By Kevin O'Marah | January 09, 2015

Pause the AI Hype, Let's Talk About the Weather

July 17 2026

By Kevin O'Marah | January 09, 2015

Volatility in the financial markets has caused a media frenzy this week, but the implications for global supply chains are less significant than many suppose. While oil producers and their supply base are badly affected by a price of $50 per barrel (bbl), transport and energy intensive industries stand to benefit, as will consumers. The resulting picture looks much more like a draw.

Listening to the talking heads on TV can be confusing, with so many pundits offering contradictory arguments about where oil will go next: back over $100/bbl or down further to $30/bbl. Speculators will no doubt pocket some big bucks, guessing right on the frothy sentiments driving this market, but business planning for everyone else should stay the course.

The LA Times reported an interesting factoid attributed to Howard Silverblatt of S&P Dow Jones Indices. It seems energy stocks currently make up 8.9% of the total market value of the S&P 500. Back in 1980 the corresponding figure was 28.8%. Oil was pretty much king in the 20th century, but today not so much.

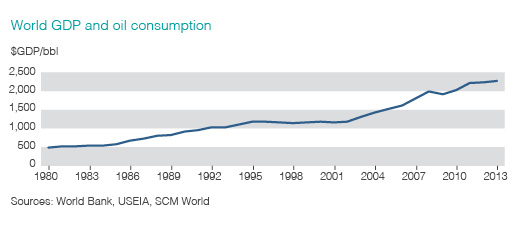

Oil demand lags economic growth

Using 1980 as a reference point, I collected data from the World Bank and the US Energy Information Administration to see how much things have changed in the past 35 years. Using constant dollars, the data shows a nearly fivefold increase in output per barrel of oil consumed.

This dematerialisation of the global supply chain is decoupling economic growth from energy consumption. This is the key for supply chain strategies meant to deliver information value, not just material value. Apple, for instance, books $2,200 revenue per kilo of product it delivers. Compare this to about eight cents per kilo for iron ore and the direction is clear.

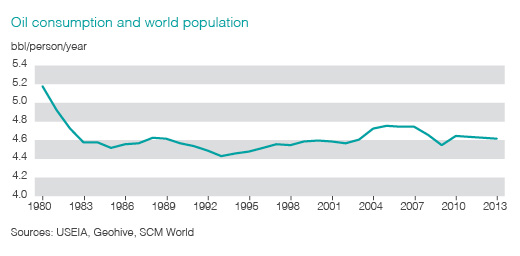

I also took a look at population trends against oil consumption and found another reason to relax. Starting in 1980 with a consumption of 5.2 barrels of oil per person per year, we see a dramatic drop of nearly 13% by 1985, followed by a fairly steady run of around 4.6 barrels per person per year continuing to the present day.

The jump in world population during this time took us from 4.4 billion to 7.2 billion people, with nearly all of this growth originating in developing markets. Worries that bringing China, India and the rest of the developing world up to western living standards will destroy the planet may be overstating the case, since it seems that growth in emerging markets is not necessarily “dirtier” than in Europe or North America.

These two megatrends point happily to a future that is cleaner, more inclusive and more sustainable than many had feared. For supply chain leaders the takeaway is simply that oil matters less today than yesterday and will matter even less in years to come.

Stay the course, but look ahead

What about volatility? Most supply chain executives hate volatility, and swings like those we’ve seen in oil should surely cause some heartburn. In fact, our Chief Supply Chain Officer Survey data finds that commodity price volatility is the third highest ranking supply chain risk among the 15 considered. Further, certain industries have significantly greater exposure than others, with metals, food & beverage, agriculture & mining and CPG most exposed.

Unfortunately, the financial manipulators fostering volatility in oil are generally leaving operators in the real world without much protection. Commodity price hedging with financial instruments is among the least successful tactics in use today to deal with volatility.

Of the eight sectors most directly impacted by price volatility in oil and other commodities, all see a big gap between success with price hedging and their level of concern over this risk. In comparison to other risk mitigation strategies such as dual sourcing or inventory buffering, hedging is the clear underperformer.

The conclusion for most supply chain strategists is that oil’s behaviour, while hugely unpredictable, weighs less than other factors on decisions about sourcing locations, network designs and inventory. Proximity to customers and markets, value-added service from key suppliers and postponement tactics are likely to pay off now and even more richly in the future.

Beyond Supply Chain

Subscribe on LinkedIn to receive the biweekly Beyond Supply Chain newsletter.