By Wade McDaniel | October 20, 2023

Advancing the Mind, Body and Soul of Sentient Operations

August 07 2026

By Wade McDaniel | October 20, 2023

In June, we asked the Gartner Chief Supply Chain Officer (CSCO) community about its level of optimism for the remainder of 2023. I was surprised to learn that more than 85% of worldwide respondents said they felt optimistic overall. A mere four months on and the mood has shifted more negatively with 60% of the group feeling optimistic headed into 2024.

Not that much really. The IMF is predicting slow global growth in 2024 at 2.9%, which is below historical averages. Inflation is on the way down, but not as much as central banks would like to see, which may result in additional monetary tightening.

Global manufacturing PMI in developed economies has generally been trending downwards in terms of output and new orders. And service sector-driven improvements over the summer months have run out of steam as we exit the year.

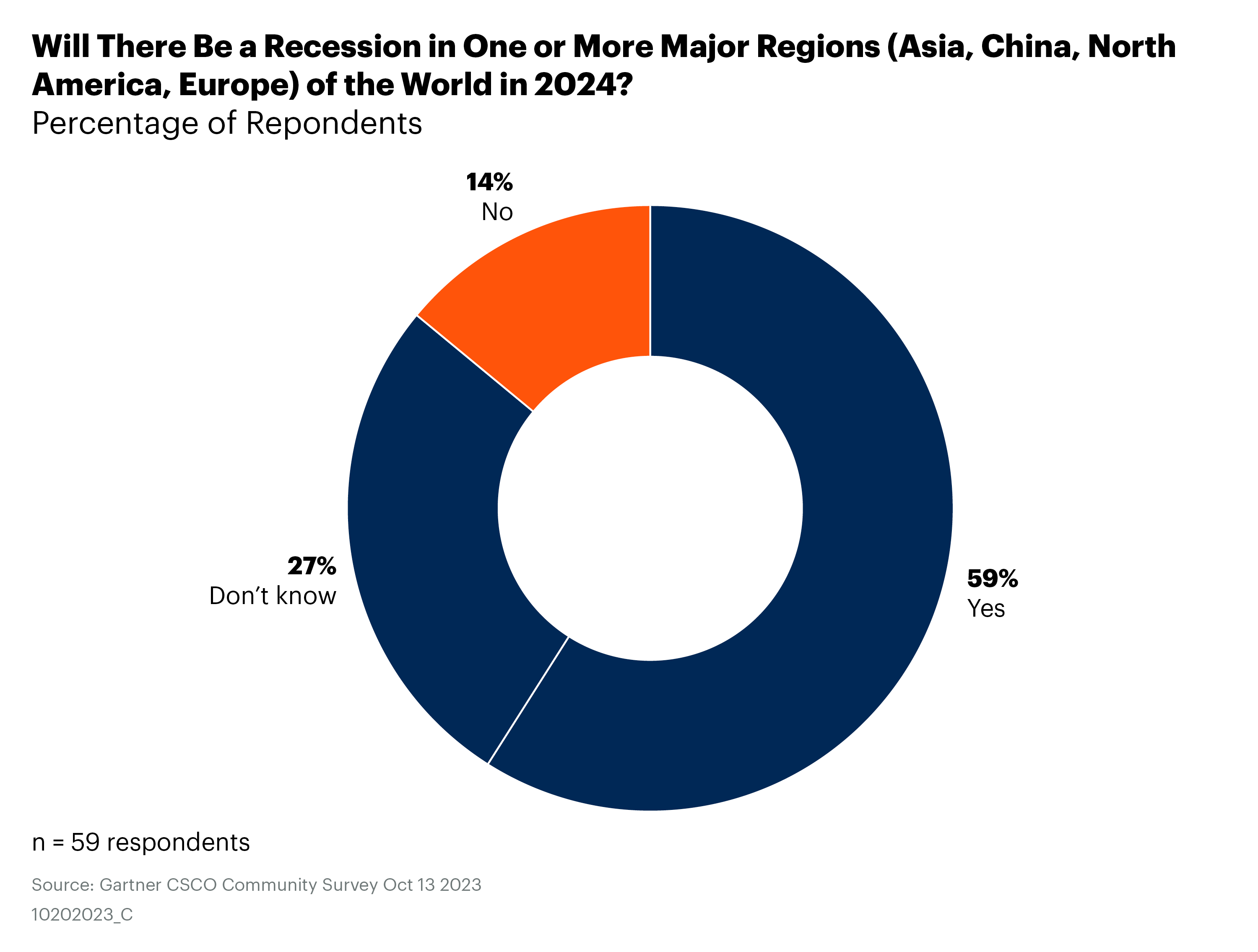

The likelihood of soft landings has increased, but that news isn’t providing much comfort to the CSCO community. In a just-fielded survey, only 14% think the world’s major economies will avoid a recession in 2024.

The bottom line is this economic data is just about what was expected.

So how are CSCOs planning to deal with this outlook? Summing up: They are planning for the downsides and hoping things go as they expect, and stay slightly boring. And by boring, I mean things go according to the annual plan and there are no major hits to the business.

The community is anticipating overall cost inflation to continue in 2024, but to be less intense than in the past few years. About 80% are seeing increases of between 1% to 5%. And just over half of that group are planning on 3%-to-5% increases. A small, fortunate cohort (15%) aren’t planning to see any cost inflation.

To combat the cost increases, off-setting cost reductions are planned as well. The net being most are attempting to stay neutral on costs. However, about 40% of those surveyed are targeting 3%-to-7% overall reductions which would result in a net gain.

While all areas of operations are targets for cost reductions, one area stands out a bit: indirect labor. But on the flip side is the No. 1 driver of cost increases: direct labor. CSCOs are grappling with frontline labor costs and back-office productivity. By 2025, Gartner predicts (subscription required) that productivity will be in the top 5 priorities (currently ranked 9) for CEOs. Choosing the right digital investments to gain back-office productivity will be top of mind in 2024.

