A Gartner, Inc. analysis of 796 financial statements revealed that provisions and write-offs of bad debt increased from $9,750 million in 2019 to $12,262 million in 2020 — a 25.8% increase. The standard approach to determining receivables risk underestimates the risk of customer nonpayment because it fails to account for those who can pay but still won’t, according to Gartner, Inc.

“The typical way the finance department assesses receivables risk is to evaluate the financial health of their customers and attempt to identify those who cannot pay,” said Mallory Barg Bulman, director, research in the Gartner Finance practice. “The problem with that approach is that it misses the risk of customers who are financially able to pay but still do not.”

Underestimating the actual nonpayment risk can obscure finance leaders’ view of cash flow and acceptable credit risks, leading to missed investment opportunities, increased bad debt and heightened risk of bankruptcy.

“We’re still seeing heightened concerns from prepandemic levels because there is so much uncertainty about which businesses will survive after government support ends, and the long term impact of the pandemic on consumer behavior is also still largely unknown,” Barg Bulman said.

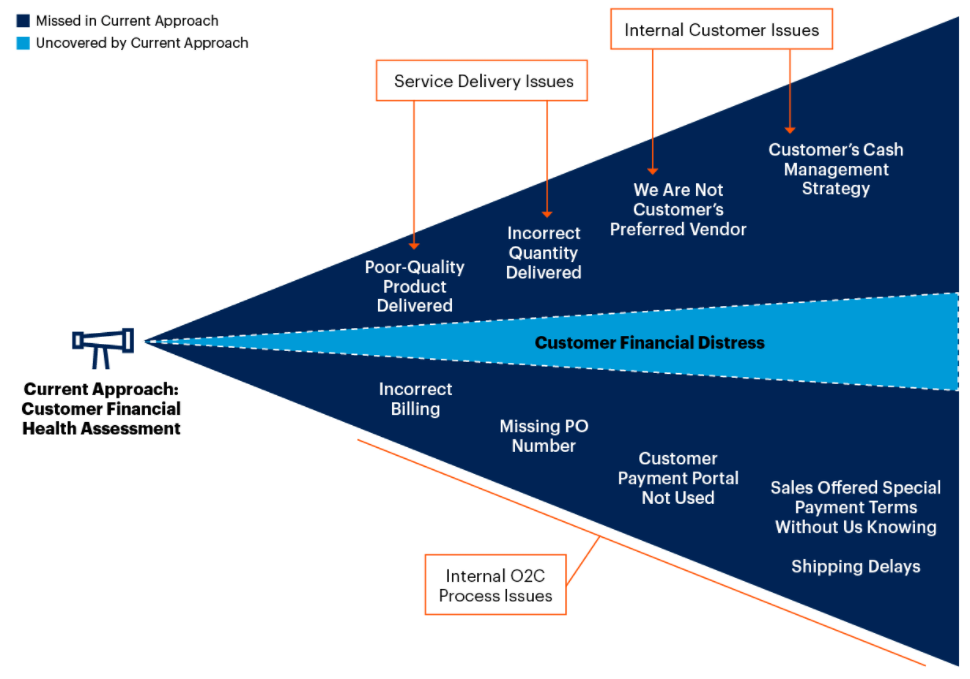

The current approach to assessing receivables risk, looking at a customer’s financial health, fails to spot some of the main reasons for nonpayment (see Figure 1).