By Stan Aronow | January 12, 2024

![[ALT TEXT]](https://emt.gartnerweb.com/ngw/globalassets/en/supply-chain/blog/beyond-supply-chain/images/bsc120124.jpg)

Pause the AI Hype, Let's Talk About the Weather

July 17 2026

By Stan Aronow | January 12, 2024

As we roll into the new year, it’s time to place bets on what 2024 has in store — for the world, more generally, and supply chain, specifically.

Some of this is based on extrapolation of trends or anticipation of key events, but there are always wild cards. In our profession, we need to be persistently tuned into the risks that will disrupt today’s operations and the strategic threats that might cause us to preemptively change our network or operating models.

A good starting point is comparing last year’s predictions to actual events.

Last January, I wrote a blog entry titled Supply Chain 2023: What’s Next? In it, I predicted stabilized supply, lower global inflation and slowing central bank rate increases by the end of 2023. China was just emerging from its Zero-COVID lockdowns and it was viewed that the reopening could power global growth, but also reignite inflation. Chalk me up for one out of two, as China has been in an economic slump since reopening its economy.

On the geopolitical front, I focused attention not on the actions of major powers, but of those straddling the line between East and West. India and Turkey are two examples of countries operating in this middle zone — participating in alliances such as the Quad and NATO, while continuing significant trade with Russia. Expect this dynamic to continue unabated in 2024. Will “neutral shoring” become a viable complement to “friendshoring” for Western companies?

I also pointed to the impact of demographic shifts. Longer term, the governments of more developed economies aren’t having much luck incentivizing young people to have babies, which will ultimately shrink the overall size of the economic pie, in line with declining populations. In 2023, demographic shifts led to my predicted bumper crop of executive retirements in supply chain. It also empowered organized labor to negotiate double-digit raises over the next several years. While the underlying inflation prompting huge raises has diminished, the generational trend driving retirements has not.