Only about 45% of the companies surveyed said they would be passing on their increased costs to customers. And this is in sharp contrast with 2022 and ’23 when more than 65% said they would. This indicates that customers are probably tapped out on their willingness to spend, and companies are nervous about continued increases.

We hear that CSCOs want to be more strategic, and they say so themselves. In 2024 they will spend 75% of their time on strategic endeavors. But again, there is a flip side. In conversations with Gartner analysts and researchers, CSCOs understand that the core of supply chain is tactical. High-performing execution on the details is what the enterprise needs, and the C-suite expects.

Geopolitical risks are the biggest challenge they face going into 2024. But most are resolved to a position of limited preparedness. There is only so much that can be done to mitigate risk in such a volatile landscape. De-risking and moving supply chains is no simple thing, and it will take years to make significant progress. But this work will continue.

We all want to gain insight on what things are lurking around the corner — for good or ill. The definition of good seems to be morphing into the absence of bad. So, leaders are placing a bit more emphasis on trying to identify disruptions heading their way, but they are proving more difficult to spot.

There are a few places to look for signs that might seem unconventional but have been solid indicators over the years. These are insurance companies. Specifically, reinsurers. Examples are Swiss Re, Berkshire Hathaway, Lloyd’s and Allianz. They are always looking for things that can go wrong: climate events, cybercrime and war, to name a few. If you don’t know your insurance provider or broker, it might be a good time to strike up that relationship.

Other places to look are risk consultancies. There is a possibility that these relationships already exist within your company: general counsels, CFOs and boards engage with companies like Control Risks and Dentons Global Advisors. A quick internal investigation may net a valuable resource that is already at hand.

Many we’ve spoken to have experienced pessimism fatigue and are learning to shrug off the continuous onslaught of distressing news and challenges. What 2024 will bring isn’t as clear as the CSCO community would like, but they are maintaining an overall sense of optimism.

Once more, we’ll leave it there for now.

Wade L. McDaniel

Distinguished Advisor VP

Gartner Supply Chain

Wade.Mcdaniel@gartner.com

Download the report to learn how to measure, manage and improve your supply chain agility.

Listen and subscribe to the Gartner Supply Chain Podcast on Gartner.com, Apple Podcasts, Spotify and Google Podcasts

Beyond Supply Chain

Subscribe on LinkedIn to receive the biweekly Beyond Supply Chain newsletter.