By Kevin O'Marah | January 23, 2015

Pause the AI Hype, Let's Talk About the Weather

July 17 2026

By Kevin O'Marah | January 23, 2015

Despite the collapse in commodity prices, The Economist recently reported that Africa, historically sustained almost exclusively by its extractive industries, has remained afloat. The year-low prices of commodities like copper, cotton and platinum, and the continuing fall of oil, have failed to overturn the bright growth forecasts for 2015, which rank the continent among the highest in the world. How can this be?

History and prejudice may obscure the truth of Africa’s emergence as a fully fledged participant in the modern global economy. Images of a continent too poor to feed itself and too corrupt to govern itself suggest a business environment suitable only for the bravest of miners and planters. Today, however, an emerging middle class and an increasingly connected population of nearly one billion people wants and is ready to pay for consumer goods like those sold in Europe and the US.

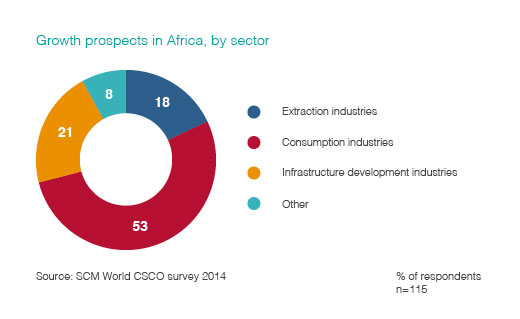

In our annual survey of supply chain executives last year, more than 10% of 920 respondents who were asked to name their top three growth opportunities identified one or more sub-Saharan African countries. Among the 115 individuals who chose at least one African country as a top three growth prospect, more than half came from consumer industries, while less than a fifth were from extractive industries.

The Economist’s take on how Africa is breaking its traditional link to volatile commodity markets includes the recognition of improving governance, which makes business investment easier and more attractive. One example is Rwanda, which just 20 years ago was the scene of a historic genocide but today is friendlier to business than Italy.

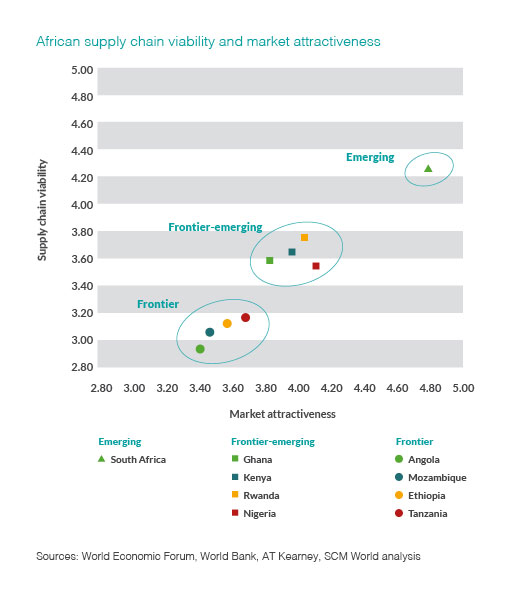

SCM World recently studied the question of supply chain viability and market attractiveness in sub-Saharan Africa and found that many countries long synonymous with war, poverty and misery – including not only Rwanda, but also Nigeria, Ethiopia and Angola – offer worthy potential for businesses and are willing to play the long game.

The results of this analysis are summarised in an index that clusters individual country markets under the labels of “emerging”, “frontier-emerging” and “frontier”.

Among the nine countries analysed here, only Angola and Nigeria are heavy net exporters of primary commodities like food, fuel and metals. Four, including Kenya, Ethiopia, Tanzania and Rwanda, are net importers. Growth in financial services, telecommunications and construction appears prominently in the macroeconomic statistics across the region, suggesting a near-term future built on a domestic middle class rather than warlords and blood diamonds.

One of the persistent objections to the idea of a robust consumer economy in Africa is poverty. How, many ask, can CPG or healthcare businesses justify entering these markets when the people can’t afford the products? The answer is twofold.

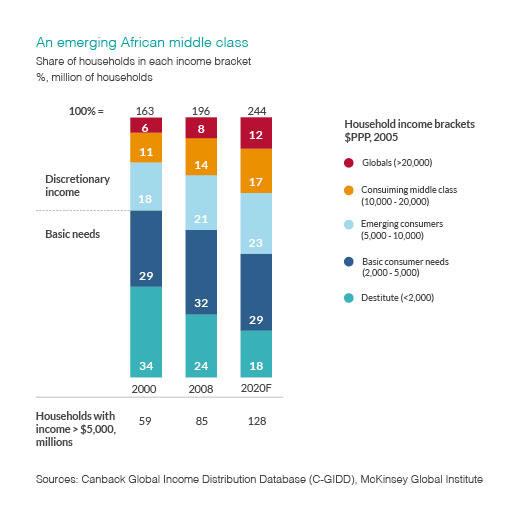

First, people are not as poor as is commonly believed. The McKinsey Global Institute offers an analysis that shows Africa just now crossing over from a majority of households at subsistence living standards to a majority with discretionary spending power. It’s not exactly London, but within five years Africa will comprise 128 million households that do at least some shopping.

The second part of the answer lies in the supply chain itself. Ten years ago the great business strategist CK Prahalad published a book called The Fortune at the Bottom of the Pyramid, which encouraged business leaders to rethink the profit potential of poor regions in India, Africa and, as of then, China. Central to his pitch was the idea that products and their supply chains can and should be redesigned to hit price points and penetrate channels accessible to billions of potential new consumers.

The lesson was not lost on global pioneers like Coca-Cola, Pfizer, Diageo, GlaxoSmithKline, Unilever and Nokia, all of whom have had success with supply chain strategies built specifically for Africa. Distribution networks are challenging, retail outlets are typically much smaller, and credit is often non-existent, but some have still managed to gain a real foothold.

The motivation for these forays is obvious: growth in the saturated northern hemisphere is increasingly difficult, while the product-poor southern hemisphere craves a consumer economy. Demand is what draws us.

Beyond Supply Chain

Subscribe on LinkedIn to receive the biweekly Beyond Supply Chain newsletter.