By Wade McDaniel | February 9, 2024

![[ALT TEXT]](https://emt.gartnerweb.com/ngw/globalassets/en/supply-chain/blog/beyond-supply-chain/images/bsc090224v2.png)

Pause the AI Hype, Let's Talk About the Weather

July 17 2026

By Wade McDaniel | February 9, 2024

My colleague Stan Aronow and I have been on a topical binge as we kick off 2024. He’s dug into some predictions and looked at some risks, while I’ve recommended some things to keep tabs on. We decided to round things out by looking at the economic landscape and how supply chain leaders are responding.

In my experience, supply chain leaders are a glass-half-empty crowd. So, when I asked chief supply chain officers a few months back about their thoughts on a recession in 2024, it wasn't surprising that more than half of them said there will be one. And of those, the majority said it will hit more than one major economy. Wow. We asked the same question about 2023 and got much the same result.

If things go as economically forecasted, it will be an unexceptional year.

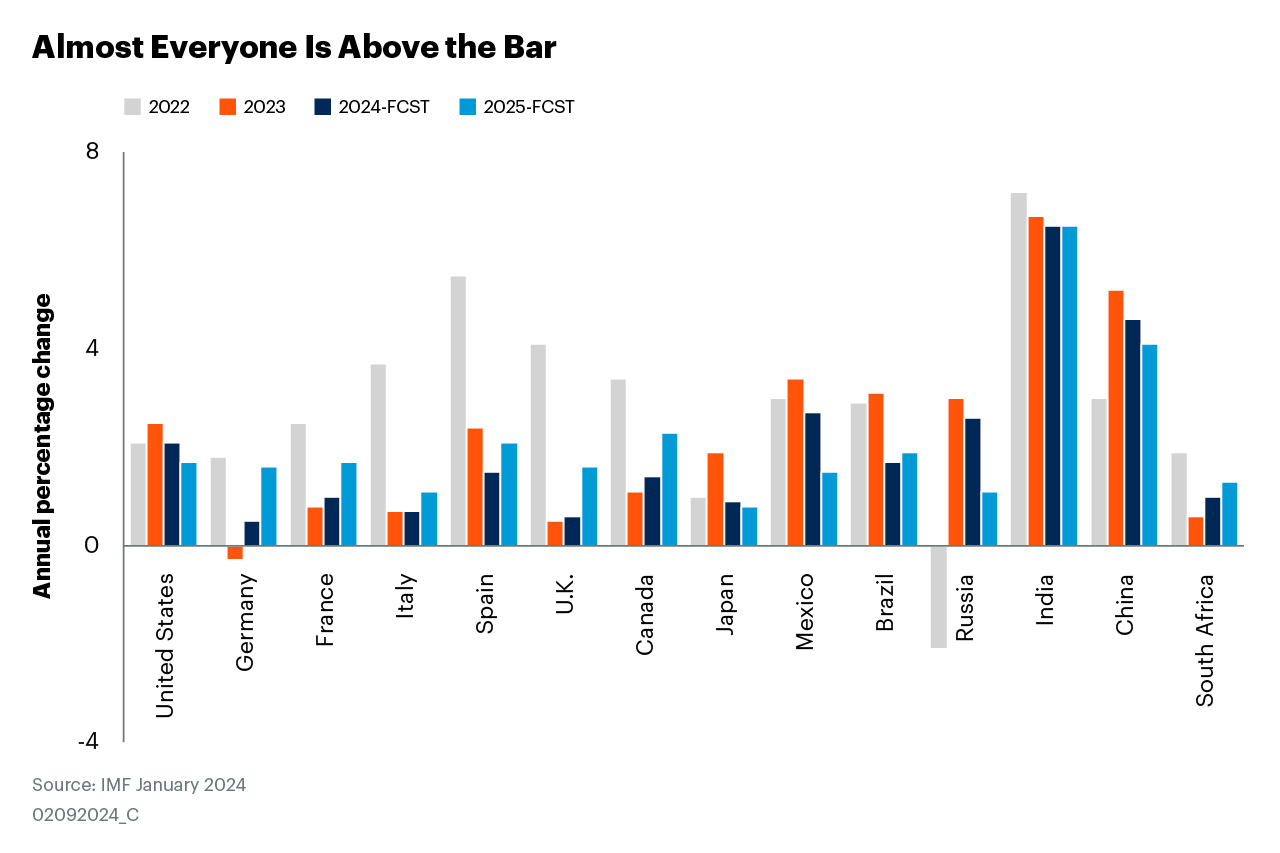

Our outlook shouldn’t be so bleak if we look at the actual performance and the projections from the IMF. A quick scan of results for three major economies in 2023 shows China met its 5.2% growth target, the United States overperformed and grew 2.5%, and the Euro area narrowly averted a technical recession. Looking ahead to 2024, the IMF said this at the end of January: “Moderating inflation and steady growth open path to soft landing.”

