, etc., and a variety of sensors, MEMS sensors are small, lightweight, inexpensive, and easy to be integrated. They make the terminals smarter.

As sensing technologies develop, the average price of sensors continues to fall globally, and the cost of network deployment of smart devices has been greatly reduced, which supports the development of the AIoT industry from the infrastructure level.

Figure 7: 2010-2018 Global Average Unit Price of Sensors

(2) Semiconductor chips: At this stage, AIoT devices still need smart phones or Wi-Fi to be connected to the network. In order to improve the flexibility and portability of AIoT terminals, it is necessary to ensure that the built-in batteries of AIoT smart terminals are small, lightweight and have a long battery life. Therefore, the built-in device processor (semiconductor chip) is getting more energy-efficient and high-performing. MCU2 and SoC3, which enjoy notable advantages in performance, cost, low power, reliability, and scope of application, have matured and become an important technical support for the AIoT industry.

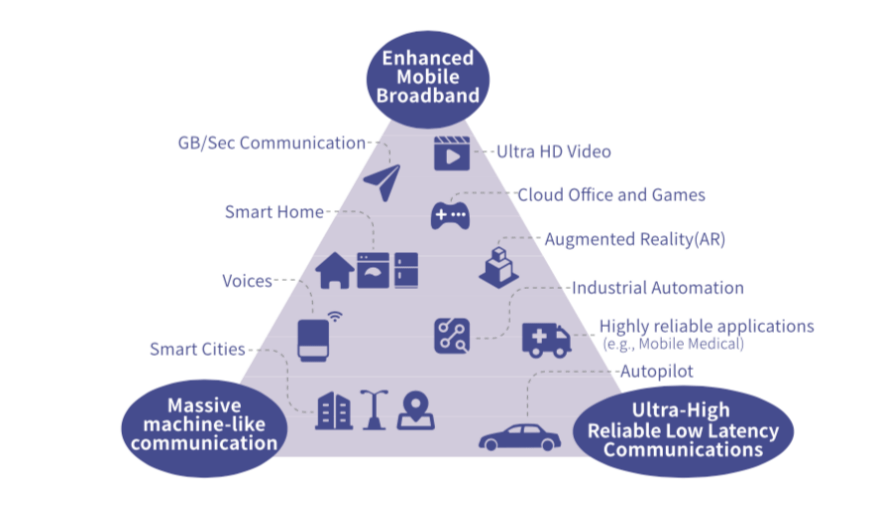

(3) Network and communication technology: In the era of "All Things Connected", connected devices continue to increase. In order to simultaneously connect an enormous number of devices and reduce latency, the iterative evolution of network and communication technologies are essential. Therefore, in order to support the development of the AIoT industry, the performances of network and communication technologies in terms of transmission rate, bandwidth, connection capacity, low power, delay, etc. have been greatly improved, including 5G, Wi-Fi6, IPv64, Zigbee5, LPWAN6 (NB-IoT7, LoRa8), among other network and communication technologies widely used in the AIoT industry.

Massive machine-type-communications (mMTC) in the three major commercial scenarios of 5G technology include narrowband Internet of Things (NB-IoT) and enhanced machine type communication (eMTC), which can be adapted to large-scale IoT applications.

Figure 8: Three Commercial Scenarios of 5G

Image source: ITU

LPWAN (Low-Power Wide-Area Network): It is suitable for IoT terminals. It has low broadband, low power consumption, long range, and large connection. It will cover 60% of IoT devices in the future.

Compared with Wi-Fi5, Wi-Fi6 has been comprehensively improved in terms of performance. The total bandwidth has been increased from 2.4Gbps to 9.6Gbps, the number of connected devices from 5-10 to 50, and the network delay reduced from 30ms to 20ms. All of these improvements enable communication with terminal equipment while reducing power consumption.