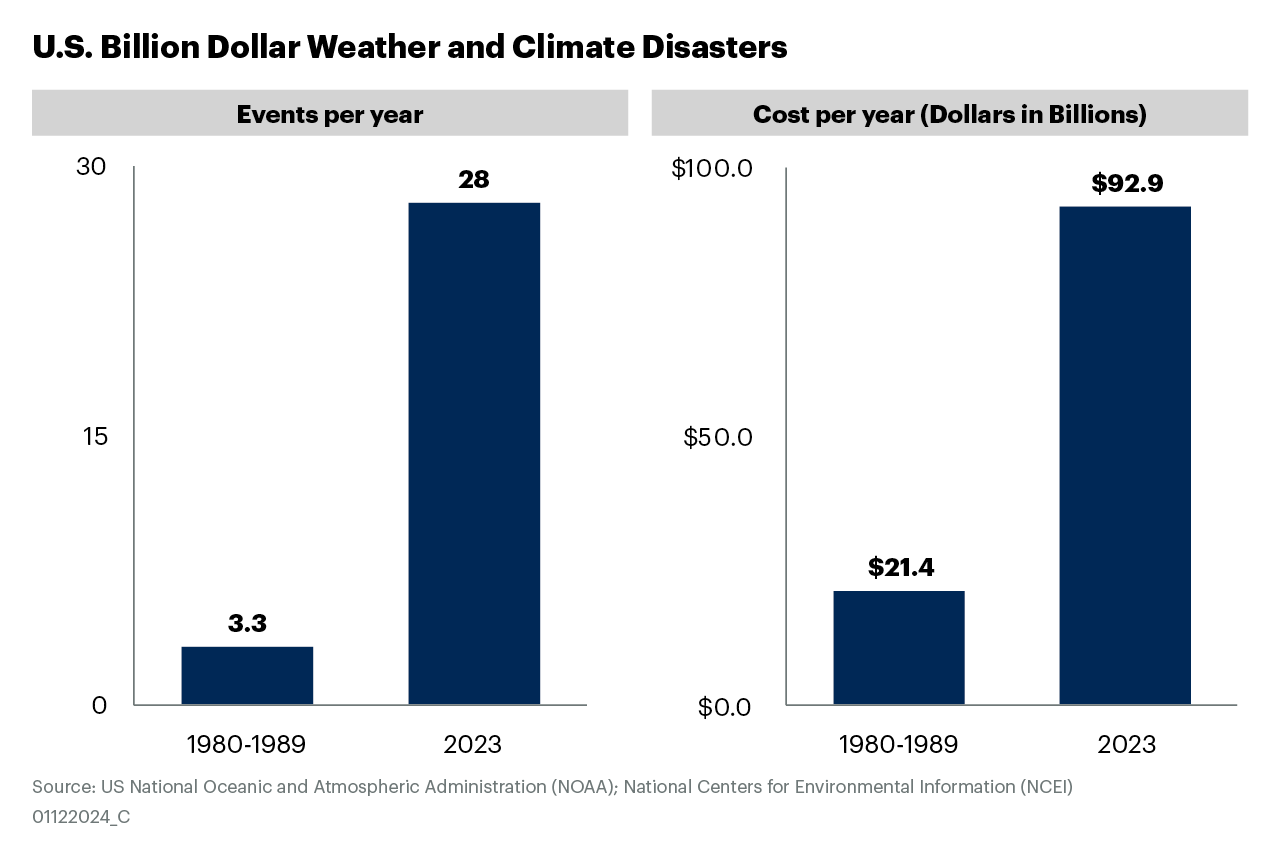

Finally, I noted that ecological trends such as the return of El Niño would require greater climate resilience in 2023. This proved very true and will unfortunately get worse before hopefully improving later this decade. In the United States alone, natural disasters caused a billion-dollar-plus damage event every two weeks, as compared to approximately every four months during the 1980s. Even when figures are adjusted for cost inflation, the total cost of these weather and climate events in 2023 exceeded four times the 1980s average.

The much-ballyhooed prospect of a soft landing (i.e., dampened inflation without an attendant recession) for the U.S. economy in 2024 might excite Fed-watching investors, but the reality for businesses might be 1-ish% growth for the largest global economy. China is the biggest X factor. Given President Xi’s maximalist control over policies aimed more toward ideology than economic stimulus, the main fulcrum is whether the risk of social disruption from dire economic conditions could ever outweigh the headwinds of said social policies and over-leveraged local governments and real estate firms. Lifting Zero-COVID lockdowns was a rare example of people over policy, but I don’t see a repeat in 2024. China is a key trading partner for Europe and the former’s slower growth will weigh on the latter’s prospects for economic uplift.

Countries representing more than half the global population will hold elections this year and U.S. contests hold the biggest wild cards for impacting world events. In this case, the balance of power sits with swing voters in just a half-dozen states. A big open question is whether traditional and social media will place intentional guardrails on the spread of misinformation. Absent governance in the online world, rogue actors located anywhere on the planet can, and will, wreak havoc. On a related note, cyberattacks continued trending upward in 2023. More than 72% of businesses worldwide were affected by ransomware attacks. Distributed denial-of-service attacks on governments and companies were also up significantly. Finally, while few will be happy with the aftermath, some political scientists see cessation of the current level of hostilities in Ukraine by the end of 2024. Unfortunately, the situation will likely worsen before improving.

Gartner’s Hype Cycle for Generative AI, 2023, (subscription required) shows some capabilities just rolling over the “Peak of Inflated Expectations,” though one can only wonder what will happen once ChatGPT 5.0 is (potentially) released before the end of 2024. Another important consideration will be the sheer amount of electricity required to power it. The use cases for GenAI seem larger outside the domain of supply chain, though it is showing some promise in KPI discovery and diagnostics, and improved explainability for traditional AI models. A recent Gartner study shows that nearly 80% of supply chain respondents plan to pilot or implement GenAI capabilities in 2024 using an average of 6% of the overall supply chain technology and transformation budget.

As mentioned above, supply chain leaders will need to continue investing in climate resilience and adaptability to work through natural disasters in 2024. A raft of rules and regulations tied to sustainability and ethical labor practices driven mostly by the European Union, but also the United Kingdom and United States will increase the cost of reporting and potentially the overall cost of running supply chains. 2024 will also be a year that sees more companies recalibrate their positions on ambitious sustainability goals like net-zero emissions as they realize their original commitments were untenable. This will introduce broader reputational risk and it will be important to maintain discipline in driving toward updated targets.

I was struck by a recent Korn Ferry survey showing that CEOs are much gloomier about economic conditions in 2024 than investors and traditional economists. The subtext was that resilient global employment levels driven by talent hoarding might suddenly reverse. Put another way, there is a tug of war between near-term margin pressures and FOMO tied to longer-term skill shortages, driven by demographics and fast-moving technologies. It’s another signal that supply chain leaders should monitor as the year proceeds. Mergers and acquisitions (M&A) represent a separate force that will shake up supply chain organizations in 2024. According to Goldman Sachs, total M&A levels in 2023 were the lowest they’ve been since the early 2010s. Expect a snap back due to lower interest rates and improved financial market health.

In today’s intense environment, it would be easy to feel adrift in a sea of menacing external forces. For most of us, what we experience and manage in our immediate worlds is much safer and more stable. Moreover, we should remember that we are not hapless participants, but powerful co-creators of this global experience. Let’s start with gratitude for our gifts and those around us, grab the wheel and steer toward more collective goodness in 2024.

Stan Aronow

VP Distinguished Advisor

Gartner Supply Chain

Stan.Aronow@gartner.com

Register Now: The 2024 Gartner Power of the Profession Supply Chain Award Winners

Beyond Supply Chain

Subscribe on LinkedIn to receive the biweekly Beyond Supply Chain newsletter.