By Suzie Petrusic | August 26, 2022

Pause the AI Hype, Let's Talk About the Weather

July 17 2026

By Suzie Petrusic | August 26, 2022

In recent conversations with COOs and CSCOs, we are hearing a lot of uncertainty and anxiety on where the economy and their businesses go next.

Amid a volatile global risk environment, record inflation and fiscal policy changes, warnings of a coming recession are at least credible. Inflation is at multidecade highs. And over the short- and long-term, models show unemployment is likely to rise. That said, unemployment is also presently at multidecade lows. And two other reliable indicators of a recession — the credit spread and term spread — signal low risk of a recession in the near future.1

This ambiguous threat of a coming recession in late 2022 or 2023 has some cautious supply chain leaders searching for a strategy. They want to ensure the supply chain is properly prepared to control costs but be ready for a mild, or strong, return of demand, and ready for a continued period of volatility. To do so, supply chain leaders must consider some of the critical differences between the present situation and the periods preceding past recessions.

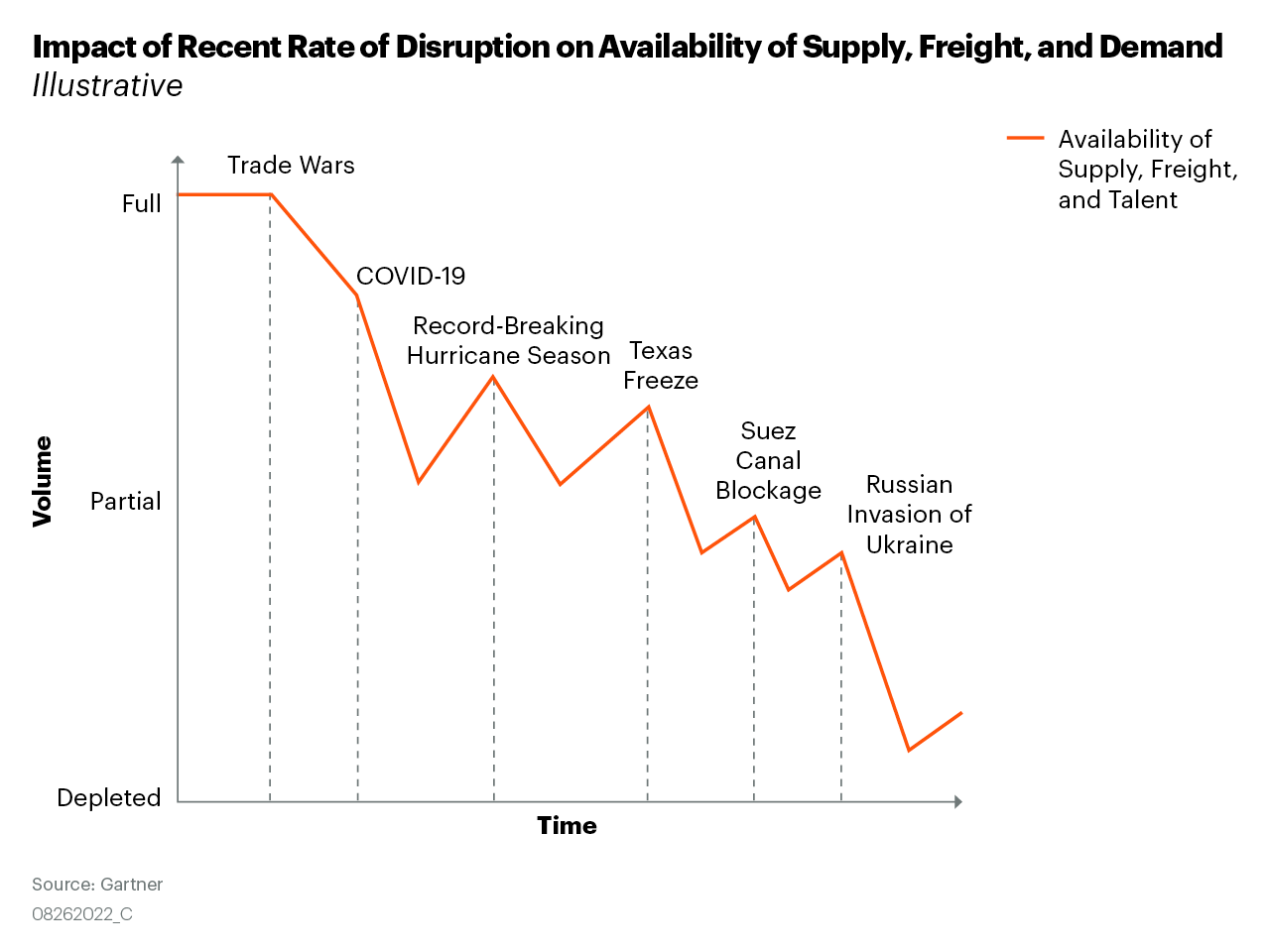

In the extremely volatile environment between 2019 and 2022, the number of risk events disrupting supply chains has been on the rise. The rate and volume of these disruptions have many supply chain leaders concerned about continuity for at least a part of their supply chain.

Some supply chains, with retail being a notable exception, have depleted some of their own critical resources and safety stocks and are facing an upstream supply chain in a very similar situation. At the same time, the labor market is extremely challenging, with more jobs open than people looking for employment in the United States. Lastly, the impact of travel restrictions during the COVID pandemic, shortages of labor and some bad freight actors have created untenable bottlenecks throughout the freight and transport functions globally. All of this adds up to a generalized low level of volume of supply, talent and freight availability in many supply chains today. That is, the state of the supply chain heading into a potential recession in 2022 or 2023 is dramatically and meaningfully different than in the past.