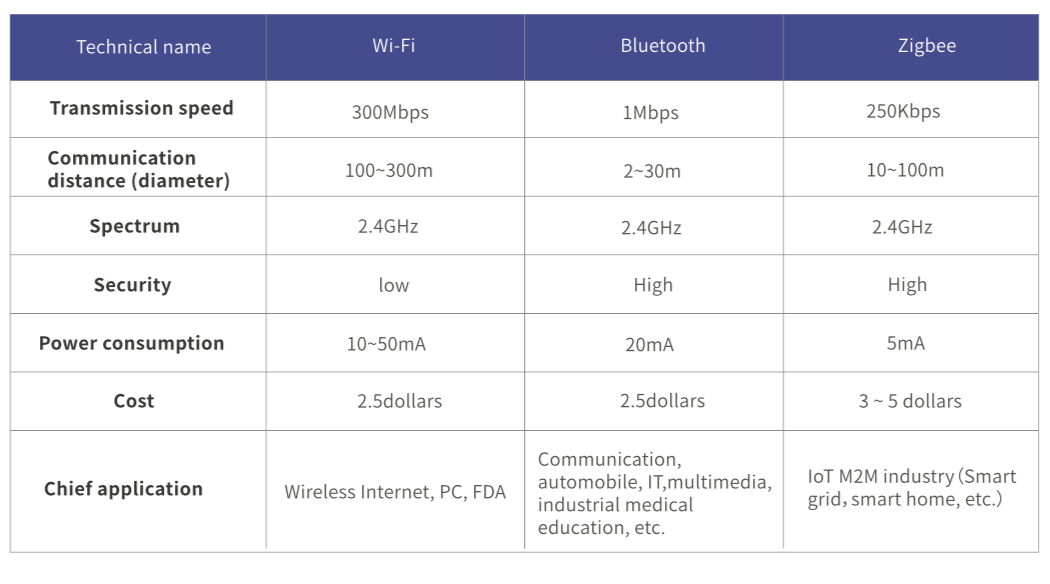

Bluetooth technology is an open global standard for wireless data and voice communication. It is a radio technology that supports short-distance communication between devices, enabling short-distance data exchange among fixed devices, mobile devices (mobile phones, PDAs, wireless headsets, laptops, etc.) and personal LANs within buildings. Bluetooth connects multiple devices and offers the solution to data synchronization. Its advantages include applicability among multiple devices, national working frequency bands and strong anti-interference, but it is insufficient in terms of power consumption and safety. BleMesh (Bluetooth Mesh) network is a new network topology of Bluetooth Low Energy (also known as Bluetooth LE) used to establish many-to-many device communication. Its advantages are low module cost, lower packet loss rate and delay during data transmission, directly supported by smart phones, portable networking, and strong anti-interference performance. Currently, BleMesh is getting the attention of the entire industry. It has certain commercialization potential in smart lighting control systems, and could also be promoted and applied to other industries.

Zigbee is a short-range (10-100m), low-bit (250Kbps), low-power, low-cost, two-way wireless communication technology. It can work on three frequency bands: 2.4GHz (globally common), 868MHz (common in Europe) and 915 MHz (common in the US). It is mainly used for data transmission among various electronic devices with short range, low power consumption and low transmission rate, and can be embedded in various devices. The advantages of Zigbee include: low power consumption, low cost, large network capacity, reliability, security, and great scalability. However, Zigbee mainly uses the 2.5G frequency in the ISM frequency band, and has weak diffraction and insufficient wall penetration in the home environment, greatly affecting the signal.

Figure 9: Comparison of Wi-Fi, Bluetooth and Zigbee: Three Wireless Communication Technologies

A comparative analysis shows that Wi-Fi is currently the most widely used wireless communication technology with the highest transmission rate; Zigbee's advantages are ad hoc network and low power consumption, and Bluetooth's advantage is easy networking.

(4) Cloud computing and AI: In recent years, artificial intelligence has fully entered the era of machine learning. With the support of data mining, cloud services, data analysis and other technologies, AI now has access to massive pools of data for learning, and AI technologies and their core algorithms are constantly being upgraded and iterated. Core AI technologies, most notably, computer vision technology, natural language processing technology, and intelligent adaptive learning technology, have achieved great breakthroughs. Due to the fact that the technologies are becoming more and more mature, AI technology has gradually entered the commercialization stage, integrating with traditional industries to improve the production efficiency.

More connected devices will inevitably lead to a surge in data volume, so there will be a higher demand for data storage and data processing technology. The development of cloud computing and big data technology also provides support to the AIoT industry. Currently, more mature cloud computing technologies include hybrid cloud technology (for horizontal modular expansion), hyper-convergence technology (to solve the problem of storage device capacity, performance and computing power mismatch) and edge computing technology (to solve issues related to central capacity, network delay, transmission energy consumption, privacy protection, etc.).