The possibility of recession is fading into the rearview mirror (I’m resisting my glass-half-empty tendency), but supply chain leaders aren’t behaving in a way that reflects economic relaxation. What we’re seeing is active cost-cutting and inventory reduction. Could inflation be driving this behavior?

Perhaps.

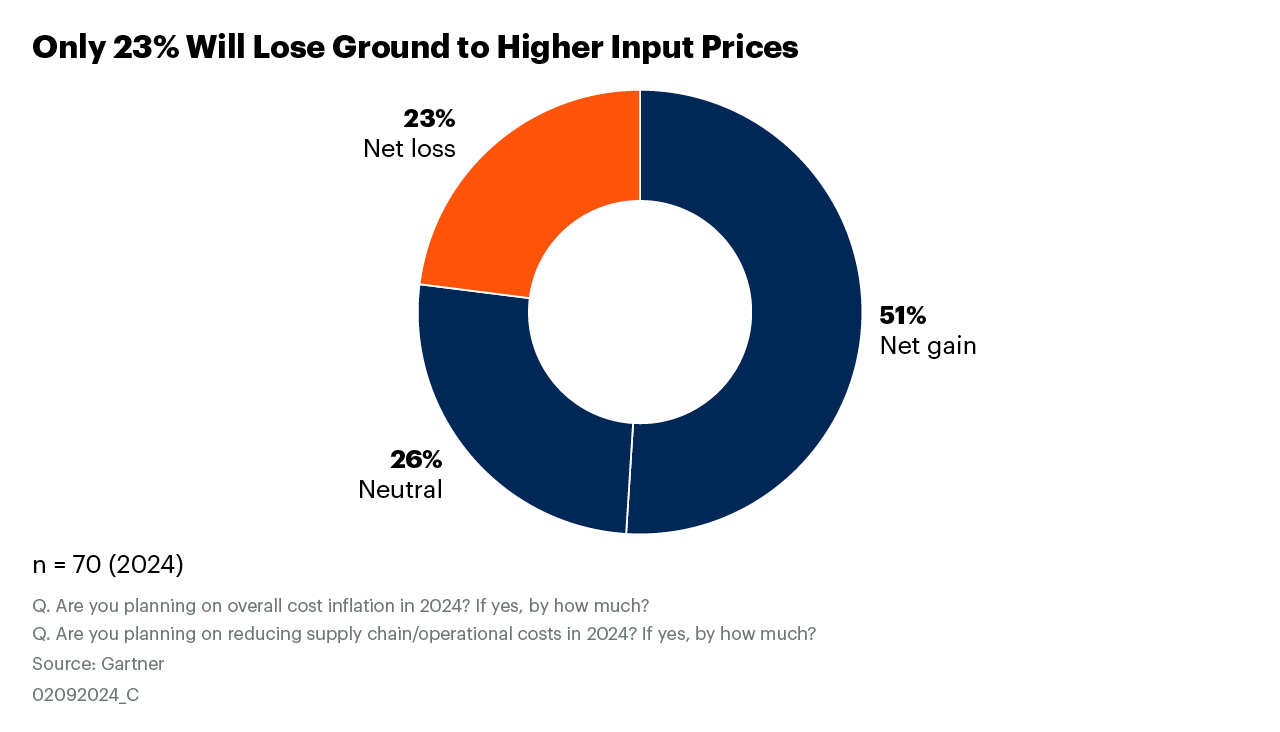

Core inflationary trends are also headed in the right directions, which is up in China and down in the U.S. and Euro area. This is something that CSCOs are embracing. About half say they will win their fight against their input prices and make gains against them in ’24. A quarter will break even, but some will lose ground.

To be fair, a company’s production input prices can’t precisely mirror macroeconomic indicators, but they are more closely aligned to supply chain’s thinking. We feel the effort to make those gains against input prices isn’t trivial.

