By Kevin O'Marah | November 28, 2014

Advancing the Mind, Body and Soul of Sentient Operations

August 07 2026

By Kevin O'Marah | November 28, 2014

A confluence of little problems morphing into a big problem. That’s how the logistics bottleneck currently affecting Los Angeles/Long Beach, Seattle, Oakland and other US west coast ports is being explained.

Many commentators blame chassis shortages. Others blame bigger vessels. Some even invoke weather problems months ago to explain why cargo such as apples, meat and other agricultural products can’t get out of the country, while toys, clothes and Christmas merchandise can’t get in.

I think it’s simpler than that. The union is girding for battle while management holds its ground and the result is an epidemic of work slowdowns that neither side really wants to talk about. Regional press in Seattle, LA and San Francisco are covering the story with credible evidence of “industrial action”, as the Brits call it, yet all seem worried about the black eye this gives Pacific trade routes.

They should worry.

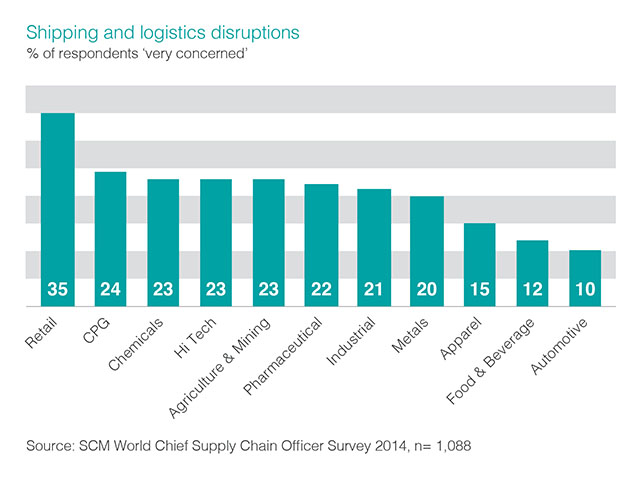

Supply chain risk has become a hot topic lately with concerns about rising costs, capricious regulations and long supply lines dampening the appeal of China sourcing. This effect is worst for retailers that have come to rely so heavily on suppliers producing in China that they worry more than any other industry about logistics disruptions. The data below, which was collected this past summer, shows that many foresaw the current problem.

Regardless of how negotiations between the International Longshore & Warehouse Union (ILWU) and the Pacific Maritime Association (PMA) go, the damage may already have been done. Research we conducted almost two years ago found that over half of supply chain executives (57%) planned to reshore at least some of their manufacturing, with the biggest winner of new capacity being Mexico.

At the same time, increasing automation and new manufacturing technologies create more opportunities for smaller run, agile manufacturing closer to end markets. One loser is obviously low-cost country sourcing from China, but as the ILWU and PMA will likely discover, another is Los Angeles/Long Beach.

The struggle between the ILWU and PMA may well end in tears. If a full-scale strike (or lockout) were to happen, the impact on the US economy could be severe. Back in 2002 a similar situation supposedly cost $1 billion per day in lost business.

Today it would be worse, with some retailers unable to restock after this weekend’s post-Thanksgiving sales bonanza and exporters, especially food producers, watching as produce and meat bound for holiday markets in Asia and Latin America rots. Such a doom scenario seems too stupid to even be possible, but pride could override wisdom and everyone would be sorry.

The union in this case has been working without a contract since July, which means grievance procedures have been out of commission. Tit-for-tat disagreements under such conditions tend to fester and worsen. Plus, the last contract was agreed after the S&P 500 had already lost over 25% of its value and imports to LA/Long Beach had been in decline for over a year from 2007 peak volumes, which means the union probably got a rough deal.

Labour fears about job losses due to increasing automation are well founded. Our data says that by a ratio of 7:1 logistics firms plan to increase investments in equipment and automation over people. For supply chain strategists, the important implication of this fact is greater agility rather than lower costs.

Maybe the best thing to do is offer decent pay rises and increased investment in training to give longshoremen careers built on human intellectual capital rather than extortion masking as seniority. Unions must realise that fixed productive assets, including ports, can only be held hostage temporarily in the modern global supply chain. Trade will bypass the west coast if it becomes too risky, inflexible or expensive.

For its part, the PMA has to look at this situation as an opportunity to prepare for the future. Megatrends including demographics, digitisation of the economy and even sustainability make me believe that Pacific trade had probably already peaked in volume. I’d start looking for ways to add value rather than just cut costs.

Beyond Supply Chain

Subscribe on LinkedIn to receive the biweekly Beyond Supply Chain newsletter.