The development of AI and IoT technologies are complementary to each other. AI technologies advance from learning big data, and the smart connection of the IoT requires intelligent analysis from AI. Therefore, developing these technologies in synergy helps the AIoT industry to grow.

Notes:

[1] MEMS: stands for Micro-Electro Mechanical Systems, which refers to micro components or systems that can be produced in batches, and serve to integrate micro mechanisms, micro sensors, micro actuators, signal processing and control circuits, even interfaces, communication modules, and power modules into one or multiple chips.

[2] MCU: Microcontroller Unit, also known as Single-Chip Microcomputer or single-chip unit, serves to moderately reduce the frequency and performance of the central processing unit (CPU), and to integrate memory, Timer, USB, A/D conversion, UART, PLC, DMA and other peripheral interfaces, and even LCD drive circuit into a single chip to form a chip-level computer, providing various control combinations for different applications.

[3] SoC: System-level chip, or System on a Chip. Academia in China and abroad generally tend to define SoC as an integration of microprocessor, analog IP core, digital IP core and memory (or off-chip storage control interface) on a single chip. It is usually custom-made or a standard product for specific purposes.

[4] IPv6: Internet Protocol Version 6, is the next generation IP protocol designed by the Internet Engineering Task Force (IETF) to replace IPv4.

[5] Zigbee: It is a wireless network protocol for low-bit and short-distance transmission. It is low-bit, low-power, inexpensive; supports a large number of network nodes and multiple network topologies; and it is also incomplex, fast, reliable and secure.

[6] LPWAN: Low-Power Wide-Area Network, also known as LPWA or LPN, is a wireless network used in the Internet of Things, enabling communication over long distances at low transmission rates.

[7] NB-IoT: Narrow Band-Internet of Things. It is a new narrowband cellular communication LPWAN technology proposed by the 3GPP, a group of standard organizations, in September 2015. Its core application is low-end IoT terminals (low current consumption), suitable for broad deployment in smart homes, smart cities, smart production, etc.

[8] LoRa: Long Range Radio is a low-power wide-area network protocol developed by Semtech. Under the same power consumption, it has 3-5 times the frequency communication distance of the traditional radio, achieving low power consumption and long distance simultaneously.

1.4 Analysis of the global AIoT market

AIoT market has been expanding due to the powerful convergence of artificial intelligence(AI) technologies and IoT applications. According to recent reports, the global IoT market size was $686 billion in 2019 and will exceed $1 trillion by 2022. In the meantime, data transmitted via IoT has reached 14 ZB in 2019 and will reach 80 ZB by 2025. As IoT, 5G, big data, and other technologies develop, the penetration of AI in IoT market will rapidly grow in the next few years. Global Smart Business estimates that the global AIoT market size was about $226 billion in 2019 and will grow to $482 billion by 2022, with a compound annual growth rate of around 28.6%.

(1) China

Since many IoT companies and manufacturers (with a low AI adoption rate) are relatively young, China’s AIoT market only took up a small share in the overall IoT market in 2019 compared with other regions, but it also means opportunities for future development. Global Smart Business estimates that China's AIoT market size in 2019 was about USD 55 billion, and thanks to recent policies on new infrastructure, it will reach USD 128 billion in 2022, with a compound annual growth rate of about 33%. The growth rate will surpass the United States, the European Union, Japan, South Korea, and other regions, making China one of the world's most potential AIoT markets.

(2) the United States

As the world's largest AIoT market, the United States will remain on top for the next three years. Global Smart Business estimates that the US AIoT market size in 2019 was approximately USD 68 billion, and will reach USD 136 billion by 2020 with a stead annual growth rate of 26%.

(3) the European Union

Similar to the United States, the EU has a higher AI adoption rate. Therefore, despite its IoT market size was smaller than China in 2019, its AIoT market size was almost as big as China’s and was about USD 55 billion. According to the forecast of Global Smart Business, the EU’s AIoT market size will reach USD 120 billion in 2022, with a compound annual growth rate of about 30% and the potential to become a more mature and stable AIoT market.

