By Kevin O'Marah | March 29, 2013

Advancing the Mind, Body and Soul of Sentient Operations

August 07 2026

By Kevin O'Marah | March 29, 2013

This week in Durban, South Africa, the fifth annual BRICS summit was held convening leaders from Brazil, Russia, India, China and South Africa to discuss (“dream” may be a more appropriate verb) plans for their role as drivers of the world economy. I have long been bullish on Africa and cautious about China as elements of a global supply chain strategy, but find myself today focused on how badly Brazil is handling its chance to ride this unlikely train of momentum into the future.

Much recent research says that new risks in the global supply chain point to a future based less on distant low-cost-country sourcing and more built around regional manufacturing and supply chain strategies. Rising costs and worries about intellectual property theft are driving some location decisions for new plant or capacity away from China, just as fast-growing consumer markets all around the world have begun to justify investment in local-for-local production.

The implications for Brazil should be all good news: a huge domestic market, loads of cheap green energy, an existing manufacturing base and a time-zone overlap with the United States. Global companies considering a three-theatre supply chain strategy (Americas, EMEA, APAC) might logically look at Brazil first. Unfortunately, its over-eager, activist government cannot seem to get out of the way.

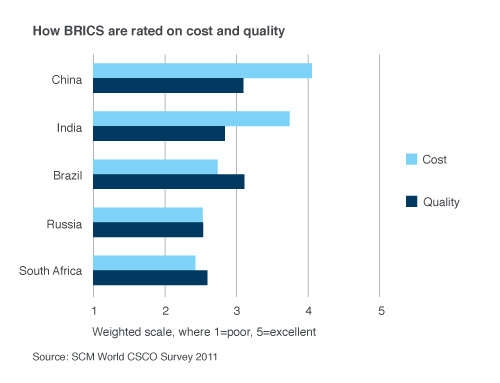

Almost two years ago we gathered opinion data on the BRICS as manufacturing locations, judged by over 700 supply chain professionals. China clearly held the favoured spot, both in terms of cost and quality, but Brazil ranked second overall in quality, barely below the rating achieved by China (see chart below). Brazil’s costs, although not as attractive as China’s or India’s, are hardly out of line and for a strategist looking to supply the US market and diversify sourcing risks, the country might seem a great option.

An analysis of Brazil in the Financial Times this week was headlined “Humbled heavyweight”. It points to a decisive shift by investors away from Brazil in favour of Mexico, despite the fact that Mexico is still plagued by crazy levels of drug violence. The article wants to be bullish on Brazil’s chances to get things straightened out, but ends up weaving a tale of government actions gone wrong. Everything from capital controls meant to weaken the currency to tax cuts meant to help certain selected industries appear to have congealed into a nasty blob of regulatory uncertainty.

Uncertainty is, of course, part of the deal in supply chain with wage inflation, transport cost volatility and exchange rate swings all representing important variables demanding careful analysis and scenario modelling to at least scope the risk. Regulations, taxes, local content rules and other government interventions are, however, fundamentally political variables and thus less susceptible to analysis in the way oil prices are.

Research under way at SCM World into global manufacturing footprints points to a fairly heavy role played by the three Ts – taxes, tariffs and terms. It may be the case that added complexity authored by well-meaning but clumsy governments (state as well as federal governments in Brazil have tariff and taxation powers) inhibits foreign investment. It is certainly fair to say that it is confusing and opaque. According to the World Bank, Brazil ranks 130th in terms of ease of doing business – Mexico is 48th and the US is 4th.

One other factor that is both surprising and worrying is Brazil’s lack of inbound intellectual capital. The front page of the Miami Herald on 26 March featured a story about the country’s recently publicised quest to attract immigrants. In it, the Secretary of Strategic Affairs, Ricardo Paes de Barros, lamented a lack of human capital rooted in the paradoxical fact that Brazil’s population is only 0.3% foreign born compared to 13% for the US. The problem is – you guessed it – complex policies and procedures for getting a work visa.

Global manufacturing networks should include a substantial footprint in Brazil. Supply chain executives have plenty to gain from a regional base that can supply US markets easily while also tapping domestic consumers. Abundant raw materials nearby and very low carbon footprint energy are a real plus in any global resource portfolio. Throw in football’s World Cup next year and the Olympics in 2016 and what’s not to like?

How about the fact that you can’t get your best people in there to work and you’re not sure whether you’ll be able to get you money back out. Maybe Brazil’s politicians shouldn’t try so hard.

Kevin O’Marah

Chief Content Officer

SCM World

Please contact me directly with any comments, questions or suggestions. I welcome your feedback.

Beyond Supply Chain

Subscribe on LinkedIn to receive the biweekly Beyond Supply Chain newsletter.