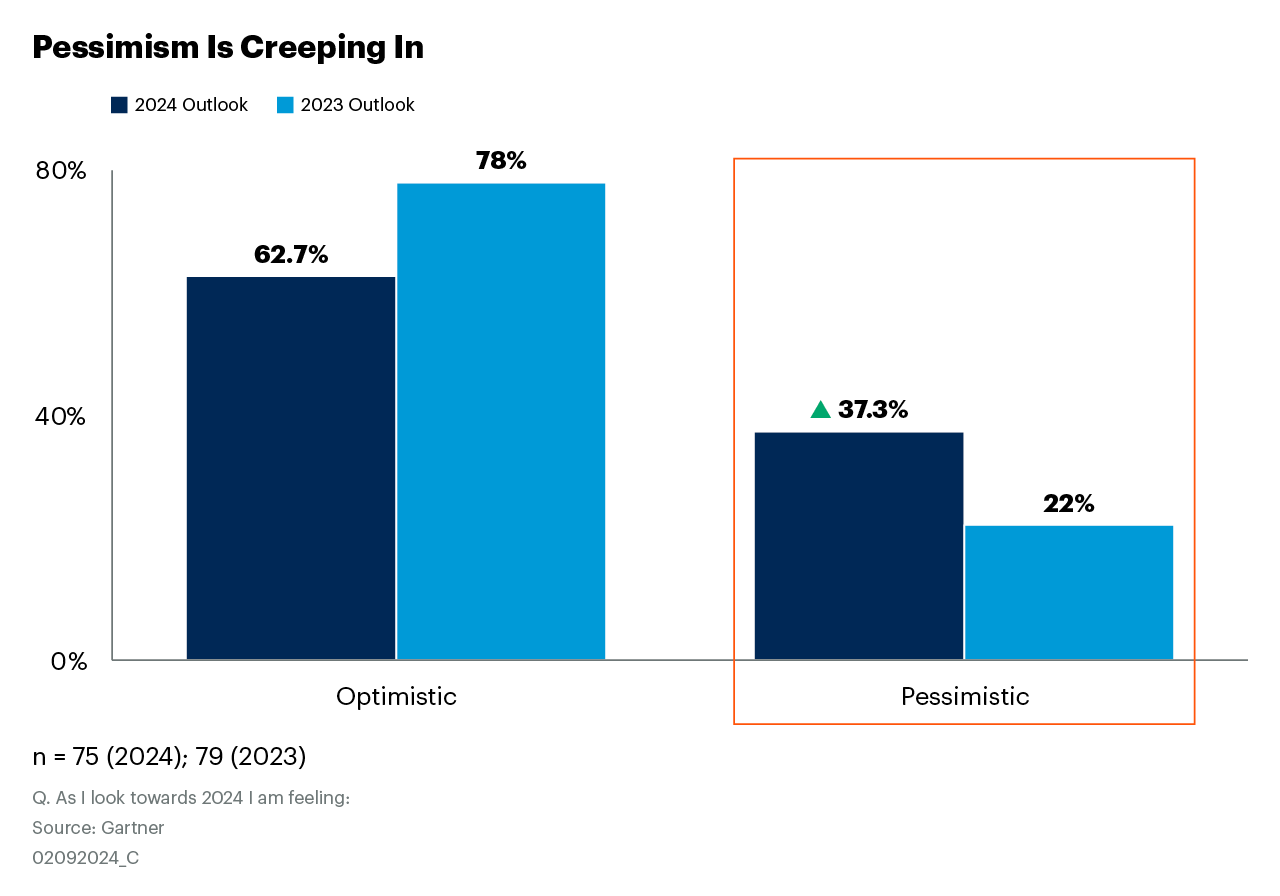

So, how does the CSCO community feel about taking that effort on in ’24? Well, it’s less optimistic than it felt in 2023, but that level was so high that we thought there might be an optimism bubble. And there turned out to be one, but not for any apparent reason. We believe it was due to pessimism fatigue. One can only feel glum for so long; either stay in the game and press on or take a seat.

The outlook for 2024 is probably more realistic. But it still doesn’t explain why leaders are down on the economy when the outlook is, uh, unremarkable.

We should take a quick peek at labor and unemployment. CSCOs agree that direct and indirect labor costs will be challenging in 2024 but turnover would cool. Forecasters say the same; labor markets will cool, unemployment rates will increase slightly, but wages will remain strong. Predictable.

Even though the economic landscape is settling down, this is not a return to a pre-COVID state, a.k.a. the good old days. However, leaders should feel reasonably confident about growth and prepare their operations to be ready for an upside. Not a shortage-riddled, stimulus-driven, revenge-buying environment. But good old-fashioned stable growth.

Wade L McDaniel

VP Distinguished Advisor

Gartner Supply Chain

Wade.Mcdaniel@gartner.com

Register Now: The 2024 Gartner Power of the Profession Supply Chain Award Winners

Register Now: The Future of Supply Chain: Redefine Business Value for 2024 & Beyond

Beyond Supply Chain

Subscribe on LinkedIn to receive the biweekly Beyond Supply Chain newsletter.