(4) Japan and South Korea

Japan and South Korea started early on the combination of AI and the IoT, so their technologies are relatively mature. The AIoT market size in 2019 was about USD 34 billion. However, since they have experienced a rapid growth at the early stage, the growth of the AIoT market in Japan and South Korea in the next three years will slow down, and the market size is expected to reach USD 64 billion in 2022, with a compound annual growth rate of about 24%, which is relatively lower compared to the US market.

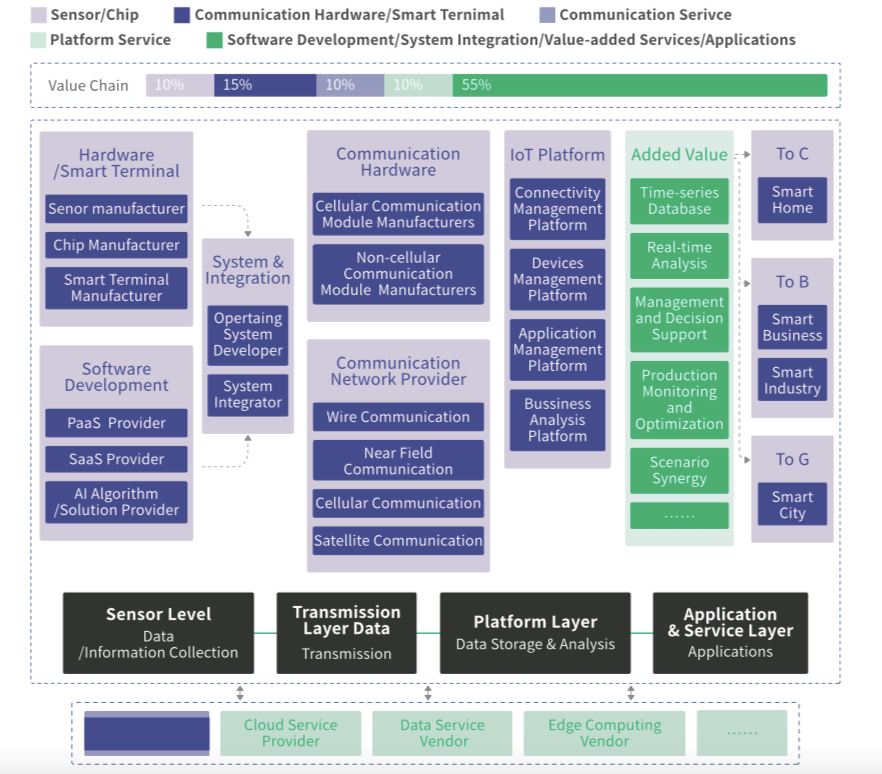

1.5 The introduction and analysis of the AIoT value chain

The AIoT value chain can be divided into four levels: sensor layer, transmission layer, platform layer, application and service layer. Sensor layer is to collect data and information, it includes basic components like sensors and chips, smart terminals, operating systems and software adapted to IoT smart terminals, and AI algorithms/solutions that support and analyze terminal devices, and the key player here is product/solution providers, such as iFlyteck; transmission layer is to transmit data from sensor layer, it includes communications hardware and connectivity networks, and the key player here is service providers, such as China Mobile and Orange; platform layer is to store and analyze data and the key player here is IoT platform providers such as Tuya Smart; application and service layer is to provide applications and services, with added values from AI technologies, for downstream companies, and the key players here include Baiseniao, Schneider Electric, Siemens, etc.

In conclusion, AIoT is the extension of IoT with more emphasis on AI chips, AI solution providers, and AI open platforms. Therefore, software development/system integration/value-added AI services have become an important part of the AIoT market. According to Ericsson, hardware/smart terminals (chips, sensors, modules, smart terminals) account for 25% of AIoT value chain, communication services account for 10%, platform services account for 10%, and software development/system integration/value-added services/applications account for 55%.

Figure 10: AIoT industry chain and value distribution

1.6 AIoT investment and financing status and investment trends

IoT, AI and AIoT all have received a lot of attention of capital market in recent years. From 2016 to 2017, many startups just established but investment institutions were optimistic about AIoT’s future and invested a lot in early-stage and mid-stage projects; since 2019, capital market has cooled down and as good projects and enterprises stand out, the amount of a single investment increases, but the number of investments decreases.