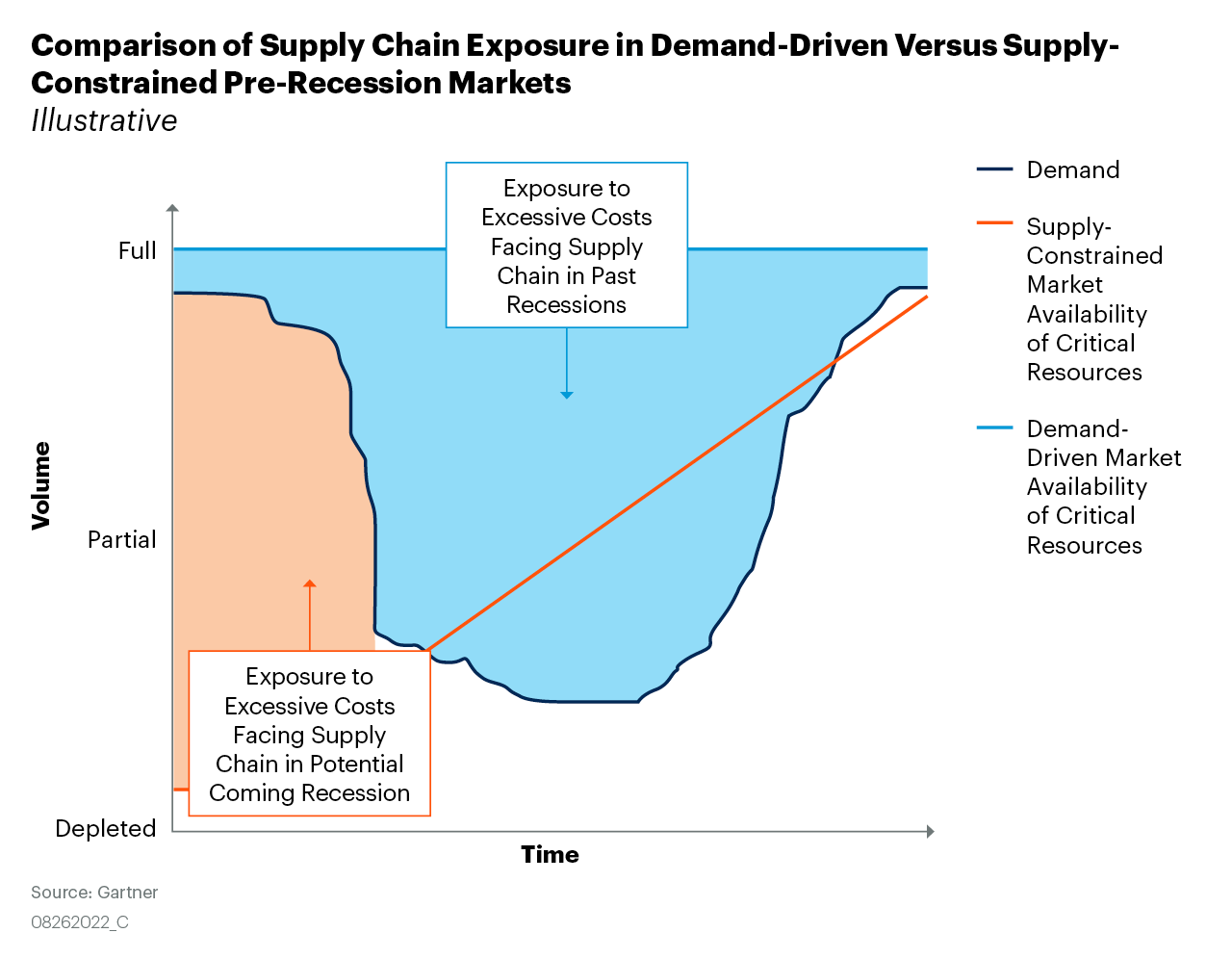

That low level of availability creates another important difference: demand-driven markets preceded previous recessions versus the supply-constrained market dynamic of the present. In the past, CSCOs have entered recessions with levels of inventory and inputs appropriate to meet demand and have consequently faced the threat of holding too much inventory and other costs given a sudden and sustained drop in demand.

By contrast, the market facing most supply chains today is supply-constrained, where often supply cannot meet demand, retail again being a notable exception. A recession now presents an opportunity for the supply chain to once again balance demand and supply and ready their supply chains for continued disruption.

These two critical differences in the supply chain’s reality change the calculation supply chain leaders should make as they prepare for a potential recession in 2022 or 2023. Figure 3 places a U-shaped recession recovery over top of these two different supply chains — one risk-ready in a demand-driven pre-recession market, the other risk-vulnerable in a supply-constrained pre-recession market.

In the case of a recession in 2022 or 2023, many supply chains will continue to find themselves facing the orange rather than the blue — insufficient inventories and inputs and talent to meet demand before it falls. In that case, a sharp decline in demand would assist the supply chain in rebalancing demand and supply. This also creates an opportunity for the supply chain to reset risk readiness.

To set the right course for the supply chain given these two differences, CSCOs should delay changes in strategic direction that rely on a too-early assessment of the duration and depth of the recession and the fulness of its recovery. Instead, supply chain leaders should first:

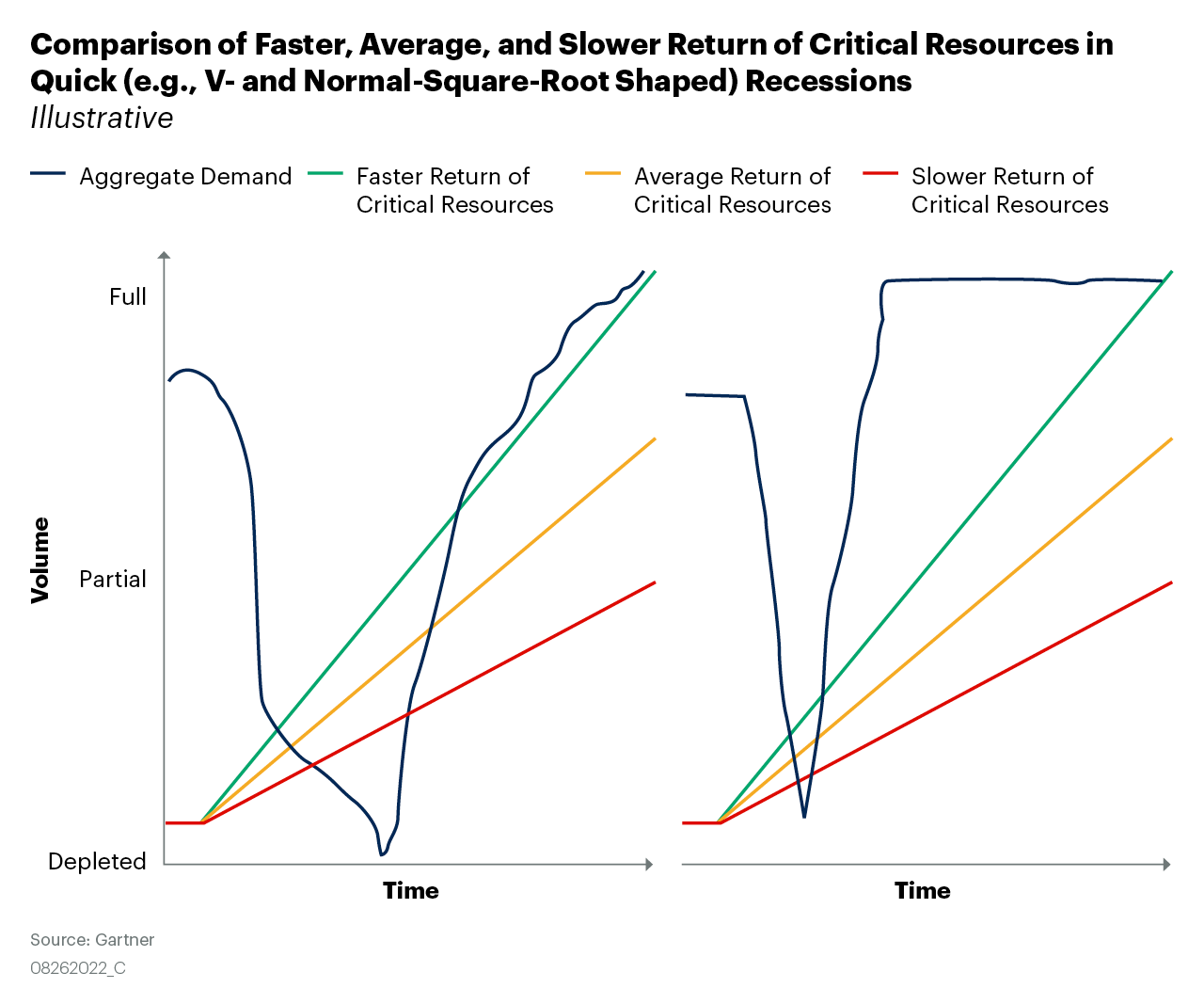

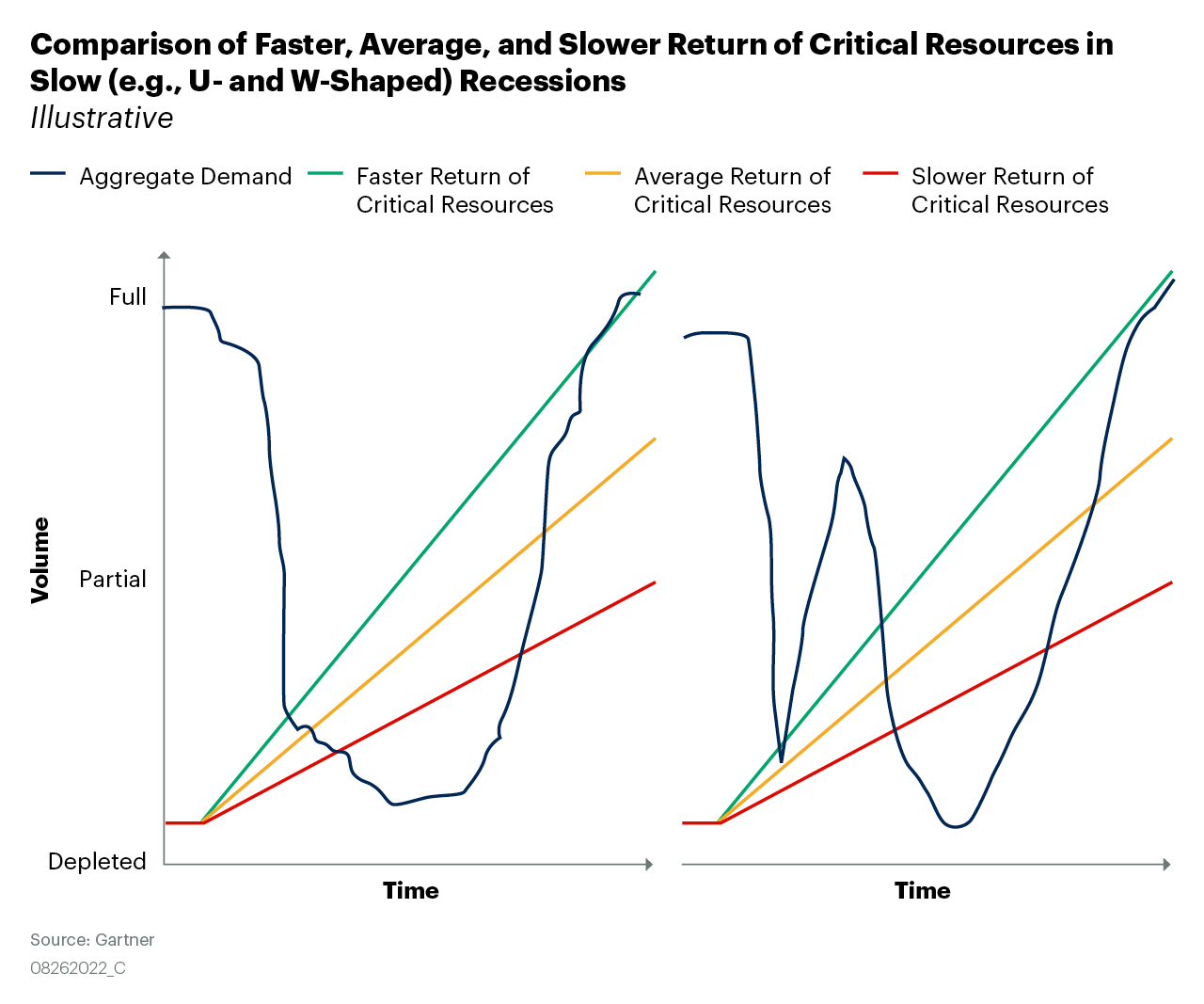

As the graphs show, the most likely scenario is that supply chains will have to shift back and forth between a demand-driven posture and a supply-constrained one. The supply chain should continue to monitor its actual volume in relation to target volume.

The big takeaway is that the coming recession is different from past recessions, and supply chain leaders can take a cool-headed approach to their response. Leverage the drop in demand as an opportunity to rebalance demand with supply, ready the supply chain for continued volatility and base significant shifts in strategy on assessments of both the shape of the recovery and likely rate of recovery for critical resources.

Suzie Petrusic

Director, Research

Gartner Supply Chain

suzie.petrusic@gartner.com

1 https://www.federalreserve.gov/econres/notes/feds-notes/financial-and-macroeconomic-indicators-of-recession-risk-20220621.htm

Listen and subscribe to the Gartner Supply Chain Podcast on Gartner.com, Apple Podcasts, Spotify and Google Podcasts

Beyond Supply Chain

Subscribe on LinkedIn to receive the biweekly Beyond Supply Chain newsletter.