Venture Scanner’s statistics show that IoT startups raised a great number of funds from 2016 to 2017, but the amount of each fund wasn’t big so the total capital was relatively small; in 2018, the number of funds fell dramatically but the amount of each fund increased, so the total capital was large; in the first 6 months of 2020, the investment market has been cautious and the amount of one single fund has only increased slightly, so it is estimated the total financing amount will surpass that in 2019 by merely a little.

Number of financing events for startups in global IoT, 2016~2019 H1 and Total Amount of Financing for Startups in Global IoT (in USD million), 2016~2019H1

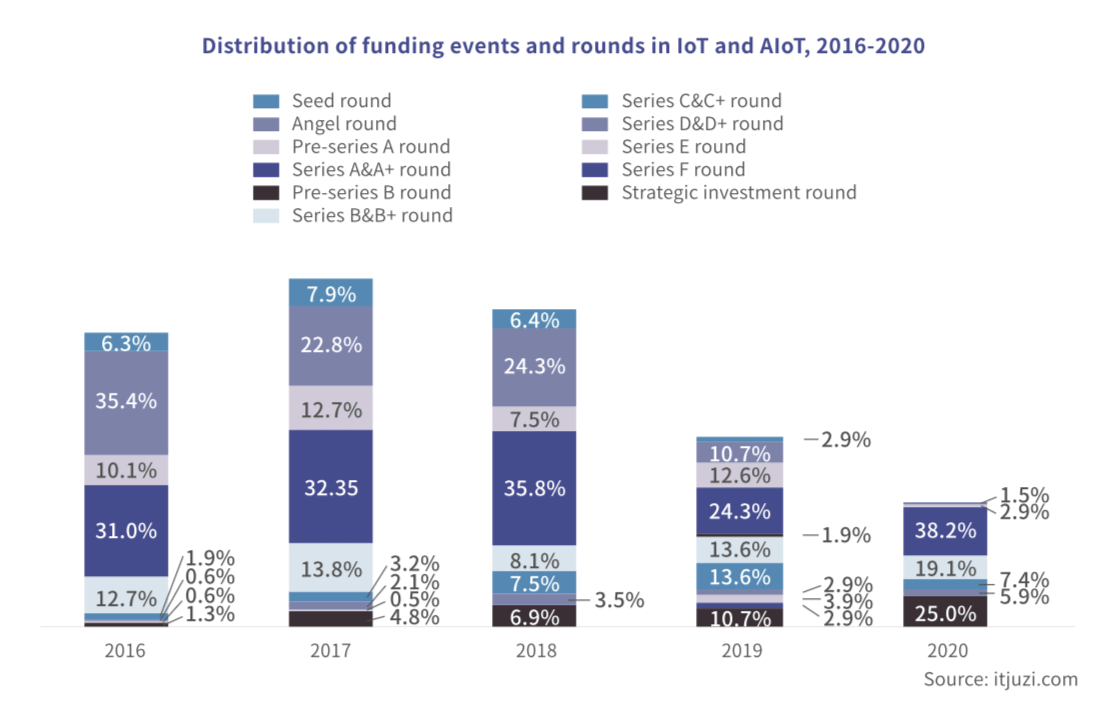

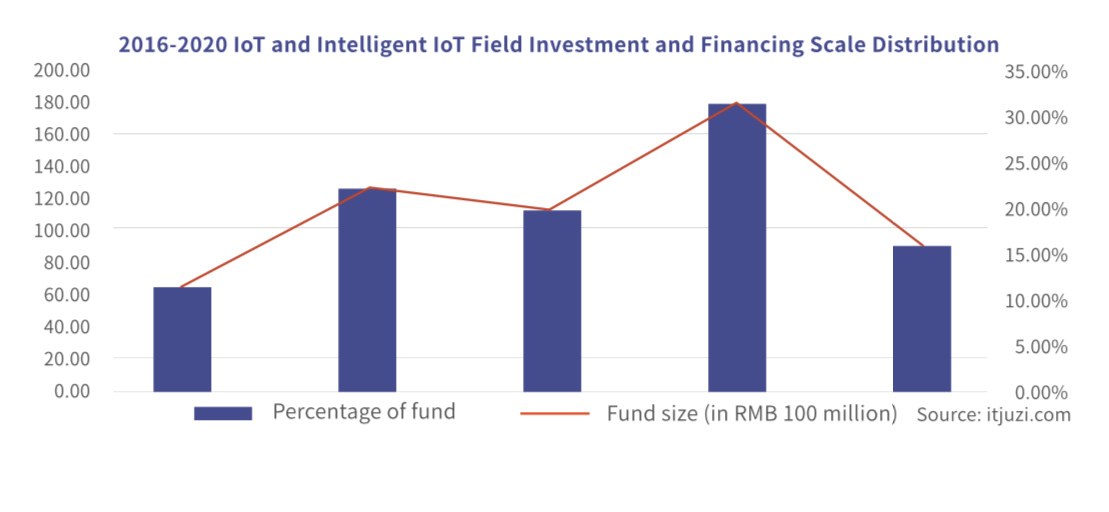

Based on the investing and financing activities recorded by itjuzi.com in the past 5 years (from 2016 to October 2020), the capital market has paid more attention to projects in a relatively early stage in this field with the most investments being Series A & Series A+ fundings every year. From 2016 to 2018, the capital market was enthusiastic: not only the number of investing activities accounted for a relatively high proportion, but also investors were willing to invest in projects in the very early stage. The number of projects in angel rounds was 35.4%, 22.8% and 24.3% respectively from 2016 to 2018, which indicates the confidence the capital market had for IoT and AIoT. From 2019 to 2020, quality companies have stood out, and internet giants have entered the competition, and therefore the capital market has cooled off.

In terms of deal size, fundings in 2019 were the largest and single deal reached the highest level. Due to the pandemic this year, the capital market has grown tighter in general and it has also affected the investment and financing in IoT to a certain extent.

Figure 11: Distribution of funding events and rounds in IoT and AIoT, 2016-2020 and Investing and financing size distribution in IoT and AIoT, 2016-2020

(Note: If the investment size is not disclosed, it is not counted; “hundreds of thousands” is counted as 700,000, “millions” as 5,000,000, “tens of millions” as 30,000,000, “hundreds of millions” as 200,000,000; the USD to CNY exchange rate is 6.7, the euro to CNY exchange rate is 7.8, the GBP to CNY exchange rate is 8.6, the JPY to CNY exchange rate used is 0.064, and the INR to CNY exchange rate is 0.090.)

In terms of investment direction, sensors and chips, software development and services, cloud platform and data services are the major investment targets for sensor layer, transmission layer and platform layer respectively in AIoT. Generally speaking, Investors are more interested in investing in companies working in the application of AIoT, especially those who provide solutions or operation services. Smart home, smart industry and smart business (including smart retail, smart logistics, smart community, smart agriculture, smart education, etc.) are relatively popular investment directions.

Figure 12: Breakdown of investing and financing events in IoT and AIoT, 2016-2020

Kevin Wang, a partner at Mount Morning Capital, has been looking at 5G and IoT, smart manufacturing, and enterprise services for long. According to him, the business models and market values of the AIoT companies worth investing will continue to evolve as technologies and enterprises develop. The first stage of the development is networking and digitalization, with the aim to connect devices and digitalize internal business processes; the second stage is using data generated by the action of connecting devices to provide value-added services for operations and to help customers transform from traditional transaction-based enterprises to service-oriented enterprises; the third stage is the connection and integration of value chain components through multi-party collaboration to form a network of multipoint-to-multipoint services. Take Tuya Smart as an example, it provides IoT modules to help home appliance manufacturers and developers to connect devices to the cloud first, enables customers to create value-added services and new business models with operation data generated at the platform next, and finally integrates upstream and downstream resources of the industry chain to helps customers access overseas ecosystem and market resources via a comprehensive developer platform.

Wang also pointed out that the connection of devices is the foundation of AIoT but the market for connectivity is limited, and the value created through the data generated by the connection is worth more attention. AIoT can be applied to many vertical industries, such as industrial engineering, logistics, energy, city management and other industries with huge market potential. Cost savings, efficiency improvement and business model reforms that are driven by AIoT data will create huge value. Investors should focus on how much value AIoT applications and services can create, how much profit AIoT technology or services providers can make, and how much money and time is needed.

Wang shared 4 areas that he believes are worth investing in AIoT in the future: value-added AIoT applications based on data, 3D vision and applications, low-cost sensors (MEMS), and IoT security (IoT will be adopted in a large number of active devices, such as automobiles and industrial production equipment, so its security is crucial).

Source: Tuya